Antibody Drug Conjugates Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

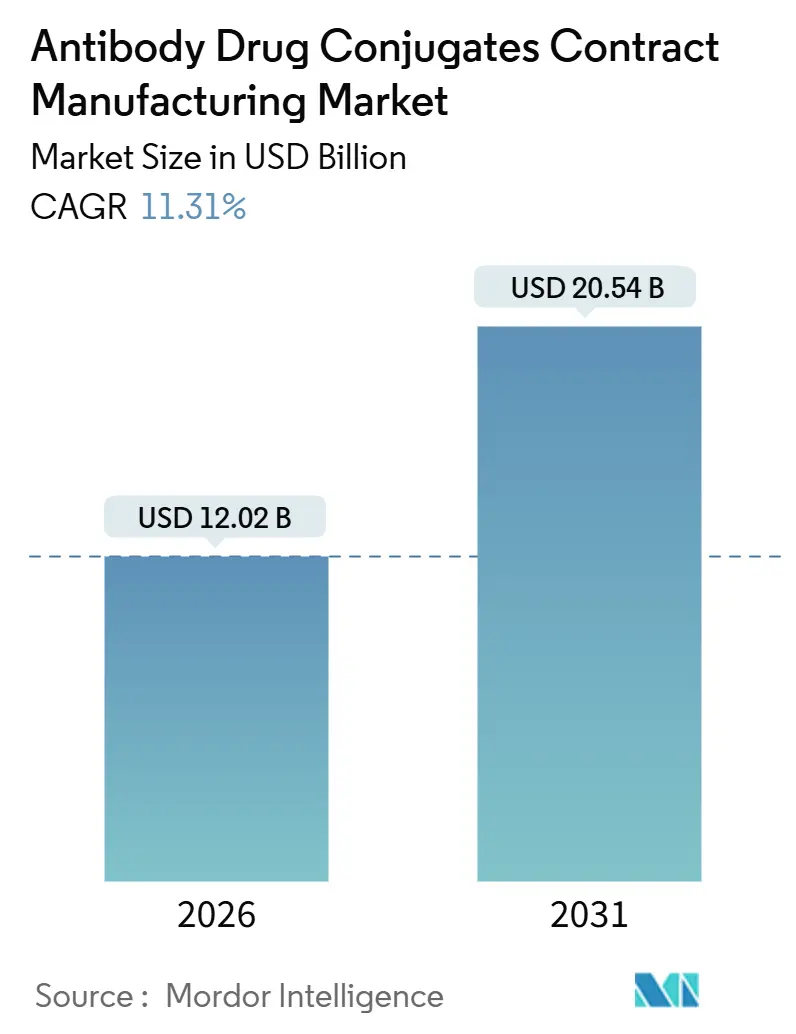

| Market Size (2026) | USD 12.02 Billion |

| Market Size (2031) | USD 20.54 Billion |

| Growth Rate (2026 - 2031) | 11.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibody Drug Conjugates Contract Manufacturing Market Analysis by Mordor Intelligence

The Antibody Drug Conjugates Contract Manufacturing Market size is estimated at USD 12.02 billion in 2026, and is expected to reach USD 20.54 billion by 2031, at a CAGR of 11.31% during the forecast period (2026-2031).

Capacity additions in high-potency suites, the capital burden of in-house builds, and the growing clinical pipeline of next-generation conjugates are steering sponsors toward external partners. Premium pricing for OEB 4-5 containment, regulatory convergence under ICH Q13, and the need to balance speed with quality are reinforcing the value proposition of specialized CDMOs. Consolidation among innovators - illustrated by Pfizer’s Seagen and AbbVie’s ImmunoGen deals - has expanded outsourced volumes even as acquirers rationalize legacy plants. Investments by Lonza, Samsung Biologics, and WuXi Biologics signal confidence that unmet demand for flexible clinical and commercial capacity will persist through the forecast window.

Key Report Takeaways

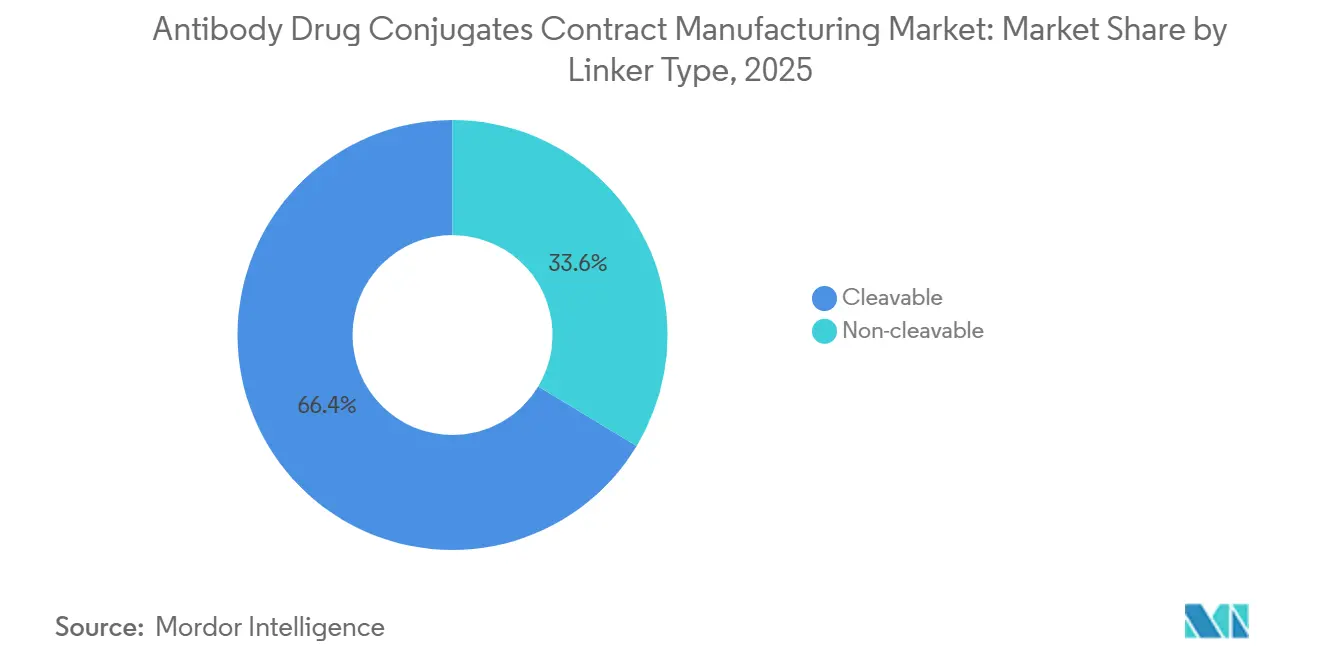

- By linker type, cleavable chemistries held 66.37% of antibody drug conjugates contract manufacturing market share in 2025, while non-cleavable formats are projected to post a 15.25% CAGR to 2031.

- By therapeutic area, solid tumors led with 57.94% revenue share in 2025; autoimmune and infectious-disease programs are forecast to expand at a 14.45% CAGR through 2031.

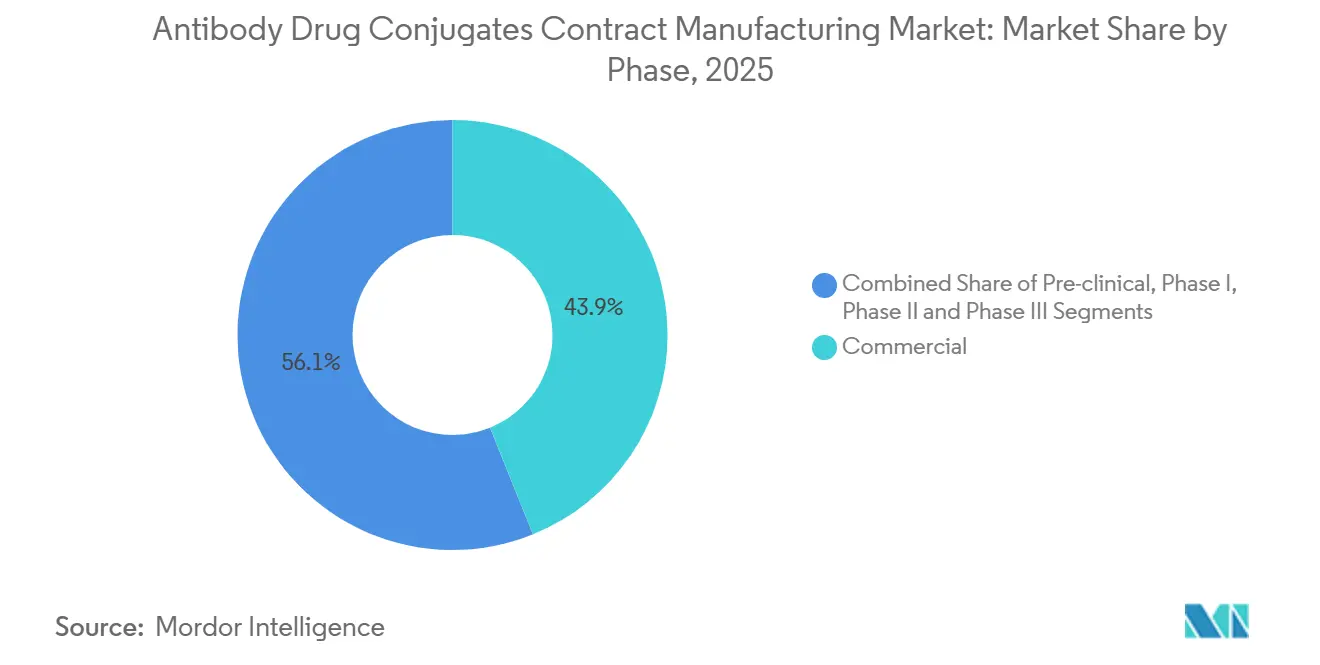

- By phase, commercial manufacturing captured 43.89% of the antibody drug conjugates contract manufacturing market size in 2025 and is advancing at a 13.68% CAGR to 2031.

- By service type, cGMP conjugation and drug-linker production generated 39.73% of revenue in 2025, whereas fill-finish services will accelerate at a 14.83% CAGR through 2031.

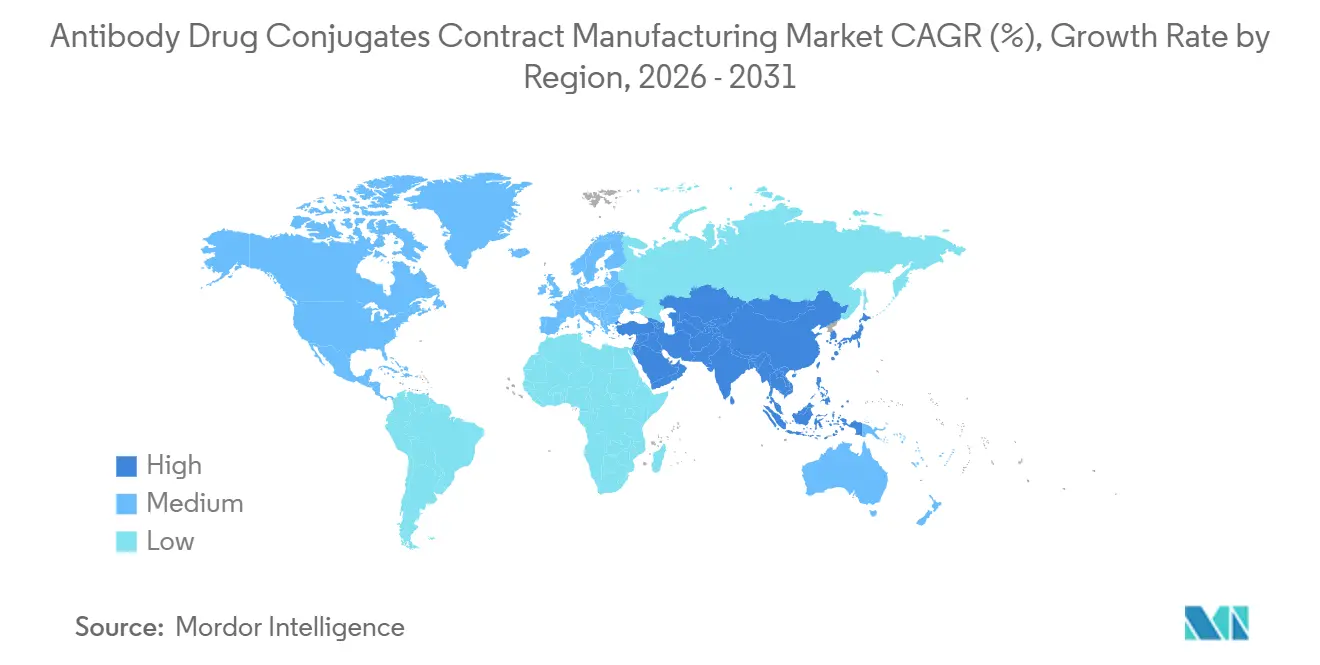

- By geography, North America retained 44.68% share in 2025, but Asia-Pacific is poised to grow at a 14.04% CAGR on the back of large-scale greenfield builds.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging oncology incidence & larger addressable patient pool | 2.3% | Global, with highest concentration in North America & Europe | Medium term (2-4 years) |

| Big-pharma pivot to outsourced biologics manufacturing | 2.8% | Global, led by North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Expansion of ADC clinical pipeline beyond oncology | 1.9% | North America & Europe early adopters, APAC following | Long term (≥ 4 years) |

| Capacity constraints at HPAPI facilities triggering premium pricing | 1.7% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Emergence of site-specific conjugation & continuous flow enabling faster tech-transfer | 1.5% | North America & Europe leaders, technology transfer to APAC | Medium term (2-4 years) |

| Regulatory convergence (ICH Q13, Annex 1 rev.) easing multi-site release testing | 1.1% | Global, harmonizing North America, Europe, APAC regulatory pathways | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Oncology Incidence & Larger Addressable Patient Pool

Global cancer cases reached 20 million in 2024, and WHO projects a rise to 35 million by 2050, sustaining demand for safer targeted therapies.[1]World Health Organization, Cancer Fact Sheet, World Health Organization, who.intEnhertu’s 2024 approval for HER2-low breast cancer validated biomarker-driven expansion and added 1.2 million eligible patients per year.[2]U.S. Food and Drug Administration, “FDA Approves Enhertu for HER2-Low Breast Cancer,” U.S. Food and Drug Administration, fda.gov CDMOs responded by installing multi-product conjugation suites sized for 50-200 kg batches, bridging late-stage and early commercial needs, exemplified by Lonza’s twin 1,200 L reactors at Visp scheduled for 2028 service.

Big-Pharma Pivot to Outsourced Biologics Manufacturing

A BCG review found that 70-80% of developers lacked in-house conjugation capacity in 2024. Pfizer halted a USD 350 million build in Everett and instead signed a USD 1.24 billion contract with Samsung Biologics, prioritizing external scale while focusing internal plants on development. AstraZeneca’s Singapore site, slated for 2029, will cover only early phase work, reserving commercial supply for CDMOs.

Expansion of ADC Clinical Pipeline Beyond Oncology

Developers opened 18 Phase I/II autoimmune trials in 2024, applying cytotoxic payloads to selective B-cell depletion. Gilead’s USD 900 million pact with Sutro pursues folate receptor alpha in ovarian cancer and Crohn’s disease under one IND, demonstrating platform flexibility. CDMOs are expanding analytical offerings to characterize immune-modulating effects beyond standard cytotoxicity panels.

Capacity Constraints at HPAPI Facilities Triggering Premium Pricing

Fewer than 25 CDMOs operate OEB 4-5 suites. Samsung’s USD 1.24 billion award in October 2024 carried a 40% per-kilogram premium over mAb pricing. MilliporeSigma tripled capacity in St. Louis yet sold out 2026-2027 slots within three months. Scarcity is steering sponsors toward continuous processes that cut cycle time by a week, although regulatory uptake is still evolving.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cytotoxic payload supply bottlenecks & hazardous-material logistics | -1.4% | Global, acute in North America & Europe due to regulatory scrutiny | Short term (≤ 2 years) |

| High COGS owing to multi-modal analytical release requirements | -1.2% | Global, with higher impact in North America & Europe | Medium term (2-4 years) |

| Tight environmental rules on solvent & waste incineration for HPAPIs | -0.9% | Europe & North America, emerging in APAC | Medium term (2-4 years) |

| Patent cliffs for first-generation ADCs tempering legacy line utilisation | -0.7% | North America & Europe, limited APAC impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cytotoxic Payload Supply Bottlenecks & Hazardous-Material Logistics

Fewer than 10 suppliers produce GMP auristatins and maytansinoids, with 18-month lead times in 2024. New IATA rules reclassifying certain payloads as Category 1A carcinogens raised air-freight costs by up to 70%. Daiichi Sankyo’s Shanghai payload plant, set for 2030, reflects vertical-integration efforts to mitigate shortages.

High COGS Owing to Multi-Modal Analytical Release Requirements

ADC lots need 15-20 orthogonal assays, pushing analytical costs to USD 50,000-80,000 per batch.[3]Ronald A. Rader, BioProcess International: Analytical Challenges in ADC Lot Release, BioProcess International, bioprocessintl.com Thermo Fisher’s automated platform trims hands-on time by 40% yet still consumes 72 hours of instrument use. Regulators have granted limited waivers under ICH Q6B for continuous processes, but broader acceptance is pending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Linker Type: Non-Cleavable Momentum Outpaces Historical Leaders

Cleavable linkers controlled 66.37% of antibody drug conjugates contract manufacturing market share in 2025, yet non-cleavable systems are forecast to grow 15.25% annually through 2031, outstripping the overall market. The antibody drug conjugates contract manufacturing market size tied to non-cleavable constructs will therefore expand more quickly than cleavable revenue during the period. Developers favor non-cleavable designs for better systemic stability, releasing payload only after lysosomal degradation. Enhertu’s USD 3.1 billion 2024 sales proved that a hybrid approach using membrane-permeable toxins can offset the lower bystander effect seen in first-generation non-cleavables.

CDMOs have invested in flexible conjugation skids that switch between cleavable and non-cleavable chemistries without lengthy changeovers. Lonza’s XpressCys system allows a sponsor to move from early discovery to GMP within a single platform, shortening time to clinic. Cleavable linkers remain essential for hematologic cancers where rapid intracellular release is desirable; however, solid-tumor programs increasingly demand acid-labile and protease-sensitive designs to localize drug activity.

By Therapeutic Area: Autoimmune Upswing Redraws the Map

Solid tumors generated 57.94% of 2025 revenue, but autoimmune and infectious-disease projects are projected to log a 14.45% CAGR to 2031. The antibody drug conjugates contract manufacturing market size tied to autoimmune indications is therefore widening faster than oncology growth alone. Sponsors initiated 18 early-phase autoimmune trials in 2024, betting that selective B-cell ablation can deliver durable remission with intermittent dosing. Solid-tumor demand remains robust, driven by HER2-low, TROP2, and Nectin-4 targets, yet market planners now view non-oncology as the top incremental growth driver.

The autoimmune push requires segregated manufacturing to avoid cross-contamination with high-potency oncology payloads, adding 15-20% to contract pricing. CDMOs willing to dedicate cleanrooms to non-oncology customers stand to command premium margins. Infectious-disease ADCs are nascent, but early venture investment signals future diversification.

By Phase: Commercial Contracts Dominate Revenue Mix

Commercial programs accounted for 43.89% of 2025 revenue and will expand at a 13.68% CAGR, cementing their role as the largest contributor to antibody drug conjugates contract manufacturing market size through 2031. Sponsors increasingly lock in five-year supply deals at fixed prices, as seen in Samsung’s record award, passing inflation risk to manufacturers. Late-stage validation runs attract a 20-30% price uplift, motivating CDMOs to allocate scarce HPAPI capacity to near-commercial assets. Early-phase work is more variable and price-sensitive, with Chinese suppliers under-cutting Western peers by up to 40%.

CDMOs counter this price pressure by bundling development, conjugation, and fill-finish under single contracts, reducing tech-transfer friction. Lonza’s Portsmouth-Visp-Stein network exemplifies the integrated model, guaranteeing timeline certainty to sponsors facing competitive pressure.

By Service Type: Fill-Finish Complexity Spurs Fastest Growth

Fill-finish services will grow 14.83% per year through 2031, eclipsing conjugation and linker manufacture even though the latter held 39.73% of 2025 revenue. Pre-filled syringe and autoinjector formats, enabled by FDA draft guidance on combination products, expand the observable market beyond vials. The antibody drug conjugates contract manufacturing market size associated with fill-finish is therefore climbing sharply as containment and sterility requirements add value.

Conjugation remains the cornerstone service. However, the rise of continuous flow and site-specific technologies is shifting value from sheer capacity toward differentiated process know-how. CDMOs offering both legacy stochastic methods and advanced site-specific platforms can serve a broader client mix.

Geography Analysis

North America held 44.68% of revenue in 2025, powered by a dense innovator base and ongoing brownfield expansions in Missouri, North Carolina, and Massachusetts. The region’s regulatory environment supports first-to-trial ambitions, keeping average project timelines shorter than in Europe. The antibody drug conjugates contract manufacturing market share held by North America will erode slightly as APAC capacity comes online, but absolute revenue will rise given healthy underlying demand.

Asia-Pacific is set to post a 14.04% CAGR, the fastest among regions. Samsung Biologics’ 256 kL Plant 5 and AGC Biologics’ Yokohama facility together add 350 kL of capacity by 2026, equal to 15% of global supply. Lower labor costs and supportive government incentives underpin competitive pricing, drawing late-stage programs from cost-conscious sponsors.

Europe captured 28% of 2025 revenue, led by Germany, Switzerland, and the United Kingdom. The revised Annex 1 rules have improved operating margins by lowering cleanroom capital outlays, yet divergent post-Brexit filing rules add complexity. Smaller European economies lag due to higher labor costs and less generous R&D tax credits.

Competitive Landscape

The top five CDMOs represented a large share of 2025 revenue, indicating moderate concentration. No single player exceeded a 12% share, reflecting the capital barrier but also the broadening of global capacity. Samsung Biologics set a new benchmark with its USD 1.24 billion bundled contract, signaling buyer appetite for one-stop solutions.

Technology leadership is increasingly decisive. Lonza’s XpressCys, Catalent’s SMARTag, and Thermo Fisher’s continuous flow offering provide differentiation beyond scale. Smaller firms form consortia to compete: Cerbios-Pharma partnered with CARBOGEN AMCIS in 2024 to combine conjugation and analytics under a joint bid model. Emerging Chinese and Indian CDMOs undercut on price but must secure multi-region regulatory track records to win commercial phase contracts.

Antibody Drug Conjugates Contract Manufacturing Industry Leaders

Lonza Group

Samsung Biologics

Piramal Pharma Solutions

Catalent Inc.

WuXi Biologics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Harbour BioMed entered a long-term collaboration with Lannacheng to advance next-generation radionuclide drug conjugates.

- June 2025: Simtra BioPharma Solutions and Merck KGaA’s Life Science arm launched a five-year partnership to streamline ADC manufacturing.

- May 2025: Shilpa Biologicals opened a bioconjugation site in Dharwad, India, with capacity for 30 kg of ADC per year.

- April 2025: LOTTE Biologics signed a manufacturing agreement for a clinical-stage ADC candidate with an Asia-based biotech partner.

Global Antibody Drug Conjugates Contract Manufacturing Market Report Scope

Contract Development & Manufacturing Organizations (CDMOs) offer specialized services for the production of complex Antibody Drug Conjugates (ADCs). This intricate process involves a multi-step approach: linking potent cytotoxic drugs to monoclonal antibodies, which act as delivery vehicles, using a specialized linker. The process is further refined through purification, formulation, and fill-finish stages. Each step demands specialized high-containment facilities and expert knowledge, especially during the final conjugation.

The antibody-drug conjugates contract manufacturing market is segmented by Linker Type, therapeutic area, phase, service type, and geography. By Linker Type, the market is segmented into Cleavable and Non-cleavable. By Therapeutic Area into Hematologic Cancers, Solid Tumours, and Other Indications. By Phase, the market is segmented into Pre-clinical, Phase I-III, and Commercial. By Service Type, the market is segmented into Process Development, Analytical/QC, cGMP Conjugation, and Fill-Finish. By Geography, the market is segmented into North America, Europe, APAC, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers values in USD million for the abovementioned segments.

| Cleavable | Acid-labile |

| Protease-cleavable | |

| Disulfide-cleavable | |

| Non-cleavable |

| Hematologic Cancers | Multiple Myeloma |

| Lymphoma | |

| Solid Tumours | Breast |

| Lung | |

| Gastric & GI | |

| Other Indications (Auto-immune, Infectious) |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Commercial |

| Process / Cell-line Development |

| Analytical, Bio-assay & QC |

| cGMP Conjugation & Drug-linker Manufacturing |

| Fill-Finish & Packaging |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Linker Type | Cleavable | Acid-labile |

| Protease-cleavable | ||

| Disulfide-cleavable | ||

| Non-cleavable | ||

| By Therapeutic Area | Hematologic Cancers | Multiple Myeloma |

| Lymphoma | ||

| Solid Tumours | Breast | |

| Lung | ||

| Gastric & GI | ||

| Other Indications (Auto-immune, Infectious) | ||

| By Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Commercial | ||

| By Service Type | Process / Cell-line Development | |

| Analytical, Bio-assay & QC | ||

| cGMP Conjugation & Drug-linker Manufacturing | ||

| Fill-Finish & Packaging | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the antibody drug conjugates contract manufacturing market in 2026 and how fast is it growing?

The market reached USD 12.02 billion in 2026 and is forecast to grow at an 11.31% CAGR to USD 20.54 billion by 2031.

Which linker type is expanding fastest in outsourced ADC production?

Non-cleavable linkers are projected to post a 15.25% CAGR between 2026 and 2031, outpacing cleavable formats.

Why are sponsors outsourcing commercial-scale ADC manufacturing instead of building in-house plants?

Building an OEB 4-5 suite costs USD 80-120 million and takes up to 30 months, whereas CDMOs already operate validated capacity that can be accessed under long-term supply deals.

Which region will add the most new ADC capacity through 2031?

Asia-Pacific leads with USD 3.5 billion in announced greenfield projects, driving a 14.04% regional CAGR.

What is driving premium pricing for ADC contract manufacturing?

Scarce HPAPI containment suites, complex analytical release requirements, and sustained oncology demand allow CDMOs to price ADC contracts 30-40% higher than monoclonal antibody work.

Page last updated on: