Cell Harvesting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

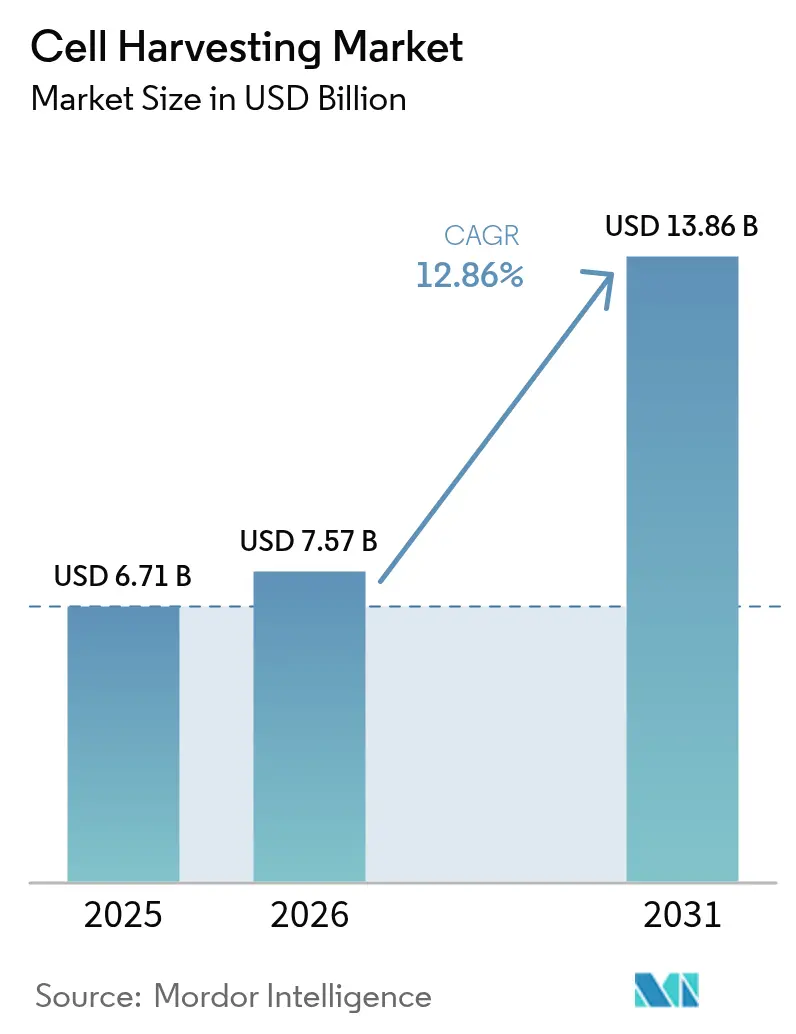

| Market Size (2026) | USD 7.57 Billion |

| Market Size (2031) | USD 13.86 Billion |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

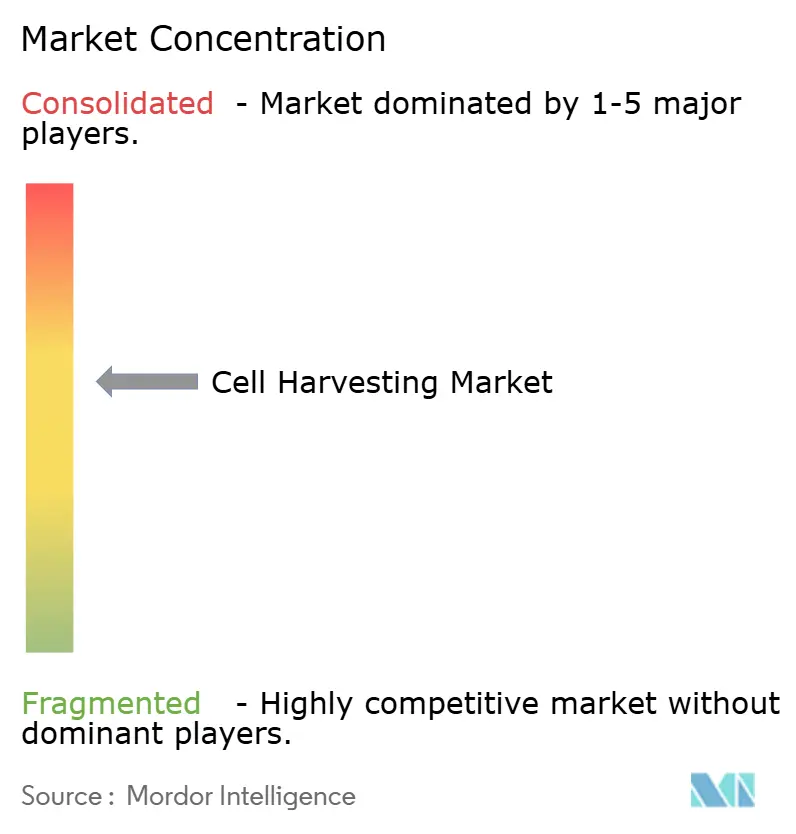

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Harvesting Market Analysis by Mordor Intelligence

The cell harvesting market size in 2026 is estimated at USD 7.57 billion, growing from 2025 value of USD 6.71 billion with 2031 projections showing USD 13.86 billion, growing at 12.86% CAGR over 2026-2031. Widespread adoption of advanced, closed, and automated harvesters that cut labor requirements by up to 75% and improve batch consistency is the prime growth catalyst. Public- and private-sector financing worth USD 2.3 billion over the past decade, regulatory commitments to approve 10–20 cell and gene therapies per year, and supply-chain investments in point-of-care (PoC) manufacturing hubs reinforce this expansion. North American early-adopter demand, Asia-Pacific capacity build-outs, and continuous platform innovation that combines AI analytics with single-use hardware create additional momentum.

Key Report Takeaways

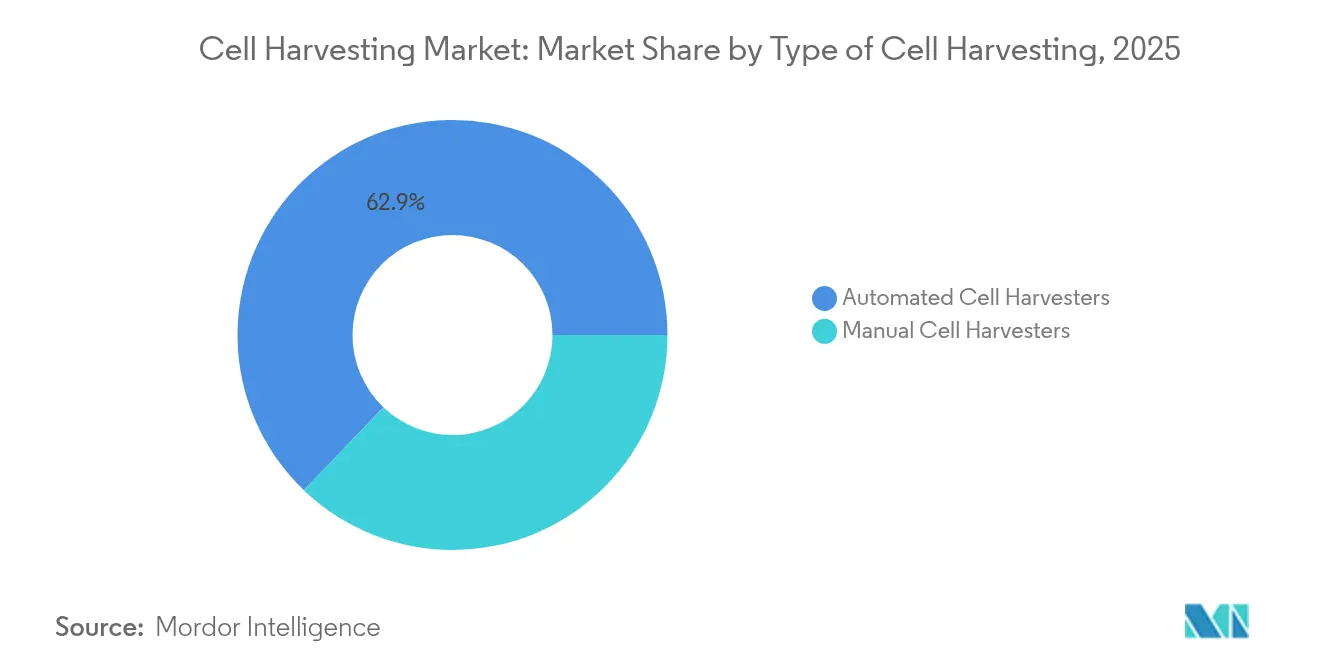

- By type of cell harvesting, automated cell harvesters held 62.85% share in 2025 and are projected to expand at a 14.92% CAGR through 2031.

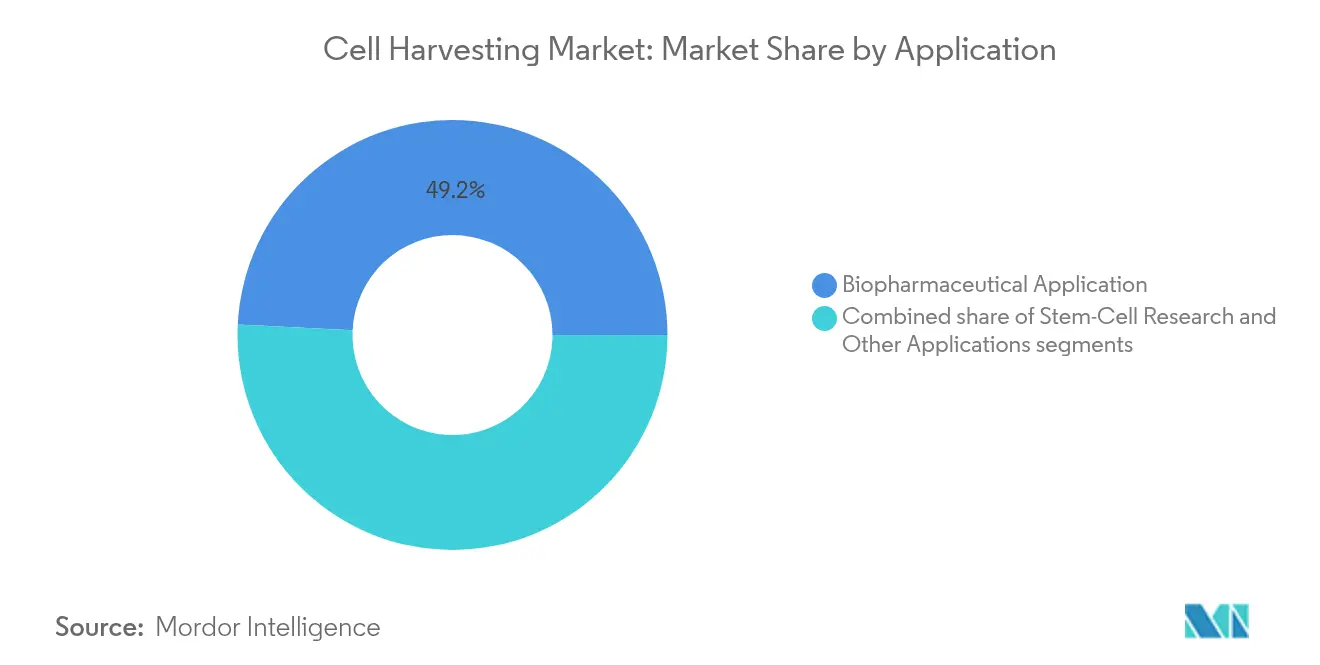

- By application, biopharmaceutical production accounted for 49.23% of revenue in 2025, while stem-cell research is expected to post a 16.05% CAGR to 2031.

- By end user, biotechnology and biopharmaceutical companies commanded 51.84% of the cell harvesting market size in 2025; research institutes are set to grow at a 15.67% CAGR during 2026-2031.

- By geography, North America contributed 38.95% of global sales in 2025, whereas Asia-Pacific is anticipated to deliver a 14.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Harvesting Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing investment in cell and gene therapies | +3.2% | North America and Europe | Long term (≥ 4 years) |

| Expansion of biopharmaceutical manufacturing infrastructure | +2.8% | Global, APAC rising | Medium term (2–4 years) |

| Rising prevalence of chronic diseases requiring cell therapies | +2.1% | Global | Long term (≥ 4 years) |

| Technological advancements in automated cell processing | +2.4% | North America and EU, APAC adoption | Medium term (2–4 years) |

| Supportive regulatory frameworks for advanced therapies | +1.8% | North America, EU, Japan, South Korea | Medium term (2–4 years) |

| Emergence of personalized and PoC cell therapy platforms | +1.3% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Investment in Cell and Gene Therapies

More than USD 2.3 billion in equity has entered cell and gene therapy ventures during the last decade, underpinning over 1,500 active clinical studies worldwide[1]Journal of Translational Medicine, “Global Cell Therapy Market Forecast,” translational-medicine.biomedcentral.com. The FDA cleared eight novel advanced therapies in 2024, including the first mesenchymal stromal cell product, Ryoncil, demonstrating regulatory confidence in complex biologics[2]U.S. Food and Drug Administration, “Cellular & Gene Therapy Guidance Documents,” fda.gov. Pharmaceutical majors are scaling quickly: Bristol Myers Squibb opened three dedicated CAR-T plants, and AstraZeneca spent USD 425 million for EsoBiotec to accelerate in vivo programs. Capital inflows shorten development timelines and increase the volume of autologous and allogeneic batches that require reliable, high-throughput harvesters. Investors now prioritize platforms that can support multiproduct pipelines, lifting the appeal of integrated harvest devices with modular add-ons.

Expansion of Biopharmaceutical Manufacturing Infrastructure

Fujifilm Diosynth’s USD 1.6 billion Denmark-Texas expansion adds eight 20,000 L bioreactors and specialized downstream suites, while Lotte Biologics is committing USD 1 billion for its Songdo Bio Campus to reach 120,000 L capacity by 2027. Such mega-projects create regional clusters that need harvesters compatible with both single-use and stainless-steel trains. Many CDMOs still operate at less than 50% utilization, prompting demand for flexible systems that can cost-effectively handle clinical-scale autologous lots today and pivot to large allogeneic runs tomorrow. Suppliers offering modular skid architecture with interchangeable centrifugation or filtration elements address this utilization gap and can be rapidly redeployed as production priorities change.

Rising Prevalence of Chronic Diseases Requiring Cell Therapies

Cancer incidence and refractory hematological conditions continue to rise, expanding the pool of patients who may benefit from CAR-T and NK-cell therapies. Autologous treatment protocols demand time-critical harvesting of functional cells, motivating oncology centers to deploy closed, sterile harvest workstations. Parallel growth in orthopedic and cardiovascular regenerative applications fuels demand for large, high-quality mesenchymal stromal cell yields. Demographics in North America, Europe, and high-income Asian economies magnify this trend, as aging populations require novel regenerative interventions. Providers that can deliver consistent, viable harvests despite patient-to-patient variability are well placed to capture clinician trust.

Technological Advancements in Automated Cell Processing

Terumo BCT’s Quantum Flex system cuts harvest time by 88% relative to manual flasks while preserving >90% viability. Cellares reports 760% throughput gains and 80% floor-space savings with its Cell Shuttle compared with traditional laminar-flow suites. Sartorius’ Ksep instrument achieves >90% cell recovery under low-shear conditions, reducing contamination risks through single-use chambers. Emerging AI layers adjust spin speed and buffer exchanges in real time, lowering error rates that currently range from 4–10% in commercial CAR-T batches. Smaller footprints, lower headcount requirements, and digital batch records combine to improve cost-of-goods and regulatory traceability.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical and regulatory concerns around stem cell sourcing | -1.9% | Global, intensity varies by jurisdiction | Medium term (2–4 years) |

| High cost of automated harvesting systems | -2.3% | Global, greater impact in emerging markets | Short term (≤ 2 years) |

| Variability and quality control challenges in donor-derived cells | -2.0% | Global, pronounced where donor pools are heterogeneous | Medium term (2–4 years) |

| Cold-chain and logistics complexities for live cells | -1.6% | Global, especially regions with limited infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ethical and Regulatory Concerns Around Stem Cell Sourcing

Embryonic stem cell research and unproven adipose-derived procedures face increased oversight after U.S. appellate courts confirmed that reinjected cells fall under FDA biologics regulation. Divergent donor screening rules in the EU, United States, and Asia complicate multinational studies and raise documentation costs. Unlicensed clinics advertising miracle cures in regions with light enforcement undermine public confidence, prompting regulators to publish warning letters and mandate clinic closures. Compliant suppliers that document ethical sourcing and GMP provenance can differentiate, but they must navigate evolving consent requirements and tissue-bank audits that vary by country.

High Cost of Automated Harvesting Systems

Top-tier automated harvesters often exceed USD 1 million per unit, and annual validation plus service contracts add further burden. Smaller biotechs, early-stage academic labs, and emerging-market hospitals frequently lack capital to purchase such systems, postponing adoption. Manufacturing-as-a-service models are easing the pain: Cellares offers pay-per-batch access to its Cell Shuttle, eliminating upfront investment. Competitive pressure has spurred development of modular harvesters priced 20–30% below flagship devices, but the need for trained technicians and validated clean utilities continues to slow uptake in low-resource settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Cell Harvesting: Automation Drives Market Evolution

Automated systems held 62.85% of the cell harvesting market share in 2025 thanks to closed, programmable workflows that cut labor hours and contamination risk. They are projected to record a 14.92% CAGR through 2031. Manual harvesters remain relevant for exploratory work or highly variable early-phase protocols that benefit from hands-on manipulation. However, even academic labs are adopting semi-automated modules that bolt onto legacy incubators, blending tactile oversight with digital monitoring. Industry-wide migration toward continuous processing and single-use assemblies will likely elevate automated systems to more than 70% of the cell harvesting market size by decade’s end.

Automation’s momentum aligns with factory digitization goals. Vendors are bundling integrated centrifugation, filtration, and washing in one chassis to streamline line clearance and validation. Remote diagnostics and software updates provide shorter downtimes and keep performance within specification. Suppliers able to certify systems in multiple jurisdictions and offer 24-hour parts support gain a competitive edge as global trials expand.

By Application: Biopharmaceutical Dominance with Research Acceleration

Commercial biologics accounted for 49.23% of the 2025 revenue pool, supported by an increasing number of on-market CAR-T products and regulatory approvals for next-generation allogeneic candidates. Autologous oncology programs drive batch volumes that must meet stringent sterility and timeline targets, reinforcing demand for robust harvest platforms. Meanwhile, stem-cell and regenerative medicine research is the fastest-growing application, advancing at a 16.05% CAGR to 2031. Investment in induced pluripotent stem cell lines, 3D organoid models, and CRISPR-edited therapeutics boosts laboratory harvesting requirements. High-throughput screen-expansion-harvest combinations permit scientists to analyze hundreds of cell lines per week, accelerating lead identification.

Cross-disciplinary convergence blurs historical boundaries. Vaccine developers adapting cell-based production, exosome therapy startups, and protein deuteration specialists are adopting the same harvest infrastructure. Vendors certified for multi-mode payloads gain preferential status because clients can amortize equipment across several programs. As product pipelines diversify, harvesters capable of switching from T lymphocytes to MSCs with minimal cleaning or changeover time become essential.

By End User: Biotech Leadership with Academic Growth

Biotechnology and biopharmaceutical companies represented 51.84% of 2025 demand due to their focus on late-stage trials and commercial launches that require cGMP harvest capacity. They prefer integrated, high-throughput suites featuring automated cell collection, concentration, and buffer exchange modules. Academic and government institutes are the fastest-growing end user group, expanding at 15.67% CAGR, fueled by public grants and collaborative research initiatives. Canada’s USD 22.5 million grant to STEMCELL Technologies for a GMP plant exemplifies this support. Hospitals and specialized treatment centers are piloting PoC manufacturing, often via containerized cleanrooms that host compact harvesters. Suppliers offering turnkey service packages—compliance documentation, operator training, remote monitoring—stand to expand market reach among resource-constrained centers.

Geography Analysis

North America held 38.95% of global revenue in 2025, supported by a mature CGT regulatory framework, extensive CDMO network, and specialized logistics operators. Yet fewer than 20% of eligible U.S. patients accessed available therapies in 2024, underscoring process inefficiencies that automated harvesters can mitigate. Regional growth also depends on skilled labor supply, prompting partnership programs between equipment vendors and community colleges to cultivate technicians.

Asia-Pacific is projected to expand at 14.11% CAGR to 2031. China hosted 37% of global CGT trials in 2024, and Japan’s Fast Track and South Korea’s Regenerative Medicine Law cut approval timelines. Domestic players like WuXi AppTec and SK Bioscience have invested heavily in CGT hubs, driving bulk orders for harvest modules compatible with local GMP guidelines. Lower operating costs, government incentives, and rising chronic-disease prevalence amplify demand, but suppliers must adapt to evolving import regulations and multilingual quality documentation.

Europe maintains a sizable share anchored by harmonized EMA guidelines and robust CDMO infrastructure in Denmark, Ireland, and Germany. Fujifilm Diosynth’s Danish plant expansion exemplifies continued capital inflow aimed at increasing regional self-sufficiency. Energy costs push facilities to adopt energy-efficient harvesters with shorter cycle times. The Middle East & Africa and South America are emerging opportunity zones as healthcare systems invest in tertiary care and establish bilateral technology-transfer agreements. Compact, rugged harvesters that tolerate power fluctuations find growing reception in these regions.

Competitive Landscape

The cell harvesting market features moderate fragmentation, yet consolidation is accelerating. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification and filtration business and Danaher’s merger of Cytiva and Pall into a USD 7.5 billion bioprocess entity illustrate platform convergence. Large vendors leverage scale to offer integrated upstream-to-downstream suites, pressuring smaller specialists focused on single modalities. Mid-size firms differentiate via technological depth—for example, Miltenyi Biotec’s magnetic separation or Sartorius’ low-shear centrifugation—and by offering flexible financing plans attractive to smaller clients.

White-space opportunities center on point-of-care systems and AI-driven optimization layers. Orgenesis’ PoCare cabins and Cellares’ Cell Shuttle reduce capital outlay and operational complexity for autologous products. Emerging startups harness real-time imaging and predictive analytics to automate harvest end-points, attracting strategic partnerships with established equipment brands. Service models that bundle validation, remote monitoring, and cybersecure cloud batch records offer additional revenue streams and help vendors differentiate in an otherwise hardware-centric competitive arena.

Supply-chain resilience remains a strategic concern. Only a handful of companies can supply GMP-compliant, closed-system harvesters at commercial volumes across three continents. Manufacturers seeking dual sourcing push vendors to open regional assembly facilities and expand spare-parts depots to minimize downtime.

Cell Harvesting Industry Leaders

Perkin Elmer Inc.

Sartorius AG

Terumo Corporation

Danaher Corporation

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AstraZeneca acquired EsoBiotec for USD 425 million, strengthening its in vivo cell therapy portfolio.

- March 2025: DHL Group bought CRYOPDP from Cryoport to expand specialized pharma logistics for CGT shipments.

- February 2025: Thermo Fisher announced a USD 4.1 billion purchase of Solventum’s purification & filtration unit, adding complementary bioproduction capabilities.

- January 2025: Terumo BCT partnered with FUJIFILM Irvine Scientific to combine Quantum Flex with PRIME-XV media for rapid T-cell expansion.

- December 2024: The FDA approved Ryoncil, the first mesenchymal stromal cell therapy for pediatric GVHD.

- December 2024: Sumitomo Chemical formed RACTHERA, aiming for ¥350 billion regenerative medicine revenue by the late 2030s.

Global Cell Harvesting Market Report Scope

As per the report's scope, cell harvesting is a technique for collecting different types of cells on the cultural surface. Multiple cell harvesting methods, such as centrifugation, filtration, microfiltration, cell separation, and T-cell culture, are used depending on the types of samples and experiments. Cell harvesting is considered an important operation that involves the removal of cells, cell debris, and other soluble and insoluble impurities that are detrimental to the subsequent chromatographic separation process.

The cell harvesting market is segmented by type of cell harvesting, application, end user, and geography. By type of cell harvesting, the market is segmented into manual cell harvesters and automated cell harvesters. By application, the market is segmented into biopharmaceutical applications, stem cell research, and other applications. By end user, the market is segmented into biotechnology and biopharmaceutical companies, research institutes, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in value (USD) for the above segments.

| Manual Cell Harvesters |

| Automated Cell Harvesters |

| Biopharmaceutical Application |

| Stem-Cell Research |

| Other Applications |

| Biotechnology & Biopharmaceutical Companies |

| Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type of Cell Harvesting | Manual Cell Harvesters | |

| Automated Cell Harvesters | ||

| By Application | Biopharmaceutical Application | |

| Stem-Cell Research | ||

| Other Applications | ||

| By End User | Biotechnology & Biopharmaceutical Companies | |

| Research Institutes | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the cell harvesting market?

The cell harvesting market size is USD 7.57 billion in 2026 and is forecast to reach USD 13.86 billion by 2031.

Which segment holds the largest cell harvesting market share?

Automated cell harvesters led with a 62.85% share in 2025, driven by demand for process intensification.

Which application area is growing fastest?

Stem-cell research is registering a 16.05% CAGR through 2031, making it the most rapid-growth application.

Which region is expected to expand quickest?

Asia-Pacific is projected to achieve a 14.11% CAGR to 2031 due to regulatory fast-track programs and extensive clinical trial activity.

What are the key restraints limiting adoption of automated harvesters?

High capital cost—often exceeding USD 1 million per unit—and varying ethical regulations on stem cell sourcing continue to impede widespread uptake.

How consolidated is the competitive landscape?

The market scores a 6 on a 10-point concentration scale, with the top five vendors holding around 60% of worldwide revenue.

Page last updated on: