Market Overview

| Study Period | 2020 - 2031 |

|---|---|

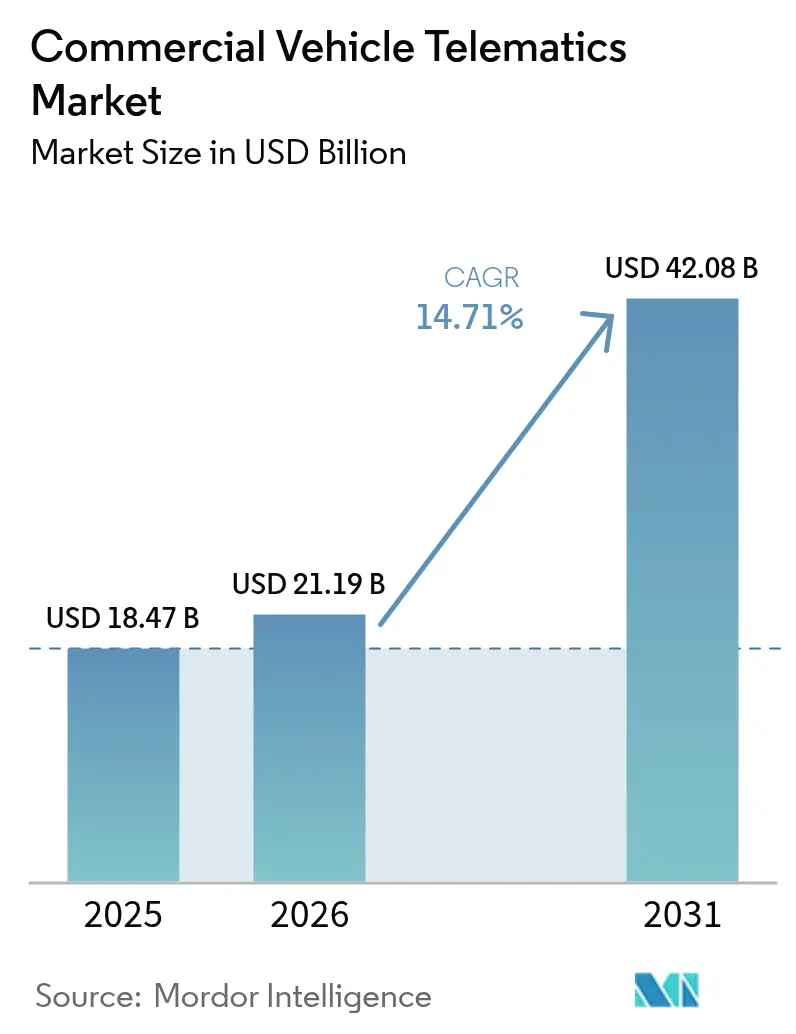

| Market Size (2026) | USD 21.19 Billion |

| Market Size (2031) | USD 42.08 Billion |

| Growth Rate (2026 - 2031) | 14.71% CAGR |

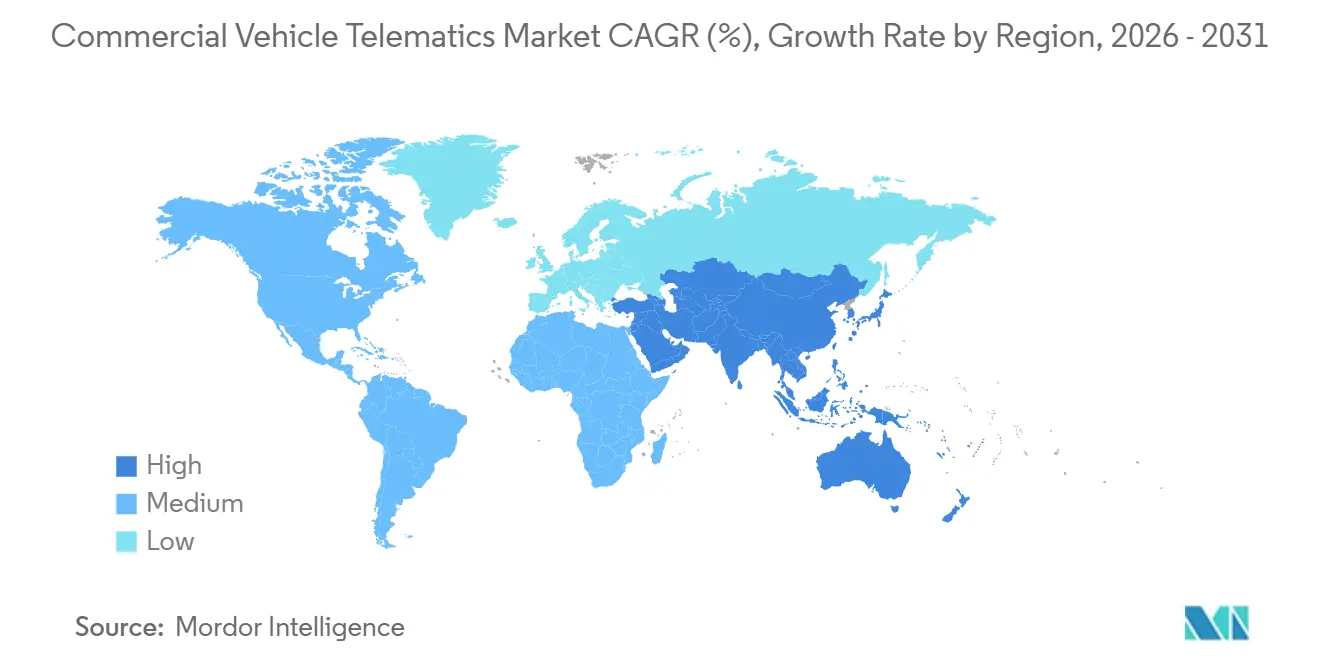

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Vehicle Telematics Market Analysis by Mordor Intelligence

The commercial vehicle telematics market size is expected to increase from USD 18.47 billion in 2025 to USD 21.19 billion in 2026 and reach USD 42.08 billion by 2031, growing at a CAGR of 14.71% over 2026-2031. Operators are moving past basic location tracking toward connected-asset strategies that improve fuel efficiency, driver safety, and vehicle uptime. Regulatory deadlines for electronic logging devices, the factory-fitment of telematics hardware by truck makers, and the rapid infusion of artificial intelligence into routing and maintenance workflows are reshaping total cost of ownership calculations. Rising e-commerce volumes have spawned large last-mile delivery fleets that adopt connectivity by default, while subscription-based data marketplaces allow operators to monetize anonymized insights, offsetting monthly service fees. These themes, together with the need to manage battery health in zero-emission trucks, sustain double-digit expansion even as hardware prices fall and competition intensifies.

Key Report Takeaways

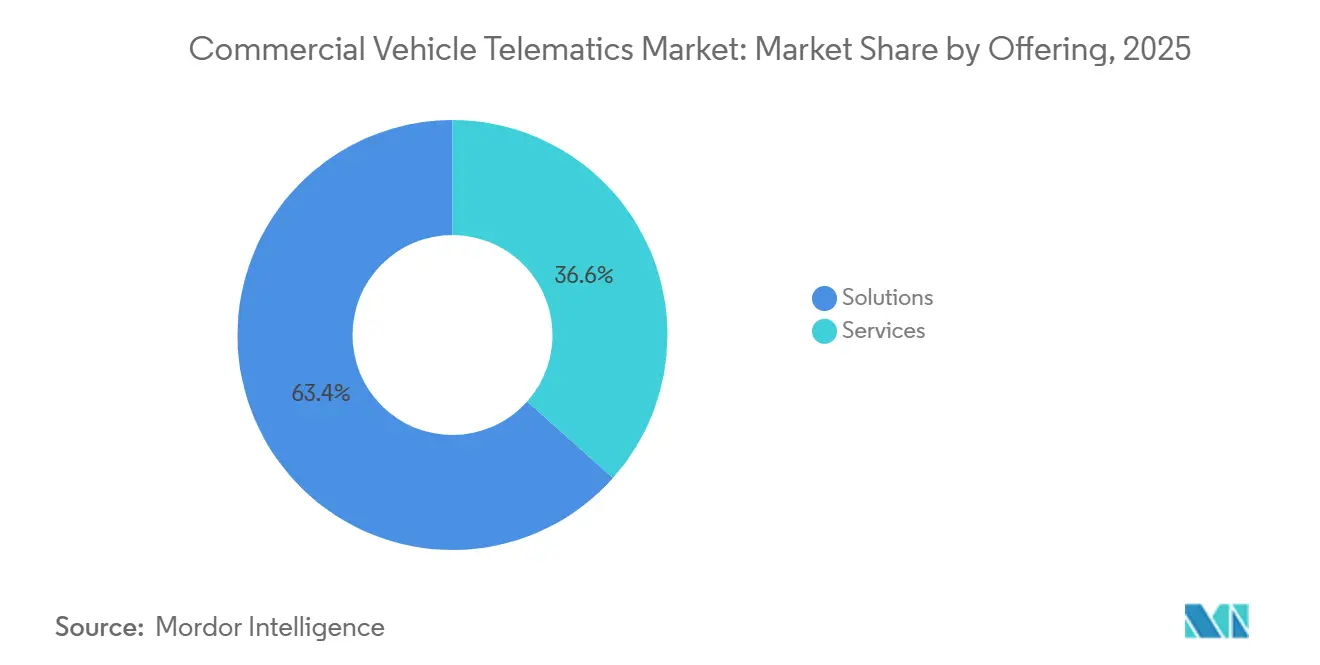

- By offering solutions, the company captured 63.42% of revenue in 2025, while services are projected to expand at a 15.11% CAGR to 2031.

- By provider type, OEM platforms held 58.71% of the commercial vehicle telematics market size in 2025; aftermarket systems deliver the highest 15.14% CAGR over the forecast horizon.

- By vehicle class, light commercial vehicles accounted for 48.89% of revenue in 2025, yet heavy and medium trucks are set to grow at a 15.17% CAGR through 2031.

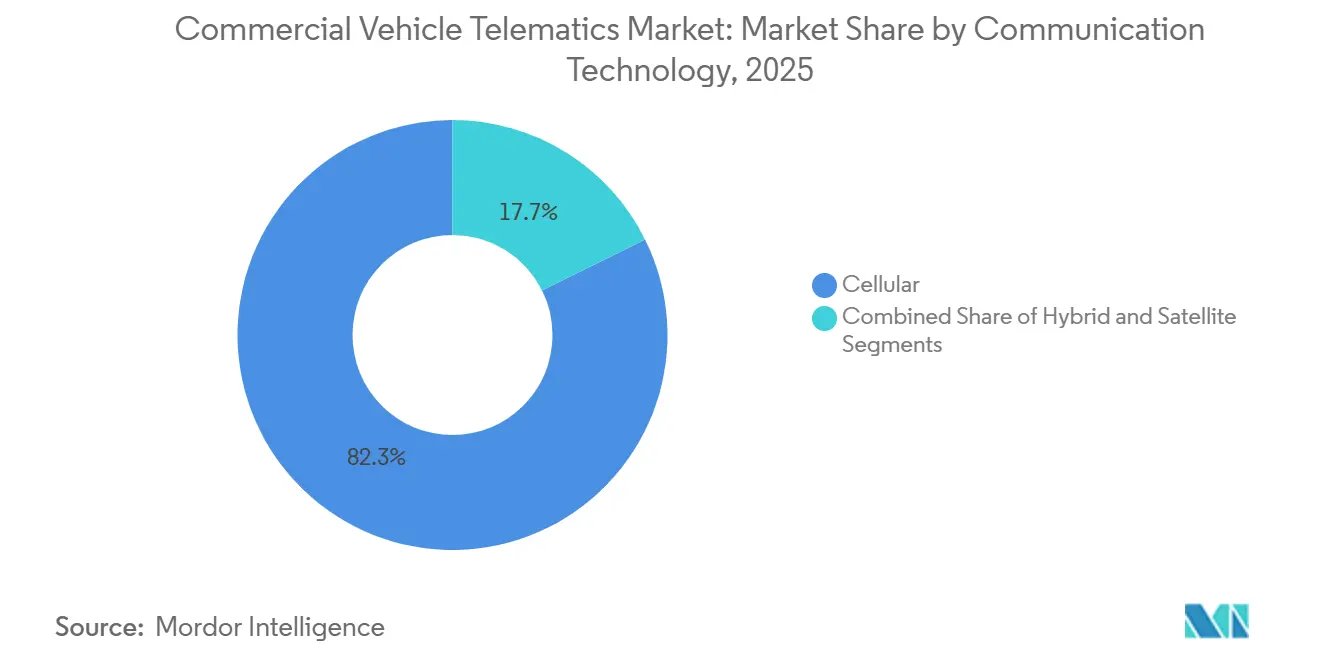

- By communication technology, cellular connectivity dominated with 82.33% share in 2025, but hybrid architectures are climbing at a 15.38% CAGR.

- By end-user vertical, transportation and logistics accounted for 39.63% of demand in 2025, while construction and mining are the fastest-growing segments at a 16.19% CAGR to 2031.

- By geography, North America led the commercial vehicle telematics market with a 34.66% share in 2025, while Asia-Pacific is advancing at the fastest 15.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Vehicle Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Factory-Installed OEM Telematics in Heavy Trucks | +3.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Mandatory Electronic Logging-Device and Safety Regulations | +2.9% | North America, Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Demand for AI-Driven Fleet Optimisation to Cut Total Cost of Ownership | +2.6% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rapid Expansion of Last-Mile E-Commerce Delivery Fleets | +2.4% | Global, highest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Emergence of Subscription-Based Telematics Data Marketplaces | +1.8% | North America and Europe, early Asia-Pacific | Long term (≥ 4 years) |

| Integration of Telematics with Zero-Emission Truck Energy and Charge Management | +1.7% | Europe and North America, expanding Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Factory-Installed OEM Telematics in Heavy Trucks

Truck makers now pre-install telematics units on the assembly line, giving fleets instant access to vehicle data without downtime for retrofits. Daimler Truck, for instance, links its TruckCharge software to factory devices so operators fine-tune charging stops for electric tractors.[1]Daimler Truck, “TruckCharge Network Launch,” daimlertruck.com Volvo Trucks surpassed one million connected heavy units, streaming diagnostics that cut surprise breakdowns and fuel waste. TRATON reported 1.15 million connected trucks across its Scania, MAN, and Navistar brands, turning data subscriptions into a margin lever. Factory integration lowers lifetime hardware cost per truck, yet raises switching barriers when fleets run mixed brands, pushing software vendors to aggregate multiple OEM feeds in one dashboard.

Mandatory Electronic Logging-Device and Safety Regulations

Governments require electronic logging devices to police driver hours, making telematics compulsory rather than optional. The Federal Motor Carrier Safety Administration conducts roadside audits that pull hours-of-service files directly from cab units.[2]FMCSA, “Electronic Logging Devices,” fmcsa.dot.gov Europe’s smart tachograph upgrade aligns with working-time directives, forcing fleets to replace first-generation recorders by 2026. India’s transport ministry mandates location tracking and an emergency button on trucks and buses, accelerating adoption across a price-sensitive market. Complying with different regional standards inflates engineering costs, but the rulebook still guarantees baseline device demand for vendors.

Demand for AI-Driven Fleet Optimisation to Cut Total Cost of Ownership

Artificial intelligence now parses engine, route, and video data to squeeze every dime from fuel and maintenance budgets. A joint study by Einride and Fraunhofer showed AI routing and predictive service can drive 8%–13% total cost savings for mixed diesel and electric fleets.[3]Einride, “Total Cost of Ownership Study for Electric and Diesel Heavy-Duty Fleets,” einride.tech Deloitte’s latest outlook notes that unplanned downtime drops by up to 25% when machine-learning models spot early signs of brake wear or coolant issues. Motive Technologies adds computer-vision dashcams that lower collision frequency by 80%, trimming insurance bills for policyholders. With payback measured in months, procurement teams prioritize platforms that bundle AI analytics with compliance and dispatch tools.

Rapid Expansion of Last-Mile E-Commerce Delivery Fleets

Soaring online orders compel carriers to add thousands of light vans, all shipped with embedded trackers that feed real-time delivery apps. McKinsey estimates that last-mile work already accounts for 53% of shipping costs, so operators are pursuing telematics-enabled dynamic routing to shave 15%–30% off travel time. Retail giants like Amazon and Walmart internalize logistics, building proprietary telematics stacks that pressure traditional parcel firms to modernize. The United States Postal Service is rolling out fleet-wide connectivity to boost route efficiency and cut fuel spend, signaling public-sector momentum. This arms race fuels record device orders and recurring data-service contracts for vendors who can scale quickly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security Vulnerabilities in Connected Commercial Vehicles | -1.4% | Global, heightened in North America and Europe | Short term (≤ 2 years) |

| Fragmented Connectivity Infrastructure in Developing Regions | -1.2% | Africa, South America, rural Asia-Pacific | Medium term (2-4 years) |

| Cost and ROI Concerns for Small Fleet Operators | -0.9% | Global, acute in emerging markets | Medium term (2-4 years) |

| Data-Ownership and Privacy-Compliance Hurdles | -0.7% | Europe, North America, expanding Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Vulnerabilities in Connected Commercial Vehicles

Rolling computers on wheels expose braking, steering, and payload systems to hackers. The European Union’s WP.29 regulation now obliges truck makers to certify secure development practices and ensure life-cycle patching, but millions of legacy units lack encrypted boot loaders. A 2025 report from the EU Agency for Cybersecurity warns that over-the-air updates introduce new attack vectors if cryptographic keys are poorly managed. High-profile breaches could immobilize fleets or compromise cargo, delaying investment among risk-averse small operators until vendors add intrusion detection and bundled cyber insurance. As security hardening raises device cost, buyers weigh the price premium against potential liability.

Fragmented Connectivity Infrastructure in Developing Regions

Outside dense corridors, cellular dead zones hobble real-time tracking. Store-and-forward modes delay driver coaching and exception alerts, limiting the operational upside for fleets in rural Africa, inland South America, and interior Asia. Deloitte notes operators often pay for dual-mode cellular-satellite hardware, doubling airtime spend to maintain uptime. Hybrid modems improve coverage but add provisioning complexity, prolonging deployment schedules. Until governments or mobile carriers fill the gaps in remote areas, uptake remains muted in regions that arguably need fleet visibility the most.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Expand as Managed Models Gain Traction

Solutions held 63.42% of commercial vehicle telematics market revenue in 2025, covering tracking, driver management, insurance telematics, compliance, V2X, predictive maintenance, and asset monitoring. Services are projected to outpace the overall market, with a 15.11% CAGR to 2031, as operators prefer predictable operating budgets to capital outlays. The commercial vehicle telematics market for managed services is growing as vendors now bundle hardware, airtime, analytics, and support into a single invoice that scales with fleet count.

Fleet tracking remains the largest solution subset, yet predictive maintenance gains ground as downtime penalties escalate. Professional services such as system integration and custom analytics are critical for large, mixed-asset fleets that link legacy dispatch systems with modern cloud dashboards. Managed offerings resonate with small carriers lacking full-time IT staff, tipping contract awards toward providers that guarantee uptime, remote troubleshooting, and compliance reporting with minimal operator intervention.

By Provider Type: Aftermarket Retrofit Demand Surges in Aging Fleets

OEM channels accounted for 58.71% of revenue in 2025 because factory-installed units are shipped with every new heavy truck platform. Meanwhile, aftermarket vendors post a 15.14% CAGR as retrofit kits modernize older vehicles that still dominate many regional haul and vocational operations. The commercial vehicle telematics market share remains split as operators weigh deep vehicle-network integration from OEM devices against the vendor neutrality and faster innovation cadence of aftermarket plugs.

Mixed-brand fleets welcome middleware that consolidates proprietary OEM data feeds under a single user interface, reducing dispatcher workload. OEMs respond by opening APIs and co-marketing hybrid packages with leading aftermarket dashboards. This coopetition model preserves hardware standardization leverage for truck builders while satisfying fleets that demand analytics uniformity across diverse brands and model years.

By Vehicle Class: Heavy and Medium Trucks Face Regulatory Pressure

Light commercial platforms generated 48.89% revenue in 2025, reflecting their sheer numbers in parcel, service, and utility fleets. Heavy and medium trucks, however, are forecast to grow 15.17% annually because they attract higher per-unit telematics spend driven by electronic logging mandates and energy-management needs in electrified drivelines. The commercial vehicle telematics market for heavy tractors continues to expand as OEMs roll out battery-state-of-health dashboards, charger reservation tools, and over-the-air powertrain firmware updates that operators view as mission-critical.

Regulatory oversight of driver hours, weight compliance, and environmental footprints concentrates on heavy segments, making telematics non-optional. Light vans benefit from lower device price points and quick installations, yet their revenue intensity per vehicle is modest compared to a long-haul Class-8 tractor equipped with multiple cameras, advanced driver-assistance sensors, and 5G gateways. Consequently, vendors pursue margin by upselling premium analytics to heavy-duty operators even as they chase volume in light-duty delivery fleets.

By Communication Technology: Hybrid Architectures Hedge Coverage Gaps

Cellular maintained an 82.33% share in 2025 thanks to ubiquitous 4G LTE, falling module costs, and competitive data-plan pricing. Hybrid solutions combining cellular with satellite or Wi-Fi backhaul are set to grow at a 15.38% CAGR as operators demand always-on visibility for safety-critical functions. The commercial vehicle telematics market share tied to hybrid modems will rise when fleets hauling high-value cargo cross deserts, mountains, or maritime routes where cellular coverage is intermittent.

5G rollouts in North America, Europe, and advanced Asia-Pacific economies promise sub-50 ms latency, enabling real-time video streaming and cooperative driving features. Yet rural blind spots persist, pushing fleets to specify dual-mode devices that automatically switch to satellite for exception alerts. Vendors partner with mobile network operators to aggregate traffic volumes and secure bulk airtime discounts, passing savings to fleets while protecting margins.

By End-User Vertical: Construction and Mining Adoption Accelerates

Transportation and logistics accounted for 39.63% demand in 2025, reflecting the sector’s early embrace of connectivity for routing and compliance. Construction and mining, though smaller, will post the fastest 16.19% CAGR to 2031 as off-highway equipment managers seek real-time utilization dashboards, fuel-burn analytics, and operator safety coaching. The commercial vehicle telematics market, tied to yellow-iron machinery, is expanding as quarry owners and contractors integrate engine-hour data with enterprise resource planning systems for preventive maintenance scheduling.

Retail and e-commerce fleets emphasize proof-of-delivery and customer notification workflows, while utilities leverage telematics for crew dispatch and hazardous-material compliance. Insurance and leasing firms embed devices to enable usage-based premium structures, aligning risk pricing with actual driving behavior. Public-sector emergency services deploy connectivity to optimize response times and asset allocation. The diversity of requirements encourages vendors to build vertical-specific templates and analytics modules that plug into a common cloud backbone.

Geography Analysis

North America retained 34.66% of the commercial vehicle telematics market revenue in 2025, owing to strict hours-of-service enforcement and dense cellular coverage. Large enterprise haulers have largely completed rollouts, so incremental growth stems from municipal, postal, and small-fleet segments that sign managed-service deals rather than self-hosting software. The rising adoption of battery-electric delivery trucks, particularly in California compliance zones, is boosting demand for integrated energy-management dashboards that forecast range and direct drivers to charging stations. Cross-border carriers link United States, Canadian, and Mexican operations under unified compliance portals despite patchy rural coverage in northern Canada and southern Mexico.

Asia-Pacific carries the fastest 15.78% CAGR through 2031. China enforces connected-vehicle targets that compel OEMs to embed devices, while domestic logistics giants integrate telematics with warehouse automation and ride-hailing style freight platforms. India’s emergency-button and location-tracking mandate removes cost-sensitive barriers, pushing basic units into millions of trucks and buses. Japan combats driver shortages with route-optimization algorithms, and South Korea funds 5G-based smart logistics corridors. Rural coverage gaps and the prevalence of low-cost local suppliers temper average revenue per unit, but volume outweighs pricing headwinds, expanding total regional spend.

Europe combines mature adoption with stringent data privacy and cybersecurity rules. Digital tachograph stage-II upgrades, low-emission zones, and zero-emission truck incentives keep replacement cycles brisk. Operators increasingly purchase software-defined services that unlock enhanced analytics without swapping hardware, aligning with over-the-air update strategies from Volvo and Daimler. Growth moderates as large fleets complete full penetration, pushing vendors to upsell managed analytics and battery optimization modules tied to the commercial vehicle telematics market. Eastern European corridors offer white-space opportunities where road freight is rising, but connectivity penetration still trails Western averages.

South America, the Middle East, and Africa collectively post mid-teens growth from smaller bases. Brazil’s dense agribusiness corridors demand asset tracking across remote plantations, yet macro-economic volatility slows capital budgets. Gulf Cooperation Council states invest in smart-city freight initiatives that bundle telematics with automated tolling and green-zone enforcement. Africa’s challenge remains network coverage, although mining companies in South Africa and Botswana adopt satellite-linked units to manage high-value equipment. Government fleet-digitization programs across Egypt and Saudi Arabia spur public-sector uptake, providing anchor accounts for international vendors.

Competitive Landscape

The commercial vehicle telematics market is moderately fragmented. Independent platform leaders such as Geotab, Samsara, and Trimble compete with telecom-backed Verizon Connect and OEM captives from Daimler, Volvo, and TRATON. Geotab’s integration with Daimler Trucks exemplifies hybrid ecosystems where aftermarket dashboards surface proprietary OEM diagnostics inside a common interface. Samsara grows enterprise accounts by pairing AI dashcams with driver-coaching workflows, recording USD 300 million revenue in calendar 2025. Verizon Connect leverages its parent’s network assets to bundle airtime, devices, and analytics into turnkey contracts, challenging smaller specialists on price and coverage quality.

Strategic moves concentrate on three fronts. First, vertical integration: Lytx merges video safety with telematics to offer unified risk scoring, and GPS Trackit absorbs Zonar Systems to combine inspection tools with tracking. Second, horizontal expansion: platforms add support for trailers, forklifts, and refrigerated containers, widening wallet share per fleet. Third, ecosystem orchestration: open APIs invite insurers, maintenance software vendors, and fuel card providers to build apps that leverage telematics data, embedding the host platform at the operational core of fleet customers.

White-space opportunities include energy-management telemetry for battery-electric and hydrogen trucks, cargo-centric trailer tracking, and anonymized data exchanges that sell road-condition information to mapping companies and city planners. Compliance with ISO/SAE 21434 cybersecurity standards is turning into a ticket-to-play for Tier-1 OEM partnerships, separating well-capitalized vendors from smaller entrants. Price competition remains fiercest in North America and Europe, but Asia-Pacific’s fragmented regulatory landscape allows local firms to thrive on country-specific compliance features, forcing multinationals to localize software rapidly.

Commercial Vehicle Telematics Industry Leaders

Verizon Communications Inc.

Geotab Inc.

Samsara Inc.

Trimble Inc.

Powerfleet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Lytx announced the general availability of Lytx+ with Geotab GO Anywhere, integrating its video safety platform with Geotab hardware for unified driver behavior analytics.

- September 2025: Volvo Trucks confirmed surpassing one million connected trucks worldwide, enabling predictive maintenance, fuel coaching, and remote diagnostics services.

- August 2025: Motive Technologies raised USD 150 million to expand its AI fleet platform after reporting an 80% collision reduction among customers using its dashcam-telematics suite.

- June 2025: Daimler Truck and Volvo Group formed Coretura, a joint venture developing a software-defined commercial-vehicle platform that embeds telematics and supports third-party apps.

Global Commercial Vehicle Telematics Market Report Scope

The Commercial Vehicle Telematics Market Report is Segmented by Offering (Solutions and Services), Provider Type (Original Equipment Manufacturer, and Aftermarket), Vehicle Class (Light Commercial Vehicles, and Heavy and Medium Commercial Vehicles), Communication Technology (Cellular, Satellite, Hybrid), End-User Vertical (Transportation and Logistics, Construction and Mining, Public Sector and Emergency Services, Utilities, Insurance and Leasing, Retail and E-Commerce, Other End-User Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Fleet Tracking and Monitoring |

| Driver Management | |

| Insurance Telematics | |

| Safety and Compliance | |

| V2X Solutions | |

| Predictive Maintenance and Diagnostics | |

| Asset and Trailer Tracking | |

| Services | Professional Services |

| Managed Services |

By Provider Type

| Original Equipment Manufacturer |

| Aftermarket |

By Vehicle Class

| Light Commercial Vehicles |

| Heavy and Medium Commercial Vehicles |

By Communication Technology

| Cellular |

| Satellite |

| Hybrid |

By End-User Vertical

| Transportation and Logistics |

| Construction and Mining |

| Public Sector and Emergency Services |

| Utilities |

| Insurance and Leasing |

| Retail and E-Commerce |

| Other End-User Verticals |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Offering | Solutions | Fleet Tracking and Monitoring | |

| Driver Management | |||

| Insurance Telematics | |||

| Safety and Compliance | |||

| V2X Solutions | |||

| Predictive Maintenance and Diagnostics | |||

| Asset and Trailer Tracking | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Provider Type | Original Equipment Manufacturer | ||

| Aftermarket | |||

| By Vehicle Class | Light Commercial Vehicles | ||

| Heavy and Medium Commercial Vehicles | |||

| By Communication Technology | Cellular | ||

| Satellite | |||

| Hybrid | |||

| By End-User Vertical | Transportation and Logistics | ||

| Construction and Mining | |||

| Public Sector and Emergency Services | |||

| Utilities | |||

| Insurance and Leasing | |||

| Retail and E-Commerce | |||

| Other End-User Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the commercial vehicle telematics market by 2031?

It is forecast to reach USD 42.08 billion by 2031, supported by a 14.71% CAGR over 2026-2031.

Which region is expanding fastest in connected fleet solutions?

Asia-Pacific leads with a 15.78% CAGR as China and India roll out connected-vehicle mandates.

Why are services outpacing hardware sales in fleet telematics?

Operators prefer subscription models that bundle devices, connectivity, and analytics, driving services at a 15.11% CAGR.

How do OEM and aftermarket platforms differ for fleet managers?

OEM systems offer deep vehicle integration, while aftermarket solutions deliver brand-agnostic analytics and faster feature updates.

What role does telematics play in zero-emission trucking?

It monitors battery health, optimizes charging schedules, and ensures range reliability, making connectivity core to electric truck operations.

Which vertical shows the strongest growth potential?

Construction and mining is set to expand 16.19% annually as off-highway equipment adopts predictive maintenance and utilization analytics.

Page last updated on: