Cellular Health Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

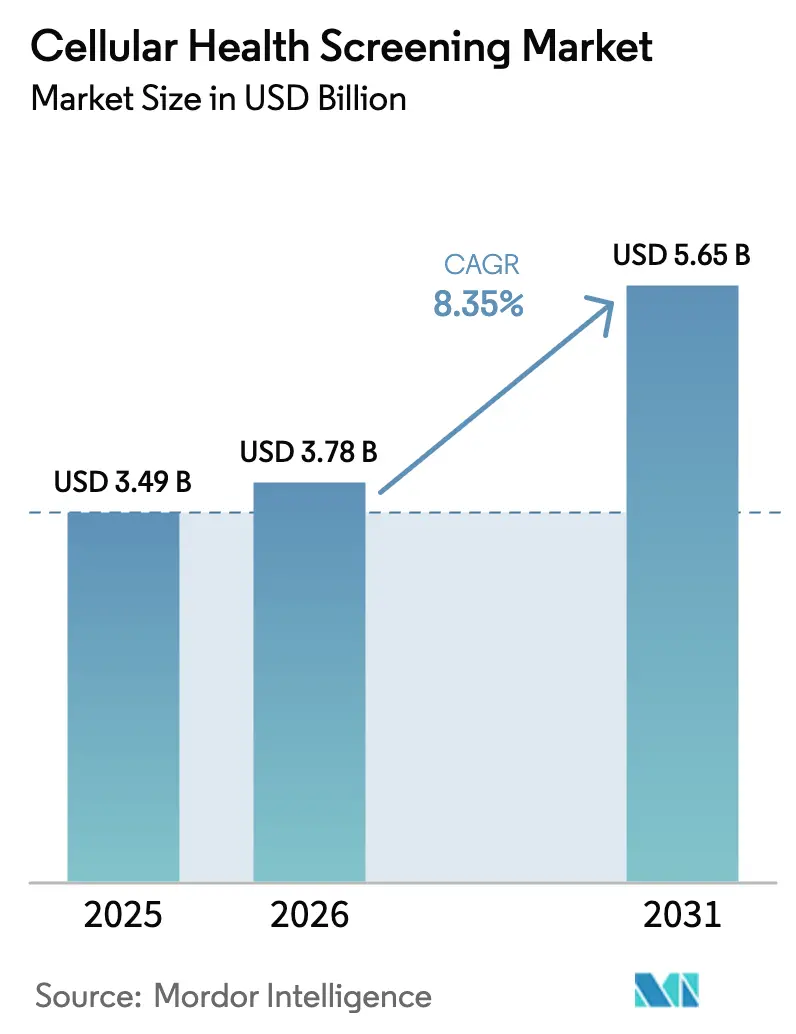

| Market Size (2026) | USD 3.78 Billion |

| Market Size (2031) | USD 5.65 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

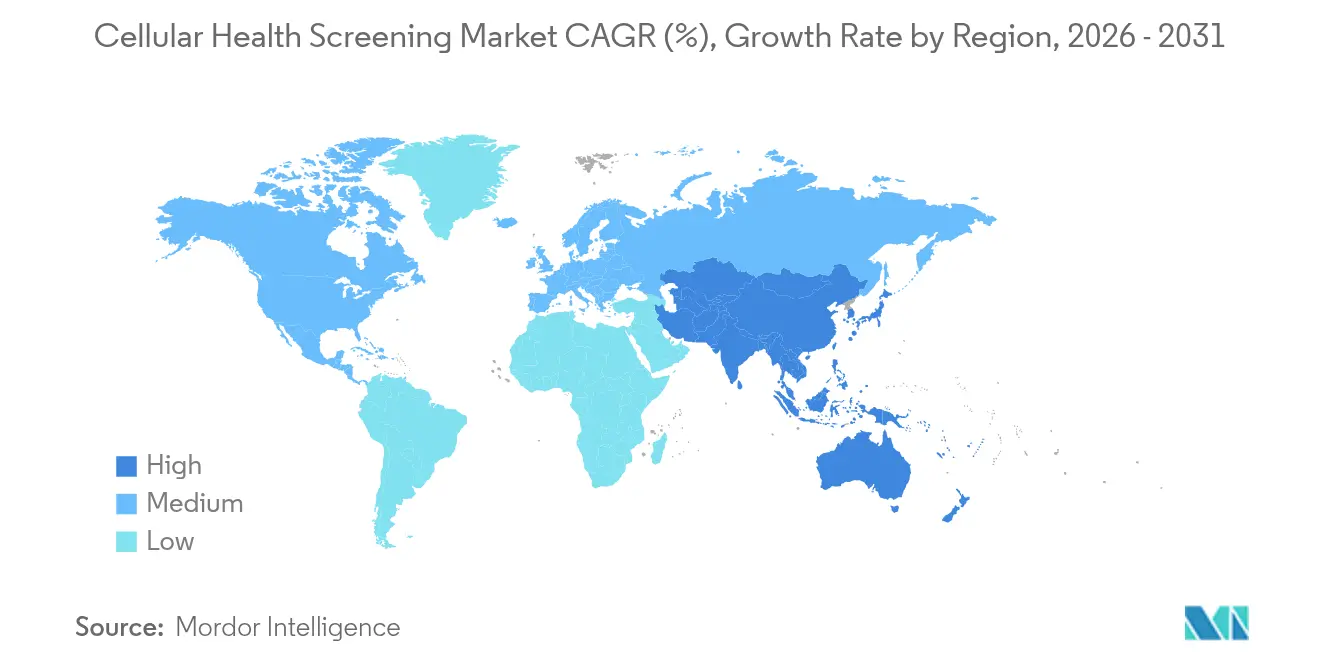

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cellular Health Screening Market Analysis by Mordor Intelligence

Cellular health screening market size in 2026 is estimated at USD 3.78 billion, growing from 2025 value of USD 3.49 billion with 2031 projections showing USD 5.65 billion, growing at 8.35% CAGR over 2026-2031. Strong public interest in personalized medicine, regulatory clarity for laboratory-developed tests, and the growing priority of preventive care underpin this expansion. North America remains the largest regional buyer, supported by extensive laboratory networks and early direct-to-consumer (DTC) adoption. Asia-Pacific posts the fastest regional advance, propelled by state funding for aging-research programs and expanding middle-class demand. Single-test panels still dominate revenues, yet multi-test panels and saliva-based collection kits are scaling rapidly, aided by machine-learning analytics that transform raw biomarker data into actionable recommendations. Mounting clinical evidence linking mitochondrial dysfunction to chronic disease continues to spur new product launches and investment in advanced cellular diagnostics.

Key Report Takeaways

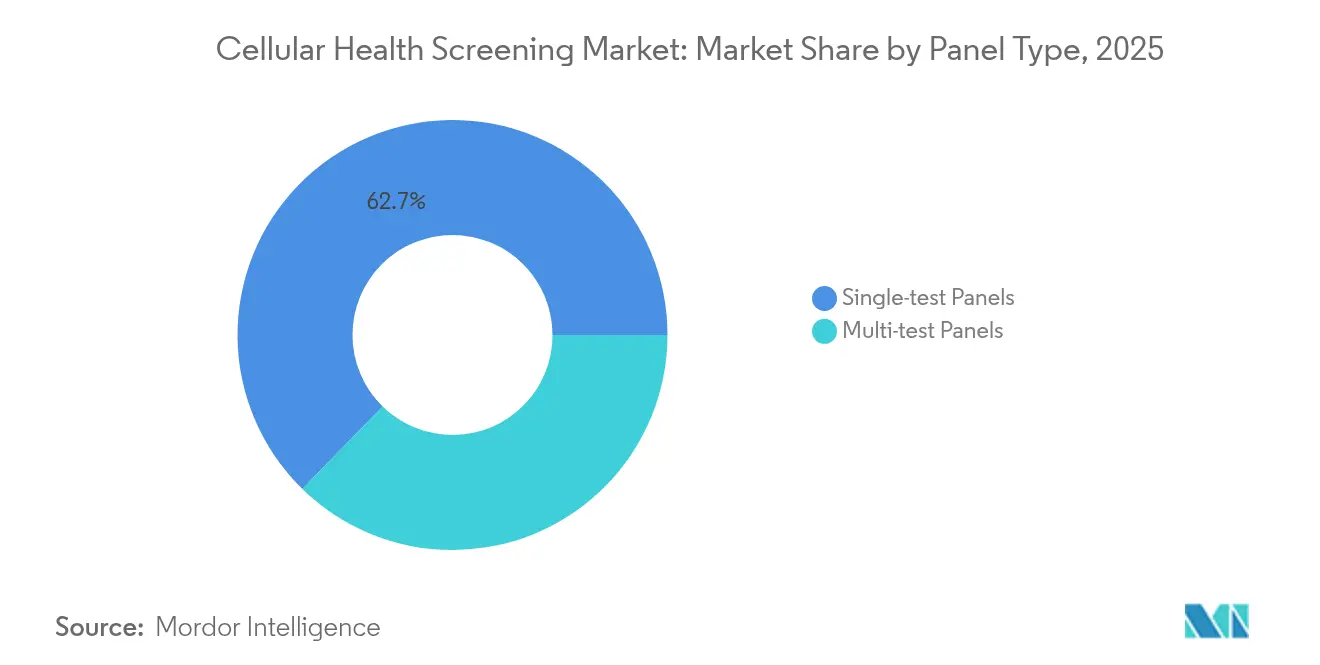

- By panel type, single-test panels held 62.70% of the cellular health screening market share in 2025, while multi-test panels expand fastest at a 12.82% CAGR to 2031.

- By test type, telomere length led with 40.05% revenue share in 2025; mitochondrial function testing is set to grow at a 15.44% CAGR through 2031.

- By sample type, blood accounted for 69.10% of the cellular health screening market size in 2025, whereas saliva sampling is projected to advance at a 15.18% CAGR to 2031.

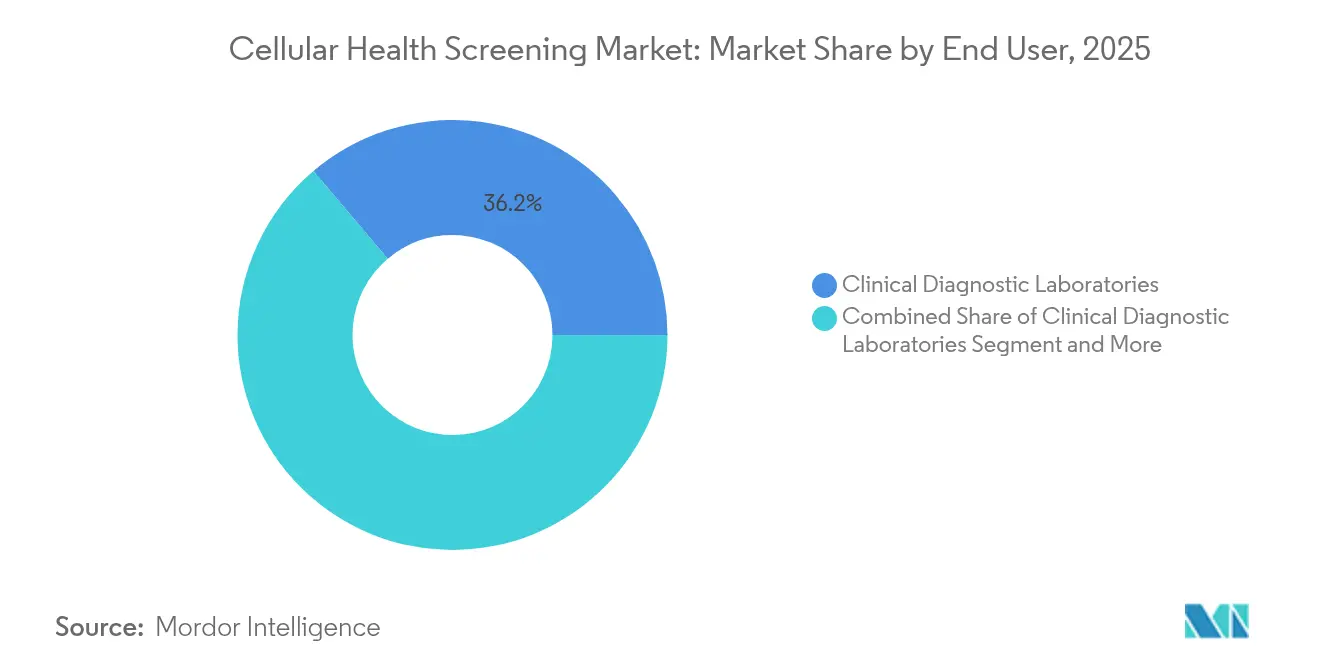

- By end user, clinical diagnostic laboratories captured 36.20% revenue in 2025; home-healthcare/individual consumers record the quickest growth at 14.28% CAGR.

- By distribution channel, physician-ordered pathways retained 54.10% share in 2025; online DTC services demonstrate an 17.63% CAGR, the highest among channels.

- By geography, North America commanded 37.30% revenue in 2025, while Asia-Pacific is expanding at 13.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cellular Health Screening Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption Of Personalized-Medicine Programs | +2.1% | Global, with North America & Europe leading | Medium term (2-4 years) |

| Government Funding For Preventive Healthcare | +1.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Ageing Population & Chronic-Disease Burden | +2.3% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Expansion Of Direct-To-Consumer Test Platforms | +1.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-Driven Biological-Age Scoring Integrations | +1.4% | Global, early adoption in tech-forward markets | Medium term (2-4 years) |

| Employer Wellness Schemes Tying Premiums To Telomere Metrics | +0.8% | North America & EU corporate markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Personalized-medicine programs

Hospitals increasingly couple companion diagnostics with drug regimens, using telomere length and oxidative-stress scores to refine dosing. The FDA authorization of Illumina’s TruSight Oncology Comprehensive assay in 2024 validated multiplex biomarker panels for mainstream care[1]Illumina, “FDA Approves Next-Generation Cancer Biomarker Test and Companion Diagnostics,” myadlm.org. Oncology and cardiology units now embed cellular markers inside electronic health-record workflows, enabling risk-stratified treatment selection. Corporate wellness contracts add momentum, with employers tying premiums to biological-age metrics gathered via employee screening programs. Machine-learning engines enrich these datasets, improving prediction accuracy and allowing continuous model refinement as new outcomes emerge.

Government funding for preventive healthcare

Japan’s Ministry of Health has adopted magnetocardiography for nationwide metabolic disease risk checks, signaling policy commitment to early detection tools. Horizon Europe grants and NIH geroscience budgets channel fresh capital toward biomarker validation studies, accelerating pipeline progress from lab bench to clinic. National payers see cost-avoidance value in finding disease at a reversible stage, and grant calls now specify integration of AI algorithms that mine multi-omics datasets. These incentives encourage start-ups to standardize protocols early, reducing downstream regulatory friction and shortening commercialization timelines.

Aging population and chronic-disease burden

By 2030, people aged 60 plus will constitute one-sixth of the global population, amplifying demand for tools that differentiate biological from chronological age[2]Health Club Management, “Longevity Clinics,” healthclubmanagement.co.uk. Telomere attrition, mitochondrial insufficiency, and systemic inflammation scores now feature in routine cardiac and diabetic check-ups. Research published in 2024 highlighted mitochondrial dysfunction as a primary driver of atherosclerosis, underscoring the diagnostic relevance of these assays. Policymakers in high-income economies respond by shifting resources toward preventive frameworks that leverage such early-warning markers.

Expansion of DTC test platforms

Online portals post double-digit growth because kits arrive at the doorstep, require brief sample collection, and return anonymized dashboards within days. FDA finalization of its laboratory-developed-test rule in 2024 spelled out safety benchmarks, enabling firms to scale while retaining innovation flexibility. Platform providers now bundle tele-consults and lifestyle coaching inside subscription packages, creating recurring revenue and higher client retention. However, the financial volatility witnessed at 23andMe illustrates that user acquisition must be matched by robust monetization and clear clinical utility to endure.

Restraints Impact Analysis of Cellular Health Screening Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sample-Transport Stability & Cold-Chain Risk | -1.2% | Global, acute in developing markets | Short term (≤ 2 years) |

| Evolving Regulatory & Reimbursement Uncertainty | -0.9% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Data-Privacy Concerns For At-Home Genomic Telomere Data | -0.7% | EU & North America primarily | Short term (≤ 2 years) |

| Inter-Lab Variability Of Oxidative-Stress Assay Results | -0.6% | Global, standardization challenges | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sample-transport stability and cold-chain risk

Oxidative-stress and cytokine assays degrade when shipments encounter temperature spikes, compromising result accuracy. Modeling studies show even brief excursions outside 2–8 °C diminish biomarker integrity. Advanced thermal packaging and on-box dataloggers help, yet add cost and weight. Companies respond by locating satellite labs nearer collection hubs and experimenting with dried-blood-spot formats that travel safely without refrigeration. In low-income regions, insufficient cold-chain networks remain a barrier to broad uptake of the cellular health screening market.

Evolving regulatory and reimbursement uncertainty

The FDA will phase LDT oversight through 2028, compelling laboratories to submit stepwise data packages while maintaining service continuity. Europe’s IVDR expands notified-body review requirements, stretching capacity and lengthening approval cycles[3]European Commission, “Medical Devices – In Vitro Diagnostics,” health.ec.europa.eu. Insurers have yet to define uniform payment codes for preventive biomarker panels, so many tests remain consumer-paid. This fragmented environment deters small entrants and slows diffusion, particularly for novel assays lacking extensive outcome data.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cellular Health Screening Market Segment Analysis

By Panel Type:

Multi-test integration drives growthSingle-test formats held 62.70% of the cellular health screening market in 2025, supported by clear clinical indications and lower cost. Multi-test bundles, though smaller in revenue, record a 12.82% CAGR to 2031 thanks to consumer appetite for holistic health snapshots. The cellular health screening market size for multi-test offerings is projected to expand rapidly as algorithmic platforms can interpret dozens of markers within minutes, converting complex data into concise action plans. Physicians increasingly order multiplex panels during annual physicals to capture telomere, inflammation, and mitochondrial markers in one visit. DTC brands leverage multi-test convenience to upsell subscription coaching, reinforcing engagement.

Vendors address price sensitivity by tiering panels, letting users start with an entry bundle then add biomarkers over time. Growth also stems from employers that deploy multi-test kits in workforce wellness drives to reduce absenteeism. Laboratories integrate high-throughput sequencing and mass-spectrometry workflows to manage the rising sample volume without delaying turnaround. Hardware automation further trims per-sample cost, supporting competitive pricing in the cellular health screening market.

By Test Type:

Mitochondrial function testing leads innovationTelomere assays retained 40.05% share in 2025, yet mitochondrial function testing will post the highest 15.44% CAGR as research confirms links between mitochondrial health, cardiovascular risk, and metabolic disease. The cellular health screening market size tied to mitochondrial assays will therefore widen swiftly.

Novel fluorescence-based readouts and respirometry platforms increase throughput and sensitivity, making these evaluations practical for routine screening. Some providers package mitochondrial scores with dietary recommendations that target NAD⁺ pathways, giving users a clear intervention roadmap. Oxidative-stress and inflammatory-cytokine panels maintain demand because clinicians value their role in monitoring chronic-disease progression. Heavy-metal burden assays carve a niche in regions with industrial pollution, supported by microfluidic sensor innovations that cut analysis time. AI overlays identify biomarker clusters predictive of early pathology, further raising the clinical appeal of comprehensive mitochondrial testing in the cellular health screening market.

By Sample Type:

Saliva testing gains momentumBlood remained the dominant collection matrix at 69.10% share in 2025, bolstered by decades of validated protocols and broad biomarker coverage. Saliva registers the fastest 15.18% CAGR as consumers favor painless self-collection. Buccal epigenetic clocks such as CheekAge demonstrate strong correlation with blood-based aging indices, enhancing confidence in alternate sampling.

The cellular health screening market share for saliva kits will keep climbing as logistics improve; ambient-temperature shipping removes cold-chain dependence, lowering cost. However, variability in enzyme activity within saliva necessitates strict pre-test instructions and robust controls. Urine retains a role for specific metabolites, while hair samples support long-term heavy-metal exposure profiling. Research groups continue to cross-validate matrices, aiming to create interchangeable algorithms that reconcile readings from blood and saliva, broadening access to the cellular health screening market.

By End User:

Home healthcare segment acceleratesClinical laboratories captured 36.20% revenue in 2025, anchored by established quality-management systems and payer connections. Nevertheless, home-healthcare users generate a 14.28% CAGR as pandemic-era testing habits persist. Consumers appreciate privacy and the ability to track progress over time without clinic visits. Longevity centers offer premium memberships costing up to USD 40,000 annually, bundling regular cellular panels, exercise coaching, and diet planning.

The cellular health screening industry therefore sees demand from both mass-market and luxury segments. Hospitals integrate at-home sampling kits into telemedicine pathways to keep chronic-disease patients engaged between appointments. Research institutions use the same infrastructure for large-cohort longitudinal studies, capturing real-world biomarker data at scale. Insurers pilot reimbursement for remote testing when outcomes show reduced downstream treatment costs, further legitimizing the home-health approach in the cellular health screening market.

By Distribution Channel:

Digital transformation acceleratesPhysician-ordered pathways held 54.10% share in 2025 because many biomarkers still require clinical interpretation and insurance documentation. Online DTC platforms, however, expand at an 17.63% CAGR as intuitive dashboards demystify results for lay users. These portals secure CLIA-certified lab partnerships to guarantee accuracy while focusing internal resources on user experience. Employer-sponsored portals bundle cellular tests with wearable-device analytics, creating unified health dashboards that encourage healthier habits.

Retail pharmacies explore in-store kiosks that guide customers through finger-stick collection, merging convenience with pharmacist counseling. The cellular health screening market size captured by digital channels is expected to broaden further once payers recognize certified DTC results for wellness incentives. Regulators emphasize transparent marketing and evidence-backed claims, encouraging responsible growth and protecting consumers from unsubstantiated offerings.

Geography Analysis

North America Cellular Health Screening Market

North America generated 37.30% of 2025 revenue, anchored by dense laboratory networks, supportive reimbursement pilots, and a tech-savvy population willing to pay for proactive care. The United States benefits from clear FDA guidance on LDT oversight, giving laboratories predictable pathways to market while safeguarding test quality. Canada’s market outlook strengthened when Quest Diagnostics closed its USD 985 million LifeLabs purchase, boosting nationwide capacity to deliver integrated screening services. Mexico’s emerging middle class drives demand for affordable DTC kits, and local distributors partner with U.S. vendors to localize logistics.

Europe Cellular Health Screening Market

Europe maintains solid momentum as the IVDR harmonizes technical standards, improving public trust in assay validity though raising compliance costs. Germany and the United Kingdom lead adoption, backed by strong clinical-research ecosystems, while France sees rising participation from private insurers that reimburse cellular panels within wellness packages. Southern European countries tap EU recovery funds to modernize laboratory infrastructure, narrowing historical capacity gaps. Strict data-privacy norms resonate with consumers wary of genomic misuse, positioning European providers that embed privacy-by-design as preferred options.

APAC Cellular Health Screening Market

Asia-Pacific records the fastest regional CAGR at 13.05% through 2031. China expands hospital-grade laboratory clusters and supports domestic test developers through innovation grants. Japan institutionalizes preventive medicine through nationwide magnetocardiography screening, underscoring government belief in early biomarker detection. India’s digital-health initiatives open rural channels, with mobile phlebotomy services collecting samples door-to-door. South Korea and Australia encourage university-industry consortia that fuse AI with biomarker discovery, accelerating product pipelines. Despite progress, disparate regulatory frameworks and uneven cold-chain infrastructure mean vendors must tailor go-to-market strategies by country, partnering with local distributors to address logistical and cultural nuances.

Regulatory Landscape

Regulatory requirements for cellular health screening continue to tighten as laboratory-developed tests (LDTs) and in vitro diagnostics (IVDs) face more formalized oversight. In the United States, the FDA is advancing its LDT framework with concrete near-term compliance milestones, including labeling requirements for most IVDs offered as LDTs and establishment registration and device listing obligations by May 6, 2026. The FDA Quality Management System Regulation (QMSR) also became effective on February 2, 2026, increasing emphasis on quality systems across IVD operations and documentation.

In Europe, Regulation (EU) 2017/746 (IVDR) is reshaping market access through legacy-device transition rules and stronger notified-body involvement. A key continuity anchor for legacy Class C IVDs is the May 26, 2026 deadline to submit a formal conformity-assessment application to an IVDR Notified Body to qualify for extended transition, alongside the move toward EUDAMED as a central database for new IVDs starting May 28, 2026. Across Asia, screening policies are also linking diagnostics to digital health infrastructure, including Vietnam's Directive 17/CT-TTg (signed May 6, 2026) that mandates nationwide free periodic health check-ups and integration of electronic health records with the VNeID application, raising interoperability and traceability expectations for population-scale screening workflows.

Competitive Landscape

The cellular health screening market features moderate fragmentation. Quest Diagnostics and Labcorp leverage nationwide logistics, broad payer contracts, and deep assay menus to anchor their leadership. Quest’s USD 985 million LifeLabs acquisition expanded reach in Canada and augmented capacity for preventive-health panels. In May 2025, Labcorp moved to purchase select Incyte Diagnostics assets to strengthen same-day pathology coverage in the Pacific Northwest. These moves reflect a consolidation trend as large players seek geographic coverage and cost efficiencies.

Specialists such as Telomere Diagnostics, SpectraCell, and TruDiagnostic focus narrowly on telomere biology, micronutrient analytics, or epigenetic clocks. They differentiate through proprietary algorithms and publish validation studies in peer-reviewed journals to secure clinician confidence. Technology-oriented entrants blend AI pipelines with cloud dashboards to personalize interventions and maintain user engagement. Financial hurdles witnessed by 23andMe underscore the importance of sustainable pricing models and continuous product innovation to retain market share.

Competitive advantage increasingly hinges on data assets. Firms that securely aggregate long-term longitudinal biomarker datasets can refine predictive models and attract pharmaceutical partners seeking biomarkers for trial stratification. Patents around sample-collection devices and assay workflows provide additional protection. As regulatory demands intensify, companies with established quality-management systems and capitalization stand best placed to secure global approvals, setting high entry barriers for lean start-ups in the cellular health screening market.

Cellular Health Screening Industry Leaders

Quest Diagnostics Inc.

Laboratory Corporation of America Holdings (Labcorp)

SpectraCell Laboratories Inc.

Genova Diagnostics

Telomere Diagnostics Inc.

- *Disclaimer: Major Players sorted in no particular order

Cellular Health Screening Market Companies Covered in this Report

- Quest Diagnostics

- LabCorp

- SpectraCell Laboratories

- Genova Diagnostics

- Bio-Reference Laboratories Inc. (OPKO Health)

- Telomere Diagnostics

- Segterra

- Grail LLC

- RepeatDx

- Agilent Technologies

- Bloom Diagnostics

- Cell Science Systems Corp.

- Fagron Genomics

- Life Length S.L.

- Chronomics Ltd.

- Zymo Research Corp.

- TruDiagnostic LLC

- 23andMe

- MyDNAge (Epiq MD)

- Beckton Dickinson

Market Opportunities and Future Outlook

One clear whitespace for cellular health screening sits at the intersection of multi-analyte panels and higher-automation analytics that translate complex biomarker data into clinically usable risk scoring. Peer-reviewed advances in 2026 highlight this pathway: a large-scale proteomics study across 60,542 individuals reported an integrated polycellular aging risk score (PARS) derived from plasma proteins, reinforcing demand for validated biological-age scoring that can be embedded into physician-ordered pathways and longitudinal monitoring programs. In parallel, cell-free multi-omics methods are moving closer to practical screening use cases, including automated capture of cell-free histone modifications from plasma (cf-EpiTracing) for early-stage disease detection and stratification workflows.

Commercial opportunity also expands where regulatory and operational standardization reduces friction for scaling, especially in regulated IVD pathways and upgraded quality systems. The FDA LDT phaseout actions that began in 2025, and the 2026 implementation anchors for QMSR and LDT-related registration and labeling requirements, underscore the value of robust, repeatable test workflows that can be deployed consistently across large laboratory networks and DTC platforms. Within this context, multi-test bundles that combine telomere, metabolic, micronutrient, and genetic markers align with the market shift toward holistic baselines and subscription-style tracking, while advances such as transformer-based models for processing plasma cfRNA (GeneLLM, 2026) point to cost-reduction routes that can make higher-resolution panels more scalable for broader preventive screening adoption.

Recent Industry Developments in Cellular Health Screening Market

- June 2026: SpectraCell Laboratories released updated specimen packing and return resources to support safe and accurate return of home test kits. The update strengthens pre-analytical quality controls for mail-in screening workflows, which affects result consistency for multi-marker cellular health panels. Improved kit logistics also reduces operational friction for DTC and hybrid clinic-at-home programs.

- May 2025: Labcorp agreed to acquire select assets of Incyte Diagnostics clinical and anatomic pathology testing businesses to expand its testing footprint in the Pacific Northwest. The move adds regional capacity and breadth that can support preventive and precision-oriented testing menus, including cellular health screening panels routed through large laboratory networks. It also reflects continued consolidation among scaled diagnostics providers seeking faster turnaround and localized coverage.

- August 2024: Quest Diagnostics completed its USD 985 million purchase of LifeLabs, expanding its Canadian laboratory footprint. The acquisition increases access points and processing capacity that can be leveraged for preventive-health testing and broader biomarker panel deployment. With cross-provincial reach, Quest strengthened its ability to standardize logistics, quality systems, and digital reporting across Canada.

Cellular Health Screening Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue generated from cellular health screening tests and panels that assess cell function and stress using measurable biomarkers, along with the supporting services needed to process and report results for preventive or wellness use.

Scope exclusions: It does not count broad routine clinical diagnostics that are not positioned as cellular health screening, nor does it count general wellness coaching without a test component.

Segments Covered in This Report

- By Panel Type

- Single-test Panels

- Telomere Tests

- Oxidative Stress Tests

- Inflammation Tests

- Heavy-Metals Tests

- Multi-test Panels

- Single-test Panels

- By Test Type

- Telomere Length

- Oxidative Stress Markers

- Inflammatory Cytokines

- Heavy-Metal Burden

- Mitochondrial Function

- By Sample Type

- Blood

- Urine

- Saliva

- Buccal Swab

- Hair / Other Tissues

- By End User

- Clinical Diagnostic Laboratories

- Hospital Laboratories

- Research & Academic Institutes

- Wellness & Anti-aging Clinics

- Home Healthcare / Individual Consumers

- Corporate Wellness Providers

- By Distribution Channel

- Direct-to-Consumer (Online)

- Physician-Ordered / Clinic-Based

- Employer-Sponsored Programs

- Retail Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what is actually sold and billed in cellular health screening, and then tying it to observable healthcare activity and lab testing patterns. We used public sources such as the US FDA site for LDT and diagnostic policy context, the US CDC and National Center for Health Statistics for preventive care indicators, and the World Health Organization for cross-country health system signals.

To avoid building the model on assumptions alone, we also reviewed sources such as OECD health statistics for testing capacity context, PubMed indexed clinical literature for common biomarker groups used in practice, and trade association or regulator portals that describe laboratory operations and quality standards. Company filings, investor presentations, and reputable press were used to understand business mixes and how test menus are described. Paid database subscriptions were used selectively for company financials and for patent landscaping around biomarker and assay activity. These are illustrative sources only, and many other public and internal references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with laboratory leaders, test developers, channel partners, and clinical and wellness stakeholders who influence ordering and adoption. Since this is a global market, we made sure views were captured across APAC, EMEA, and the Americas to check utilization patterns, pricing logic, and what is considered in-scope versus adjacent preventive testing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | APAC: 41% |

| Mid tier: 46% | Functional/Unit leaders: 38% | EMEA: 36% |

| Smaller Players: 17% | Managers: 46% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where healthcare testing activity, preventive screening adoption, and the share of panels positioned as cellular health screening are used to reconstruct the addressable demand pool. Those totals are then stress-tested with selective bottom-up checks, like sampled price points by panel type, channel markups, and limited roll-ups of publicly visible supplier and lab revenues, which helped us correct for double counting.

Inputs used in the model include the mix shift from single-test to multi-test panels, typical biomarker group usage (such as oxidative stress, inflammation, telomere related markers, and heavy metals), sample type splits (blood, urine, and others), the share of at-home versus in-facility collection, and regional differences in preventive care spend. When a variable was not consistently available by country, we filled gaps using proxy indicators from comparable markets and then reviewed the implied results with interview feedback.

Forecasting uses scenario analysis supported by trend smoothing on core drivers, so near-term growth follows observed adoption, while medium-term growth reflects expected expansion of test menus and channel availability. We then align the final path with what experts consider reasonable for pricing progression and utilization growth in each region.

Data Validation & Update Cycle

Outputs are validated through repeated cross-checks against independent signals, such as reported lab testing volumes, public preventive screening indicators, and the implied revenue per test that falls out of the model. Any sharp year-to-year step changes are rechecked, and the assumptions behind them are reviewed by a second analyst before sign-off.

Reports are refreshed annually, and interim updates are made when material events change pricing, reimbursement direction, or test availability. Before delivery, a final review pass is completed so the latest public data and interview learnings are reflected in the numbers clients receive.

Mordor Intelligence's Cellular Health Screening Market Size Versus Other Published Estimates

Published market values for cellular health screening can look different because groups draw the line around what counts as a cellular panel, they pick different base years, and they handle pricing and test mix in their own way. Currency timing and how fast assumptions are refreshed also add to the spread, especially in a market that mixes wellness-led demand with lab processing economics.

The benchmark table shows a gap across the 2024 to 2026 reference points, and in Mordor Intelligence's model the 2026 total is built around cellular health screening panels and related lab services, rather than rolling in broader preventive diagnostics that are not marketed or ordered as cellular screening.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.78 B (2026) | |

| Industry Publisher A | USD 3.30 B (2024) | Uses an earlier base year and typically captures a wider biomarker testing basket tied to aging and wellness, which can pull in adjacent preventive diagnostics that are not always sold as cellular screening. |

| Global Publisher B | USD 3.59 B (2025) | Anchors the model in 2025 and may apply a different price progression and regional weighting, which changes the implied revenue per test when multi-panel adoption is rising. |

Taken together, the spread is mainly explained by scope boundaries, base-year selection, and how pricing and panel mix are treated during the forecast build. Our approach keeps the model traceable to clear demand signals and test economics, and then it is checked with real-world stakeholder feedback before totals are finalized.

Key Questions Answered in the Report

What is the current value of the cellular health screening market?

Sales reached USD 3.78 billion in 2026, with an expected rise to USD 5.65 billion by 2031.

Which region leads the cellular health screening market?

North America holds 37.30% of 2025 revenue, boosted by early DTC adoption and clear FDA guidance.

What segment is growing the fastest within this market?

Mitochondrial function assays record a 15.44% CAGR through 2031, the quickest among test types.

Why are saliva kits gaining popularity?

Saliva offers painless self-collection and ambient shipping, and new epigenetic clocks show strong accuracy correlation with blood tests.

How are regulations shaping market growth?

The FDA’s laboratory-developed-test rule and Europe’s IVDR raise quality standards, benefiting firms with robust compliance systems.

Which companies recently expanded their footprint?

Quest Diagnostics acquired LifeLabs in 2024, and Labcorp announced a 2025 deal for Incyte Diagnostics assets to enlarge regional coverage.

Page last updated on: