Cell Reprogramming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

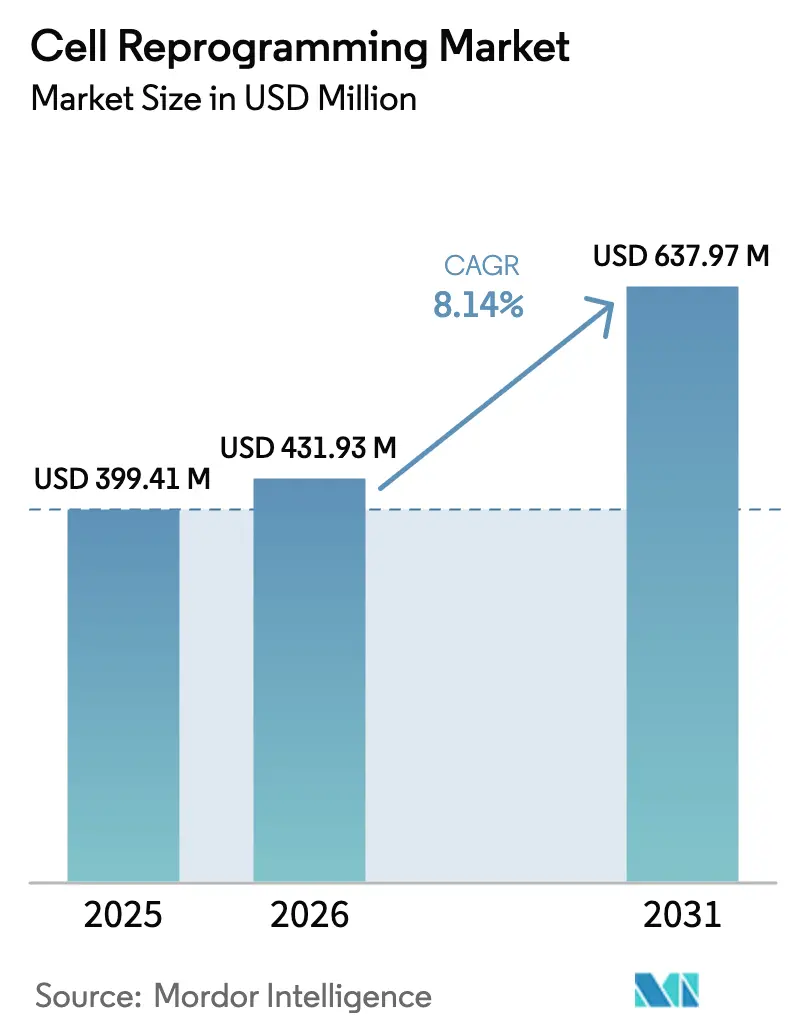

| Market Size (2026) | USD 431.93 Million |

| Market Size (2031) | USD 637.97 Million |

| Growth Rate (2026 - 2031) | 8.14% CAGR |

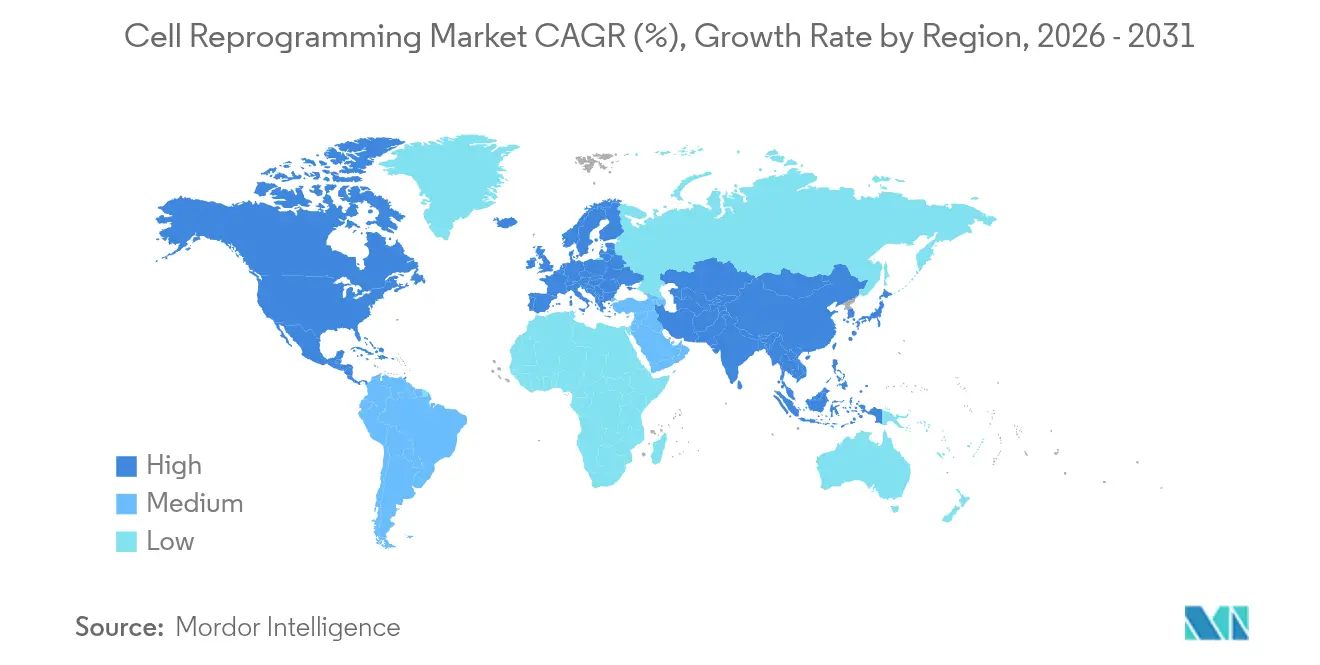

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

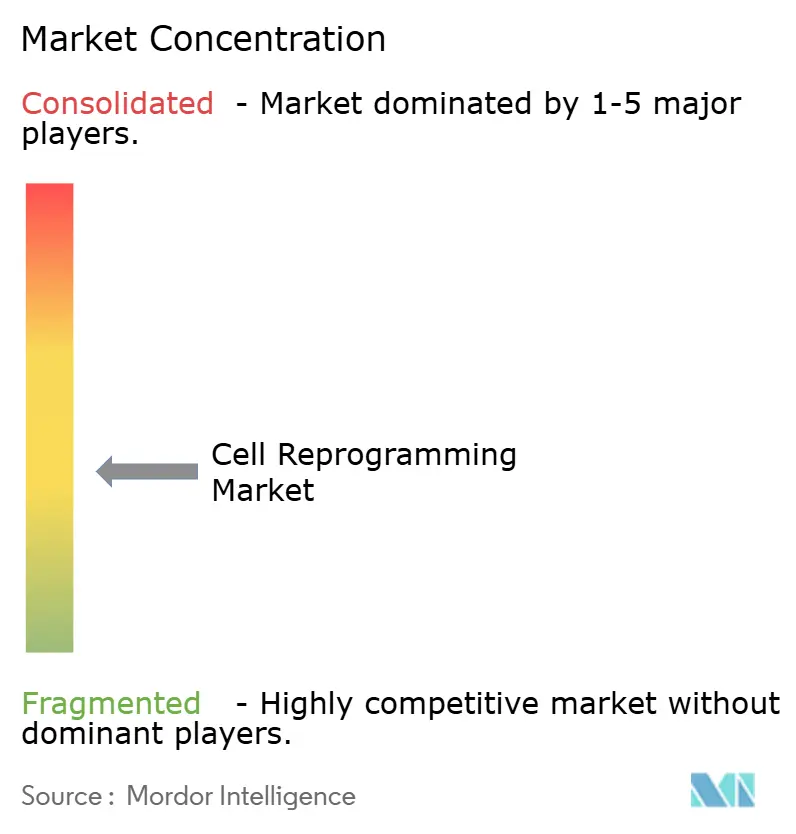

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Reprogramming Market Analysis by Mordor Intelligence

The cell reprogramming market size was valued at USD 399.41 million in 2025 and estimated to grow from USD 431.93 million in 2026 to reach USD 637.97 million by 2031, at a CAGR of 8.14% during the forecast period (2026-2031). The upward trajectory is supported by the maturation of integration-free technologies, growing regenerative-medicine pipelines, and expanding use cases in neurodegenerative, ocular, and cardiac care. Sendai-virus and mRNA toolkits allow safer, scalable production for clinical studies, attracting new funding from institutional and strategic investors. Rising clinical trial activity, especially in Japan and the United States, signals regulatory confidence and shortens the time to market for advanced therapies. Competitive intensity is moderate yet rising as large life-science firms and specialist biotechs race to secure GMP capacity and build diverse intellectual property portfolios.

Key Report Takeaways

- By technology, Sendai-virus reprogramming held 37.62% of the cell reprogramming market share in 2025, while mRNA platforms are advancing at an 8.22% CAGR through 2031.

- By application, research activities accounted for 61.74% share of the cell reprogramming market size in 2025, whereas therapeutics is growing fastest at a 9.07% CAGR to 2031.

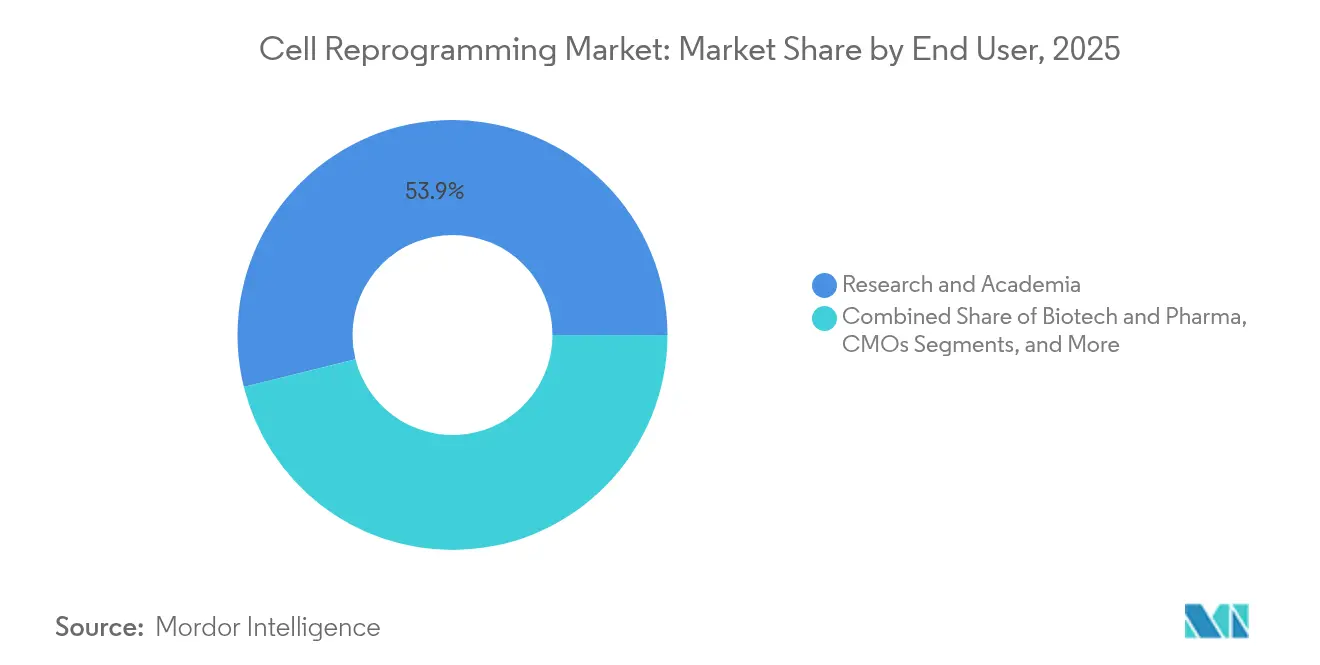

- By end user, research and academic institutes led with 53.88% revenue share in 2025, while contract manufacturing organizations are expanding at a 6.87% CAGR through 2031.

- By geography, North America commanded 44.15% revenue in 2025, and Asia Pacific is projected to register a 7.55% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Reprogramming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Chronic Diseases & Ageing Population | +1.80% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Expanding Investment In Regenerative-Medicine Pipelines | +2.10% | Global, led by North America & Asia Pacific | Medium term (2-4 years) |

| Rapid Advances In Integration-Free Reprogramming Tool-Kits | +1.50% | Global, with early adoption in Japan & US | Short term (≤ 2 years) |

| Government GMP Incentives For Autologous Cell Factories | +1.20% | Asia Pacific core, spill-over to North America | Medium term (2-4 years) |

| Demand For Personalised Neo-Antigen DC Vaccines | +0.90% | North America & EU, expanding to Asia Pacific | Long term (≥ 4 years) |

| Cost-Saving AI-Guided Protocol Optimisation Platforms | +1.20% | Global, with tech hubs leading adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases and Ageing Population

An expanding cohort aged 65 years and older is doubling by 2050, which elevates demand for regenerative approaches aimed at neurodegeneration and organ failure. Global health systems view cell-based therapies as a route to reduce long-term expenditure on chronic care. The United States Food and Drug Administration (FDA) targets 10-20 annual cell and gene therapy approvals by 2025, translating demographic pressure into actionable regulatory goals. Pharmaceutical companies respond by funding partial reprogramming programs that rejuvenate tissue without full differentiation. Payers also show interest in one-time interventions that offset future treatment burdens, reinforcing market expansion.

Expanding Investment in Regenerative Medicine Pipelines

Global cell therapy funding momentum is unprecedented, highlighted by Japan’s JPY 110 billion (USD 0.76 billion) commitment to accelerate induced pluripotent stem cell (iPSC) commercialization.[1]Nature, “Japan Allocates ¥110 Billion for Regenerative Medicine,” nature.com Sovereign grants attract multinational firms and venture capital, while expedited pathways such as the FDA RMAT designation clarify risk profiles for financiers. Autologous products dominate funding pools because they mitigate immunogenicity, yet new alliances are forming to develop off-the-shelf allogeneic options. Strategic collaborations pair pharmaceutical scale with biotechnology agility, creating diversified pipelines and fueling the cell reprogramming market.

Rapid Advances in Integration-Free Reprogramming Toolkits

Recent chemical systems produce human iPSCs in 10 days with 20-fold efficiency gains and full donor coverage, eliminating viral integration concerns. Sendai-virus kits now offer ligand-responsive switches for precise factor withdrawal, further reducing genomic risk.[2]Journal of Biological Engineering, “Ligand Responsive Sendai Systems,” springeropen.com Machine-learning models minimize experimental iterations by predicting optimal factor combinations, cutting timelines, and consumable costs. Such gains support clinical translation and make integration-free platforms the default industry standard.

Government GMP Incentives for Autologous Cell Factories

Regulators deploy targeted subsidies and tax credits to expand clean-room capacity, recognizing manufacturing as a growth bottleneck. China allows foreign firms to operate cell therapy plants in free-trade zones, accelerating regional investment. The FDA loosens master-cell-bank reporting requirements when genome editing is used once, reducing paperwork and cost for iPSC lines.[3]Federal Register, “FDA Draft Guidance on Genome Editing,” federalregister.govJapan’s fast-track approvals, combined with public funding, deliver first-to-market advantages for local innovators. These incentives shorten build times for compliant suites and broaden participation by midsize entities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tumourigenicity & Genomic-Instability Safety Concerns | -1.40% | Global, with stricter oversight in EU & US | Long term (≥ 4 years) |

| High CAPEX/OPEX For Clinical-Grade Reprogramming Suites | -1.10% | Global, particularly affecting smaller biotechs | Medium term (2-4 years) |

| Patent Thickets Around Key IPSC Technologies | -0.80% | Global, with concentration in US & Japan | Long term (≥ 4 years) |

| Shortage Of GMP-Grade SeV & Synthetic-MRNA Supply | -0.60% | Global, with acute impact in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tumorigenicity and Genomic-Instability Safety Concerns

Twenty-two percent of pluripotent stem cell lines harbor at least one cancer-linked mutation, most commonly in TP53, prompting tighter genomic surveillance. Prolonged culture time adds chromosomal gains that give growth advantages, compelling industry revisions to passage limits and release testing protocols. Regulators such as the FDA draft new guidance on risk-based assays, stretching development timelines and cost. Developers explore partial reprogramming to sidestep full pluripotency while achieving rejuvenation, though these methods remain at an early stage.

High CAPEX/OPEX for Clinical-Grade Reprogramming Suites

Constructing GMP suites costs tens of millions of USD and requires specialized staff and validated platforms, pushing many startups toward outsourcing. Contract development and manufacturing organizations (CDMOs) are forecast to supply 54% of global biologics capacity by 2028, highlighting reliance on third parties. Automation providers secure large deals for robotic production lines, yet entry costs still inhibit smaller firms from building facilities. This capex pressure shapes competitive strategy and slows geographic capacity expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Integration-Free Methods Drive Safety

Sendai-virus reprogramming generated the largest revenue in 2025 at 37.62% because it reliably produces transgene-free iPSCs and supports current good manufacturing practice workflows. Continual refinements in viral clearance and temperature sensitivity sustain demand among clinical developers. mRNA systems record the fastest 8.22% CAGR, helped by chemical kits that attain 100% success across varied donors. Episomal plasmids remain favored for academic screening due to low reagent cost, while integrative retroviral vectors decline as safety expectations rise.

Momentum is shifting toward platform facilities that can toggle between Sendai, mRNA, and small-molecule approaches without major capital changes. Artificial intelligence software shortens optimization cycles and links to automated bioreactors, lowering failure risk. Virus-like particles for CRISPR factor delivery broaden the menu of integration-free tools and support targeted lineage conversion studies. Competition now focuses on shortening footprint, reducing consumable cost, and embedding electronic batch records for regulatory audits.

By Application: Therapeutics Accelerate Clinical Translation

Research activities dominated 61.74% of revenue in 2025, funding disease models and compound screening that underpin pipeline discovery. Nonetheless, the therapeutic line is growing fastest at 9.07% because Parkinson’s, retinal, and cardiac trials show early safety and efficacy readouts. Regulators cleared seven advanced cell and gene therapies in 2024, validating commercial pathways and reinforcing investment inflows.

The cell reprogramming market size for therapeutic programs is expanding as sponsors broaden indications beyond hematology to solid organ repair. Diagnostic assay demand rises in parallel because regulators mandate deeper genomic stability checks. Cell banks proliferate to secure diverse haplotypes, supporting off-the-shelf allogeneic strategies. Improved cryopreservation and AI-guided quality control are compressing release timelines and scaling capacity.

By End User: CMOs Enable Specialized Manufacturing

Academic institutions generated 53.88% of revenue in 2025 due to grant funding for discovery science and repository building. Pharmaceutical and biotechnology firms translate breakthroughs to clinics yet often outsource production steps to focus on trial design and regulatory strategy. Contract manufacturers, expanding at 6.87% CAGR, fill this gap with modular clean rooms and process-development expertise that accelerate scale-up.

Strategic alliances multiply as large CDMOs sign multi-product supply deals with therapy sponsors, ensuring early capacity reservation. Nikon and Lonza co-manage facilities in Japan, while Vertex secures long-term slots for exa-cel manufacture. Automation and digital twins widen service offerings, making CMOs indispensable partners in the cell reprogramming market.

By Cell Source: Accessibility Drives Adoption

Dermal fibroblasts remain the prevalent source because skin biopsies are minimally invasive and protocols are well established. Neonatal fibroblasts display lower immunogenicity, favoring allogeneic product concepts. Peripheral blood mononuclear cells gain share thanks to simple venipuncture harvesting and successful reprogramming methods that yield hematopoietic lines with improved engraftment.

Cord blood and perinatal tissues carry immunological naivety and high proliferation but face supply limits. Adipose derived mesenchymal cells offer abundant volume from routine liposuction and have long safety records, making them attractive for metabolic and orthopedic programs. Emerging work on urine and hair follicle cells underscores a trend toward patient friendly sourcing and diversified biobanks that support precision medicine objectives.

Geography Analysis

North America led with 44.15% revenue in 2025 driven by a proactive FDA, substantial public grants, and a dense network of GMP plants. The agency approved eight novel regenerative products in 2024 and maintains a target of 10-20 annual approvals going forward. Capital projects such as Thermo Fisher’s USD 475 million plant in Princeton and Lonza’s USD 1.2 billion Vacaville acquisition fortify regional production depth. Collaborations between universities and venture funds sustain a robust discovery pipeline and cement regional dominance.

Asia Pacific is the fastest expanding zone with a 7.55% CAGR to 2031. Japan’s JPY 110 billion (USD 0.76 billion) program accelerates iPSC therapies and delivers 60+ clinical trials that show encouraging safety profiles. China’s policy shift to permit foreign cell therapy ventures in free-trade areas and its ballooning CAR-T pipeline encourage multinational investment. Nikon-Lonza and Atelerix-MineBio partnerships demonstrate surging cross-border technology exchange and local manufacturing upgrades.

Europe retains sizeable presence owing to strong academic networks and pharmaceutical heritage. The European Medicines Agency pilots joint health technology assessments that aim to harmonize member state access procedures. Accelerated acceptance of ExCellThera’s UM171 therapy signals openness to innovative modalities, yet reimbursement and capacity constraints temper momentum. Emerging regions in the Middle East, Africa, and South America launch supportive biotech policies, though infrastructure development will dictate adoption speed.

Competitive Landscape

The market remains moderately fragmented as Thermo Fisher Scientific, Merck KGaA, and FUJIFILM Holdings leverage global logistics, diversified reagent portfolios, and multi-modal manufacturing sites. Specialized players such as REPROCELL, Mogrify, and BlueRock Therapeutics focus on iPSC derivation, direct conversion, and disease-specific applications. Competitive pressure intensifies because integration-free safety profiles narrow differentiation, shifting emphasis to cost per dose and regulatory clarity.

Vertical integration is a defining tactic, with leaders acquiring or building GMP suites to safeguard supply and improve margins. Investment flows into automation firms that promise reproducible processes and electronic data capture. Intellectual property filings rise as companies stake claims on lineage conversion recipes and AI protocol workflows. The convergence of gene editing, machine learning, and bioprocess engineering expands the field of combatants and accelerates innovation velocity.

Strategic moves underscore the shift toward capacity control and therapeutic focus. Lonza’s USD 1.2 billion purchase of Genentech’s Vacaville site adds 330,000 L of bioreactors to support complex biologics. FUJIFILM invests USD 10 billion in life-science capabilities, rebranding units under one identity to streamline service offerings. Vertex seeks priority review for exa-cel, the first CRISPR therapy, positioning itself at the gene editing vanguard. These examples illustrate how capital strength and technology depth shape competitive outcomes in the cell reprogramming market.

Cell Reprogramming Industry Leaders

Thermo Fisher Scientific Inc.

Merck KGaA

Lonza

Creative Bioarray

FUJIFILM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FUJIFILM completed a broad life-science rebrand, consolidating cell reprogramming assets after USD 10 billion of sector investment.

- May 2025: Capricor Therapeutics received FDA priority review for deramiocel to treat Duchenne cardiomyopathy, setting a target action date of Aug 31 2025.

- April 2025: Vertex Pharmaceuticals secured FDA priority review for exa-cel, the inaugural CRISPR gene-editing therapy targeting severe sickle cell disease.

- January 2025: REPROCELL announced the world’s first live birth using StemRNA Clinical Seed iPSCs for oocyte maturation outside the body, marking a milestone in reproductive medicine.

Global Cell Reprogramming Market Report Scope

As per the scope of the report, cell reprogramming is a process in which the identity and characteristics of differentiated cells are altered, typically by inducing the expression of specific genes or manipulating cellular factors. Cell reprogramming aims to convert a specialized cell, often somatic or differentiated, into another cell type.

The cell reprogramming market is segmented into technology, application, end user, and geography. The market is segmented by technology into Sendai virus reprogramming, episomal reprogramming, mRNA reprogramming, and other technology types. The market is segmented by application into research and therapeutics. By end user, the market is segmented into research & academic institutes and biotechnology & pharmaceutical companies. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report also offers the market sizes and forecasts for 13 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Sendai-virus Reprogramming |

| Episomal Plasmid Reprogramming |

| Synthetic-mRNA Reprogramming |

| Retroviral/Lentiviral Reprogramming |

| Small-molecule & CRISPR-aided Reprogramming |

| Other Technologies |

| Research |

| Therapeutics |

| Diagnostics & QC assays |

| Cell-banking & biobanking |

| Research & Academic Institutes |

| Biotech & Pharma Companies |

| Contract Manufacturing Organisations |

| Hospitals & Speciality Clinics |

| Dermal Fibroblasts |

| Peripheral Blood Mononuclear Cells |

| Cord-blood / Perinatal Cells |

| Adipose-derived Cells |

| Other Somatic Sources |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Sendai-virus Reprogramming | |

| Episomal Plasmid Reprogramming | ||

| Synthetic-mRNA Reprogramming | ||

| Retroviral/Lentiviral Reprogramming | ||

| Small-molecule & CRISPR-aided Reprogramming | ||

| Other Technologies | ||

| By Application | Research | |

| Therapeutics | ||

| Diagnostics & QC assays | ||

| Cell-banking & biobanking | ||

| By End User | Research & Academic Institutes | |

| Biotech & Pharma Companies | ||

| Contract Manufacturing Organisations | ||

| Hospitals & Speciality Clinics | ||

| By Cell Source | Dermal Fibroblasts | |

| Peripheral Blood Mononuclear Cells | ||

| Cord-blood / Perinatal Cells | ||

| Adipose-derived Cells | ||

| Other Somatic Sources | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected growth rate for the cell reprogramming market to 2031?

The market is forecast to expand at an 8.14% CAGR, rising from USD 431.93 million in 2026 to USD 637.97 million in 2031.

Which technology currently dominates the cell reprogramming market?

Sendai-virus reprogramming leads with 37.62% revenue share in 2025 and remains the preferred platform for integration-free iPSC generation.

Why is Asia Pacific considered the fastest growing region

Policy incentives, large sovereign investments such as Japan’s USD 0.76 billion program, and streamlined review pathways drive a 7.55% regional CAGR through 2031.

How are safety concerns being addressed in clinical programs?

Developers adopt integration-free toolkits, enforce rigorous genomic testing, and explore partial reprogramming to mitigate tumorigenicity and instability risks.

Why are contract manufacturers gaining influence in this industry?

Building GMP suites requires high capital and specialized staff, so firms outsource to CDMOs that provide ready capacity and regulatory expertise, growing at 6.87% CAGR.

Page last updated on: