Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

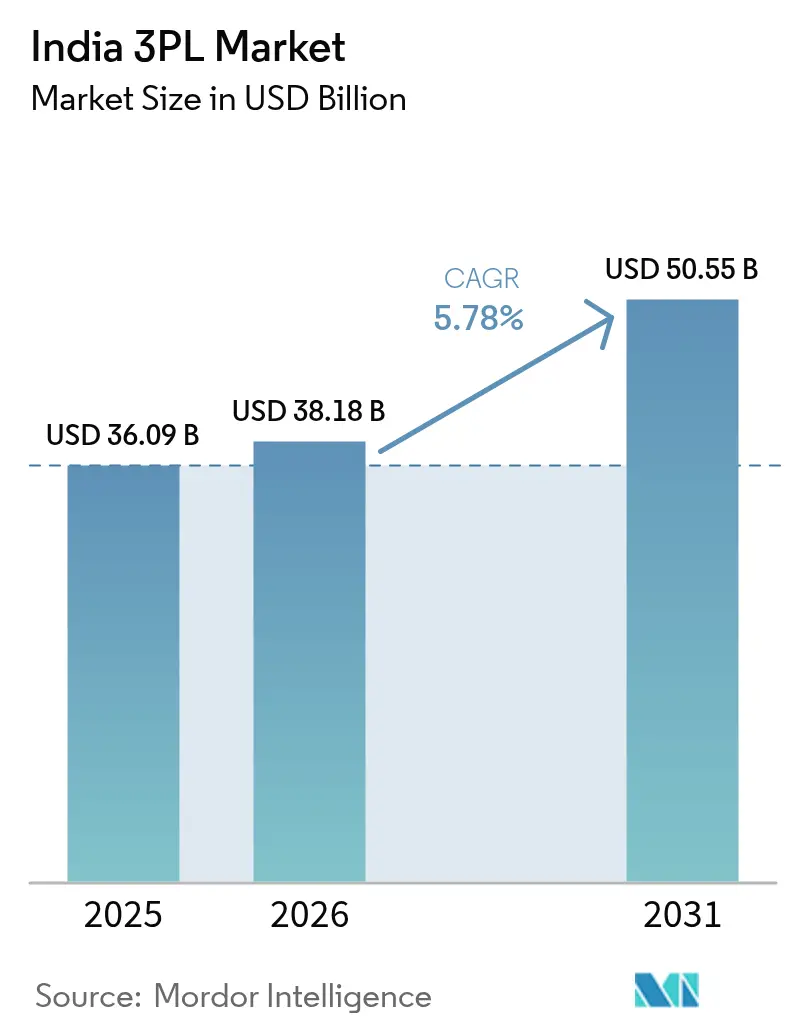

| Base Year Market Size (2025) | USD 36.09 Billion |

| Market Size (2026) | USD 38.18 Billion |

| Market Size (2031) | USD 50.55 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

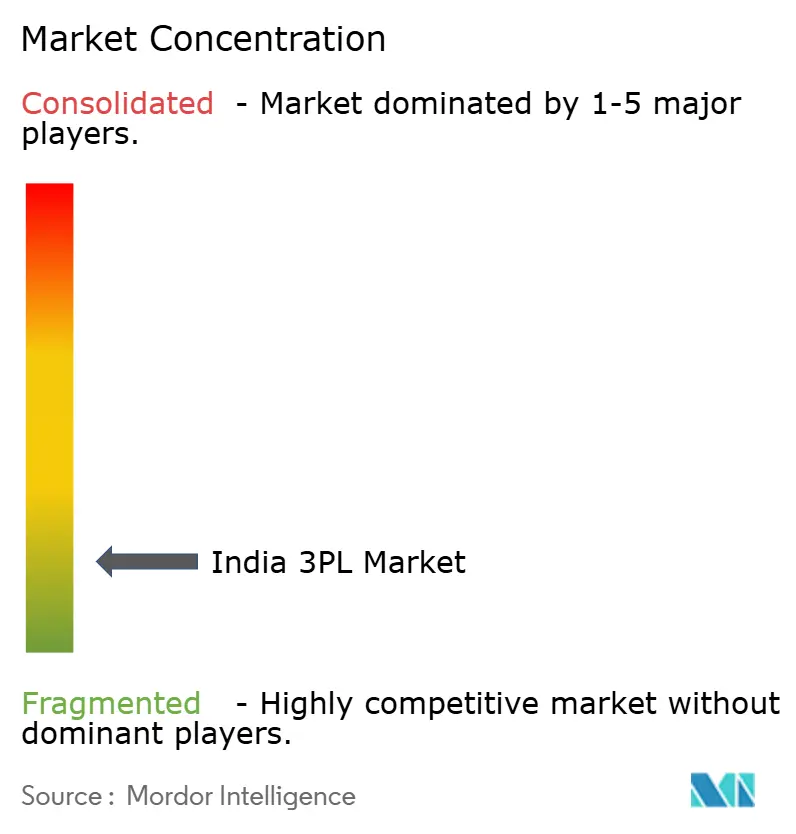

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India 3PL Market Analysis by Mordor Intelligence

India 3PL market size in 2026 is estimated at USD 38.18 billion, growing from 2025 value of USD 36.09 billion with 2031 projections showing USD 50.55 billion, growing at 5.78% CAGR over 2026-2031.

Growth stems from multi-modal infrastructure upgrades, expanding export manufacturing, and digital platforms that compress delivery lead times while lowering fulfillment costs. Shippers increasingly demand real-time shipment visibility, pushing providers toward cloud control towers and automated sortation that convert fragmented networks into integrated solutions. Asset-light orchestration, coupled with selective investment in automated hubs, is becoming the preferred scaling model as firms balance capital discipline with service assurance. Regulatory incentives under the PM GatiShakti National Master Plan reinforce the transition, targeting a reduction in logistics expenditure from 13-14% of GDP toward single-digit global benchmarks.

Key Report Takeaways

- By service, domestic transportation management led with 55.40% revenue share of the India third-party logistics market in 2025. Value-added warehousing and distribution is advancing at a 6.84% CAGR, the fastest among all offerings, through 2031.

- By end user, E-commerce captured 26.80% share of the India third-party logistics market size in 2025, while life sciences & healthcare is projected to expand at an 7.92% CAGR through 2031.

- By logistics model, asset-light operators held 41.60% of the India third-party logistics market share in 2025; hybrid models exhibit the highest growth at a 6.55% CAGR to 2031.

- By Region, West India accounted for 28.70% of revenue in 2025, whereas South India is slated to post the quickest 6.96% CAGR on the back of technology and automotive clusters.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce order-volume surge | +1.8% | West & South India concentration | Medium term (2-4 years) |

| Government infrastructure push | +1.2% | Nationwide; early gains in Delhi-NCR, Maharashtra, Karnataka | Long term (≥ 4 years) |

| FMCG & retail demand for integrated solutions | +0.9% | National; spill-over to tier-2/3 cities | Medium term (2-4 years) |

| MSME shift to multi-client automated warehouses | +0.7% | Gujarat, Tamil Nadu, Telangana | Short term (≤ 2 years) |

| Sustainability mandates from shippers | +0.4% | Maharashtra, Karnataka | Long term (≥ 4 years) |

| D2C & quick-commerce penetration | +0.6% | Tier-2/3 cities nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce order-volume surge

Rapid growth in online shopping has shifted freight from bulk B2B pallets to millions of B2C parcels that demand precise last-mile execution. Quick-commerce platforms now promise two-hour delivery windows, compelling 3PLs to install micro-fulfillment nodes and AI-enabled sorters that compress cycle times. Providers such as Delhivery are pooling dark stores to boost network density for same-day reach. ONDC’s open network integrates hyperlocal specialists, giving smaller sellers instant access to nationwide delivery rails. Annual express-parcel movements are on course for double-digit expansion, and the provider that balances urban speed with rural reach will capture an outsized wallet share.

Government infrastructure push (Gati Shakti, DFCs)

A unified digital portal now synchronizes 44 ministries, enabling project approvals and cargo routing to converge on a single map. The completed Eastern and Western Dedicated Freight Corridors have already trimmed transit times for export consignments leaving Gujarat ports for northern consumption centers, lifting rail freight revenue and reliability. Over USD 602 billion in planned public investment under the National Infrastructure Pipeline is unlocking land for multimodal parks that knit road, rail, and coastal shipping into continuous corridors. For the India third-party logistics market, these corridors lower direct operating costs and encourage modal shifts that dilute road congestion[1]Press Information Bureau, “Eastern and Western Dedicated Freight Corridors: Operational Update,” Ministry of Railways, pib.gov.in.

FMCG & retail demand for integrated solutions

Consumer-goods majors are replacing fragmented trucking contracts with single-window 3PL relationships that envelop primary haulage, cross-docking, and value-added tasks such as kitting and labeling. Grade-A warehouse stock is on pace to surpass 300 million sq ft by 2025, and 3PL operators are behind one-quarter of that build-out to serve organized retail. Temperature-controlled nodes support fresh and packaged foods as modern trade reaches smaller cities. Real-time dashboards cut inventory buffers, letting brands shrink working capital while safeguarding service levels. Compliance under GST has further advantaged organized players that can automate e-way bill generation and audit trails[2]IBEF Research Team, “Indian Warehousing Market Report 2025,” India Brand Equity Foundation, ibef.org.

MSME shift to multi-client automated warehouses (ONDC)

ONDC’s roll-out across 85 cities connects thousands of micro-sellers to plug-and-play logistics modules. Shared facilities divide fixed costs and offer robotics-enabled picking that was once the preserve of large retailers. Government incentives extend soft loans for racking and sorting automation, lowering the entry barrier for professional warehousing. Platforms such as Shiprocket bolt stock visibility to storefronts across beauty, fashion, and electronics, reinforcing omnichannel fulfilment. The India third-party logistics market consequently gains new volume streams from MSMEs that previously relied on informal trucking[3]Thampy Koshy, “ONDC Progress Report September 2024,” Open Network for Digital Commerce, ondc.org.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented trucking capacity & low visibility | -0.8% | East & Central India | Medium term (2-4 years) |

| Rising fuel, toll, and compliance costs | -0.6% | Long-haul corridors nationwide | Short term (≤ 2 years) |

| Warehouse-automation talent crunch | -0.4% | Major logistics hubs | Medium term (2-4 years) |

| Data-localization-driven IT-cost inflation | -0.3% | Large operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented trucking capacity & low visibility

Road freight still leans on millions of single-truck owners who operate without telematics or route optimization. The dominance of such micro-fleets erodes service reliability, inflates empty-haul mileage, and limits the real-time updates shippers expect. Multiple roadside inspections exacerbate dwell times, particularly on east-bound lanes where infrastructure lags. Although digital freight exchanges are emerging, adoption remains uneven, keeping the visibility gap wide for the India third-party logistics market.

Rising fuel, toll, and compliance costs

Diesel accounts for up to 40% of door-to-door road costs, and every upward tick in pump prices compresses provider margins. Toll hikes on national highways widen route economics between rail and road, nudging 3PLs to re-engineer line-haul configurations. GST slabs lifted levies on handling services, amplifying administrative overhead. Fleet upgrades to BS-VI norms raise capital outlay, while mandatory e-way bills add paperwork costs for operators lacking automated back-office systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation dominates while warehousing accelerates

Domestic transportation management generated 55.40% of India's third-party logistics market in 2025, reflecting the economy’s continued road dependence for inter-city cargo. Fuel volatility and driver scarcity, however, are pressuring margins, pushing incumbents toward route optimization algorithms and relay trucking concepts. Value-added warehousing & distribution is growing at a 6.84% CAGR, the fastest among all services, as omnichannel retailers demand deferred customization, kitting, and temperature-controlled storage. Dedicated freight corridors funnel more bulk product to rail, nudging road-only operators to partner for line-haul legs, a shift that exemplifies the market’s multimodal evolution.

Automated storage and retrieval systems and goods-to-person robots are now standard in new builds, and cloud WMS lets 3PLs integrate inventory views across multiple clients in real time. International transportation rides on India’s export ambitions; alliances like Delhivery–Team Global Logistics offer LCL connectivity to 120 countries. Coastal shipping remains niche but gains relevance under Sagarmala, while airfreight addresses time-critical pharma and electronics consignments. As customers prize turnkey visibility, providers that knit these modes into one control-tower dashboard are winning longer contracts and cross-selling opportunities in the India third-party logistics market.

By End User: E-commerce leads while healthcare surges

E-commerce occupied 26.80% of the India third-party logistics market share in 2025, thanks to a quadrupling in grade-A warehousing since 2017 and the march of quick-commerce into tier-3 districts. Order patterns have fragmented into high-frequency, low-value parcels that strain legacy hub-and-spoke models, fueling investment in regional sort centers and delivery lockers. Life sciences & healthcare shows the highest 7.92% CAGR to 2031. Export-oriented pharmaceutical clusters around Hyderabad and Ahmedabad require GDP-certified cold chain, lane validation, and regulatory documentation. Vaccine distribution and specialty biologics have accelerated demand for validated packaging and multi-temperature storage.

Automotive volumes stabilize as OEMs shift to just-in-time sequencing and explore electric-vehicle component flows, creating needs for hazmat battery transport and reverse logistics. Production-Linked Incentive schemes spur electronics and textile factories to scale, feeding new B2B flows. Temperature-controlled segments in food & beverages capitalize on rising urban disposable incomes, pushing 3PLs to extend refrigerated capacity deeper into smaller towns. Energy projects, particularly renewables, draw specialized heavy-lift and last-mile microgrid deliveries, broadening the India third-party logistics market canvas.

By Logistics Model: Asset-light prevails while hybrid gains momentum

Asset-light orchestration captured 41.60% of 2025 revenue, validating a strategy that privileges network reach over fixed-asset ownership. Tech platforms match loads with third-party carriers, turning variable costs into a leverable advantage. Yet hybrid models, combining strategic asset control with outsourced spokes, are expanding at a 6.55% CAGR. Providers selectively own automated mega-hubs and trailer pools for peak assurance while subcontracting last-mile vans to regional partners. Asset-heavy players maintain end-to-end control but face utilization risk.

API-first platforms let hybrid operators surface unified visibility, enabling dynamic SLA allocation regardless of asset owner. ONDC integration makes dormant capacity discoverable, effectively expanding the virtual fleet for asset-light orchestrators. As contract tenures lengthen and customers audit ESG metrics, selective asset ownership—especially electric vehicle fleets—can hedge supply risk and bolster sustainability credentials in the India third-party logistics market.

Geography Analysis

West India led with a 28.70% share in 2025, propped up by Maharashtra’s Mumbai-Pune industrial belt and Gujarat’s twin-port engine of JNPT and Kandla. Automotive, pharma, and chemical exporters rely on dense road-rail-port linkages, and the Western Dedicated Freight Corridor now moves containers from hinterland factories to docks faster than legacy lines. Grade-A warehouses continue to cluster along the NH-48 corridor, though land prices and congestion push new facilities toward peripheral nodes. Providers with rail-road transloading capability gain an edge by blending cheaper rail for trunk movement with road for the final 100 km stretch.

South India is on track for the fastest 6.96% CAGR through 2031. Bangalore anchors high-value electronics returns and forward flows, demanding secure cross-dock and reverse logistics. Chennai’s auto OEMs integrate inbound sequencing yards with just-in-time assembly, requiring hour-level precision. Hyderabad’s pharmaceutical exports call for GDP-qualified cold rooms and validated packaging lanes. Ports such as Chennai, Ennore, Krishnapatnam, and Visakhapatnam provide multimodal exits, lowering dwell times for export boxes. 3PLs that align hub locations to this mixed cargo base are positioned to capture recurring contract revenue within the India third-party logistics market.

North India’s Delhi-NCR remains a consumption magnet, feeding steady FMCG and retail inbound tonnage. Connectivity upgrades like the 121-km Haryana Orbital Rail Corridor will divert industrial freight away from saturated urban arterials, unlocking land for new logistics parks. Seasonal farm output from Punjab and Haryana, however, imposes capacity peaks that strain fragmented truck supply. East India, historically constrained by limited industry and infrastructure gaps, is set to benefit as the Eastern Dedicated Freight Corridor links Kolkata hinterlands to northern demand centers. Central India, with land-locked Madhya Pradesh at its core, is pitching itself as a pan-India DC location, leveraging equidistant access to four metros and offering lower real-estate costs.

Competitive Landscape

The competitive terrain is transitioning from fragmented regional operators to a tiered structure of pan-India giants, tech-first disrupters, and niche specialists. Incumbents such as Allcargo, Mahindra Logistics, and TVS Supply Chain leverage multimodal assets, while digital natives like Delhivery emphasize cloud orchestration and data analytics. Delhivery’s USD 170 million purchase of Ecom Express in 2025 unlocks network overlap savings and raises the entry bar for mid-sized parcel players.

International integrators—DHL, FedEx, and Kuehne + Nagel—retain strongholds in temperature-controlled pharma and automotive sequencing but face price competition on domestic lanes. Growth white space lies in tier-2/3 cities where organized penetration remains shallow; here, shared dark stores and drone pilots promise differentiated reach. Sustainability is emerging as a tie-breaker; early adopters of electric vans and solar-powered DCs secure mandates from ESG-focused shippers. Compliance mastery around GST, e-invoicing, and safety certifications serves as a moat, nudging informal fleets either toward aggregation platforms or exit. Over the next five years, industry observers expect accelerated roll-ups as capitalized leaders consolidate scale, data, and talent-dense automation infrastructure within the India third-party logistics market.

India 3PL Industry Leaders

Allcargo Logistics Ltd.

DHL Supply Chain India

Mahindra Logistics Ltd.

TVS Supply Chain Solutions Ltd.

Delhivery Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UK-India Free Trade Agreement Signed – The bilateral pact is expected to lift annual two-way trade by USD 34 billion, expanding demand for cross-border freight forwarding and customs brokerage services.

- April 2025: Delhivery completed its USD 170 million acquisition of Ecom Express, creating India’s largest express-delivery network by parcel volume.

- January 2025: Blue Dart Unveils Delhi Logistics Hub – The automated facility can handle 50,000 shipments daily, reinforcing the carrier’s presence in North India.

- January 2025: LEAP India acquired CHEP India’s pallet pooling operations, deepening its end-to-end supply-chain solutions capability.

India 3PL Market Report Scope

A comprehensive background analysis of the India 3PL Market, covering the current market trends, restraints, technological updates and detailed information on various segments and competitive landscape of the industry.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light |

| Asset-Heavy |

| Hybrid |

By Region (Value)

| North India | Delhi-NCR |

| Punjab | |

| Haryana | |

| Others | |

| South India | Karnataka |

| Tamil Nadu | |

| Telangana | |

| Others | |

| West India | Maharashtra |

| Gujarat | |

| Others | |

| East India | West Bengal |

| Odisha | |

| Others | |

| Central India | Madhya Pradesh |

| Chhattisgarh |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light | |

| Asset-Heavy | ||

| Hybrid | ||

| By Region (Value) | North India | Delhi-NCR |

| Punjab | ||

| Haryana | ||

| Others | ||

| South India | Karnataka | |

| Tamil Nadu | ||

| Telangana | ||

| Others | ||

| West India | Maharashtra | |

| Gujarat | ||

| Others | ||

| East India | West Bengal | |

| Odisha | ||

| Others | ||

| Central India | Madhya Pradesh | |

| Chhattisgarh | ||

Key Questions Answered in the Report

How large is the India third-party logistics market in 2026?

The market stands at USD 38.18 billion and is on a 5.78% CAGR trajectory toward USD 50.55 billion by 2031.

Which service segment is growing quickest?

Value-added warehousing and distribution is expanding at a 6.84% CAGR thanks to omnichannel fulfillment demand.

What end-user vertical shows the fastest logistics growth?

Life sciences & healthcare leads with an 7.92% CAGR driven by cold-chain pharmaceutical exports.

Why are hybrid logistics models gaining ground?

They blend ownership of critical automation assets with outsourced route legs, balancing capital efficiency and service control.

Which region is expected to post the highest growth?

South India is forecast to grow at 6.96% CAGR on the back of technology, automotive, and pharma clusters.

How is government policy influencing logistics costs?

PM GatiShakti corridors and ULIP digital integration are designed to push logistics costs toward single-digit GDP levels by enhancing multimodal efficiency.

Page last updated on: