In-Vitro Diagnostics (IVD) Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

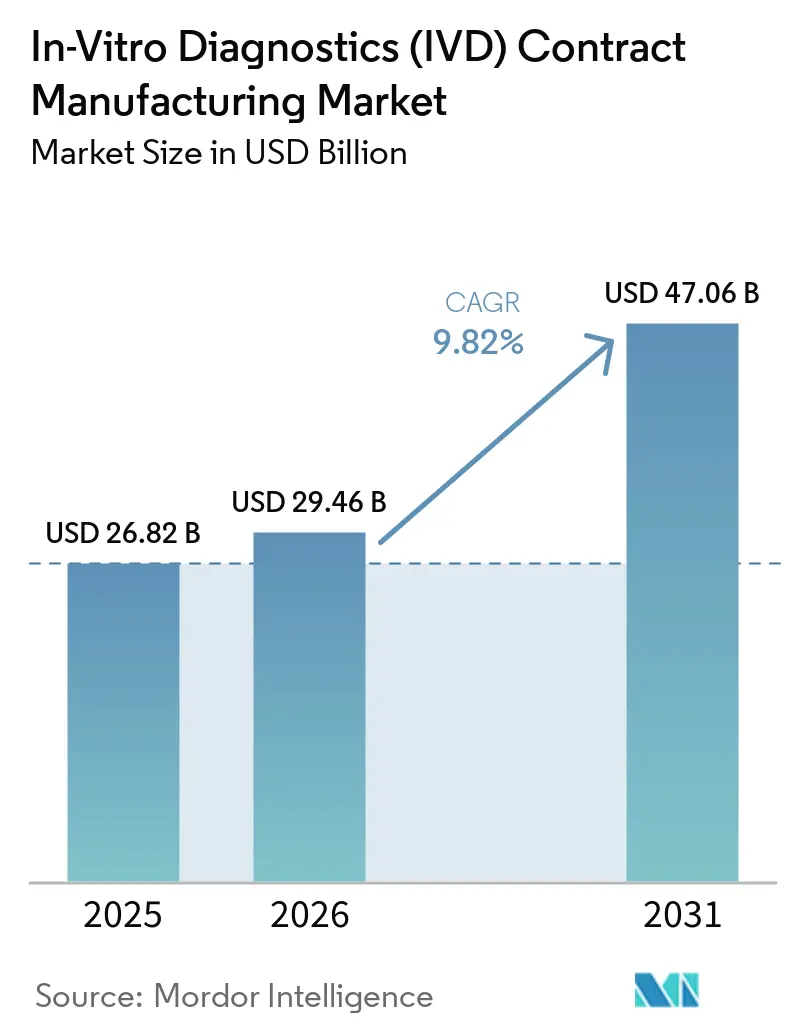

| Market Size (2026) | USD 29.46 Billion |

| Market Size (2031) | USD 47.06 Billion |

| Growth Rate (2026 - 2031) | 9.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In-Vitro Diagnostics (IVD) Contract Manufacturing Market Analysis by Mordor Intelligence

The In-Vitro Diagnostics (IVD) Contract Manufacturing Market size is projected to expand from USD 26.82 billion in 2025 and USD 29.46 billion in 2026 to USD 47.06 billion by 2031, registering a CAGR of 9.82% between 2026 to 2031.

The market is moving toward a more outsourced operating model because cleanroom buildouts, regulatory documentation, and platform validation now demand a larger fixed-cost base than many OEMs can support internally. The shift is also changing the role of contract manufacturers, as they now support assay transfer, process validation, quality oversight, and commercialization readiness instead of only low-value production tasks. Regulatory tightening is reinforcing this model, since OEMs remain accountable for product quality even when operations are outsourced, which makes qualified manufacturing partners more central to launch planning and lifecycle management. Expansion opportunities are strongest where OEMs need flexible capacity for complex formats, faster menu expansion, and localized supply near demand centers. The IVD contract manufacturing market is also seeing a clearer split between high-volume scale providers and specialist platforms that compete on assay chemistry depth, audit readiness, and integrated development-to-manufacturing support.

Key Report Takeaways

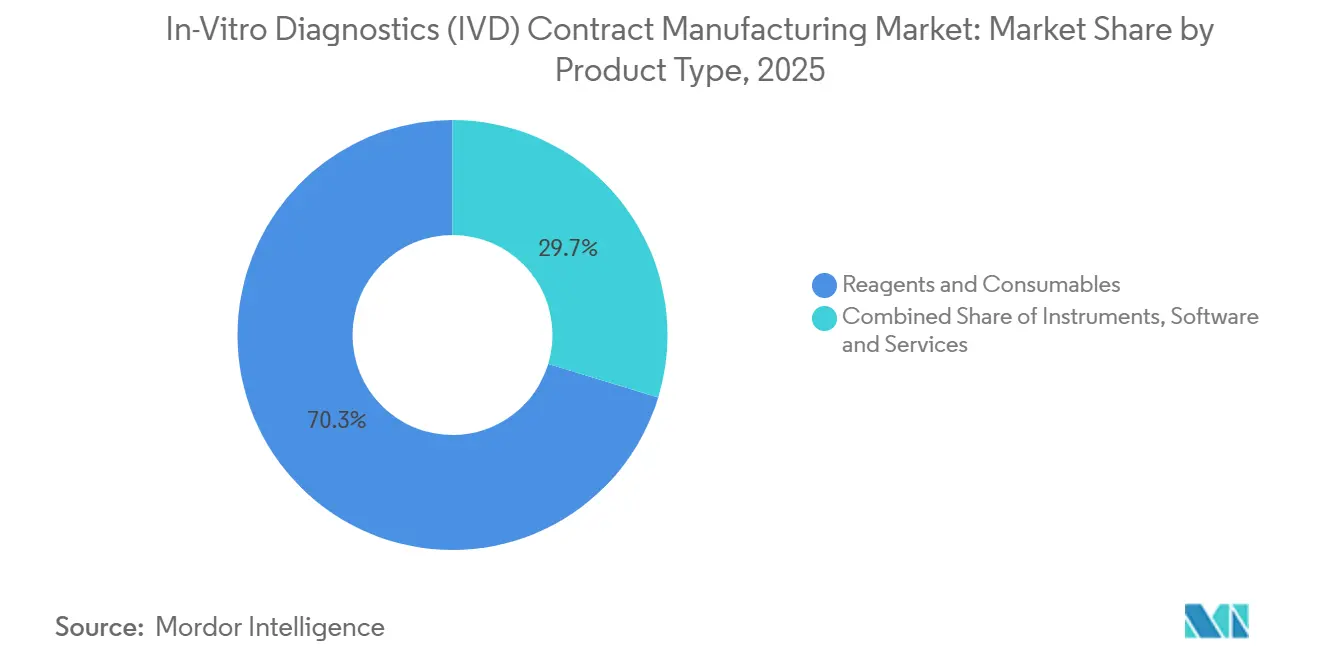

- By product type, Reagents and Consumables led with 70.31% share in 2025, while Instruments are projected to expand at a 12.38% CAGR through 2031.

- By service type, Manufacturing Services held 45.24% share in 2025, while Assay Development Services are projected to have a CAGR at 10.52% through 2031.

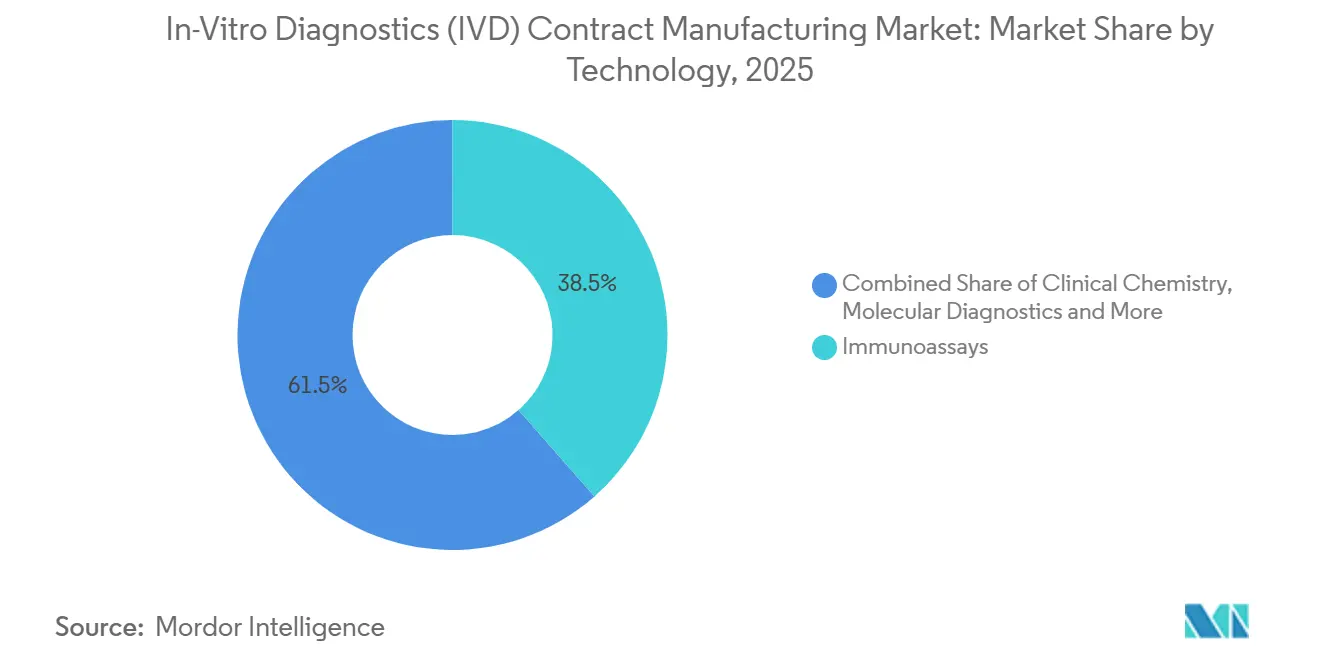

- By technology, Immunoassays accounted for 38.52% share in 2025, while Clinical Chemistry is expected to advance at an 11.25% CAGR through 2031.

- By end user, Medical Device and Biotechnology Companies captured 38.24% share in 2025, while Research and Academic Institutes are forecast to grow at an 11.52% CAGR through 2031.

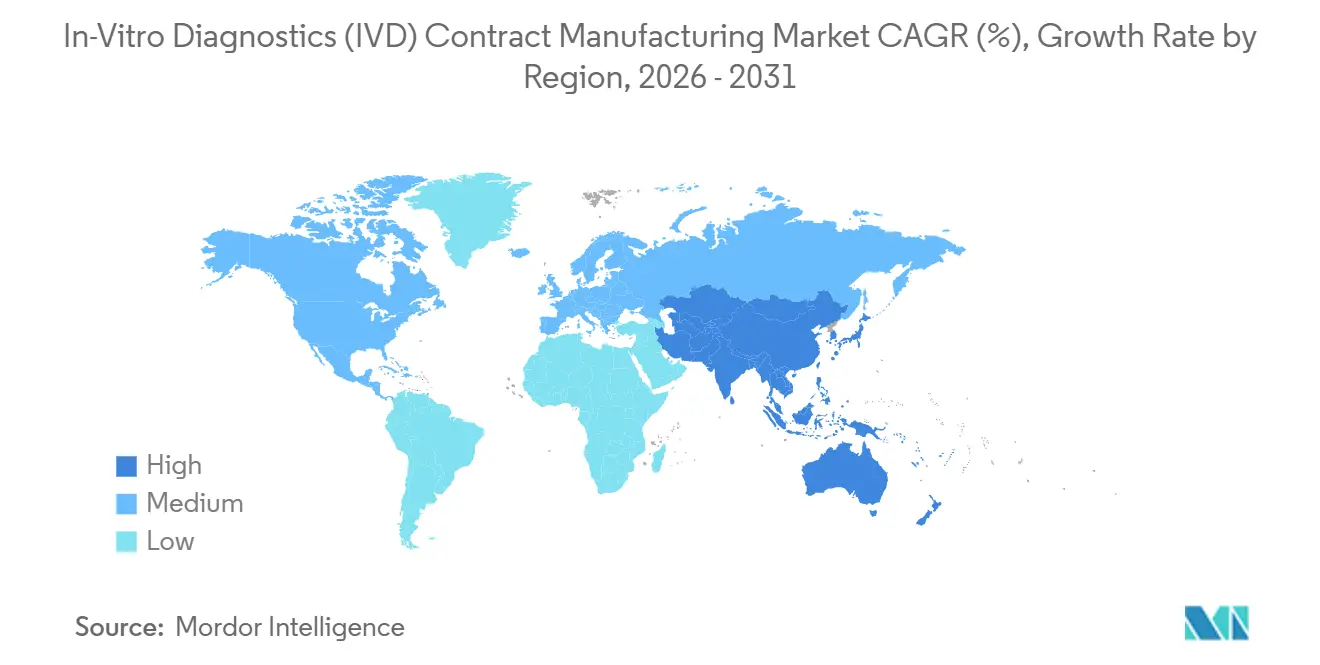

- By geography, North America held 41.22% of the IVD contract manufacturing market share in 2025, while Asia-Pacific is expected to grow at a 12.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global In-Vitro Diagnostics (IVD) Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Outsourcing of IVD Manufacturing by OEMs | +2.5% | Global, highest in North America and Europe | Short term (≤ 2 years) |

| Expanding Molecular Diagnostics and Immunoassay Pipelines | +2.0% | Global, with APAC acceleration | Medium term (2-4 years) |

| Regulatory Burden Favoring Specialist Contract Manufacturers | +1.5% | North America & EU | Short term (≤ 2 years) |

| Scaling Need for High-Mix, Low-Volume Diagnostic Production | +1.2% | Global, with North America & EU core | Medium term (2-4 years) |

| Rapid Localization of Supply Chains Near Demand Centers | +1.0% | North America, APAC core, spill-over to MEA | Medium term (2-4 years) |

| More Frequent Platform Revalidation After Minor Assay Changes | +0.8% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Outsourcing of IVD Manufacturing by OEMs

The IVD contract manufacturing market is benefiting from a clear change in OEM behavior, as outsourcing is now used to transfer operating risk and compliance burden, not only to reduce cost. Diagnostic platforms now combine multiplex chemistries, microfluidic cartridges, and embedded software, which makes it harder to justify separate in-house production lines for every product variation. The IVD contract manufacturing market is therefore expanding because validated external capacity offers a practical alternative to repeated capital spending on specialized facilities. In 2026, the FDA implements the Quality Management System Regulation, which aligns 21 CFR Part 820 with ISO 13485:2016 and reinforces accountability across outsourced operations. That regulatory structure does not reduce sponsor responsibility, but it does make experienced partners more valuable because they already operate within mature quality frameworks. The IVD contract manufacturing market is gaining from this preference for fewer and more deeply integrated manufacturing relationships.

Expanding Molecular Diagnostics and Immunoassay Pipelines

The IVD contract manufacturing market is also being lifted by broader test menu expansion across immunoassay, molecular, and point-of-care formats. Roche Diagnostics disclosed a pipeline of around 130 new tests planned for launch across 2025 to 2028, which shows the scale of commercialization work that large OEMs are trying to manage without building all related manufacturing internally[1]Roche, “Roche Diagnostics Day 2025,” Roche Investor Relations, roche.com. The IVD contract manufacturing market benefits when OEMs choose to direct capital toward pipeline expansion and leave process scale-up, batch transfer, and production readiness to outside partners. This pattern is especially supportive for CMOs that can handle development transfer and manufacturing ramp-up within the same operating model. It shortens the path from assay design to commercial output and reduces friction between R&D teams and production teams. The IVD contract manufacturing market is therefore seeing stronger demand for partners that can absorb both scientific complexity and launch execution.

Regulatory Burden Favoring Specialist Contract Manufacturers

The IVD contract manufacturing market is being shaped by a compliance environment that favors specialist platforms with stronger documentation systems and audit readiness. European and North American OEMs still retain legal responsibility for product quality, testing, and oversight, even when work is outsourced, which raises the cost of using underprepared subcontractors. As a result, the IVD contract manufacturing market is rewarding providers that already operate with established quality contracts, change control discipline, and validated processes. This is widening the gap between certified specialists and smaller manufacturers that cannot support more demanding customer audits. It is also encouraging OEMs to consolidate production with partners that can support multiple steps of the workflow under one quality system. The IVD contract manufacturing market gains from this shift because compliance strength is now a commercial differentiator, not only an operating requirement.

Scaling Need for High-Mix, Low-Volume Diagnostic Production

The IVD contract manufacturing market is responding to a production mix that is becoming broader, smaller in batch size, and more frequent in turnover. Point-of-care, near-patient, and home-use formats have increased the number of product configurations that need to move through qualified production environments without sacrificing documentation rigor. Specialized providers are better positioned for this profile because they are investing in automation that supports fast line changeovers and more efficient validation. ENGEL presented a fully automated diagnostics production solution at K 2025 that reported a 25% efficiency improvement over conventional methods and included a digital validation assistant to support faster qualification timelines[2]ENGEL, “Maximum Productivity With All-Electric Efficiency, ENGEL Presents Fully Automated Production Solution for the Diagnostics Market at K 2025 With Significant Cost Savings,” ENGEL, engelglobal.com. The IVD contract manufacturing market is benefiting because these tools fit the needs of OEM programs that involve many SKUs but limited individual volumes. The result is a stronger role for CMOs that can economically manage complex portfolios without relying on long, single-product production runs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intellectual Property Leakage Risk Across Multi-Site Partners | -1.2% | Global, heightened in APAC multi-site operations | Long term (≥ 4 years) |

| High Validation, Documentation, and Quality System Costs | -1.0% | North America & EU | Medium term (2-4 years) |

| Capacity Bottlenecks for Specialized Reagents and Cartridges | -0.8% | Global | Short term (≤ 2 years) |

| Supplier Qualification Complexity for Critical Inputs | -0.6% | Global, most acute in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intellectual Property Leakage Risk Across Multi-Site Partners

The IVD contract manufacturing market still faces a basic tension between scale expansion and protection of core assay know-how. Assay formulations, antibody clone identities, and reagent compositions remain central competitive assets for OEMs, and wider distribution across multiple partner sites increases exposure. The IVD contract manufacturing market is constrained because smaller innovators are often cautious about how far they extend production across a broader network, especially when workflows cross several jurisdictions. In practice, many programs respond through compartmentalized tech transfer, narrower information access, and site-specific process segregation. Those controls reduce risk, but they also add coordination time and management overhead. The IVD contract manufacturing market therefore expands more slowly in some programs than demand alone would suggest, because IP protection still shapes partner selection and network design.

High Validation, Documentation, and Quality System Costs

The IVD contract manufacturing market is also limited by the cost and time involved in transferring an assay into a new production environment. Each site change or manufacturing transfer can trigger added work across design history files, process validation, supplier qualification, stability documentation, and change control frameworks. The IVD contract manufacturing market feels this burden most strongly among small and mid-sized diagnostics companies, because these fixed compliance costs must be spread over a smaller revenue base. FDA oversight continues to reinforce the need for clearly assigned quality responsibilities across outsourced operations, which keeps documentation expectations high. ISO 13485 alignment and post-market support requirements add more operating layers when a program spans several regions. The IVD contract manufacturing market remains attractive, but the economics work best when outsourcing volume is large enough to absorb these recurring quality system costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reagents remain the revenue base while instrument outsourcing grows faster

Reagents and Consumables held 70.31% share of the IVD contract manufacturing market size in 2025, which kept this category as the core revenue base for outsourced diagnostics production. The IVD contract manufacturing market depends heavily on this recurring demand because reagent replenishment happens continuously across hospital laboratories, point-of-care settings, and research workflows. The reagent-lease model in clinical chemistry and immunoassay systems supports long-tail reagent volumes after instrument placement, which makes demand more predictable for manufacturing partners. Lateral flow strips, ELISA components, and monoclonal antibody-based reagent kits remain central product classes in this part of the IVD contract manufacturing market.

The smallest product category still adds strategic value because software and related services are increasingly bundled with premium manufacturing contracts instead of being sold as stand-alone add-ons. Instruments are the fastest-growing product segment, with a forecast CAGR of 12.38% over 2026-2031, and this is one of the clearest signs that the IVD contract manufacturing market is moving deeper into higher-complexity hardware work. OEMs are handing over PCB assembly, optical subsystems, and full final assembly to partners with electronics manufacturing heritage because in-house hardware lines are harder to justify for anything other than the highest-volume platforms. As next-generation systems combine microfluidics, embedded software, wireless connectivity, and tighter quality assurance needs, the IVD contract manufacturing market is seeing more value move toward CMOs that can manage complete instrument builds instead of only consumables.

By Service Type: Manufacturing services anchor revenue while assay development becomes more central

Manufacturing Services captured 45.24% of the IVD contract manufacturing market size in 2025, which shows that core production work still anchors most commercial relationships. In the IVD contract manufacturing industry, this segment is often the first point of entry because OEMs begin with fill-finish, kitting, lot release, or basic production support before expanding the scope of work. The IVD contract manufacturing market continues to rely on these services across nearly every product and technology category, which makes the segment less exposed to shifts in any single platform type. Packaging, labeling, and quality support are also expanding because OEMs increasingly want one partner to absorb more downstream execution.

Assay Development Services are growing faster, with a 10.52% CAGR projected for 2026-2031, and that growth reflects a more involved relationship between development and manufacturing. The IVD contract manufacturing market is increasingly shaped by early-stage collaboration, where manufacturability is addressed before a product reaches full commercial transfer. That model is attractive because even small assay changes can lead to fresh validation work, which keeps development support relevant well after launch. The IVD contract manufacturing industry is therefore shifting away from simple build-to-print engagement and toward longer partnerships where development, validation, and production are managed as one continuous workflow.

By Technology: Immunoassays lead current demand while clinical chemistry gains momentum in new regions

Immunoassays held 38.52% of the market in 2025, giving the segment the largest technology position in the IVD contract manufacturing market. Its lead comes from broad use across infectious disease testing, oncology biomarkers, cardiac markers, and hormonal panels, all of which support ongoing reagent and consumable throughput. The large installed base of automated immunoassay analyzers in hospital core labs also supports stable replenishment demand, which strengthens the recurring revenue profile of the IVD contract manufacturing market. This technology therefore remains highly attractive for CMOs that can manage assay chemistry, quality documentation, and large-volume reagent production with consistent batch performance.

Clinical Chemistry is the fastest-growing technology segment, with an 11.25% CAGR expected over 2026-2031, even though it is a mature testing category. The IVD contract manufacturing market is seeing this growth because automated clinical chemistry analyzers are expanding into hospital laboratories across emerging regions, where OEMs often prefer outsourced fulfillment over new local plant construction. That creates a favorable demand profile for high-volume reagent manufacturing and steady recurring supply. Molecular diagnostics, hematology, microbiology, and coagulation and hemostasis each bring different outsourcing profiles, but the IVD contract manufacturing market rewards providers that can match their operating model to the technical and margin structure of each modality.

By End User: Medtech and biotech companies remain the main customer base while academic demand rises faster

Medical Device and Biotechnology Companies held 38.24% share in 2025, which made them the largest customer group in the IVD contract manufacturing market. This lead reflects a structural dependence on outsourcing because many mid-size and emerging IVD companies cannot support the full cost of equipment, quality systems, and registrations across several jurisdictions. The IVD contract manufacturing market therefore draws its most stable demand from companies that need commercial-scale output without building a full manufacturing footprint of their own. Pharmaceutical companies add a second layer of demand as companion diagnostic programs become more common in oncology and other targeted therapy areas.

Research and Academic Institutes are the fastest-growing end-user segment, with an 11.52% CAGR projected for 2026-2031, and that growth is tied to translational programs that need small-batch or GMP-adjacent manufacturing support. The IVD contract manufacturing market is gaining from the fact that university-linked biomarker discovery and pilot clinical studies increasingly move through formal external production pathways before reaching regulatory-grade commercialization. Akoya Biosciences selected Argonaut Manufacturing Services in January 2025 as its IVD manufacturing partner for the PhenoImager spatial phenotyping platform, which illustrates how advanced research-origin technologies are moving into structured contract manufacturing relationships. Hospitals and clinical laboratories remain a smaller but steady part of the IVD contract manufacturing market, mostly as buyers of manufactured products rather than direct sponsors of large CMO programs.

Geography Analysis

North America accounted for 41.22% of the IVD contract manufacturing market size in 2025, which kept it as the largest regional base for outsourced diagnostics production. The region benefits from a dense concentration of OEM headquarters, a large network of FDA-registered manufacturing sites, and stronger demand for audit-ready partners. The IVD contract manufacturing market in North America is also being lifted by the 2026 QMSR implementation, because OEMs are already favoring partners that can show stronger alignment with mature quality systems before enforcement hardens. Roche announced a USD 550 million investment in its Indianapolis diagnostics manufacturing hub in May 2025, aimed at expanding domestic diagnostics capacity and supporting supply security. That kind of investment shows why the IVD contract manufacturing market in the region remains closely tied to reshoring, regulatory readiness, and the value of domestic manufacturing depth.

Europe held the second-largest regional position in 2025, and the IVD contract manufacturing market there continues to be shaped by the IVDR transition and the need for certified capacity. Germany remained the largest national IVD base in Europe. bioMérieux broke ground on 29 May 2026 for a new EUR 250 million (USD 296.25 million) PCR test production facility in La Balme-les-Grottes, France, which is intended to strengthen European supply security for BIOFIRE syndromic panels. The IVD contract manufacturing market in Europe is therefore moving toward fewer, larger, and more compliance-ready production platforms.

Asia-Pacific is the fastest-growing region in the IVD contract manufacturing market, with a forecast CAGR of 12.65% over 2026-2031. Growth is supported by expanding hospital infrastructure, rising chronic disease burden, and policy support for local diagnostics manufacturing in countries such as China, India, and South Korea. The IVD contract manufacturing market in Asia-Pacific also benefits from the fact that OEMs want production closer to end demand in order to reduce logistics exposure and respond faster to regional procurement conditions. Middle East and Africa and South America remain smaller in absolute terms, but the IVD contract manufacturing market is still gaining ground there as regional demand builds around local supply security and targeted specialist production.

Competitive Landscape

The IVD contract manufacturing market remains moderately fragmented, with a visible split between global EMS groups and specialist IVD CDMOs. Large EMS providers compete on scale, cleanroom depth, logistics reach, and experience with complex hardware assembly. Specialist CDMOs compete on assay transfer, antibody production, reagent chemistry, and regulatory documentation. The IVD contract manufacturing market has become more contested because OEMs now want both technical specialization and geographic flexibility from the same partner network. That has pushed competition toward broader service scope, stronger quality systems, and better support across development, manufacturing, and post-market activity.

The IVD contract manufacturing market is also being reshaped by strategic moves that deepen local production and tighten service integration. Roche expanded its Indianapolis diagnostics hub with a USD 550 million investment in 2025, which reinforced domestic manufacturing capacity in the United States. bioMérieux started a new PCR production facility in France in May 2026, which shows how localization and supply security are now part of competitive positioning. Thermo Fisher Scientific signed an agreement in April 2026 to sell its microbiology business to Astorg, which signals continued portfolio reshaping around higher-priority platforms and service lines.

The IVD contract manufacturing market still has open space where reagent capability, instrument assembly, and regulatory support must come together in one operating model. That gap is most visible in companion diagnostics, spatial biology, and advanced molecular systems, where customers need both chemistry depth and hardware execution. BD showed the value of dual-market regulatory capability in November 2025 when it received both FDA 510(k) clearance and CE-IVDR certification for high-throughput enteric bacterial panels on the BD COR System[3]Becton, Dickinson and Company, “BD Receives FDA 510(k) Clearance and CE-IVDR Certification for High-Throughput Enteric Bacterial Panels on BD COR System,” BD Newsroom, bd.com. The IVD contract manufacturing market is likely to keep favoring providers that can combine compliant scale with enough technical depth to support both consumables and instrument-heavy platforms.

In-Vitro Diagnostics (IVD) Contract Manufacturing Industry Leaders

Thermo Fisher Scientific Inc.

Celestica Inc.

Jabil Inc.

Sanmina Corporation

Invetech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: bioMérieux broke ground on a new EUR 250 million (USD 296.25 million) PCR test production facility in La Balme-les-Grottes, Isère, France, targeting BIOFIRE syndromic test supply for the European market and expected to create approximately 400 jobs upon reaching operations in 2030. This investment reflects European diagnostic supply chain localisation strategy following post-pandemic dependencies.

- April 2026: Thermo Fisher Scientific signed an agreement to sell its microbiology business to Astorg private equity, the business generated USD 645 million in revenue in 2025 and forms part of the Specialty Diagnostics segment. The transaction is expected to close in the second half of 2026, signalling portfolio rationalisation toward core CDMO and life science tools operations.

Global In-Vitro Diagnostics (IVD) Contract Manufacturing Market Report Scope

As per the scope of the report, IVD Contract Manufacturing refers to the process where a company (the client or sponsor) partners with a third-party manufacturer to produce In Vitro Diagnostic (IVD) devices or test kits. In this arrangement, the manufacturing company handles the production, assembly, and sometimes packaging of the IVD products according to the client's specifications, quality standards, and regulatory requirements.

The segmentation for the in-vitro diagnostics (IVD) contract manufacturing market is categorized by product type, service type, technology, end user, and geography. By product type, the market includes instruments, reagents and consumables, and software and services. By service type, it is segmented into manufacturing services, assay development services, and packaging, labeling, and quality and regulatory support services. By technology, the market is divided into immunoassays, molecular diagnostics, clinical chemistry, hematology, microbiology, and coagulation and hemostasis. By end user, the segmentation includes medical device and biotechnology companies, pharmaceutical companies, hospitals and clinical laboratories, and research and academic institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Instruments |

| Reagents and Consumables |

| Software and Services |

| Manufacturing Services |

| Assay Development Services |

| Packaging, Labeling, and Quality and Regulatory Support Services |

| Immunoassays |

| Molecular Diagnostics |

| Clinical Chemistry |

| Hematology |

| Microbiology |

| Coagulation and Hemostasis |

| Medical Device and Biotechnology Companies |

| Pharmaceutical Companies |

| Hospitals and Clinical Laboratories |

| Research and Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Instruments | |

| Reagents and Consumables | ||

| Software and Services | ||

| By Service Type | Manufacturing Services | |

| Assay Development Services | ||

| Packaging, Labeling, and Quality and Regulatory Support Services | ||

| By Technology | Immunoassays | |

| Molecular Diagnostics | ||

| Clinical Chemistry | ||

| Hematology | ||

| Microbiology | ||

| Coagulation and Hemostasis | ||

| By End User | Medical Device and Biotechnology Companies | |

| Pharmaceutical Companies | ||

| Hospitals and Clinical Laboratories | ||

| Research and Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size of the IVD contract manufacturing market in 2026?

The IVD contract manufacturing market is valued at USD 29.46 billion in 2026 and is forecast to reach USD 47.06 billion by 2031 at a CAGR of 9.82%.

Which product category leads outsourced IVD manufacturing demand?

Reagents and Consumables lead the IVD contract manufacturing market with a 70.31% share in 2025 because recurring replenishment demand remains high across laboratories, point-of-care settings, and research use.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a forecast CAGR of 12.65% over 2026-2031, supported by hospital expansion and domestic manufacturing policies.

Why are OEMs increasing their use of contract manufacturers for IVD products?

OEMs are outsourcing more because platform complexity, cleanroom investment, and regulatory documentation costs have made full in-house manufacturing less economical for many companies.

Which service area is expanding the fastest in this space?

Assay Development Services are projected to grow at a 10.52% CAGR through 2031, reflecting stronger demand for early-stage manufacturing support and repeat validation work after assay changes.

Which end-user group is expected to grow the fastest?

Research and Academic Institutes are forecast to grow at an 11.52% CAGR through 2031 as translational research and biomarker programs increasingly require pilot-scale or GMP-adjacent manufacturing support.

Page last updated on: