Fecal Immunochemical Test (FIT) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

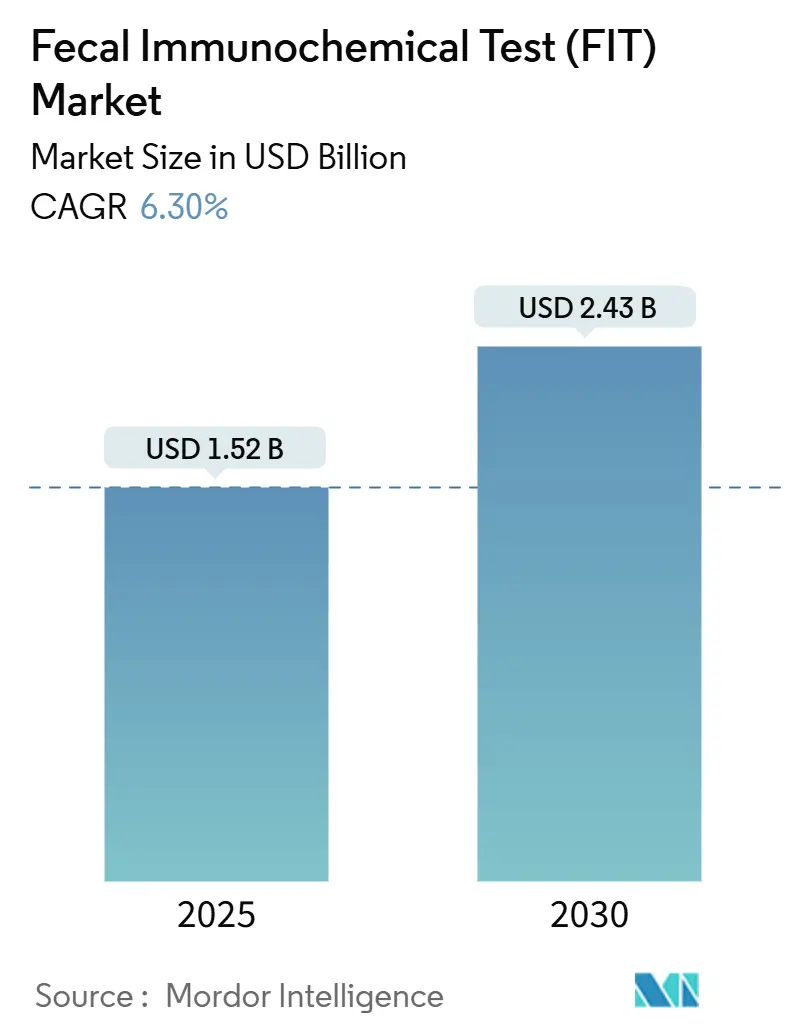

| Market Size (2025) | USD 1.52 Billion |

| Market Size (2030) | USD 2.43 Billion |

| Growth Rate (2025 - 2030) | 6.30% CAGR |

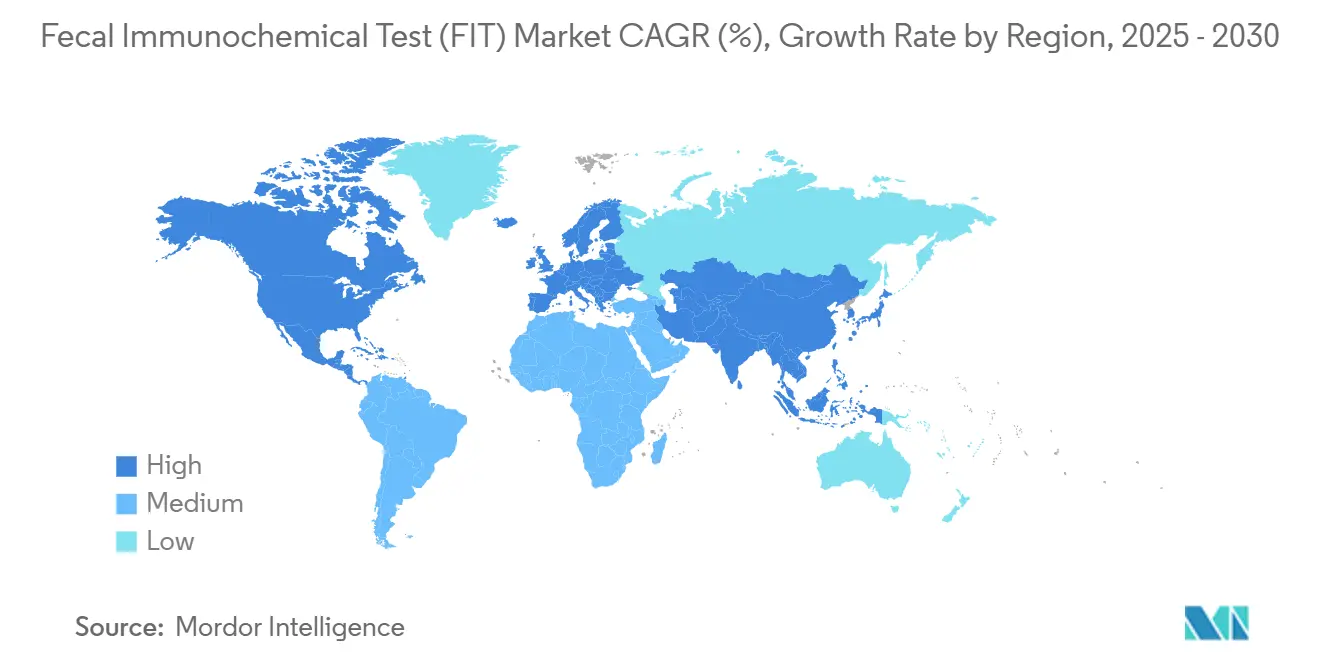

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

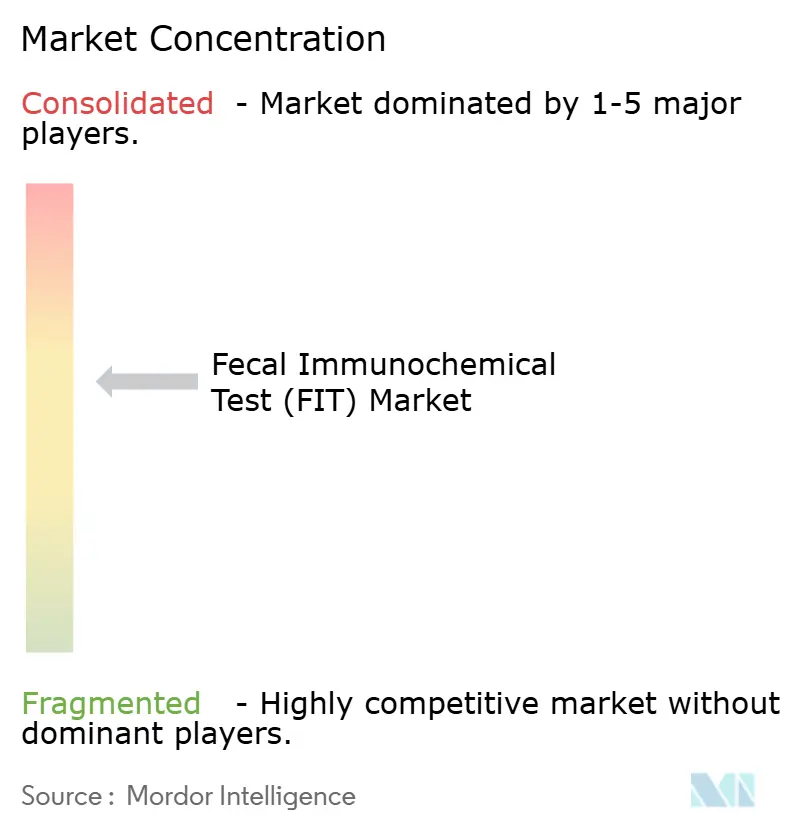

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fecal Immunochemical Test (FIT) Market Analysis by Mordor Intelligence

The fecal immunochemical test market size reached USD 1.52 billion in 2025 and is projected to attain USD 2.43 billion by 2030, expanding at a 6.30% CAGR. Rising early-onset colorectal cancer incidence, broader reimbursement, and guideline shifts lowering the screening age to 45 are enlarging the eligible population while constraining colonoscopy capacity. Mail-out programs that surged during COVID-19 cemented home‐based collection as a mainstream option, and automated analyzers now allow laboratories to process growing volumes with fewer manual steps. Technology approvals such as multitarget DNA-FIT combinations are intensifying competition yet also reinforcing stool-based testing as the backbone of organized screening. Together, these factors sustain robust demand for the fecal immunochemical test market across high- and middle-income settings.

Key Report Takeaways

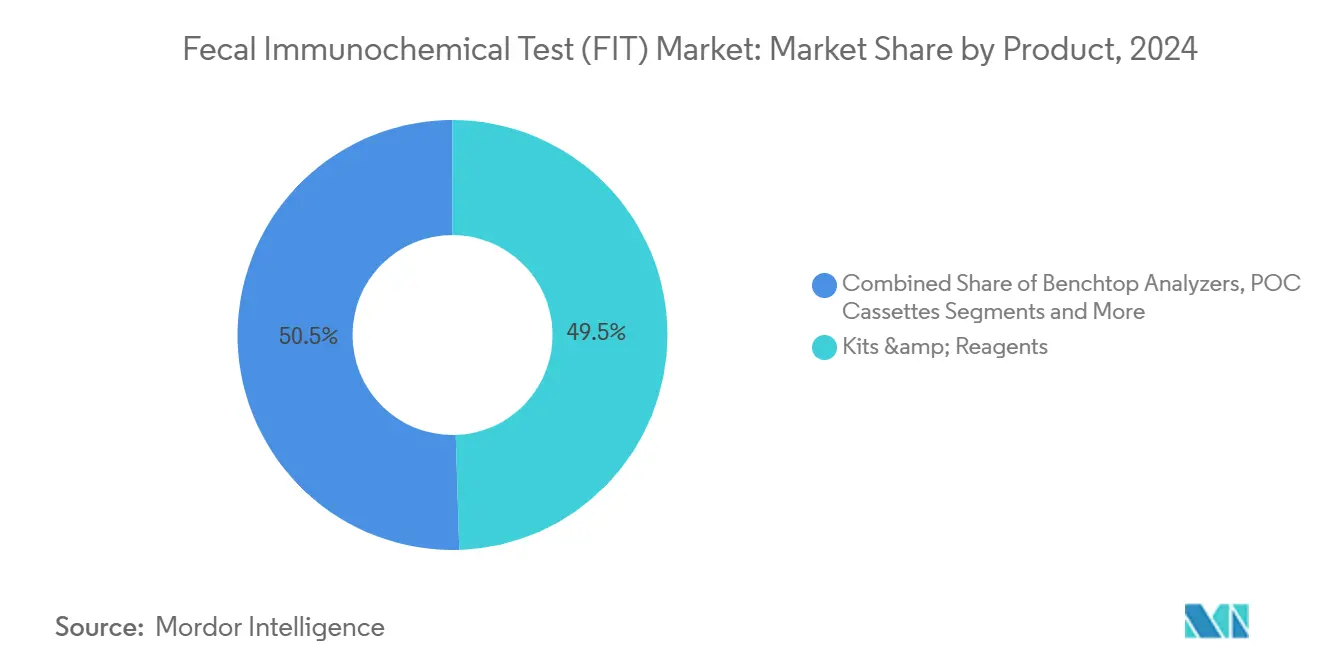

- By product type, Kits & Reagents held 49.5% of the fecal immunochemical test market share

- in 2024, whereas Benchtop Analyzers are forecast to expand at an 11.2% CAGR through 2030.

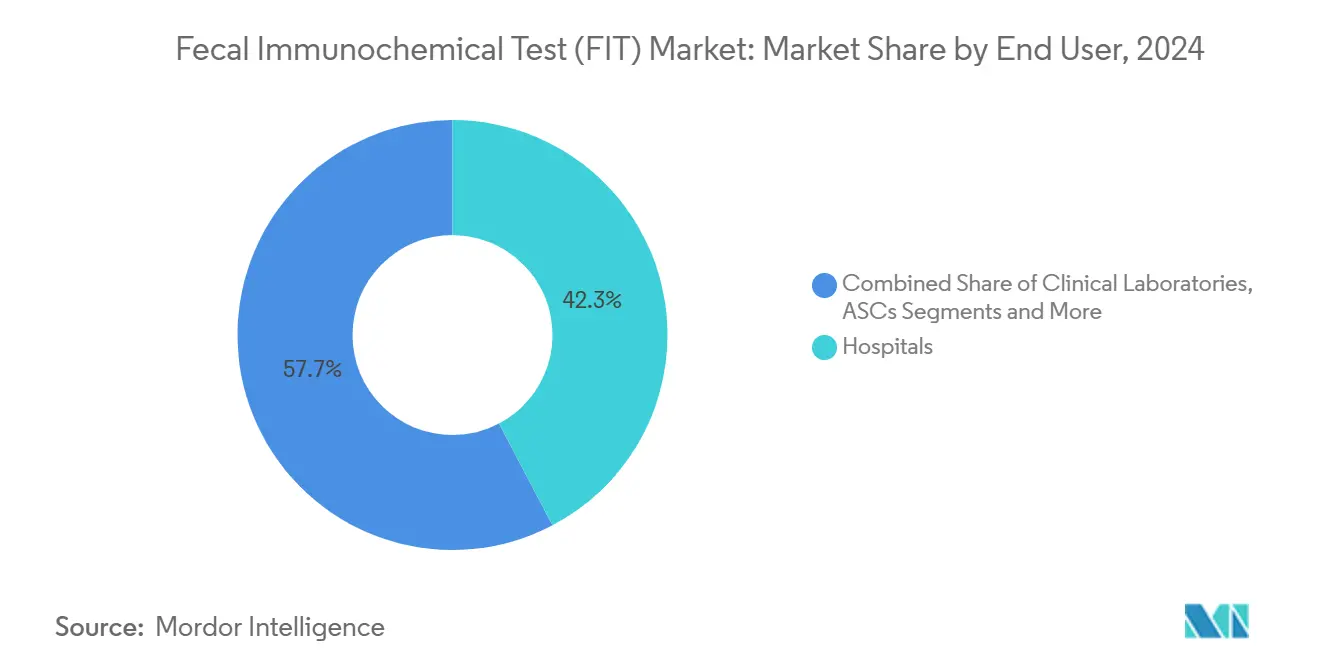

- By end user, Hospitals accounted for 42.3% of the fecal immunochemical test market size in 2024, while Home Care/DTC is advancing at a 12.6% CAGR between 2025-2030.

- By geography, North America led with 38.60% revenue share in 2024; Asia Pacific is projected to post the fastest 9.20% CAGR to 2030.

Global Fecal Immunochemical Test (FIT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising colorectal-cancer incidence and aging demographics | +1.80% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Favorable clinical guidelines endorsing FIT-first screening | +1.50% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Cost-effectiveness versus colonoscopy & imaging | +1.20% | Global, pronounced in resource-constrained markets | Medium term (2-4 years) |

| Expanding public & private reimbursement coverage | +1.00% | North America & EU core, spill-over to emerging markets | Short term (≤ 2 years) |

| Telehealth-enabled home sample logistics | +0.80% | Global, early uptake in developed markets | Short term (≤ 2 years) |

| Employer wellness programs using mail-out kits | +0.50% | North America first, moving global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Colorectal-Cancer Incidence and Aging Demographics

Colorectal cancer rates in adults aged 45-49 now mirror the incidence once seen at 50, prompting societies to lower the recommended screening age.[1]American College of Gastroenterology, “Updates on Age to Start and Stop Colorectal Cancer Screening,” journals.lww.com This younger cohort enlarges the immediate addressable pool and embeds lifelong screening habits, while aging baby boomers sustain high utilization. Asia Pacific registers some of the steepest incidence gains, spurring governments to integrate FIT into national programs; Japan already achieves participation above 40% in organized campaigns. Demographic momentum, therefore, underpins long-run demand across the fecal immunochemical test market.

Favorable Clinical Guidelines Endorsing FIT-First Screening

Guidelines now place FIT on equal footing with colonoscopy for average-risk individuals, removing historical hierarchies that discouraged non-invasive options. Convergent recommendations in North America, Europe, and the Asia Pacific accelerate payer alignment and technology approvals. Regulators such as the FDA have synchronized by granting clearances to next-generation FIT platforms, creating a virtuous cycle of evidence and adoption.

Cost-Effectiveness Versus Colonoscopy and Imaging Modalities

Economic assessments consistently show FIT delivers similar cancer detection at materially lower program costs; in France, the incremental cost-effectiveness ratio was EUR 3,600 (USD 4,224) per QALY, far below threshold values.[2]SAGE Publications, “Cost-effectiveness Analysis of Alternative Colon Cancer Screening Strategies,” ncbi.nlm.nih.gov Savings derive from lower per-test prices, mail-based logistics, and avoidance of procedure-related adverse events. Health systems facing constrained budgets thus prioritize FIT to maximize population coverage.

Expanding Public and Private Reimbursement Coverage

Medicare’s 2025 coverage, starting at age 45, instantly added roughly 19 million eligibles and sets the tone for private insurers. Value-based contracts reward plans that lift screening rates, funneling volumes toward manufacturers. Parallel moves in Europe and employer wellness programs further widen access, amplifying the fecal immunochemical test market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited sensitivity for right-sided lesions | -0.80% | Global, affecting clinical confidence | Long term (≥ 4 years) |

| Patient reluctance toward stool sampling | -0.60% | Cultural variations worldwide | Medium term (2-4 years) |

| Quality variability among low-cost imports | -0.50% | Emerging and cost-sensitive markets | Medium term (2-4 years) |

| Environmental rules on single-use plastics | -0.40% | EU and other strict jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Sensitivity for Right-Sided Lesions (False Negatives)

Right-sided tumors bleed intermittently, allowing occult blood levels to fall below detection thresholds and eroding physician confidence in FIT alone. Some programs now alternate FIT with colonoscopy or adopt multitarget DNA-FIT hybrids, but the biological constraint continues to temper growth.

Patient Reluctance Toward Stool Sampling Lowers Participation

Surveys show roughly 30% of eligible individuals decline FIT due to discomfort with handling stool, especially in conservative cultures.[3]Asian Pacific Journal of Cancer Prevention, “Preferences and Acceptance of Colorectal Cancer Screening in Thailand,” web.archive.org Education and simplified collection help, yet participation ceilings persist and cap achievable coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automation Drives Laboratory Efficiency

Benchtop Analyzers generated the highest forecast growth, climbing at an 11.2% CAGR as laboratories automate high-volume workflows and seek consistent analytics. Kits & Reagents still controlled 49.5% of the fecal immunochemical test market share in 2024, underpinning current revenue while automation ramps up. The fecal immunochemical test market size attributable to analyzers is on track to widen rapidly as health systems scale population screening. Automated platforms like Sentinel’s SENTiFIT 800, distributed by Sysmex, process up to 550 tests hourly and integrate bidirectional LIS connectivity, cutting technician time and error risk. Point-of-care cassettes target low-infrastructure settings, whereas combo calprotectin-FIT kits meet gastroenterologists’ need to triage inflammatory bowel disease alongside cancer risk. Accessory sales track installed analyzer growth, providing recurring revenue.

The competitive tilt toward automation reflects broader laboratory medicine trends favoring throughput, traceability, and integration with digital quality-management systems. Analyzer vendors bundle reagents and service contracts, locking in customers and stabilizing margins, while kit-only suppliers differentiate via antibody specificity and longer onboard stability. As screening volumes climb, throughput requirements elevate analyzers from optional to essential, reinforcing their double-digit expansion within the fecal immunochemical test market.

By End User: Home Care Disrupts Traditional Models

Hospitals retained 42.3% of the fecal immunochemical test market size in 2024, anchored by inpatient diagnostics and outpatient screening drives. Yet Home Care/DTC channels are advancing fastest at 12.6% CAGR, propelled by telehealth, e-commerce logistics, and regulatory clarity around mail-based collection. Clinical laboratories function as the central processing backbone regardless of collection point, channeling rising volumes through automated immunochemistry lines. Ambulatory surgical centers and physician offices still play roles in initial counseling and follow-up colonoscopy referrals, but face share erosion as consumers order kits directly. FDA clearances for home-oriented assays such as Cologuard Plus validate decentralized testing and widen consumer choice.

Consumer ownership of preventive care aligns with broader digital-health adoption, and employers increasingly subsidize mail-out kits within wellness incentives. The fecal immunochemical test market, therefore, continues its pivot from facility-centric to hybrid models where laboratories, e-commerce logistics, and virtual-care platforms intersect.

Geography Analysis

North America held 38.60% of global revenue in 2024, underpinned by Medicare coverage, commercial-payer parity, and national awareness campaigns. U.S. screening programs integrate FIT as a co-primary option, while Canada’s provinces deploy organized invitations that lift participation. Mexico’s healthcare reforms are beginning to adopt stool-based screening as a scalable substitute for limited endoscopy resources. FDA authorizations for multitarget stool and emerging blood tests further reinforce the stool-based paradigm even as competitive modalities appear.

Europe maintains a cohesive framework through European Commission guidance, with individual states operating national call-recall systems that mail FIT kits to target ages every two years. Participation reaches 70% in Finland and continues to climb in Denmark and Norway, highlighting effective program governance. Economic analyses from multiple public payer systems confirm FIT’s favorable cost-utility, sustaining budgetary support even amid broader healthcare austerity.

Asia Pacific, posting the leading 9.20% CAGR, combines high disease burden with rapid health-system modernization. Japan’s long-running program showcases sustained adherence, while China’s Healthy China 2030 reforms and India’s Ayushman Bharat scheme allocate funds for scalable screening. Governments prioritize stool-based approaches to reach vast rural populations where colonoscopy infrastructure is sparse. Manufacturers tailor distribution through local partners and introduce analyzer models geared to medium-sized provincial laboratories, reinforcing growth prospects within the fecal immunochemical test market.

Competitive Landscape

The fecal immunochemical test market remains moderately fragmented, with scale advantages offset by ongoing product innovation. Diagnostics majors—Sysmex, Abbott, Roche, Danaher’s Beckman Coulter—leverage global distribution and automated platforms, while specialized firms such as Eiken Chemical and Sentinel Diagnostics focus on reagent specificity and analyzer throughput. Sysmex’s fiscal-2025 half-year revenue rose 14.0%, illustrating sustained demand for its stool-testing portfolio. Partnerships, exemplified by Sysmex and Sentinel’s Canadian deal, allow rapid geographic expansion without heavy capital deployment.

Competitive intensity escalated after FDA approval of multitarget stool-DNA and RNA assays from Exact Sciences and Geneoscopy, each touting sensitivity above 90% for colorectal cancer. These entrants challenge traditional FIT on clinical performance yet still rely on immunochemical detection for hemoglobin alongside additional biomarkers, blending paradigms rather than replacing them. Laboratories and payers weigh cost per detected lesion and downstream colonoscopy demand, fostering coexistence of classic FIT, hybrid DNA-FIT, and emergent blood tests within broader stool-based screening ecosystems.

Strategic focus has shifted toward digital integration—auto-result uploads to patient portals, AI-based quality checks, and predictive analytics that flag non-returned kits for targeted reminders. Vendors able to embed such capabilities into analyzers or connected kits gain stickiness with health-system IT departments. Environmental sustainability also surfaces as a differentiator, with European tenders increasingly scoring bidders on recyclable plastics and carbon-neutral logistics.

Fecal Immunochemical Test (FIT) Industry Leaders

Sysmex Corporation

Abbott Laboratories

Eiken Chemical Co., Ltd.

QuidelOrtho Corporation

Sentinel Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sysmex America signed a distribution agreement with Sentinel Diagnostics to supply SENTiFIT analyzers across Canada, adding 550-test-per-hour capacity to regional laboratories.

- August 2024: The FDA issued a warning letter to Pinnacle Labs for marketing a second-generation FIT without clearance, underscoring regulatory vigilance.

- February 2025: The FDA finalized amendments harmonizing device quality-system rules with international standards, impacting FIT manufacturers’ compliance frameworks.

Global Fecal Immunochemical Test (FIT) Market Report Scope

| Kits & Reagents |

| Benchtop Analyzers |

| POC Cassettes |

| Combo Calprotectin-FIT Kits |

| Accessories & Consumables |

| Hospitals |

| Clinical Laboratories |

| Ambulatory Surgical Centers |

| Physician Offices |

| Home Care / DTC |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Kits & Reagents | |

| Benchtop Analyzers | ||

| POC Cassettes | ||

| Combo Calprotectin-FIT Kits | ||

| Accessories & Consumables | ||

| By End User | Hospitals | |

| Clinical Laboratories | ||

| Ambulatory Surgical Centers | ||

| Physician Offices | ||

| Home Care / DTC | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global fecal immunochemical test market in 2025?

The market stands at USD 1.52 billion in 2025 and is forecast to reach USD 2.43 billion by 2030.

What CAGR is expected for fecal immunochemical test demand between 2025-2030?

Demand is projected to expand at 6.30% annually over the forecast period.

Which region leads current sales of fecal immunochemical tests?

North America commands the largest share at 38.60% thanks to mature screening infrastructure and broad reimbursement.

Which product segment is growing fastest?

Benchtop Analyzers show the strongest outlook, rising at an 11.2% CAGR as labs automate high-volume processing.

Why is home-based screening gaining traction?

Telehealth expansion, insurer mail-out programs, and consumer preference for convenience are pushing Home Care/DTC channels to a 12.6% CAGR.

What key restraint affects FIT accuracy?

Limited sensitivity for right-sided colorectal lesions leads to occasional false negatives, prompting some programs to combine FIT with other tests.

Page last updated on: