Cell Freezing Media Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

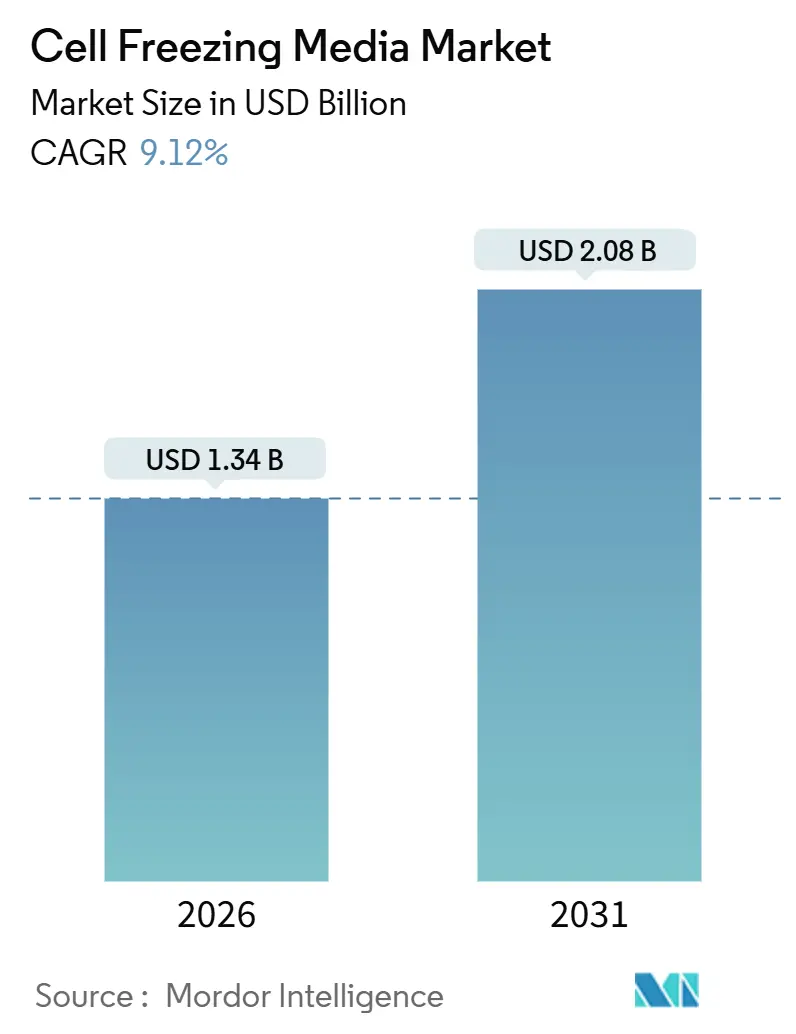

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 2.08 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

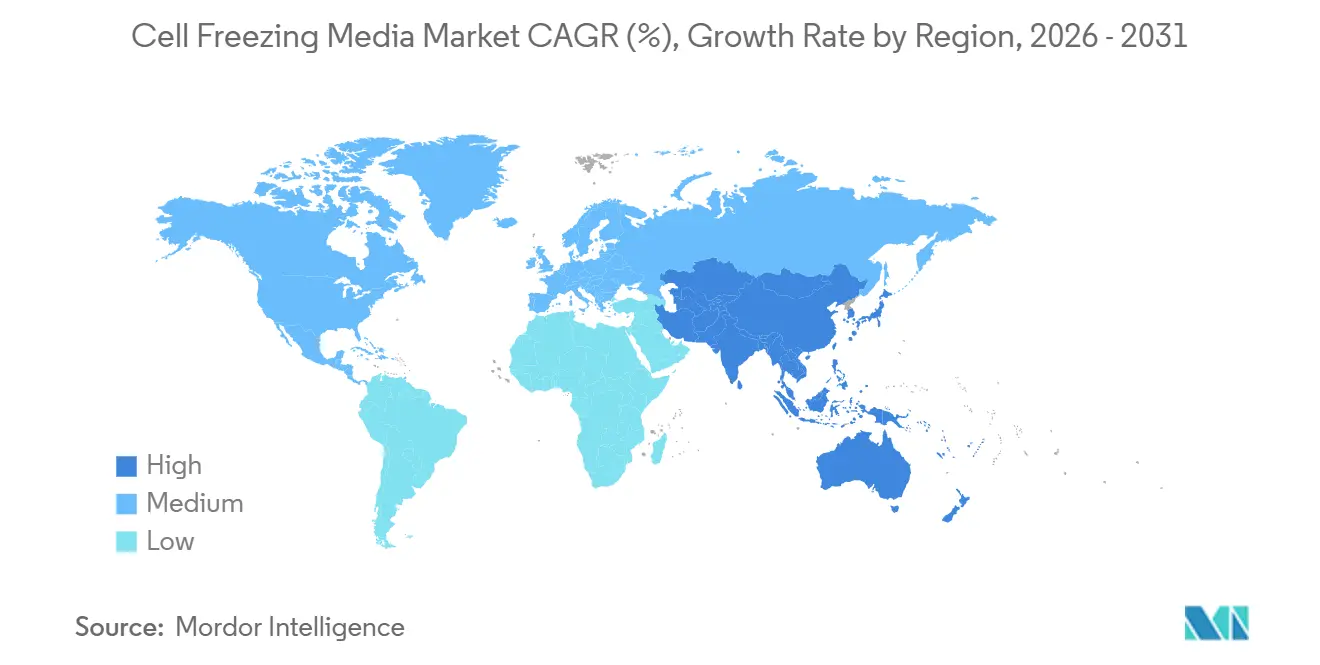

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Freezing Media Market Analysis by Mordor Intelligence

The Cell Freezing Media Market size is estimated at USD 1.34 billion in 2026, and is expected to reach USD 2.08 billion by 2031, at a CAGR of 9.12% during the forecast period (2026-2031).

Momentum stems from three reinforcing trends: regulators in the United States, Europe, and Japan now favor serum-free and xeno-free formulations; distributed manufacturing models demand longer storage stability across multiple sites; and the pipeline of approved CAR-T and other autologous therapies keeps lengthening. Competitive intensity is shaped by mid-sized suppliers that specialize in dimethyl sulfoxide (DMSO) blends, while large life-science conglomerates bundle cryoprotectants with bioprocess hardware and logistics. At the same time, biobanks, IVF clinics, and academic centers are standardizing controlled-rate protocols to ensure traceability, a requirement that increases demand for good-manufacturing-practice (GMP) grade inputs. The cost premium on USP-grade DMSO persists, yet capacity expansions at top suppliers and diversification of raw-material sourcing are expected to narrow price spreads during the medium term. Altogether, these factors keep the cell freezing media market on a steady growth trajectory that rewards suppliers who can align their product portfolios with evolving regulatory and clinical practice standards.

Key Report Takeaways

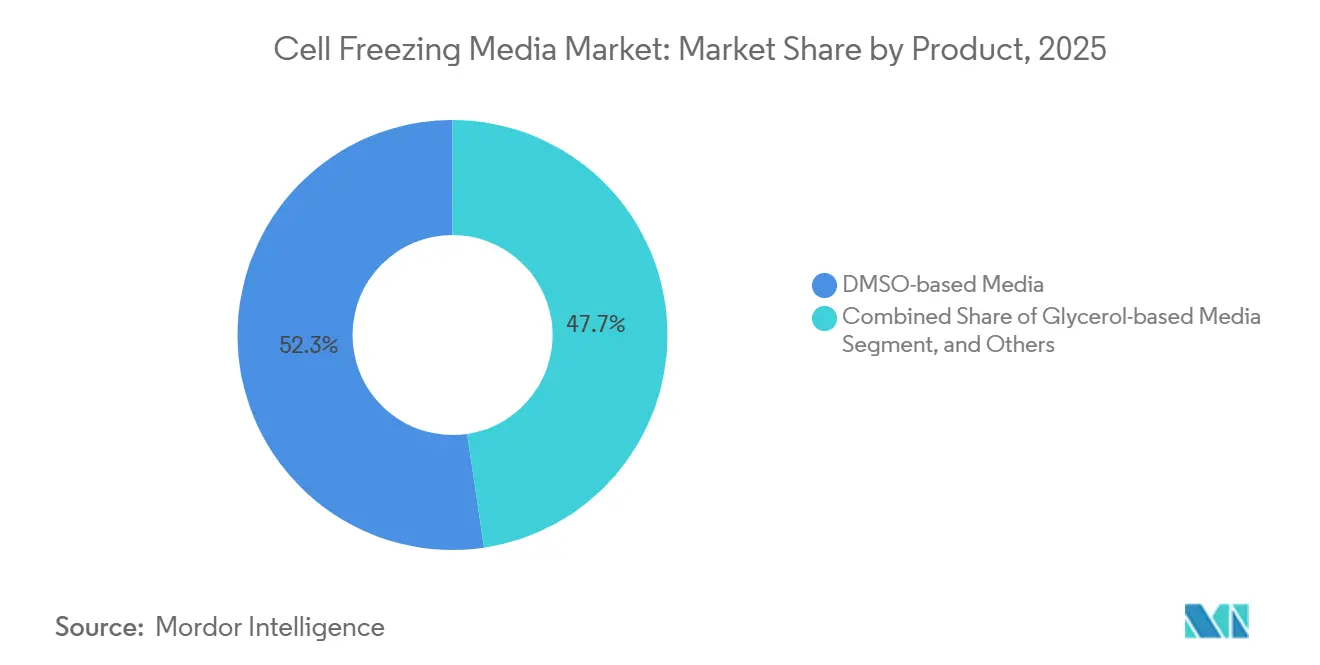

- By product type, DMSO-based formulations held 52.34% of 2025 revenue, while glycerol-based alternatives trailed; DMSO blends are projected to advance at an 11.43% CAGR to 2031.

- By freezing protocol, slow-rate controlled freezing accounted for 68.65% of demand in 2025, whereas vitrification is forecast to post an 11.65% CAGR through 2031.

- By cell culture system, suspension culture led with 45.65% 2025 volume; three-dimensional organoid and spheroid culture is set to accelerate at an 11.56% CAGR.

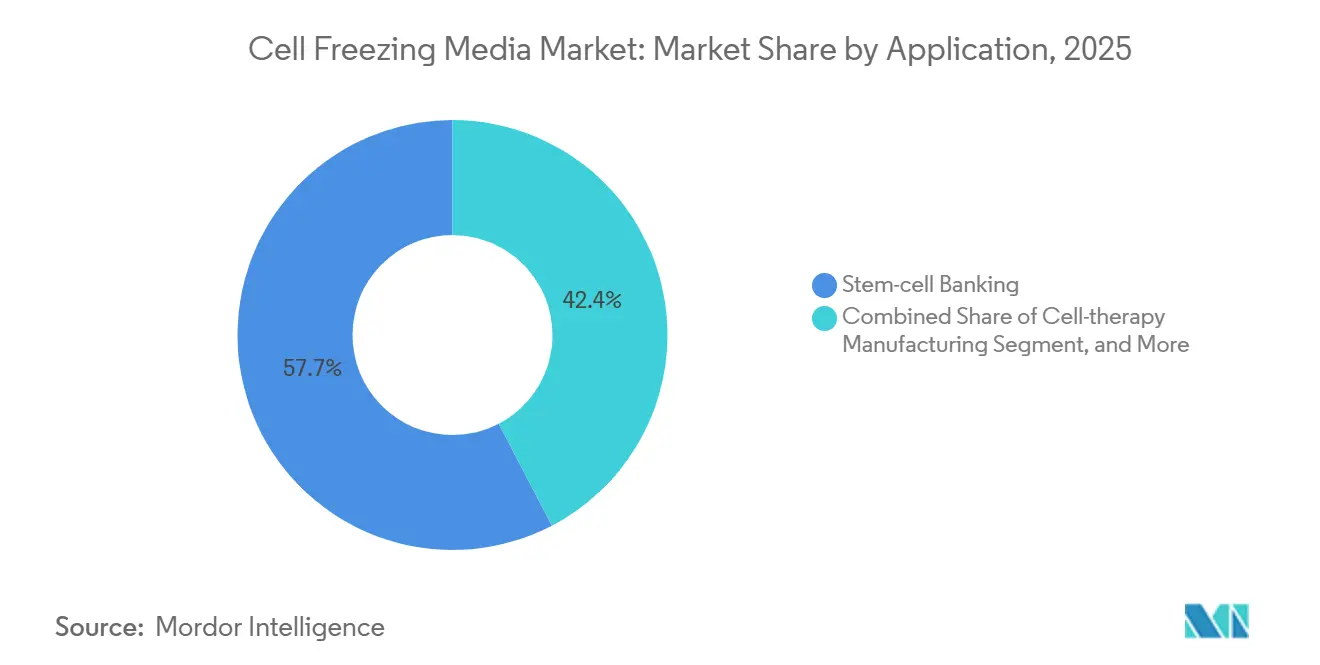

- By application, stem-cell banking commanded 57.65% of 2025 revenue, yet cell-therapy manufacturing is on track for the fastest 12.45% CAGR.

- By end user, pharmaceutical and biotechnology companies accounted for 48.65% of 2025 spending, while biobanks will expand at a 12.76% CAGR through 2031.

- By geography, North America accounted for 42.32% of 2025 revenue; Asia-Pacific is poised for a 10.43% CAGR on the back of multiple CAR-T approvals in China and Japan.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cell Freezing Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread adoption of cell and gene therapies | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion of global biobanking networks | +1.9% | Global, Asia-Pacific core with spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Advances in controlled-rate and closed-system freezing | +1.5% | North America and European Union, early adoption in Asia-Pacific | Short term (≤ 2 years) |

| Regulatory shift to serum-free and xeno-free media | +2.1% | Global, enforced earliest in European Union and North America | Medium term (2-4 years) |

| Decentralized cell-therapy manufacturing needs | +1.4% | North America and European Union, pilot programs in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Widespread Adoption of Cell and Gene Therapies

Regulatory approvals for CAR-T and other autologous treatments compel manufacturers to demonstrate post-thaw viability above 70% and functional potency within a 10% margin of pre-freeze benchmarks, performance thresholds codified in the U.S. Food and Drug Administration’s January 2024 chemistry, manufacturing, and controls draft guidance[1]U.S. Food and Drug Administration, “Chemistry, Manufacturing and Controls for CAR-T,” fda.gov. Commercial CAR-T workflows involve at least one freeze between leukapheresis and transduction, often a second freeze before patient infusion, which doubles the cryopreservation media consumption per patient compared with older allogeneic models. Contract development and manufacturing organizations (CDMOs) such as Lonza expanded Houston capacity in 2024, integrating controlled-rate freezers with real-time temperature mapping, enabling standardized execution of media protocols across client programs. Broader therapy pipelines and outsourcing trends, therefore, translate into sustained volume growth for ready-to-use GMP-grade media.

Expansion of Global Biobanking Networks

National precision-medicine initiatives continue to scale repositories. The U.S. National Institutes of Health All of Us Research Program passed 1 million participants in mid-2024, each contributing samples preserved in DMSO blends and stored in vapor-phase liquid nitrogen[2]National Institutes of Health, “All of Us Research Program,” nih.gov. The UK Biobank, already beyond 500,000 participants, is piloting serum-free formulations to eliminate bovine components and mitigate long-term regulatory risk. China’s National GeneBank added modules for 50 million vials in 2024 and standardized on controlled-rate freezing to harmonize quality across provincial collection sites. Biobanks purchase media in bulk and demand full traceability documentation, a profile that supports long-range supply agreements for high-volume, cost-sensitive formulations.

Advances in Controlled-Rate and Closed-System Freezing

Integration of programmable freezers with closed fluid paths minimizes contamination while raising reproducibility. Cytiva’s VIA Freeze platform allows cooling rates as low as 0.1 °C per minute and records every temperature excursion for regulatory submission, capabilities adopted by multiple GMP facilities. The University of Edinburgh implemented liquid-nitrogen-free controlled-rate freezers in 2024, trimming operational costs by 20% while maintaining post-thaw viability above 85% for mesenchymal stem cells. Closed bags that are gamma-irradiated and pre-filled with media eliminate open transfers, which have historically been responsible for most microbial contamination events. Miltenyi Biotec’s automated platform now bundles inline cryopreservation, positioning hospitals to produce CAR-T at the point of care without the need for complete clean-room infrastructure.

Regulatory Shift to Serum-Free and Xeno-Free Media

The FDA’s April 2024 guidance demands sponsors justify any animal-derived components, pushing the industry toward chemically defined alternatives. The European Medicines Agency’s July 2025 advanced-therapy guideline further requires complete traceability of raw materials and recommends chemically defined formulations. Major suppliers have responded: Thermo Fisher Scientific’s Gibco CTS Synth-a-Freeze Medium, a serum-free xeno-free blend, is used in several phase III CAR-T trials. CelProgen introduced a similar reagent in 2025 for academic labs navigating stricter institutional review board requirements. As regulatory scrutiny tightens, adoption of defined formulations accelerates across clinical and research settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of GMP-grade cryopreservation inputs | -1.2% | Global, most acute in cost-sensitive Asia-Pacific markets | Medium term (2-4 years) |

| Cell viability loss from improper freeze-thaw | -0.9% | Global, higher in regions with limited GMP expertise | Short term (≤ 2 years) |

| DMSO cytotoxicity drives costly reformulation | -0.7% | North America and European Union | Long term (≥ 4 years) |

| USP-grade DMSO and additive supply bottlenecks | -0.5% | Global, sporadic shortages in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of GMP-Grade Cryopreservation Inputs

USP-grade DMSO sells at a 30–40% premium over industrial-grade DMSO because suppliers such as Gaylord Chemical impose stringent certificate-of-analysis requirements, which extend lead times and raise inventory costs. For a 10-dose CAR-T run, cryopreservation media accounts for 8–12% of the total cost of goods, rising to 18% when proprietary serum-free blends are used. CDMOs frequently lock in annual volume commitments, reducing flexibility to adopt lower-cost alternatives, and smaller biotech firms incur validation expenses of USD 200,000–500,000 per product when switching suppliers, further reinforcing the cost barrier.

Cell Viability Loss from Improper Freeze-Thaw

An international study published in 2024 found that 18% of mesenchymal stem-cell batches failed to meet the 70% viability requirement after a single freeze-thaw cycle, primarily due to cooling rates outside the optimal 1–3 °C per minute range. Decentralized hospital sites have steeper learning curves, and calibration errors can create gradients that crystallize intracellular water, resulting in costly batch rejections. A single failed CAR-T dose can represent a USD 300,000–500,000 write-off and may trigger mandatory adverse-event reporting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: DMSO Formulations Anchor Clinical Validation

The cell freezing media market, attributed to DMSO-based formulations, accounted for 52.34% of 2025 revenue and is projected to grow at an 11.43% CAGR through 2031, well ahead of glycerol and polymer alternatives. DMSO remains the only cryoprotectant with four decades of clinical precedent in hematopoietic stem-cell transplantation, simplifying regulatory review. Trehalose- and polymer-based blends address DMSO cytotoxicity yet still lag on colony-forming efficiency, a performance gap that keeps sponsors aligned with legacy DMSO recipes. The cell freezing media market share of glycerol products is likely to remain modest because glycerol permeates membranes slowly, leading to hold times incompatible with high-throughput manufacturing. Suppliers such as STEMCELL Technologies differentiate by incorporating antioxidants that extend the post-thaw functional lifespan, a feature prized by biobanks seeking to maximize downstream use.

By Freezing Protocol: Vitrification Gains in Speed-Sensitive Applications

Slow-rate controlled freezing accounted for 68.65% of total demand in 2025 because it scales to multi-liter bags and integrates with automated fill lines, attributes valued by CAR-T manufacturers and biobanks. Conversely, vitrification is clocking an 11.65% CAGR due to strong uptake in IVF clinics where oocytes and blastocysts must avoid ice-crystal formation for clinical success. Media used for vitrification contain 30–40% cryoprotectant, triple the DMSO level in controlled-rate blends, underscoring the need for highly optimized formulations. Hybrid strategies that control-rate-cool to –40 °C followed by a rapid plunge are being explored for organoid preservation to curb toxicity while safeguarding tissue architecture.

By Cell Culture System: 3-D Models Drive Innovation

Suspension culture systems accounted for 45.65% of the 2025 volume, driven by their dominance in T-cell expansion for CAR-T therapy, a core application for the cell freezing media market. Meanwhile, organoid and spheroid cultures are growing at an 11.56% CAGR because pharmaceutical firms prefer 3-D tumor models that predict drug response more accurately than 2-D monolayers. Suppliers have introduced organoid-specific protocols that tune DMSO concentrations and cooling rates to diverse membrane compositions, pushing boundaries in complex tissue banking. As 3-D models migrate from research to regulated manufacturing, demand for defined, low-toxicity media variants is set to climb.

By Application: Cell-Therapy Manufacturing Outpaces Legacy Banking

Stem-cell banking retained 57.65% of revenue in 2025, reflecting decades of cord-blood and bone-marrow storage programs. Yet cell-therapy manufacturing offers the fastest 12.45% CAGR, as every commercial autologous product requires at least one cryostep. The cell freezing media market size allocated to cell-therapy manufacturing, therefore, rises proportionally with each new therapy approval. Even so, cord-blood banks are updating recipes to serum-free blends to align with new ethics standards, signaling that legacy segments are not immune to product innovation.

By End-User: Biobanks Accelerate Fastest

Pharmaceutical and biotechnology companies accounted for 48.65% of 2025 spending, driven by dual roles as both therapy producers and primary-cell consumers. Biobanks, however, are charting a 12.76% CAGR as nations scale population genomics programs exceeding one million participants apiece. This shift nudges suppliers to package large-volume, cost-optimized SKUs with robust chain-of-custody documentation. Hospitals pulled into decentralized CAR-T workflows now require point-of-care media stocks, expanding the customer base but also elevating expectations for ready-to-use formats.

Geography Analysis

North America captured 42.32% of 2025 revenue, anchored by dense CAR-T manufacturing clusters and the region’s extensive network of public and private biobanks. The area benefits from harmonized FDA guidance that clarifies post-thaw performance metrics, reducing regulatory uncertainty for new entrants. Europe follows with steady adoption thanks to the European Medicines Agency’s July 2025 guideline that standardizes raw-material traceability, lowering the administrative burden of multi-country trials.

Asia-Pacific is advancing at a 10.43% CAGR, propelled by the National Medical Products Administration’s approval of 15 CAR-T therapies by late 2024 in China and six regenerative-medicine products cleared in Japan over 2023–2024[3]National Medical Products Administration, “CAR-T Approvals List,” nmpa.gov.cn. China’s expansion of its National GeneBank underscores domestic commitment to large-scale sample preservation, while India and South Korea ramp up academic and clinical programs that integrate controlled-rate protocols to meet upcoming GMP standards. The Middle East and Africa remain nascent, with growth hubs in the United Arab Emirates and South Africa. In contrast, Latin America’s momentum concentrates in Brazil and Argentina amid improving regulatory clarity.

Logistics infrastructure keeps pace. Cryoport opened a Belgium hub in November 2024 with capacity for 1,100 leukapheresis products yearly to serve European trials and launches. The expansion illustrates how third-party logistics providers partner with media suppliers to offer turnkey services that include validated cryopreservation workflows. Consequently, regional growth hinges not only on therapy approvals but also on coordinated cold-chain networks that guarantee viability across transcontinental routes.

Competitive Landscape

The top five suppliers, Thermo Fisher Scientific, Merck KGaA, BioLife Solutions, STEMCELL Technologies, and Sartorius, collectively hold roughly 55-60% of global revenue, reflecting moderate concentration. Large incumbents leverage broad portfolios that cover DMSO blends, glycerol variants, and proprietary serum-free recipes, enabling cross-selling to diverse segments. BioLife Solutions’ USD 76 million purchase of Sexton Biotechnologies in October 2024 added fill-finish and lyophilization capabilities, letting the firm offer freeze-dried kits optimized for decentralized sites. Emerging players such as X-Therma and Akron Biotechnology focus on DMSO-free or low-DMSO formulations to minimize cytotoxicity, though widespread GMP validation remains pending.

Partnerships between equipment and media vendors are tightening. Lonza bundles its Cocoon platform with pre-qualified cryopreservation kits, while Miltenyi Biotec packages freezing media with automated cell-processing systems to attract hospital-based manufacturers. Intellectual-property filings in 2024-2025 target zwitterionic polymers and trehalose carriers designed to reduce DMSO concentrations to below 5% v/v while maintaining post-thaw viability above 80%—a threshold consistent with forthcoming FDA expectations. Suppliers offering ISO 13485 certification and end-to-end traceability documentation command price premiums and longer-term supply contracts, reinforcing the value of compliance as a competitive lever.

Cell Freezing Media Industry Leaders

Thermo Fisher Scientific Inc.

Merck KGaA

STEMCELL Technologies

Sartorius AG

BioLife Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Evia Bio, one of the leading providers of non-DMSO cryopreservation solutions for the cell therapy and in vitro fertilization industries, launched CellShieldTM MSC, its first proprietary cryopreservation solution that enables MSC-based therapy developers to achieve equivalent or better performance compared to traditional, DMSO–based media.

- October 2024: Nucleus Biologics, one of the leading providers of cell culture and bioprocessing solutions for the cell and gene therapy (CGT) industry, launched NB-KUL DF, a DMSO-free, chemically defined cryomedia, set to redefine cryopreservation standards. Designed for CGT manufacturers, NB-KUL DF matches the performance of DMSO-based media and outperforms DMSO-free options in cell viability, recovery, and expansion.

Global Cell Freezing Media Market Report Scope

As per the scope of the report, cell freezing media is a specialized solution, usually containing a base medium, serum/protein, and a cryoprotectant like DMSO or glycerol, designed to protect cells during slow freezing and long-term storage by preventing damaging ice crystal formation, ensuring high viability upon thawing for future use in research or therapy.

The Cell Freezing Media Market is Segmented by Product Type (DMSO-based, Glycerol-based, and Other), Freezing Protocol (Slow-rate Controlled and Vitrification), Cell Culture System (Suspension, 2-D Adherent, 3-D Organoid/Spheroid, and Others), Application (Stem-cell Banking, Cell-therapy Manufacturing, Drug Discovery & Screening, IVF, and Academic Research), End-User (Pharma & Biotech, Academic & Research Institutes, CROs/CDMOs, Hospitals & Clinical Labs, and Biobanks), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| DMSO-based Media |

| Glycerol-based Media |

| Other Product Types |

| Slow-rate (Controlled) Freezing |

| Vitrification |

| Suspension Cell Culture |

| 2-D Adherent Cell Culture |

| 3-D Organoid / Spheroid Culture |

| Others |

| Stem-cell Banking |

| Cell-therapy Manufacturing |

| Drug Discovery & Screening |

| In-vitro Fertilization (IVF) |

| Academic Research |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research / Development & Manufacturing Orgs (CROs/CDMOs) |

| Hospitals & Clinical Labs |

| Biobanks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | DMSO-based Media | |

| Glycerol-based Media | ||

| Other Product Types | ||

| By Freezing Protocol | Slow-rate (Controlled) Freezing | |

| Vitrification | ||

| By Cell Culture System | Suspension Cell Culture | |

| 2-D Adherent Cell Culture | ||

| 3-D Organoid / Spheroid Culture | ||

| Others | ||

| By Application | Stem-cell Banking | |

| Cell-therapy Manufacturing | ||

| Drug Discovery & Screening | ||

| In-vitro Fertilization (IVF) | ||

| Academic Research | ||

| By End-User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Contract Research / Development & Manufacturing Orgs (CROs/CDMOs) | ||

| Hospitals & Clinical Labs | ||

| Biobanks | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the cell freezing media market in 2031?

The market is expected to reach USD 2.08 billion by 2031, reflecting a 9.12% CAGR.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to expand at a 10.43% CAGR, led by multiple CAR-T approvals in China and Japan.

Why do DMSO-based formulations dominate?

They hold 52.34% of 2025 revenue because four decades of clinical precedent simplify regulatory review and ensure consistent post-thaw performance.

What segment is set for the fastest application growth?

Cell-therapy manufacturing is projected to grow at a 12.45% CAGR because every autologous therapy requires at least one freeze step.

How are regulations influencing product development?

FDA and EMA guidance now favor serum-free, xeno-free formulations with full traceability, prompting suppliers to develop chemically defined media lines.

Who are the leading companies in the space?

Thermo Fisher Scientific, Merck KGaA, BioLife Solutions, STEMCELL Technologies, and Sartorius together account for roughly 55-60% of global revenue.

Page last updated on: