In-Vehicle Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

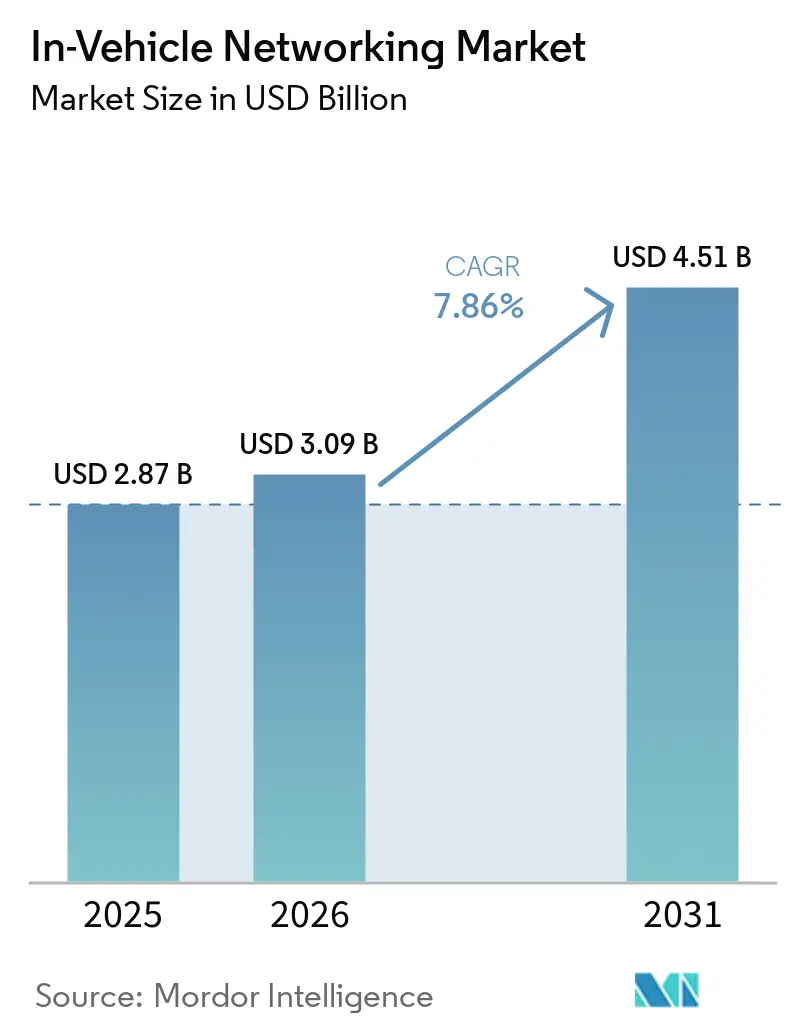

| Market Size (2026) | USD 3.09 Billion |

| Market Size (2031) | USD 4.51 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

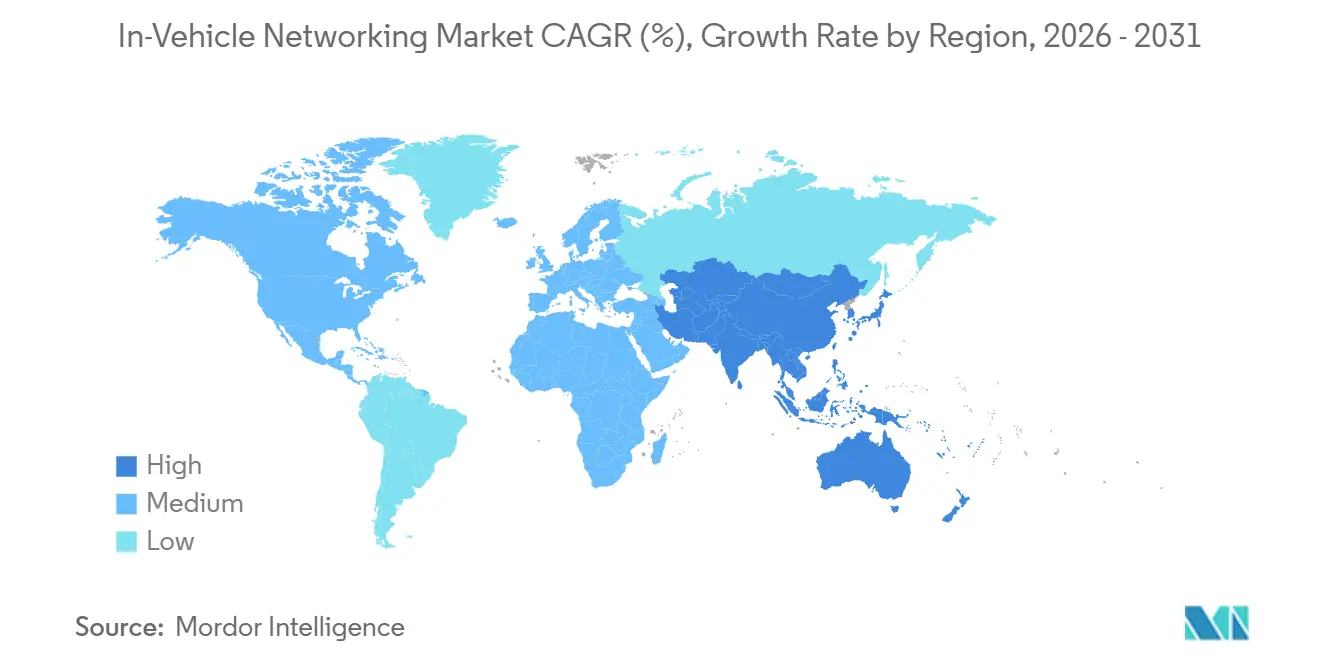

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

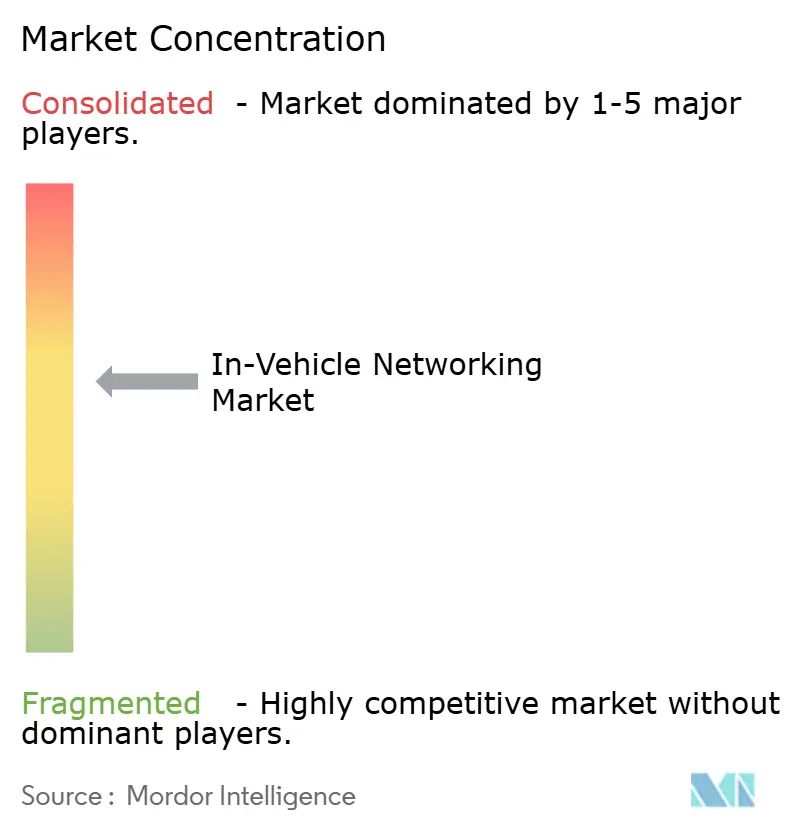

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In-Vehicle Networking Market Analysis by Mordor Intelligence

The in-vehicle networking market size was valued at USD 2.87 billion in 2025 and estimated to grow from USD 3.09 billion in 2026 to reach USD 4.51 billion by 2031, at a CAGR of 7.86% during the forecast period (2026-2031). Convergence of zonal electrical-electronic architectures, mandatory Time-Sensitive Networking (TSN) standards, and escalating ADAS sensor bandwidth is reshaping product roadmaps worldwide. Original equipment manufacturers are consolidating as many as 100 electronic control units into fewer than 15 zonal gateways, shrinking wiring mass by up to 30% and compressing vehicle development cycles. Automotive Ethernet is displacing legacy protocols in infotainment and ADAS domains as multi-gigabit backbones support over-the-air updates and centralized compute. Semiconductor vendors with vertically integrated microcontroller, switch, and transceiver portfolios are tightening their grip on gateway design-ins while smaller software-defined-vehicle specialists fill middleware gaps. Heightened cybersecurity certification costs, raw-material inflation, and electromagnetic-compatibility bottlenecks remain near-term headwinds but are not expected to derail the long-run trajectory of the in-vehicle networking market.

Key Report Takeaways

- By geography, Asia-Pacific retained 43.78% of the 2025 value, while the Middle East and Africa segment is on track for the highest 8.94% CAGR t. the fastest 7.93% CAGR through 2031.

- By vehicle type, passenger cars captured 55.34% revenue in 2025, whereas off-highway and specialized vehicles are forecast to expand at an 8.23% CAGR to 2031.

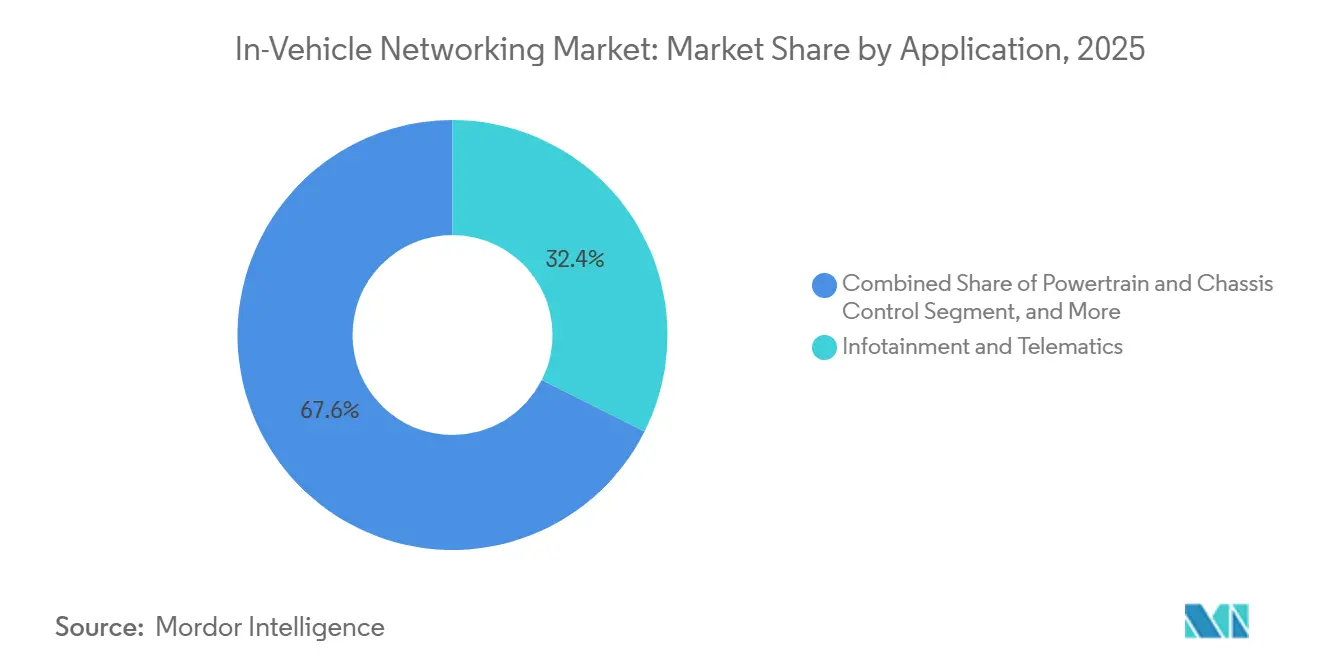

- By application, infotainment and telematics accounted for a 32.45% share of the in-vehicle networking market size in 2025 and are advancing at a 7.97% CAGR through 2031.

- By component, transceivers dominated with 39.86% share in 2025, yet controllers and gateways are set to grow fastest at a 7.92% CAGR as zonal architectures gain scale.

- By geography, Asia-Pacific retained 43.78% of the 2025 value, while the Middle East and Africa segment is on track for the highest 8.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of In-Vehicle Networking Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle Electrification and Escalating ADAS Bandwidth Needs | +1.8% | Global, early concentration in China, the European Union, and North America | Medium term (2-4 years) |

| OEM Migration from Domain to Zonal E and E Architecture | +1.5% | Global, led by European Union and China OEMs | Medium term (2-4 years) |

| Adoption of Time-Sensitive Networking in Automotive Ethernet | +1.3% | Global, pushed by IEEE standardization | Long term (≥4 years) |

| Infotainment and Telematics Feature Proliferation | +1.2% | Global, premium-segment early adoption in North America and the European Union | Short term (≤2 years) |

| Regulatory Mandates for Advanced Safety Networks | +1.0% | European Union, China, spillover to India and ASEAN | Short term (≤2 years) |

| China’s NEV Platform Standardization Pressure | +0.8% | China's domestic market, export impact on ASEAN, and the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vehicle Electrification and Escalating ADAS Bandwidth Needs

Battery-electric and plug-in hybrid platforms embed up to 40% more sensors than internal-combustion counterparts, producing several terabytes of raw data every hour. Legacy five-megabit-per-second CAN-FD links cannot move this volume efficiently, prompting widespread deployment of 100BASE-T1 and 1000BASE-T1 Ethernet for sensor fusion backhaul. Microcontroller vendors now integrate 10BASE-T1S low-speed Ethernet into edge nodes so inexpensive temperature and pressure sensors can feed zonal gateways, which then uplink aggregated traffic to gigabit trunks. Centralized architectures also slash wiring length, driving range gains for energy-dense battery packs.[1]BMW Group, “Neue Klasse Zonal Platform Wiring Reduction,” BMW.com Over-the-air updates for perception software can exceed ten gigabytes per vehicle, a load that only gigabit Ethernet paired with 5G or satellite offload can manage. China’s GB/T 32960 real-time telematics rule further boosts uplink demand, reinforcing Ethernet adoption.[2]Ministry of Industry and Information Technology, “GB/T 32960 NEV Remote Service Rules,” Miit.gov.cn

OEM Migration from Domain to Zonal E and E Architecture

Traditional domain layouts required kilometers of harnesses and up to 100 controllers. Zonal topologies reposition compute into three to five regional gateways located near the physical loads, trimming cable weight by as much as 30% and reducing latency by eliminating inter-domain hops. Early production proof came from Volkswagen’s China Electronic Architecture, which cut its controller count by 30% and halved software release cycles. Zonal gateways must bridge LIN, CAN-FD, FlexRay, and Ethernet while satisfying ISO 21434 cybersecurity and AUTOSAR Adaptive compatibility. Silicon that unifies 16 or more CAN channels with integrated TSN switches and hardware security modules is therefore in high demand.

Adoption of Time-Sensitive Networking in Automotive Ethernet

TSN brings deterministic timing to shared Ethernet fabrics so safety-critical steer-by-wire packets never wait behind video streams. The IEEE 802.1DG-2025 profile packages time synchronization, traffic shaping, and frame preemption for automotive platforms. Production-grade ten-port switches with hardware Qbv scheduling now guarantee sub-100-microsecond latency from sensor to processor. Premium brands have published data showing ten-millisecond loop closure for automated emergency braking using TSN trunks. Certification bodies launched TSN interoperability testbeds in 2024, helping OEMs reduce black-box integration risk.

Infotainment and Telematics Feature Proliferation

High-definition streaming, real-time navigation, and voice assistants are pushing infotainment bandwidth well past 1 gigabit-per-second. A 2025 over-the-air rollout of conversational AI to 2.5 million vehicles required multi-gigabit Ethernet to synchronize models locally. Broadcast standards such as ATSC 3.0 can deliver ten-gigabyte files simultaneously to large fleets, but vehicles still need Ethernet storage controllers to buffer the data. Publish-subscribe middleware certified to ASIL-D now rides on Ethernet to decouple applications from network plumbing, accelerating feature releases. As display counts climb, Automotive SerDes over Ethernet is rapidly displacing MOST and LVDS.

Restraints Impact Analysis of In-Vehicle Networking Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Harness Weight and Cost Inflation Versus BOM Targets | -0.9% | Global, most acute in India, ASEAN, and South America | Short term (≤2 years) |

| Cyber-Security Certification Complexity for Multi-Protocol Stacks | -0.7% | European Union, China, global spillover | Medium term (2-4 years) |

| Thermal and EMC Integrity Limits At ≥1 Gbps | -0.5% | Global, especially compact vehicle layouts | Long term (≥4 years) |

| OEM-Specific Proprietary Network Stacks Hindering Interoperability | -0.4% | Global, Tier-2 fragmentation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Harness Weight and Cost Inflation Versus BOM Targets

Wiring looms weigh up to 80 kilograms in battery-electric models, adding drag on driving range. Early-2026 copper averaged USD 10,700 per tonne, and silver rose to USD 99 per ounce, inflating cable bills by nearly one-fifth. Moving from 400-volt to 800-volt architectures halves the conductor cross-section but requires higher-rated connectors that claw back some savings. Zonal integration cuts cable length by roughly one-quarter, yet it demands additional gateway silicon that pushes controller costs up more than one-third. Indian suppliers localizing under production-linked incentives face especially tight bill-of-materials limits.

Cyber-Security Certification Complexity for Multi-Protocol Stacks

UN ECE R155 and R156 mandate end-to-end cybersecurity governance, while ISO/SAE 21434 requires threat analysis for every network interface. Gateways that translate among CAN-FD, FlexRay, and Ethernet now undergo multiple rounds of penetration testing, fuzzing, and continuous monitoring, extending validation schedules by up to nine months. Hardware accelerators for MACsec encryption and post-quantum cryptography reduce runtime overhead but add design complexity and silicon cost. Certification bodies introduced fee-based audits that can tack USD 100 per vehicle onto launch budgets, a burden that smaller Tier-2 suppliers struggle to absorb.[3]Korea Quality Foundation, “ISO/SAE 21434 Audit Offering,” Kqf.or.kr

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

In-Vehicle Networking Market Segment Analysis

By Protocol/Technology:

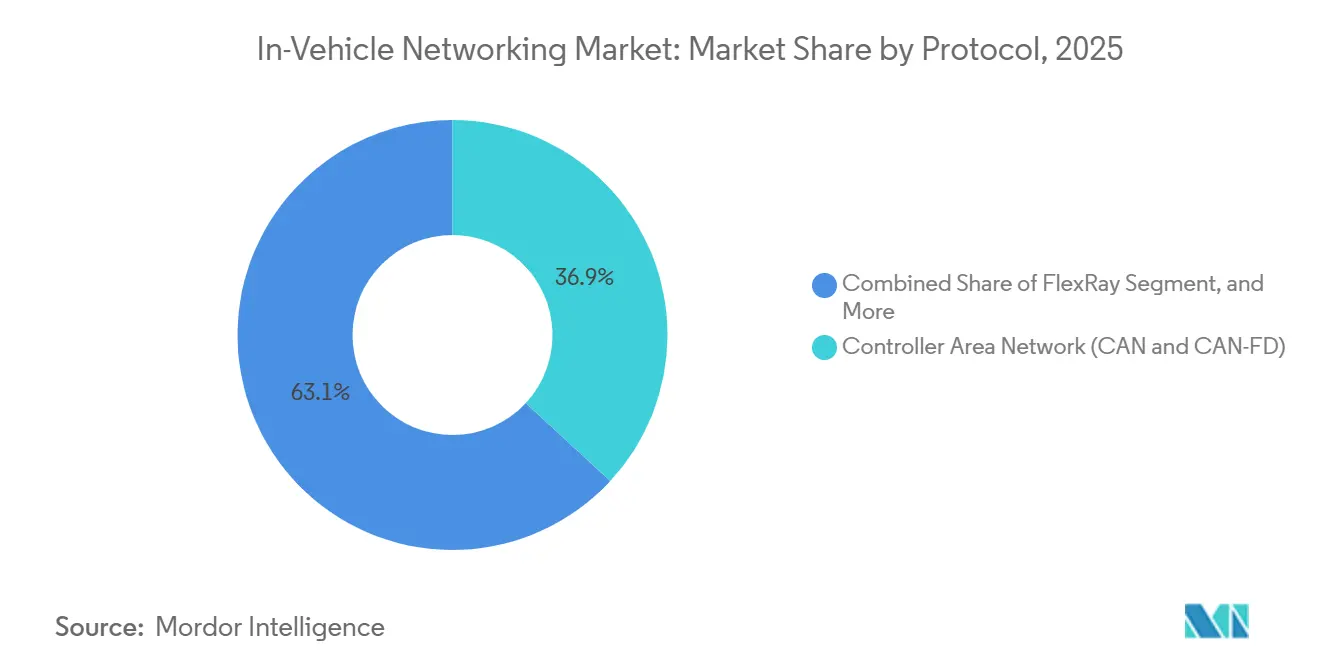

Ethernet Expands as CAN-FD Retains Volume LeadershipCAN and CAN-FD maintained 36.89% of the in-vehicle networking market share in 2025 thanks to their low cost and entrenched use in powertrain and body-control loops. FlexRay, though a niche, is positioned for a 7.93% CAGR because steer-by-wire and brake-by-wire platforms need its deterministic dual-channel redundancy. Automotive Ethernet now scales from 10 megabits to 10 gigabits per second, so infotainment, ADAS, and centralized compute can coexist on one backbone, a shift formalized by IEEE 802.1DG-2025. LIN remains the sub-20-kilobit workhorse for seat, mirror, and lighting functions. MOST continues to decline as its 150-megabit ceiling cannot keep pace with 4K streaming demands.

Multi-protocol microcontrollers that integrate CAN-FD, LIN, and FlexRay reduce board count and shorten validation time as zonal gateways absorb body functions. Emerging CAN-XL raises single-frame payloads to 2,048 bytes, positioning itself as the bridge between legacy control loops and Ethernet tunnels. Secure 1000BASE-T1 PHYs with built-in MACsec and 1588 timestamping now reduce board area by up to 15% compared with discrete implementations. The in-vehicle networking market size attached to Ethernet PHYs will therefore outgrow node counts as the average price per port climbs.

By Vehicle Type:

Off-Highway Equipment Gains MomentumIn 2025, passenger cars accounted for 55.34% of total revenue, translating to an annual output of approximately 70 million units. While construction, agriculture, and mining machinery saw lower volumes, they are projected to experience a CAGR of 8.23%. This growth is driven by fleet owners increasingly seeking predictive maintenance and remote diagnostics, both of which necessitate Ethernet gateways. The rising adoption of advanced telematics systems and IoT integration in these machinery segments further supports this trend.

Light commercial vehicles benefit from passenger-car component commonality, allowing them to inherit gigabit backbones at minimal incremental cost. Heavy trucks must meet new automated steering regulations that make deterministic Ethernet mandatory. Off-highway designers adopt IP69K-rated CAN-to-Ethernet bridges so equipment can survive dust, vibration, and water jets. These trends keep the in-vehicle networking market size in the specialty-vehicle segment on a steeper slope than the overall base.

By Application:

Infotainment and ADAS Drive Bandwidth UpsideInfotainment and telematics already contribute 32.45% of the 2025 value and will grow at 7.97% because high-definition displays, streaming content, and artificial intelligence assistants require multi-gigabit links. The increasing adoption of connected vehicle ecosystems and over-the-air (OTA) updates is further driving advancements in this segment. Autonomous driving compute domains, although newer, represent the fastest-growing slice as centralized processors ingest 10-Gigabit sensor data for Level 2+ functions. The growing focus on sensor fusion technology is also propelling the development of autonomous driving systems.

Safety-critical messaging moves to TSN-enabled Ethernet so brake-by-wire and steer-by-wire loops close in under ten milliseconds. Powertrain control still favors CAN-FD for its sub-USD 5 bill-of-materials and proven reliability. Body control remains LIN-centric until further cost declines in Ethernet. Growing data density ensures that the in-vehicle networking market size tied to infotainment and ADAS rises faster than unit shipments.

By Component:

Controllers and Gateways Capture Zonal UpsideIn 2025, transceivers dominated the market, capturing a significant 39.86% share across every network node. Meanwhile, as functions began to consolidate, both controller and gateway silicon experienced a robust growth rate of 7.92%. This surge can be attributed to regional aggregates' increasing demand for high-port-count TSN switches and hardware security modules. The increasing deployment of industrial automation systems and the shift toward Industry 4.0 are further fueling the demand for these technologies. Moreover, the integration of advanced communication protocols is enhancing the efficiency and scalability of network infrastructures.

Eight-port Gigabit switches that embed traffic-shaping and MACsec reduce gateway board area by double digits and underpin secure mixed-criticality fabrics. Cabling and connectors, though a volume staple, expand more slowly given copper price pressures and OEM migration to aluminum conductors. EMI-suppressing chokes shrink connector footprints and cut harness weight, answering OEM cost and mass mandates. As zonal architectures proliferate, the in-vehicle networking market share commanded by smart gateways will keep growing relative to passive cabling.

Geography Analysis

APAC In-Vehicle Networking Market

Asia-Pacific retained 43.78% of 2025 revenue, anchored by China’s 27 million-unit passenger-car output and India’s newly announced 300,000-unit plant that targets 75% NEV content localization. Platform rules under GB/T 32960 push every Chinese OEM toward Ethernet gateways with integrated 5G uplink, accelerating silicon volume. India’s production-linked incentives are drawing network-component suppliers into local clusters, lowering tariff exposure and bolstering the regional in-vehicle networking market. Japan and South Korea concentrate on premium ADAS features, creating early demand for TSN hardware.

North America In-Vehicle Networking Market

North America held roughly one-quarter of 2025 spending, supported by 11 million light-truck and SUV builds in the United States and export-oriented assembly in Mexico. Regulatory momentum for automated lane keeping and over-the-air cyber-secure updates sustains Ethernet penetration. Silicon Valley start-ups provide SDV middleware that reduces integration time for Detroit-area OEMs, supporting healthy investment in gateways and centralized compute. The United States Inflation Reduction Act spurs domestic battery and electronics supply, giving subsidies that indirectly boost the in-vehicle networking market.

EMEA and South America In-Vehicle Networking Market

Europe achieved a 20-22% share on the back of luxury and performance brands that lead in zonal topologies, centralized ADAS, and ISO 21434 certification. UN ECE rulemaking synchronizes safety and cybersecurity deadlines across member states, stimulating predictable rollout schedules for Ethernet and FlexRay upgrades. Eastern European plants leverage lower wage costs to assemble wiring harnesses and optical-fiber links, ensuring regional cost competitiveness. Middle East and Africa, although only a mid-single-digit base today, is tracking toward an 8.94% CAGR through 2031 as smart-city megaprojects mandate vehicle-to-infrastructure connectivity. South America benefits from Mercosur rules that reduce import duties on localized CAN-FD and Ethernet components, but macro volatility tempers absolute market size growth.

Competitive Landscape

Moderate concentration characterizes the in-vehicle networking market, with the top five semiconductor providers supplying more than half of gateway silicon revenue. NXP spans microcontrollers, Ethernet switches, and physical interfaces, enabling single-vendor zonal platforms that cut qualification work for carmakers. Infineon integrates MACsec and IEEE 1588 timing inside 1000BASE-T1 PHYs, trimming bill-of-materials by 10-15% for gateway builders. Renesas differentiates by embedding post-quantum cryptography accelerators, future-proofing designs against new NIST standards, and positioning for extended vehicle lifecycles.

Tier-1 integrators such as Bosch, Continental, and Aptiv compete on orchestration software, harness design, and system integration. Bosch’s AUTOSAR-compliant middleware and wiring-harness capacity in South Africa allow full-stack delivery, giving OEMs a single contract for hardware and software. Continental leverages production scale in Morocco and Romania to supply cost-sensitive Ethernet and CAN harnesses to European mass-market brands. Aptiv pairs gateway electronics with over-the-air update platforms, providing bundled cybersecurity services that meet UN ECE R155 evidence requirements.

Start-ups fill white-space opportunities. Sonatus offers TSN orchestration middleware that abstracts protocol heterogeneity, cutting months from integration time for small OEMs. Optical-link specialists are positioning fiber to solve 10-Gigabit electromagnetic issues in centralized ADAS trunks, a niche underserved by incumbent copper-focused suppliers. Connector makers TE Connectivity, Molex, and Amphenol are consolidating to reach scale in high-speed Ethernet plugs. Independent cybersecurity labs monetize ISO/SAE 21434 audits, creating an additional barrier to entry for small hardware vendors.

In-Vehicle Networking Industry Leaders

NXP Semiconductors N.V.

Robert Bosch GmbH

Texas Instruments Incorporated

Microchip Technology Inc.

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

In-Vehicle Networking Market Companies Covered in this Report

- NXP Semiconductors N.V.

- Robert Bosch GmbH

- Texas Instruments Incorporated

- Microchip Technology Inc.

- STMicroelectronics N.V.

- Broadcom Inc.

- Marvell Technology, Inc.

- Infineon Technologies AG

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- Analog Devices, Inc.

- Realtek Semiconductor Corp.

- Rohm Co., Ltd.

- Melexis N.V.

- ON Semiconductor Corporation

- Molex LLC

- TE Connectivity Ltd.

- Aptiv PLC

- Continental AG

- Marvell Technology, Inc.

Recent Industry Developments in In-Vehicle Networking Market

- April 2026: Caterpillar announced fleet-wide integration of Geotab telematics, combining CAN diagnostics with cloud analytics to boost equipment uptime.

- March 2026: Vantron introduced the AG605 automotive gateway based on NXP i.MX 94, delivering CAN-FD, LIN, and gigabit Ethernet bridges for zonal platforms.

- February 2026: NXP released TJA1410 and TJF1410 10BASE-T1S transceivers for low-speed sensor aggregation at zonal edges.

- February 2026: JSW MG Motor committed USD 330-440 million to a 300,000-unit NEV plant in India, targeting 75% local network-component sourcing.

Global In-Vehicle Networking Market Report Scope

Segmentation Overview

| Local Interconnect Network (LIN) |

| Controller Area Network (CAN and CAN-FD) |

| FlexRay |

| Automotive Ethernet (10 Mbps - 10 Gbps) |

| Media Oriented Systems Transport (MOST) |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Off-Highway and Specialized Vehicles |

| Powertrain and Chassis Control |

| Safety and ADAS |

| Infotainment and Telematics |

| Body Control and Comfort |

| Autonomous Driving Compute Domains |

| Transceivers |

| Controllers and Gateways |

| Switches and Routers |

| Cabling and Connectors |

| Network ICs and PHYs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Protocol / Technology | Local Interconnect Network (LIN) | ||

| Controller Area Network (CAN and CAN-FD) | |||

| FlexRay | |||

| Automotive Ethernet (10 Mbps - 10 Gbps) | |||

| Media Oriented Systems Transport (MOST) | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Off-Highway and Specialized Vehicles | |||

| By Application | Powertrain and Chassis Control | ||

| Safety and ADAS | |||

| Infotainment and Telematics | |||

| Body Control and Comfort | |||

| Autonomous Driving Compute Domains | |||

| By Component | Transceivers | ||

| Controllers and Gateways | |||

| Switches and Routers | |||

| Cabling and Connectors | |||

| Network ICs and PHYs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the in-vehicle networking market?

The in-vehicle networking market size is USD 3.09 billion in 2026 and is projected to reach USD 4.51 billion by 2031.

Which vehicle type segment will grow fastest in networking adoption?

Off-highway and specialized vehicles are forecast to record an 8.23% CAGR to 2031 as Ethernet-based telematics becomes standard.

Why are zonal architectures gaining momentum?

Zonal gateways cut harness weight by up to 30%, enable software updates regionally, and simplify cybersecurity audits, making them economically attractive despite higher gateway silicon costs.

How does Time-Sensitive Networking benefit automotive Ethernet?

TSN guarantees deterministic latency below 100 microseconds, allowing safety-critical steer-by-wire and brake-by-wire data to coexist with infotainment traffic on the same Ethernet backbone.

What challenges slow the rollout of multi-gigabit Ethernet in cars?

Rising copper prices, electromagnetic-compatibility issues above 1 Gbps, and lengthy ISO/SAE 21434 cybersecurity certification all extend program timelines.

Which components will outpace the broader market in growth?

Controllers and gateways are poised for a 7.92% CAGR because zonal designs need high-port-count switches with integrated security and TSN features.

Page last updated on: