Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

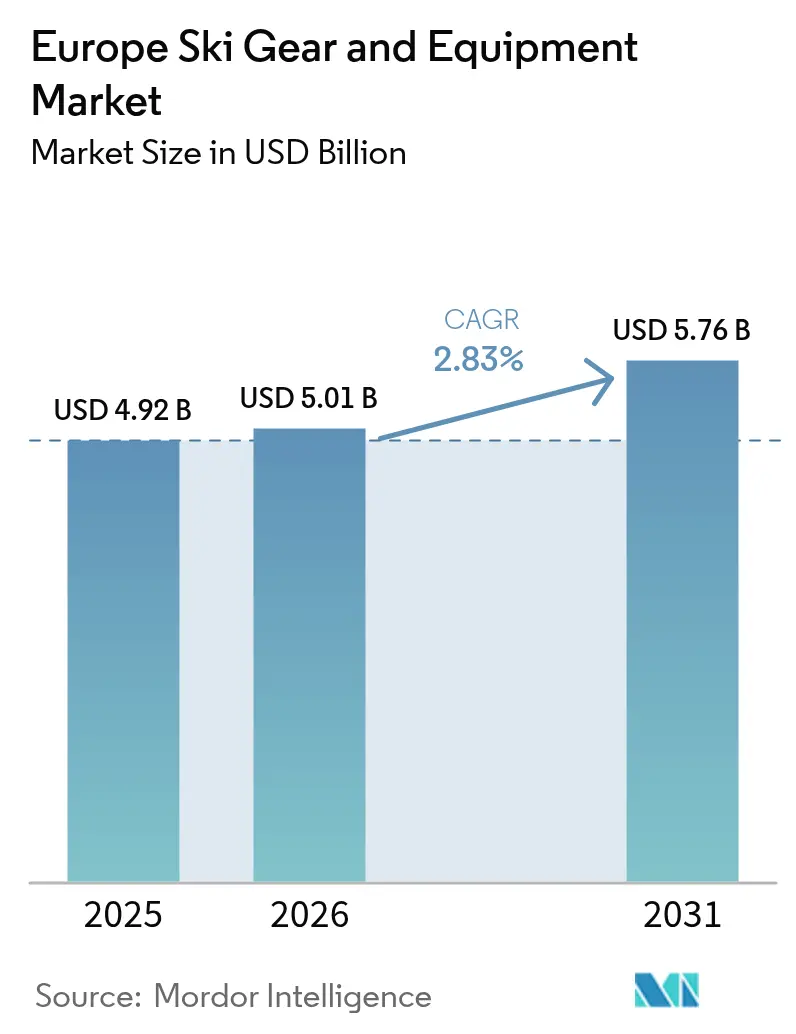

| Base Year Market Size (2025) | USD 4.92 Billion |

| Market Size (2026) | USD 5.01 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 2.83% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Ski Gear And Equipment Market Analysis by Mordor Intelligence

The Europe ski gear and equipment market size reached USD 4.92 billion in 2025, and is projected to reach USD 5.01 billion in 2026, and USD 5.76 billion by 2031, with a CAGR of 2.83% from 2026 to 2031. Consumer behavior is shifting as rental subscriptions gain popularity, reducing the emphasis on ownership. At the same time, premiumization strategies are enabling brands to maintain margins despite a plateau in total skier-days. Factors such as mandatory helmet laws, school-based youth programs, and EU sustainability regulations are driving shorter replacement cycles for protective gear and apparel. Digital commerce is addressing the advice gap through tools like virtual boot-fit applications, expanding geographic accessibility, and mitigating peak-season stock shortages. Additionally, infrastructure investments in Spain and Eastern Europe are redirecting demand from saturated Alpine regions to emerging markets with fewer altitude-related snow challenges.

Key Report Takeaways

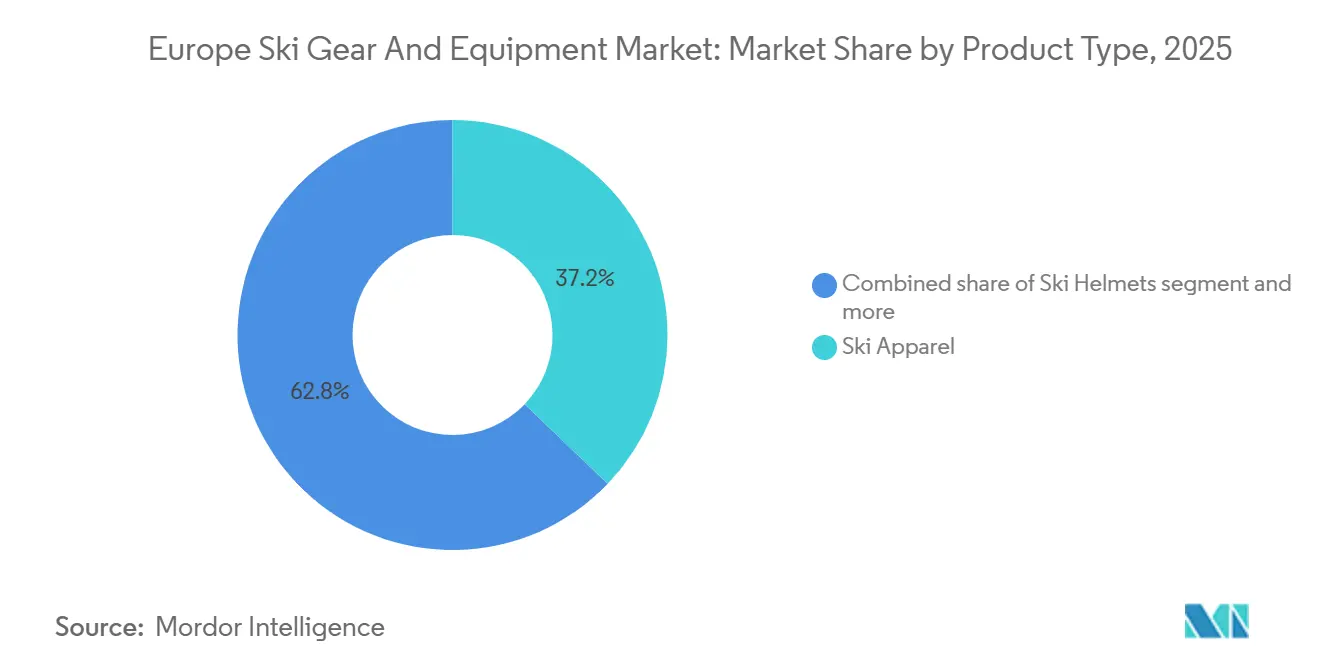

- By product type, ski apparel led with 37.17% share in 2025, while ski helmets posted the fastest 3.38% CAGR forecast for 2026-2031 across the Europe ski gear and equipment market.

- By end-user, male skiers accounted for 59.09% share in 2025, whereas the female segment is on track for a 4.56% CAGR through 2031.

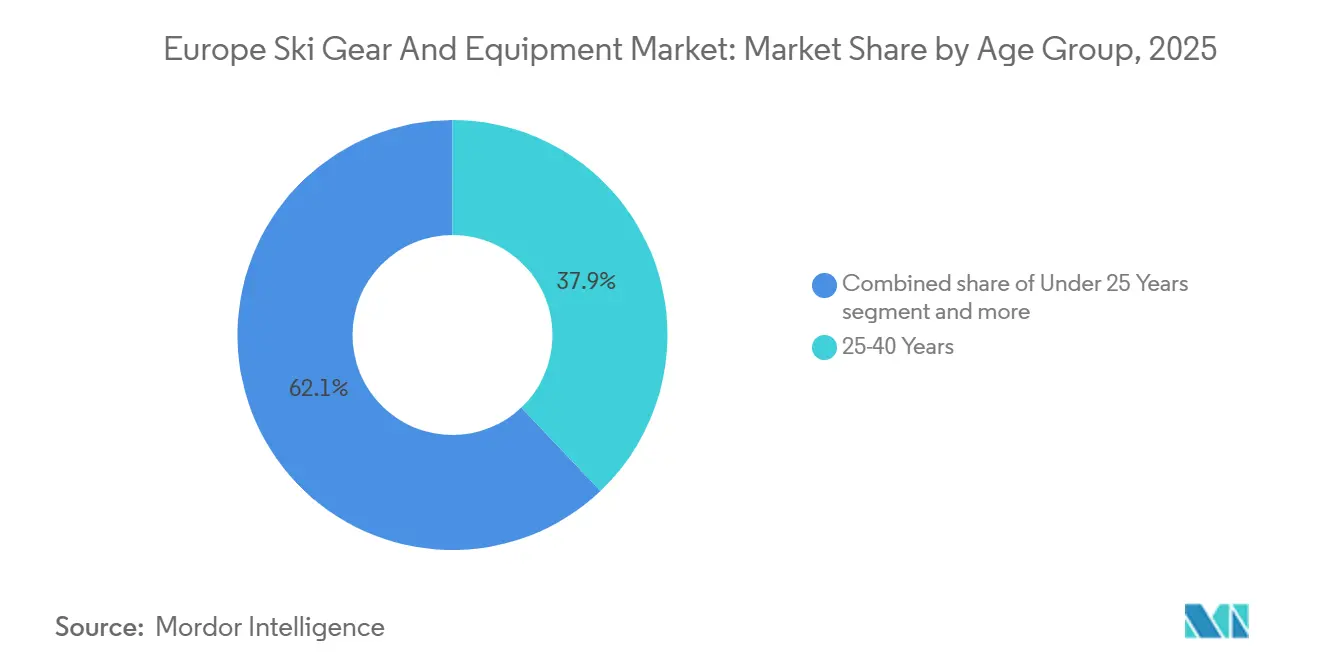

- By age group, the 25-40 years cohort captured 37.91% in 2025, yet the under-25 segment is accelerating at a 5.58% CAGR to 2031.

- By distribution, offline retail stores retained 65.15% share in 2025, but online channels are expanding at a 5.94% CAGR during 2026-2031.

- By geography, Germany held 16.87% share in 2025, while Spain shows the quickest 4.76% CAGR outlook to 2031 for the Europe ski gear and equipment market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ski Gear And Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing popularity of winter sports tourism | +0.8% | Germany, Austria, Switzerland, France, spillover to Spain and Italy | Medium term (2-4 years) |

| Expansion of ski resorts and facilities | +0.6% | Spain, Poland, Slovakia, secondary markets in Italy | Long term (≥ 4 years) |

| Rising participation in recreational skiing | +0.5% | Pan-European, concentrated in Sweden, Norway, emerging markets | Medium term (2-4 years) |

| Expansion of ski gear rental models | +0.4% | Urban centers in Germany, France, Netherlands; airport hubs | Short term (≤ 2 years) |

| Focus on sustainability and eco-friendly products | +0.3% | EU-27, led by Germany, France, Scandinavia | Long term (≥ 4 years) |

| Technological innovations in design and materials | +0.3% | Research and Development clusters in Switzerland, Austria, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing popularity of winter sports tourism

The growing popularity of winter sports tourism across Europe is a significant driver for the ski gear and equipment market. Factors such as rising disposable incomes, improved access to ski resorts, and appealing winter travel packages have contributed to increased participation in activities like skiing and snowboarding. According to the Sport England report, approximately 298,500 people in England participated in winter sports between November 2023 and November 2024, up from 290,500 in the previous period, indicating a steady increase in engagement [1]Source: Sport England, "Active Lives Adult Survey November 2023-24", sportengland.org. Similarly, major winter tourism destinations are experiencing robust growth in visitor activity. Statistics Austria reported that overnight stays in Austrian winter tourism accommodations reached 51.35 million from November 2024 to February 2025, a 1.5% rise compared to the previous year, highlighting sustained demand for winter travel experiences[2]Source: Statistics Austria, "Already 51 million overnight stays in the 2024/25 winter season", statistik.at. These developments are encouraging consumers to invest in high-quality ski gear, apparel, and accessories, not only for improved performance and safety but also to enhance their overall winter sports experience. As a result, the growth in participation and tourism is driving the continued expansion of the European ski gear and equipment market.

Expansion of ski resorts and facilities

The expansion and modernization of ski resorts across Europe are key factors driving the growth of the ski gear and equipment market. Upgraded resorts and enhanced facilities improve the skiing experience, attracting more domestic and international tourists and encouraging greater participation in winter sports. As resorts invest in advanced infrastructure, visitors are more likely to purchase high-quality ski equipment, apparel, and accessories, thereby increasing market demand. For instance, in December 2025, Spain’s Sierra Nevada ski resort allocated approximately EUR 19 million for upgrades during the winter season. These upgrades included new conveyor lifts in the Borreguiles beginner area, improved snowmaking systems, renovated on-mountain facilities, and additional snow groomers to enhance slope conditions. This investment reflects a broader trend among European ski destinations to modernize facilities, expand slope capacity, and improve visitor experiences, directly contributing to the growth of the ski gear and equipment market. Additionally, expanded resort facilities often include ski schools, rental shops, and specialized zones catering to both beginners and advanced skiers, driving demand for both entry-level and premium ski products. As resorts continue to improve accessibility and on-mountain services, the demand for high-performance, safety-oriented, and comfort-focused ski gear is expected to grow steadily across Europe.

Rising participation in recreational skiing

The increasing popularity of recreational skiing across Europe is a key driver for the ski gear and equipment market. Factors such as rising disposable incomes, greater leisure time, and improved access to ski resorts have encouraged more individuals and families to adopt skiing as a recreational activity. Demographic changes are also reshaping the participant base, with first-time skiers over the age of 30 constituting a significant share of new participants. This group demonstrates unique purchasing behavior, prioritizing safety, evidenced by helmet adoption rates nearing 100%, and favoring rentals over ownership during their initial seasons. Typically, they transition to equipment ownership after 3-4 seasons of consistent skiing. To address this segment, brands are offering bundled helmets with apparel packages, trade-in credits, and beginner-friendly kits to ease the shift from rentals to ownership. The expansion of recreational skiing is also driving demand for a broader range of products beyond traditional ski gear. Consumers are increasingly investing in high-performance apparel, technical gloves, goggles, and other accessories to enhance both comfort and safety. Furthermore, the growing number of adult beginners has led brands to emphasize ergonomic designs, adjustable equipment, and customizable options, catering to varying body types and skill levels.

Expansion of ski gear rental models

The increasing adoption of ski gear rental models across Europe is driving growth in the ski gear and equipment market. Ski resorts, specialty stores, and online platforms are offering flexible rental options, enabling consumers to access high-quality skis, snowboards, boots, and protective gear without the need for full ownership. This approach is particularly appealing to beginners, occasional skiers, and adult-onset participants who value convenience, cost-effectiveness, and safety. The expansion of rental programs is also encouraging consumers to experiment with premium or technologically advanced equipment that they might not initially purchase. This exposure to high-end products increases brand visibility and can drive future ownership. Additionally, brands and resorts are enhancing customer experiences by bundling rental packages with apparel, helmets, and accessories, creating opportunities for upselling. Rental models also promote sustainable practices by allowing multiple users to share high-quality gear, aligning with the growing consumer focus on environmental responsibility. By reducing entry barriers and providing access to a diverse range of equipment, these rental models are increasing participation in winter sports. This, in turn, is boosting demand for both rental services and eventual personal ownership, contributing to the growth of the European ski gear and equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal dependence of skiing activities | -0.5% | Pan-European, acute in low-altitude resorts (<1,500 meters) in Germany, France, Italy | Short term (≤ 2 years) |

| Intense competition from alternative winter sports | -0.3% | Urban markets in Netherlands, United Kingdom, Germany; youth demographics | Medium term (2-4 years) |

| High cost of ski gear and equipment | -0.2% | Price-sensitive markets in Southern and Eastern Europe | Short term (≤ 2 years) |

| Dependency on tourism trends | -0.2% | Tourism-dependent economies: Austria (Tyrol), Switzerland (Valais), France (Savoie) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonal dependence of skiing activities

The ski gear and equipment market in Europe is significantly impacted by the seasonal nature of skiing activities, which restricts revenue generation primarily to the winter months. This seasonal concentration limits revenue to a 16–20 week period each year, creating inventory and cash-flow challenges, particularly for independent retailers. During the off-season, demand for skis, snowboards, boots, and accessories declines sharply, resulting in underutilized inventory, higher storage costs, and the need for markdowns to clear unsold stock. This seasonality also reduces revenue predictability and complicates cash-flow management, posing difficulties for smaller retailers and new market entrants in sustaining operations throughout the year. Manufacturers and distributors face similar challenges, as production and supply planning must align with short demand periods, often requiring rapid scaling or temporary workforce adjustments. Additionally, the seasonal dependency limits opportunities for continuous customer engagement and brand loyalty, as purchasing decisions are typically confined to a few peak months. While strategies such as off-season promotions, rental models, and diversification into complementary winter sports equipment can help mitigate some of these challenges, the inherent seasonality of skiing remains a structural constraint on consistent market growth in Europe.

Intense competition from alternative winter sports

The European ski gear and equipment market is experiencing increasing competition from alternative winter sports, which are drawing consumer interest and discretionary spending. As winter sports enthusiasts explore diverse activities, traditional alpine skiing now competes with snowboarding, winter hiking, and cross-country skiing, each requiring specialized gear. Between 2020 and 2025, snowboarding participation in Europe grew at an annual rate of 4.2%, surpassing alpine skiing's 2.1% growth [3]Source: International Ski Federation, fis-ski. This trend is driven by the expansion of terrain parks and the strong appeal of snowboarding among younger consumers. The diversification of winter sports spending limits expenditure on traditional ski equipment, creating challenges for alpine skiing brands in retaining market share. The rise of alternative sports also impacts innovation and pricing strategies, as consumers evaluate the perceived value and excitement of various activities before making purchasing decisions. Retailers and manufacturers must address the evolving preferences of a younger, trend-driven demographic that may favor one activity over another. As a result, the growth of alternative winter sports serves as a structural constraint on the ski gear and equipment market, compelling brands to adapt their product offerings to remain competitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Dominates, Helmets Accelerate

Ski apparel accounted for 37.17% of market revenue in 2025, driven by its high replacement frequency and fashion-driven obsolescence cycles, which encourage repeat purchases every 2-3 seasons. The skis and poles segment, while essential, is facing commoditization pressures due to increasing rental penetration. Growth in this segment is further limited by extended replacement cycles, as recreational skiers now replace skis every 7-8 years compared to 5-6 years a decade ago. This shift is attributed to advancements in materials, such as carbon-reinforced cores and sintered bases, which enhance durability. Ski boots are benefiting from customization trends, with innovations like heat-moldable liners and 3D-printed shells improving fit.

Ski helmets are projected to grow at a CAGR of 3.38% through 2031, supported by mandatory helmet laws in Austria (introduced in 2016 for minors and extended to adults in 2024) and Italy (mandating helmet use for all ages by 2025). These regulations are driving the normalization of helmet use across various demographics. The "Others" category, which includes goggles, gloves, and accessories, is experiencing growth through the integration of smart technologies. For instance, goggles equipped with heads-up displays for speed and navigation sold 85,000 units across Europe in 2024-2025, with price points ranging from EUR 400-600 (USD 432-648).

By End-User: Female Segment Outpaces Male Growth

In 2025, the male segment accounted for a dominant 59.09% share of the European ski gear and equipment market, reflecting historically higher participation rates among men. However, the female segment is projected to grow at a notable CAGR of 4.56% through 2031, driven by targeted product development, gender-specific designs, and focused marketing efforts. Ski brands are increasingly acknowledging the purchasing power and influence of female skiers, leading to innovations such as lightweight skis, ergonomically designed boots, stylish apparel, and performance-oriented accessories tailored specifically for women. Furthermore, social media, influencer campaigns, and women-focused ski events are enhancing engagement and fostering brand loyalty among female consumers.

The maturity of the male segment has prompted brands to focus on expanding wallet share rather than participant growth. Affluent male skiers are increasingly investing in premium touring equipment, including skis with integrated climbing skins and lightweight bindings, for backcountry skiing. In contrast, the female segment presents opportunities for both participant growth and wallet share expansion, as more women are entering skiing and snowboarding through beginner programs, ski schools, and recreational packages.

By Age Group: Youth Engagement Drives Future Pipeline

The 25-to-40-year demographic segment is projected to maintain its market dominance, holding a 37.91% market share in 2025. This group exhibits significant purchasing power and established preferences for outdoor recreational activities. They display strong brand consciousness and a consistent willingness to invest in premium-quality, technologically advanced ski equipment and apparel. Their influence as market trendsetters plays a critical role in shaping product demand and driving innovation. Additionally, their participation in organized skiing expeditions and family-oriented recreational activities supports sustained demand for ski equipment.

The under-25 age demographic is expected to achieve the highest growth in the European ski gear and equipment market, with a compound annual growth rate of 5.58% through 2031. This growth is driven by increased youth participation in winter sports, supported by structured youth development programs, educational initiatives, and family-focused winter tourism offerings. This segment shows a strong preference for beginner-level equipment and modern ski gear tailored to young consumers. Market players are fostering this growth through the introduction of equipment rental services and specialized product lines. Additionally, the widespread use of digital media platforms portraying winter sports as aspirational activities further enhances youth engagement, positioning this demographic as a key driver of market growth in Europe.

By Distribution Channel: Digital Gains, Physical Endures

Offline retail stores accounted for 65.15% of the market share in 2025, driven by the tactile nature of ski equipment purchasing. Boot fitting often requires in-person try-ons, and ski selection benefits from expert consultation, which online channels find challenging to replicate. These stores excel in providing personalized shopping experiences and technical expertise, which are critical for specialized equipment purchases. Customers frequently visit specialty stores or brand-owned outlets to test products, receive professional fittings, and obtain expert guidance tailored to their skill level and skiing style. Strategically located in ski resort areas and urban sports retail centers, these stores also cater to tourists' immediate equipment needs. Additionally, they strengthen their market position by offering services such as equipment maintenance, rentals, and customization.

Online retail stores are experiencing the highest growth rate in the European ski gear and equipment market, with a CAGR of 5.94% projected through 2031. This growth is fueled by consumers' increasing preference for convenient shopping options, extensive product selections, and accessibility. E-commerce platforms offer 24/7 shopping access, competitive pricing, detailed product information, and easy comparison tools, appealing particularly to younger and urban consumers. The adoption of digital technologies, such as augmented reality (AR) for virtual fittings, user reviews, and personalized recommendations, enhances the online shopping experience. Furthermore, online retail enables brands to reach customers beyond traditional resort locations, facilitating expansion into new geographical markets.

Geography Analysis

Germany is projected to lead the European ski equipment market with a 16.87% share in 2025. This dominance is attributed to high consumer purchasing power, which supports consistent investment in quality ski gear and apparel. The country's extensive retail networks ensure widespread accessibility to equipment in both urban areas and ski resorts. Additionally, Germany's proximity to the Bavarian Alps, Austria, and Switzerland encourages regular skiing participation. The market's strength is further bolstered by active ski clubs, government support, and well-developed winter sports infrastructure.

Spain's ski equipment market is expected to grow at a compound annual growth rate (CAGR) of 4.76% through 2031. This growth is driven by rising interest in winter sports, increasing disposable incomes, and the expansion of ski tourism infrastructure. Government and tourism agencies actively promote winter sports, particularly in the Pyrenees and Sierra Nevada regions. Improved transportation networks and enhancements to ski resorts have made these areas more accessible to both domestic and international visitors. Additionally, evolving lifestyle preferences toward outdoor activities and greater health awareness among younger populations contribute to market growth.

The United Kingdom, Italy, France, the Netherlands, Switzerland, Austria, and Sweden maintain strong positions in the European ski equipment market, supported by high participation rates and established equipment preferences. France and Austria remain key Alpine destinations, offering extensive lift systems and international appeal, which drive significant rental and premium equipment sales. Switzerland continues to hold a premium market position due to its luxury resorts and advanced infrastructure. Collectively, the Europe ski-gear and equipment market is characterized by a mix of established Alpine regions and emerging high-growth areas. While traditional Alpine markets defend their value share through experience and premium pricing, the market landscape is increasingly influenced by growth in peripheral regions with rising participation and infrastructure development.

Competitive Landscape

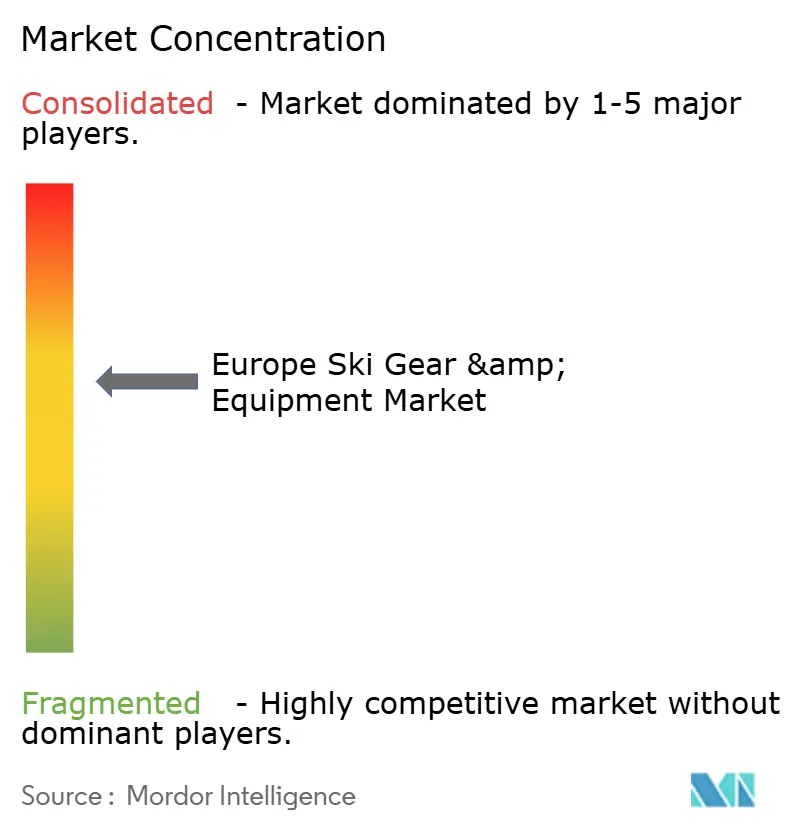

The European ski equipment market exhibits moderate concentration, with several established manufacturers holding significant market shares. Key players in the market include Amer Sports, Inc., Skis Rossignol S.A., Fischer Sports GmbH, Tecnica Group S.p.A., and Head Sport GmbH. These companies leverage their strong brand recognition and diverse product portfolios to cater to various consumer segments. Their established market presence is further supported by extensive distribution networks and partnerships with ski resorts and retailers, enabling them to maintain competitive positions. The market also witnesses consistent merger, acquisition, and collaboration activities aimed at geographical expansion and technological advancements.

The primary competitive focus among key players revolves around technological differentiation. Manufacturers invest in proprietary innovations to enhance performance, comfort, and safety features, thereby distinguishing their products in this mature market. For instance, HEAD's EMC (Energy Management Circuit) electronic dampening system exemplifies advanced technology that improves ski stability and reduces vibrations. Additionally, companies are focusing on lightweight composite materials, integrated sensors, and smart connectivity features to cater to the demands of technology-oriented consumers. These innovations not only enhance the user experience but also serve as effective tools for building brand loyalty and supporting premium pricing strategies.

The European ski equipment market offers several growth opportunities. One significant area of potential lies in adaptive equipment designed for older demographics, addressing the needs of the region's aging yet active population seeking comfortable, safe, and high-performance gear. Furthermore, the development of sustainable products using recyclable and biodegradable materials provides manufacturers with an opportunity to differentiate their offerings while complying with environmental regulations. Additionally, the integration of digital services, such as equipment tracking, maintenance notifications, and connectivity with ski resort operations, presents opportunities to enhance customer engagement and create new revenue streams.

Europe Ski Gear And Equipment Industry Leaders

-

Amer Sports, Inc.

-

Skis Rossignol S.A.

-

Fischer Sports GmbH

-

Tecnica Group S.p.A.

-

Head Sport GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Sustainability compliance and circularity are opening whitespace in product design, traceability, and end-of-life handling across Europe. Industry work on Product Environmental Footprint Category Rules (PEFCR) for winter sports, aligned with EU Product Environmental Footprint methods and moving toward European Commission recognition in 2H 2026, is pushing brands to quantify impacts consistently and to redesign material choices and construction for repair and reuse. This is visible in material and design experimentation such as Zag Skis pre-production touring prototypes using bio-based epoxy systems, alongside mainstream brand programs such as Atomic having its net-zero emissions targets validated by SBTi (January 2025) and certifying its Altenmarkt production facility to ISO 14001 (2024). As rental subscriptions grow and replacement cycles shorten for protective gear, circular product claims and measured footprints become more commercially actionable at retail and in resort-rental procurement.

Digital product identity and service layers are becoming a new battleground as the EU pushes traceability and brands seek to monetize maintenance and refurbishment. In April 2026, Salzburg Research, Atomic, and Wintersteiger presented a digital product passport demonstrator at Hannover Messe under the PASSAT initiative, highlighting a pathway for lifecycle tracking, authentication, and service records for skis. In parallel, EU-cofunded LIFE re-WINTER is building an industrial-scale circular processing model targeting 10,000 end-of-life skis, boots, and bindings sourced from rental networks, which strengthens the business case for take-back logistics, reconditioning partnerships, and secondary-market channels. Product innovation also extends to modular and repairable equipment concepts, such as ZUFOs carbon fiber exoskeleton ski boot prototype moving toward industrialization, reinforcing opportunities for brands and specialty retailers to differentiate through fit, service, and upgrade ecosystems rather than only new-unit sell-through.

Recent Industry Developments

- April 2026: Salzburg Research, Atomic, and Wintersteiger presented a digital product passport demonstrator at Hannover Messe under the PASSAT initiative, advancing lifecycle tracking, authentication, and service records for skis. The collaboration signals progress toward scalable lifecycle data integration across brands and rental networks.

- September 2025: HTI-High Technology Industries completed acquisition of HKD Snowmakers, expanding its resort technology portfolio to include advanced snowmaking capabilities, which strengthens market access for snow sports equipment suppliers.

- June 2024: Atomic achieved ISO 14001 certification for its Altenmarkt production facility, reinforcing its sustainability credentials and aligning with EU circularity objectives.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers consumer spending on ski gear and equipment sold across Europe, including core hardware and protective items that are bought, replaced, or rented for alpine and related skiing activities.

Scope exclusions: We exclude ski resort services, lift tickets, travel and lodging, ski instruction, and general winter clothing that is not made for skiing use.

Segmentation Overview

-

By Product Type

- Skis and Poles

- Ski Boots

- Ski Helmets

- Ski Apparel

- Others

-

By End-User

- Male

- Female

-

By Age Group

- Under 25 Years

- 25 to 40 Years

- 40 to 55 Years

- Above 55 Years

-

By Distribution Channel

- Offline Retail Stores

- Online Retail Stores

-

By Geography

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Switzerland

- Austria

- Sweden

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to map the demand pool and to set realistic boundaries for what counts as ski gear and equipment in Europe. We start with public signals like Eurostat household consumption and tourism-related datasets, then connect them to equipment replacement behavior and pricing direction in the region.

Sources used include public materials such as European Commission policy updates affecting consumer goods and product compliance, national statistics offices for sports participation and retail trends, and customs and trade statistics portals that track relevant goods flows. We also review company annual reports, investor presentations, and reputable trade press for brand mix, channel shifts, and promotional intensity. For specific cross checks, we use paid subscriptions for company financials and intelligence, and a patent database to understand product change cycles. This list is not exhaustive, and many other sources were referenced for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work is used to pressure test assumptions that are hard to observe in public sources, especially replacement cycles, the split of rental versus ownership, and how price points move by product category. We speak with a mix of brand-side leaders, distributors, specialty retailers, rental operators, and category managers across major European ski markets, so the model reflects both sell-in and sell-through realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | |

| Mid tier: 48% | Functional/Unit leaders: 40% | |

| Smaller Players: 21% | Managers: 44% |

Market-Sizing & Forecasting

Sizing is built using a top-down structure where Europe-level demand is reconstructed from skier participation, destination season intensity, and equipment ownership and replacement patterns, which are then translated into value using category price points. Once the demand pool is established, it is split into major gear lines like skis and poles, boots, helmets, and other protective gear and accessories, and then aligned to country mix within Europe.

To keep the totals grounded, the outputs are corroborated with selective bottom-up approximations, such as sampling average selling prices by channel, checking typical unit-to-revenue relationships for key gear lines, and validating distribution intensity through retailer and rental operator feedback. Inputs that materially move the model include resort day trends and snow reliability expectations, the share of rental subscriptions versus outright purchases, online versus specialty store mix, helmet and safety adoption rates, and premiumization in boots and protection. Forecasts use scenario analysis supported by expert views on winter conditions and discretionary spending, with annual adjustments to volumes and prices so the trajectory stays plausible even when a season runs unusually short or long.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as category growth patterns in sporting goods retail, visible shifts in channel mix, and the pace of premium price movement described by industry contacts. Where results look inconsistent, the assumptions are revisited, and follow-up outreach is triggered to confirm what changed and whether it is temporary or structural.

Before sign-off, the work goes through multi-step analyst review, including variance checks by country and by product group so any outliers are explained. Reports are refreshed annually, and interim updates are completed when material events occur, such as abnormal winter seasons or major pricing resets. Right before delivery, a fresh pass is done to ensure the latest available inputs have been applied.

Mordor Intelligence's Europe Ski Gear and Equipment Market Sizing Compared With Other Published Estimates

Published market sizes for Europe ski gear and equipment can look far apart even when everyone is analyzing a similar activity set. In practice, the spread usually comes from differences in what is counted as equipment versus apparel-like items, how rental activity is treated, and how pricing is converted and updated across countries.

In this study, the main drivers behind gaps are the timing of currency conversion, how average selling prices are progressed across product types, and whether off-season discounting is reflected in the base year. Some publishers also expand the scope into broader winter sports equipment or include more apparel content, which naturally lifts the number in a given year. A refresh-led build, where assumptions are re-validated before finalizing the base-year price and volume mix, is the check that keeps the 2025 value aligned to current season realities, which is how Mordor Intelligence arrives at USD 4.92 B.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.92 B (2025) | |

| Regional Consultancy A | USD 3.40 B (2024) | Uses a prior base year and a higher-growth projection window, and it appears to treat pricing at a more aggregated level, which can understate premium boots and protective gear value in Europe. |

| Industry Research Desk B | USD 4.28 B (2025) | Broader winter sports framing and category mapping can shift value away from ski-specific gear, and the estimate is presented at a higher level without clear checks on rental versus purchase mix by country. |

The table shows that year choice, scope boundaries, and price handling explain most of the spread rather than a single structural disagreement. By keeping the definition tight to ski gear and equipment, and by tying pricing and mix to season-timed validation, we end up with a number that is easier to trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the Europe ski gear and equipment market in 2026 and where is it headed?

It stands at USD 5.01 billion in 2026 and is projected to reach USD 5.76 billion by 2031, advancing at a 2.83% CAGR.

Which product category generates the most revenue?

Ski apparel holds the largest slice, contributing 37.17% of 2025 sales thanks to rapid style-driven replacement cycles.

What is driving helmet demand across Europe?

Austria and Italy introduced universal helmet laws in 2024-25, lifting adoption and pushing helmets toward a 3.38% CAGR through 2031.

Why is Spain considered the fastest-growing national market?

EUR 85 million in Pyrenean and Sierra Nevada upgrades extend seasons and are lifting Spain’s segment at a 4.76% CAGR.

Page last updated on: