Cell Lysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

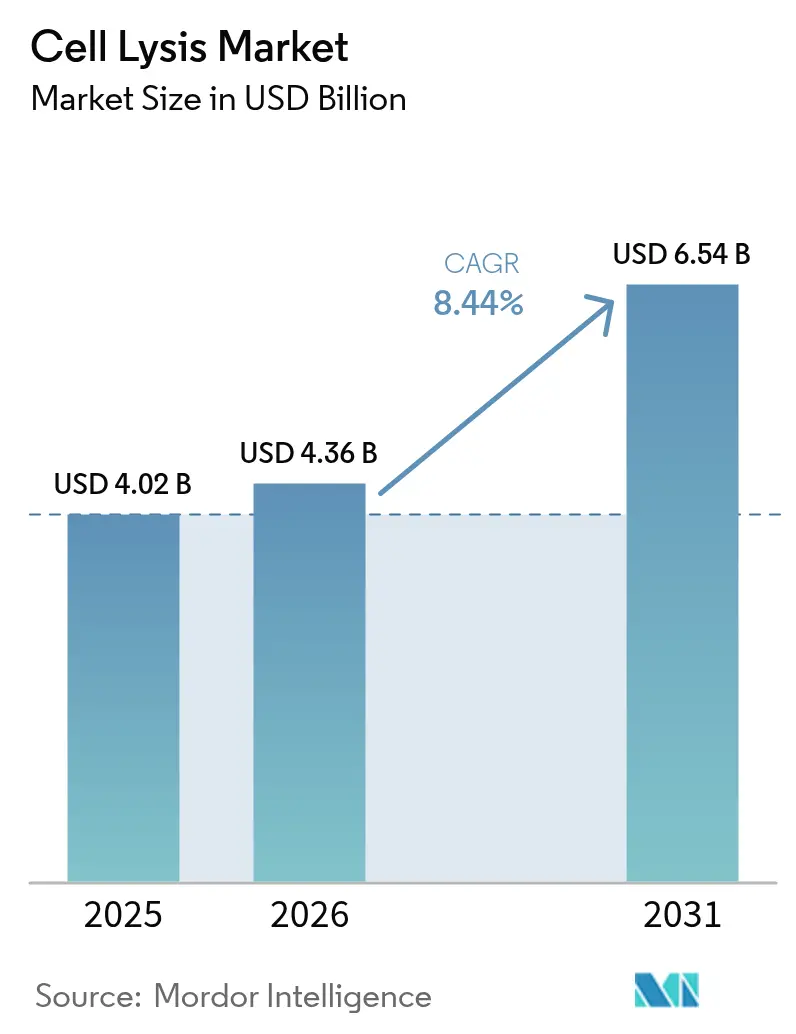

| Market Size (2026) | USD 4.36 Billion |

| Market Size (2031) | USD 6.54 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

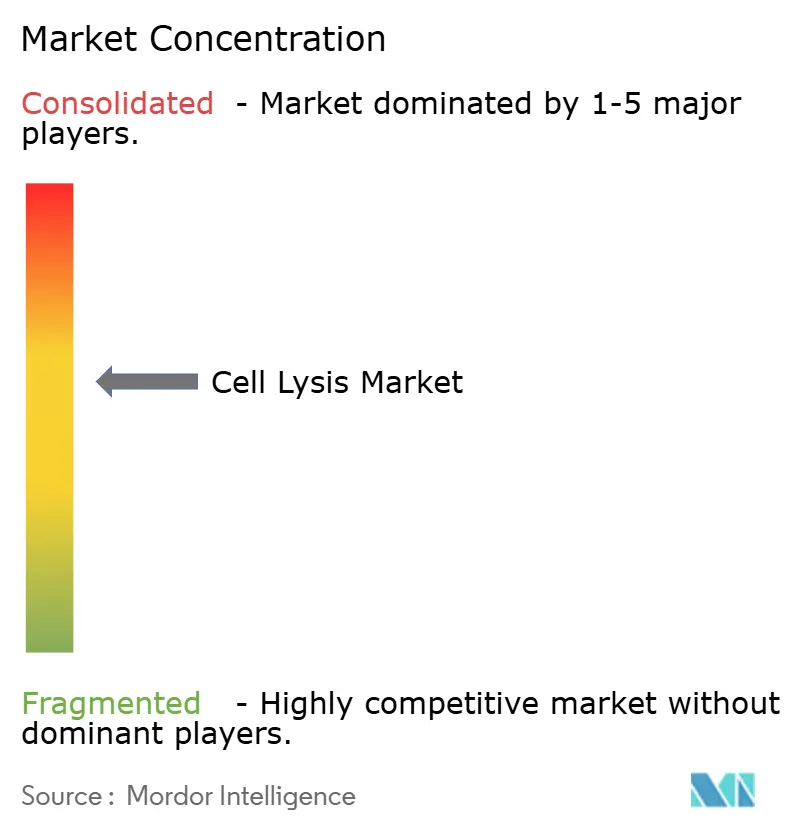

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Lysis Market Analysis by Mordor Intelligence

The cell lysis market size is expected to grow from USD 4.02 billion in 2025 to USD 4.36 billion in 2026 and is forecast to reach USD 6.54 billion by 2031 at 8.44% CAGR over 2026-2031. Sustained investment in single-cell omics, continuous bioprocessing, and automated sample-prep platforms anchors this growth trajectory. Broad adoption of gentle yet high-throughput lysis protocols supports expanding gene-therapy pipelines, while scalable mechanical systems protect product integrity in mammalian perfusion runs. Tight alignment with precision-medicine requirements has elevated lysis efficiency and reproducibility to core purchasing criteria. Companies are prioritizing closed, automated hardware to reduce contamination risk and accelerate regulatory filings. Meanwhile, environmental mandates that phase out cytotoxic detergents are steering procurement toward eco-compliant reagents and validated enzyme cocktails.

Key Report Takeaways

- By product type, reagents led with 52.07% revenue share in 2025; instruments are forecast to expand at a 12.03% CAGR through 2031.

- By cell type, mammalian cells held 45.13% of the cell lysis market share in 2025, while viral particles are projected to grow at a 16.62% CAGR to 2031.

- By lysis technique, mechanical methods captured 45.32% share of the cell lysis market size in 2025; enzymatic lysis is advancing at a 10.45% CAGR through 2031.

- By application, protein purification & proteomics accounted for a 42.52% share of the cell lysis market size in 2025, while cell-based vaccines are expanding at a 12.04% CAGR through 2031.

- By end user, biotechnology & biopharma firms led with 41.22% revenue share in 2025; the CRO/CMO segment is growing at a 13.25% CAGR to 2031.

- By geography, North America commanded 38.52% revenue share in 2025, while Asia-Pacific is projected to expand at an 11.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Lysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Single-Cell Omics Sample-Prep Demand | +2.1% | Global, with concentration in North America & EU research hubs | Medium term (2-4 years) |

| Expanding Biologics & Biosimilars Pipeline | +1.8% | Global, led by APAC manufacturing expansion | Long term (≥ 4 years) |

| Uptake Of High-Throughput Automated Workflows | +1.5% | North America & EU early adoption, APAC rapid scaling | Short term (≤ 2 years) |

| Growing Funding For Cell-Based Vaccines | +1.2% | Global, with government-backed initiatives in developed markets | Medium term (2-4 years) |

| Adoption Of Plant Molecular Farming Platforms | +0.8% | EU & North America regulatory leadership, APAC production scaling | Long term (≥ 4 years) |

| CRISPR-Based Synthetic Biology Toolkits Requiring Gentle Lysis | +1.1% | Global research centers, commercial applications in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Single-Cell Omics Sample-Prep Demand

Rapid growth in single-cell sequencing and proteomics has recalibrated lysis requirements toward extreme gentleness and contamination control. Advanced droplet and microwell platforms now process thousands of cells in parallel, demanding reagent formulations that preserve RNA and protein integrity for downstream barcoding. Vendors have responded with enzyme buffers tuned for sub-microliter reaction volumes and microfluidic hardware that shortens library-prep cycles to under 10 hours. Clinical labs now leverage these kits for minimal-invasive tumor profiling, expanding the addressable cell lysis market. Continuous feedback between reagent chemistry and consumable design accelerates protocol standardization, driving multi-site reproducibility and regulatory confidence.

Expanding Biologics & Biosimilars Pipeline

Patent expiries on blockbuster antibodies have triggered a manufacturing build-out that raises demand for large-volume, scalable lysis hardware capable of processing high-cell-density mammalian cultures. Asia-Pacific facilities contribute more than 4.7 million L of stainless and single-use capacity, reinforcing regional pull for robust homogenizers and microfluidizers. Regulatory pathways for biosimilars require validated, consistent release of intracellular product, incentivizing producers to adopt closed, automated lysis skids that integrate real-time monitoring. As continuous perfusion achieves titers above 1 g/L/day, gentle lysis becomes essential for maintaining glycosylation patterns and minimizing aggregation. Reagent suppliers benefit from multi-lot qualification programs that lock in long-term purchasing.

Uptake of High-Throughput Automated Workflows

Automation has shifted from operational convenience to strategic necessity. AI-guided sonication systems now equalize acoustic energy across 96-well plates, slashing operator variability and batch-release deviations[1]Hielscher Ultrasonics, “96-Well Plate Sonicator UIP400MTP,” hielscher.com. Capital spend is justified by lower labor costs, higher sample throughput, and tighter process-validation packages. Instruments equipped with closed-loop temperature control protect thermolabile proteins, widening applicability to fragile viral vectors. Vendors expanding software ecosystems that log every run facilitate CFR Part 11 compliance and accelerate regulatory review, further enlarging the cell lysis market.

Growing Funding for Cell-Based Vaccines

Public-sector grants are catalyzing specialized lysis solutions for viral vector and mRNA platforms. CEPI-backed spin-freezing tech and living-bioreactor projects require detergents that inactivate host cells while safeguarding enveloped virions. NIH SBIR awards for dynamic single-cell analytics highlight government recognition of upstream lysis as a rate-limiting step in vaccine R&D. These initiatives amplify demand for GMP-grade enzymes and low-shear mechanical devices that can be rapidly scaled under biosafety constraints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Bioprocess Validation & QA/QC Protocols | -1.4% | Global, with heightened requirements in North America & EU | Long term (≥ 4 years) |

| High Capital Cost Of Microfluidic Lysis Systems | -0.9% | Emerging markets and smaller biotech firms globally | Medium term (2-4 years) |

| Cytotoxic Detergent Disposal & ESG Pressures | -0.7% | EU leadership, expanding to North America & APAC | Short term (≤ 2 years) |

| Scale-Up Inefficiencies For Mammalian-Cell Intensification | -1.1% | Global manufacturing hubs, particularly APAC expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Bioprocess Validation & QA/QC Protocols

Increased FDA emphasis on real-time release tests forces manufacturers to prove lysis consistency across scales and environmental variables, lengthening development timelines and raising cost of goods. Advanced therapy developers must document viral integrity, impurity clearance, and residual-detergent profiles, often requiring multi-year comparability studies. Smaller firms without dedicated quality teams face steep barriers, reinforcing buyer preference for platforms with extensive validation dossiers and historical performance data.

High Capital Cost of Microfluidic Lysis Systems

Cutting-edge microfluidic devices deliver unrivaled gentleness and sample conservation but command premium pricing that deters adoption in resource-constrained settings. Total installed costs encompass specialized pumps, disposable chips, and proprietary software, pushing breakeven analyses beyond the reach of many pre-revenue start-ups. While contract manufacturers offer rental models, budget limitations continue to cap penetration in academic labs and emerging markets, tempering the overall cell lysis market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instruments Drive Innovation Despite Reagent Dominance

Reagents produced 52.07% of 2025 revenue as routine workflows rely on consumables for every batch, yet instruments are set to outpace with a 12.03% CAGR through 2031, underscoring their strategic importance to automated bioprocessing. Demand for smart homogenizers and bead-mill lysers is climbing as sponsors move toward 24/7 continuous operations that require minimal operator intervention. Ultrasonic disruptors now include embedded sensors that track cavitation intensity, ensuring protein integrity during high-throughput runs.

Instrument growth is also propelled by microfluidizers designed for gentle disruption of viral particles and engineered cells. Suppliers offering single-use flow-paths mitigate cross-contamination risks and streamline cleaning validation, creating long-term recurring revenue from cartridge sales. On the reagent side, enzyme cocktails tailored for plant or algal cells are gaining traction, while eco-friendly detergent replacements address Triton X-100 restrictions. Complete lysis kits integrate buffers, inhibitors, and protocols, enabling small labs to meet regulatory expectations without in-house method development.

By Cell Type: Mammalian Cells Lead While Viral Particles Surge

Mammalian cells maintained 45.13% of 2025 demand, reflecting their centrality in monoclonal antibody and recombinant protein production. The cell lysis market size for mammalian cultures is projected to expand steadily as intensified perfusion bioreactors raise cell densities that require robust yet gentle disruption. Viral particles, however, represent the fastest-growing opportunity at a 16.62% CAGR, fueled by adeno-associated virus (AAV) and lentiviral vector programs in gene and cell therapy.

Viral-specific lysis protocols combine enzymatic digestion and low-shear microfluidics to preserve capsid integrity, a prerequisite for high infectious titers downstream. Microbial cells continue to supply enzymes and industrial metabolites, sustaining solid demand for bead-beating and high-pressure homogenization. Plant cells, driven by molecular-farming initiatives, open niche avenues for proprietary enzymes that break robust cell walls while maintaining glycoprotein quality.

By Lysis Technique: Mechanical Methods Dominate Despite Enzymatic Growth

Mechanical disruption held 45.32% revenue share in 2025, confirming its status as the default choice for scale-up due to proven robustness and straightforward validation. High-pressure homogenizers and bead-mills deliver consistent particle-size reduction across batch volumes, forming the backbone of large-scale antibody purification. The cell lysis market is nevertheless witnessing a 10.45% CAGR in enzymatic methods as recombinant enzymes enable low-temperature processing that preserves conformational epitopes vital for downstream analytics.

Chemical detergents are under scrutiny following EU regulation, accelerating a shift toward biodegradable surfactants that match historic performance. Hybrid workflows integrating pulsed electric fields with enzymes illustrate a convergence of gentleness and efficiency. Osmotic shock remains confined to specialized research applications but continues to serve as a low-cost alternative when product stability permits.

By Application: Protein Purification Leads While Cell-Based Vaccines Accelerate

Protein purification & proteomics represented 42.52% of 2025 revenue, anchoring the cell lysis market with mature, validated protocols across research and manufacturing. Rising antibody titers and growing interest in subunit vaccines keep this segment resilient. Cell-based vaccines, expanding at 12.04% CAGR, benefit from global pandemic preparedness funding that fast-tracks advanced lysis solutions capable of preserving viral infectivity.

Nucleic-acid extraction supports booming sequencing and CRISPR-editing workflows, maintaining double-digit growth. Drug discovery labs rely on automated lysis in high-throughput screening to improve hit-identification fidelity. Decentralized diagnostic platforms require cartridge-integrated lysis that operates at room temperature, widening adoption in emerging healthcare settings.

By End User: Biotechnology Firms Lead While CRO/CMO Segment Surges

Biotechnology and biopharma enterprises commanded 41.22% of 2025 spending, leveraging in-house process-development teams to specify bespoke lysis hardware and reagents. The CRO/CMO sector, posting a 13.25% CAGR, scales capacity to meet global outsourcing demand, creating sizable recurring orders for turnkey lysis skids compatible with diverse client protocols.

Academic research institutes retain steady purchasing but increasingly favor eco-friendly reagents that ease laboratory disposal. Clinical diagnostic centers adopt cartridge-based systems that integrate lysis, extraction, and amplification to reduce hands-on time and biohazard exposure. Government laboratories and quality-control units complete the demand landscape, focusing on validated kits that support standardized testing frameworks.

Geography Analysis

North America captured 38.52% revenue in 2025, supported by a deep biopharmaceutical manufacturing base, significant NIH and BARDA funding, and an FDA framework that rewards validated automation. Large multi-site manufacturers deploy enterprise-wide specifications that harmonize lysis protocols across drug-substance and drug-product facilities. The United States continues to lead new-drug approvals in advanced therapies, reinforcing domestic demand for GMP-grade kits.

Asia-Pacific is forecast to achieve an 11.35% CAGR, driven by aggressive government incentives and rising CDMO activity. China’s USD 4.17 billion biomanufacturing commitment for 2025 anchors multiple industrial parks that specify closed, automated lysis modules for monoclonal and gene-therapy programs. India expands as an alternative supply-chain hub, benefiting from policy alignment with the US BioSecure Act and large domestic talent pools. Regional producers target export-grade quality, elevating demand for systems with comprehensive validation packages.

Europe remains a pivotal market where stringent environmental policies shape purchasing decisions. The ban on Triton X-100 forces rapid transition to biodegradable detergents, placing early-mover suppliers at an advantage. Manufacturers adapt by certifying alternative surfactants and updating master batch records, a process that drives reagent sales but slows new-equipment procurement until qualification completes. Northern Europe’s focus on circular economy principles encourages adoption of energy-efficient ultrasonic devices.

South America and the Middle East & Africa collectively represent smaller shares but register rising interest in decentralized diagnostic kits and local vaccine fill-finish plants. Brazil’s public vaccine institutes allocate capital toward low-shear viral-lysis technology, while Gulf region free zones court CDMOs with tax incentives covering bioprocess equipment importation. Infrastructure constraints, however, temper near-term uptake of high-cost microfluidic instruments, aligning demand toward proven mechanical systems with flexible financing.

Competitive Landscape

The cell lysis market features medium concentration: global multinationals hold sizable shares, yet niche innovators continue to enter. Thermo Fisher Scientific leads with an acquisitive strategy targeting USD 40–50 billion in M&A to extend its automation and reagent portfolio. Sartorius partners with contract manufacturers to bundle high-performance cell lines with downstream process equipment, creating turnkey packages that shorten client timelines.

Technological differentiation centers on closed automation, AI-assisted parameter control, and eco-compliant reagent chemistry. QIAGEN’s upcoming sample-prep instruments promise reduced plastic use and streamlined robotic integration, positioning the firm for laboratories seeking green credentials. Microfluidics firms emphasize gentle shear environments favorable to CAR-T workflows, while ultrasonic specialists refine cavitation management software.

White-space opportunities lie in single-cell mammalian workflows, enzymatic kits for plant molecular farming, and regional distribution in Latin America. Vendors pursuing joint ventures with local CDMOs gain early access to expansion projects, locking in preferred-supplier status before large-scale procurement cycles begin. Regulatory expertise, particularly in validation documentation, remains a decisive advantage for established players when bidding for GMP installations.

Cell Lysis Industry Leaders

Thermo Fisher Scientific

Bio-Rad Laboratories, Inc.

F. Hoffmann-La Roche Ltd.

Merck KGaA

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thermo Fisher Scientific launched the 5 L DynaDrive single-use bioreactor, boosting productivity by 27% and simplifying scale-up from 1 L to 5,000 L.

- March 2024: Sartorius and LFB Biomanufacturing partnered to create an integrated cell-line-development and manufacturing service that accelerates biologics pipelines.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cell lysis market as global sales of reagents, consumable kits, and benchtop-to-pilot instruments that rupture microbial, plant, or animal cells so researchers, clinicians, and bioprocess engineers can recover intracellular biomolecules for downstream use. According to Mordor Intelligence analysts, revenues are counted when products are sold as stand-alone units or as parts of automated sample-prep systems across academic, industrial, and clinical settings.

Scope exclusion: Tissue dissociation enzymes promoted solely for histology or regenerative medicine are not included.

Segmentation Overview

- By Product Type

- Instruments

- Homogenizers

- Bead-mill Lyser

- Ultrasonic Disruptors

- Microfluidizers

- Centrifuges

- Reagents

- Detergent Kits

- Enzymes & Nucleases

- Chemical Buffers

- Complete Lysis Kits

- Instruments

- By Cell Type

- Mammalian Cells

- Microbial Cells

- Plant Cells

- Viral Particles

- Others

- By Lysis Technique

- Mechanical (Physical)

- Chemical / Detergent

- Enzymatic

- Osmotic Shock

- By Application

- Protein Purification & Proteomics

- Nucleic-Acid Extraction & Genomics

- Cell-Based Vaccines

- Drug Discovery & Screening

- Diagnostics

- By End User

- Biotechnology & Biopharma Firms

- Contract Research & Manufacturing Organizations (CRO/CMO)

- Academic & Research Labs

- Clinical Diagnostics Centers

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Phone and web interviews with process scientists, procurement managers, and single-cell core directors across North America, Europe, and Asia tested secondary findings, clarified reagent-per-batch ratios, and confirmed adoption trends for microfluidic disruption systems.

Desk Research

We started with tier-1 public datasets such as NIH RePORTER grants, Eurostat code 847982 trade flows for homogenizers, and the WHO biologics pipeline tracker. We then added releases from BIO, ABRF, and ISCT. Annual reports, Form 10-Ks, and investor presentations revealed shipment volumes and average selling prices, while D&B Hoovers and Dow Jones Factiva validated regional splits. The sources named are illustrative only; many additional records informed data gathering and cross-checks.

Market-Sizing & Forecasting

A top-down model converted biologics batch volumes and standard lysis-reagent factors into global demand, which we then tested against a bottom-up sample of manufacturer shipments and distributor channel checks. Key inputs include biologics batch counts, single-cell sequencing kit shipments, installed high-pressure homogenizers, reagent ASP shifts, and regional biotech R&D outlays. Forecasts through 2030 draw on multivariate regression supported by scenario analysis, and gaps in bottom-up totals are reconciled through weighted averaging.

Data Validation & Update Cycle

Our analysts run a double review, variance screens against import logs and equipment registrations, and historical trend checks. Reports refresh annually, with mid-cycle updates when a material event such as a sharp capacity expansion triggers a re-run.

Why Mordor's Cell Lysis Baseline Inspires Confidence

Published estimates vary because publishers apply different scopes, base years, and exchange assumptions.

Large gaps arise when industrial fermentation skids are counted, pre-COVID datasets are rolled forward without new validation, or bundled sample-prep kits are shifted into genomics categories.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.02 B (2025) | Mordor Intelligence | |

| USD 5.70 B (2024) | Regional Consultancy A | counts capital skids and downstream filtration |

| USD 5.37 B (2023) | Global Consultancy B | folds single-cell analysis reagents, older base year |

| USD 4.10 B (2026) | Trade Journal C | secondary extrapolation, no primary interviews |

These comparisons show that Mordor's disciplined scope selection, annual refresh cadence, and dual-route validation give decision-makers a transparent, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current value of the cell lysis market?

The market is valued at USD 4.36 billion in 2026 and is projected to reach USD 6.54 billion by 2031.

Which product category is growing fastest?

Instruments are forecast to register a 12.03% CAGR through 2031 as labs invest in automation.

Why are viral-particle lysis solutions gaining traction?

Gene-therapy and vaccine programs require gentle disruption methods that protect viral infectivity, driving a 16.62% CAGR for this segment.

How do environmental regulations affect reagent choices?

The EU ban on Triton X-100 is pushing manufacturers toward biodegradable detergents and enzyme-based kits.

Which region offers the highest growth potential?

Asia-Pacific is projected to expand at an 11.35% CAGR thanks to large-scale capacity additions in China and India.

Page last updated on: