HERG Screening Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

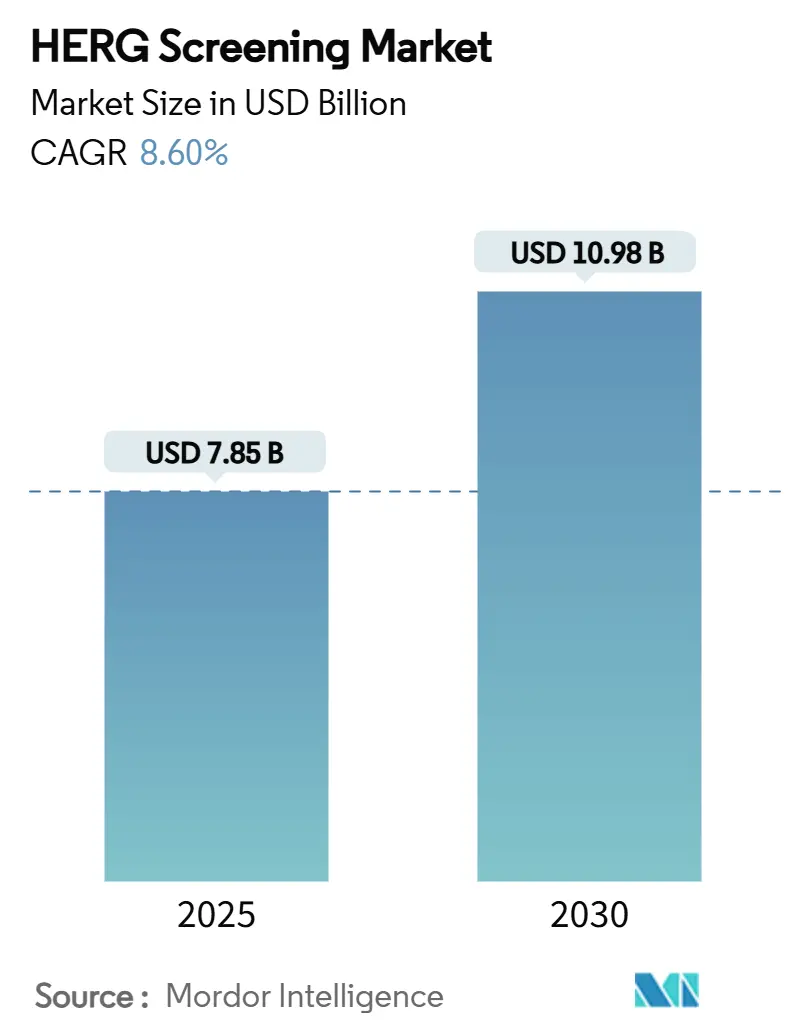

| Market Size (2025) | USD 7.85 Billion |

| Market Size (2030) | USD 10.98 Billion |

| Growth Rate (2025 - 2030) | 8.60% CAGR |

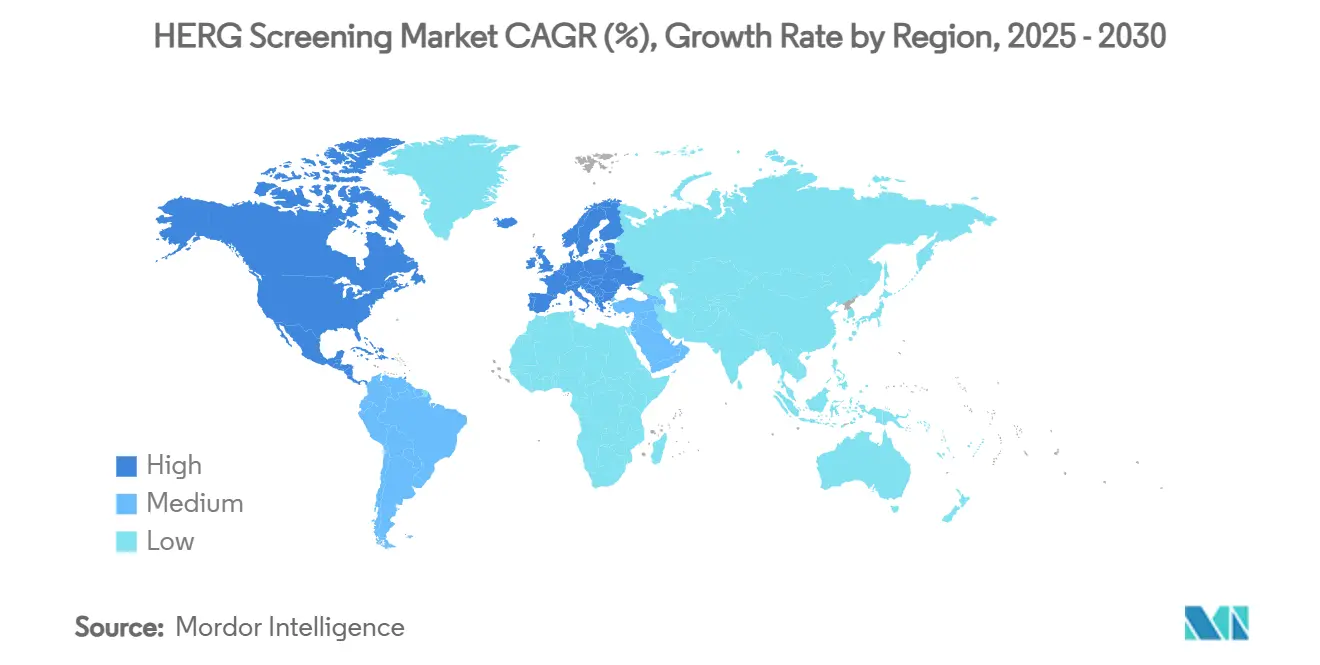

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HERG Screening Market Analysis by Mordor Intelligence

The hERG screening market size stands at USD 7.85 billion in 2025 and is forecast to reach USD 10.98 billion by 2030, expanding at a 8.60% CAGR. Strong growth is powered by mandatory cardiac safety regulations, a record wave of pharmaceutical R&D spending, and high-throughput automated patch-clamp platforms that push daily screening capacity beyond 6,000 data points. Pharmaceutical companies are front-loading cardiotoxicity testing to avoid the USD 2.2 billion average late-stage drug failure cost, while the Comprehensive in vitro Proarrhythmia Assay (CiPA) framework keeps hERG as the anchor of a seven-channel panel. The rapid pairing of artificial intelligence with automated electrophysiology now enables real-time quality control and predictive ranking of compound libraries. Contract research organizations (CROs) are scaling capacity through acquisition programs that add specialized hERG infrastructure across North America, Europe, and Asia Pacific. Asia Pacific CROs are gaining share as global sponsors redirect work to cost-competitive, quality-accredited laboratories that meet ICH E14 and S7B requirements.

Key Report Takeaways

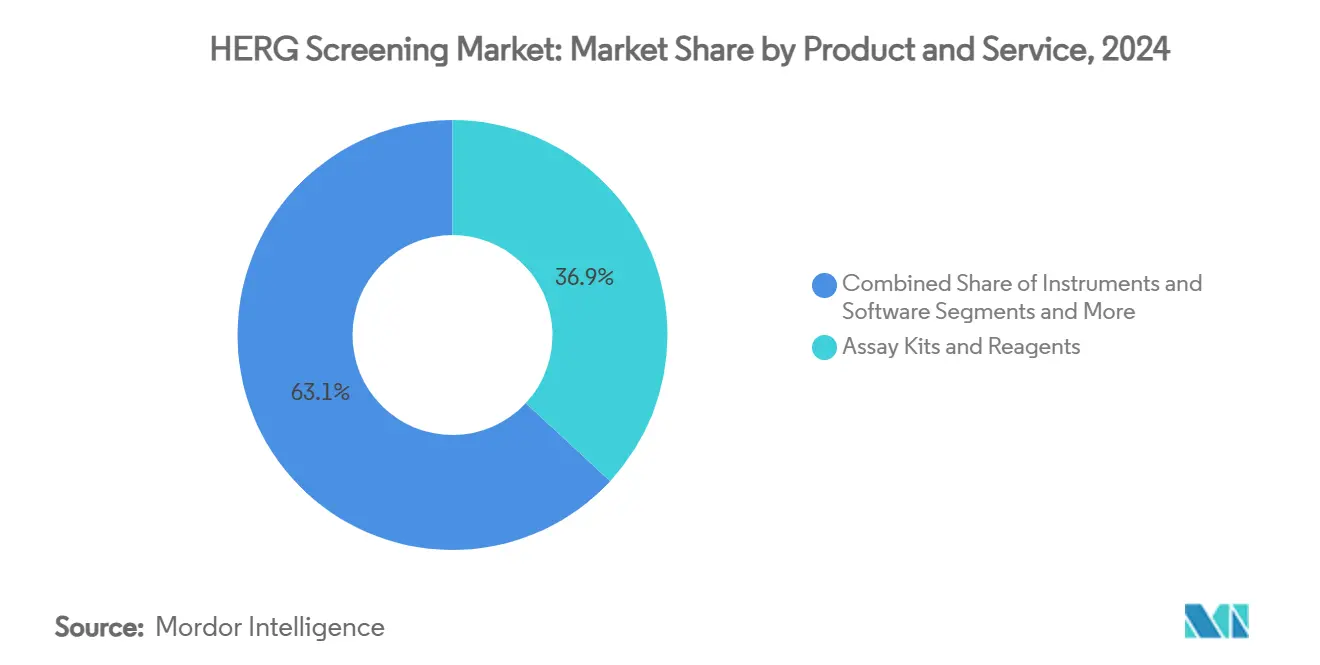

- By product & service, assay kits & reagents captured 36.9% of the hERG screening market share in 2024, while Contract Screening Services are advancing at an 11.8% CAGR to 2030.

- By assay type, automated patch clamp held 38.1% revenue share in 2024; In-silico/In-vitro Hybrid Models are projected to grow at a 14.1% CAGR through 2030.

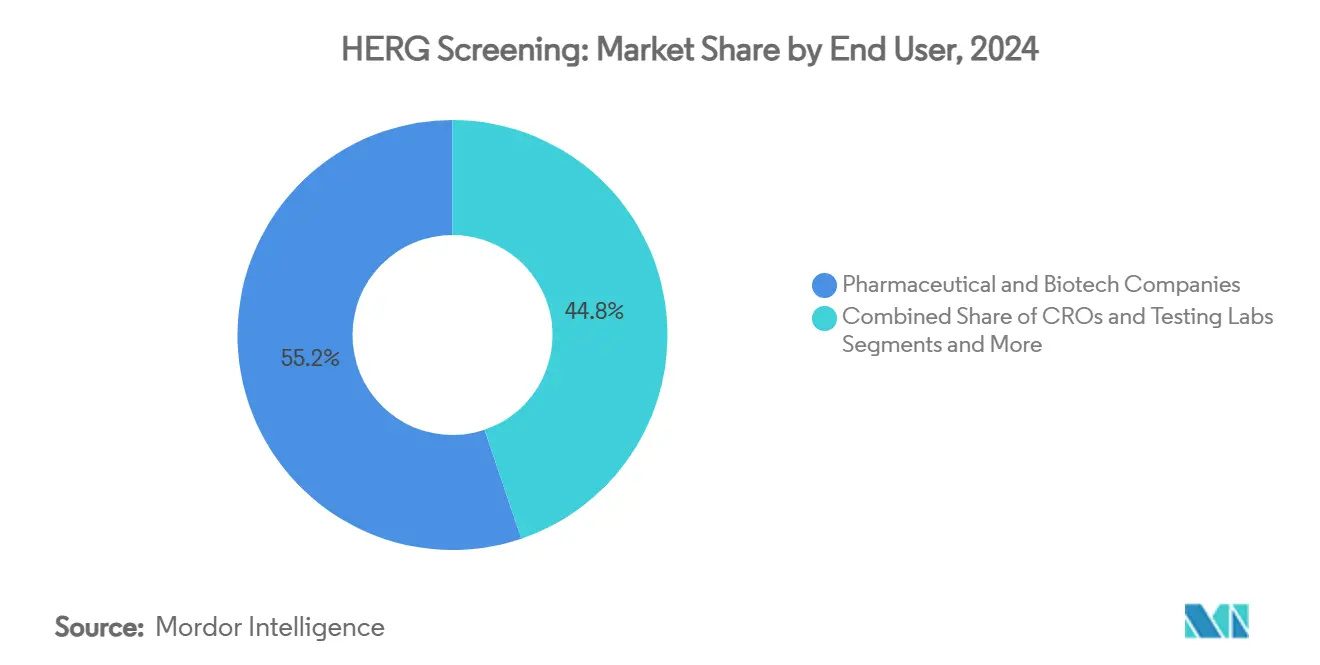

- By end user, pharmaceutical & biotech companies accounted for 55.2% of the hERG screening market size in 2024, whereas CROs & Testing Labs lead growth at a 10.7% CAGR.

- By ion-channel panel, hERG-only protocols represented 48.2% share in 2024; Comprehensive CiPA Panels are forecast to expand at a 13.7% CAGR.

- By geography, North America dominated with a 38.7% share in 2024, and Asia Pacific is on track for a 9.5% CAGR to 2030.

Global HERG Screening Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened regulatory focus on cardiac safety (ICH E14/S7B, CiPA) | +3.20% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rising pharma R&D spend & cost of late-stage attrition | +2.80% | Global, concentrated in major pharma markets | Long term (≥ 4 years) |

| Technology advances in automated patch-clamp platforms | +2.10% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Broader CiPA multi-ion panel adoption | +1.90% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-enabled in-silico cardiotoxicity prediction models | +1.60% | Global, with concentration in tech-advanced markets | Long term (≥ 4 years) |

| iPSC-derived cardiomyocyte assays gaining traction | +1.40% | Global, led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Regulatory Focus on Cardiac Safety (ICH E14/S7B, CiPA)

Worldwide regulators now require mechanistic proarrhythmia risk assessments that keep hERG current block as the critical gatekeeper of cardiac safety. The CiPA paradigm embeds hERG in a multiparametric seven-channel panel, compelling sponsors to pair hERG data with Nav1.5 and Cav1.2 results for more granular predictions. FDA guidance issued in 2024 clarified that peptide and protein therapeutics with naturally occurring amino acids may forgo thorough QT studies, creating service niches that tailor hERG testing to small-molecule pipelines.[1]Regulatory Decision-Making for Drug and Biological Products,” fda.gov Harmonization between the FDA and the European Medicines Agency accelerates global uptake of CiPA-aligned assays that integrate automated patch-clamp and in silico models for submission dossiers. Small and mid-sized biopharma companies lacking electrophysiology capacity are increasingly outsourcing to CROs that offer validated CiPA-ready hERG workflows. Continuous updates to question-and-answer documents under ICH S7B keep the market in a cycle of equipment upgrades and staff training.

Rising Pharma R&D Spend and Cost of Late-Stage Attrition

Global pharmaceutical R&D outlays jumped 50% between 2018 and 2024 and topped USD 161 billion in 2024, reinforcing early-stage cardiac safety screens as insurance against billion-dollar setbacks. hERG blocking remains the chief root of torsade de pointes liability, so management teams approve higher upfront budgets for comprehensive screens that flag liabilities before IND submission. Improved R&D returns to 5.9% in 2024 coincide with the wider use of hERG data to down-select leads, shortening development cycles. As modality diversity grows, first-in-class assets with unfamiliar target spectra must pass robust hERG panels to secure venture rounds and partnership deals. The dynamic fuels sustainable demand for consumables and high-throughput instrumentation even during macroeconomic slowdowns.

Technology Advances in Automated Patch-Clamp Platforms

Third-generation automated patch-clamp systems deliver hERG success rates above 79% and daily throughputs topping 6,000 recordings, a scale impossible with manual rigs.[2]Li Tianbo et al., “High-throughput electrophysiological assays for voltage-gated ion channels,” journals.plos.org Temperature-controlled current-clamp modes replicate physiological conditions and sharpen IC50 precision, raising confidence in negative predictive value. AI-enhanced quality metrics flag seal drops and unstable currents in real time, letting operators reject compromised traces before data export. Consumable cartridges have higher cell-catch success and lower resistance variability, driving cost per data point down yet safeguarding trace fidelity. Equipment suppliers differentiate with intuitive GUIs and open-access SDKs that link directly into corporate compound-management systems. Broadening user profiles now encompass biotech start-ups and translational academic centers that run hERG assays to attract pharmaceutical partnerships.

Broader CiPA Multi-Ion Panel Adoption

Pharmaceutical programs applying CiPA panels report a marked reduction in false-positive terminations versus legacy hERG-only approaches.[3]J. Finkle et al., “Rechanneling the Cardiac Proarrhythmia Safety Paradigm: A Meeting Report from the Cardiac Safety Research Consortium,” American Heart Journal, sciencedirect.com hERG remains the most predictive single assay, but its integration with NaV1.5 and CaV1.2 data improves specificity and informs structure–activity redesign cycles. Early adopters note smoother global filings because one harmonized panel satisfies multiple agencies, cutting redundant animal studies. CROs respond by embedding hERG capacity into turnkey CiPA suites that combine automated patch-clamp, optical mapping, and in silico modeling validated under FDA AI guidance. Suppliers of reagents and cell lines enjoy recurring sales as laboratories expand beyond a single channel into full cardiac ion repertoires.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & running costs of HT electrophysiology systems | -1.80% | Global, particularly impacting smaller companies | Short term (≤ 2 years) |

| Shortage of skilled electrophysiologists | -1.40% | Global, acute in emerging markets | Medium term (2-4 years) |

| False-positive/negative rates causing pipeline losses | -1.20% | Global, concentrated in early-stage drug development | Medium term (2-4 years) |

| Lack of inter-platform data standardization | -0.90% | Global, affecting multi-site pharmaceutical companies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Running Costs of HT Electrophysiology Systems

State-of-the-art automated patch-clamp units optimized for hERG screening sell for several hundred thousand USD and require consumables that can exceed USD 50,000 each year. Smaller drug developers cannot justify that burden and often redirect budgets to fee-for-service CROs, dampening direct instrument sales but boosting outsourcing volume. Single-use chips and specialty cell lines remain sizeable ongoing expenses even for high-volume labs, so total cost of ownership can deter facility expansion in cost-sensitive regions. Vendors attempt to ease adoption by rolling out lease and pay-per-data-point models, yet these options still carry minimum usage commitments that some biotechs find restrictive. High-end rigs also need dedicated temperature-controlled rooms and uninterrupted power supplies, pushing infrastructural barriers higher in emerging markets.

Shortage of Skilled Electrophysiologists

Despite automation, data interpretation and troubleshooting still rely on experts versed in hERG kinetics and gating artifacts. Global demand outstrips supply, and top talent commands premium salaries that inflate operating costs for both sponsors and CROs. Academic curricula lag behind industry needs, so on-the-job training often stretches six months or more before analysts are fully productive. Talent scarcity is most acute in Asia Pacific, where rapid outsourcing growth outpaces regional workforce development. Competition among CROs for senior electrophysiologists drives staff turnover, forcing companies to set up retention bonuses and career development programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Reagents Dominate, Services Accelerate

Assay Kits & Reagents generated 36.9% of the hERG screening market size in 2024, underscoring the consumable nature of ion-channel experiments that require stable cell lines, test compounds, and low-noise solutions on a continual basis. Recurring sales provide predictable annuity income for suppliers, while constant optimization of buffer chemistries and reference blockers supports price premiums. Contract Screening Services grow fastest at an 11.8% CAGR as sponsors outsource electrophysiology to laboratories with validated CiPA workflows that bundle hERG with six other cardiac channels.

Pharmaceutical teams cite speed-to-data and regulatory credibility as primary reasons to contract external providers, shifting capital expenditure into operating expense lines. Service vendors differentiate through AI-augmented analytics platforms, twenty-four-hour global project tracking, and integrated toxicology suites that convert raw hERG traces into submission-ready reports. Continued expansion of CRO footprints in Asia Pacific offers cost benefits without compromising ICH compliance, deepening outsourcing momentum.

By Assay Type: Automation Leads, Hybrid Models Surge

Automated Patch Clamp accounted for 38.1% revenue share in 2024, confirming its role as the benchmark for quantitative hERG block data that regulators accept without reservation. Throughput gains and lower failure rates now let single instruments process 60 compounds per hour, shrinking screening backlogs during lead optimization. In-silico/In-vitro Hybrid Models rise at a 14.1% CAGR as machine learning classifiers trained on historical hERG datasets triage libraries, so only high-risk chemotypes proceed to electrophysiology benches.

Integration of computational filters reduces consumable spend, maximizes machine utilization, and accelerates design–make–test cycles. The FDA draft guidance published in January 2025 outlines credibility frameworks for AI models, encouraging broader submission use and widening the addressable market for hybrid tool providers. Manual patch-clamp persists for niche mechanistic studies, while fluorescence-based assays cover cost-effective primary screens that guide medicinal chemistry away from cation-binding motifs.

By End User: Pharma Dominates, CROs Accelerate

Pharmaceutical & Biotech Companies represented 55.2% of total demand in 2024, reflecting their regulatory obligation to submit hERG data packages with every new therapeutic candidate. These organizations often run confirmatory tests internally then outsource high-volume structure–activity screens to external partners. CROs & Testing Labs, the fastest-growing cohort at a 10.7% CAGR, extend capacity with dedicated CiPA suites that integrate automated patch-clamp and high-content cardiomyocyte imaging under a single quality system.

Academic and translational institutes help drive innovation in assay formats and ion-channel target identification, although their spending is smaller in absolute terms. They frequently collaborate with instrument vendors to validate emerging sensing modalities such as optogenetic pacing that could complement the classical voltage clamp.

By Ion-Channel Panel: hERG Legacy, CiPA Future

hERG-Only protocols retained a 48.2% share in 2024 because historical datasets, validated SOPs, and risk-based submissions still rely heavily on IC50 thresholds. However, the comprehensive CiPA panel segment expands at 13.7% CAGR, reflecting sponsor preference for one harmonized package that satisfies regulators across regions. Multi-ion panels embed hERG alongside NaV1.5, CaV1.2, and late Na+ currents, generating layered decision matrices that cut false positives.

Laboratories offering turnkey CiPA packages command premium pricing given the complexity of coordinating seven channels, integrated in silico modeling, and stem-cell cardiomyocyte action-potential reconstruction. Suppliers of CiPA-qualified cell lines and reference compounds secure recurring revenue as each panel multiplies consumable demand versus single-channel screens.

Geography Analysis

North America controlled 38.7% of the hERG screening market in 2024 thanks to the FDA’s early adoption of CiPA and the region’s dense cluster of large pharmaceutical R&D hubs. Continuous guidance updates on AI use in drug submissions keep domestic laboratories at the forefront of hybrid hERG prediction models. CRO conglomerates headquartered in the United States deploy acquisition strategies that integrate smaller electrophysiology specialists, strengthening full-service packages for global clients.

Europe follows closely with well-funded life-science corridors in Germany, France, and the United Kingdom that invest in automated patch-clamp upgrades and iPSC-derived cardiomyocyte platforms. EMA alignment with FDA mechanistic expectations streamlines pan-Atlantic development programs and stabilizes demand for harmonized CiPA-ready hERG panels. Academic institutes in the Netherlands and Denmark publish seminal work on ion-channel kinetics that feeds directly into assay protocol refinement.

Asia Pacific is the fastest-advancing region at a 9.5% CAGR, propelled by CRO giants that combine scale with competitive pricing. Chinese and Indian laboratories earn GLP accreditation and adopt 768-well automated patch-clamp systems to capture outsourced Western pipelines while supporting a growing domestic innovation scene. Japanese pharma invests heavily in hybrid in silico and in vitro hERG toolkits to accelerate specialty indications such as rare cardiac channelopathies. Government incentives for high-value biologics manufacturing in Singapore and South Korea further lift regional demand for CI-qualified cardiac safety data packages.

Competitive Landscape

The hERG screening market shows moderate fragmentation as roughly two dozen significant players compete on technology depth, regulatory track record, and geographic penetration. Platform specialists such as Nanion Technologies and Sophion Bioscience release incremental hardware upgrades, adding temperature control and advanced voltage protocols that yield cleaner hERG traces. Full-service CROs, including Charles River Laboratories and Eurofins Scientific, pursue bolt-on acquisitions that broaden electrophysiology footprints and enhance data analytics depth.

Three strategy archetypes emerge. First, instrument innovators chase performance leadership to lock in reagent sales and maintenance contracts. Second, vertically integrated CROs package hERG within IND-to-NDA toxicology suites, appealing to mid-cap biotech firms that prize single-vendor accountability. Third, boutique laboratories carve niches in AI-enabled hERG liability mitigation, offering rapid synthesis and screening loops that slide seamlessly into medicinal chemistry workflows. White-space opportunities revolve around gene and cell-therapy modalities, where unorthodox vectors may interact with hERG in ways that legacy screens cannot fully predict.

Integration of cloud-hosted data lakes and secure client portals has become a key differentiator, enabling real-time review of hERG traces and AI interpretive dashboards. Suppliers that certify cybersecurity compliance gain an edge with European customers bound by GDPR. Talent retention programs, including graduate academies for electrophysiology, are now standard among market leaders to counteract the global skills gap.

HERG Screening Industry Leaders

Eurofins Scientific

Charles River Laboratories

WuXi AppTec

Nanion Technologies

Sophion Bioscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Charles River Laboratories broadened its Apollo ecosystem with the CRADL cloud platform to streamline data flow across 30 facilities that host automated hERG suites.

- June 2025: The FDA issued draft guidance on AI credibility for drug submissions, endorsing model risk-management frameworks applicable to in silico hERG predictions.

- April 2025: Metrion Biosciences deployed a high-throughput NaV1.9 assay, adding breadth to its ion-channel portfolio that complements existing hERG services.

- March 2025: Charles River and Valo Health identified a potential lupus therapeutic using the Logica AI engine that integrates automated hERG profiling in discovery cycles.

Global HERG Screening Market Report Scope

| Assay Kits & Reagents |

| Instruments & Software |

| Contract Screening Services |

| Automated Patch Clamp (APC) |

| Manual Patch Clamp |

| Fluorescence-based Membrane Potential Assays (e.g., FLIPR) |

| Radioligand Binding Assays |

| In-silico / In-vitro Hybrid Models |

| Pharmaceutical & Biotech Companies |

| Contract Research Organizations (CROs) & Testing Labs |

| Academic & Research Institutes |

| hERG-Only Screening |

| Comprehensive CiPA Panel (hERG + Nav1.5, Cav1.2, etc.) |

| Expanded Cardiac Ion Panel (≥ 7 channels) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product & Service | Assay Kits & Reagents | |

| Instruments & Software | ||

| Contract Screening Services | ||

| By Assay Type | Automated Patch Clamp (APC) | |

| Manual Patch Clamp | ||

| Fluorescence-based Membrane Potential Assays (e.g., FLIPR) | ||

| Radioligand Binding Assays | ||

| In-silico / In-vitro Hybrid Models | ||

| By End User | Pharmaceutical & Biotech Companies | |

| Contract Research Organizations (CROs) & Testing Labs | ||

| Academic & Research Institutes | ||

| By Ion-Channel Panel | hERG-Only Screening | |

| Comprehensive CiPA Panel (hERG + Nav1.5, Cav1.2, etc.) | ||

| Expanded Cardiac Ion Panel (≥ 7 channels) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the hERG screening market by 2030?

The hERG screening market is projected to reach USD 4.53 billion by 2030.

Which product category currently generates the highest revenue?

Assay Kits & Reagents hold the lead with 36.9% revenue share in 2024.

Which assay type is growing fastest?

In-silico/In-vitro Hybrid Models are expanding at a 14.1% CAGR through 2030.

Why is Asia Pacific the fastest-growing region?

Outsourcing to cost-competitive, GLP-accredited CROs and rising local drug discovery lift Asia Pacific at a 9.5% CAGR.

How does CiPA influence future cardiac safety testing?

CiPA positions hERG data within a seven-channel panel, improving proarrhythmia prediction and driving demand for integrated screening suites.

What is the primary restraint limiting new entrants?

The high capital and consumable costs of automated patch-clamp systems remain the main barrier for smaller organizations.

Page last updated on: