Lateral Flow Assays Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

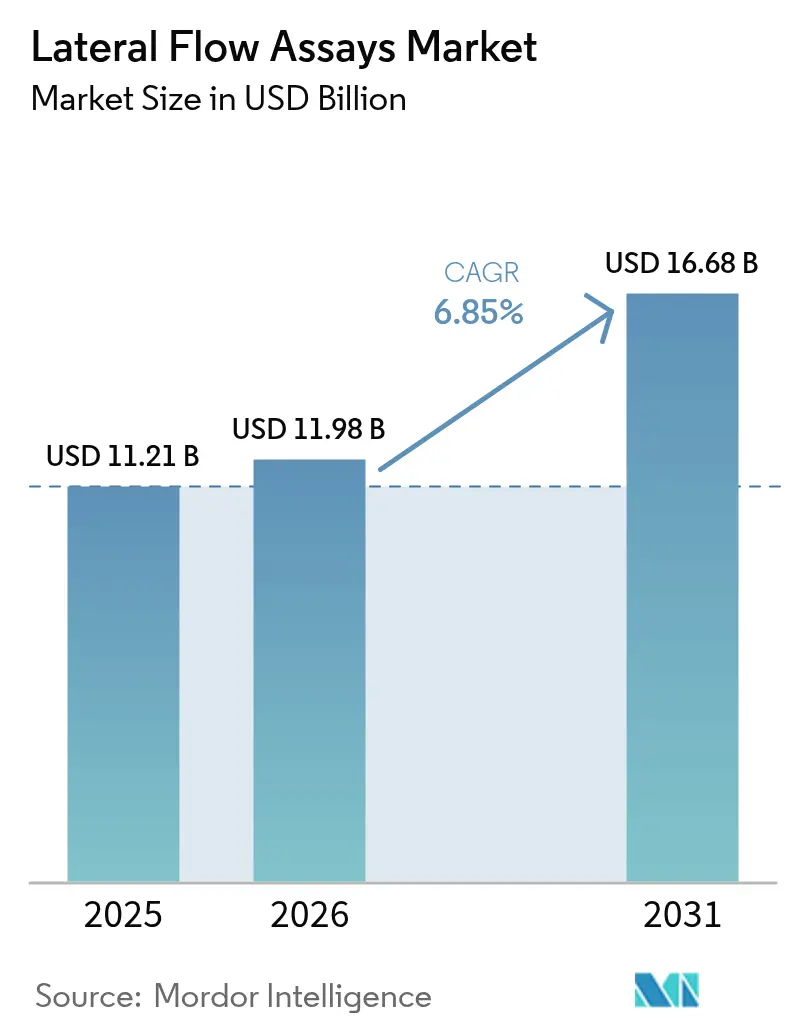

| Market Size (2026) | USD 11.98 Billion |

| Market Size (2031) | USD 16.68 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

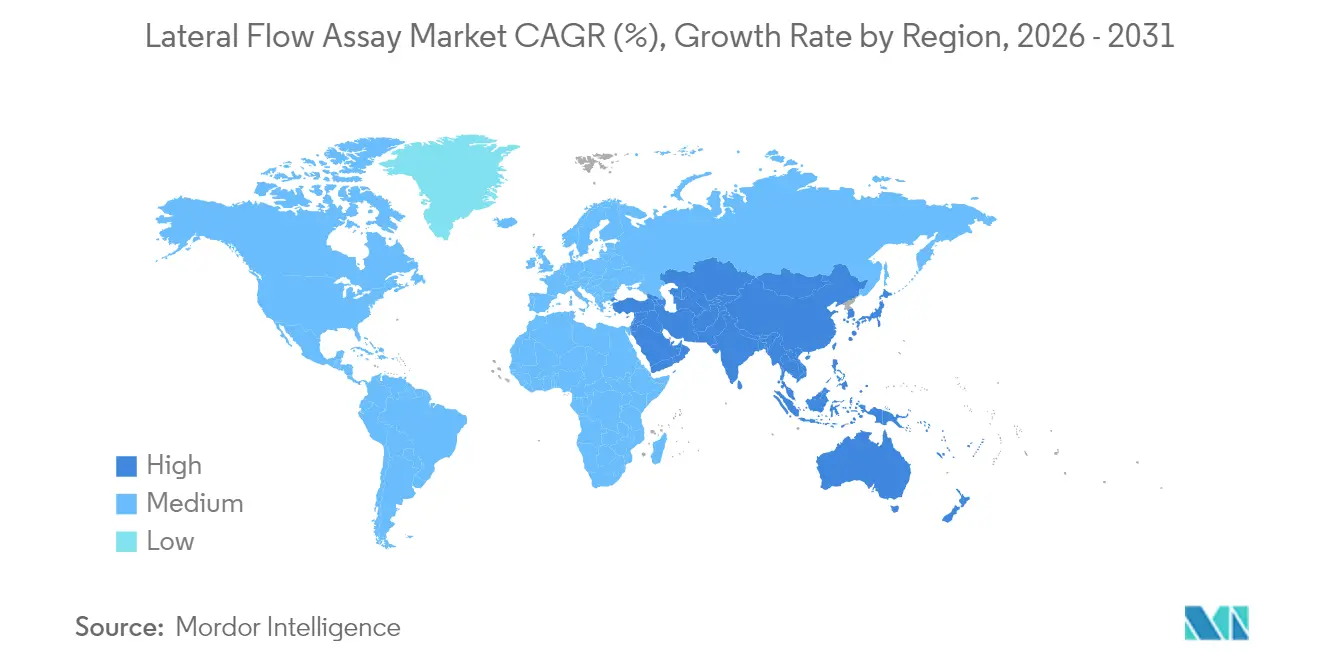

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

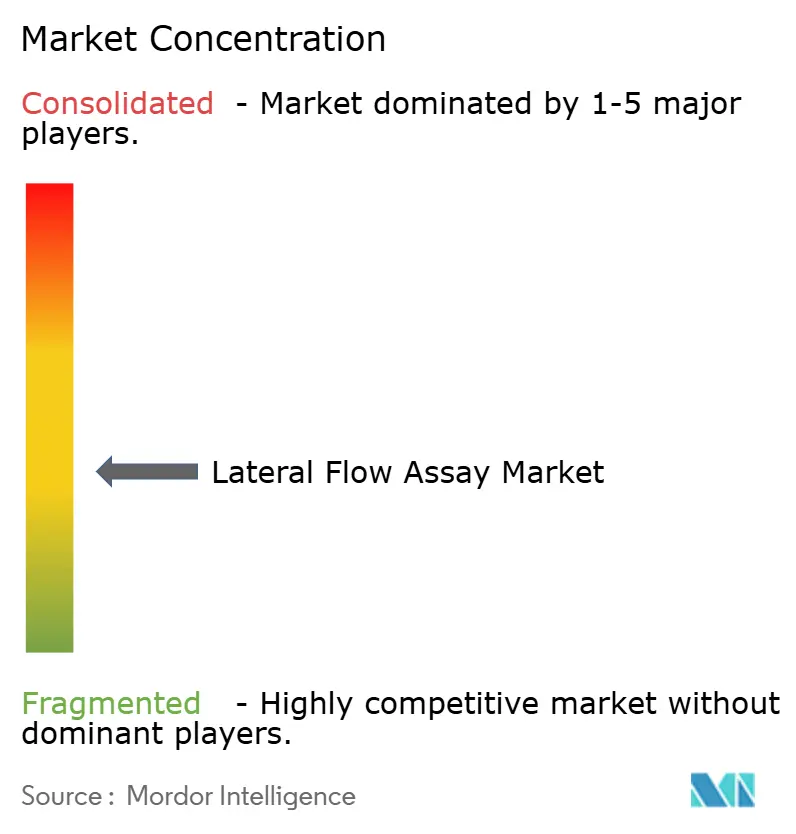

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lateral Flow Assays Market Analysis by Mordor Intelligence

The Lateral Flow Assay Market size was valued at USD 11.21 billion in 2025 and estimated to grow from USD 11.98 billion in 2026 to reach USD 16.68 billion by 2031, at a CAGR of 6.85% during the forecast period (2026-2031).

Consistent demand for decentralized diagnostics, expanding use in home settings, and rapid regulatory evolution underpin this growth. Manufacturers benefit from the United States Food and Drug Administration’s (FDA) phased regulation of laboratory-developed tests, which improves product reliability and fosters clinician confidence. Technology convergence especially multiplex detection and digital readers opens white-space opportunities across clinical, veterinary, and food-safety domains. Meanwhile, environmental sustainability pressures incentivize research into biodegradable substrates and circular-economy manufacturing, creating additional avenues for differentiation.

Key Report Takeaways

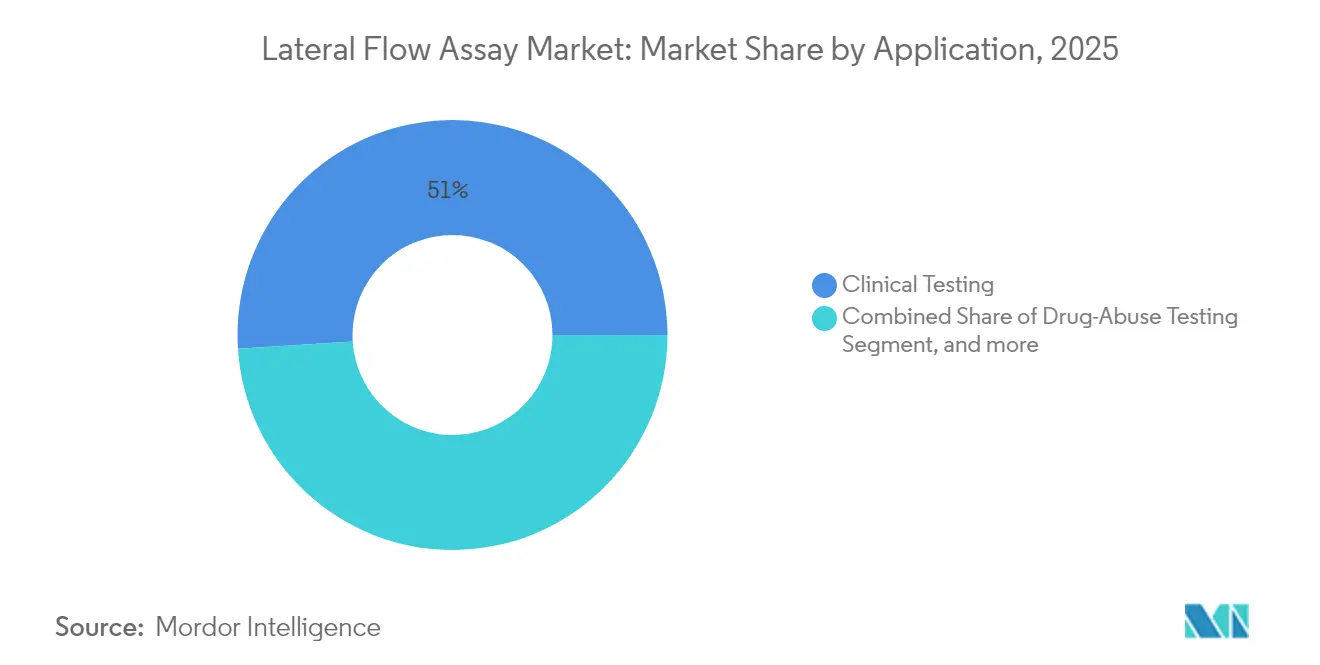

- By application, clinical testing retained 51.02% of the lateral flow assays market share in 2025, while drug-abuse testing is poised for a 10.24% CAGR through 2031.

- By technique, sandwich assays dominated with 66.02% lateral flow assays market share in 2025; multiplex assays are forecast to expand at 11.32% CAGR to 2031.

- By product, kits and reagents commanded 71.10% share of the lateral flow assays market size in 2025 and are set to grow at 11.98% CAGR.

- By end user, hospitals and clinics accounted for 46.50% of the 2025 lateral flow assays market size, whereas home care settings will accelerate at 12.95% CAGR.

- By geography, North America led with 37.70% revenue share in 2025; Asia-Pacific is projected to register the fastest regional CAGR of 10.63% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lateral Flow Assays Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating demand for point-of-care diagnostics | +1.8% | Global; strongest in North America & APAC | Medium term (2-4 years) |

| Surge in home-based testing adoption | +1.5% | North America & Europe; expanding to APAC | Short term (≤ 2 years) |

| Expansion into veterinary diagnostics & food safety | +1.2% | Global; early gains in North America, Europe, APAC | Long term (≥ 4 years) |

| Increased preparedness for biothreats | +1.0% | North America & Europe; spill-over to MEA | Medium term (2-4 years) |

| Integration with smartphone apps & digital readers | +0.8% | Global; led by North America & APAC | Long term (≥ 4 years) |

| Cost-effectiveness and scalability | +0.6% | Global; high impact in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Demand for Point-of-Care Diagnostics

Healthcare providers intensify adoption of rapid testing to shorten treatment cycles and improve patient throughput. The FDA’s clearance of a high-sensitivity cardiac troponin I assay that delivers results in 17 minutes validates the clinical utility of advanced lateral flow formats.[1]Association for Diagnostics & Laboratory Medicine, “FDA Clears First Point-of-Care High-Sensitivity Cardiac Troponin I Test,” adlm.org Retail clinics, urgent-care centers, and workplace programs now deploy multiplex respiratory panels that simultaneously identify SARS-CoV-2, influenza A/B, and RSV, enabling single-visit triage. Investments in miniaturized detection modules and wireless connectivity position lateral flow platforms as core elements of continuous monitoring ecosystems and remote patient-management models.

Surge in Home-Based Testing Adoption

COVID-19 normalized self-testing, and regulators are widening the over-the-counter pathway. The FDA authorized an antigen combination test for COVID-19 and influenza under a standard 510(k) in 2024, lowering barriers for similar multiplex home tests.[2]U.S. Food and Drug Administration, “Healgen COVID-19/Flu A&B Antigen Test Authorization,” fda.gov Direct-to-consumer distribution provides manufacturers with recurring revenue streams and richer real-world data. Consumers favor the convenience of 15-minute results from single finger-stick blood drops, as exemplified by the First To Know Syphilis Test. Home-based diagnostics reduce clinical visits, cut payer costs, and support earlier therapeutic intervention, reinforcing market expansion.

Expansion into Veterinary Diagnostics and Food Safety Applications

Growing scrutiny of zoonotic disease transmission and stringent food-safety regulations drive lateral flow penetration beyond human healthcare. Rapid avian-influenza panels for H5 and H7 strains give poultry producers actionable results in 30 minutes, limiting culling losses. Similar platforms detect Salmonella enterica with 100-fold higher sensitivity than traditional PCR methods, trimming turn-around from seven days to three. Paper-based assays for porcine epidemic diarrhea virus reach 95.3% sensitivity compared with RT-PCR. One-Health initiatives endorsed by the World Organisation for Animal Health (WOAH) position these assays as cornerstone tools for integrated surveillance.

Increased Preparedness for Biothreats and Public Health Emergencies

Government biodefense budgets channel funding to rapid, field-deployable diagnostics. Programs exploring bioagent-agnostic signatures require multiplex immunoassays capable of detecting pathogen DNA alongside host-response biomarkers.[3]Johns Hopkins Center for Health Security, “Detecting Biological Threats: BIOINT Paradigm,” healthsecurity.com The U.S. Department of Health and Human Services prioritizes domestic manufacturing capacity for surge demand, encouraging on-shore production partnerships. Such investments create steady demand for innovative lateral flow formats with metagenomic integration that can handle novel or engineered threats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented and evolving regulatory frameworks | -1.2% | Global; variable by region | Medium term (2-4 years) |

| Higher false-negative risk vs. PCR | -0.8% | Global; acute in clinical settings | Short term (≤ 2 years) |

| Volatility in supply of key raw materials | -0.6% | Global; acute in APAC manufacturing | Short term (≤ 2 years) |

| Environmental concerns over single-use plastics | -0.4% | Europe & North America; growing globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented and Evolving Regulatory Frameworks

Divergent rules across the United States, China, and the European Union complicate global submission strategies. The FDA’s four-year phase-out of enforcement discretion on laboratory-developed tests could cost the sector between USD 566 million and USD 3.56 billion in compliance spending. China’s National Medical Products Administration (NMPA) is simultaneously rolling out a 24-measure reform program, and the EU continues to refine in-vitro diagnostic regulations. Smaller firms face disproportionate burden, curbing innovation velocity despite the long-term benefit of universally higher quality standards.

Higher False-Negative Risk Compared to Molecular Diagnostics

Conventional immunoassays may detect as little as 30% of influenza A cases relative to PCR benchmarks. This performance gap curtails adoption for critical diagnoses. However, DNA-origami amplification and plasmonic scattering enhancements now cut detection limits by up to 4,400-fold, narrowing the gap and highlighting that sensitivity constraints are engineering challenges rather than intrinsic limitations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Clinical Testing Retains Primacy

Clinical testing captured 51.02% of the 2025 lateral flow assays market, underpinning routine workups in hospitals, clinics, and laboratories. The segment benefits from renewed growth in multiplex respiratory panels that diagnose SARS-CoV-2, influenza A/B, and RSV in a single visit. Pregnancy testing remains a mainstay across all care settings, while tuberculosis assays gain traction thanks to global elimination initiatives. Drug-abuse testing, currently smaller in absolute dollars, accelerates at a 10.24% CAGR through 2031 as employers respond to evolving marijuana legalization and safety mandates. Environmental monitoring and veterinary testing collectively account for a modest share today but show strong upside as regulators tighten surveillance requirements.

Clinical testing’s continued dominance is reinforced by improved reimbursement pathways and clinician trust in sandwich formats that deliver 15-minute results. Meanwhile, the fastest-growing drug-abuse segment benefits from advancements in multiplex panels capable of detecting synthetic cannabinoids and opioids without sacrificing speed. These developments solidify diversified revenue streams and mitigate reliance on legacy pregnancy testing.

By Technique: Multiplex Assays Drive Innovation

Sandwich assays anchored 66.02% of the 2025 lateral flow assays market share owing to established manufacturing and high specificity. Yet, multiplex formats are projected to expand at 11.32% CAGR as health systems demand concurrent detection of multiple pathogens or biomarkers. CRISPR-Cas13a strips have already shown perfect concordance with RT-qPCR for multivirus panels, signaling a new performance benchmark. Competitive and reverse-flow assays continue serving niche applications such as small-molecule drug screening and enhanced-sensitivity hormone testing.

Multiplex innovation is propelled by radially compartmentalized paper chips that identify multiple gene targets within 10 minutes and integrate seamlessly with smartphone readers. Phenylboronic acid-modified magnetic quantum dots further raise the sensitivity ceiling, bringing molecular-class performance to low-cost substrates. This technical momentum suggests escalating adoption of multiplex platforms across infectious disease, oncology, and companion-diagnostic workflows.

By Product: Kits and Reagents Command Dual Leadership

Kits and reagents accounted for 71.10% of total revenue in 2025 and also exhibit the highest growth trajectory at 11.98% CAGR. The consumable nature of reagents ensures recurring revenue and creates low switching costs for customers. Nanotechnology innovations, such as gold-nanostar antibody conjugates detecting alpha-fetoprotein at 8.6 ng/mL, raise assay sensitivity while preserving cost advantages.

Digital and mobile readers, a subsegment within instrument hardware, deliver the fastest gains as health providers seek quantitative outputs and seamless data integration. Benchtop readers remain critical in core laboratories where higher throughput offsets capital expenditure. The convergence of novel labels like polymerized alizarin red-inorganic hybrids with connected hardware creates an ecosystem effect that supports sustained product demand.

By End User: Home Care Takes the Growth Spotlight

Hospitals and clinics represented 46.50% of the 2025 lateral flow assays market size, drawing on entrenched procurement pipelines and integrated electronic-medical-record systems. Nonetheless, home care settings are expected to outpace all others with a 12.95% CAGR as consumers prioritize convenience. The FDA’s clearance of a 30-minute home test for chlamydia, gonorrhea, and trichomoniasis illustrates regulator willingness to broaden at-home diagnostics. Laboratories and research centers continue to employ lateral flow strips as rapid confirmation methods and screening tools, ensuring balanced demand across user categories.

Ultra-sensitive bead-based immunoassays are now supporting continuous-flow analysis for toxins, enabling future home-monitoring applications in chronic disease management. Such innovations expand the technology’s value proposition beyond episodic testing, reinforcing home care’s role as a structural growth driver.

Geography Analysis

North America maintained the largest share at 37.70% in 2025. Robust healthcare infrastructure, payer reimbursement, and the FDA’s clear LDT framework underpin consistent demand. U.S. retail clinics and pharmacy chains increasingly deploy multiplex respiratory panels, while Canada and Mexico leverage USMCA supply-chain synergies to broaden access.

Asia-Pacific is the fastest-growing region at 10.63% CAGR. China’s 24-measure medical-device reform and the Healthy China 2030 agenda elevate domestic innovation and expedite approvals. The region also benefits from cost-competitive manufacturing that shortens time-to-market and expands availability in populous nations such as India and Indonesia. Japan’s aging demographics further fuel demand for rapid, user-friendly diagnostics.

Europe posts steady growth based on stringent performance requirements and environmental sustainability mandates that drive adoption of biodegradable substrates. Coordinated procurement in the European Union supports pan-regional launches, while national health systems adopt point-of-care platforms to lower hospital burden. The Middle East & Africa and South America record rising uptake aided by public-health programs and international funding, although supply-chain volatility and import duties occasionally temper growth. Geographic diversification ensures the lateral flow assays market remains resilient to localized downturns.

Competitive Landscape

The lateral flow assays market exhibits moderate fragmentation, with multinational leaders consolidating specialized know-how through mergers and acquisitions. Roche’s USD 295 million purchase of LumiraDx’s point-of-care platform strengthens its decentralized portfolio and expands global distribution. Danaher’s new CLIA-certified Centers of Innovation and Thermo Fisher’s reagent manufacturing expansions illustrate strategic capacity building.

Emerging entrants leverage DNA origami, plasmonic nanoparticles, and CRISPR systems to leapfrog legacy performance. QuidelOrtho’s leadership realignment underscores the importance of operational agility amid fast-moving technological shifts. Sustainable manufacturing and biodegradable strip materials increasingly influence purchasing decisions, conferring competitive advantage to early adopters. Digital-health capabilities further differentiate players, turning data analytics and connectivity into critical selection criteria for health-system buyers.

Lateral Flow Assays Industry Leaders

F. Hoffmann-La Roche AG

Abbott Laboratories

Danaher Corporation

Thermo Fisher Scientific Inc.

bioMérieux SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Abingdon Health plc entered a co-development and commercialization agreement with Okos Diagnostics B.V. to accelerate next-generation lateral flow platform deployment.

- May 2024: In collaboration with Salignostics and Crest Medical, Abingdon Health PLC, one of the key lateral flow Contract Development and Manufacturing Organisation (CDMO), launched Boots' own-brand saliva pregnancy self-test in the United Kingdom.

Global Lateral Flow Assays Market Report Scope

As per the scope of the report, lateral flow assays, also referred to as lateral flow immunochromatographic assays, are cellulose-based devices used to detect the presence of a target analyte in the sample without the need for specialized and costly equipment and highly skilled healthcare professionals for their operation.

The lateral flow assay market is segmented by application, technique, product, end user, and geography. By application, the market is segmented into clinical testing, drug abuse testing, and other applications. The clinical testing segment includes pregnancy testing, influenza testing, tuberculosis, D-dimer testing, and other clinical testing. By technique, the market is segmented into sandwich assay, competitive assay, and multiplex assay. By product, the market is segmented into lateral flow readers and kits and reagents. The lateral flow readers include digital/mobile readers and benchtop readers. By end user, the market is segmented into home care, hospitals and clinics, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for all the above segments.

| Clinical Testing | Pregnancy Testing |

| Influenza Testing | |

| Tuberculosis Testing | |

| D-dimer Testing | |

| Other Clinical Testing | |

| Drug-Abuse Testing | |

| Environmental Monitoring | |

| Other Applications |

| Sandwich Assay |

| Competitive Assay |

| Multiplex Assay |

| Reverse Flow Assay |

| Kits & Reagents | |

| Lateral-Flow Readers | Digital / Mobile Readers |

| Benchtop Readers |

| Home Care Settings |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Veterinary & Food Testing Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Clinical Testing | Pregnancy Testing |

| Influenza Testing | ||

| Tuberculosis Testing | ||

| D-dimer Testing | ||

| Other Clinical Testing | ||

| Drug-Abuse Testing | ||

| Environmental Monitoring | ||

| Other Applications | ||

| By Technique | Sandwich Assay | |

| Competitive Assay | ||

| Multiplex Assay | ||

| Reverse Flow Assay | ||

| By Product | Kits & Reagents | |

| Lateral-Flow Readers | Digital / Mobile Readers | |

| Benchtop Readers | ||

| By End User | Home Care Settings | |

| Hospitals & Clinics | ||

| Diagnostic Laboratories | ||

| Veterinary & Food Testing Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the lateral flow assays market?

The lateral flow assays market is valued at USD 11.98 billion in 2026.

Which application segment is growing fastest?

Drug-abuse testing leads growth with a projected 10.24% CAGR through 2031.

Why is Asia-Pacific considered the most attractive growth region?

Regulatory reforms, expanding healthcare access, and cost-effective manufacturing drive an 10.63% regional CAGR.

How are smartphone readers changing lateral flow assays?

They transform qualitative strips into quantitative, connected tools, enabling real-time data capture and remote monitoring.

What sustainability initiatives are influencing product design?

Manufacturers are developing biodegradable polylactic-acid substrates and adopting circular-economy practices to reduce plastic waste.

Who are the major players in the market?

Key companies include Abbott, Roche, Thermo Fisher Scientific, Danaher, and QuidelOrtho, all pursuing acquisitions and technology partnerships to strengthen portfolios.

Page last updated on: