India 3PL Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

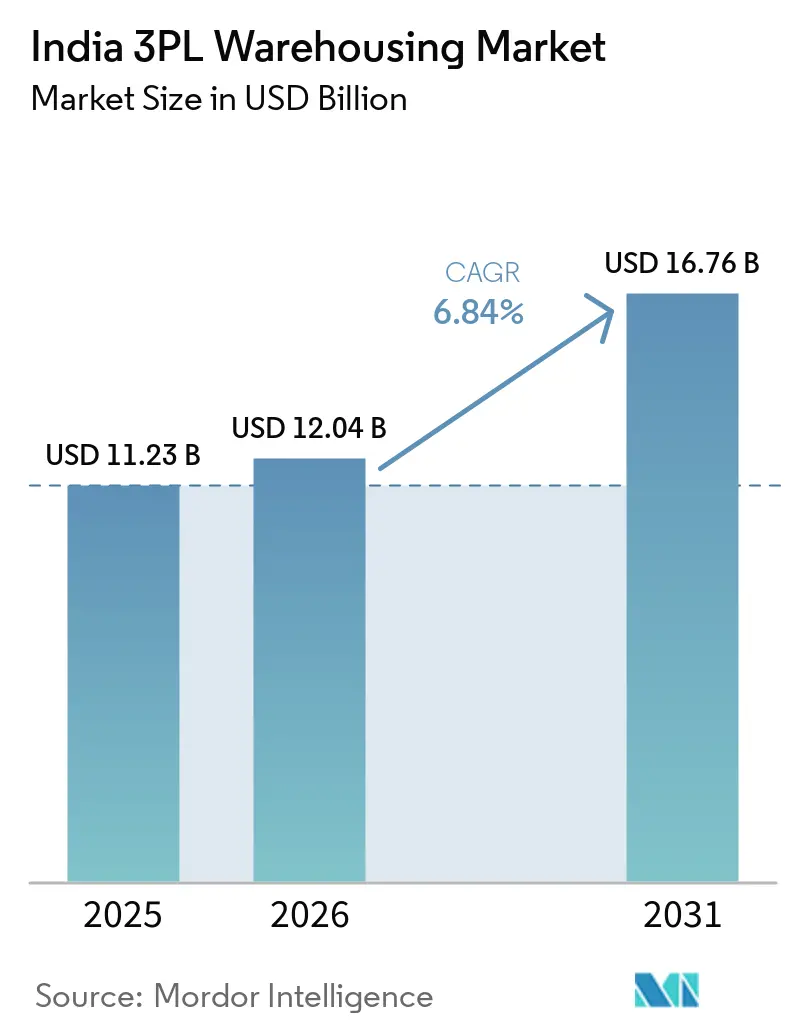

| Base Year Market Size (2025) | USD 11.23 Billion |

| Market Size (2026) | USD 12.04 Billion |

| Market Size (2031) | USD 16.76 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India 3PL Warehousing Market Analysis by Mordor Intelligence

The India 3PL warehousing market size is expected to increase from USD 11.23 billion in 2025 to USD 12.04 billion in 2026 and reach USD 16.76 billion by 2031, growing at a CAGR of 6.84% over 2026-2031.

India’s 3PL warehousing market is performing well, driven by rising outsourcing, e-commerce growth, manufacturing expansion, and the shift toward organized supply chains. The market is moving from basic storage toward modern, tech-enabled warehouses with better inventory control, faster fulfillment, and value-added services. Demand is spreading beyond major metros into tier 2 and tier 3 cities as companies seek wider coverage and shorter delivery times. Over the next few years, the outlook remains positive, supported by infrastructure upgrades, logistics formalization, and stronger demand for Grade A facilities. Growth will likely be shaped more by quality, automation, and integrated logistics solutions than by simple capacity expansion.

Key Report Takeaways

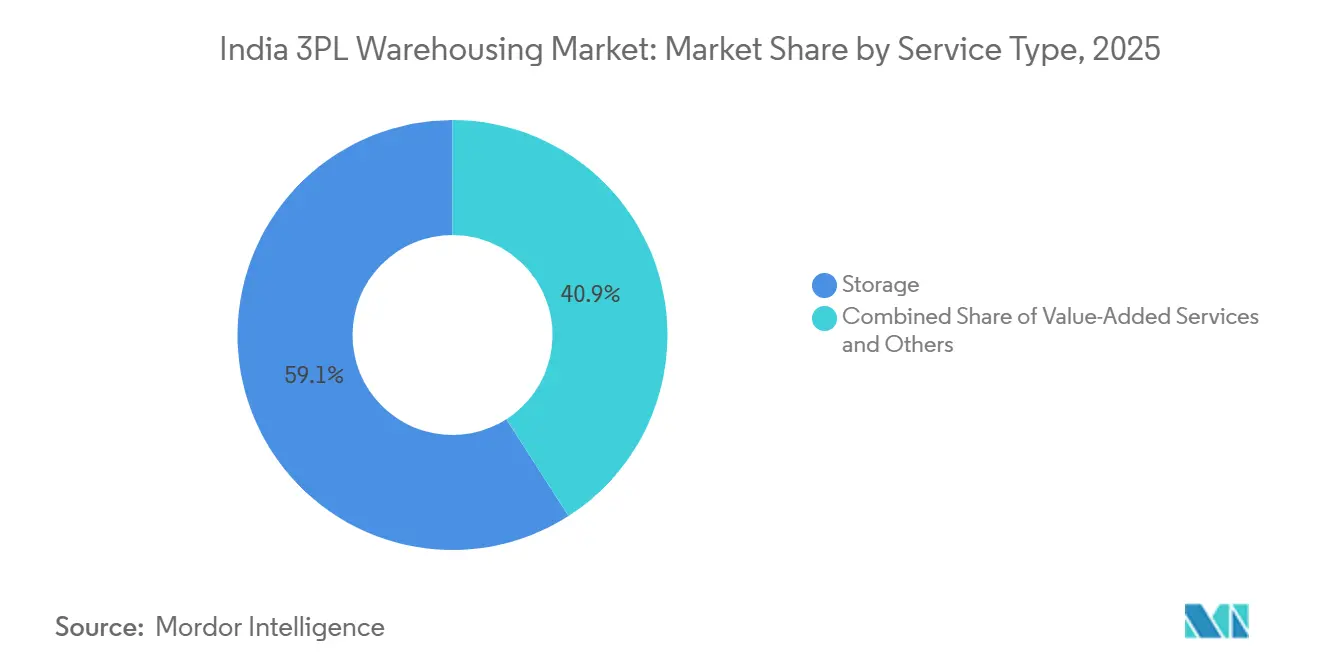

- By service type, storage held 59.07% of India 3PL warehousing market share in 2025, while value-added services are forecast to expand at 9.67% CAGR through 2031.

- By warehouse type, general shared/multi-client warehousing accounted for 55% of the India 3PL warehousing market size in 2025, while bonded warehousing is advancing at an 8.85% CAGR through 2031.

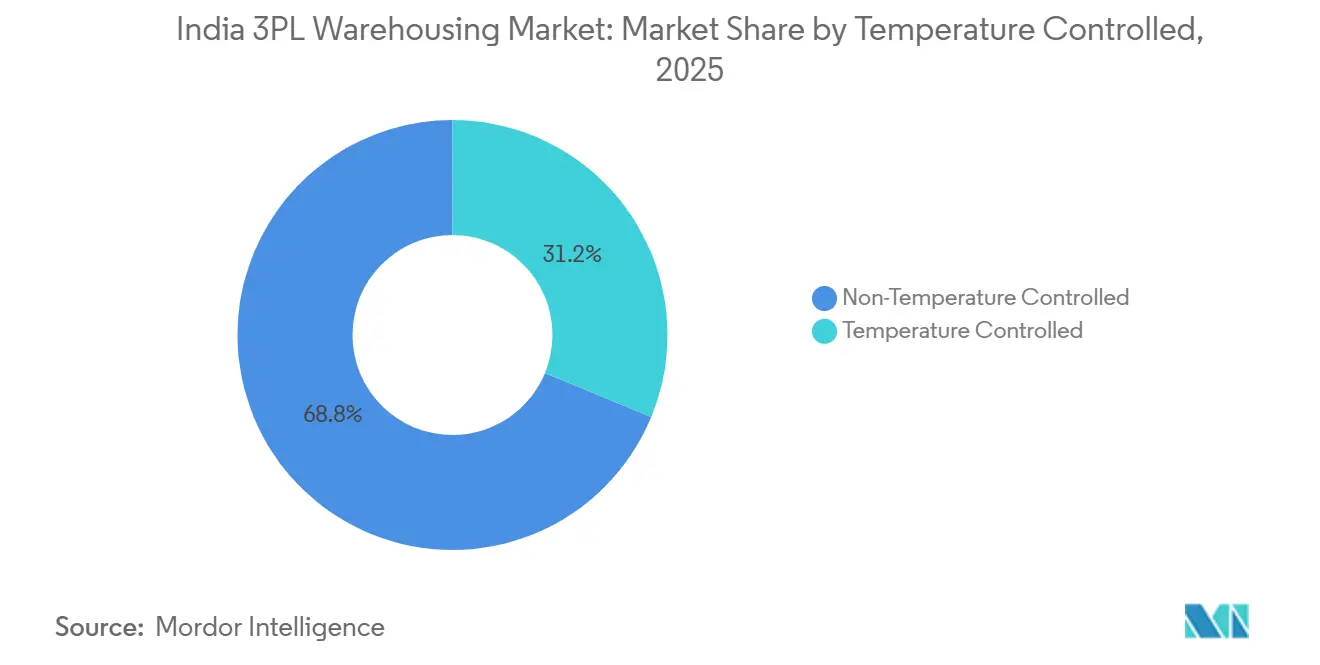

- By temperature control, non-temperature-controlled facilities held 68.78% of India 3PL warehousing market share in 2025, while temperature-controlled warehousing is growing at 10.55% CAGR through 2031.

- By technology adoption, manual warehousing captured 61.42% of India 3PL warehousing market size in 2025, while semi-automated facilities recorded the highest projected CAGR at 12.52% through 2031.

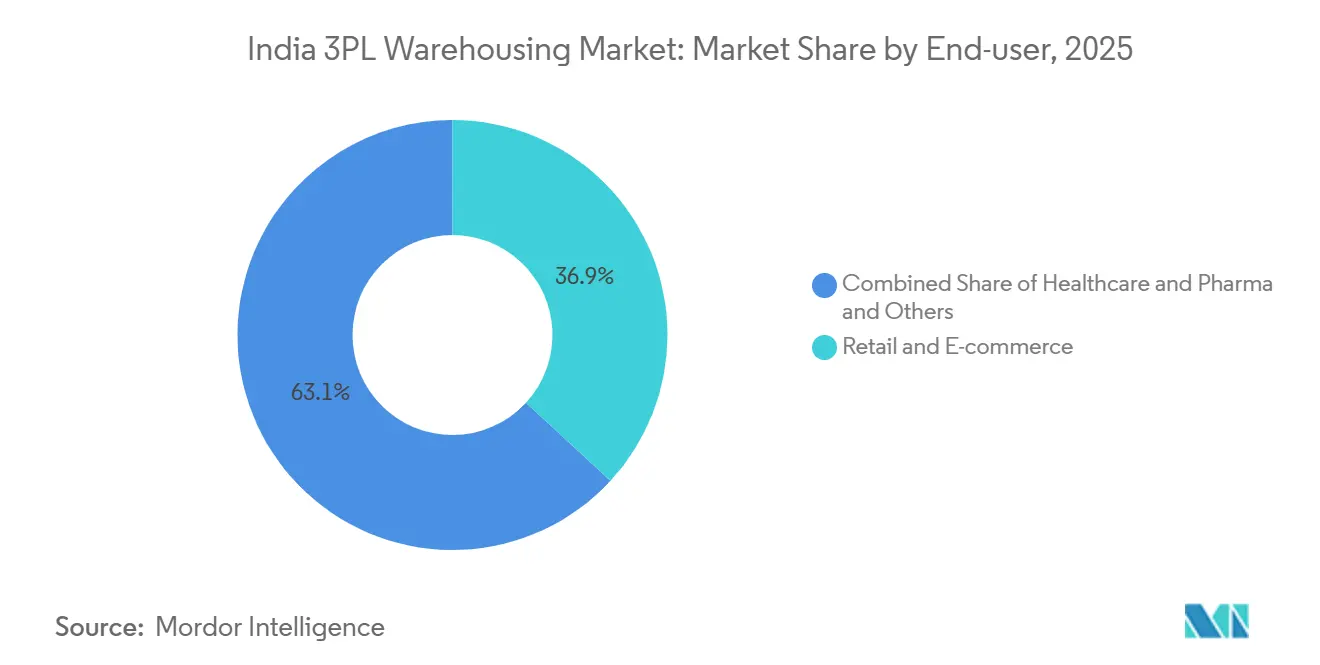

- By end user industry, retail and e-commerce held 36.86% of India 3PL warehousing market share in 2025, while healthcare and pharma are projected to grow at 9.98% CAGR through 2031.

- By region, the West region held 29.11% of the India 3PL warehousing market share in 2025, while the South region is projected to expand at 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India 3PL Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of E-Commerce Fulfillment | +1.8% | National, with concentration in Delhi-NCR, Mumbai, Bengaluru, Hyderabad | Short term (≤ 2 years) |

| Infrastructure Push | +1.2% | National, with early gains in highway corridors and DFC nodes | Medium term (2-4 years) |

| GST-Driven Network Consolidation | +0.9% | National, strongest in multi-state FMCG, pharma, and e-commerce corridors | Short term (≤ 2 years) |

| Organized Retail Demand for Grade-A Space | +0.7% | Tier-1 cities with spillover into Tier-2 cities | Medium term (2-4 years) |

| Rise of Dark Stores and Quick-Commerce Micro-Warehousing | +1.1% | Top 8 metros, with growing presence in Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| PLI Schemes Triggering Near-Factory Logistics Hubs | +0.9% | Industrial corridors across Chennai, Pune, Delhi-NCR, Gujarat, and Telangana | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of E-Commerce Fulfillment

The India 3PL warehousing market is seeing a sharper shift toward fulfillment-led demand rather than simple capacity booking. E-commerce operators are expanding dark-store and replenishment networks because speed now matters as much as inventory depth in major cities. Flipkart Minutes targeted 1,000 dark stores by April 2026, up from more than 500 in late 2025, underscoring how quickly urban replenishment networks are scaling. India had 2,525 operational dark stores as of October 2025, and this base is projected to reach 7,500 by 2030, keeping demand high for intra-city mother hubs, local storage points, and rapid-picking formats. This pattern is forcing 3PL operators to redesign legacy hub-and-spoke models around denser urban layouts, smaller footprints, and faster inventory turns.

Infrastructure Push

The India 3PL warehousing market is also benefiting from transport upgrades that reduce movement time and support larger, more efficient warehouse networks. The Eastern and Western dedicated freight corridors were 96.4% operational by March 2025, covering 2,741 route km and cutting Delhi-Mumbai freight transit time by close to 40%, while wagon turnaround dropped from 15-16 days to 2-3 days. Indian Railways had also commissioned 118 Gati Shakti Multimodal Cargo Terminals across 18 states by October 2025, which widened the map for rail-linked warehousing demand. The opening of the PM GatiShakti portal to private users also improves site planning by enabling operators to assess corridor access, utility links, and land suitability through a common data layer. Better corridor visibility and lower transit variability are making bigger multi-client and factory-linked locations more viable across the India 3PL warehousing market.

PLI Schemes Triggering Near-Factory Logistics Hubs

PLI-led manufacturing is creating a different demand pattern in the India 3PL warehousing market, as it requires bonded storage, inbound material control, and plant-adjacent distribution support. PLI investments crossed INR 2.16 lakh crore (USD 25.7 billion) by December 2025 across 14 sectors, widening the base for factory-linked logistics demand. The manufacturing push is also reinforced by the BHAVYA scheme, approved in March 2026, with an outlay of INR 33,660 crore (USD 4.0 billion) to develop 100 plug-and-play industrial parks that include warehousing and logistics facilities. This creates durable warehouse demand near electronics, automotive, pharmaceutical, and semiconductor clusters where inventory reliability matters more than just rental cost. It also supports faster growth in bonded and dedicated formats because manufacturers increasingly need warehousing close to ports, supplier corridors, and production campuses.

Rise of Dark Stores and Quick-Commerce Micro-Warehousing

Quick commerce is widening the operating range of the India 3PL warehousing market by creating demand for very small, very fast, and highly localized facilities. This demand does not align with the economics of traditional regional fulfillment, as stock must remain close to dense consumption clusters and be replenished several times each day. The result is a fresh capex cycle in micro-warehousing, mother-hub design, and high-frequency urban distribution. It also means the India 3PL warehousing market is developing a separate provider layer for quick-commerce support, where store operations, replenishment timing, and local inventory visibility matter more than pure scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land Acquisition and Zoning Bottlenecks | -0.7% | National, acute in urban micro-markets | Short term (≤ 2 years) |

| Weak First/Last-Mile Multimodal Links | -0.5% | Eastern India, Central India, North-East, rural, and Tier-3 corridors | Medium term (2-4 years) |

| Fragmented Cold-Chain Compliance | -0.4% | National, concentrated in UP, West Bengal, Gujarat | Long term (≥ 4 years) |

| High Power Tariffs Denting Automation ROI | -0.3% | National, acute in states with high tariffs and outages | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Land Acquisition and Zoning Bottlenecks

Land access remains a direct growth constraint for the India 3PL warehousing market, especially where demand is shifting closer to city limits and industrial corridors. The Warehousing Association of India stated in July 2025 that setting up a warehouse still needed close to 60 state and central permissions, which slows development and raises execution risk. Urban zoning rules add another layer because several cities restrict warehouse and cold-storage use in residential zones. At the same time, many states require wider access roads and minimum plot sizes that are hard to secure in dense neighborhoods. These frictions are particularly difficult for quick-commerce and small-format operators because they need sites close to consumers rather than far from the urban core. They also favor well-capitalized operators that can manage approvals, buy better land parcels, and wait longer for project completion.

Fragmented Cold-Chain Compliance

Cold-chain compliance remains one of the hardest gaps to close in the India 3PL warehousing market, as capacity shortages and quality inconsistencies coexist. India has a cold storage capacity of 37 million MT, against an estimated requirement of 60 million MT, leaving a structural deficit that continues to limit reliable, temperature-controlled logistics[1]National Center for Cold-chain Development, “Energy Transition in Cold Chain Infrastructure,” National Center for Cold-chain Development, nccd.gov.in. A 2026 journal study noted that only 8-10% of cold-chain operators meet WHO-GDP standards, while close to 20% of temperature-sensitive healthcare shipments are damaged or degraded in transit. This raises the cost of expansion because operators need better monitoring, documentation, equipment quality, and trained handling before they can win premium pharma and food contracts. It also means the India 3PL warehousing market will continue to reward a small group of certified operators that can offer dependable multi-zone storage and validated handling processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Redefine the Outsourcing Contract

Storage accounted for 59.07% of the India 3PL warehousing market share in 2025, indicating that basic space-and-handle outsourcing still accounts for the largest share of current demand. Distribution and inventory management remained the second-largest service line because e-commerce, consumer goods, and retail clients increasingly need stock rotation, order handling, and returns support within a single operating network. Value-added services are the fastest-growing sub-segment, with a 9.67% CAGR through 2031, confirming that the India 3PL warehousing industry is moving beyond static storage toward integrated fulfillment. This shift is strongest where clients want kitting, labeling, secondary packaging, and documentation support within the warehouse, rather than managing those steps internally. The service mix is changing because clients want fewer handoffs and greater visibility across a single operating platform.

The growth of value-added work also reflects a higher quality threshold in the India 3PL warehousing market. Food and pharma customers need tighter record keeping, batch control, FIFO or FEFO discipline, and stronger process compliance, which makes specialist outsourcing more useful. Operators that invest in better warehouse management systems and traceability tools are better positioned to capture these contracts, as clients prefer connected data and cleaner execution. The result is that service depth is becoming a clearer differentiator than floor space alone, especially in shared facilities serving multiple categories.

By Warehouse Type: Bonded Warehousing Reflects India’s Export Ambition

General shared/multi-client warehousing held 55% of the India 3PL warehousing market share in 2025, reflecting the continued preference for flexible, asset-light warehousing among shippers. This format works well for seasonal demand, early-stage D2C brands, and mid-sized manufacturers that do not want to commit to long leases or dedicated capacity. Dedicated contract warehousing remains important for anchor clients that need plant-adjacent facilities, custom layouts, and protected throughput. Bonded warehousing is the fastest-growing format, with a 8.85% CAGR through 2031, because export-oriented manufacturing and multi-country sourcing require duty-deferred storage and tighter customs-linked controls. That makes bonded space more strategic than its current scale might suggest.

The strength of this segment comes from a different demand logic inside the India 3PL warehousing market. PLI-linked electronics, semiconductor, and industrial supply chains need inbound component management before production starts, and that supports bonded facilities near ports and industrial corridors. TVS Supply Chain Solutions opened a 40,000 ft² FTWZ facility near Chennai in March 2026 to support Caterpillar’s global supply chains from India, underscoring the growing prominence of bonded warehousing in industrial logistics. Nippon Express also discussed a semiconductor logistics hub in Dholera in January 2026, with plans for specialized bonded warehousing for semiconductor materials. These moves suggest that bonded infrastructure is becoming a long-term enabler of export-linked growth rather than a niche customs service.

By Temperature Control: Cold Chain Investment Accelerates to Address Structural Deficit

Non-temperature-controlled facilities accounted for 68.78% of the India 3PL warehousing market size in 2025, consistent with the weight of dry goods, consumer products, and general manufacturing in warehouse demand. Temperature-controlled warehousing is the fastest-growing segment, and the India 3PL warehousing market size for this segment is projected to expand at 10.55% CAGR through 2031. This growth premium is directly tied to the structural cold-chain gap, as capacity remains well below the national requirement and multi-zone, multi-commodity storage is still limited. The India 3PL warehousing market is therefore seeing cold-chain investment as both a compliance response and a capacity response. Operators are investing in better refrigeration systems, energy management, and validated handling rather than simply adding general dry space.

The recent buildout shows that this segment is moving from shortage toward structured expansion. DP World launched a 110,000 ft² sustainable cold chain facility in Taloja in May 2025 with 11,000 pallet positions and multiple temperature zones[2]DP World, “DP World Strengthens Cold Chain Capabilities with New Facility in Taloja,” DP World, dpworld.com. TCI Cold Chain added a 150,000 ft² temperature-controlled warehouse in Gurugram in December 2025 with frozen, chilled, and ambient zones and SCADA monitoring. Kuehne+Nagel then launched a temperature-controlled airfreight cross-dock in Hyderabad in May 2026, strengthening its pharma handling capabilities in one of India’s most important drug manufacturing hubs. These additions support a clearer shift toward certified, higher-value cold-chain services in the India 3PL warehousing market.

By Technology Adoption: Semi-Automation as the Mainstream Upgrade Path

Manual operations accounted for 61.42% of the India 3PL warehousing market size in 2025, indicating that the installed base is still early in its automation cycle. Semi-automated facilities are the fastest-growing technology segment, with a 12.52% CAGR through 2031, as operators choose practical upgrades before moving to full robotics. Conveyors, sorters, and warehouse management systems improve throughput and accuracy without the cost intensity of full automation. That makes semi-automation the most realistic near-term upgrade path for many operators in the India 3PL warehousing industry. It is especially useful in multi-client facilities where throughput varies by customer mix and season.

This operating logic is already visible in recent capacity additions. Delhivery’s chandigarh gateway hub, launched in June 2025, combined a 235,000 ft² footprint with a hub conveyor solution, a cross-belt sorter, and rooftop solar, and it lifted capacity by 30% without moving to full automation. Kuehne+Nagel added 100,000 m² across five new fulfillment centers in October 2025 and deployed automation to increase peak order-handling capacity by 75%. DHL is also scaling automated multi-client operations in India, indicating that larger global operators are using technology to improve density, speed, and labor productivity. The market is therefore moving in layers, with semi-automation spreading first and full automation concentrating where volume and process discipline are strong enough to justify it.

By End User Industry: Healthcare Logistics Competes with E-Commerce for Investment Priority

Retail and e-commerce accounted for 36.86% of the market in 2025, making it the largest end-user segment in the India 3PL warehousing market share. This leadership comes from the scale of online retail, dark-store replenishment, organized retail distribution, and rising delivery speed expectations across major cities. Manufacturing, consumer goods, and food and beverage also provide a broad base of demand because factory output and modern retail networks require larger, more structured inventory flows. Healthcare and pharma is the fastest-growing end user, with a 9.98% CAGR through 2031, and this part of the India 3PL warehousing market is expanding faster than the overall market as compliance and temperature-control needs rise. Stricter quality requirements and the need for dependable cold-chain operations support the segment’s growth.

The South region reinforces this trend, as Hyderabad remains a major pharmaceutical anchor and attracts specialized warehousing investment. Kuehne+Nagel launched a HealthChain-certified pharma cross-dock in Hyderabad in May 2026, which shows how global operators are adding healthcare-focused infrastructure where production density is high. The India 3PL warehousing market is therefore seeing healthcare and retail compete for capital, but for different reasons. Retail needs speed, density, and omnichannel support, while healthcare needs compliance, validation, and multi-zone temperature control. That difference is pushing operators to build more specialized networks rather than one uniform warehousing model for all customers.

Geography Analysis

The West region held 29.11% of the India 3PL warehousing market share in 2025, which makes it the largest regional base in the country. Its lead comes from Mumbai’s Bhiwandi cluster, which remains India’s largest Grade-A warehousing hub at close to 42 million ft², and from the strong port advantage of Jawaharlal Nehru Port Authority, which handles more than 40% of India’s container traffic. This combination gives the India 3PL warehousing market in the West a natural edge in import-linked inventory, multi-client warehousing, and EXIM-oriented storage. The North region also remains important because Delhi-NCR connects consumption demand with inland industrial corridors and national distribution routes. Together, the West and North continue to anchor the core operating network for the India 3PL warehousing market.

The South region is the fastest-growing geography, with a 8.22% CAGR through 2031. Chennai is driving much of this expansion because its NH-16, NH-48, and Oragadam clusters are linked to electronics and automotive manufacturing. Hyderabad adds another layer, as pharma production drives stronger demand for validated, temperature-controlled warehousing. Bengaluru remains an important demand center because e-commerce and technology-linked consumption keep warehouse requirements high around the western corridor. This regional mix makes the South the clearest growth engine for the India 3PL warehousing market over the forecast period.

The East and Central regions are also becoming more visible in the national map. Mahindra Logistics added more than 4 lakh ft² of Grade-A warehousing in Guwahati and Agartala in October 2025, improving formal warehousing access in the North-East and widening organized reach in the East[3]Mahindra Group, “Mahindra Logistics Unveils 4 Lakh Square Feet of Warehousing Capacity to Strengthen Eastern India Connectivity,” Mahindra Group, mahindra.com. In Central India, DP World signed an agreement with the state of Madhya Pradesh in January 2026 to develop the Powarkheda inland logistics hub, a rail-centric facility designed to reduce transit time to JNPA by 30-40%. These moves show that the India 3PL warehousing market is widening beyond its established metro clusters and gradually linking more interior production and consumption zones into formal logistics networks.

Competitive Landscape

The India 3PL warehousing market remains less fragmented, with global operators, domestic groups, express specialists, and tech-led firms all competing across overlapping service lines. This broad field includes DHL Supply Chain, Kuehne+Nagel, DP World, FedEx, Nippon Express, Mahindra Logistics, TVS Supply Chain Solutions, Delhivery, Shadowfax, Prozo, Blue Dart, Safexpress, and others. The fragmented structure means no single company controls the operating landscape, but the top end is becoming more organized through investment, acquisitions, and corridor-based expansion. Large firms are leveraging scale, technology, and deep compliance to secure stronger positions in faster-growing niches such as healthcare logistics, bonded storage, and integrated fulfillment. That is gradually lifting the entry threshold across the India 3PL warehousing market.

One visible strategic move is Delhivery’s acquisition of Ecom Express, completed in July 2025 for INR 1,407 crore (USD 167.5 million), which expanded Delhivery’s infrastructure network and strengthened its scale position. Another is DHL Group’s EUR 1 billion (USD 1.15 billion) India investment program through 2030, announced in November 2025, which includes health logistics, EV and battery logistics, and network upgrades across multiple business lines. Kuehne+Nagel also expanded by 100,000 m² across five new fulfillment centers in October 2025, raising order-handling capacity and widening its footprint in the India 3PL warehousing market[4]Kuehne+Nagel, “Kuehne+Nagel Opens New Container Freight Station to Meet India’s Growing Trade Needs,” Kuehne+Nagel, mykn.kuehne-nagel.com. DP World strengthened its logistics position in the South by acquiring a 49% stake in the Chennai Global Logistics Park in 2026, tying warehousing growth to multimodal infrastructure. These examples show that scale is being built through both ownership moves and targeted capacity placement.

Technology and certification are also becoming sharper competitive levers in the India 3PL warehousing market. Operators with stronger automation, better WMS capability, and faster throughput can serve e-commerce and retail clients more efficiently. Operators with GDP-aligned processes, multi-zone temperature control, and stronger documentation are better positioned in healthcare and pharma. FedEx’s fully automated 300,000 ft² cargo hub at Navi Mumbai International Airport, announced in February 2026, shows how larger international firms are pairing physical infrastructure with digital handling systems to deepen their presence in India. The market is still open enough for regional and specialist operators to grow. Still, the India 3PL warehousing market is clearly rewarding firms that can combine scale, process quality, and network precision.

India 3PL Warehousing Industry Leaders

Mahindra Logistics Ltd.

TVS Supply Chain Solutions

Allcargo Supply Chain Pvt. Ltd. (Gati-Allcargo ecosystem)

Safexpress Pvt. Ltd.

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Nippon Express Holdings launched the Indian Ocean Rim Strategy Office with full-scale operations in Mumbai, targeting logistics growth across South Asia, the Middle East, and Africa.

- March 2026: TVS Supply Chain Solutions opened a 40,000 ft² warehousing facility at the FTWZ in Mannur Village, near Chennai, to strengthen Caterpillar's global supply chain from India.

- February 2026: FedEx broke ground on a fully automated 300,000 ft² air cargo hub at Navi Mumbai International Airport, representing an investment of more than INR 2,500 crore (USD 310 million).

- February 2026: Kuehne+Nagel opened a new 3,500 m² Container Freight Station in Mumbai near JNPA, adhering to CTPAT, AEO, and ISO compliance standards and featuring electric material-handling equipment. The move supports India's expanding logistics requirements for sea trade.

India 3PL Warehousing Market Report Scope

| Storage |

| Distribution and Inventory Management |

| Value-Added Services and Others (Kitting, Labelling) |

| General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing |

| Bonded Warehousing |

| Non-Temperature Controlled |

| Temperature Controlled |

| Manual |

| Semi-automated |

| Fully Automated |

| Manufacturing |

| Consumer Goods |

| Food and Beverage |

| Retail and E-commerce |

| Healthcare and Pharma |

| Other End-user Industries |

| North |

| Central |

| West |

| East |

| South |

| By Service Type | Storage |

| Distribution and Inventory Management | |

| Value-Added Services and Others (Kitting, Labelling) | |

| By Warehouse Type | General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing | |

| Bonded Warehousing | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Technology Adoption | Manual |

| Semi-automated | |

| Fully Automated | |

| By End User Industry | Manufacturing |

| Consumer Goods | |

| Food and Beverage | |

| Retail and E-commerce | |

| Healthcare and Pharma | |

| Other End-user Industries | |

| By Region | North |

| Central | |

| West | |

| East | |

| South |

Key Questions Answered in the Report

What is the expected value of the India 3PL warehousing space by 2031?

The India 3PL warehousing market is projected to reach USD 16.76 billion by 2031 from USD 12.04 billion in 2026, growing at a 6.84% CAGR.

Which region leads warehouse outsourcing demand in India?

The West region leads with 29.11% share in 2025, supported by Bhiwandi and strong port connectivity through JNPA.

Which warehouse format is growing the fastest in India?

Bonded warehousing is the fastest-growing warehouse type with an 8.85% CAGR through 2031, supported by export-linked and PLI-driven manufacturing supply chains.

Why is temperature-controlled storage gaining traction so quickly?

Temperature-controlled warehousing is growing at 10.55% CAGR because India still has a large cold storage gap, and healthcare and food users need more compliant handling.

What is driving higher demand from retail and e-commerce users?

Retail and e-commerce accounted for 36.86% of demand in 2025, supported by dark-store growth, faster delivery models, and a broader need for urban replenishment hubs.

How is automation evolving across Indian 3PL warehouses?

Manual facilities still hold 61.42% share, but semi-automated sites are growing the fastest at 12.52% CAGR as operators invest in WMS, conveyors, and sorters before full robotics.

Page last updated on: