Healthcare Contract Research Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

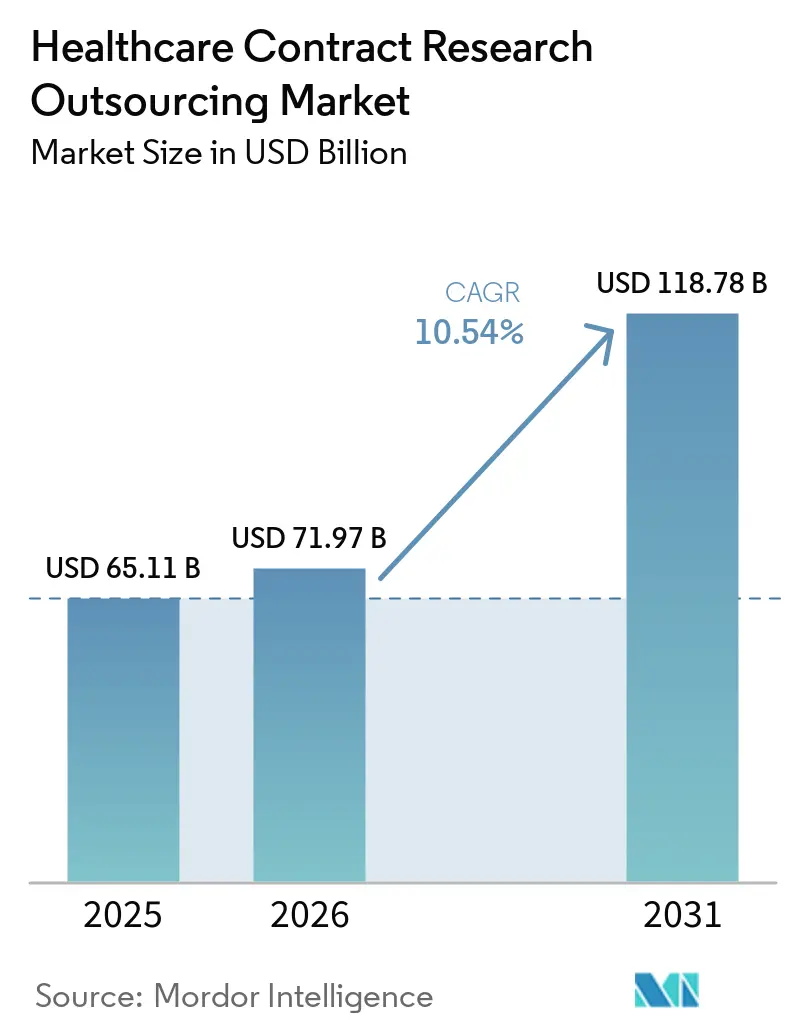

| Market Size (2026) | USD 71.97 Billion |

| Market Size (2031) | USD 118.78 Billion |

| Growth Rate (2026 - 2031) | 10.54% CAGR |

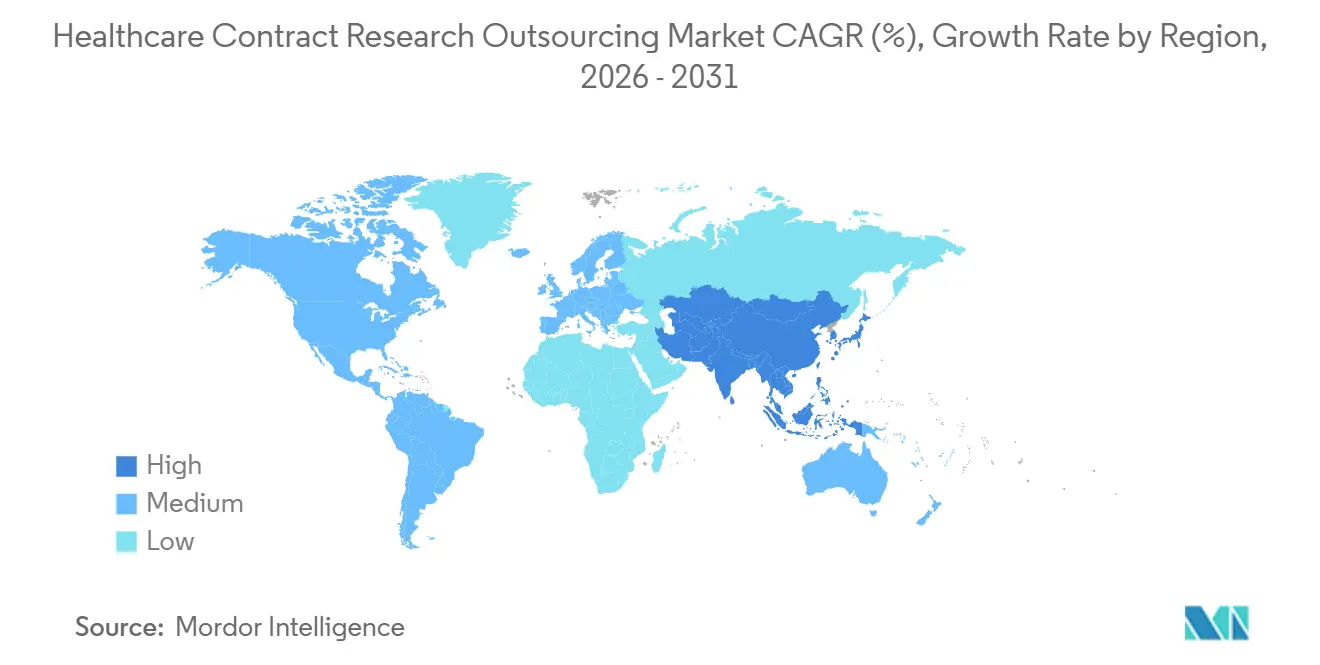

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Contract Research Outsourcing Market Analysis by Mordor Intelligence

The Healthcare Contract Research Outsourcing Market size is expected to increase from USD 65.11 billion in 2025 to USD 71.97 billion in 2026 and reach USD 118.78 billion by 2031, growing at a CAGR of 10.54% over 2026-2031.

Sponsors maintain outsourcing momentum as they seek faster cycle times and predictable cost structures that internal teams struggle to meet at scale, reinforcing the role of global providers with proven delivery models. Backlog visibility at large providers, combined with flexible contracting options, supports steady near-term conversion of awarded programs into revenue, which signals durable demand across therapeutic areas. Functional service provider models continue to gain ground as sponsors look for embedded, fit-for-purpose capacity without the overhead of full end-to-end contracts, especially for data-rich and frequently updated processes. Technology-led study start-up and site enablement increasingly differentiate vendors as AI-driven document intelligence and workflow standardization remove administrative friction that often delays first patient. Data and site intelligence platforms that automate feasibility and enrollment targeting further compress timelines, allowing sponsors to redirect scarce resources toward protocol design and decision-making.

Key Report Takeaways

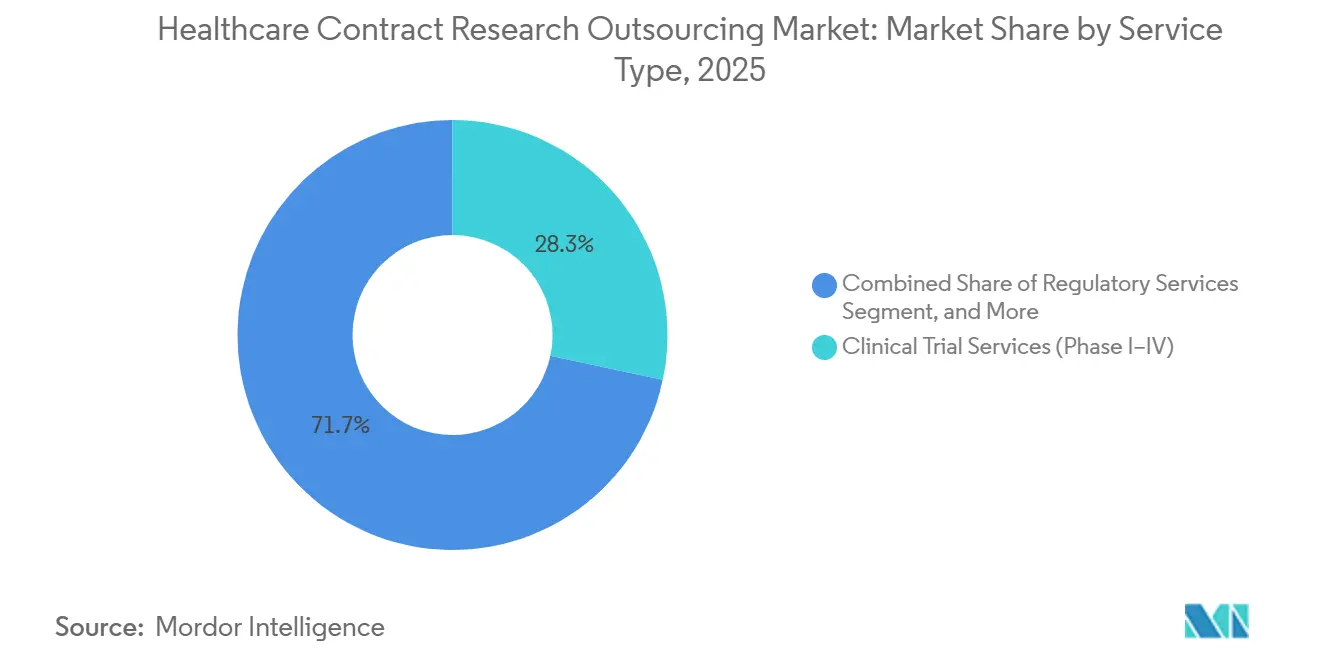

- By service type, clinical trial services (Phase I–IV) accounted for 62.34% share of the healthcare contract research outsourcing market size in 2025, while clinical data management is poised to expand at a 12.56% CAGR through 2031.

- By type, clinical research represented 43.23% share in 2025; pre-clinical research is projected to grow at a 14.31% CAGR over 2026–2031.

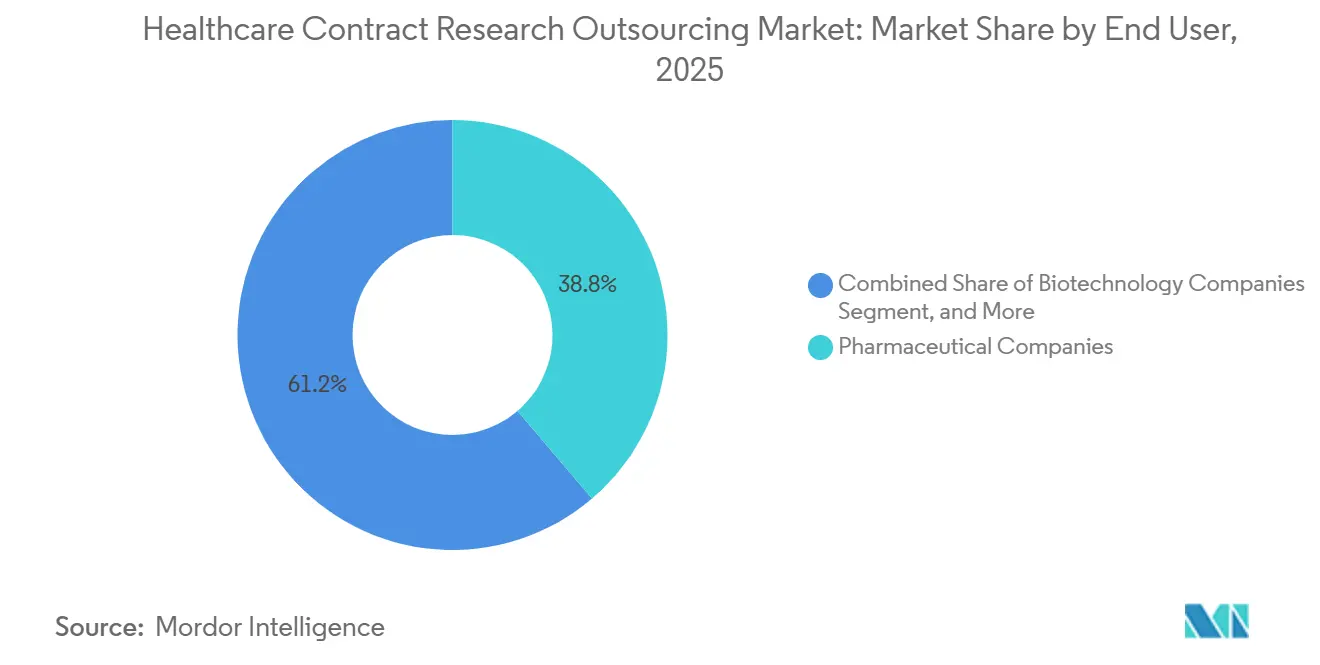

- By end user, pharmaceutical companies held 38.76% in 2025; biotechnology companies are set to record a 13.27% CAGR through 2031.

- By geography, North America captured 37.23% of the healthcare contract research outsourcing market share in 2025, while Asia-Pacific is forecast to advance at a 15.83% CAGR during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Contract Research Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Biopharma R&D Investments and Pipeline Intensity | +2.5% | Global, with concentration in North America, Europe, and emerging APAC markets | Medium term (2-4 years) |

| Cost Pressure and Speed-To-Market Imperatives Drive Externalization | +2.8% | Global, particularly acute in mid-sized biotech firms across North America and Europe | Short term (≤ 2 years) |

| Increasing Clinical Trial Complexity | +1.9% | Global, with advanced protocol designs concentrated in North America, Europe, and China | Medium term (2-4 years) |

| Preference for Specialized Full-Service and FSP Models | +1.7% | North America and Europe primary; APAC adoption accelerating | Medium term (2-4 years) |

| Expansion of Platform/Master Protocols Elevates Program-Level CRO Demand | +1.4% | North America and Europe lead; selective APAC adoption in oncology | Long term (≥ 4 years) |

| AI-Enabled Protocol, Site, and RBQM Optimization Expands Data/Tech-Led CRO Revenue | +2.1% | Global, with early adoption concentrated in technologically advanced North American and European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Biopharma R&D Investments and Pipeline Intensity

Novel drug approvals across leading regulators in 2025 confirm continued sponsor focus on specialized indications where clinical complexity and regulatory scrutiny require strong development partners.[1]Andreas Papapetropoulos et al., “Novel Drugs Approved by the EMA, the FDA and the MHRA in 2025: A Year in Review,” A higher share of orphan-designated therapies within the annual approval mix points to sustained emphasis on targeted patient populations, which raises the need for protocol designs that maximize data yield per subject and accelerate demand for outsourced biostatistics and site operations. Continuous platform-style studies in oncology and other complex areas favor CRO partners that can stand up governance structures and adaptive analytics across multi-arm frameworks rather than isolated single-protocol engagements.[2]Worldwide Clinical Trials, “Considering Master Protocol Use in Your Trial: Baskets & Umbrellas,” Sponsors increasingly rely on embedded statistical and data science capacity to segment subpopulations, align endpoints to regulatory expectations, and streamline submission pathways, which strengthens program-level outsourcing relationships.[3]Quanticate Commercial Team, “FSP Models in Clinical Trials: Types, Differences & Key Considerations,” As larger providers integrate real-world data and technology capabilities into research solutions, they extend support from early evidence development to late-phase outcomes research, reinforcing the outsourcing value proposition across the asset lifecycle.

Cost Pressure and Speed-To-Market Imperatives Drive Externalization

Sponsors under budget constraints balance time-to-data with predictable resourcing, leading many to expand functional service provider models that embed teams within sponsor systems while preserving accountability for delivery quality. Backlog visibility and near-term conversion at large players indicate that staged commitments and flexible contracting are now a standard approach to manage portfolio risk and to match spend to milestone attainment.[4]IQVIA Holdings Inc., “IQVIA Reports Fourth-Quarter and Full-Year 2025 Results; Issues Full-Year 2026 Guidance,”AI-enabled contracting and study start-up tools flag document misalignments early and reduce reconciliation cycles, shrinking activation timelines that often impede first patient. Site intelligence platforms now index hundreds of thousands of institutions and millions of study sites across dozens of countries, which strengthens feasibility accuracy and lifts enrollment performance when sponsors prioritize speed. These operational gains help sponsors compress decision gates and direct investment to the most promising programs, creating a reinforcing cycle for the healthcare contract research outsourcing market as timelines and cost per data point improve.

Increasing Clinical Trial Complexity

Master protocols that run continuously with shared control arms and adaptive decision rules push operational and analytical needs beyond what many in-house teams can support at scale. CROs that can coordinate multi-arm governance, central monitoring, and rolling amendments across sites and vendors become essential to sustain the cadence of decision-making in these platforms. Risk-based quality management has become a core expectation under evolving GCP guidance, which resets monitoring toward centralized analytics, clear traceability of risk decisions, and documented thresholds tied to Critical to Quality factors. Predictive RBQM and centralized monitoring approaches also reduce on-site workload and prioritize visits where signals matter most, improving both compliance and economics for complex protocols. In parallel, decentralization components require validation of telehealth, sensors, and eConsent flows, which increases the importance of CROs with robust technology governance to avoid audit findings under digital-first execution .

Preference for Specialized Full-Service and FSP Models

Sponsors continue to bifurcate outsourcing between turnkey study delivery and embedded functional teams, often within the same portfolio, to balance end-to-end accountability and precision resourcing. Decision frameworks to select FSP versus full-service increasingly factor therapeutic complexity, data intensity, and internal bandwidth, which drives hybrid strategies where biostatistics, data management, and study start-up functions are provisioned as specialized pods. Oncology and cell and gene therapy programs favor partners with deep scientific and operational knowledge plus the flexibility to scale across sites and countries as cohorts evolve, which supports the shift toward modular capacity anchored by shared SOPs. CROs are expanding biometrics and programming hubs to meet demand for continuous data review and standardized analytics packages, which shortens lock cycles and improves database quality. These choices reinforce a vendor ecosystem where full-service leadership coexists with focused FSP centers of excellence that plug into sponsor workflows without fragmenting oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Divergence and CTR/GCP Tightening | -1.8% | Global (EU, UK, US, APAC) | Short term (≤ 2 years) |

| Data Security, IP Protection, and Vendor Governance | -1.5% | Global (cloud/AI operations) | Medium term (2-4 years) |

| Geopolitical/Biosecurity Scrutiny (China-Linked Vendors) | -1.2% | Global (US/EU sponsors) | Short term (≤ 2 years) |

| Site Workforce Shortages and Investigator Burnout | -1.9% | Global (severe in North America/Europe) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Divergence and CTR/GCP Tightening Across Regions

Evolving GCP guidance places stronger emphasis on risk-based quality management and continuous quality improvement, which requires CROs and sponsors to upgrade SOPs, retrain teams, and adapt monitoring models to centralized analytics and clear traceability of risk decisions. Sponsors are expected to demonstrate why and how particular risks were prioritized, including the evidence and thresholds applied, which increases documentation workloads for protocol teams and vendor oversight groups. Functional teams must realign data flows and audit trails to ensure that remote monitoring, eConsent, and sensor-derived data remain inspection-ready, which can extend transition timelines during multi-country study execution. To address this, many sponsors strengthen embedded partnerships where CROs manage regulatory intelligence and training programs that keep global studies on a consistent quality baseline. These adjustments create near-term drag but support longer-term efficiency gains once standardized analytics, documentation, and RBQM platforms are in place, which steadies compliance across a diversified study portfolio.

Data Security, IP Protection, and Vendor Governance Risks

Sponsors face heightened expectations for vendor oversight as data volume and tool diversity increase, which raises the stakes for clear accountability in statements of work and traceable performance metrics across third and fourth parties. Contracting and study start-up systems now embed AI-driven checks that align template language and obligations across parties, reducing the risk of inconsistent terms that can create exposure during audits or disputes. CROs that formalize governance frameworks for AI, remote monitoring, and data handling help sponsors de-risk execution in multi-vendor environments, which becomes a selection criterion for larger, multi-year programs. Workforce development programs at academic and professional bodies also contribute to a stronger compliance culture by expanding the pool of trained personnel familiar with modern digital workflows and documentation standards. This governance emphasis supports the healthcare contract research outsourcing market by directing more specialized, compliance-sensitive work to partners with proven controls and validated platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Management Drives Functional Specialization Amid Phase I–IV Dominance

Clinical trial services (Phase I–IV) captured 62.34% of the healthcare contract research outsourcing market in 2025, while clinical data management is set to grow fastest at a 12.56% CAGR through 2031 as real-time capture and centralized analytics become standard practice. Functional teams focused on data curation, edit checks, and anomaly detection are embedded earlier in the workflow to support risk-based quality management and drive predictable database lock performance under evolving GCP guidance. Providers with site intelligence platforms help sponsors improve screening and enrollment by targeting institutions with proven infrastructure for telehealth, ePRO, imaging, and cardiology endpoints, which reduces screen failure and accelerates milestone attainment. As AI support extends from feasibility to medical writing and data cleaning, large providers maintain margin stability even as protocol demands rise, which sustains investment in analytics capabilities within research delivery units. Study start-up is another focal area, with contract and budget automation reducing administrative latency that often slows first patient in and creates cost risk for sponsors.

Clinical data management gains momentum as sponsors standardize data flows across decentralized components, imaging, and specialty labs, which increases the need for harmonized dictionaries, reusable edit checks, and real-time dashboards. Vendors expand biometrics and programming hubs to address these needs; this evolution is visible in regional capacity investments that bring statistical programming and clinical data operations closer to multinational study footprints. As real-world evidence and late-phase work move closer to clinical operations, sponsors increasingly look for integrated solutions that manage observational cohorts, registries, and safety follow-up under one governance umbrella. The cumulative effect is a service mix where high-volume Phase I–IV activity anchors demand, while data-centric functions command premium growth on the back of RBQM, decentralized elements, and expanding endpoint complexity.

By Type: Pre-Clinical Research Surges as Sponsors Front-Load Risk Mitigation

Clinical research represented 43.23% in 2025, yet pre-clinical research is projected to grow at a 14.31% CAGR through 2031 as sponsors front-load risk management to avoid costly late-stage failures. Backward integration by large providers extends capabilities into discovery and IND-enabling studies, as seen in transactions that add in vitro, NAMs, and small-molecule AI platforms designed to improve clinical translatability from preclinical endpoints. These moves position discovery and preclinical teams to hand off to clinical delivery units with standardized data packages and governance, which lifts execution quality and reduces duplication of effort across the development continuum. Sponsors in fast-moving areas such as obesity and cardiometabolic disease also prioritize partners with combined clinical and data science infrastructure to run large-scale, multi-site programs with payer-relevant outcomes. This alignment supports the healthcare contract research outsourcing market as earlier risk assessment and translational analytics reduce attrition later in development.

Pre-clinical outsourcing also benefits from specialized platform technologies in complex modalities, where scale-up, bioanalytics, and CMC interlock with discovery to support faster iteration cycles. Partnerships and collaborations around next-generation payload-linker technologies, bispecific antibodies, and multi-functional fusion proteins illustrate how platform-level expertise at CDMO and CRO partners shapes development plans and production pathways. Broader corporate collaborations in complex biologics and ADCs extend integrated discovery-to-manufacturing pipelines, narrowing the gap between target ID and clinical readiness through standardized assay and analytics architectures. These specialty capabilities raise switching costs and reinforce long-term outsourcing relationships that move from transactional scopes to multi-asset programs. As a result, the healthcare contract research outsourcing market benefits from sustained investment in discovery-enabling infrastructure that feeds clinical portfolios with better characterized candidates.

By End User: Biotechnology Companies Outpace Pharma Giants Through Venture-Backed Growth

Pharmaceutical companies accounted for 38.76% of demand in 2025, while biotechnology companies are positioned as the fastest-growing end user segment with a 13.27% CAGR over 2026–2031. Biotech sponsors often operate with lean infrastructures, which makes embedded FSP teams attractive for biostatistics, data management, and study start-up while maintaining sponsor ownership of protocol decisions. Oncology specialists and mid-tier providers that combine early-phase expertise with FSP capabilities continue to attract biotech programs that need hands-on guidance and flexible scale. Biometrics and programming expansions near key delivery hubs also support biotech outsourcing by reducing time zone friction and enabling continuous data review across global studies. These dynamics reinforce outsourcing penetration in biotech, which sustains growth for the healthcare contract research outsourcing market as assets advance toward pivotal stages.

Biotech growth also draws support from academic ecosystems and professional bodies that expand the pool of trained researchers and future principal investigators. Programs that connect university health systems and CRO partners increase access to early-phase infrastructure and create pathways for investigators to lead or participate in sponsor studies under modern compliance standards. Workforce development initiatives deepen the talent base in clinical research operations, data management, and regulatory documentation, which helps smaller sponsors execute to high standards with outsourced teams. Combined with flexible outsourcing models and specialized partners, these factors position biotech as a core growth driver while large pharma sustains the baseline volume of global studies the healthcare contract research outsourcing industry serves.

Geography Analysis

North America accounted for 37.23% of the healthcare contract research outsourcing market in 2025, supported by extensive investigator networks, mature site infrastructure, and a large base of sponsors. Strong vendor presence in the United States ensures access to full-service and FSP models along with advanced data platforms that align to updated GCP expectations on documentation and centralized monitoring. Study start-up and contract optimization capabilities further enhance execution speed across this region, as AI-powered checks reduce friction in agreements with sites and vendors. As large providers integrate obesity, cardiometabolic, and real-world evidence collaborations into research offerings, the region benefits from scaled infrastructure that supports late-phase and outcomes studies alongside pivotal trials. These features sustain North America’s anchor role in the healthcare contract research outsourcing market even as sponsors diversify trial footprints globally.

Asia-Pacific is the fastest-growing region with a projected 15.83% CAGR through 2031, reflecting the rapid buildout of clinical infrastructure and strategic collaborations that expand early-phase capacity. Partnerships that link university health systems with global CRO capabilities give sponsors efficient access to large patient bases and integrated clinical ecosystems, which are vital for first-in-human and dose-ranging studies. Regional platform and modality specialists continue to scale capabilities in biologics and complex modalities, which increases outsourcing options for sponsors seeking APAC patient access with high-quality analytics and manufacturing integration. As integrated discovery-to-manufacturing pipelines mature in the region, sponsors can align pre-clinical and clinical supply chains with study timelines, supporting faster program progression and reinforcing the healthcare contract research outsourcing market in APAC.

European expansions by CROs increase access to specialized early-phase and biometrics capabilities, which helps sponsors balance regulatory and operational needs across the continent. Oncology-focused providers with embedded FSP capacity continue to build on regional strengths in precision medicine, where complex master protocols and biomarker-driven cohorts demand strong governance and analytics. As centralized monitoring and RBQM-based oversight are standardized in European operations, vendors with validated processes and training programs gain selection advantages, strengthening contributions to the healthcare contract research outsourcing market.

Competitive Landscape

Scale providers lead by combining global delivery with investment in data and AI platforms that streamline feasibility, start-up, and data cleaning while preserving operating margins. A large player’s reported 2025 performance and 2026 guidance highlight a substantial contracted backlog and steady near-term conversion, reinforcing the sector’s visibility into awarded work and revenue timing. Strategic moves to acquire discovery assets broaden end-to-end coverage from preclinical to pivotal stages, positioning providers to control data standards and governance from early translational studies onward. Partnerships that align clinical operations with leading academic research centers also expand capabilities in high-priority areas such as obesity and cardiometabolic disease, where large patient cohorts and outcomes data are critical. Together, these strategies reinforce leadership positions in the healthcare contract research outsourcing market.

Mid-tier specialists differentiate through therapeutic focus, regional density, and targeted technology capabilities. Oncology-focused CROs that combine early-phase execution with FSP programs offer biotech and mid-size pharma sponsors tailored capacity where trial complexity and cohort fragmentation require hands-on governance. AI-enabled site intelligence platforms that connect millions of sites across dozens of countries support enrollment planning and rapid feasibility, which addresses a long-standing pain point in global studies. Contracting and start-up tools that automate agreement review and harmonize terms reduce activation delays, positioning technology-enabled providers to capture time-sensitive programs across indications. These differentiators support a competitive middle tier that thrives alongside global leaders within the healthcare contract research outsourcing market.

Regional builds and capability expansions continue through M&A and organic investments. European acquisitions expand early-phase and regulatory capabilities on the continent, which improves access for sponsors planning multinational designs. Biometrics teams added in Asia-Pacific increase 24-hour cycle coverage for data review and cleaning, which contributes to faster database locks and higher data quality in global studies. Platform technology collaborations around ADCs and fusion proteins strengthen the region’s role in complex biologics development and manufacturing, and these platforms often anchor multi-asset, multi-year partnerships that extend from discovery into late-stage development. Strategic evaluations by emerging companies to acquire niche CRO capabilities in oncology and rare disease also point to an active consolidation pipeline that will further shape the competitive set through 2026.

Healthcare Contract Research Outsourcing Industry Leaders

Charles River Laboratories International, Inc.

Eurofins Scientific

ICON plc

IQVIA Holdings Inc.

Parexel International Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Monash University and ClinChoice formed a strategic partnership to accelerate early-phase clinical trials by connecting five major affiliated health services with over 7,000 hospital beds, more than 3,000 general practitioners, and access to 4.5 million patients to ClinChoice’s global development, regulatory, and data science capabilities.

- March 2026: Thermo Fisher Scientific, inc. completed its USD 8.875 billion acquisition of Clario Holdings, announced in October 2025, with an additional USD 125 million due in January 2027 plus up to USD 400 million in earn-out payments. Clario's endpoint data platform, which supported approximately 70% of new drug approvals by the FDA and EMA over the past decade, integrates with Thermo Fisher's PPD CRO and laboratory services to create unified clinical endpoint capabilities.

- March 2026: Syneos Health acquired Chinese CRO Bestudy to strengthen its presence in China's rapidly growing biopharma market, where clinical trial sites expanded 51% from 2023 to 2025, surpassing the 42% growth rate in the United States. Bestudy will maintain independent operations, leadership, and branding post-acquisition, with financial terms undisclosed.

Global Healthcare Contract Research Outsourcing Market Report Scope

As per the scope of the report, healthcare contract research outsourcing refers to the practice where pharmaceutical, biotechnology, medical device, and healthcare companies delegate research and development activities such as clinical trials, data management, biostatistics, regulatory affairs, and pharmacovigilance to external specialized providers (CROs). It enables sponsors to reduce costs, accelerate development timelines, access global expertise, and improve operational efficiency.

The healthcare contract research outsourcing market is segmented by service type, type, end user, and geography. By service type, the market is segmented into Clinical Trial Services (Phase I–IV), regulatory services, clinical data management, pharmacovigilance, site management & monitoring, central lab & bioanalytical Services, real‑world evidence & late phase, and others. By type, the market is segmented into drug discovery, Pre-clinical research, and Clinical research. By end user, the market is segmented into pharmaceutical companies, biotechnology companies, and medical device companies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Clinical Trial Services (Phase I-IV) |

| Regulatory Services |

| Clinical Data Management |

| Pharmacovigilance |

| Site Management & Monitoring |

| Central Lab & Bioanalytical Services |

| Real World Evidence & Late Phase |

| Others |

| Drug Discovery |

| Pre-clinical Research |

| Clinical Research |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical Device Companies |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Clinical Trial Services (Phase I-IV) | |

| Regulatory Services | ||

| Clinical Data Management | ||

| Pharmacovigilance | ||

| Site Management & Monitoring | ||

| Central Lab & Bioanalytical Services | ||

| Real World Evidence & Late Phase | ||

| Others | ||

| By Type | Drug Discovery | |

| Pre-clinical Research | ||

| Clinical Research | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Medical Device Companies | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the healthcare contract research outsourcing market size outlook to 2031?

The healthcare contract research outsourcing market size is projected to reach USD 118.78 billion by 2031, rising from USD 65.11 billion in 2025 at a 10.54% CAGR.

Which segments are leading growth within healthcare contract research outsourcing?

Clinical trial services led in 2025, while clinical data management, pre-clinical research, and biotechnology sponsors show the fastest growth trajectories through 2031.

How are AI and RBQM changing execution in healthcare contract research outsourcing?

AI improves feasibility, start-up, and data cleaning, while RBQM shifts monitoring to centralized analytics with documented risk traceability, which shortens timelines and strengthens inspection readiness.

Why is Asia-Pacific attracting more outsourced trials?

Strong university-health system partnerships, growing modality platforms, and integrated pipelines from discovery to clinical supply are drawing more studies to APAC, which supports the region’s leading growth rate.

What outsourcing models are sponsors choosing most often?

Sponsors combine full-service engagements for end-to-end delivery with FSP models for embedded, specialized functions such as biostatistics, data management, and start-up to balance speed and control.

Which capabilities differentiate leading CROs today?

Leaders invest in AI-driven start-up and site intelligence, expand biometrics hubs, and add discovery assets and academic collaborations to control data standards from preclinical through pivotal stages.

Page last updated on: