Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 204.84 Billion |

| Market Size (2031) | USD 477.47 Billion |

| Growth Rate (2026 - 2031) | 18.43% CAGR |

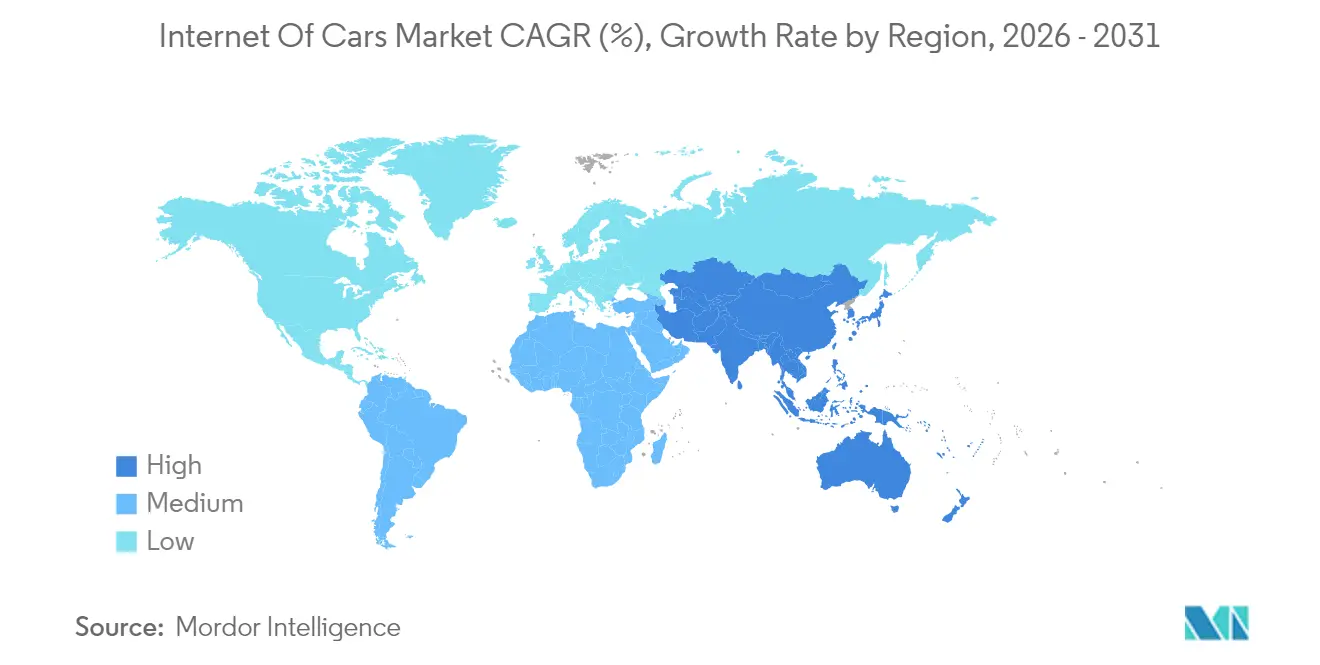

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Internet Of Cars Market Analysis by Mordor Intelligence

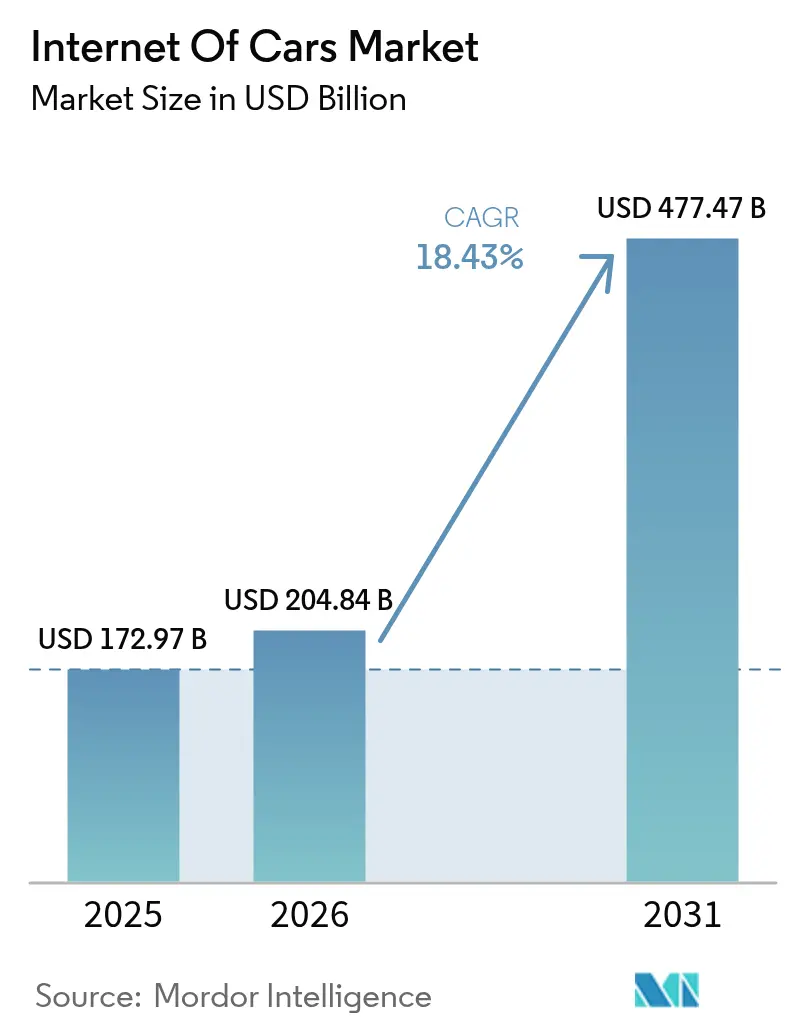

Internet of Cars market size in 2026 is estimated at USD 204.84 billion, growing from 2025 value of USD 172.97 billion with 2031 projections showing USD 477.47 billion, growing at 18.43% CAGR over 2026-2031. Vehicles are shifting from hardware‐centric products to connected data hubs, and this pivot is opening recurring software and services revenue streams for automakers. Large public investments in vehicle-to-everything infrastructure, insurers’ rapid move toward usage-based pricing, and 5G-enabled edge computing are reinforcing demand pull that legacy automotive supply chains were not built to satisfy. Competitive pressure is also intensifying as semiconductor houses and cloud platforms enter the value chain. At the same time, fragmented connectivity standards and heightened consumer privacy concerns threaten to slow adoption if governance frameworks fail to keep pace with technical progress.

Key Report Takeaways

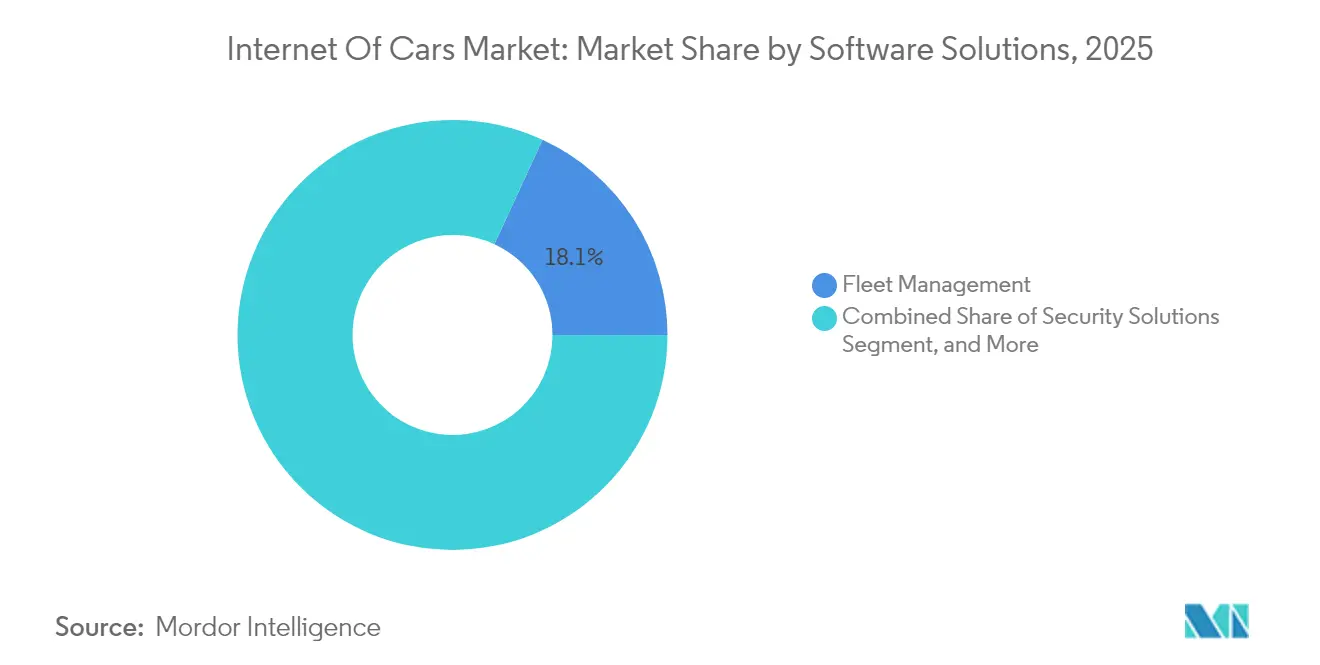

- By software solutions, fleet management led with 18.12% of the Internet of Cars market share in 2025, while security software is forecast to expand at a 18.92% CAGR through 2031.

- By hardware components, telematics control units held a 12.18% share of the Internet of Cars market size in 2025, and embedded modems are projected to advance at a 19.76% CAGR between 2026 and 2031.

- By connectivity technology, 5G cellular-V2X commanded an 10.98% share in 2025 and is expected to grow at a 20.98% CAGR over the forecast period.

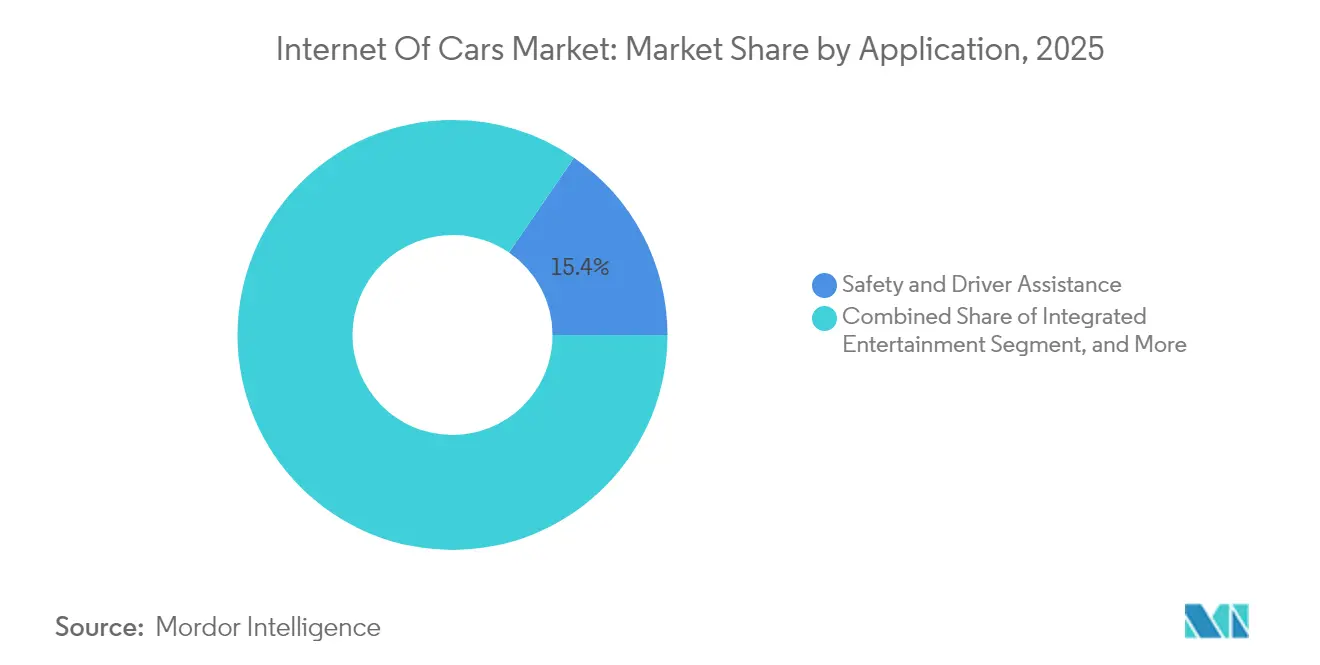

- By application, safety and driver assistance accounted for 15.44% of demand in 2025, whereas integrated entertainment is the fastest-growing segment, with a 19.21% CAGR to 2031.

- By end-user industry, automotive OEMs captured a 22.05% revenue share in 2025; however, ride-hailing and car-sharing fleets are projected to advance at a 20.04% CAGR during 2026-2031.

- By geography, the Asia Pacific region dominated with a 33.62% share in 2025 and is on track to register the highest regional CAGR of 19.02% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Internet Of Cars Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Government Funding for V2X Infrastructure | +3.2% | Global, with concentration in China, the United States, the European Union, the Middle East | Medium term (2-4 years) |

| Integration of 5G and Edge Computing in Vehicle Platforms | +4.1% | Global, led by Asia Pacific and North America | Short term (≤ 2 years) |

| OEM Pivot Toward Data-Monetization Business Models | +3.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Insurer Adoption of Usage-Based Policies | +2.7% | North America and Europe core, expanding to the Asia Pacific | Short term (≤ 2 years) |

| Real-Time OTA Cybersecurity Frameworks | +2.3% | Global, regulatory-driven in Europe and North America | Short term (≤ 2 years) |

| Smart City Mandates in Middle-Income Economies | +2.5% | Asia Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Government Funding for V2X Infrastructure

National and regional authorities are underwriting roadside communication nodes, lowering the cost hurdle for private investors and speeding rollouts. The United States awarded USD 60 million in 2024 to equip 1,200 intersections with cellular Vehicle-to-Everything (V2X) hardware.[1]U.S. Department of Transportation, “V2X Infrastructure Grants and Deployment Programs,” TRANSPORTATION.GOV China mandated that all new highways integrate C-V2X by 2025, trimming deployment timelines by 18 months. The European Commission directed EUR 1.3 billion (USD 1.39 billion) toward cooperative transport systems along trans-European corridors. Saudi Arabia’s NEOM project earmarked USD 500 billion for a 5G-enabled mobility grid. To gain access to these funds, suppliers must document ISO 21434 cybersecurity compliance at the design stage.

Integration of 5G and Edge Computing in Vehicle Platforms

5G paired with multi-access edge computing is compressing latency to below 10 milliseconds, enabling safety-critical functions. Qualcomm’s Snapdragon Ride was shipped in production cars in 2024, featuring an integrated edge AI accelerator that processes sensor data locally.[2]Qualcomm Technologies, “Snapdragon Ride Platform,” QUALCOMM.COM Verizon and Nissan cut over-the-air update times to less than five minutes at 150 U.S. dealerships. China Mobile established 320 edge sites, which reduced the average travel time by 12% along a major freight corridor. European operators remain behind; Vodafone’s coverage reached only 8% of Germany’s autobahn network by the end of 2024.

OEM Pivot Toward Data-Monetization Business Models

Automakers are targeting subscription income to offset thinning hardware margins. General Motors generated USD 2 billion in platform revenue during Ultifi’s first year. Tesla’s Full Self-Driving subscription exceeded 500,000 users by September 2024. Ford created Ford Pro Intelligence to monetize fleet data, aiming for USD 1 billion in revenue by 2026. Still, GDPR audits found 22% of consent flows non-compliant in 2024, forcing costly redesigns.

Insurer Adoption of Usage-Based Policies

Carriers are incorporating telematics into their pricing algorithms. A SambaSafety survey found that 82% of U.S. insurers offered or planned to offer usage-based products by 2026.[3]SambaSafety, “Usage-Based Insurance Adoption Survey 2024,” SAMBASAFETY.COM Progressive’s Snapshot program enrolled 8 million vehicles and cut loss ratios by 18 percentage points. Allianz introduced pay-per-kilometer cover in Germany, supported by live traffic APIs. India allowed usage-based policies in 2024, with early movers issuing policies 30% faster.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Global Cellular-V2X Standards | -2.8% | Global, most acute in cross-border corridors between the United States, Europe, and China | Medium term (2-4 years) |

| High Upfront Cost of Telematics ECUs | -1.9% | Emerging markets in the Asia Pacific, Latin America, and Africa | Short term (≤ 2 years) |

| Skill Shortage in Automotive Software Engineering | -2.1% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Consumer Privacy Concerns Around In-Car Data Streams | -2.4% | Europe and North America core, expanding to the Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Global Cellular-V2X Standards

Inconsistent spectrum allocation is forcing automakers to engineer multiple hardware variants, which inflates costs and slows launches. The U.S. allows Wi-Fi devices in the 5.9 GHz band, which raises the risk of interference.[4]Federal Communications Commission, “5.9 GHz Band Allocation,” FCC.GOV Europe allows member states to choose between C-V2X and DSRC, resulting in a patchwork of different technologies. China has standardized on 3GPP Release 16, while Europe and the United States are moving to Release 17. Continental said maintaining separate variants added EUR 180 million (USD 193 million) to its 2024 R&D budget.

Consumer Privacy Concerns Around In-Car Data Streams

Reluctance to share driving data is limiting opt-in rates. A 2024 Deloitte survey found 68% of consumers unwilling to share real-time location data without compensation. GDPR fines totaled EUR 420 million (USD 450 million) against three automakers that bundled consent requests. California’s updated privacy act added USD 15 million in annual compliance costs per OEM. Tesla opened a Shanghai data center in 2024 to comply with China’s local storage rule.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Solutions: Security Spending Outpaces Fleet Platforms

Security software is forecast to grow at a 18.92% CAGR through 2031 as July 2024 UNECE rules require intrusion detection on every new model. Fleet management retained the largest share, at 18.12%, in 2025, highlighting the commercial fleets’ focus on uptime and route efficiency. Real-time transit systems gained momentum when the Los Angeles Metro reduced passenger wait times by eight minutes by connecting 2,300 buses. Remote monitoring has become routine for electric fleets that need battery health diagnostics. Bandwidth management tools are gaining popularity because Ford spent USD 120 million on cellular data in 2024, prior to deploying edge caching.

Demand for security is reconfiguring procurement. OEMs now insist suppliers show third-party ISO 21434 audits, adding up to nine months to product timelines. Vendors that pre-certified solutions reported faster design wins, positioning cybersecurity as the next pricing lever. Fleet platforms remain sticky, but over-the-air update orchestration is emerging as a cross-segment opportunity that software firms are racing to capture. As a result, the Internet of Cars market continues to migrate toward a software-first revenue profile.

By Hardware Components: Embedded Modems Displace Aftermarket Dongles

Telematics control units accounted for 12.18% of 2025 revenue; however, embedded 5G modems are projected to grow at a 19.76% CAGR to 2031. Qualcomm’s single-chip radio merges C-V2X and cellular broadband, shaving 30% off bill-of-materials costs. Vehicles shipped in 2024 carried an average of 17 connected sensors, up from 11 two years earlier. Continental’s 48-inch OLED cluster illustrates how human-machine interfaces are converging into software-defined cockpits.

Growth is constrained by semiconductor supply tightness; lead times for telematics ECUs hit 26 weeks in 2024. Three suppliers—Bosch, Continental, and Denso—controlled 60% of the output, underscoring the concentration risk. Antenna innovation is accelerating as millimeter-wave 5G becomes viable; Amphenol’s phased-array design supports 28 GHz and 39 GHz bands for gigabit car streaming. These shifts signal that hardware will increasingly be standardized, while differentiation moves to the software layer, reinforcing the data-centric outlook for the Internet of Cars market.

By Connectivity Technology: 5G C-V2X Eclipses Legacy DSRC

Cellular-V2X built on 5G held 10.98% share in 2025 and is forecast to expand at 20.98% CAGR through 2031. Release 16 sidelink enables direct car-to-car messaging without network coverage, which is vital for rural safety use cases. China’s nationwide mandate enabled the deployment of 1.2 million C-V2X vehicles on roads in 2024. The U.S. shifted USD 200 million from DSRC to cellular pilots.

Satellite links are gaining traction for remote regions; Starlink’s automotive terminal delivers 100 Mbps where 5G is absent. Wi-Fi and Bluetooth remain common in-cabin, yet add little incremental revenue. Regulatory convergence is improving: a September 2025 EU directive reserves the 5.9 GHz band exclusively for C-V2X starting in 2027, reducing compliance costs and bolstering the Internet of Cars market.

By Application: Entertainment Subscriptions Fuel Revenue Growth

Safety and driver assistance accounted for 15.44% of 2025 demand, driven by the mandatory implementation of automatic emergency braking in key markets. Integrated entertainment is projected to grow at a 19.21% CAGR as users expect smartphone-grade streaming and gaming capabilities. Samsung and Stellantis brought 4K video and Xbox Cloud Gaming to 12 models in 2024. Mobility management is gaining traction; Uber now displays public transit fares in 85 cities.

Vehicle management features, such as remote diagnostics, are table stakes; Tesla issued 12 fleet-wide updates in 2024. Venture investors injected USD 800 million into vehicle-to-grid and peer-to-peer sharing startups. As recurring content fees outpace hardware margins, connected entertainment stands to be a primary revenue accelerator for the Internet of Cars market.

By End-User Industry: Ride-Hailing Fleets Drive Connectivity Adoption

Automotive OEMs generated 22.05% of 2025 revenue, but ride-hailing and car-sharing fleets are forecast to grow at a 20.04% CAGR. Uber equipped 500,000 North American cars with bespoke telematics to inform dynamic pricing and maintenance. Lyft monetizes anonymized driving data through partnerships with urban planners.

Transportation and logistics firms embraced advanced fleet tools; DHL saved 9% on fuel after deploying Verizon Connect in 12,000 vans. Allstate tied premiums to real-time braking and mileage for 2 million users in six months. With fleet managers focused on cost per mile, centralized telematics investments continue to expand the Internet of Cars market size across commercial verticals.

Geography Analysis

The Asia Pacific led the Internet of Cars market in 2025, with a 33.62% share, and is expected to sustain a 19.02% CAGR through 2031. China budgeted RMB 50 billion (USD 6.9 billion) for smart roadside assets in Wuxi, Shanghai, and Chongqing. Japan’s 5G-V2X program aims to deploy 50,000 cooperative cruise-control cars by 2027. India’s USD 15 billion Smart Cities Mission has completed pilots that reduced wait times by 18% at intersections. South Korea plans to install C-V2X technology on every new expressway starting from 2025. Indonesia and Vietnam are slower due to limited 5G coverage; however, ride-hailing firms are deploying telematics on their two-wheel fleets.

North America and Europe are mature yet divergent. Washington authorized USD 1.2 billion for V2X corridors on Interstates 80 and 95. The EU has financed 23 cross-border freight projects that enable fuel savings of 10-15% through truck platooning. Canada’s Ontario pilot cut rear-end collisions by 22% at signalized intersections. Mexico focuses on plant-side 5G networks for vehicle testing. Stricter privacy rules in Europe increased compliance spending and impacted monetization timelines.

The Middle East and Africa are riding the smart-city megaprojects. Saudi Arabia’s USD 500 billion NEOM will deploy 5G-ready V2X across 26,500 square kilometers. Dubai connected 1,200 buses and cut delays by 12 minutes. South Africa’s Gauteng province plans 300 C-V2X intersections by 2027. Nigeria and Kenya focus on delivery-motorcycle tracking for theft reduction. Latin America lags due to funding gaps; Brazil’s 5G road-coverage mandate faces uncertain timelines. These diverse trajectories outline how regional policies and telecom readiness will shape the future growth of the Internet of Cars market.

Regulatory Landscape

Regulation is increasingly framed around cybersecurity, software-update governance, and data-access obligations for connected vehicles. UNECE WP.29 UN Regulation No. 155 (CSMS) and UN Regulation No. 156 (software updates/OTA) are built into vehicle type-approval pathways across multiple markets, which raises the compliance bar for OEMs and tier suppliers shipping telematics, ECUs, and OTA toolchains. In the United States, NHTSA continues to shape industry behavior through its non-binding Cybersecurity Best Practices for the Safety of Modern Vehicles, keeping lifecycle risk management and coordinated vulnerability disclosure as reference points for connected-vehicle programs.

In Europe, the regulatory perimeter is moving beyond vehicle safety into data governance. The EU Data Act (Regulation (EU) 2023/2854) creates product-design and service obligations for access to and use of data generated by connected products, including vehicles, with requirements applying from September 12, 2026 for in-scope provisions such as user accessibility under Article 3. The United Kingdom has also aligned its GB type-approval framework with UN R155 and UN R156, tightening expectations for cybersecurity and software updating processes for connected and automated vehicles.

Value Chain Analysis

The Internet of Cars value chain runs from silicon and module providers (embedded modems, C-V2X radios, telematics control units) to automotive tier suppliers that integrate connectivity and sensors, telecom operators that deliver network access and managed services, and cloud or software platforms that provide OTA, fleet, security, and data products for OEMs and commercial fleets. As software-defined vehicle (SDV) architectures spread, leverage shifts toward compute and software stacks, reflected in OEM engagements around integrated platforms such as Qualcomm Snapdragon Digital Chassis (for zonal architectures, infotainment, connectivity, and ADAS) and in cloud-led toolchains for system management at scale.

Security requirements, national supply-chain scrutiny, and interoperability standards are now influencing sourcing and partner selection alongside cost and performance. In the United States, the ICTS Connected Vehicle Rule and follow-on actions such as BIS General Authorization 3 (GA3) for a Trusted Supplier program add diligence for covered hardware and software, affecting how OEMs qualify suppliers and structure multi-sourcing. At the same time, alliance and ecosystem programs are pushing common interfaces to reduce integration burden, while telecom-operator partnerships (for example, 5G standalone telematics offerings tied to automotive deployments) pull carriers deeper into the post-sale services layer and recurring revenue streams.

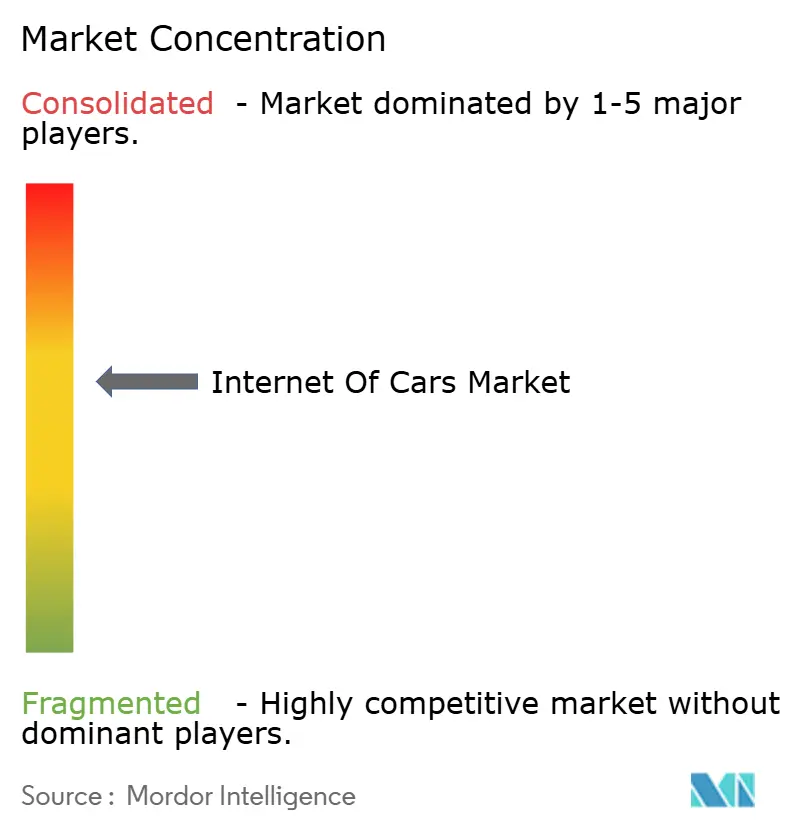

Competitive Landscape

The Internet of Cars market is moderately fragmented because value creation spans silicon, connectivity, software stacks, and data services, with no single firm controlling a significant share of global revenue. Traditional tier-one suppliers such as Bosch, Continental, and Denso still anchor the hardware layer, but their collective share has slipped as software and cloud spending grow faster than telematics hardware shipments. Competitive intensity is rising as semiconductor specialists and cloud hyperscalers move up the stack, compressing margins for long-time automotive suppliers. Scale does matter—combined, the top five vendors command around 45-50% of revenue, which produces a mid-level concentration that allows regional challengers to gain ground without facing a single dominant platform. For automakers, this structure provides leverage to negotiate multi-sourcing contracts, but it also forces costly systems-integration work that lengthens launch cycles.

Incumbent suppliers are investing heavily to protect their franchise. Continental spun off a cloud-native software arm with EUR 2 billion in funding in 2024 to accelerate over-the-air update rollouts and provide automotive cybersecurity services. Bosch and Denso both secured ISO 21434 certification across their telematics portfolios by 2025, cutting OEM qualification cycles by several quarters and winning design wins on next-generation electric platforms. Qualcomm is bundling 5G modems, high-performance computing, and AI accelerators in its Snapdragon Digital Chassis, a package adopted by 25 automakers that reduces bill-of-materials costs and secures recurring software royalties. Microsoft signed a USD 4 billion deal with Volkswagen to run Azure Automotive Cloud across 10 million connected vehicles, positioning the hyperscaler as the data backbone for Europe’s largest carmaker.

White-space opportunities remain in edge orchestration, cross-OEM data exchanges, and managed security monitoring. Startups such as Wejo and Otonomo aggregate anonymized driving data from multiple brands; yet, both firms struggled to achieve profitability in 2024, highlighting unresolved economic issues in large-scale data marketplaces. Chinese technology vendors continue to undercut Western price points; Huawei’s Intelligent Automotive Solution group landed contracts with 12 domestic automakers in 2024, though export controls still limit its reach outside China. Telecom operators are repositioning themselves from pipe providers to solution integrators. In 2025, AT&T added real-time cybersecurity and fleet analytics to its 5G data plans, creating a managed service targeted at logistics fleets that lack in-house IT resources.

Internet Of Cars Industry Leaders

AT&T Inc.

Robert Bosch GmbH

Cisco Systems Inc.

Continental AG

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standardization and compliance-driven redesign are creating whitespace for platforms that reduce fragmentation across OEMs, regions, and suppliers. The EU Data Act requirements taking effect in 2026 will require new data-access interfaces and governance workflows for vehicle-generated data, increasing demand for compliant in-vehicle data layers, consent management, and secure APIs that connect OEM back ends, third-party services, and fleet operators. Industry coordination is also tightening around SDV interoperability, with COVESA and JASPAR signing an MoU in June 2026 to standardize vehicle APIs using VSS and VISS, and COVESA positioning these specifications as building blocks for Data Act-aligned data sharing.

V2X and digital key ecosystems are also opening opportunity across spectrum access, certification, and multi-market rollout tooling. India implemented a licence-exempt spectrum regime for V2X equipment in the 5875-5905 MHz band in July 2026, which lowers a barrier for deployments that connect vehicles to roadside units and traffic infrastructure. On the product and integration side, CCC activity at Auto China 2026, including new task groups (Fleet Management, Alternate Markets, and Light Motor & Mobility), points to a certification and feature portability pipeline beyond premium passenger cars into fleets and new mobility form factors. In China, MIITs 2026 Key Tasks for Automotive Standardization under the 15th Five-Year Plan prioritize vehicle-road-cloud integration, automotive AI, and data security, reinforcing near-term demand for compliant V2X stacks, secure OTA operations, and edge-enabled architectures across the connected-vehicle ecosystem.

Recent Industry Developments

- June 2026: AT&T expanded its Connected Car platform by integrating LiveOne streaming services and using Cisco technology to support multi-party SIM management and billing. The update reinforces operator-led in-vehicle entertainment bundles while simplifying monetization and subscription management across OEM and third-party content partners.

- August 2025: DENSO and AT&T initiated a partnership to offer a customizable portfolio of intelligent transportation systems services and hardware/software, including MobiQ V2X units. The collaboration links tier-one suppliers' V2X and roadside capabilities with carrier connectivity and deployment scale, supporting broader V2X rollouts for safety and mobility use cases.

- September 2024: Tesla opened a data center in Shanghai to meet Chinas local data storage requirements for connected-vehicle data. This move supports continued deployment of connected services and data-intensive features while aligning operations with data localization rules that influence how OEMs architect global vehicle-cloud platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the internet of cars market is defined as revenue generated from in-vehicle connectivity hardware, enabling software, and related services that allow vehicles to exchange data with networks, infrastructure, and other vehicles.

Scope exclusions: We exclude general consumer mobile data plans that are not bundled with vehicle connectivity solutions, and we also exclude standalone infotainment content subscriptions that are not linked to in-car connectivity delivery.

Segmentation Overview

- By Software Solutions

- Real-Time Transit Management Systems

- Security Solutions

- Remote Monitoring Systems

- Network Bandwidth Management

- Fleet Management

- By Hardware Components

- Telematics Control Units

- On-Board Sensors

- Embedded Modems

- HMI Displays

- Antennas and Cables

- By Connectivity Technology

- Cellular-V2X (5G)

- Dedicated Short-Range Communications (DSRC)

- Satellite

- Wi-Fi / Bluetooth

- By Application

- Mobility Management

- Vehicle Management

- Integrated Entertainment

- Safety and Driver Assistance

- Other Applications

- By End-user Industry

- Transportation and Logistics

- Automotive OEMs

- Car-Sharing and Ride-Hailing Operators

- Insurance

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the value chain, understand typical technology bundles, and set realistic guardrails for adoption and pricing across regions. We referenced public sources such as vehicle production and registration statistics from government transport agencies, telecom regulator releases on 4G and 5G coverage, standards and safety publications from bodies such as ISO and SAE, and spectrum and connected mobility updates from groups like 3GPP.

To keep assumptions grounded, we also reviewed OEM and supplier annual reports, investor presentations, earnings call notes, reputable press coverage, and association websites that track connected mobility and automotive electronics. Where helpful, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to confirm corporate exposure to connected-car programs and to cross-check timing of technology rollouts. The desk sources listed here are illustrative only, and many other references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets counted as internet of cars revenue at the supplier and OEM program level, and how pricing changes as connectivity moves from basic telematics toward V2X and software-led services. We spoke with a mix of OEM program teams, automotive electronics suppliers, telecom ecosystem participants, fleet and mobility operators, and insurance-linked stakeholders across key regions. This helped close gaps from desk research and stress-test key assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | APAC: 43% |

| Mid tier: 45% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 21% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool reconstruction, where global vehicle production, connected-vehicle penetration, and the attach rate of connectivity modules and services are applied by region and vehicle class. Once the demand pool was shaped, selective bottom-up checks were used to keep totals realistic. For example, we sampled ASPs against shipment volumes for key hardware blocks, such as telematics control units and embedded modems, and we checked service revenue per connected vehicle using service channel signals.

Inputs used in the model include connected-vehicle adoption by region, the share of vehicles with embedded connectivity versus tethered approaches, V2X technology mix (such as cellular-V2X versus DSRC), typical content of a connectivity bill of materials, and service monetization patterns by use case (fleet management, safety and driver assistance, and mobility management). When a bottom-up proxy was not available for a sub-area, we used adjacent segment ratios and then validated those ratios with interview feedback.

For forecasting, scenario analysis was applied because the market is sensitive to changes in 5G rollout timing, regulation for safety and data privacy, and the pace of OEM feature standardization. The scenarios were translated into yearly adoption and ASP pathways, and then reviewed with experts so the final trajectory stayed practical.

Data Validation & Update Cycle

Outputs are checked through multiple steps, starting with internal consistency tests across regions, technologies, and applications so totals reconcile back to the same demand pool. Variances are then reviewed against independent signals, such as vehicle shipment trends, connectivity coverage milestones, and known timing of V2X deployment. If anomalies appear, inputs are re-checked and selected respondents are re-contacted when needed.

Before sign-off, another analyst reviews key assumptions, calculations, and year-on-year movements to ensure the story matches the numbers. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory shifts or large changes in connectivity module pricing. Right before delivery, a final pass is performed so clients receive the latest updated view.

Mordor Intelligence's Internet of Cars Market Market Size Measured Against Other Published Estimates

Published market values for internet of cars can look far apart because firms do not always count the same revenue streams, and they also anchor their models to different base years and adoption curves. Differences typically come from whether studies treat services as recurring revenue, how hardware and software are bundled, and how regional rollout timing is assumed.

Vehicle production signals, connected-car penetration trends, and V2X rollout checkpoints are used as evidence to keep Mordor Intelligence tied to a defined demand pool that only counts monetizable connectivity hardware, software solutions, and related services included in this report scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 204.84 B (2026) | |

| Industry Publisher A | USD 187.99 B (2024) | Uses an earlier base year and applies a broader automotive IoT narrative, which can shift what is treated as internet of cars revenue and how early adoption is captured. |

| Industry Publisher B | USD 323.20 B (2024) | Reports a larger 2024 starting value that likely reflects wider bundling of services and software across connected mobility, which can inflate totals if non-vehicle specific digital revenue is included. |

The spread in the table mainly comes from base-year choice and how strictly each estimate separates vehicle connectivity revenue from adjacent digital categories. By keeping the demand pool traceable to vehicle volumes, attach rates, and realistic ASP paths that are rechecked through interviews, the final number stays balanced and repeatable for planning.

Key Questions Answered in the Report

What is the projected value of the Internet of Cars market by 2031?

The market is expected to reach USD 477.47 billion by 2031 at an 18.43% CAGR.

Which region will grow fastest in connected-vehicle adoption through 2031?

The Asia Pacific is set to post a 19.02% CAGR, driven by large-scale C-V2X mandates and smart city funding.

Which software segment is expanding most rapidly?

Security software, driven by UNECE cybersecurity rules, is forecast to grow at a 18.92% CAGR to 2031.

How are ride-hailing fleets influencing connectivity demand?

Centralized telematics helps ride-hailing operators reduce per-vehicle costs by 10-15%, making them the fastest-growing end-user group with a 20.04% CAGR.

Why is standard fragmentation a concern for automakers?

Divergent C-V2X specifications across major markets compel OEMs to develop and certify multiple hardware variants, thereby increasing R&D expenses and delaying launches.

What role does 5G play in the Internet of Cars ecosystem?

5G, especially with edge computing, enables sub-10 ms latency essential for safety functions and high-bandwidth in-vehicle entertainment, and 5G C-V2X is forecast to grow at a 20.98% CAGR.

Page last updated on: