Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

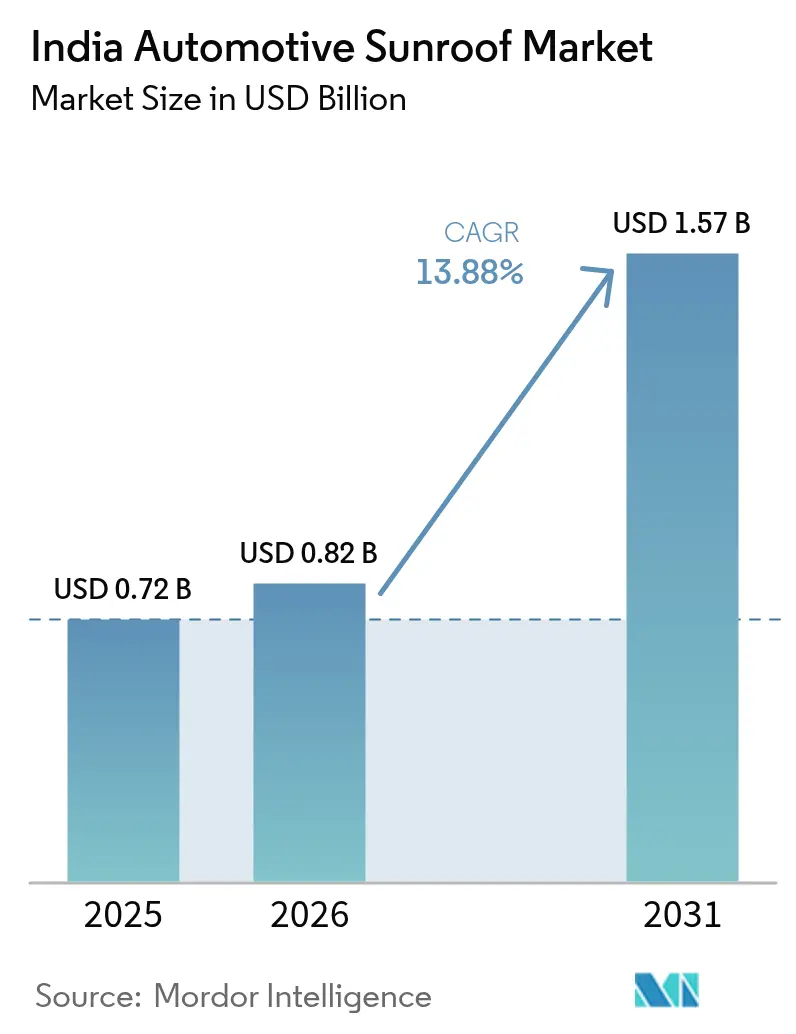

| Base Year Market Size (2025) | USD 0.72 Billion |

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 13.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Sunroof Market Analysis by Mordor Intelligence

The India automotive sunroof market size was valued at USD 0.72 billion in 2025 and estimated to grow from USD 0.82 billion in 2026 to reach USD 1.57 billion by 2031, at a CAGR of 13.88% during the forecast period (2026-2031). Rising consumer demand for premium features, the entry of domestically manufactured modules under the Production Linked Incentive (PLI) scheme, and the widening SUV mix are accelerating both volume and value growth within the India automotive sunroof market. Rapid localization of glazing and mechanism sub-components is compressing bill-of-materials costs, letting OEMs deploy factory-fitted sunroofs on models priced below INR 1 million, while still protecting margins. At the same time, escalating CO₂-compliance pressure is nudging manufacturers toward photovoltaic glass options, adding an energy-management dimension to what was once a pure styling element. Finally, the OEM–aftermarket balance is evolving: although factory integration still commands more than four-fifths of unit shipments, the retrofit channel is scaling quickly on the back of experiential tourism fleets and urban customization culture.

Key Report Takeaways

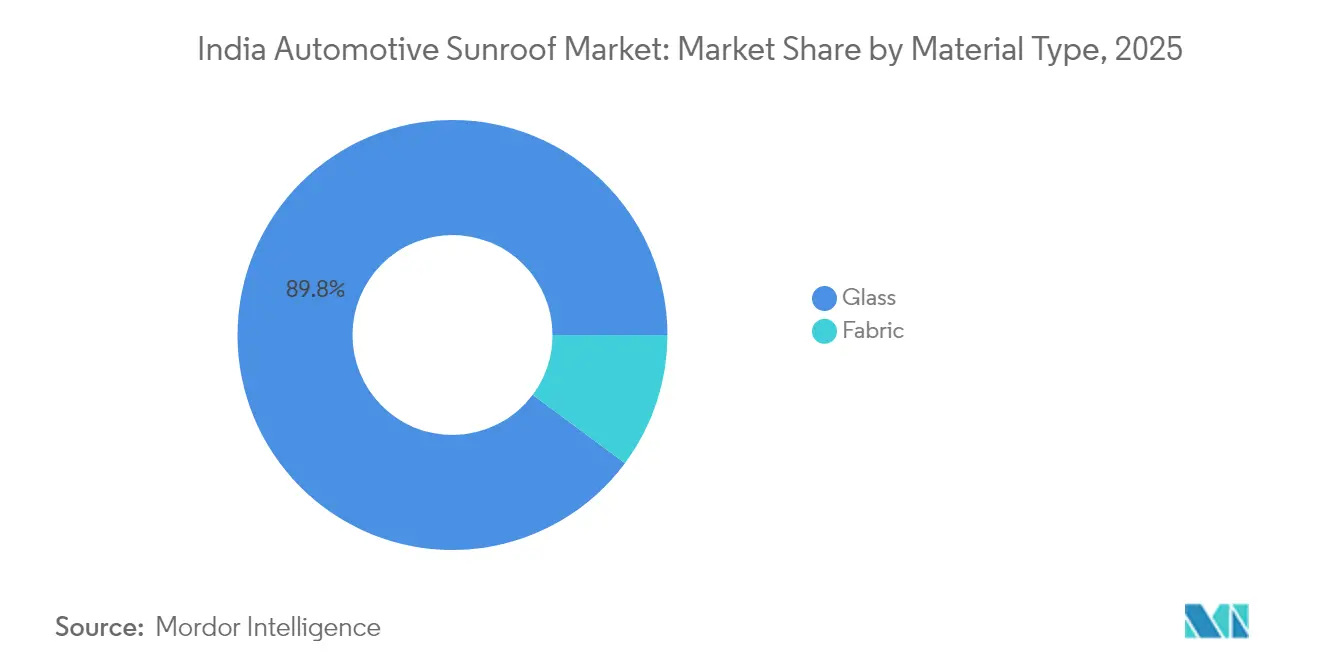

- Glass accounted for 89.82% of the Indian automotive sunroof market share by material type in 2025, while fabric is forecast to advance at a 14.6% CAGR through 2031.

- By operation type, panoramic systems led with a 46.82% of the Indian automotive sunroof market share in 2025; solar-integrated roofs are poised for the fastest 15.02% CAGR to 2031.

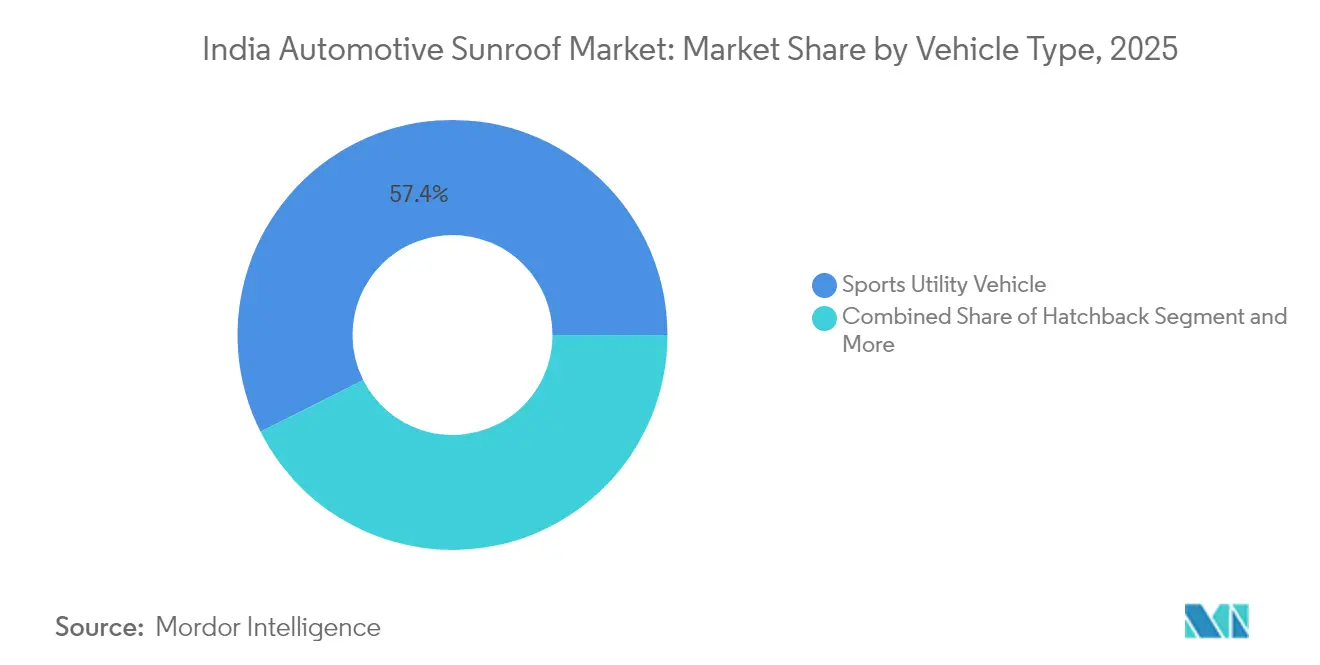

- By vehicle type, SUVs captured 57.43% of the Indian automotive sunroof market share in 2025, whereas MPVs and other body styles will climb at a 14.55% CAGR.

- By sales channel, OEM-fitted installations represented 81.63% of the Indian automotive sunroof market share in 2025; the aftermarket retrofit route is set to grow 14.82% annually.

- By region, North India dominated at 36.44% of the Indian automotive sunroof market share in 2025, while East and North-East India will register the highest 15.55% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automotive Sunroof Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-Feature Adoption in Mass-Market Cars | +2.1% | National, with early gains in North India, Maharashtra | Medium term (2-4 years) |

| Solar-Integrated Roofs to Meet CO₂ Norms | +1.9% | National compliance, early adoption in tech hubs | Long term (≥ 4 years) |

| OEM Differentiation Race Via Factory-Fitted Sunroofs | +1.8% | North India, West India manufacturing hubs | Short term (≤ 2 years) |

| Experiential Tourism Drives Rental-Fleet Retrofits | +1.5% | Tourism corridors, metropolitan areas | Medium term (2-4 years) |

| Domestic Manufacturing Lowers Module Costs | +1.2% | Tamil Nadu, Maharashtra, Gujarat clusters | Long term (≥ 4 years) |

| Ventilated/Anti-Smog Sunroofs for Urban Heat | +1.3% | Delhi NCR, Mumbai, Bangalore, Chennai | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium-Feature Adoption in Mass-Market Cars

Penetration of factory-installed sunroofs has reached roughly one in four new-car sales, underlining a decisive shift toward experiential content in the Indian automotive sunroof market offerings. Mainstream brands now equip mid-trim variants—rather than only top trims—because economies of scale from local sourcing have cut system costs by nearly one-third since. Volume leaders consistently package sunroofs alongside connectivity and safety bundles, allowing customers to perceive a step-up in lifestyle value for a modest incremental outlay. Younger urban buyers equate a powered sunroof with social-status signaling and open-air leisure, moving it from optional to expected equipment. As a result, feature parity has supplanted price as a winning formula in fiercely contested B-segment hatchbacks and compact SUVs.

Solar-Integrated Roofs to Meet CO₂ Norms

Embedded photovoltaic cells now offer a practical 80–100 W trickle-charge benefit, extending EV range or powering auxiliary ventilation in idling ICE vehicles. Early adopters previewed the technology at Auto Expo 2025, signaling a ramp-up path once battery pack prices cross the USD 80 per kWh threshold. Forward-looking OEMs view solar roofs as a compliance hedge against the Bharat Stage VII emissions roadmap, while tech-savvy buyers prize the environmental narrative. As module efficiencies rise above 20%, solar-equipped variants will migrate from halo products into core model lines, raising the innovation bar for the entire India automotive sunroof market.

OEM Differentiation Race via Factory-Fitted Sunroofs

Manufacturers are deploying sunroofs as a line-item weapon in variant planning, squeezing more profit per unit while tightening competitive gaps in headline pricing across rival nameplates. Factory integration guarantees warranty coverage, structural integrity, and optimized drainage—advantages that the retrofit trade cannot fully replicate. On refreshed models launched since mid-2024, panoramic glass roofs simultaneously serve as a visual hero element in marketing campaigns and a tangible upsell lever inside showrooms. Higher perceived resale value further nudges shoppers toward these factory-equipped trims, bolstering stickiness for the OEM channel in the India automotive sunroof market.

Domestic Manufacturing Lowers Module Costs

The PLI scheme earmarking INR 25,938 crore (USD 3.1 billion) for automotive value addition has catalyzed capacity builds across sunroof frame stamping, tempered-glass lamination, and mechatronics sub-assemblies [1]“PLI Scheme Outlay for Automobile & Auto Component Sector,”, Press Information Bureau, pib.gov.in. Fresh investments—such as Webasto’s Pune plant and Minda Corporation’s joint venture with HSIN Chong—shorten lead times and shave logistics overhead, producing a 7-10% system-cost reduction versus fully imported kits. Localization also insulates suppliers from foreign exchange swings, allowing OEM partners to receive stable pricing. Over the long term, these clusters will anchor export programs that feed rising demand across South-East Asia and Africa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-Sensitive Entry-Level Segment | -2.2% | Rural and semi-urban markets | Long term (≥ 4 years) |

| Glare/UV Discomfort in Tropical Climate | -1.6% | Southern and coastal regions | Medium term (2-4 years) |

| Leakage and High Maintenance Perception | -1.4% | National, particularly monsoon-affected regions | Short term (≤ 2 years) |

| Head-Room and Rollover Safety Concerns | -1.1% | Safety-conscious urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-Sensitive Entry-Level Segment

In India, a large segment of car buyers remains focused on affordability, steering their purchases towards budget-friendly options. For these consumers, essentials like fuel efficiency and safety overshadow luxury features, such as sunroofs, which are often deemed non-essential and a financial strain. Without a significant reduction in the cost of sunroof systems by suppliers, their adoption in entry-level vehicles will likely stay constrained, limiting the market's potential in this segment for the foreseeable future.

Leakage and High-Maintenance Perception

India’s intense monsoon spells make headlines whenever owners report water ingress, fueling social-media skepticism that disproportionately hurts first-time buyers. Even though OEM drainage designs now include wider channels and double-lip seals, memories of earlier failures linger. Poorly executed aftermarket cuts compound the issue, tarnishing perceptions of the category at large. To counteract the narrative, leading manufacturers now provide extended leak warranties and publish care guides, yet the restraint will persist until mass evidence of zero-defect performance permeates consumer circles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Glass Dominance Drives Premium Positioning

Glass held a 89.82% share of 2025 shipments within the Indian automotive sunroof market. The laminated safety glass, UV-filter interlayers, and structural rigidity align neatly with the SUV body styles that dominate new-car bookings. Electrochromic glazing and solar-reflective coatings, now entering mid-segment nameplates, further entrench glass as the aspirational baseline. Fabric modules appeal to price-conscious buyers who still crave an open-sky feel, and their 14.6% CAGR underscores untapped headroom once localized textile skins and sealants bring costs below glass alternatives. Manufacturers are already experimenting with dual-layer synthetic weaves that promise improved noise insulation, hinting at a broader role for fabric in upcoming refreshes.

Looking ahead, the Indian automotive sunroof industry will see glass evolve into a multifunction platform that integrates ambient LEDs, heads-up projection, and antenna arrays—all without compromising rollover strength. Fabric, meanwhile, will anchor emerging crossover body styles where weight reduction ranks higher than panoramic visuals. Both materials ensure that the Indian automotive sunroof market retains flexibility across the pyramid, from sub-compact commuters to premium electric crossovers.

By Operation Type: Panoramic Systems Lead Premium Integration

Panoramic roofs captured 46.82% of 2025 revenue, underlining a consumer appetite for near-full-length glazing that amplifies cabin spaciousness. The segment’s dominance is built on economies of scale from shared SUV platforms, enabling OEMs to spread costs across multi-brand portfolios. Slide-in and spoiler variants retain relevance in hatchbacks where roof curvature limits panel travel, yet their combined share steadily erodes. Solar-integrated designs, though only a fraction of units today, are forecast to clock a 15.02% CAGR, thanks to incoming fleet-average CO₂ targets and customer interest in self-charging convenience.

The Indian automotive sunroof market size attached to panoramic systems will likely widen as two-panel architectures move down-segment. Conversely, solar roofs will play a critical role in premium EVs, offering a marketing halo that transcends kWh savings. Over the forecast window, hybrid formats—panoramic glass embedded with thin-film photovoltaic stripes—could emerge, marrying the visual drama of full glass with measurable energy gains.

By Vehicle Type: SUV Preference Drives Market Expansion

SUVs delivered 57.43% of 2025 sunroof fitments, reflecting the body-in-white packaging advantage and the consumer gravitation toward high-stance vehicles. Elevated rooflines allow larger aperture cut-outs without eroding headroom, while rugged branding pairs naturally with open-air leisure cues. MPVs and crossover vans, propelled by family travel and ride-sharing platforms, will accelerate at 14.55% until 2031, aided by the multi-row ventilation benefits of panoramic glass. Sedan and hatchback applications remain constrained by structural torsion limits and roof thickness tolerances, yet incremental gains are expected as lightweight frames and low-profile drive motors mature.

As urban infrastructure expands and long-distance tourism flourishes, the Indian automotive sunroof market size attributed to MPVs may rise faster than anticipated. That growth will, however, depend on OEMs integrating modular roof beams that preserve crash-worthiness while accommodating multi-panel openings.

By Sales Channel: OEM Integration Maintains Quality Leadership

Factory installations controlled 81.63% of shipments in 2025, underscoring trust in OEM engineering validation and warranty coverage within the Indian automotive sunroof market. High-volume procurement contracts let automakers negotiate 10-15% lower unit cost versus single-order aftermarket purchases, reinforcing the channel’s cost advantage. Retrofit demand, growing at 14.82% annually, finds traction in tourism fleets and enthusiasts who wish to upgrade existing vehicles without trading up. Specialist installers are adopting OE-grade adhesive sealants and offering two-year leak guarantees, shrinking the perceived risk gap.

Over time, the Indian automotive sunroof industry will likely bifurcate: factory units will dominate new-car volumes up to 2031, while premium retrofit boutiques capture customization-driven niches. Policy-driven scrappage incentives may also funnel older cars into retrofit channels as owners seize one last upgrade before disposal.

Geography Analysis

North India retained a 36.44% hold on 2025 revenue, benefitting from proximity to Gurugram-Manesar, Neemrana, and Lucknow OEM hubs. Agglomeration effects include shared supplier parks, throughput-driven courier networks, and a deep talent pool in stamping and glazing trades. East & North-East India will post the fastest 15.55% growth, buoyed by expanding highway corridors and state EV-purchase subsidies that favor feature-rich models. West India’s Pune-Aurangabad belt sits at the crossroads of export logistics and domestic assembly, ensuring balanced up-trend momentum. At the same time, South India leverages the Chennai corridor with a significant national component output to pivot into solar-embedded roof exports.

West India centers on Maharashtra, where the Pune-Chakan belt hosts mixed passenger-vehicle and commercial-vehicle assembly plants. Webasto’s newest facility in this zone has doubled domestic capacity, giving OEMs a just-in-time buffer against port congestion on the western seaboard . Mumbai’s coastal humidity drives interest in glass with advanced anti-salt corrosion coatings, nudging suppliers to differentiate via materials science. The region’s exporter orientation—facilitated by Jawaharlal Nehru Port—also means that India-made sunroof modules increasingly ship to ASEAN final-assembly plants, embedding West India deeper into global value chains.

South India thrives on Tamil Nadu’s component prowess and Karnataka’s tech-savvy consumer demography. The Chennai-Sriperumbudur node houses die-press workshops and glass-tempering furnaces that feed both domestic OEMs and international CKD kits. Bangalore’s electric-vehicle cluster now specifies solar-ready roof panels, embracing a sustainability ethos that is reshaping feature checklists among first-time EV buyers. In parallel, East & North-East India is transforming from low-penetration to high-growth territory; state-sponsored charging grids and tourism circuit investments are steering aspirational buyers toward feature-rich SUVs, lifting the overall India automotive sunroof market growth trajectory despite lower starting volumes.

Competitive Landscape

Competition straddles global incumbents with patented kinematics and domestic newcomers leveraging cost agility. Webasto, Inalfa, and Yachiyo collectively supply over half of SUV-grade panoramic assemblies, wielding multi-continent validation data and the ability to integrate emerging technologies such as electrochromic panes. Yet, local groups like Samvardhana Motherson and Minda Corporation are rapidly absorbing design know-how through acquisitions and technical alliances, pulling India toward self-reliance targets stated in the PLI charter.

Innovation revolves around smart-glass electronics, weight-optimized aluminum frames, and self-learning motor controllers that adapt torque to aging seals—all areas where tier-one suppliers can command price premiums. Localization remains the key battleground: firms that hit the 50% domestic-value threshold earn incremental incentives, offsetting capital depreciation faster than import-dependent rivals. On the demand side, OEM platform consolidation grants suppliers double-digit program volumes and raises switching barriers; consequently, incumbents protect share through early-design collaboration and co-located engineering centers. Retrofit specialists, though fragmented, carve out loyalty via concierge installation and warranty-backed leak remediation, illustrating how service excellence can substitute for scale in the Indian automotive sunroof market.

Future rivalry will intensify around solar integration and active-dimming glass, with startups pitching plug-and-play PV laminates to traditional frame makers. Meanwhile, safety regulators’ push for Bharat NCAP compliance increases validation costs, subtly favoring entrenched players with accredited test rigs. Despite these hurdles, the sheer volume potential of 5 million-plus annual light-vehicle sales keeps the competitive field open for disciplined new entrants.

India Automotive Sunroof Industry Leaders

Webasto Roof Systems Inc.

Inalfa Roof Systems Group

Motherson Yachiyo Automotive Systems Co., Ltd.

CIE Automotive

Inteva Products

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Inalfa Gabriel Sunroof Systems Private Limited, a joint venture of Inalfa Roof Systems and Gabriel India Limited (the flagship company of the USD 2.2-billion ANAND Group), is poised to establish new plants in India's Western and Northern automotive hubs, responding to the surging demand for sunroofs.

- June 2024: In a strategic move, Minda Corporation Limited, the flagship entity of Spark Minda and a prominent supplier of automotive components, has inked a joint venture agreement with Taiwan's HSIN Chong Machinery Works Co. Ltd. The collaboration seeks to harness advanced technology to produce sunroof and closure systems for passenger cars in India.

India Automotive Sunroof Market Report Scope

The India Automotive Sunroof Marker report covers the growing demand for India Automotive Sunroofs across the globe, sunroof penetration across different models/trims/versions and by vehicle segment, latest product developments and market shares of players operating across the India Automotive Sunroof market. The scope of the report includes:

By Material Type

| Glass |

| Fabric |

By Sunroof Operation Type

| Pop-up |

| Slide-in / Spoiler |

| Panoramic |

| Solar-integrated |

By Vehicle Type

| Hatchback |

| Sedan |

| Sport Utility Vehicle |

| MPV / Others |

By Sales Channel

| OEM-fitted |

| Aftermarket Retrofit |

By Region

| North India |

| South India |

| West India |

| East and North-East India |

| By Material Type | Glass |

| Fabric | |

| By Sunroof Operation Type | Pop-up |

| Slide-in / Spoiler | |

| Panoramic | |

| Solar-integrated | |

| By Vehicle Type | Hatchback |

| Sedan | |

| Sport Utility Vehicle | |

| MPV / Others | |

| By Sales Channel | OEM-fitted |

| Aftermarket Retrofit | |

| By Region | North India |

| South India | |

| West India | |

| East and North-East India |

Key Questions Answered in the Report

How large will the India automotive sunroof market be by 2031?

It is projected to reach USD 1.57 billion by 2031, growing at a 13.88% CAGR during 2026-2031.

Which sunroof type contributes the most revenue today?

Panoramic modules commanded 46.82% of 2025 revenue, reflecting consumer preference for full-length glass roofs.

Why are OEM-fitted systems preferred over retrofits?

Factory installations ensure warranty protection, structural integrity, and optimized drainage, explaining their 81.63% shipment share in 2025.

Which region is growing fastest for sunroof demand?

East & North-East India is forecast to expand at a 15.55% CAGR through 2031 as incomes rise and vehicle ownership spreads.

Are solar-integrated sunroofs commercially viable in India?

Yes. Early models unveiled at Auto Expo 2025 demonstrate photovoltaic roofs that can add up to 20 km of daily range in sunny conditions.

Page last updated on: