Cell Signaling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

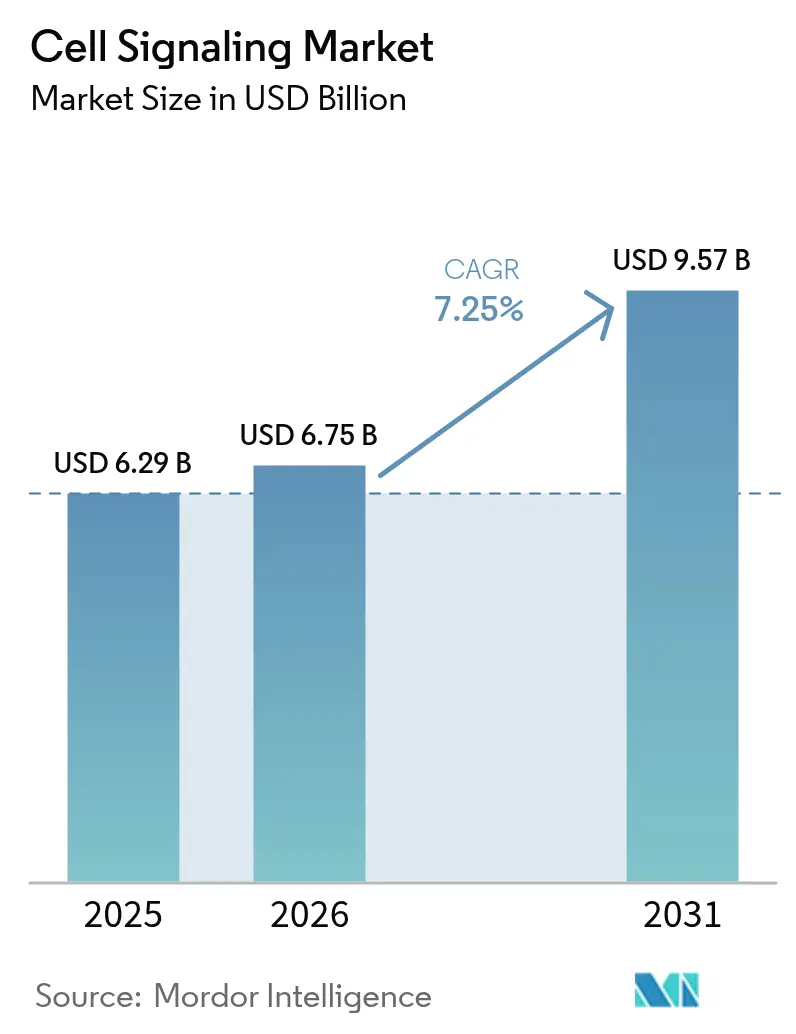

| Market Size (2026) | USD 6.75 Billion |

| Market Size (2031) | USD 9.57 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

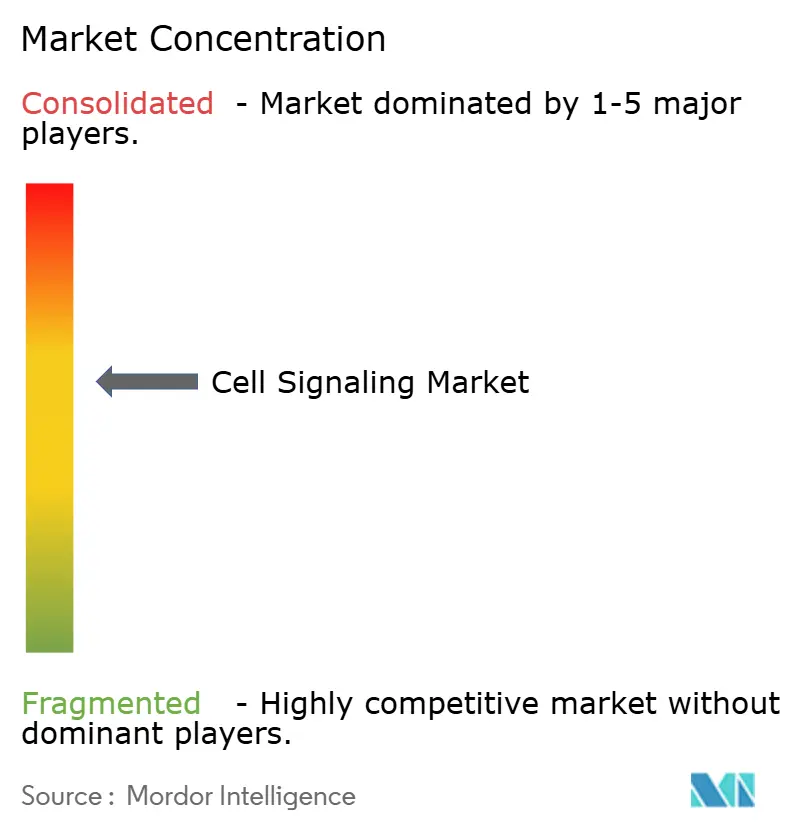

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Signaling Market Analysis by Mordor Intelligence

The cell signaling market size was valued at USD 6.29 billion in 2025 and estimated to grow from USD 6.75 billion in 2026 to reach USD 9.57 billion by 2031, at a CAGR of 7.25% during the forecast period (2026-2031). Growth rests on sustained capital spending for automated flow cytometers, mass spectrometers and multiplex imaging systems that generate richer cellular data with fewer manual steps. North America retains leadership on the back of generous National Institutes of Health (NIH) grants and a receptive regulatory climate, while Asia-Pacific posts the fastest gains as Japan, South Korea and China expand single-use bioreactor capacity for clinical-grade cell and gene therapies. Momentum is reinforced by the U.S. Food and Drug Administration’s (FDA) 2024 clearance of Ryoncil, the first allogeneic mesenchymal stromal cell product for steroid-refractory acute graft-versus-host disease, which signals wider acceptance of cell-based interventions. Leading suppliers are sharpening artificial-intelligence modules that cut assay-development cycles and improve reagent selection, thereby raising entry barriers for smaller competitors.

Key Report Takeaways

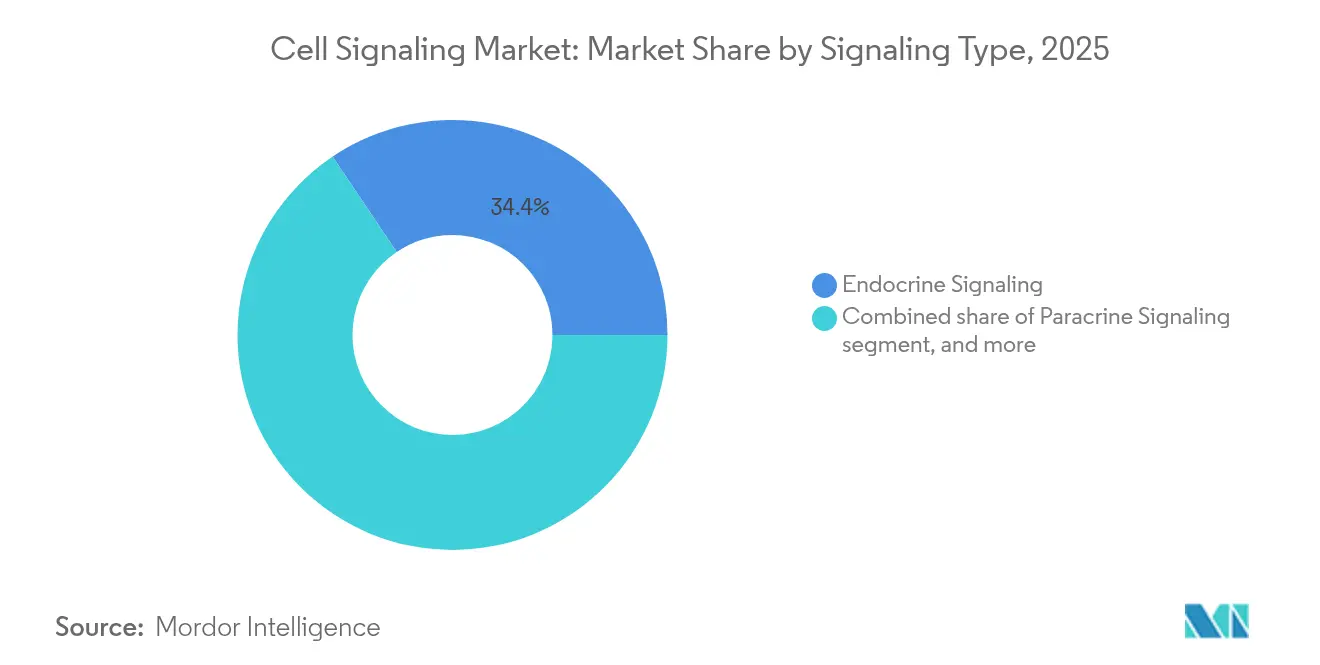

- By signaling type, endocrine signaling led with 34.41% revenue share in 2025, whereas autocrine signaling is projected to expand at a 8.88% CAGR through 2031.

- By product category, instruments accounted for 55.10% of the cell signaling market share in 2025, while consumables are forecast to post a 9.15% CAGR to 2031.

- By technology, flow cytometry captured 45.98% of the cell signaling market size in 2025; western blotting is advancing at a 9.55% CAGR through 2031.

- By pathway, the AKT/PI3K cascade held 22.18% of 2025 revenue, whereas AMPK signaling records the quickest 10.64% CAGR over the forecast window.

- By application, drug discovery and development commanded 34.12% of the cell signaling market in 2025; cancer and stem-cell research is pacing at a 10.15% CAGR.

- By end user, pharmaceutical and biotech companies generated 45.02% of demand in 2025, while contract research organizations (CROs) show the strongest 11.85% CAGR outlook.

- By geography, North America dominated with 42.02% revenue share in 2025; Asia-Pacific leads growth at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Signaling Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence Of Chronic And Autoimmune Diseases | +0.8% | Global | Long term (≥ 4 years) |

| Expanding Funding For Cell-Based Life Science Research | +0.7% | North America & Europe | Medium term (2-4 years) |

| Continuous Technological Innovations In Cell Analysis Platforms | +0.9% | Global | Short term (≤ 2 years) |

| Increasing Adoption Of Artificial Intelligence In Bioassay Design | +0.5% | North America | Medium term (2-4 years) |

| Emergence Of Three-Dimensional Microfluidic Cell Culture Models | +0.6% | Europe & Asia-Pacific | Long term (≥ 4 years) |

| Rapid Scale-Up Of Cell Therapy Manufacturing Workflows | +0.5% | Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic and Autoimmune Diseases

The rising incidence of chronic and autoimmune disorders is redirecting capital toward modular lipid-nanoparticle platforms that generate CAR-T cells in vivo, eliminating lengthy ex-vivo manufacturing. Mesenchymal stromal cell (MSC) transplantation continues to produce compelling remission rates across rheumatoid arthritis and systemic sclerosis, fueling wider payer acceptance. As aging populations swell in high-income economies, regenerative medicine trials targeting joint degeneration and metabolic syndrome further accelerate demand for advanced pathway analyses and functional-immune readouts.

Expanding Funding for Cell-Based Life-Science Research

Thermo Fisher Scientific is investing USD 2 billion over four years—USD 500 million earmarked for R&D—to anchor U.S. production of high-impact analytical systems, a move mirroring similar manufacturing onshoring initiatives by rivals. In parallel, Orionis Biosciences secured USD 105 million upfront from Genentech for molecular-glue programs, underscoring venture appetite for next-generation modality platforms. Across Asia-Pacific, sovereign wealth funds have started funneling capital into cell-therapy process-development hubs, compressing technology-transfer timelines for local biologics manufacturers.

Continuous Technological Innovations in Cell-Analysis Platforms

BD’s FACSDiscover A8 marries spectral flow cytometry with high-speed imaging, letting scientists interrogate more than 50 cellular attributes in one run. Beckman Coulter’s Mosaic module pushes spectral detection to 88 channels, while Thermo Fisher’s Orbitrap Astral Zoom increases mass-spectrometry throughput six-fold. The common thread is tighter integration between optical, mass-analytic and informatics stacks, reducing sample-to-result cycles and widening possible biomarker panels.

Increasing Adoption of Artificial Intelligence in Assay Design

Large-language-model algorithms are now embedded in primer-design portals that predict off-target binding and optimize GC content in minutes, freeing researchers from iterative wet-lab validation. Machine-learning classifiers trained on public phospho-proteomics datasets deliver pathway-activation maps that inform drug-screen hit prioritization. Companies pairing such tools with automated liquid handlers report double-digit reductions in reagent waste and faster lot-release decisions for critical antibodies.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Required For Advanced Cell Signaling Systems | -0.4% | Global | Short term (≤ 2 years) |

| Ethical And Regulatory Concerns Surrounding Stem Cell Research | -0.3% | Europe & North America | Long term (≥ 4 years) |

| Inconsistent Quality Of Critical Reagents And Antibodies | -0.3% | Asia-Pacific & Latin America | Medium term (2-4 years) |

| Big-Data Management Challenges In Single-Cell Omics Workflows | -0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Required for Advanced Cell-Signaling Systems

Turn-key spectral cytometers exceed USD 750,000 per unit, stretching academic grant cycles and delaying upgrades in lower-income regions. Therapeutic-grade monoclonal antibody production still costs between USD 15,000 and USD 140,000 annually for a single indication, which inflates downstream consumable budgets. Contract manufacturing organizations report sub-50% utilization rates, revealing a supply–demand mismatch that exacerbates cost-recovery challenges for platform owners.

Ethical and Regulatory Concerns Surrounding Stem-Cell Research

Utah and Florida statutes allowing certain unapproved stem-cell therapies dilute federal oversight and introduce multi-jurisdictional compliance hurdles. The FDA’s draft guidance on allogeneic-cell safety testing tightens donor-screening, viral-inactivation and tumorigenicity-assessment requirements, adding time and cost burdens to development programs. European directives remain more restrictive, which can slow multicenter trial initiation and cross-border sample movement for sponsored studies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Signaling Type: Endocrine Pathways Drive Systemic Research

Endocrine signaling held 34.41% of the cell signaling market in 2025, underpinning metabolic and reproductive studies that require hormone-receptor assays at organ scale. Autocrine signaling is on track for the fastest 8.88% CAGR because oncology programs increasingly dissect self-stimulating loops that govern tumor proliferation. Paracrine signaling retains relevance for tissue-repair models, while synaptic mechanisms benefit from higher neuroscience funding.

Growing mechanistic clarity around autocrine feedback has spurred design of pathway-selective inhibitors and companion diagnostics. Paracrine insights have inspired nanoparticle carriers programmed to home lymph-node chemokine gradients, an approach now in mid-phase breast-cancer trials. Together, these advances keep the cell signaling market firmly focused on translating pathway biology into precision therapeutics.

By Product: Instruments Lead Despite Consumables Growth

Instruments accounted for 55.10% of 2025 revenue, reflecting the hefty ticket price of analytical workstations that constitute the core lab infrastructure. Consumables, however, are poised to outpace with a 9.15% CAGR as recurring reagent orders scale with assay volume. Flow-cytometry skids, high-resolution imaging chips and microfluidic cartridges dominate replacement cycles, especially in decentralized CRO facilities.

Consumables demand also rises because recombinant antibodies outperform conventional polyclonal reagents on specificity, trimming reproducibility failures that previously cost U.S. labs up to USD 1.8 billion annually. Suppliers offering antibody-validation data sets gain customer stickiness and incremental margins.

By Technology: Flow-Cytometry Dominance Amid Western-Blotting Surge

Flow cytometry retained 45.98% of the cell signaling market share in 2025 on the strength of multiplexed phenotyping and cell-sorting flexibility. Western blotting, rejuvenated by parallel-reaction-monitoring mass-spectrometry readouts, is rising at a 9.55% CAGR as labs pivot to quantitative proteomics. Small-particle detection down to 70 nm now blurs the line between cytometry and nanoparticle analytics, unlocking exosome-tracking workflows.

Integrated imagers and spectral optics let users visualize morphology while gating complex cell populations, a duality that unlocks new immuno-oncology endpoints. Meanwhile, ELISA remains the economical option for batch cytokine quantification in high-throughput screens.

By Pathway: AKT/PI3K Leadership Reflects Cancer Focus

The AKT/PI3K axis held 22.18% revenue in 2025, cemented by its frequent dysregulation in breast, prostate and endometrial cancers. AMPK signaling carries the fastest 10.64% CAGR thanks to mounting evidence of its role in metabolic reprogramming and age-related immune decline. Covalent-allosteric AKT inhibitors tailored to the E17K mutation demonstrate fewer glycemic-side effects, validating isoform selectivity strategies.

Natural‐product libraries that activate AMPK showcase multi-target potential against insulin resistance, encouraging botanical-extract suppliers to seek Investigational New Drug (IND) pathways.

By Application: Drug Discovery Leads Amid Cancer-Research Acceleration

Drug discovery captured 34.12% of the cell signaling market size in 2025, aligned with pharma’s priority to de-risk targets early in the pipeline. Cancer and stem-cell research is climbing quickest at 10.15% CAGR, fueled by next-generation checkpoint modulators and microenvironment-on-a-chip screens that better mimic tumor physiology.

AI-guided phenotypic screens accelerate lead identification, with Bayer and Recursion Pharmaceuticals pursuing up to seven oncology programs under a USD 1.5 billion milestone framework. In parallel, molecular-glue degraders licensed by Degron Therapeutics to Takeda illustrate how novel chemistries reshape targeted-protein-degradation strategies.

By End User: Pharma Dominance Amid CRO Expansion

Pharma and biotech companies generated 45.02% of 2025 sales, leveraging in-house pathway assays to validate biomarkers before clinical entry. CROs exhibit the strongest 11.85% CAGR as cell-therapy firms outsource analytics to scale faster. The U.S. cell-therapy space, valued at USD 2.88 billion in 2023 and projected to hit USD 19.67 billion by 2033, exemplifies the workload CROs now absorb.

Academic centers continue to supply seminal discoveries, such as sub-cellular “wearable” neuro-modulators that monitor interface currents in demyelinating diseases. These innovations often spin out into start-ups that further enlarge the CRO client base.

Geography Analysis

North America generated 42.02% of global revenue in 2025, underpinned by NIH grant stability, venture capital depth and FDA guidance that shortens regulatory review for regenerative candidates. Thermo Fisher’s multi-year USD 2 billion domestic build-out underscores supplier confidence in continued demand for high-throughput instrumentation. State-level legislation permitting certain unapproved stem-cell interventions introduces compliance fragmentation that large sponsors must now navigate.

Asia-Pacific leads growth at a 8.12% CAGR through 2031 as governments expand bioprocess tax incentives and roll out accelerated approval pathways for rare-disease therapies. China alone has compiled single-cell-omics atlases covering 120 million cells, offering unparalleled annotation depth for AI-training datasets. Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) continues to refine its Sakigake fast-track to keep pace with U.S. breakthrough designation metrics.

Europe holds material share yet lags on speed: stringent cell-therapy directives extend trial-setup timelines, though they bolster supply-chain transparency. The region’s active-pharmaceutical-ingredient (API) market is climbing 5.78% annually, with synthetic APIs largest today and biotech APIs growing fastest. Oncology remains Europe’s most dynamic indication as hospitals integrate companion diagnostics into standard-of-care pathways.

Regulatory Landscape

Regulation shaping cell signaling tools is most visible at the intersection of advanced therapies, bioassay validation, and biomedical research funding rules. In the United States, the FDA Center for Biologics Evaluation and Research (CBER) published its 2026 guidance agenda (with a multi-item therapeutic products slate) and, on January 11, 2026, issued an approach emphasizing flexible requirements for certain cell and gene therapy products. This approach influences assay design and comparability expectations, which in turn supports demand for higher-confidence pathway readouts (eg, flow cytometry, proteomics, and multiplex imaging).

Research-policy shifts also affect which signaling models and reagents labs can use under federal funding. NIH Notice NOT-OD-26-028 (effective January 22, 2026) restricts NIH funds for research involving human fetal tissue from elective abortions, while NOT-OD-26-031 paused new submissions to the Human Embryonic Stem Cell Registry during 2026 for an assessment of alternatives. NOT-OD-26-067 updated compliance for Basic Experimental Studies with Humans (BESH) for applications submitted on or after May 25, 2026. In Europe, the regulatory framework for advanced therapy medicinal products continues under Regulation (EC) No 1394/2007 and Directive 2001/83/EC, with the EMA Committee for Advanced Therapies (CAT) central to assessment. This emphasis keeps quality, safety, and traceability requirements prominent in multicenter studies that rely on standardized signaling assays and reagents.

Competitive Landscape

Industry concentration is moderate, with the top five vendors controlling roughly 55% of 2024 revenue. Thermo Fisher Scientific, Danaher’s Beckman Coulter unit and BD dominate instrument platforms, while Bio-Rad occupies niche leadership in digital PCR reagents. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s filtration division broadens its upstream bioproduction footprint, signalling an ecosystem move toward end-to-end workflow ownership.

Technology cycles are compressing: BD delivered spectral-imaging cytometers barely 15 months after its last flagship sorter, compelling rivals to accelerate roadmaps. Cytek Biosciences’ 70 nm particle-detection upgrade extends cytometry into exosome analytics, a frontier where larger incumbents have limited playbooks. Partnerships such as Cell Signaling Technology’s diagnostic tie-up with AmoyDx demonstrate the pivot toward companion-diagnostic co-development that de-risks drug-launch timelines.

White-space competition emerges in AI-driven assay-design suites. Vendors integrating transformer-based single-cell transcriptional models within instrument firmware promise one-button experiment setup, a differentiator likely to upend traditional reagent-subscription models.

Cell Signaling Industry Leaders

Bio-Rad Laboratories Inc.

Cell Signaling Technology Inc.

PerkinElmer Inc.

Becton, Dickinson and Company

Danaher Corporation (Beckman Coulter Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities concentrate in higher-reproducibility signaling reagents and in workflow integration that links pathway biology to cell therapy, organoids, and spatial and single-cell systems. In July 2026, Bio-Techne expanded its R&D Systems AI-Engineered Designer Protein portfolio (including cytokines and pathway agonists) to improve reproducibility in cell therapy and organoid development workflows. This addition aligns with the market need for more consistent, application-validated signaling inputs as assay multiplexing increases.

Manufacturing and CDMO build-outs in 2026 also expand the installed base of bioprocess and analytical users who need scalable signaling characterization and release-support assays. Examples include Johnson & Johnsons announcement of a more than USD 1 billion next-generation cell therapy manufacturing facility in Pennsylvania, Genentechs move to approximately USD 2 billion for a biomanufacturing facility in Holly Springs, North Carolina, and Evoniks July 2026 plan to invest USD 100 million over five years to modernize its Tippecanoe, Indiana drug substance site. These programs create white space for instrument and consumables vendors to standardize pathway and phenotypic assays across process development, comparability, and multi-site tech transfer, beyond stand-alone bioinformatics software.

Recent Industry Developments

- June 2026: Cell Signaling Technology partnered with Quantum-Si to develop and validate post-translational modification (PTM) analysis workflows on the Proteus single-molecule protein sequencing platform. The collaboration pairs CSTs immunoaffinity and PTM expertise with a newer sequencing modality, targeting gaps in site-resolved PTM detection that constrain pathway interpretation in drug discovery and translational research.

- June 2025: Thermo Fisher Scientific launched Orbitrap Astral Zoom and Excedion Pro mass spectrometers to increase omics throughput and sensitivity for biopharma workflows. The launches strengthen high-throughput proteomics and phospho-proteomics capabilities that underpin cell signaling pathway mapping and biomarker verification.

- October 2024: Cell Signaling Technology launched InTraSeq Single Cell Analysis Reagents to enable simultaneous measurement of intracellular proteins and the transcriptome at the single-cell level. This product direction supports integrated multi-omic signaling readouts and reduces handoffs between protein and RNA workflows in single-cell studies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cell signaling market is defined as the revenue generated from tools and related consumables used to detect, measure, or influence cellular signaling processes in lab and applied life science workflows, including research, diagnostics, and drug discovery.

Scope exclusions: Stand-alone bioinformatics software and general cell-culture consumables that are not purpose-built for signaling assays are excluded from our totals.

Segmentation Overview

- By Signaling Type

- Endocrine Signaling

- Paracrine Signaling

- Autocrine Signaling

- Synaptic Signaling

- Juxtacrine / Gap-Junction Signaling

- By Product

- Instruments

- Flow Cytometers

- Mass Spectrometers

- Western-Blot Imaging Systems

- ELISA Readers

- Other Instruments

- Consumables

- Reagents & Kits

- Antibodies

- Media & Sera

- Other Consumables

- Instruments

- By Technology

- Flow Cytometry

- Mass Spectrometry

- Western Blotting

- ELISA

- Other Technologies

- By Pathway

- AKT / PI3K Signaling

- AMPK Signaling

- ErbB / HER Signaling

- Other Pathways

- By Application

- Drug Discovery & Development

- Cancer & Stem-Cell Research

- Immunology Research

- Diagnostics

- Other Applications

- By End User

- Pharma & Biotech Companies

- Academic & Research Institutes

- Contract Research Organizations

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- GCC

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by aligning definitions and units so the market model stays comparable across countries and end users. We reviewed public sources such as the National Institutes of Health funding databases, the World Health Organization disease burden indicators, the World Bank macroeconomic series, and the U.S. FDA public databases for approvals and safety updates that affect assay adoption.

To connect demand signals with supply context, we also used sources such as peer-reviewed journals covering signaling pathways and assay methods, patents databases to track technology activity, and trade and customs statistics where relevant for life science reagent flows. Alongside this, company annual reports, investor presentations, and reputable press helped verify product mix and commercial focus, and a paid subscription for company financials and news supported cross-checks when disclosures were limited. These desk sources are not exhaustive, and we used additional public references for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to test what we saw in public data, especially around purchasing behavior, replacement cycles for instruments, and how pricing is moving for antibodies, kits, and related reagents. Interviews and surveys covered manufacturers, distributors, and end users such as pharmaceutical and biotech labs, academic institutes, and contract research organizations, and inputs were captured across APAC, EMEA, and the Americas to avoid a single-region bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 49% |

| Mid tier: 49% | Functional/Unit leaders: 27% | EMEA: 33% |

| Smaller Players: 18% | Managers: 59% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where the demand pool is reconstructed from life science research activity and downstream usage of signaling assays, and then translated into revenue using validated pricing logic. We used market-specific inputs such as research funding intensity, oncology and chronic disease research focus, assay volume trends in key workflows (for example, western blotting, ELISA, flow cytometry, and mass spectrometry-based readouts), instrument installed base and replacement timing, and the mix shift between consumables and instruments.

After the headline totals were formed, they were checked using selective bottom-up approximations, including sampled average selling price ranges multiplied by implied usage volumes for key reagents and kits, plus channel checks on purchasing frequency and discounting behavior. Where bottom-up data was incomplete for smaller countries, gaps were handled through proxy ratios tied to lab spending, publication intensity, and regional adoption patterns, which were then reviewed with interview feedback.

For forecasting, scenario analysis was used so that growth can be stress-tested under different research funding and adoption conditions, and the final trajectory was aligned with expert consensus on how quickly newer pathway assays and more sensitive detection platforms are being adopted. When the main drivers moved in different directions, assumptions were adjusted and documented until the forward curve stayed consistent with observable demand signals.

Data Validation & Update Cycle

Validation is done through multiple checks so the final outputs do not rely on any single dataset. We compare the model results against independent signals, such as public research funding trends, published workflow adoption, and broad lab spending direction, and then we investigate any large variances before sign-off.

A second analyst review is completed to test logic, math, and the consistency of assumptions across regions, and experts are re-contacted when a number looks out of line with current buying patterns or pricing. Reports are refreshed annually, and interim updates are completed when material events occur, such as major regulatory actions or sharp changes in funding direction. Before delivery, a fresh pass is done so clients receive the latest updated view available at that time.

Mordor Intelligence's Cell Signaling Market Sizing Compared With Other Published Estimates

Published market sizes for cell signaling can look different across sources, even when the topic name sounds the same. This usually happens because the scope boundary is drawn differently, the year used as the starting point is not the same, and pricing and volume assumptions are built from different demand signals.

In this market, the biggest gap drivers tend to be whether broad cell-culture consumables are counted along with signaling-specific reagents, whether stand-alone analytics software is included, and how instruments are treated when they are used across many applications. By tracking assay-workflow adoption, refreshing pricing bands across consumables and instruments, and rechecking exclusions each update, Mordor Intelligence keeps the cell signaling total tied to signaling-purpose purchases rather than adjacent lab spending buckets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.75 B (2026) | |

| Industry Publisher A | USD 5.77 B (2024) | Uses a different base year and may apply broader inclusion across product and technology buckets, which can shift totals when instruments shared across applications are allocated more aggressively. |

| Research House B | USD 4.50 B (2024) | Starts from a lower base-year value and appears to use a wider pathway and technology framing with faster growth assumptions, while scope boundaries for adjacent lab consumables are not clearly separated. |

The table shows that the spread is mainly explained by scope edges and base-year alignment, followed by how pricing and adoption are carried forward in the forecast. When the definition is kept tight around signaling-purpose tools and consumables, and when assumptions are cross-checked with workflow and purchasing reality, the final number becomes easier to trace and repeat year after year.

Key Questions Answered in the Report

What is the projected value of the cell signaling market by 2031?

The cell signaling market is forecast to reach USD 9.57 billion by 2031.

Which region is growing fastest in the cell signaling market?

Asia-Pacific is projected to grow at a 8.12% CAGR through 2031 as China, Japan and South Korea ramp up cell-therapy infrastructure.

Which technology currently leads the cell signaling market?

Flow cytometry leads with 45.98% market share due to its ability to profile multiple cellular markers simultaneously.

Why are contract research organizations important to the cell signaling market?

CROs provide specialized analytical and manufacturing services, supporting cell-therapy firms that lack in-house capacity and driving the fastest 11.85% CAGR among end users.

What are the main restraints on cell signaling market growth?

High capital costs for advanced instruments and evolving ethical-regulatory requirements around stem-cell research are the key constraints identified.

Page last updated on: