Global Hemato Oncology Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

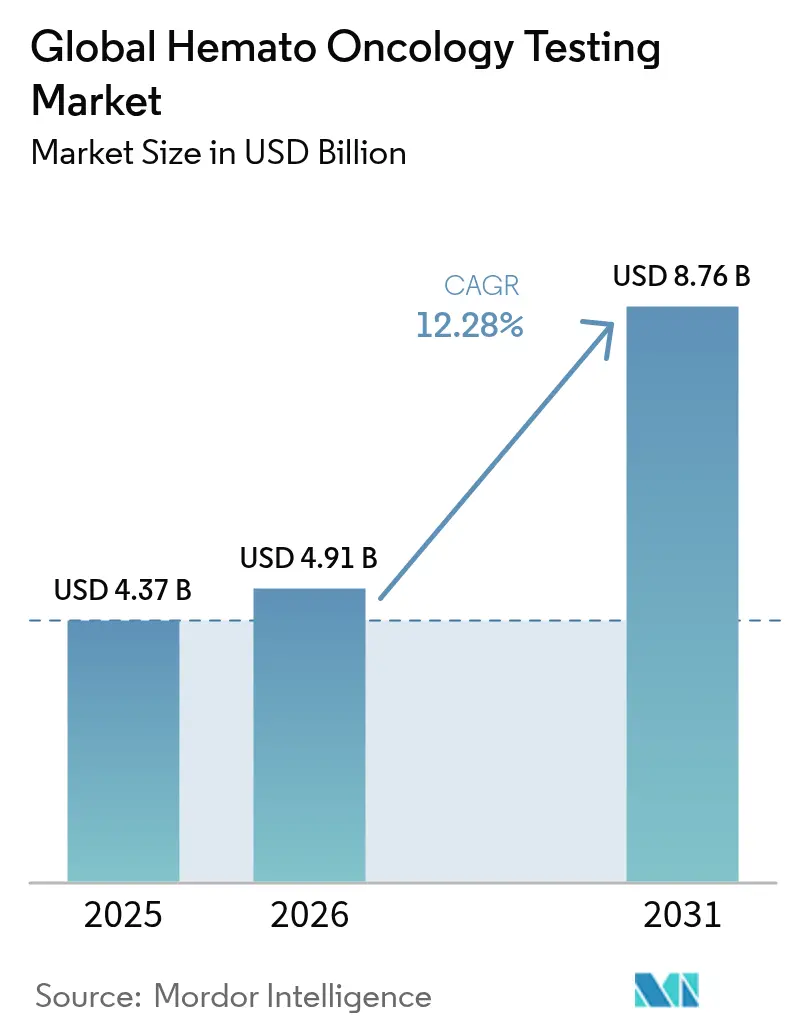

| Market Size (2026) | USD 4.91 Billion |

| Market Size (2031) | USD 8.76 Billion |

| Growth Rate (2026 - 2031) | 12.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

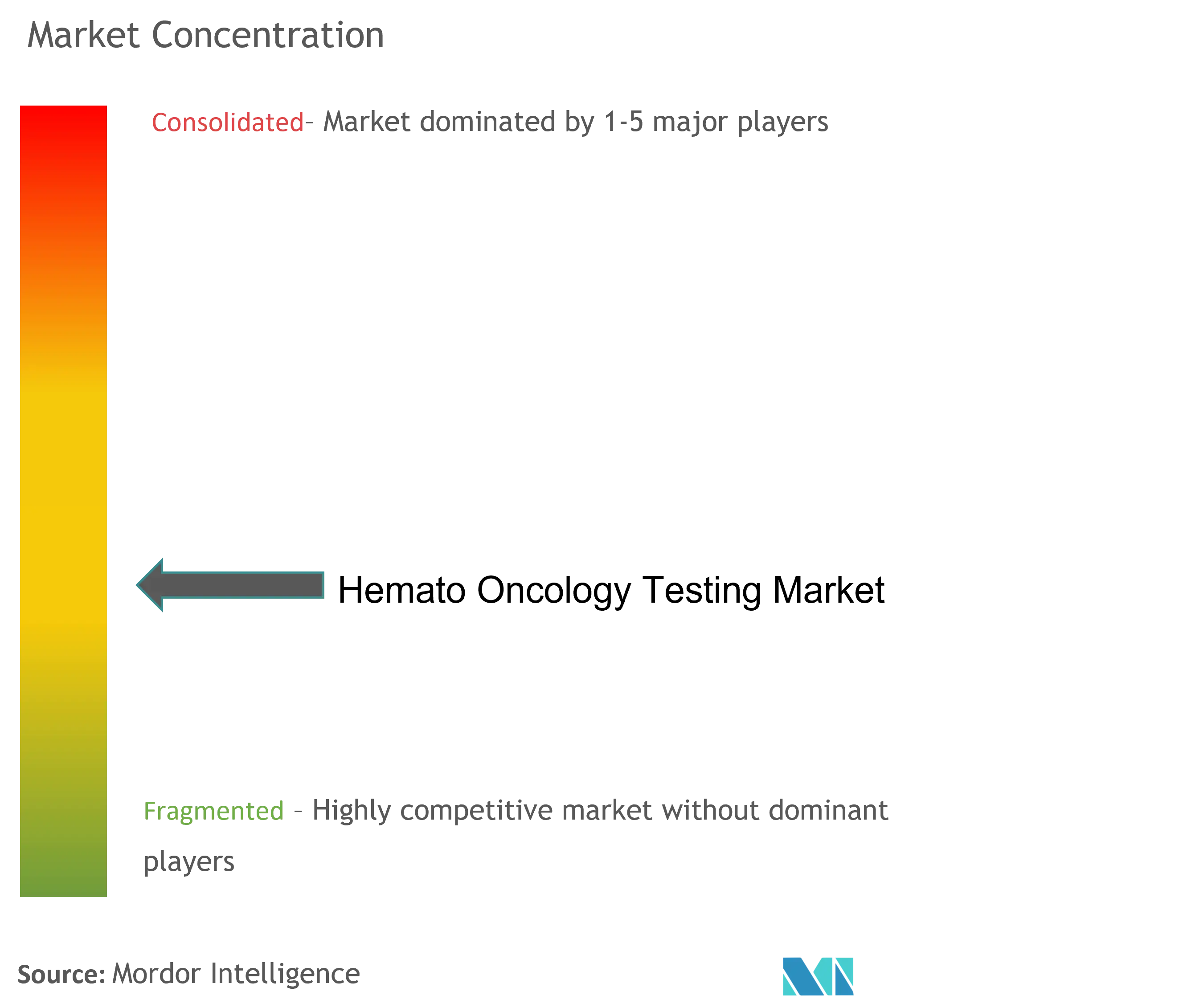

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Hemato Oncology Testing Market Analysis by Mordor Intelligence

hemato oncology testing market size in 2026 is estimated at USD 4.91 billion, growing from 2025 value of USD 4.37 billion with 2031 projections showing USD 8.76 billion, growing at 12.28% CAGR over 2026-2031. The expansion is powered by widespread adoption of artificial intelligence in diagnostic workflows, routine use of liquid biopsy, and the steady shift from first-generation genetic assays to standardised next-generation sequencing platforms. The FDA’s May 2025 decision to reclassify DNA-based minimal residual-disease (MRD) tests for hematological malignancies into Class II status reduces regulatory friction and accelerates commercial roll-out fda.gov. Heightened demand for comprehensive molecular profiling, coupled with growing physician confidence in non-invasive sampling, reinforces test utilisation across both community hospitals and specialist laboratories. In parallel, automation in cytogenetics, digital pathology, and cloud-based bioinformatics is improving laboratory throughput and lowering per-sample costs, sustaining double-digit revenue growth.

Key Report Takeaways

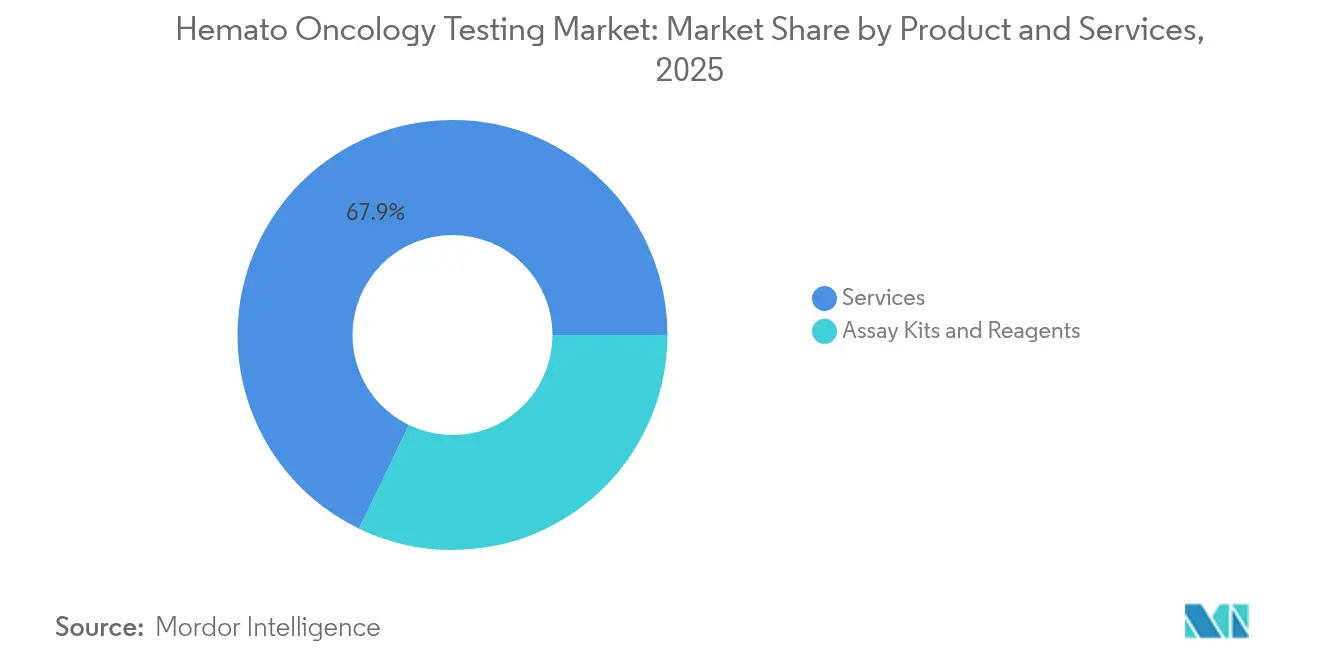

- By product & services, services led with 67.85% of the hemato oncology testing market share in 2025, whereas assay kits and reagents are projected to advance at a 12.79% CAGR through 2031.

- By cancer type, lymphoma testing commanded 40.37% of the hemato oncology testing market size in 2025, while leukemia testing is forecast to register the fastest 13.28% CAGR to 2031.

- By technology, PCR retained 42.75% of the hemato oncology testing market share in 2025; immunohistochemistry is expected to expand at a 13.66% CAGR during the outlook period.

- By end user, hospitals accounted for a dominant 56.92% share of the hemato oncology testing market size in 2025, yet reference and specialty laboratories are set for 13.34% CAGR growth.

- By geography, North America captured 41.80% revenue share in 2025, whereas Asia-Pacific is positioned to grow at 13.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemato Oncology Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of hematologic cancers | +2.8% | Global, with highest impact in aging populations of North America & Europe | Long term (≥ 4 years) |

| Growing demand for personalized therapy | +3.2% | North America & EU leading, APAC emerging | Medium term (2-4 years) |

| Advancements in molecular diagnostic technologies | +2.1% | Global, with R&D concentration in North America | Short term (≤ 2 years) |

| Rising adoption of non-invasive liquid biopsy | +1.9% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| AI-driven decision support in heme-oncology labs | +1.5% | North America & EU, selective APAC markets | Short term (≤ 2 years) |

| Decentralized PoC molecular platforms in emerging markets | +1.0% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Hematologic Cancers

Global burden studies show that multiple myeloma, acute myeloid leukemia, and diverse lymphoid neoplasms are climbing in prevalence as populations age and diagnostic programs improve case detection. Healthcare systems consequently face sustained demand for high-resolution molecular testing capable of revealing rare genotypes and complex structural variations. Third-generation sequencing already outperforms conventional methods in thalassemia screening, enabling earlier genetic counselling and prenatal decision making [1]SpringerOpen, “Advances in Molecular Cytogenetics for Haematology,” springeropen.com. With rising patient volumes, laboratories that deploy comprehensive genomic panels can provide faster, more precise classification, supporting treatment selection and monitoring. The hemato oncology testing market therefore benefits from a virtuous cycle of need, technology availability, and clinician acceptance.

Growing Demand for Personalized Therapy

Precision oncology is reshaping treatment pathways as companion diagnostics link molecular findings to targeted drugs, immunotherapies, and cell-based interventions. The FDA’s August 2024 approval of Illumina’s TruSight Oncology Comprehensive assay, the first pancancer test with claims covering more than 500 genes, underscores regulator readiness to endorse broad panels. Cost-effectiveness studies further indicate that upfront NGS profiling reduces overall spend by eliminating ineffective treatments and shortening time to optimal therapy. As payers increasingly integrate real-world evidence, molecular testing transitions from optional work-up to standard of care, enlarging the addressable base for the hemato oncology testing market.

Advancements in Molecular Diagnostic Technologies

AI-assisted flow cytometry now differentiates B-cell and T-cell malignancies with recall and precision that rival expert haematopathologists, shortening reporting times and reducing inter-reader variability [2]HemaSphere Editorial Board, “Artificial Intelligence in Flow Cytometry,” hematologylibrary.org. In cytogenetics, automated harvesters and chilled slide processors cut technologist time while improving chromosome-level image quality, directly addressing staffing shortages. Digital pathology platforms that fuse whole-slide images with genomic metadata generate multimodal dashboards that help clinicians visualise tumour biology. Such integrated toolchains enable laboratories to absorb higher case volumes without sacrificing analytical depth, reinforcing the high-growth outlook for the hemato oncology testing market.

Rising Adoption of Non-Invasive Liquid Biopsy

Bone-marrow aspiration and trephine biopsies carry discomfort and procedural risk. By contrast, cell-free DNA assays capture clonal profiles from peripheral blood, supporting early diagnosis, MRD surveillance, and relapse prediction with comparable sensitivity. Peer-reviewed studies show that circulating tumour DNA often detects actionable mutations sooner than standard microscopy [3]Frontiers Editorial Office, “Circulating DNA in Hematologic Malignancies,” frontiersin.org. Emerging assays that combine cell-free RNA with DNA reveal transcriptomic shifts alongside genomic variants, offering clinicians a single test that informs on disease evolution and treatment response. Wider use of liquid biopsy aligns with patient preferences, accelerates serial monitoring, and ultimately enlarges revenue opportunities for the hemato oncology testing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unfavorable reimbursement scenario | -2.5% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| High cost of next-generation sequencing tests | -1.8% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Shortage of skilled molecular pathologists | -1.4% | Global, acute in sub-Saharan Africa & rural areas | Long term (≥ 4 years) |

| Genomic-data interoperability & cybersecurity gaps | -0.9% | Global, regulatory focus in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unfavorable Reimbursement Scenario

CMS data reveal Medicare denial rates for laboratory NGS claims climbed from 16.8% to 27.4% after 2020 coverage adjustments, with independent labs disproportionately affected. Commercial insurers have added precertification hurdles such as Z-codes, lengthening claim cycles and introducing administrative overhead. Laboratories often subsidise unreimbursed tests to maintain clinician relationships, pressuring margins. These dynamics moderate near-term cash inflows and temper adoption in cost-sensitive settings, placing a drag on the hemato oncology testing market.

Shortage of Skilled Molecular Pathologists

A workforce analysis covering 162 countries documents only 14 practising pathologists per million population, with severe shortages in sub-Saharan Africa and parts of Latin America. In the United States, vacancy rates for molecular technologist posts rose in 2024 despite aggressive recruitment incentives, and burnout remains a recognised risk factor for early retirement. Limited personnel hampers the speed at which laboratories can implement sophisticated assays, constraining throughput in regions already facing case backlogs. Unless training pipelines expand, tight labour supply may curb the long-term addressable volume for the hemato oncology testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Services: Services Drive Market Leadership

Services contributed 67.85% revenue in 2025, making them the single largest slice of the hemato oncology testing market. Hospital networks, community clinics, and pharma sponsors rely on specialised service providers for end-to-end workflows that span sample logistics, nucleic-acid extraction, sequencing, bioinformatics, and variant curation. The segment’s high share reflects the capital intensity of molecular laboratories and the scarcity of in-house expertise. In value terms, this leadership translates into USD 2.97 billion of the 2025 hemato oncology testing market size. Market outlook remains strong as laboratories outsource overflow volumes to combat staff shortages and reduce turnaround-time penalties.

Assay kits and reagents, although smaller, exhibit a 12.79% CAGR through 2031, the fastest within the product grid. Growth centres on multiplex PCR panels, single-tube library prep chemistries, and lyophilised reagents that support field deployment. Firms such as QIAGEN announced sample-to-result platforms that integrate extraction and assay setup, enhancing consistency and lowering operator error. These improvements encourage smaller laboratories to launch molecular menus, adding incremental volume to the hemato oncology testing market.

By Cancer Type: Lymphoma Leadership Amid Leukemia Acceleration

Lymphoma testing held 40.37% of the hemato oncology testing market share in 2025, reflecting the diverse spectrum of Hodgkin and non-Hodgkin entities that each demand immunophenotyping, gene rearrangement studies, and mutational panels. The downstream linkage to antibody-drug conjugates and CAR-T therapies further entrenches comprehensive testing as a clinical imperative. Consequently, lymphoma accounted for USD 1.76 billion of the 2025 hemato oncology testing market size.

Leukemia testing, while smaller, grows at 13.28% CAGR as MRD surveillance becomes standard of care. FDA-cleared assays such as clonoSEQ enable quantitative tracking of residual clones, guiding therapy adjustment and transplant planning. Liquid biopsy approaches that monitor nucleosomal DNA fragmentation promise earlier relapse detection. As payers recognise the prognostic value of serial monitoring, volume growth in leukemia tests will meaningfully lift overall revenue for the hemato oncology testing market.

By Technology: PCR Dominance Challenged by IHC Innovation

PCR contributed 42.75% of 2025 revenue, underlining its status as a laboratory workhorse for fusion gene detection, copy-number analysis, and pathogen screening. The entrenched install base, low cost per reaction, and regulatory familiarity reinforce ongoing demand. Against this backdrop, PCR captured USD 1.87 billion within the 2025 hemato oncology testing market size.

Immunohistochemistry (IHC) is poised for a 13.66% CAGR through 2031 as multiplexed antibody panels and automated stainers elevate diagnostic throughput. Recent advances allow simultaneous visualisation of up to nine markers on a single slide, delivering richer phenotypic context for haematopathologists. AI-based image analytics extract quantitative parameters, rescuing information that manual reads can miss, and thereby justify premium reimbursement. The resulting productivity gains and clinical value position IHC as a credible challenger to PCR within the hemato oncology testing market.

By End User: Hospital Dominance Amid Laboratory Specialisation

Hospitals generated 56.92% of 2025 billings, a testament to their gatekeeper role in oncology care. Integrated test-and-treat models allow oncologists to order molecular panels and act on results within the same facility, reinforcing hospital stickiness. Hospital expenditure reached USD 2.49 billion in the 2025 hemato oncology testing market size.

Reference and specialty laboratories, however, advance at a 13.34% CAGR by offering deep assay menus and robust logistics. Partnerships such as Labcorp–Ascension illustrate mutually beneficial outsourcing, where health-system staff shortages are offset by external capacity while Labcorp gains sample inflow. Similar tie-ups in Africa, supported by grants from diagnostic vendors, demonstrate how external expertise can expand access to complex tests. These collaborative models should steadily lift the volume processed by independent labs, expanding the hemato oncology testing market.

Geography Analysis

North America led with 41.80% revenue share in 2025 as mature reimbursement structures and early technology adoption sustained high test utilisation. Despite rising Medicare denials, the United States continues to approve new assays rapidly, including Class II MRD devices that shorten time-to-market. Laboratory consolidation, exemplified by BioReference Health asset acquisitions, yields economies of scale that protect margins. Canada’s provincial health systems are introducing centralised genomic programmes, and Mexico’s private sector is scaling liquid biopsy services for medical tourism. Together, these dynamics support mid-single-digit growth in an otherwise saturated segment of the hemato oncology testing market.

Asia-Pacific is the most dynamic region, posting a 13.9% CAGR forecast to 2031. Government initiatives in China, Japan, and India fund laboratory modernisation and subsidise molecular panels as standard care. Sysmex recorded a 119.2% increase in regional hematology revenue during the first quarter of fiscal 2025, underscoring export demand for advanced analysers. Regulatory frameworks are converging toward IVD harmonisation, trimming approval times and stimulating local production. Southeast Asian countries employing decentralised point-of-care PCR platforms are leapfrogging legacy infrastructure, registering new test volumes that lift the hemato oncology testing market across the region.

Europe maintains balanced growth as public payers weigh cost-effectiveness carefully. Pan-EU initiatives encourage data interoperability, facilitating cross-border clinical trials and reference-lab collaborations. Germany and France are enlarging reimbursement codes for NGS panels, and the United Kingdom’s Genomic Medicine Service continues to add haematology indications. Eastern European health ministries fund tele-pathology pilots that connect local hospitals with central expertise, modestly raising per-capita test rates. Meanwhile, the Gulf Cooperation Council states invest in high-end oncology centres that import US- and EU-cleared assays, and South Africa positions itself as a sub-Saharan reference hub. Collectively, these trends sustain broad geographical diversity and underpin the global expansion of the hemato oncology testing market.

Competitive Landscape

The hemato oncology testing market is moderately fragmented, with the top five companies controlling an estimated 48% of 2024 revenue. Large integrated players combine reagent portfolios, sequencing platforms, and accredited service labs to deliver turnkey solutions that ease adoption barriers. Smaller innovators compete by focusing on liquid biopsy, AI-enabled informatics, or microfluidic sample prep. Competitive intensity has sharpened because technical advances reach the market faster following FDA’s Class II reclassification and evolving EU IVDR pathways.

Strategic alliances remain a principal growth lever. Adaptive Biotechnologies and NeoGenomics signed an exclusive MRD monitoring pact, pooling a proprietary T-cell receptor assay with a national laboratory network to widen test access. Agilent partnered with Incyte to develop companion diagnostics aligning with pipeline drugs, expanding Agilent’s IVD footprint. Servier and QIAGEN plan a PCR-based IDH1 companion test that promises rapid turnaround for AML care. Acquisitions also shape supply: Labcorp absorbed Incyte Diagnostics’ clinical testing business to deepen oncology competence, while several regional labs merged to achieve reimbursement clout.

Technology differentiation is increasingly data-centric. Vendors tout encrypted cloud repositories that comply with the NIST genomic data cybersecurity framework, an attribute that resonates with hospital privacy officers. AI algorithms embedded within digital pathology viewers help new entrants punch above their weight by automating routine classification tasks. Meanwhile, incumbents leverage scale to bundle instrumentation, reagents, and analytics into subscription models that lock-in customers. Price competition is muted as buyers value turnaround time and clinical sensitivity over unit cost, allowing vendors to preserve healthy margins and reinvest in R&D that sustains innovation within the hemato oncology testing market.

Global Hemato Oncology Testing Industry Leaders

Abbott

QIAGEN

F. Hoffmann-La Roche Ltd

Illumina Inc.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Agilent Technologies entered an agreement with Incyte to co-develop companion diagnostics across the latter’s hematology and oncology portfolio.

- December 2023: Huntsman Cancer Institute reported that NGS reliably predicts relapse risk in paediatric malignancies, supporting broader adoption in children’s oncology programmes.

- March 2023: Servier and QIAGEN began a strategic partnership to create a PCR-based companion diagnostic for IDH1-mutated AML, aiming for rapid lab turnaround and global distribution.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the hemato-oncology testing market as the collective revenue generated by molecular and immunohistochemical assays that detect, classify, and monitor blood-related malignancies such as leukemia, lymphoma, and multiple myeloma across clinical laboratories, hospital labs, and specialty reference centers worldwide. Tests in scope include PCR, NGS, cytogenetic, flow-based, and IHC panels used during diagnosis, treatment selection, minimal-residual-disease tracking, or relapse surveillance. According to Mordor Intelligence, this market was valued at USD 4.37 billion in 2025 and is projected to reach USD 7.87 billion by 2030.

Scope exclusion: routine complete-blood-count analyzers and generic hematology reagents that do not interrogate oncogenic biomarkers are left outside the present definition.

Segmentation Overview

- By Product & Services

- Assay Kits & Reagents

- PCR assay kits

- NGS panels & library prep kits

- IHC/Flow-cytometry reagents

- Services

- Assay Kits & Reagents

- By Cancer Type

- Leukemia

- Lymphoma

- Multiple Myeloma

- Other Hematologic Malignancies

- By Technology

- Polymerase Chain Reaction (PCR)

- Next-Generation Sequencing (NGS)

- Immunohistochemistry (IHC)

- Flow Cytometry

- Other Technologies

- By End User

- Hospitals

- Reference & Specialty Laboratories

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Insights from oncologists, molecular pathologists, lab procurement managers, and IVD product specialists across North America, Europe, Asia Pacific, and Latin America help validate incidence-to-testing conversion ratios, average selling prices, and likely adoption pacing of newer NGS panels. Follow-up surveys clarify reimbursement friction points and service mix shifts.

Desk Research

Mordor analysts begin with structured desk research that taps non-paywalled tier-1 sources such as the World Health Organization's GLOBOCAN registry, Surveillance Epidemiology and End Results databases, Eurostat cancer incidence files, and regional guidelines from NCCN and ESMO. Laboratory reimbursement fee schedules, patent filings pulled via Questel, and import-export traces from Volza supply foundational data on assay volumes and pricing. Company 10-Ks, investor decks, and peer-reviewed journals further refine technology adoption curves. This list is illustrative, and many additional open datasets inform the evidence pool.

Market-Sizing & Forecasting

A top-down incidence-based demand pool is first built by pairing country-level leukemia and lymphoma caseloads with guideline-mandated test frequencies. Results are cross-checked through selective bottom-up supplier revenue tallies and channel checks, which adjust for self-testing overlap and send-out volumes. Key variables feeding the model include annual hematologic cancer incidence, percentage of patients staged with molecular panels, median number of follow-up tests per therapy line, reference-lab penetration rates, and average panel prices. Multivariate regression with scenario analysis projects each driver to 2030, while gap areas in bottom-up estimates are bridged using benchmark ASP × volume triangulation.

Data Validation & Update Cycle

Outputs undergo consistency scans against external epidemiology trends and quarterly IVD revenue disclosures. Senior reviewers address anomalies before sign-off. Reports refresh yearly, with interim updates triggered by regulatory approvals, reimbursement shifts, or material M&A events, ensuring clients always receive the latest vetted view.

Why Mordor's Hemato Oncology Testing Baseline Deserves Trust

Published market values can differ because firms apply varying test scopes, pricing ladders, incidence datasets, and refresh cadences. Readers therefore meet divergent numbers when comparing providers.

Key gap drivers include whether benign hematology assays are bundled, how aggressively future ASP erosion is modeled, differences in assumed test frequency beyond first-line diagnosis, currency conversion dates, and the cadence of methodological updates that freeze or refresh data mid cycle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.37 B (2025) | Mordor Intelligence | - |

| USD 3.60 B (2024) | Global Consultancy A | Includes fewer follow-up tests and applies steeper ASP erosion |

| USD 3.20 B (2023) | Industry Association B | Excludes NGS service revenues and relies on static incidence figures |

These comparisons show that Mordor's balanced scope, annually refreshed incidence data, and dual-path validation deliver a dependable baseline that executives can trace back to transparent variables and repeatable steps.

Key Questions Answered in the Report

What is the current Global Hemato Oncology Testing Market size?

The hemato oncology testing market size is USD 4.91 billion in 2026, rising to USD 8.76 billion by 2031 on a 12.28% CAGR trajectory.

Who are the key players in Global Hemato Oncology Testing Market?

Abbott, QIAGEN, F. Hoffmann-La Roche Ltd, Illumina Inc. and Thermo Fisher Scientific Inc. are the major companies operating in the Global Hemato Oncology Testing Market.

Which is the fastest growing region in Global Hemato Oncology Testing Market?

A-Pacific is projected to expand at 13.9% CAGR through 2031, driven by infrastructure upgrades and supportive regulations.

Which region has the biggest share in Global Hemato Oncology Testing Market?

In 2025, the North America accounts for the largest market share in Global Hemato Oncology Testing Market.

Page last updated on: