Medical Device Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

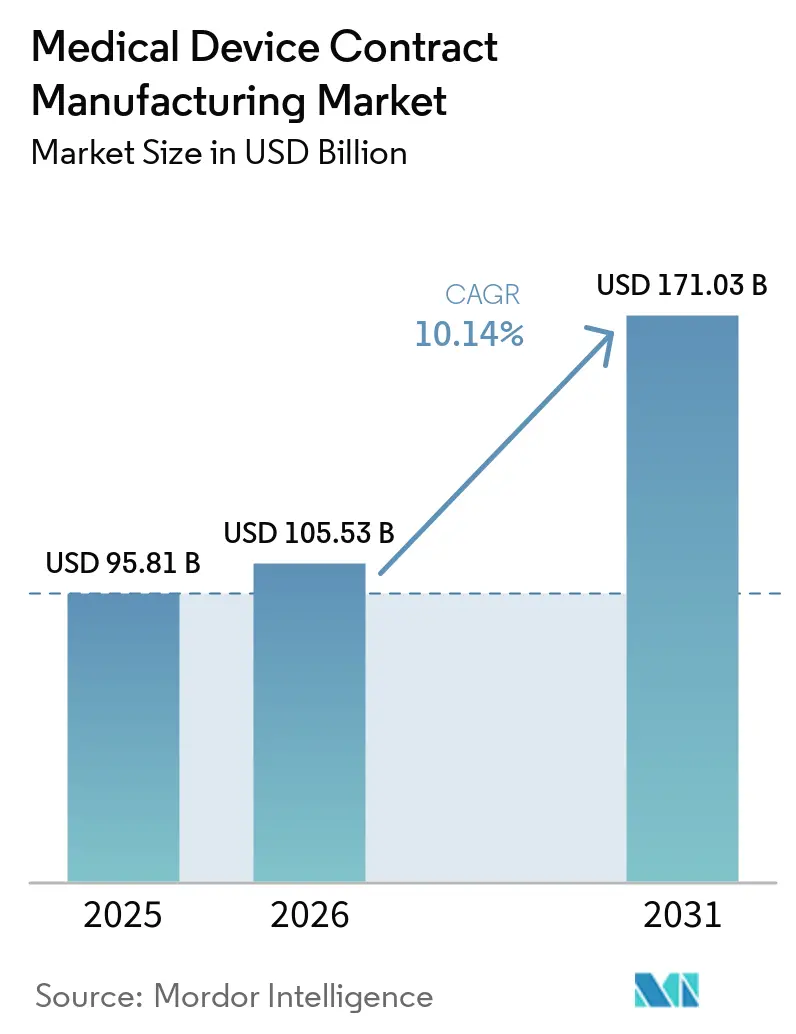

| Market Size (2026) | USD 105.53 Billion |

| Market Size (2031) | USD 171.03 Billion |

| Growth Rate (2026 - 2031) | 10.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device Contract Manufacturing Market Analysis by Mordor Intelligence

The medical device contract manufacturing market size was valued at USD 95.81 billion in 2025 and estimated to grow from USD 105.53 billion in 2026 to reach USD 171.03 billion by 2031, at a CAGR of 10.14% during the forecast period (2026-2031). Rapid expansion is underpinned by OEMs accelerating outsourcing to manage cost pressure, navigating stringent post-COVID regulations, and adopting advanced digital production. High‐value therapies that integrate electronics and software, such as connected drug-delivery and Class III life-support devices, continue to migrate toward specialist CMOs. Investors are backing vertical integration plays, especially in precision engineering, sterilization, and packaging, to capture more of the value chain. Meanwhile, near-shoring strategies, expansion of smart-factory investments, and sustained demand from an aging population collectively create sizable capacity requirements in North America, Europe, and advanced Asia Pacific hubs.

Key Report Takeaways

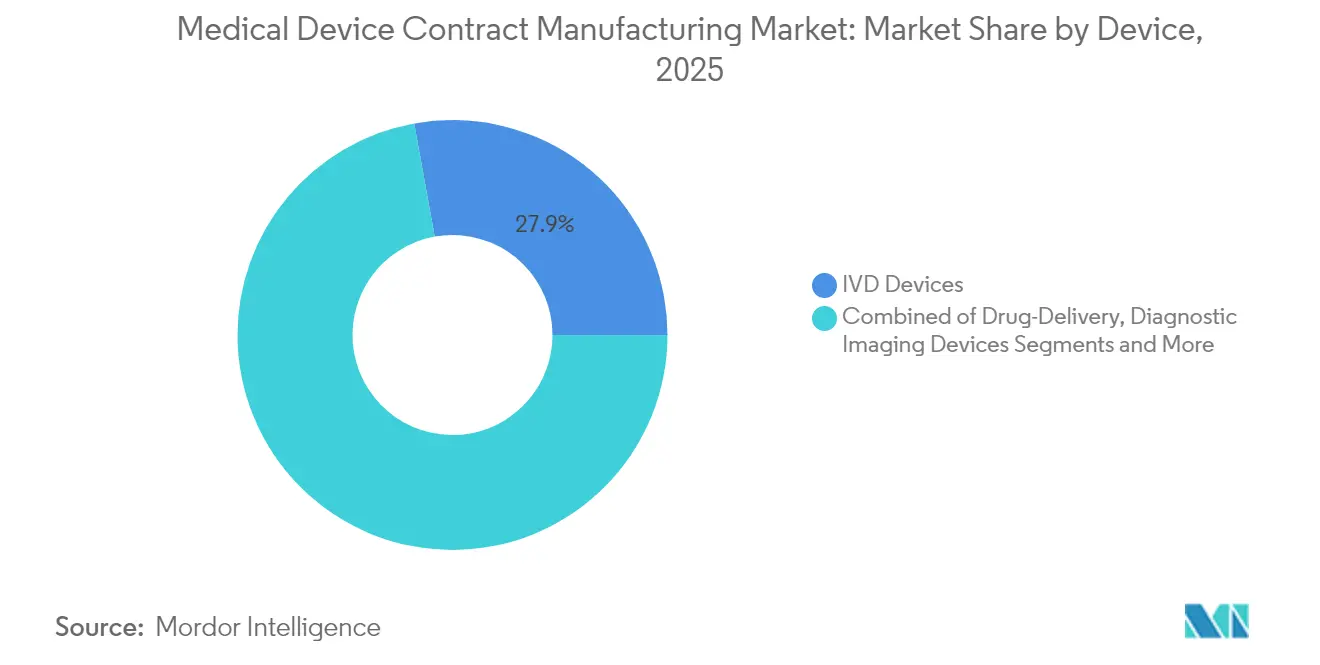

- By device type, in-vitro diagnostic devices led with 27.85% revenue share in 2025; drug-delivery devices are forecast to expand at a 11.78% CAGR through 2031.

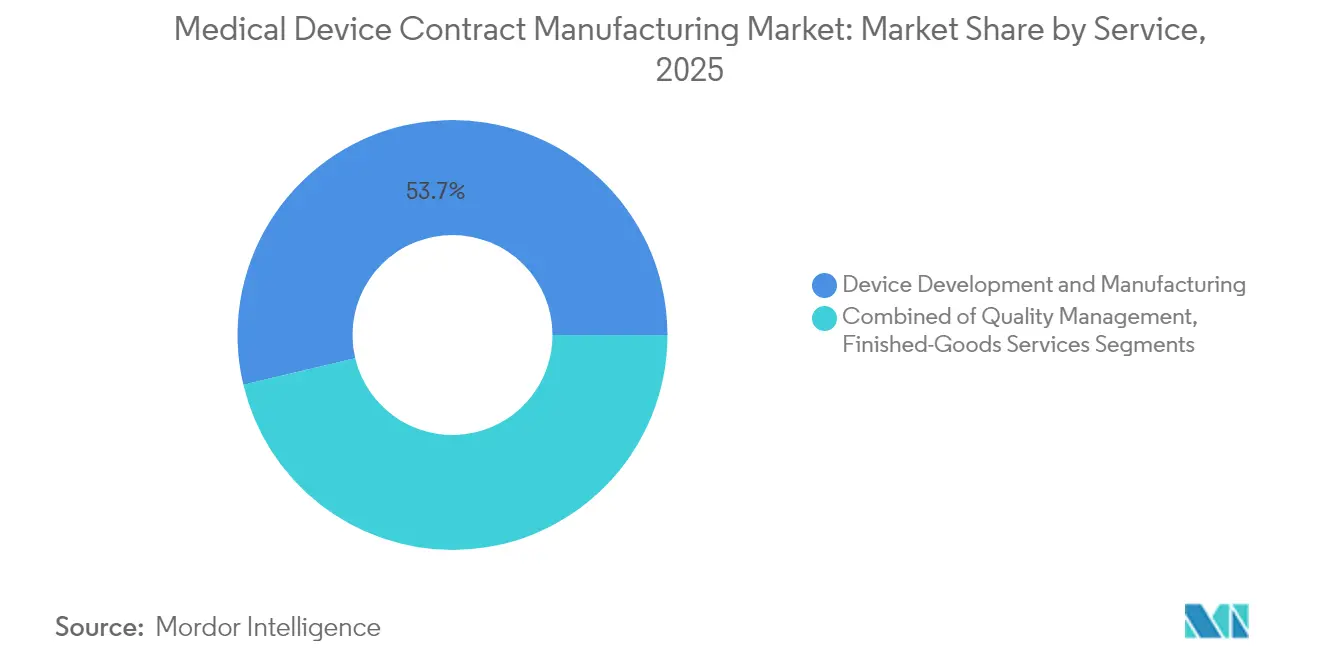

- By service type, device development & manufacturing services held 53.72% of the medical device contract manufacturing market share in 2025, while quality management services are advancing at a 13.88% CAGR to 2031.

- By geography, North America commanded 38.62% share of the medical device contract manufacturing market size in 2025, and Asia–Pacific is projected to grow at a 10.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Device Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-Pressure‐Driven OEM Outsourcing | +3.20% | Global, with highest intensity in North America & Europe | Medium term (2-4 years) |

| Post-COVID Surge in IVD & PoC Diagnostics | +2.10% | Global, with concentration in North America, Europe & urban APAC | Short term (≤ 2 years) |

| Complex Class III Device Pipeline Expansion | +1.80% | North America, Europe, Japan | Long term (≥ 4 years) |

| Aging Population Amplifying Device Volumes | +1.50% | Japan, Europe, North America, China | Long term (≥ 4 years) |

| Near-Shoring to Offset Tariff & Geopolitical Risks | +1.10% | North America (US-Mexico corridor), Europe | Medium term (2-4 years) |

| Smart-Factory/Industry 4.0 Adoption by CMOs | +0.90% | North America, Europe, Advanced APAC economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-Pressure-Driven OEM Outsourcing

OEMs cite cost containment, faster commercialization, and access to specialist skills as prime reasons to deepen strategic outsourcing. Forty-two percent of senior executives name cost optimization as the leading trigger for shifting volume to CMOs. Multi-year partnerships increasingly bundle design, regulatory, and post-market services, enabling OEMs to limit capital spend while CMOs secure predictable revenue streams. Scale players continue to invest in cleanrooms, additive manufacturing, and high-volume automation to absorb larger, more complex programs. As a result, the medical device contract manufacturing market is steadily moving from transactional supply toward integrated lifecycle management.

Post-COVID Surge in IVD & PoC Diagnostics

Sustained adoption of point-of-care testing keeps IVD volumes elevated well beyond the pandemic peak. Diagnostics developers now embed connectivity and AI analytics that demand electronics miniaturization and secure firmware upgrades, pushing OEMs toward CMOs with strong electromechanical and software validation skills. The diagnostic device outsourcing sub-segment is expanding to a 9.8% CAGR, strengthening the medical device contract manufacturing market, with quality-by-design and rapid prototyping reducing development cycles. Harmonized data standards introduced in 2025 further compress review timelines, favoring suppliers that pair robust QMS with multi-regional regulatory insight.[1]What’s Trending in Medical Devices and Diagnostics for 2025, Medical Device Innovation Consortium, clinicalleader.com

Complex Class III Device Pipeline Expansion

Breakthroughs in neuromodulation, structural heart, and life-sustaining implants add intricate requirements around biocompatibility, firmware safety, and mixed-material assemblies. The FDA’s Early Feasibility Study pathway accelerates bench-to-bedside cycles but compels tight supplier documentation to secure trial exemptions. CMOs answer with dedicated Class III production cells, advanced laser micromachining, and AI-assisted inspection, underpinning higher margins in this technically demanding tier of the medical device contract manufacturing market.

Aging Population Amplifying Device Volumes

Rising life expectancy in OECD economies multiplies chronic disease prevalence, especially cardiovascular, orthopedic, and diabetes indications. High procedure volumes translate into repeat orders for disposables and implantable, stabilizing baseline capacity utilization across the medical device contract manufacturing market. CMOs automate high-mix, low-volume lines with collaborative robots and machine vision to cope with labor shortfalls while preserving traceability. Expansion of outpatient and homecare settings also shifts device design toward user-friendly formats that require cross-disciplinary engineering expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM Consolidation Squeezing CMO Margins | -0.90% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Divergent Global Regulatory Pathways | -0.70% | Global, with particular complexity between US, EU, and China | Medium term (2-4 years) |

| Shortage Of Skilled Medtech Manufacturing Talent | -0.60% | Global, with acute impact in North America & Europe | Long term (≥ 4 years) |

| Specialty Resin & Chip Supply Volatility | -0.50% | Global, with highest vulnerability in APAC supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OEM Consolidation Squeezing CMO Margins

Large device multinationals, fortified by M&A, wield greater purchasing leverage and regularly optimize supplier rosters. The resulting volume concentration triggers aggressive price negotiations, pressing CMOs to defend profitability via operational excellence and service differentiation. Some suppliers respond by merging 84 deals closed between 2014 and mid-2020, creating regional champions with broader portfolios that appeal to consolidated buyers. Yet the top 10 CMOs still account for only 24.9% of the medical device contract manufacturing market, leaving room for niche specialists to flourish.

Divergent Global Regulatory Pathways

While global demand rises, disparate cybersecurity, UDI, and post-market surveillance rules across the US, EU, and China create costly compliance complexity.[2]Alexander Brown et al., “Investigating State Support for China’s Medical Technology Companies,” MERICS, merics.orgNew FDA mandates requiring cybersecurity plans for every novel device shipped after 2025 obliges CMOs to embed penetration testing and secure update mechanisms across production. Firms with harmonized, multi-jurisdictional QMS can shorten OEM launch timelines, but continuous investment in documentation, software bill of materials tracking, and audit readiness increases fixed overhead across the medical device contract manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device: IVD Leadership and Drug-Delivery Momentum

IVD devices generate 27.85% of 2025 revenue, cementing their status as the largest slice of the medical device contract manufacturing market. Contract manufacturers support sustained demand for molecular diagnostics, immunoassays, and portable analyzers that migrated from centralized labs to point-of-care settings. High-throughput reagent filling, precision plastic molding, and cartridge assembly lines operate under fully automated quality gates to meet tight turnaround targets.

Drug-delivery platforms, while smaller, post the fastest expansion at 11.78% CAGR through 2031. On-body pumps, wearable injectors, and connected inhalers that incorporate sensors, wireless modules, and user-feedback loops require multidisciplinary integration. CMOs respond by building sterile fill-finish suites, silicone-free syringe coating, and scalable electronics assembly under medical-grade standards. For biologics exceeding 2 mL, next-generation gas-powered autoinjectors open new modal possibilities. Reusable casings and modular drug cassettes lower waste, reinforcing sustainability mandates and underpinning volume growth across the medical device contract manufacturing industry.

By Service: Manufacturing Dominance with Quality Surge

Device development & manufacturing services command 53.72% share in 2025, underscoring the pivotal role of full-stack production partners within the medical device contract manufacturing market. CMOs invest in digital twins, design-for-assembly analytics, and hybrid prototyping to migrate concepts to scale within compressed timelines. Multi-disciplinary engineering teams co-locate with regulatory affairs units to streamline design history and risk files, anchoring the medical device contract manufacturing market around integrated value delivery.

Quality management services post a 13.88% CAGR as regulatory scrutiny intensifies cybersecurity, sterilization, and software validation requirements. Gap assessments, remediation roadmaps, and supplier qualification audits have become revenue streams in their own right. CMOs leverage cloud-based eQMS platforms with AI-enabled document parsing to maintain audit readiness. Assembly & finished-goods services round out offerings, where turnkey integration reduces OEM hand-offs; embedded serialization and advanced packaging protect product integrity across global cold chains, further enhancing the medical device contract manufacturing market size for full-service providers.

Geography Analysis

North America retains leadership with a 38.62% share in 2025, supported by robust R&D funding, deep clinical networks, and early adoption of digital surgery and connected therapeutics. CMOs in the United States scale Industry 4.0 pilots into fully networked plants, deploying AI predictive maintenance and paperless batch records to mitigate a projected 3.8-million-person labor gap by 2033. Mexico strengthens the regional supply chain as a near-shore base, leveraging USMCA tariff clarity and same-day trucking to major distribution hubs.

Asia Pacific records the fastest trajectory, rising at a 10.32% CAGR as Chinese and Indian governments court high-tech manufacturing. Chinese MedTech firms enjoy state support worth up to EUR 3.8 billion (USD 4.3 billion), enabling local CMOs to compete on sophisticated catheter, endoscope, and implant assemblies. Japanese suppliers retain specialist niches in imaging optics and miniaturized motors, while South Korean players focus on MEMS sensors and battery management for wearable therapeutics. A burgeoning talent pool and cost advantage entice Western OEMs to co-locate innovation centers, expanding the medical device contract manufacturing market across the region.

Europe continues to anchor precision engineering, with Germany, Switzerland, and Ireland excelling in micro-machining, combination-product sterilization, and high-grade polymer molding. Stringent MDR rules lengthen certification timelines, prompting many US startups to initially launch stateside before back-transferring to European plants once design is frozen. Eastern European economies gain traction for mid-volume disposables, offering competitive labor yet EU-aligned quality. The Middle East and Africa gradually scale single-use device production to serve expanding local healthcare demand, while Brazil and Costa Rica drive Latin American growth. Multi-regional diversification remains a core resilience strategy after pandemic-era supply shocks highlighted single-site vulnerabilities.

Competitive Landscape

The top ten CMOs collectively capture significant market share in the medical device contract manufacturing market, underscoring moderate fragmentation balanced by rising consolidation waves. Private-equity sponsors funnel fresh capital into tuck-in acquisitions targeting machining, sterilization, and advanced packaging shops. These roll-ups create platform companies capable of spanning concept design, rapid prototyping, regulatory submissions, and volume production in a single commercial agreement.

Technology leadership is now the primary differentiator. Jabil’s USD 126 million strategic investment in Bright Machines brings modular micro-factories and computer-vision quality inspection onto the factory floor, accelerating zero-defect initiatives. Integer Holdings meanwhile posted Q1 2025 revenue of USD 437.4 million up to 7.3% year-on-year driven by cardiovascular catheter projects and battery packs for neuromodulation implants. Other notable moves include Flex tailoring additive manufacturing hubs for orthopedic implants and Celestica expanding design centers focused on ophthalmic instrumentation.

White-space opportunities revolve around digital therapeutics, bio-resorbable materials, and AI-augmented diagnostics. CMOs sharpening data analytics, cybersecurity, and cloud-integration services become strategic co-developers rather than commodity suppliers, reinforcing customer stickiness and high switching costs. At the same time, ESG commitments push greener chemistries, energy-efficient cleanrooms, and circular-economy packaging requirements that favor suppliers nimble enough to redesign processes without disrupting validated lines. The resulting competitive dynamic ensures continuous capital investment and knowledge transfer, propelling long-term maturation of the medical device contract manufacturing industry.

Medical Device Contract Manufacturing Industry Leaders

Jabil Inc.

Gerresheimer AG

Flex Ltd.

Integer Holdings Corp.

TE Connectivity Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ADLINK Technology’s San Jose Manufacturing Center gained FDA registration, allowing accelerated production of regulated devices

- February 2025: Jabil acquired Pharmaceutics International Inc., broadening its integrated healthcare capabilities.

- January 2025: NovaLink highlighted expanding Mexican near-shoring programs driven by logistics savings and USMCA compliance.

- January 2024: Integer Holdings bought Pulse Technologies for USD 140 million, enhancing precision machining and coating offerings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical-device contract manufacturing market as the value generated when original equipment manufacturers outsource any portion of Class I, II, or III device design transfer, component machining, electronics assembly, sterilization, packaging, and finished-goods supply to specialist contract manufacturers that operate under ISO 13485 and regional agency guidelines.

Scope exclusion: disposable non-medical consumer wearables and in-house OEM captive plants are not counted.

Segmentation Overview

- By Device

- In-vitro Diagnostic (IVD) Devices

- Diagnostic Imaging Devices

- Cardiovascular Devices

- Drug-Delivery Devices

- Syringes

- Pen Injectors

- Others

- Endoscopy Devices

- Ophthalmology Devices

- Orthopedic Devices

- Dental Devices

- Other Devices

- By Service

- Device Development & Manufacturing Services

- Device Engineering

- Process Development

- Device Manufacturing

- Quality Management Services

- Inspection & Testing

- Packaging Validation

- Assembly & Finished-Goods Services

- Device Development & Manufacturing Services

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed contract-manufacturing executives across North America, Europe, and Asia Pacific, along with regulatory consultants and procurement heads at mid-sized OEMs. These discussions clarified current outsourced share by device class, average selling price (ASP) swing factors, and regional capacity additions that were not visible in public filings.

Desk Research

We began by gathering publicly available data from tier-one sources such as the US FDA 510(k) database, Eurostat Prodcom, UN Comtrade shipment codes 9018/9019, and industry association white papers from the Medical Device Manufacturers Association. Company 10-Ks, investor decks, and select paid datasets like D&B Hoovers and Volza gave us production footprints and shipment volumes that anchor baseline demand. Academic journals provided cost-of-quality benchmarks that helped us fine-tune margin assumptions. This list is illustrative; many other references supported fact-checks and variable calibration.

Market-Sizing & Forecasting

Our top-down model starts with 2024 global medical-device revenues, applies an outsourced-manufacture penetration curve by class, and then adjusts for average contract ASP differences across geographies. Results are cross-checked with selective bottom-up roll-ups of leading CMO revenues and sampled ASP × volume calculations. Key variables include FDA and CE mark approvals issued, component outsourcing intensity, tariff-adjusted trade in electromedical equipment, capital-spend outlook of major CMOs, and shift from metal to polymer additive manufacturing. A multivariate regression on these drivers underpins our 2025-2030 forecast, with scenario analysis stress-testing currency and regulatory shocks. Gaps in bottom-up coverage are bridged through ratio imputation using closest peer disclosures.

Data Validation & Update Cycle

Every iteration passes anomaly checks, peer review, and senior sign-off. We refresh models annually and then issue interim updates when material events, such as MDR enforcement milestones or large CMO capacity expansions, alter the baseline.

Why Mordor's Medical Device Contract Manufacturing Baseline Earns Dependability

Published estimates often differ because firms select varying service mixes, device classes, and update cadences.

Key gap drivers include divergent inclusion of packaging-only contracts, contrast between our blended ASP path and others' static pricing, and the fact that some publishers lock forecasts before new EU MDR compliance costs are clear.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 95.81 B | Mordor Intelligence | - |

| USD 83.77 B | Global Consultancy A | narrower service lens and biennial refresh |

| USD 84.86 B | Industry Journal B | relies on sales proxies with limited primary validation |

Taken together, the comparison shows that Mordor's continuously reviewed scope, dual-path modeling, and deep expert outreach deliver a balanced and transparent baseline clients can rely on for strategic decisions.

Key Questions Answered in the Report

What is the current size of the medical device contract manufacturing market?

The medical device contract manufacturing market size is USD 105.53 billion in 2026.

How fast is the market expected to grow?

Industry revenue is forecast to rise at a 10.14% CAGR, reaching USD 171.03 billion by 2031.

Which device category dominates outsourcing demand?

In-vitro diagnostic devices lead with 27.85% market share due to sustained demand for rapid testing platforms.

Where is the fastest regional growth anticipated?

Asia Pacific is projected to expand at a 10.32% CAGR as global OEMs leverage cost and talent advantages.

Why are quality management services growing so quickly?

Heightened regulatory scrutiny, especially new cybersecurity rules effective in 2025, is pushing OEMs to rely on CMOs with advanced QMS expertise.

How is consolidation affecting competitive dynamics?

OEM mergers compress supplier lists, prompting CMOs to merge for scale and to expand vertically, while technological capabilities such as automation and AI serve as key differentiators.

Page last updated on: