Ice Hockey Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

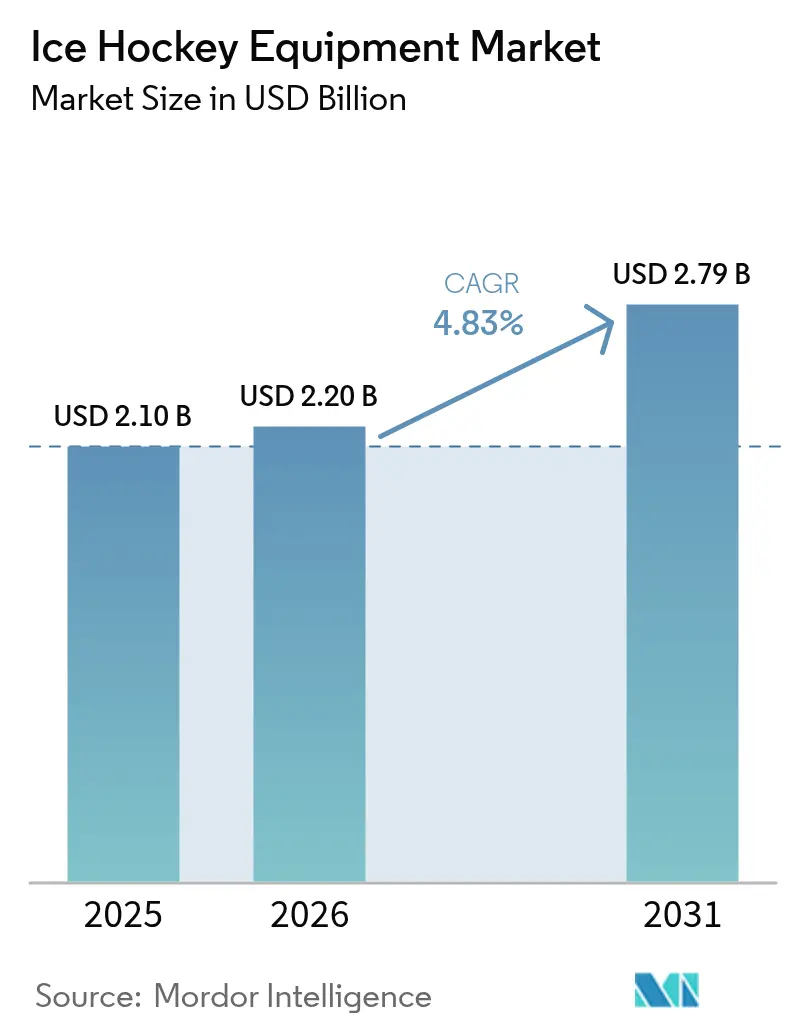

| Market Size (2026) | USD 2.20 Billion |

| Market Size (2031) | USD 2.79 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

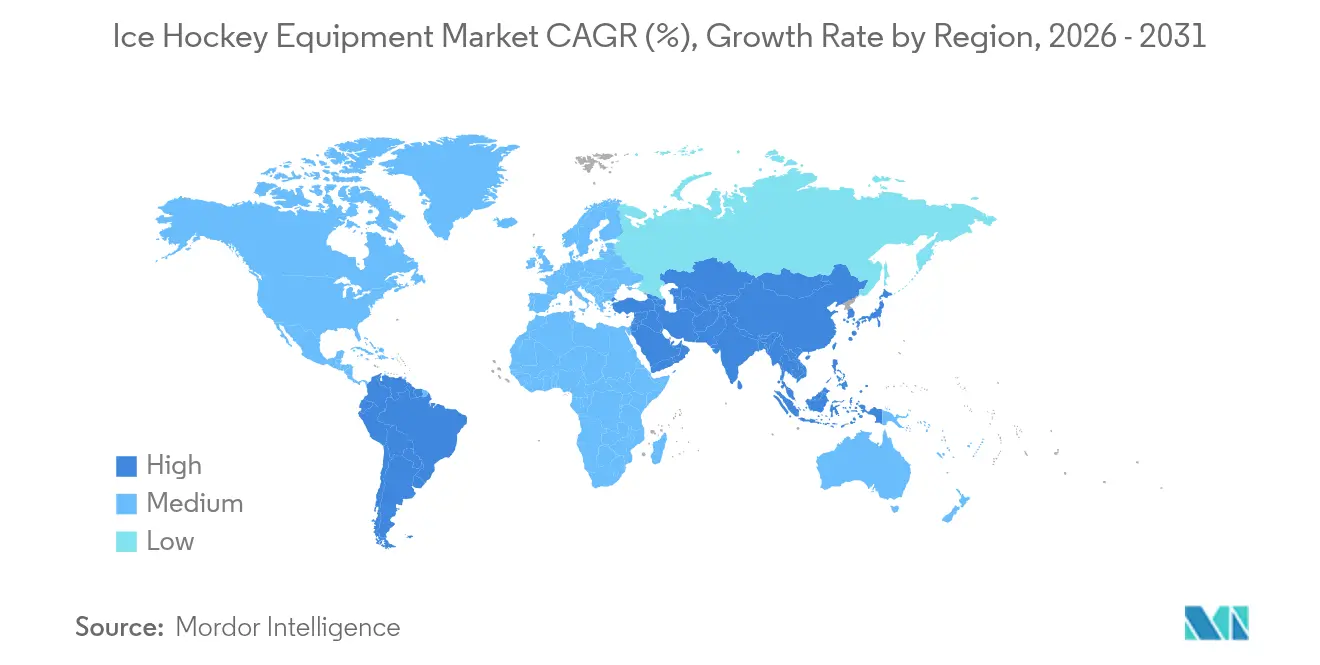

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

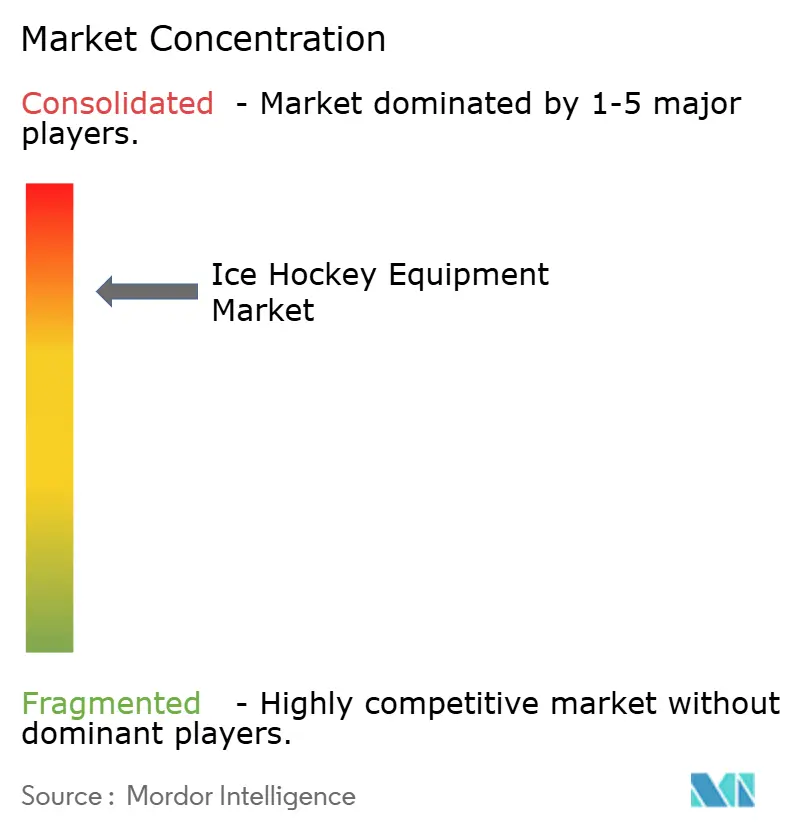

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ice Hockey Equipment Market Analysis by Mordor Intelligence

The ice hockey equipment market size is expected to increase from USD 2.10 billion in 2025 to USD 2.20 billion in 2026 and reach USD 2.79 billion by 2031, growing at a CAGR of 4.83% over 2026-2031. This growth is driven by increased global participation, expansion of professional leagues into new markets, and continuous product innovations focusing on lightweight materials and enhanced impact protection. The market received significant investment support in 2024, with private-equity funds acquiring two of the three largest manufacturers, providing capital for research, manufacturing improvements, and digital retail initiatives. Europe maintains its market dominance due to established youth development programs and IIHF safety regulations that require regular equipment replacement. The Asia-Pacific region shows the highest growth rate, supported by ice rink development in China, Japan, and Southeast Asian markets, where winter sports expenditure continues to increase. The integration of advanced materials such as carbon-fiber composites, cut-resistant fabrics, and specialized foams enables manufacturers to maintain profit margins while offering lighter equipment at premium price points.

Key Report Takeaways

- By product type, ice hockey gear and accessories led with 47.62% of the ice hockey equipment market share in 2025 and ice hockey skates are projected to expand at the fastest 5.61% CAGR between 2026-2031.

- By end user, male players accounted for 73.05% of the ice hockey equipment market size in 2025, while female participation is forecast to climb at a 5.76% CAGR to 2031.

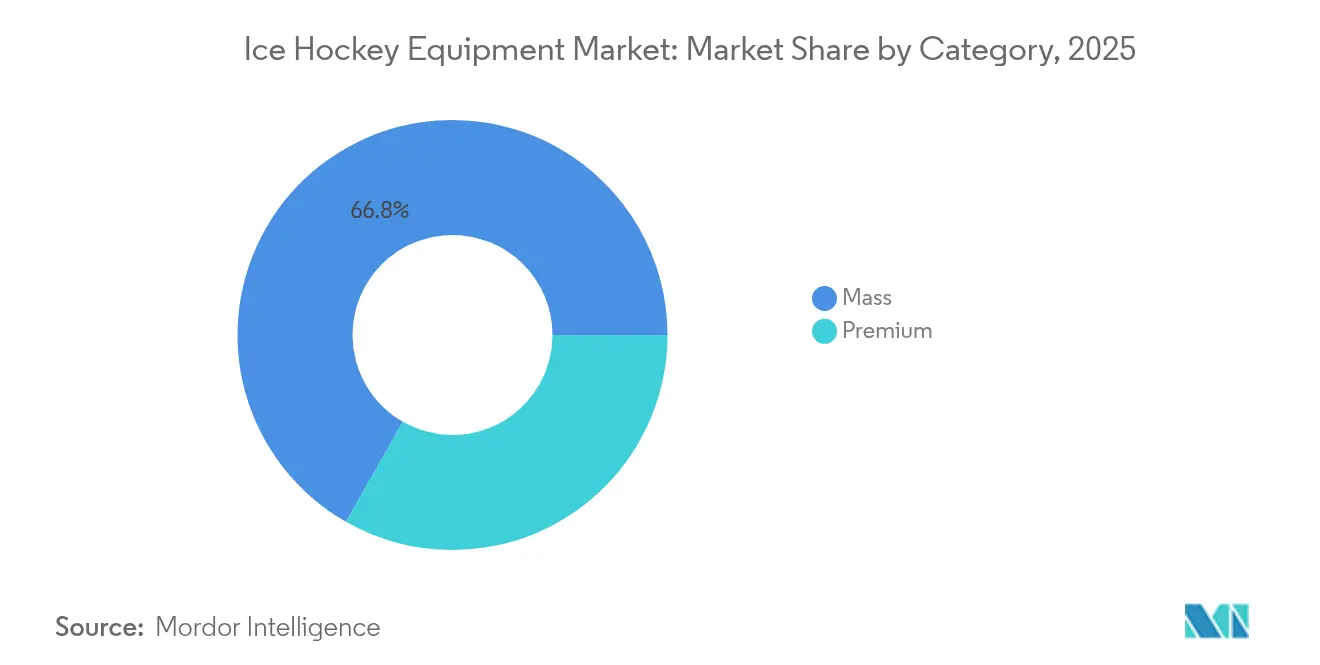

- By category, the mass segment captured 66.75% share of the ice hockey equipment market size in 2025, whereas the premium tier is pacing ahead with a 5.90% CAGR through 2031.

- By distribution channel, offline retail held 70.85% of the ice hockey equipment market share in 2025, but online outlets are accelerating at a 5.38% CAGR to 2031.

- By geography, Europe commanded 48.20% revenue in 2025; Asia-Pacific is advancing at a 6.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ice Hockey Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of ice hockey worldwide fueling demand for equipment | +1.2% | Global, with concentration in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Expansion of professional leagues and tournaments increasing visibility and sport appeal | +0.8% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Technological advancements producing lighter, more durable, and safer equipment | +1.0% | North America and Europe primarily | Short term (≤ 2 years) |

| Advances in materials like carbon fiber composites improving performance | +0.7% | Global, led by North American innovation centers | Medium term (2-4 years) |

| Product customization and variety meeting diverse consumer needs | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Influence of sports celebrities and endorsements driving equipment demand | +0.6% | Global, strongest in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Ice Hockey Worldwide Fueling Demand for Equipment

The worldwide expansion of hockey participation has generated substantial equipment demand across non-traditional markets, with the Asia-Pacific region experiencing notable growth due to improved infrastructure development. The NHL's successful international expansion strategy demonstrates this market evolution, as evidenced by capacity crowds at games in Prague and Tampere. The increasing representation of European players in the NHL, now accounting for approximately 30% of team rosters, reflects the sport's global reach. Equipment manufacturers have responded to this diversification by developing specialized product lines that address regional climate variations and distinct playing styles. The upcoming 4 Nations Face-Off tournament and the anticipated 2026 Olympic participation are expected to enhance global visibility and stimulate equipment sales across emerging markets. This growth trajectory is exemplified in markets like the Philippines, where women's hockey teams have achieved international recognition despite facing equipment accessibility challenges, highlighting the considerable untapped market opportunities in these regions.

Expansion of Professional Leagues and Tournaments Increasing Visibility and Sport Appeal

The growth of professional leagues has a significant impact on equipment demand, driven by increased media exposure and changing purchasing behaviors among amateur players. The inaugural season of the Professional Women's Hockey League (PWHL) achieved notable success, with an average attendance of 5,689 fans per game and securing over 40 sponsorship partners, including major equipment manufacturers such as Bauer. Similarly, the Utah Hockey Club's entry into the Salt Lake City market demonstrated strong results, with consistent sellout crowds and robust merchandise sales, highlighting market potential in previously untapped regions. The PWHL's planned expansion into Vancouver for the 2025-26 season at Pacific Coliseum, supported by neutral-site game attendance figures of 19,038, underscores the strategic value of geographic diversification. The increased visibility of professional hockey directly influences equipment sales, as amateur players increasingly purchase professional-grade equipment to emulate professional standards and appearances.

Technological Advancements Producing Lighter, More Durable, and Safer Equipment

Material science advancements continue to transform equipment performance in the hockey industry, as manufacturers leverage carbon fiber composites and advanced polymers to achieve significant weight reductions while ensuring robust protective capabilities. Bauer's implementation of TWITCH Taper technology demonstrates this evolution, incorporating specialized Boron fiber materials that deliver exceptional strength-to-weight ratios while enhancing energy transfer capabilities in their hockey sticks. The industry's adoption of TeXtreme Spread Tow carbon fiber fabric, initially developed for NHL goaltending equipment, has successfully bridged the gap between professional and consumer markets by providing superior balance and flexibility characteristics. The hockey equipment market has responded decisively to safety concerns, particularly with the implementation of mandatory neck laceration protection across major organizations including USA Hockey, NFHS, and AHL for the 2024-25 season. These technological developments enable manufacturers to establish premium price points while effectively addressing both evolving safety regulations and increasing performance demands from players at all levels.

Advances in Materials Like Carbon Fiber Composites Improving Performance

The integration of composite materials has fundamentally changed equipment manufacturing, allowing manufacturers to create products with exceptional combinations of strength, weight, and flexibility. Professional equipment manufacturers have successfully implemented spread tow carbon fiber technology, demonstrating how these advanced materials deliver superior performance while ensuring the durability required in professional sports. Modern manufacturing facilities now employ sophisticated processes, including automated fiber placement and resin transfer molding, which minimize production inconsistencies and provide opportunities for mass customization. These advancements in materials science create significant opportunities for premium brands to distinguish themselves in the market, while simultaneously benefiting from cost reductions through increased production volumes. The transition of these technologies from professional to amateur markets continues to accelerate as manufacturing processes become more refined, and consumers gain a better understanding of performance advantages through professional endorsements and social media influence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced equipment limiting affordability for many players | -1.5% | Global, particularly acute in developing markets | Long term (≥ 4 years) |

| Counterfeit and low-quality equipment flooding the market undermining trust | -0.8% | Global, concentrated in online channels | Medium term (2-4 years) |

| Logistics and supply chain disruptions impacting availability and prices | -0.6% | Global, with particular impact on cross-border trade | Short term (≤ 2 years) |

| Seasonal nature of ice hockey reduces steady demand across the year | -0.4% | Northern hemisphere markets primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Equipment Limiting Affordability for Many Players

The substantial financial investment required for hockey equipment presents significant participation barriers, particularly affecting youth development and market expansion in emerging economies. The considerable annual costs associated with youth hockey participation in North America, including equipment expenses, create financial strain for many families. Essential equipment like hockey sticks and comprehensive goaltender gear requires substantial financial commitment, making the sport less accessible to lower-income households. Research from the Aspen Institute highlights that a significant portion of families face challenges with youth sports participation costs, leading to a notable decline in youth sports engagement over recent years. These affordability challenges create a ripple effect throughout the industry by limiting the growth of the player base, which directly impacts equipment demand across the value chain. While premium equipment pricing enables manufacturers to invest in product innovation, it simultaneously creates market segmentation that restricts accessibility and hampers participation growth across various demographic segments.

Counterfeit and Low-Quality Equipment Flooding the Market Undermining Trust

The proliferation of counterfeit equipment threatens market integrity and creates safety risks that damage brand reputation and consumer confidence. The National Intellectual Property Rights Coordination Center's Operation Team Player seized over 94,000 counterfeit items worth USD 28.1 million between February 2023 and February 2024, demonstrating the extent of intellectual property theft in sports merchandise [1]Source: U.S. Immigration and Customs Enforcement, “Counterfeit NHL Merchandise on the Rise During 2024 Stanley Cup Final,” ice.gov. In hockey, counterfeit equipment presents significant safety risks due to the sport's physical nature and high-impact collisions, as substandard protective gear can lead to serious injuries. Online marketplaces enable counterfeit distribution by allowing anonymous sellers to reach consumers seeking lower-priced alternatives to authentic equipment. This undermining of brand integrity compels legitimate manufacturers to allocate resources toward anti-counterfeiting measures and consumer education programs, limiting funds available for product development and market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gear and Accessories Drive Market Breadth

Ice hockey gear and accessories hold a 47.62% market share in 2025, demonstrating the substantial investment required in protective equipment, helmets, and specialized accessories beyond basic playing equipment. The segment's dominant position reflects the industry's commitment to player safety, as regulations and standards require regular equipment replacement and upgrades to maintain optimal protection levels. Ice hockey skates are showing promising growth prospects, with projections indicating a 5.61% CAGR through 2031, driven by continuous improvements in blade technology and boot design that enhance player performance on the ice.

Professional athlete endorsements continue to shape consumer purchasing decisions in the market, while manufacturers invest significant resources in research and development to achieve breakthroughs in weight reduction and energy transfer capabilities. The ice hockey stick segment maintains consistent market performance, offering a range of options from premium carbon fiber composites to more affordable wood and aluminum variants, addressing diverse consumer preferences and budget considerations. The gear and accessories segment receives additional support from evolving safety regulations, particularly with the implementation of mandatory neck protection requirements across USA Hockey, NFHS, and AHL organizations in 2024-25, reinforcing the industry's focus on player safety and equipment standards.

By End User: Female Participation Accelerates Market Diversification

Male players hold a dominant 73.05% share of the hockey equipment market in 2025, reflecting the sport's historically male-focused infrastructure and participation patterns. The market landscape has been shaped by decades of investment in male-oriented facilities, training programs, and equipment development. This established ecosystem has created a self-reinforcing cycle where male participation continues to drive substantial market growth and investment decisions.

The market is experiencing a significant transformation, driven by a 5.76% CAGR in female participation through 2031. The Professional Women's Hockey League (PWHL) has played a pivotal role in this shift, with its inaugural season drawing an average of 5,689 fans per game and forming partnerships with over 40 brands. This heightened visibility has prompted increased investment in hockey equipment by female players, introducing a new dynamic to the market. In response, manufacturers are developing product lines tailored to female players, addressing their unique anatomical needs and preferences. The growing female market segment presents a notable opportunity for innovation, as traditional gear designed for male players often lacks the fit and performance required by female athletes. This focus on female-specific requirements reflects a broader evolution in the market toward more inclusive product development and distribution strategies.

By Category: Premium Segment Outpaces Mass Market Growth

The mass market equipment segment maintains its strong position with a 66.75% market share in 2025. This segment continues to attract price-sensitive consumers and entry-level players who require reliable equipment without the additional cost of advanced features. These consumers typically prioritize basic functionality and affordability in their purchasing decisions, making mass market products an essential component of the industry.

The premium segment is projected to grow at a robust CAGR of 5.90% through 2031, reflecting a notable shift in consumer preferences toward high-quality products. This growth is driven by an increasing willingness among consumers to invest in high-performance equipment that incorporates advanced technologies, such as carbon fiber composites for enhanced durability and lightweight performance, as well as improved protective materials for better safety and comfort. The influence of professional athlete endorsements further bolsters this trend, as these endorsements create aspirational value for premium products. Social media platforms also play a pivotal role in promoting these products, enabling amateur players to connect with professional standards and trends, thereby driving higher adoption rates within this segment.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline retail stores hold a 70.85% market share in 2025, as consumers prefer to evaluate equipment physically and access professional fitting services for proper sizing and performance. The technical nature of hockey equipment and safety requirements lead customers to seek in-person consultation services unavailable through online channels. Pure Hockey demonstrates the success of physical retail, with over 80 stores across 26 states and revenue of USD 332.7 million as the Official Hockey Equipment Retailer of USA Hockey. Traditional retailers benefit from immediate product availability and personalized customer service that foster customer loyalty.

Online retail stores are growing at 5.38% CAGR through 2031, supported by wider product selections, competitive prices, and enhanced logistics that improve delivery efficiency. Digital platforms effectively serve niche product segments and specialized equipment needs, particularly in regions with limited hockey retail presence. E-commerce platforms now incorporate virtual fitting tools and augmented reality features to help customers make purchase decisions remotely. The growth in online sales aligns with broader retail digitization trends and enables direct-to-consumer approaches that reduce retail markups and strengthen customer relationships.

Geography Analysis

The European hockey equipment market demonstrates substantial market leadership with a 48.20% share in 2025, underpinned by deeply embedded hockey traditions across Nordic countries, Russia, and emerging Central and Eastern European nations. This dominance is reinforced by strategic government investments in sports infrastructure, which has created a robust foundation for continuous participation growth. The region's market strength is further enhanced by well-established IIHF regulatory frameworks that maintain stringent equipment safety standards and performance consistency across national boundaries. The presence of professional leagues throughout multiple European countries generates significant visibility and equipment demand, while systematic youth development programs administered by national hockey federations ensure steady equipment replacement cycles. The recent recognition of Sweden with the IIHF Sustainability Award underscores the region's commitment to environmental considerations in equipment manufacturing and procurement decisions.

The Asia-Pacific region is experiencing remarkable growth in the hockey equipment market, recording a 6.36% CAGR through 2031. This exceptional growth trajectory is primarily attributed to substantial investments in ice rink infrastructure and increasing winter sports enthusiasm across major markets including China, Japan, Australia, and emerging economies like the Philippines. The region's expansion is characterized by significant infrastructure development and evolving cultural perspectives that position hockey as an aspirational sport, particularly among urban populations experiencing rising disposable income levels. However, the market faces notable challenges in developing regions, where complex international shipping requirements and underdeveloped local distribution networks create substantial barriers to equipment accessibility and affordability.

The North American market continues to operate as a mature yet stable segment, characterized by well-established participation patterns and comprehensive infrastructure that generates consistent demand patterns across the United States and Canada. The region confronts significant challenges related to participation affordability, particularly in youth segments, with annual participation costs reaching USD 2,583 in the United States and CAD 4,478 in Canada. Despite these constraints, the market demonstrates ongoing growth potential through professional league expansion initiatives, as evidenced by new market entries such as Salt Lake City, which typically result in notable regional increases in equipment demand.

Regulatory Landscape

Safety certification and product-performance standards shape market access for core protective categories, particularly helmets and face protection. In the United States, the Hockey Equipment Certification Council (HECC) runs third-party certification programs used across amateur hockey, aligning testing to standards such as ASTM helmet performance requirements and maintaining lists of certified models for buyer verification.

In Canada, Ice Hockey Helmet Regulations (SOR/2016-186) require helmets sold in the country to comply with the CSA Z262.1 standard, reinforcing labeling and compliance documentation throughout the supply chain. Trade-policy volatility also affects cross-border equipment flows, increasing the importance of customs documentation and classification discipline for brands and importers serving North American leagues and retail channels.

Value Chain Analysis

The ice hockey equipment value chain starts with specialized inputs, including carbon-fiber composites, advanced polymers, cut-resistant fabrics, and technical foams, which feed into component manufacturing for sticks, skates, protective gear, and helmets. High-volume manufacturing and assembly for major brands is concentrated in Asia (notably China and Taiwan) and Mexico, while a smaller set of niche or artisanal production activities remains in North America. Product compliance is embedded early in design and pre-production, with standards such as ISO 10256-1:2024 for protective equipment and certification pathways such as HECC testing for amateur-market equipment, adding cost and lead time while supporting broad market eligibility.

Brands typically route finished goods through a mix of offline specialty retailers, where fit and protection consultation support conversion, and online/direct channels that widen access in non-traditional hockey geographies. Logistics, customs, and returns management are increasingly central, particularly for cross-border North American flows where policy changes have increased shipping uncertainty and delays. Downstream, partnerships with national bodies and leagues, including USA Hockey, Hockey Canada, and CSSHL agreements referenced in the report context, influence demand planning, product validation, and replenishment cycles, while resale and re-commerce programs are emerging as an additional route to move used gear and improve affordability.

Competitive Landscape

The ice hockey equipment market exhibits significant consolidation, with industry giants Bauer Hockey and CCM Hockey maintaining their market leadership positions. The recent acquisition landscape underscores the market's robust growth potential, as demonstrated by Altor Fund VI's strategic purchase of CCM Hockey, valued at over EUR 300 million in annual turnover, and Fairfax Financial's acquisition of Bauer Hockey. These strategic moves have created substantial operational synergies, enabling the companies to optimize their manufacturing processes, expand their distribution networks, and enhance their research and development capabilities. The consolidation has also positioned these companies to better serve diverse geographic markets while achieving significant cost efficiencies across their product portfolios.

Market differentiation strategies have evolved beyond traditional product offerings, with companies now focusing on advanced technological innovations, strategic professional player endorsements, and rigorous safety compliance measures. Bauer's collaboration with Hockey Canada and CCM's partnership with USA Hockey exemplify how major players establish market credibility and strengthen their presence. In the evolving market landscape, specialized manufacturers have identified valuable opportunities in underserved segments, particularly in women's equipment and emerging international markets. Sherwood Hockey's success through partnerships with prominent athletes like Connor Bedard and William Nylander demonstrates the effectiveness of strategic endorsements and community engagement in building market share.

The competitive environment continues to transform in response to regulatory developments, particularly the implementation of mandatory neck protection requirements. These regulatory changes have created immediate market opportunities for manufacturers offering compliant equipment while potentially challenging companies with limited safety-focused product lines. The increasing influence of Hockey Equipment Certification Council (HECC) standards has become a crucial factor in market access, as safety certifications now represent an essential requirement across major jurisdictions [3]Source: Hockey Equipment Certification Council, “About Product Certification Testing,” hecc.org. This regulatory framework has fundamentally altered the competitive dynamics, making safety compliance a key determinant of market success.

Ice Hockey Equipment Industry Leaders

Bauer Hockey LLC

CCM Hockey

New Balance Inc.

True Temper Sports Inc.

Sher-wood Hockey Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-driven replacement and safety upgrades continue to create clear whitespace in protective gear, with mandatory cut-resistant neck laceration protection adopted across bodies such as USA Hockey, NFHS, and the AHL for the 2024-25 season. This has lifted demand for compliant accessories and protective systems that can be bundled with helmets, shoulder protection, and base layers, while increasing the commercial value of certification, labeling, and retail education for both offline fitters and online platforms.

Women-specific equipment and inclusive product positioning are also becoming a tangible differentiator as participation diversifies and new leagues add visibility. In 2026, CCM expanded female-oriented merchandising with the Barbie x CCM Collection, while supplier relationships with governing bodies and development leagues, including Bauer with Hockey Canada through the 2033-34 season and CCM with CSSHL, provide structured channels to introduce new fits, materials, and protective concepts. Innovation partnerships that connect brands with materials and prototyping ecosystems support product-line refreshes in premium protection, including Bauer participation in Carnegie Mellon University and Covestro-supported Rethink the Rink work on goalie chest protection prototypes in 2026.

Recent Industry Developments

- June 2026: TRUE Hockey entered an exclusive long-term partnership with Pro’s Choice to integrate premium goalie mask technology into TRUE’s equipment lineup. This move strengthens TRUE’s position in high-end goaltending protection, where performance credibility and safety features influence purchase decisions across competitive levels.

- June 2025: Seven7 partnered with Altor to invest in a minority stake in CCM Hockey, adding athlete-backed expertise alongside institutional capital. The investment supports CCM’s product development and commercialization efforts while reinforcing ongoing consolidation among leading equipment brands.

- December 2024: CCM Hockey announced a multi-year partnership with USA Hockey to supply equipment for national teams, spanning helmets, gloves, sticks, skates, and protective gear. Official-supplier status provides high-visibility validation in the United States and tightens CCM’s linkage to elite-level performance and safety expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from equipment used to play ice hockey and protect players during training and matches, counted in USD across the full value of equipment sold through offline and online channels.

Scope exclusions: Field and street hockey gear, as well as general winter sports accessories not designed for ice hockey, are excluded from this market.

Segmentation Overview

- By Product Type

- Ice Hockey Skates

- Ice Hockey Sticks

- Ice Hockey Gear and Accessories

- By End User

- Male

- Female

- By Category

- Mass

- Premium

- By Distribution Channel

- Offline Retail Stores

- Online Retail Stores

- By Geography

- North America

- United States

- Canada

- Rest of North America

- Europe

- Russia

- Finland

- Sweden

- Czech Republic

- Switzerland

- Germany

- France

- United Kingdom

- Rest of Europe

- Asia-Pacific

- China

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Middle East and Africa

- South America

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work is where we map the initial demand and supply picture before assumptions are tested. We rely on public participation signals and trade flows from sources such as national sports agencies, customs and trade statistics portals, the International Ice Hockey Federation website for rules and safety direction, and peer reviewed sports medicine and injury prevention journals that inform protective gear adoption. For context on retail and pricing direction, we also review company annual reports, investor presentations, product catalogs, and reputable press coverage around new launches and recalls.

To avoid over relying on any single data point, the desk inputs are cross checked against company financials and intelligence subscriptions, plus a patent database that helps spot product cycles (materials, helmet designs, composites) that can affect replacement timing and pricing. These sources help set starting points for addressable demand by region and for typical product mix splits, which are then stress tested with interview feedback. The desk sources listed above are illustrative only, and many other public documents and datasets were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what portion of athletes actually buy each equipment type, how often replacement happens, and how pricing moves between mass and premium categories. We spoke with manufacturers, distributors, specialty retailers, and rink linked stakeholders across major ice hockey countries, then used their inputs to tighten adoption rates, channel mix, and realistic price bands by region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | APAC: 47% |

| Mid tier: 56% | Functional/Unit leaders: 33% | EMEA: 35% |

| Smaller Players: 16% | Managers: 51% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where participation, registered player pools, and rink and league activity are translated into an equipment demand pool by region, then converted to value using typical replacement cycles and price tiers. To make this practical, we use inputs such as participation growth by age and gender, replacement frequency for skates and sticks, protective gear compliance and safety driven upgrades, premiumization trends that shift average selling price, and the offline to online channel mix that changes realized pricing.

Once the totals are formed, they are corroborated with selective bottom-up checks, including sampled product line ASPs multiplied by estimated unit volumes, retailer channel checks on fast moving categories, and supplier side sanity checks on regional splits. When product level volume is not fully visible, gaps are handled by applying interview validated mix shares and by keeping replacement assumptions conservative for low visibility segments. Forecasting is run using scenario analysis supported by a light multivariate regression, where the main drivers are participation, disposable income proxies, and the pace of premium category take up, and the final curve is adjusted only when it stays consistent with what field respondents expect for their near term order books.

Data Validation & Update Cycle

Validation is done through multiple passes so the model stays consistent with real world signals. Outputs are compared against independent indicators such as participation direction, regional retail momentum, and observed price movements, then the biggest variances are traced back to a specific input like replacement rate or channel mix before sign off. If a swing is driven by a one time event such as a regulation change, a recall, or a sudden demand jump around major tournaments, we re contact the relevant respondents to confirm the magnitude.

Each report is refreshed annually, and interim updates are made when a material event can shift the demand pool or pricing. Before delivery, a final review is completed so the latest public data and interview learnings are reflected in the market totals and the forecast trend.

Mordor Intelligence's Ice Hockey Equipment Market Estimate Compared With Other Published Estimates

Published market values for ice hockey equipment can look different across sources because each one draws the line around products, price tiers, and the timing of currency and inflation updates in its own way. Differences also come from how participation is translated into buying behavior, especially for replacement led items like sticks and skates.

Street hockey and field hockey gear sit outside Mordor Intelligence's scope, and that single exclusion can materially change totals in sources that treat hockey equipment as one blended category across surfaces. Gaps also show up when one estimate anchors pricing mainly to premium catalogs, when another assumes a faster online shift that lifts ASPs, or when the base year is set in a high promotion period without normalizing discounting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.10 B (2025) | |

| Global Research Publisher A | USD 2.30 B (2024) | Uses a 2024 base year and appears to lean on category pricing that can overweight premium products, and the scope language is less explicit on excluding adjacent hockey types. |

| Industry Research Publisher B | USD 2.02 B (2024) | Lower total is consistent with more conservative growth and pricing progression assumptions, and a shorter forecast window that reduces the effect of premiumization and replacement upgrades. |

The spread across published numbers is mainly explained by product scope boundaries, base year timing, and how ASP movement is handled across mass versus premium equipment. By keeping the demand pool tied to participation and replacement patterns and then checking results with channel and price reality checks, the totals stay traceable to simple inputs that can be reviewed and repeated.

Key Questions Answered in the Report

What is the global value of ice hockey equipment in 2026?

The ice hockey equipment market size is USD 2.2 billion in 2026.

Which region is growing fastest through 2031?

Asia-Pacific leads with a 6.36% CAGR on the strength of new rink construction and rising winter-sports interest.

What product segment posts the highest growth?

Ice hockey skates are forecast to expand at a 5.61% CAGR from 2026-2031.

How does private equity influence competition?

Acquisitions of Bauer and CCM by Fairfax and Altor inject capital for R&D, widen distribution, and intensify consolidation.

Why are neck guards suddenly important?

USA Hockey, NFHS, and the AHL made cut-resistant protection mandatory in 2024-25, creating immediate demand for compliant gear.

Page last updated on: