Allogeneic Cell Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

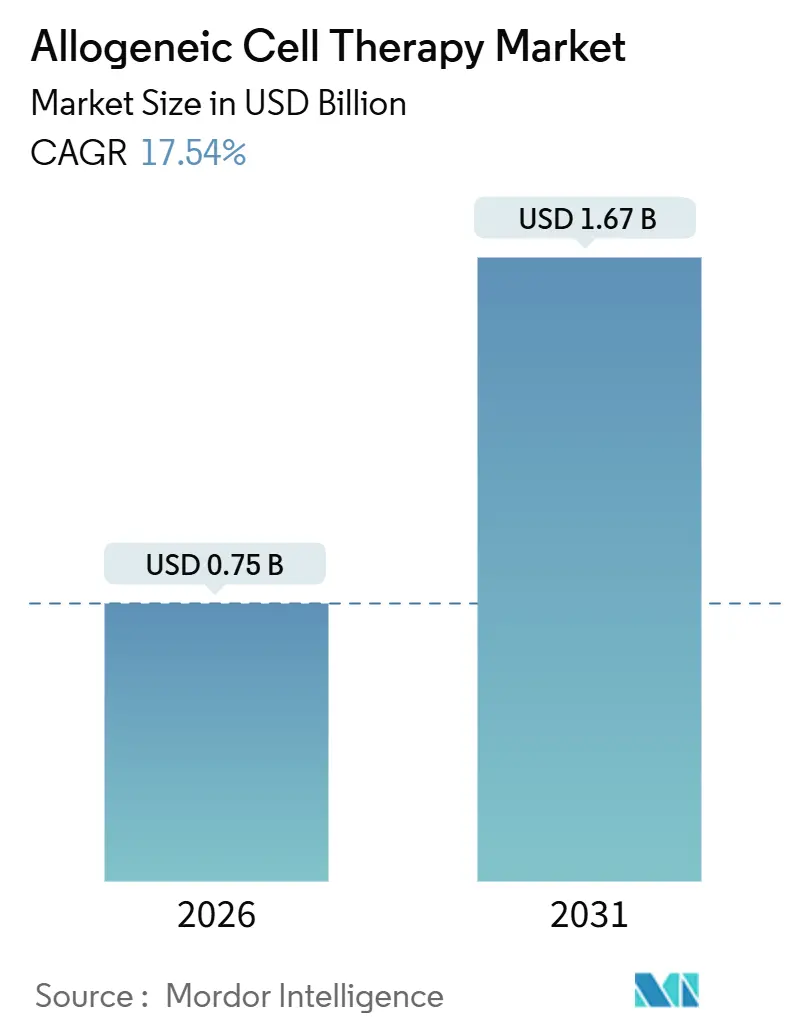

| Market Size (2026) | USD 0.75 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 17.54% CAGR |

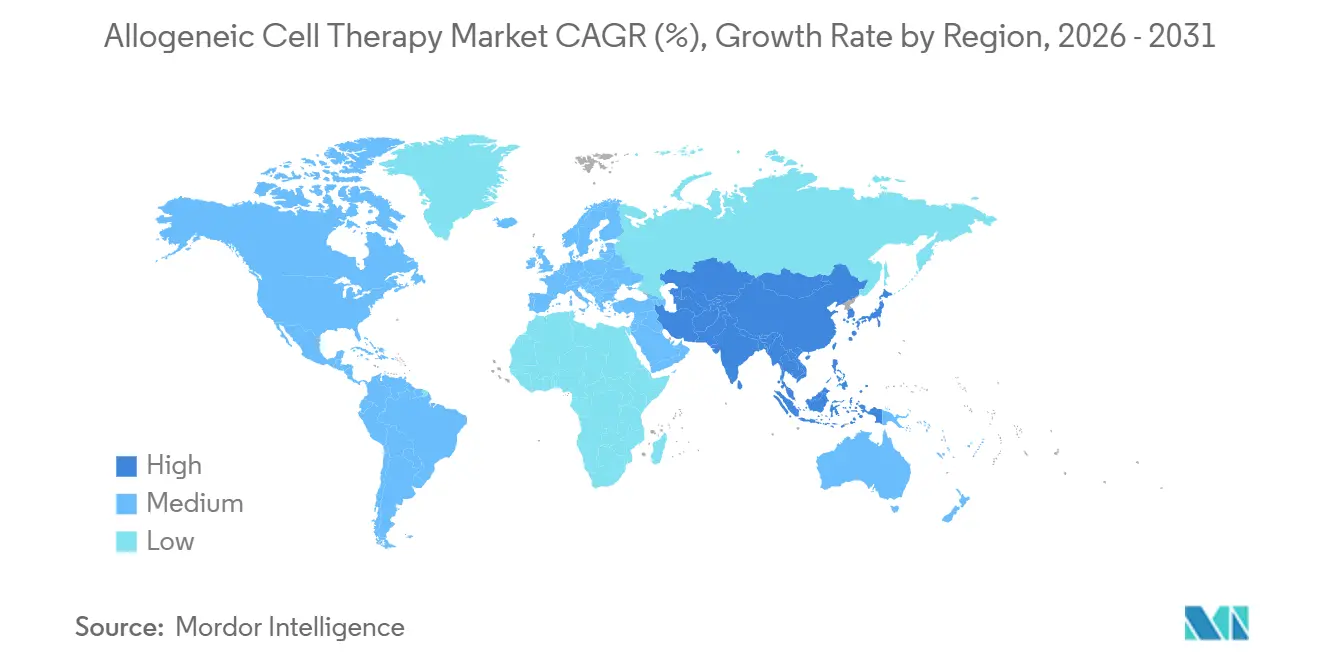

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

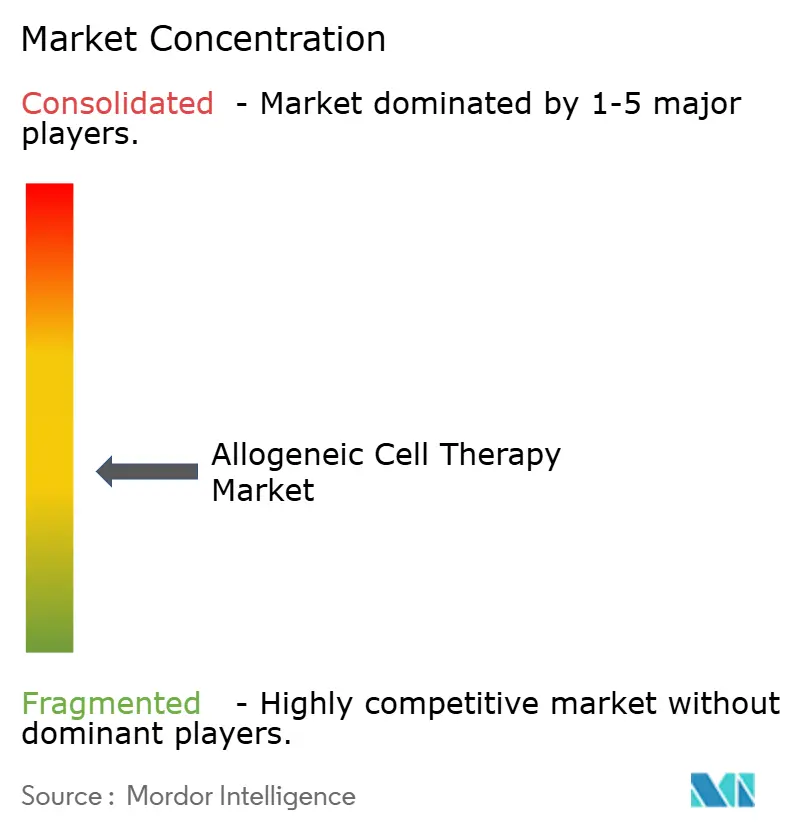

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Allogeneic Cell Therapy Market Analysis by Mordor Intelligence

The Allogeneic Cell Therapy Market size is estimated at USD 0.75 billion in 2026, and is expected to reach USD 1.67 billion by 2031, at a CAGR of 17.54% during the forecast period (2026-2031).

Rapid regulatory endorsements, strong capital inflows, and advances in gene editing are shifting allogeneic products from experimental concepts to scalable, off-the-shelf options that shorten treatment lead times and lower per-dose costs. Hospitals are broadening early access programs to include autoimmune and dermatological indications, while payers in North America and Europe are piloting outcome-based reimbursement that favors predictable batch manufacturing. Asia-Pacific is emerging as a growth engine, as China, Japan, and South Korea streamline approval processes and offer fiscal incentives to expand GMP capacity. Manufacturing automation, notably closed-system bioreactors yielding >100 doses from a single donor, is lowering the cost of goods sold and enabling smaller developers to compete in first-line oncology settings.

Key Report Takeaways

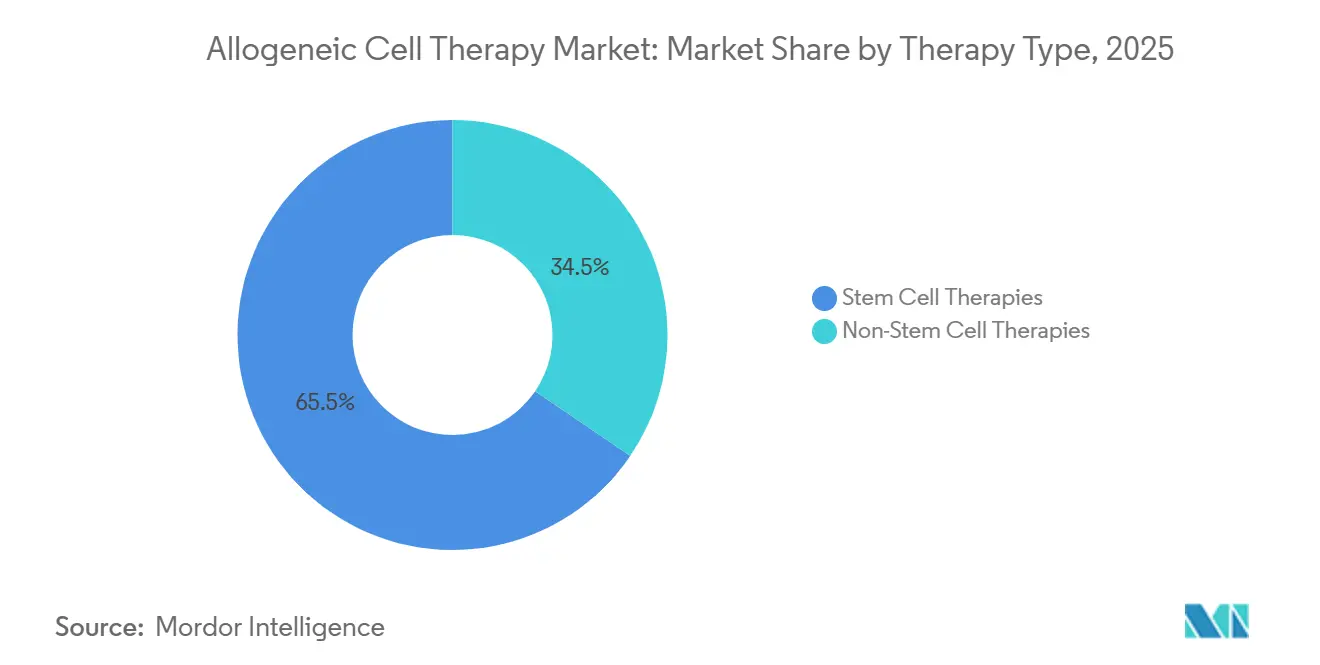

- By therapy type, stem cell therapies held 65.55% of the allogeneic cell therapy market share in 2025; non-stem cell therapies are forecast to expand at a 25.25% CAGR through 2031.

- By therapeutic area, hematological disorders accounted for 42.53% of the allogeneic cell therapy market size in 2025, while dermatological disorders are advancing at a 23.85% CAGR to 2031.

- By end user, hospitals and clinics led with 75.23% revenue share in 2025; research and academic institutes are projected to register a 21.55% CAGR between 2026 and 2031.

- By geography, North America accounted for 39.13% in 2025, whereas Asia-Pacific is forecast to grow at an 18.81% CAGR through 2031 as regional regulators adopt conditional approval frameworks.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Allogeneic Cell Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic & Rare Diseases | +3.2% | Global, acute demand in North America & Europe | Medium term (2-4 years) |

| Off-The-Shelf Scalability Cuts Lead-Time & Cost | +4.1% | Global, early adoption in US & Germany | Short term (≤ 2 years) |

| Expanding Clinical Pipeline & Strong Funding Inflows | +3.8% | North America & APAC core, spill-over to Europe | Medium term (2-4 years) |

| Favorable Expedited Regulatory Designations | +2.9% | North America & EU, emerging in Japan & China | Short term (≤ 2 years) |

| Automated Closed-System Bioreactors Enable >100-Dose Batches | +2.6% | Global, concentrated in US, Germany, South Korea | Long term (≥ 4 years) |

| MRD-Guided Early-Line Allo-CAR-T Broadens Eligible Patients | +2.3% | North America & EU, pilot programs in Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Rare Diseases

Incidence of leukemia, lymphoma, and myeloma in the United States is projected to reach 186,400 cases in 2026, up 4.2% versus 2024, while systemic lupus erythematosus diagnoses among adults aged 18-45 climbed 19% during 2020-2025[1]American Cancer Society, “Cancer Facts & Figures 2026,” cancer.org. Autologous manufacturing cannot scale quickly enough to meet this surge, as each patient-specific batch still takes weeks to produce. The allogeneic cell therapy market, therefore, offers an inventory-based solution deliverable within 48 hours, a window that can avert disease progression and costly bridging regimens[2]National Institutes of Health, “All of Us Research Program: Autoimmune Disease Trends,” nih.gov. FDA Fast-Track status for ALLO-329 in systemic lupus, granted in April 2025, further validates the demand for non-oncology use cases. Advocacy groups are pushing CMS to establish unique reimbursement codes to reflect the broader population impact and lower per-dose cost structure.

Off-the-Shelf Scalability Cuts Lead-Time & Cost

Batch manufacturing amortizes fixed expenses across hundreds of vials, driving cost of goods sold below USD 15,000 per dose in mature iPSC-NK platforms compared with USD 200,000-400,000 for autologous[3]Fate Therapeutics, “Investor Presentation: iPSC-Derived Cell Therapy Economics,” fatetherapeutics.com. A German cost-effectiveness study published by IQWiG found that allogeneic therapies priced at EUR 150,000 achieved ICERs under EUR 50,000 per QALY in large B-cell lymphoma, well inside regional willingness-to-pay thresholds. Eliminating the three-to-four-week autologous manufacturing window also reduces bridging-therapy toxicity; a review of 2024 data in Blood Advances found that 22% of autologous candidates progressed during that gap. France and Italy have begun pilot risk-sharing contracts that tie payments to 12-month progression-free survival, a model better aligned with predictable batch delivery.

Expanding Clinical Pipeline & Strong Funding Inflows

Venture and strategic investors deployed USD 2.1 billion into the space during 2024-2025, financing 127 active clinical trials as of January 2026, with 41 programs in Phase II or later. CRISPR Therapeutics’ CD19-directed CTX112 posted a 67% overall response rate in relapsed B-cell lymphoma, and Poseida’s P-BCMA-ALLO1 showed an 82% response rate in multiple myeloma. NCI awarded USD 48 million in 2025 to academic-industry consortia, while BARDA is co-funding manufacturing for infectious-disease readiness. This capital influx shortens development cycles and diversifies indications beyond oncology.

Favorable Expedited Regulatory Designations

Between January 2024 and January 2026, the FDA granted seven RMAT designations to allogeneic programs, including ALLO-316, WU-CART-007, and CTD402. RMAT provides rolling reviews and intensive CMC guidance, helping trim late-stage delays. EMA’s PRIME and Japan’s conditional approval pathway mirror this stance, while China’s NMPA now permits priority review within 200 days. Regulators increasingly view allogeneic products as strategic assets that can be rapidly deployed during public health emergencies.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High COGS & Specialized GMP-Infrastructure Needs | -2.8% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Stringent, Evolving Global CMC/GMP Regulations | -2.1% | North America & EU, tightening in APAC | Medium term (2-4 years) |

| Shrinking Cord-Blood Donor Pool Amid Lower Birth Rates | -1.6% | Global, severe in Japan, South Korea, Italy | Long term (≥ 4 years) |

| Emerging In-Vivo Gene-Editing Rivals May Cap Demand | -1.3% | North America & EU early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High COGS & Specialized GMP-Infrastructure Needs

A single GMP line processing 500-1,000 annual doses requires USD 60-80 million in upfront capital and still incurs USD 25,000-40,000 in variable costs per dose, even after scale efficiencies[4]Lonza, “GMP Manufacturing Infrastructure for Cell Therapies,” lonza.com. Contract manufacturing backlogs stretch 18-24 months, delaying trials for smaller developers. Asia-Pacific houses just a dozen FDA-compliant facilities, prompting Singapore and South Korea to cover 40% of capital costs through tax credits, though capacity remains limited.

Stringent, Evolving Global CMC/GMP Regulations

The FDA’s January 2025 draft guidance now requires potency assays that quantitatively link in vitro markers to clinical outcomes, a hurdle that adds to assay development time and requires large validation cohorts. EMA’s March 2025 reflection paper mandates surveillance for chromosomal abnormalities in gene-edited batches, extending process validation by 6-9 months. Three trials faced clinical holds in 2024-2025 due to off-target editing concerns, underscoring compliance risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Gene Editing Tilts the Balance

Stem cell modalities retained a 65.55% allogeneic cell therapy market share in 2025, but non-stem cell products are on track to grow at a 25.25% CAGR through 2031. The shift centers on CRISPR and TALEN knockouts of HLA molecules, insertion of HLA-E or CD47, and TurboCAR constructs that allow T-cells and NK-cells to evade host immune clearance. Allogene’s ALLO-316 registered a 58% objective response rate in renal cell carcinoma and secured RMAT status in late 2024, a milestone that autologous CAR-T has not achieved in solid tumors.

Gene-edited NK-cell candidates further the transition because they do not cause graft-versus-host disease and have lower rates of cytokine-release syndrome; FT596 is advancing toward pivotal trials in B-cell malignancies. Meanwhile, stem cell platforms benefit from entrenched transplant infrastructure and reimbursement codes, as illustrated by Mesoblast’s Ryoncil approval for steroid-refractory graft-versus-host disease in December 2024. Still, incremental innovation in stem cell dosing schedules cannot match the durability gains of multi-edited T-cell constructs, indicating that stem cell dominance will erode over the forecast horizon.

By Therapeutic Area: Autoimmune and Dermatological Applications Accelerate

Hematological disorders accounted for 42.53% of the allogeneic cell therapy market in 2025, supported by well-validated antigens such as CD19 and BCMA. Dermatology, however, is the fastest-growing slice, advancing at a 23.85% CAGR as allogeneic regulatory T cells advance in severe atopic dermatitis and psoriasis. Interim Phase I/II data presented in March 2025 indicated a 48% drop in EASI scores without serious adverse events.

Solid tumors lag because of hostile microenvironments, yet gene-edited constructs that incorporate dominant-negative TGF-β receptors are entering trials. Autoimmune diseases represent white space; 67 active studies are evaluating whether allogeneic CAR-T can replicate the sustained lupus remissions observed with autologous CD19 therapy. As real-world evidence accrues, payers may reallocate budgets from chronic immunosuppressants to one-time cellular interventions.

By End User: Academic Institutes Drive Indication Expansion

Hospitals and clinics contributed 75.23% of 2025 revenue, reflecting their ownership of apheresis suites, cryostorage, and intensive-care assets. Academic institutes are the fastest-growing cohort, with a 21.55% CAGR expected through 2031, powered by Moonshot-funded investigator-initiated trials in solid tumors and orphan diseases.

These centers lower entry barriers for nascent developers by providing turnkey GMP suites and regulatory expertise. The model has already delivered proofs-of-concept in relapsed T-cell leukemia, prompting Imviva to acquire University of Pennsylvania assets for pivotal expansion. Contract research organizations and cell-processing labs are expanding service menus to include donor screening, vector production, and real-time release testing, enabling developers to outsource non-core competencies.

Geography Analysis

North America accounted for 39.13% of 2025 revenue, driven by concentrated clinical-trial networks. It established reimbursement, yet growth is moderating to the mid-teens as payers implement Coverage-with-Evidence frameworks that require two-year real-world outcomes. Europe faces uneven adoption; Germany endorsed reimbursement for relapsed large B-cell lymphoma in March 2025, but France delayed coverage pending completion of Phase III trials, creating cross-border access disparities.

Asia-Pacific shows the steepest trajectory, with an 18.81% CAGR projected. China’s priority review pathway has cut dossier evaluation to 200 days, stimulating clinical-trial volume and local manufacturing investments. Japan’s April 2024 conditional approval framework already green-lighted two allogeneic CAR-T therapies for rare T-cell cancers, providing earlier revenue to fund confirmatory trials. South Korea’s January 2025 fast-track scheme offers fee deferrals and rolling CMC reviews, attracting multinational partnerships.

Emerging regions remain nascent. Brazil sanctioned its first allogeneic trial in October 2024 for COVID-19-related ARDS, and the UAE is building a cell-therapy center of excellence slated to open in 2027. Manufacturing deficits and reimbursement opacity will keep these markets below a 5% combined share through 2031.

Competitive Landscape

No company controls a significant share of the allogeneic cell therapy market, resulting in a moderately fragmented market. Legacy autologous leaders are diversifying: Gilead partnered with Shoreline Biosciences in November 2024 to co-develop iPSC-derived NK cell products, while Novartis is testing CRISPR-edited gamma delta T cells in solid tumors. Pure-play developers focus on multiplex gene-editing to differentiate; Allogene’s TurboCAR system leverages non-viral transposons to lower vector expense, whereas Poseida’s piggyBac enables site-specific integration that reduces insertional mutagenesis risk.

Manufacturing alliances are now strategic. Takeda invested USD 200 million in October 2024 to build a dedicated allogeneic facility in Osaka, offering excess capacity to partners. Contract manufacturers report multi-year order books, prompting vertical integration by cash-rich biotechs. Intellectual-property boundaries are tightening; Cellectis’ TALEN patents underpin royalty streams from Allogene and Servier, while CRISPR Therapeutics and Editas continue Cas9 litigation.

White-space persists in solid tumors and autoimmune disorders. Wugen is advancing memory-like NK constructs that show longer persistence, and Imviva’s CD7-directed CTD402 received RMAT in October 2025 after a 64.1% complete response rate, illustrating how focused assets can leapfrog broader portfolios.

Allogeneic Cell Therapy Industry Leaders

Adicet Bio, Inc.

Allogene Therapeutics Inc.

Astellas Pharma Inc.

CRISPR Therapeutics AG

Gamida Cell Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Capricor Therapeutics provided a regulatory update on its BLA submission for Deramiocel, a first-in-class therapy in Duchenne muscular dystrophy

- December 2025: CARsgen submitted two INDs to China’s NMPA for CT0596, an allogeneic BCMA-targeted CAR-T cell therapy.

Global Allogeneic Cell Therapy Market Report Scope

As per the report's scope, allogeneic cell therapy is a type of cell-based treatment that uses cells donated from a healthy individual rather than the patient. These donor cells are processed and expanded under controlled conditions and then administered to multiple recipients. The therapy is designed to repair, replace, or modulate damaged tissues or immune responses.

The allogeneic cell therapy market segmentation includes therapy type, therapeutic area, end user, and geography. By therapy type, the market is segmented into stem cell therapies and non-stem cell therapies. By therapeutic area, the market is segmented into hematological disorders, solid tumor oncology, dermatological disorders, autoimmune & inflammatory diseases, cardiovascular & ischemic conditions, and neurological disorders. By end user, the market is segmented into hospitals & clinics, specialty cancer centers, research & academic institutes, and other end users. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Stem Cell Therapies | Hematopoietic Stem Cell Therapies |

| Mesenchymal Stem Cell Therapies | |

| Non-Stem Cell Therapies | Allogeneic T-Cell Therapies |

| Allogeneic NK-Cell Therapies |

| Hematological Disorders |

| Solid Tumor Oncology |

| Dermatological Disorders |

| Autoimmune & Inflammatory Diseases |

| Cardiovascular & Ischemic Conditions |

| Neurological Disorders |

| Hospitals & Clinics |

| Specialty Cancer Centers |

| Research & Academic Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Stem Cell Therapies | Hematopoietic Stem Cell Therapies |

| Mesenchymal Stem Cell Therapies | ||

| Non-Stem Cell Therapies | Allogeneic T-Cell Therapies | |

| Allogeneic NK-Cell Therapies | ||

| By Therapeutic Area | Hematological Disorders | |

| Solid Tumor Oncology | ||

| Dermatological Disorders | ||

| Autoimmune & Inflammatory Diseases | ||

| Cardiovascular & Ischemic Conditions | ||

| Neurological Disorders | ||

| By End User | Hospitals & Clinics | |

| Specialty Cancer Centers | ||

| Research & Academic Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the allogeneic cell therapy market by 2031?

The allogeneic cell therapy market is forecast to reach USD 1.67 billion by 2031, growing at a 17.54% CAGR.

Which therapy type is expanding fastest within allogeneic cell therapy?

Non-stem cell therapies such as gene-edited T-cells and NK-cells are growing at a 25.25% CAGR through 2031.

Why is Asia-Pacific considered the fastest-growing region?

Reforms in China, Japan, and South Korea, including priority reviews and conditional approvals, are propelling an 18.81% regional CAGR.

What is the main manufacturing challenge for developers?

Building GMP lines costs USD 60-80 million and contract capacity faces 18-24-month backlogs, limiting rapid scale-up.

How are payers addressing high therapy costs?

North American and European payers are piloting outcome-based contracts that tie reimbursement to progression-free survival and real-world data.

Which companies are leading innovation?

Firms such as Allogene, CRISPR Therapeutics, and Poseida are advancing multiplex gene-edited constructs that aim to outperform legacy autologous platforms.

Page last updated on: