Off-Highway Vehicle Telematics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

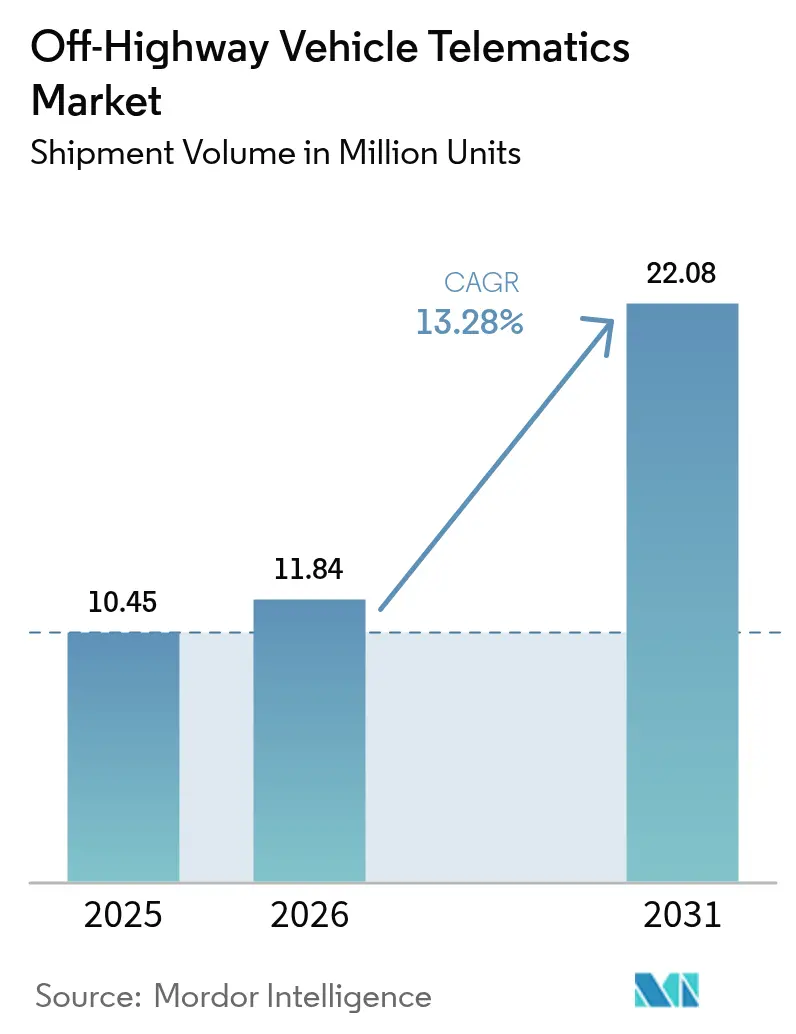

| Market Volume (2026) | 11.84 Million units |

| Market Volume (2031) | 22.08 Million units |

| Growth Rate (2026 - 2031) | 13.28% CAGR |

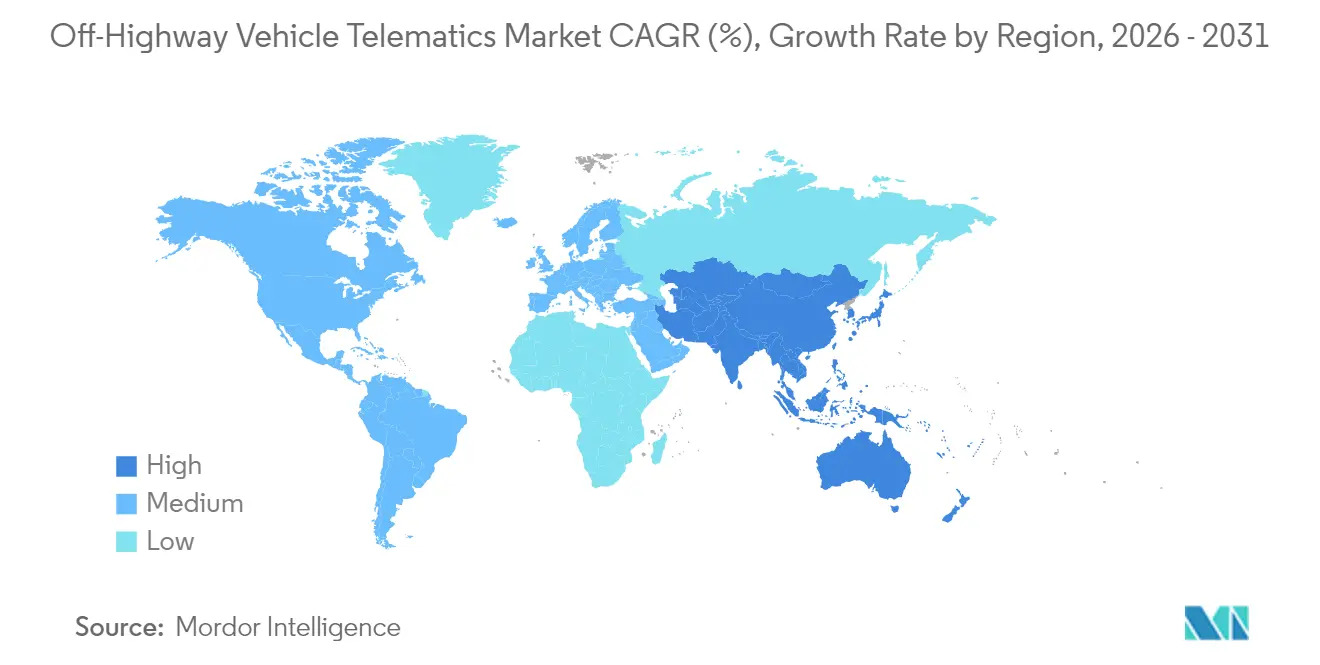

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Off-Highway Vehicle Telematics Market Analysis by Mordor Intelligence

The Off-Highway Vehicle Telematics Market size was valued at 10.45 million units in 2025 and estimated to grow from 11.84 million units in 2026 to reach 22.08 million units by 2031, at a CAGR of 13.28% during the forecast period (2026-2031). In monetary terms, the off-highway vehicle telematics market size associated with hardware, software, and services combined rose steadily through 2024 and continues to scale in 2025 on the back of stricter emissions regulations, lower device costs, and near-ubiquitous connectivity. Companies across construction, agriculture, mining, and forestry view telematics as essential infrastructure because a single day of downtime on critical equipment can exceed USD 50,000 in direct costs. Cellular networks still anchor most deployments, yet dual-mode cellular–satellite links are accelerating as remote work sites demand guaranteed coverage. OEMs such as Caterpillar, Komatsu, and John Deere are embedding telematics at the factory, while aftermarket specialists ORBCOMM, Geotab, and Trackunit serve mixed fleets. Underpinning these moves are software platforms that translate raw machine data into actionable insights—an evolution reflected in software’s position as the fastest-growing component segment.

Key Report Takeaways

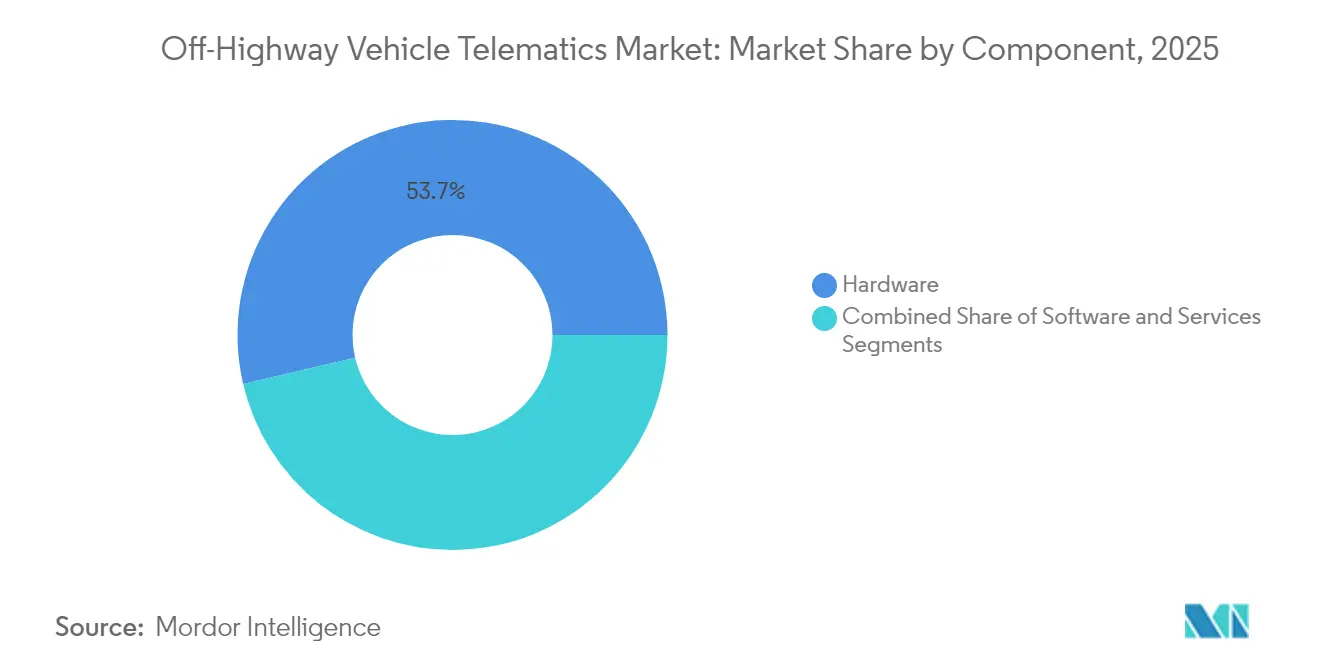

- By component, hardware held 53.65% of the off-highway vehicle telematics market share in 2025, while software is forecast to expand at a 15.72% CAGR through 2031.

- By connectivity, cellular networks led with 58.55% revenue share in 2025; dual-mode cellular–satellite solutions are projected to grow at 15.12% CAGR to 2031.

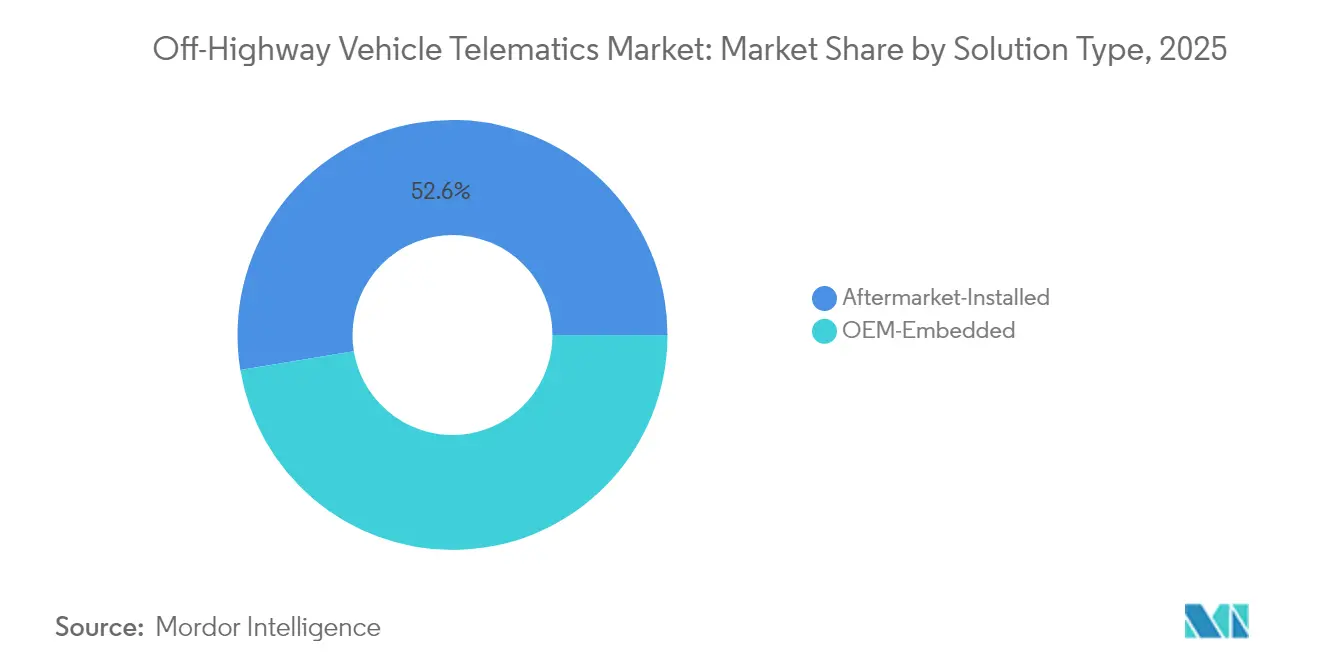

- By solution type, the aftermarket-installed segment commanded 52.60% share of the off-highway vehicle telematics market size in 2025, whereas OEM-embedded systems are rising at a 16.35% CAGR.

- By vehicle type, construction equipment accounted for a 43.85% share in 2025; material-handling machinery is advancing at a 15.62% CAGR through 2031.

- By end-user industry, construction companies controlled 48.25% share in 2025, while rental and leasing fleets recorded the highest projected CAGR at 15.89% to 2031.

- By geography, North America captured 36.35% of the 2025 volume; Asia-Pacific is forecast to grow the fastest at 15.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Off-Highway Vehicle Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulations mandating OEM-installed telematics on heavy equipment | +2.8% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Surge in low-orbit satellite constellations enabling "black-spot-free" coverage | +2.1% | Global, with priority in remote mining and agriculture regions | Long term (≥ 4 years) |

| Falling unit cost of ruggedized TCUs and sensors | +1.9% | Global, with accelerated adoption in price-sensitive APAC markets | Short term (≤ 2 years) |

| Integration of telematics-driven carbon-credit monetisation platforms | +1.4% | EU and North America initially, expanding globally | Long term (≥ 4 years) |

| OEM-agnostic AEMP 2.0 data-standard adoption unlocking mixed-fleet analytics | +1.6% | Global, with strongest impact in North America construction sector | Medium term (2-4 years) |

| Emerging AI-based predictive-maintenance marketplaces for rental fleets | +1.8% | North America and EU rental markets, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulations mandating OEM-installed telematics on heavy equipment

California’s proposed Tier 5 rules demand 90% NOx reduction for 56-560 kW engines by 2029 and require continuous emissions data uploads for compliance auditing, effectively making telematics standard rather than optional throughout North America. [1]California Air Resources Board, “CARB releases proposed Tier 5 off-road engine emission standards,” dieselnet.com European Stage V requirements echo this stance by obligating real-time monitoring of diesel particulate filters. OEMs respond by bundling telematics at the factory, lowering incremental costs and accelerating adoption curves across construction, agriculture, and mining fleets. The same provisions open the door for future mandates on operator-fatigue alerts and geofencing in sensitive zones, pushing the off-highway vehicle telematics market toward full-spectrum safety compliance.

Surge in low-orbit satellite constellations enabling “black-spot-free” coverage

Low-Earth-orbit networks such as Starlink now bridge connectivity gaps that historically limited telematics in rural agriculture and open-pit mines. John Deere’s Kansas field trials maintained continuous data flow across a 70-mile farming radius, enabling real-time agronomic tweaks and predictive maintenance that saved fuel and reduced unexpected repairs. Mining firms gain even more, as uninterrupted data streams cut costly downtime by up to 20% on high-value extraction machinery. [2]ORBCOMM, “Heavy Equipment Mining | ORBCOMM,” orbcomm.com While satellite subscriptions still range USD 50–200 per unit each month, volume pricing is trending downward alongside rapid fleet uptake, underpinning long-term growth for the off-highway vehicle telematics market.

Falling unit cost of ruggedized TCUs and sensors

The average price of a ruggedized telematics control unit fell from USD 800-1,200 in 2020 to USD 200-400 in 2024, driven by semiconductor scale economies and protocol standardization such as AEMP 2.0. Standard CAN-bus interfaces now allow plug-and-play sensor installs, slashing labor costs by 60%. Retrofit operators can outfit legacy machinery for under USD 500, broadening access for small contractors and farms. This pricing shift is a powerful tailwind for the off-highway vehicle telematics market, especially across emerging Asia-Pacific and Latin America.

Emerging AI-based predictive-maintenance marketplaces for rental fleets

Rental leaders such as United Rentals employ AI algorithms that parse engine hours, fuel burn, and duty cycles to anticipate failures, cutting unplanned breakdowns by 30% and saving up to USD 500,000 annually per large fleet. Marketplace platforms extend the same tools to mid-tier lessors on a pay-per-use model, democratizing predictive maintenance and widening the addressable base. With 70% of United Rentals’ Q1 2024 revenue already tied to digital services, AI maintenance is becoming a strategic differentiator for rental operators and a growth lever for the off-highway vehicle telematics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| End-user reluctance to alter legacy maintenance workflows | -1.8% | Global, with strongest resistance in traditional construction and agriculture sectors | Short term (≤ 2 years) |

| Shortage of certified telematics technicians in rural regions | -1.2% | Rural areas globally, particularly acute in APAC and Latin America | Medium term (2-4 years) |

| Data-sovereignty and cybersecurity compliance costs for cross-border fleets | -0.9% | EU, North America, and increasingly APAC markets | Long term (≥ 4 years) |

| Fragmented satellite subscription pricing models inhibiting small-fleet uptake | -0.7% | Global, with particular impact on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

End-user reluctance to alter legacy maintenance workflows

Many family-owned contractors and farms rely on visual inspections and mechanic intuition rather than dashboards rich in analytics, citing “data overload” and workflow disruption. Resistance is heightened where technicians lack data-analysis skills, leading to parallel paper logs that undercut digital gains. Gradual rollouts that begin with simple location tracking before moving to predictive algorithms have proven most successful, indicating cultural change—not technology—is the critical adoption hurdle for the off-highway vehicle telematics market.

Shortage of certified telematics technicians in rural regions

Telematics hardware now blends electronics, networking, and analytics, yet rural vocational programs graduate only 20–30 specialists per year per site, far short of need. OEM initiatives such as Kubota TECH and John Deere Tech introduce scholarships and mobile classrooms, but it will take several academic cycles to narrow the gap. In the interim, dealers rely on remote diagnostics and video support, limiting the scalability of advanced telematics features and restraining growth for the off-highway vehicle telematics market in hard-to-service territories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software momentum transforms value creation

Hardware retained a 53.65% share in 2025 because every deployment still begins with a telematics control unit, sensors, and antennas. Yet software’s 15.72% CAGR illustrates how the off-highway vehicle telematics market is evolving from basic tracking to advanced data analytics. The off-highway vehicle telematics market size associated with cloud platforms, AI engines, and visualization tools will outpace hardware outlays over the forecast period, reflecting demand for insight rather than raw data.

Service revenue grows in parallel as fleets lean on experts for installation, API integration, and ongoing optimization. Caterpillar’s generative-AI service engine, which mines data from 1.5 million connected assets, demonstrates how software and services combine to lift customer uptime and satisfaction. As the user base expands, subscription tiers tailored to equipment class, fleet size, and compliance needs will deepen software penetration across mixed-brand environments.

By Connectivity: Dual-mode fills the last mile

With a 58.55% share in 2025, 4G and 5G cellular remain the baseline for day-to-day data traffic. However, equipment that roams outside carrier footprints—open-pit mines, large farms, remote forestry tracts—demands seamless fail-over. Dual-mode cellular-satellite systems growing at 15.12% CAGR guarantee continuity without manual intervention, sustaining analytics pipelines and regulatory logs.

John Deere’s integration of Starlink antennas shows how OEMs package satellite as standard on premium tractors, turning downtime black spots into fully traceable acreage. Meanwhile, local mesh networks that combine Wi-Fi, Bluetooth, or ultra-wideband link neighboring machines to share collision warnings and firmware updates. Together, these hybrid topologies underpin the next phase of the off-highway vehicle telematics market.

By Solution Type: Factory install gains critical mass

Aftermarket kits still dominate with a 52.60% share because many fleets run mixed brands or older models. Yet OEM-embedded systems’ 16.35% CAGR through 2031 signals a structural pivot toward factory integration on new iron. Out-of-the-box telematics unlock proprietary engine, hydraulic and emissions data—capabilities that generic add-ons cannot fully access.

Komatsu’s KOMTRAX streams parameter-level diagnostics directly from controllers, enabling predictive interventions that trim downtime for mine operators. For owners of heterogeneous fleets, AEMP 2.0 standardization allows aftermarket portals to ingest OEM data side by side, ensuring that the off-highway vehicle telematics market continues to serve both integration models.

By Vehicle Type: Material-handling machines accelerate fastest

Construction equipment generated 43.85% of the 2025 volume because earth-moving, lifting, and paving machinery form the core of infrastructure projects. Still, forklifts, reach-stackers, and other material-handling units are on track for 15.62% CAGR on the back of e-commerce and automated warehouses. Telematics on lift trucks optimizes traffic flow, monitors impact events, and triggers geo-fenced speed limits, directly influencing safety and throughput.

Agriculture, mining, and forestry each pursue domain-specific outcomes—from precision yield mapping to autonomous haulage and sustainable harvesting—but they converge on the same data backbone. As advanced sensors reach price parity, the off-highway vehicle telematics market will see AI layers migrate across vehicle classes, compounding returns for operators diversifying into multiple verticals.

By End-user Industry: Rental fleets set the digital benchmark

Construction firms retained a 48.25% share in 2025, reflecting their sizeable equipment bases and tight project schedules. Yet rental and leasing fleets are expanding at 15.89% CAGR because telematics feed directly into the rental business model: higher utilization, theft deterrence, and value-added services. United Rentals connects more than 375,000 assets and credits digital tools for 70% of Q1 2024 revenue, exemplifying how data drives competitive advantage.

Agricultural co-ops adopt machine data to fine-tune seeding and spraying timetables, while mining firms focus on safety analytics. Forestry operators deploy geo-fencing to comply with environmental corridors. This cross-sector adoption confirms that the off-highway vehicle telematics market is far broader than a single vertical and will increasingly pivot around flexible, user-specific applications.

Geography Analysis

North America led the off-highway vehicle telematics market in 2025 with a 36.35% share, aided by well-established dealer networks, robust enforcement of emissions and safety rules, and a culture of data-driven fleet management. High disposable incomes and large contractor fleets translate into steady hardware refresh cycles and rapid uptake of subscription services. OEM-dealer partnerships further simplify onboarding, ensuring that even mid-tier owners gain access to analytics dashboards without heavy IT overhead.

Europe follows closely, propelled by Stage V emissions controls and region-wide carbon-reduction mandates that oblige equipment owners to document particulate and NOx data continually. Incentive programs in Germany and Scandinavia reward fleets that integrate telematics-based carbon accounting, driving stronger platform adoption for compliance and ESG reporting. Additionally, the EU’s General Data Protection Regulation forces vendors to engineer privacy-by-design solutions, giving European customers confidence to expand telematics footprints.

Asia-Pacific represents the growth engine, projected at a 15.78% CAGR through 2031. China’s Belt and Road Initiative and India’s National Infrastructure Pipeline collectively require millions of new machines, most factory-equipped with telematics for performance tracking. Local manufacturing keeps device costs low, accelerating penetration among cost-sensitive buyers. National governments also deploy precision-farming subsidies that reimburse farmers for connected equipment, ensuring that the off-highway vehicle telematics market spreads beyond megacities into rural provinces. While technician shortages remain acute in parts of Southeast Asia, OEMs are rapidly opening training academies and remote diagnostic centers to bridge the gap.

Competitive Landscape

The off-highway vehicle telematics market displays moderate fragmentation. Large OEMs leverage vertical stacks that pair hardware with proprietary data lakes and value-added analytics. Caterpillar, for example, generated USD 24 billion in services revenue in 2024 as VisionLink managed more than 1.5 million connected assets. [4]Construction Briefing, “Caterpillar CEO on tariffs,” constructionbriefing.com Komatsu and John Deere mirror this approach, bundling subscription offers at the equipment point of sale to secure recurring cash flows and strengthen equipment stickiness.

Specialized telematics vendors pursue a horizontal strategy, positioning themselves as brand-agnostic hubs that unify mixed fleets. ORBCOMM supplies rugged satellite modems for mining dumpers, Geotab focuses on AI-driven risk scoring, and Trackunit emphasizes construction theft prevention. Their edge lies in open APIs, rapid innovation cycles, and the ability to integrate data from dozens of OEM feeds into one dashboard. Partnership models are common; for instance, rental majors align with sensor makers to co-develop utilization dashboards that differentiate their service packages.

Emerging players—in fields like satellite connectivity, AI-driven maintenance, or carbon-credit platforms—challenge incumbents by collapsing infrastructure barriers and exploiting unmet regulatory pain points. Starlink’s broadband constellation offers OEMs a path to global coverage without carrier contracts, while AI start-ups analyze anonymized population-scale datasets to predict component failures weeks in advance. The balance between vertical depth and horizontal reach will define competitive advantage over the next half-decade.

Off-Highway Vehicle Telematics Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Deere & Company

CNH Industrial N.V.

Volvo Construction Equipment AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: John Deere introduced operator-assistance features on 900 M-Series tracked feller-bunchers to boost productivity and ease fatigue.

- March 2025: Bobcat launched Machine IQ enhancements, including remote engine disable/enable for improved security across connected equipment.

- March 2025: Kioti rolled out Kioti Connect for RX and HX tractors, supplying three-year predictive-maintenance access at no cost.

- February 2025: Komatsu unveiled new skid-steer and compact track loaders with Stage V engines and built-in telematics at Bauma 2025.

- February 2025: John Deere and GUSS Automation debuted an electric option with the Smart Apply upgrade for autonomous sprayers.

- December 2024: Mack Trucks introduced an AI-driven Premium Service Contract that adapts maintenance intervals in real time.

- November 2024: John Deere completed Starlink tests for rural connectivity ahead of the broader rollout.

- October 2024: Komatsu acquired Octodots Analytics to bolster AI-based fleet management for mines.

Global Off-Highway Vehicle Telematics Market Report Scope

Off-highway vehicle telematics solutions continuously monitor device location status, status using OHV telematics devices that support GPS, cellular, or satellite connectivity to access real-time device data. The use of technology in the industry has been beneficial, vehicle telematics has proved to be very efficient in real-time for drivers, car owners, and fleet managers. The global Off-Highway Vehicle Telematics Market is segmented By End-user Industry (Construction, Agriculture, Mining, Forestry), and Geography.

| Hardware |

| Software |

| Services |

| Cellular |

| Satellite |

| Dual-Mode (Cell + Satellite) |

| Short-Range (Wi-Fi / BLE / UWB) |

| OEM-Embedded |

| Aftermarket-Installed |

| Construction Equipment | Earth-moving |

| Lifting | |

| Road-building | |

| Agricultural Machinery | Tractors |

| Harvesters | |

| Implements | |

| Mining Equipment | Surface |

| Underground | |

| Forestry Machinery | Feller-bunchers |

| Forwarders | |

| Material-Handling and Others | Cranes |

| Forklifts | |

| ATVs |

| Construction |

| Agriculture |

| Mining |

| Forestry |

| Rental and Leasing Fleets |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Connectivity | Cellular | ||

| Satellite | |||

| Dual-Mode (Cell + Satellite) | |||

| Short-Range (Wi-Fi / BLE / UWB) | |||

| By Solution Type | OEM-Embedded | ||

| Aftermarket-Installed | |||

| By Vehicle Type | Construction Equipment | Earth-moving | |

| Lifting | |||

| Road-building | |||

| Agricultural Machinery | Tractors | ||

| Harvesters | |||

| Implements | |||

| Mining Equipment | Surface | ||

| Underground | |||

| Forestry Machinery | Feller-bunchers | ||

| Forwarders | |||

| Material-Handling and Others | Cranes | ||

| Forklifts | |||

| ATVs | |||

| By End-user Industry | Construction | ||

| Agriculture | |||

| Mining | |||

| Forestry | |||

| Rental and Leasing Fleets | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the off-highway vehicle telematics market?

Stringent emissions regulations, falling device costs and new satellite constellations that eliminate coverage gaps together underpin the 13.28% CAGR forecast through 2031.

Which segment is expanding the fastest within the off-highway vehicle telematics market?

Software platforms that translate raw machine data into predictive maintenance and fleet optimization insights are growing at 15.72% CAGR, outpacing hardware and services.

Why are rental fleets adopting telematics more aggressively than other end-users?

Telematics boosts rental profitability by increasing asset utilization, preventing theft and enabling premium digital services—drivers that support rental’s 15.89% CAGR outlook.

How are low-orbit satellites impacting telematics deployments?

New LEO networks provide continuous connectivity in remote mines and farms, enabling real-time analytics where cellular coverage is unreliable and unlocking additional ROI.

What challenges could hamper telematics adoption in the near term?

Reluctance to change legacy maintenance routines and a shortage of certified technicians in rural areas remain primary obstacles, trimming forecast growth by an estimated 3%.

Which regions offer the highest incremental opportunity for vendors?

Asia-Pacific leads on growth potential with a 15.78% regional CAGR, fueled by infrastructure megaprojects in China and India plus government incentives for connected agriculture.

Page last updated on: