Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Hydrophobic Coatings Market Report is Segmented by Product Type (Anti-Corrosion, Anti-Microbial, Anti-Fouling, Anti-Wetting, and More), Substrate (Metals, Ceramics, Glass, Concrete, and More), End-User Industry (Construction, Automotive, Aerospace, Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

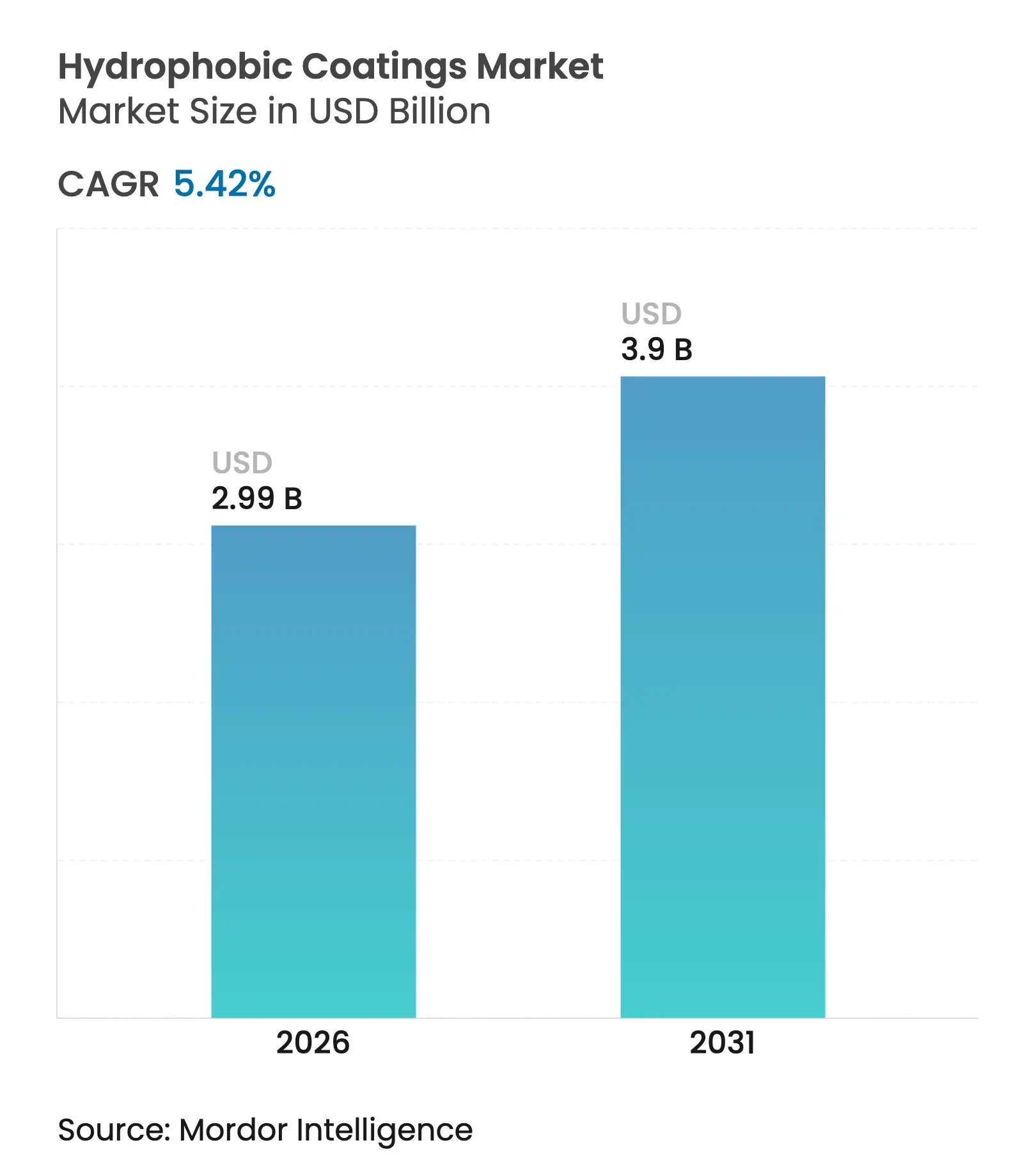

| Market Size (2026) | USD 2.99 Billion |

| Market Size (2031) | USD 3.9 Billion |

| Growth Rate (2026 - 2031) | 5.42 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Hydrophobic Coatings Market size is expected to grow from USD 2.84 billion in 2025 to USD 2.99 billion in 2026 and is forecast to reach USD 3.9 billion by 2031 at 5.42% CAGR over 2026-2031. Regulatory pressure has accelerated the transition toward fluorine-free chemistries, while sustained infrastructure investment, electronics miniaturization, and growing healthcare demand collectively reinforce volume growth. Technology differentiation now centers on silicone-, bio-based, and nanostructured solutions that match or exceed legacy fluoropolymer performance. Large buyers are prioritizing multifunctional products that combine water-repellency with anti-corrosion, antimicrobial, and anti-icing attributes, a trend that favors suppliers with broad formulation expertise. Competitive intensity is moderate as global chemical majors defend share against agile nanocoating specialists through divestment, strategic partnerships, and rapid patent filings.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Robust growth of construction sector Robust growth of construction sector | +1.80% | Global, with APAC leading at 13.4% growth | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.80% | Geographic Relevance:Global, with APAC leading at 13.4% growth | Impact Timeline:Long term (≥ 4 years) |

Rising demand from automotive industry Rising demand from automotive industry | +1.20% | Global, concentrated in APAC and North America | Medium term (2-4 years) | |||

Increasing adoption in consumer electronics Increasing adoption in consumer electronics | +1.00% | Global, with Asia-Pacific manufacturing hubs | Short term (≤ 2 years) | |||

3-D printed retro-fit superhydrophobic surfaces 3-D printed retro-fit superhydrophobic surfaces | +0.80% | North America and Europe early adoption | Medium term (2-4 years) | |||

Increasing demand for anti-viral public-infrastructure coatings Increasing demand for anti-viral public-infrastructure coatings | +0.70% | Global, post-pandemic acceleration | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Robust Growth of Construction Sector

Sustained urbanization and infrastructure renewal continue to anchor demand in the hydrophobic coatings market. Silane- and siloxane-based concrete impregnation has become standard for chloride-ion protection of bridges, tunnels, and coastal structures, extending service life and lowering maintenance costs. Alignment with green-building certifications positions bio-based hydrophobic treatments as preferred solutions for public projects that emphasize sustainability. Asia-Pacific smart-city programs are amplifying volumes by specifying water-repellent barriers against climate-induced deterioration. The construction segment’s 29.64% 2024 revenue share reflects the indispensability of protective coatings in large civil works, where asset longevity directly influences national infrastructure budgets.

Rising Demand from Automotive Industry

Automotive manufacturers have shifted toward hydrophobic multifunctional coatings that deliver paint protection, self-cleaning, and anti-corrosion benefits. Self-healing nanocomposites improve finish durability, an attribute valued by luxury car brands keen on residual-value preservation. Electrification adds new protection points as battery enclosures and power-electronics housings must resist moisture ingress and thermal cycling. Regulatory caps on VOC emissions accelerate water-borne hydrophobic chemistries, pressing suppliers to replicate solvent-based performance without sacrificing throughput. Integration of advanced driver-assistance sensors and infotainment displays further widens opportunities for ultra-thin, optically clear waterproof layers inside vehicles.

Increasing Adoption in Consumer Electronics

The hydrophobic coatings market is capitalizing on OEM demand for device waterproofing that is invisible to end-users. Nanoscale barrier layers now achieve IPX8 ratings without augmenting device weight or impeding thermal dissipation. Wearables, hearables, and IoT modules require moisture resistance that safeguards miniature sensors and micro-batteries, prompting contract manufacturers across China, South Korea, and Vietnam to qualify new fluorine-free solutions. With 5G chipsets operating at higher power densities, condensation prevention on printed circuit boards has become critical, driving adoption of vapor-phase nanocoatings that maintain electrical continuity while repelling liquid water.

3-D Printed Retro-fit Superhydrophobic Surfaces

Additive manufacturing unlocks customized surface architectures that enhance hydrophobicity beyond the capabilities of conventional spray or dip-coat lines. Research shows 3-D printed porous structures achieving 88.6% oil-water separation efficiency, indicating scalable industrial wastewater applications. Aerospace engineers are experimenting with printed anti-icing panels that integrate resistive heaters and hierarchical textures, cutting de-icing power consumption while improving flight safety. The retrofit potential stands out: operators can attach printed inserts onto existing equipment, upgrading surface performance without full replacement, an attractive proposition for resource-constrained infrastructure owners in Europe and North America.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Complex process and high initial investment cost Complex process and high initial investment cost | -1.50% | Global, particularly affecting SMEs | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.50% | Geographic Relevance:Global, particularly affecting SMEs | Impact Timeline:Medium term (2-4 years) |

Durability challenges under abrasive environments Durability challenges under abrasive environments | -1.20% | Industrial applications globally | Long term (≥ 4 years) | |||

Impending bans on long-chain fluoropolymers Impending bans on long-chain fluoropolymers | -0.80% | Europe and North America leading | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Complex Process and High Initial Investment Cost

Producing superhydrophobic layers demands precise control of surface roughness and chemistry, often involving multi-step texturing, functionalization, and curing in inert atmospheres. Capital expenditure on plasma reactors, laser patterning units, and sophisticated QC instrumentation strains the finances of small and mid-size enterprises. Down-line users also face learning curves: substrate cleaning, ambient humidity, and cure profiles must all be optimized to achieve published contact-angle specifications. These complexities restrict the pace at which new entrants can scale, limiting market competition and potentially slowing innovation diffusion in cost-sensitive end-use sectors.

Durability Challenges Under Abrasive Environments

Repeated mechanical wear, UV irradiation, and chemical attack erode superhydrophobic features, causing contact angles to drop below 90° and negating water-repellent benefits[1]Nature Communications Editors, “Durability of Superhydrophobic Surfaces,” nature.com . In maritime settings, salt spray and impact from floating debris accelerate failure, necessitating frequent reapplication that raises lifecycle costs. Aerospace components face dual stresses: thermal cycling from altitude shifts and abrasive forces during de-icing. Although self-healing polymers show promise, they remain at prototype stage and command price premiums that deter widespread adoption. The longevity gap relative to traditional epoxy and polyurethane coatings remains a critical hurdle.

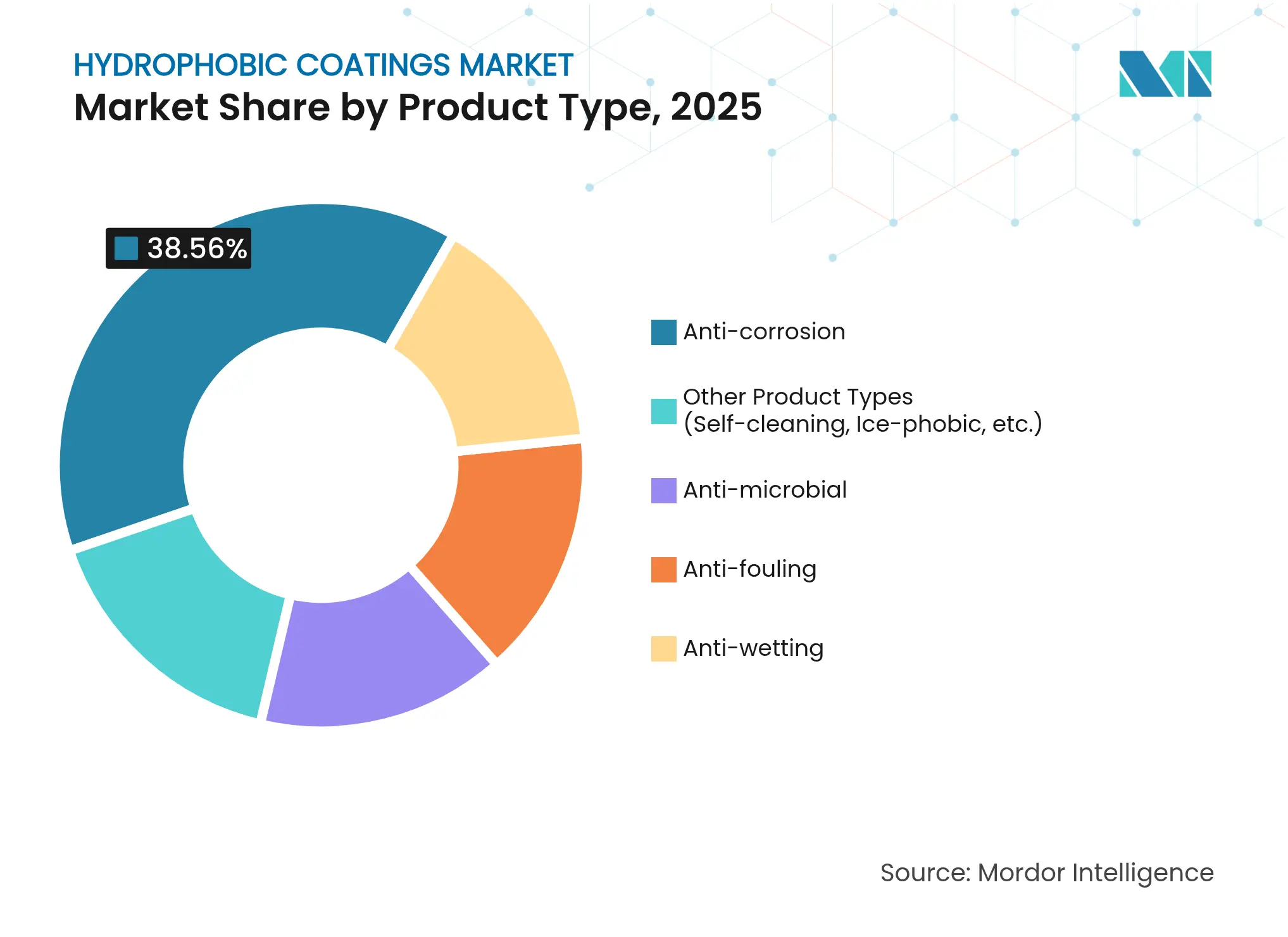

By Product Type: Anti-Corrosion Dominance Faces Specialty Challenge

Anti-corrosion formulations maintained a 38.56% hydrophobic coatings market share in 2025, reflecting the perennial need to safeguard steel and aluminum assets in marine, oil-and-gas, and transport sectors. Robust demand from bridge refurbishment and offshore wind installation projects further anchored segment revenues. In contrast, self-cleaning and ice-phobic products within the “Other Product Types” cluster are forecast to post a 6.64% CAGR, buoyed by solar O&M firms that have validated up to 15% energy-yield gains after applying nanocoatings to PV modules. Aerospace OEMs likewise value low-ice-adhesion surfaces that cut anti-icing fluid usage.

The anti-corrosion sub-sector remains price competitive, yet regulatory pressure on zinc-rich primers and solvent-borne top-coats is shifting procurement toward water-borne hybrids with embedded graphene or ceramic flakes. Specialty self-cleaning products command higher margins due to their ability to reduce manual cleaning labor for solar farms located in arid regions. Meanwhile, the hydrophobic coatings industry is witnessing the emergence of photothermal ice-phobic layers that combine passive water repellence with active sunlight-driven heating, a hybrid approach that resonates with airlines pursuing fuel-saving de-icing strategies.

Note: Segment shares of all individual segments available upon report purchase

By Substrate: Metals Leadership Challenged by Emerging Applications

Metals held 42.74% of the hydrophobic coatings market size in 2025, underpinned by global infrastructure spend and automotive build-rates. Steel bridges, aluminum body panels, and pipeline networks all rely on hydrophobic barrier technology to slow pitting and chloride attack. Laser shock peening and cold-spray technologies now create textured metallic surfaces with contact angles above 130°, enabling synergy between surface topography and chemical coatings.

Growth, however, is shifting toward textiles, paper, and other bio-derived substrates, which together are projected to log a 6.76% CAGR through 2031. PFAS-free durable water-repellent finishes on performance apparel align with brand sustainability commitments, while compostable food-service containers increasingly specify water-repellent cellulose coatings for grease resistance. The hydrophobic coatings market is thus broadening its customer base beyond heavy industry toward consumer-facing brands that prize end-of-life recyclability and lower toxicological footprints.

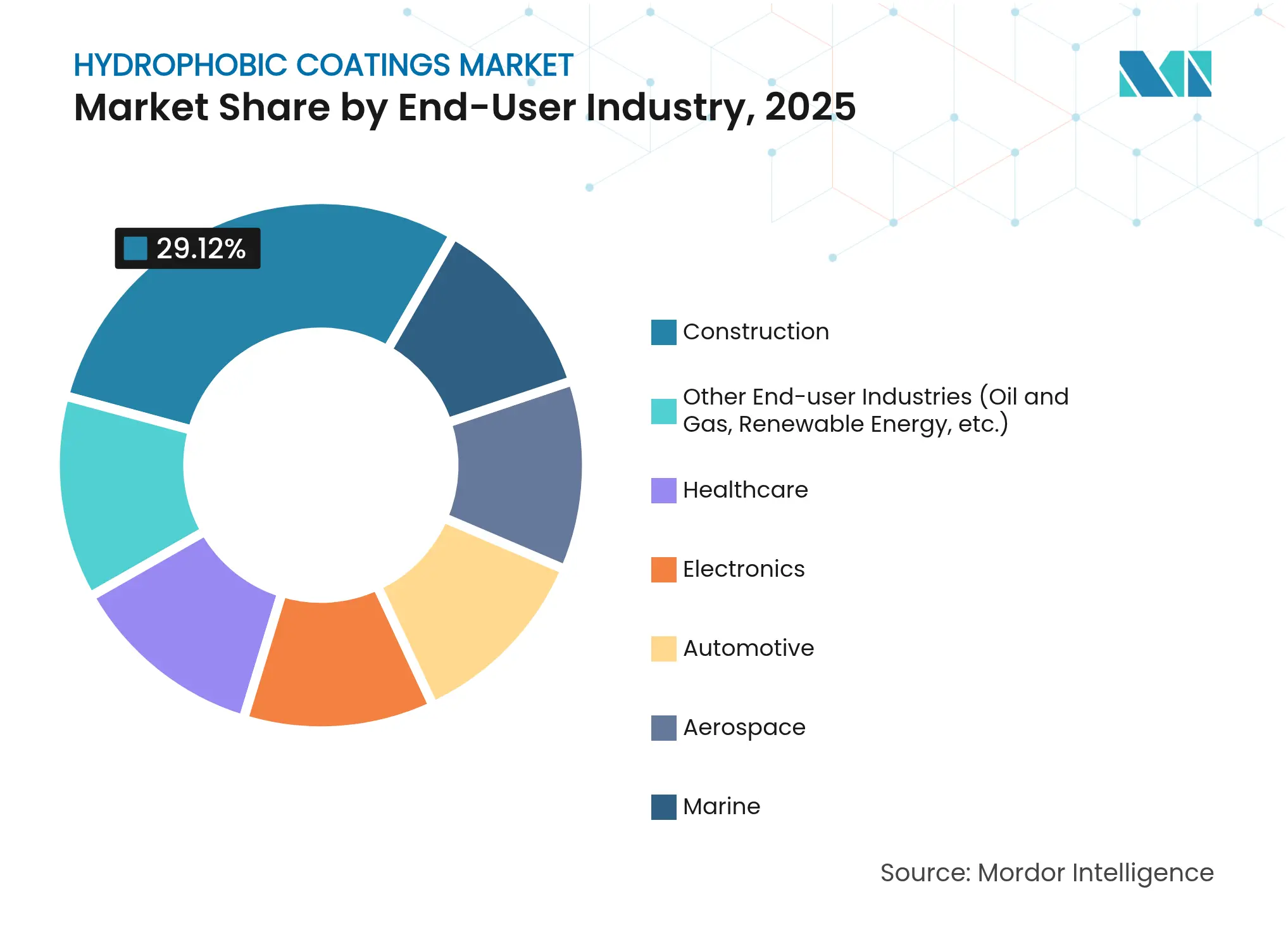

By End-User Industry: Construction Stability Meets Healthcare Innovation

Construction contributed 29.12% of 2025 revenue and remains the backbone of the hydrophobic coatings market, supported by ongoing investments in road, rail, and water infrastructure. Specifications now routinely include hydrophobic sealers for concrete decks and parking garages to arrest rebar corrosion, an inclusion that has effectively entrenched hydrophobic chemistry in routine maintenance cycles.

Healthcare, by contrast, is expected to be the fastest mover at a 6.86% CAGR. Hospitals and device OEMs are adopting antimicrobial hydrophobic barriers that resist biofilm formation on catheters, implants, and high-touch surfaces. Hydrogen-boride nanosheet-based coatings exhibiting broad-spectrum pathogen inactivation within 10 minutes underscore the potential for metal-free solutions in sterile environments. This influx of high-value medical demand elevates the average selling price across the broader hydrophobic coatings market.

Note: Segment shares of all individual segments available upon report purchase

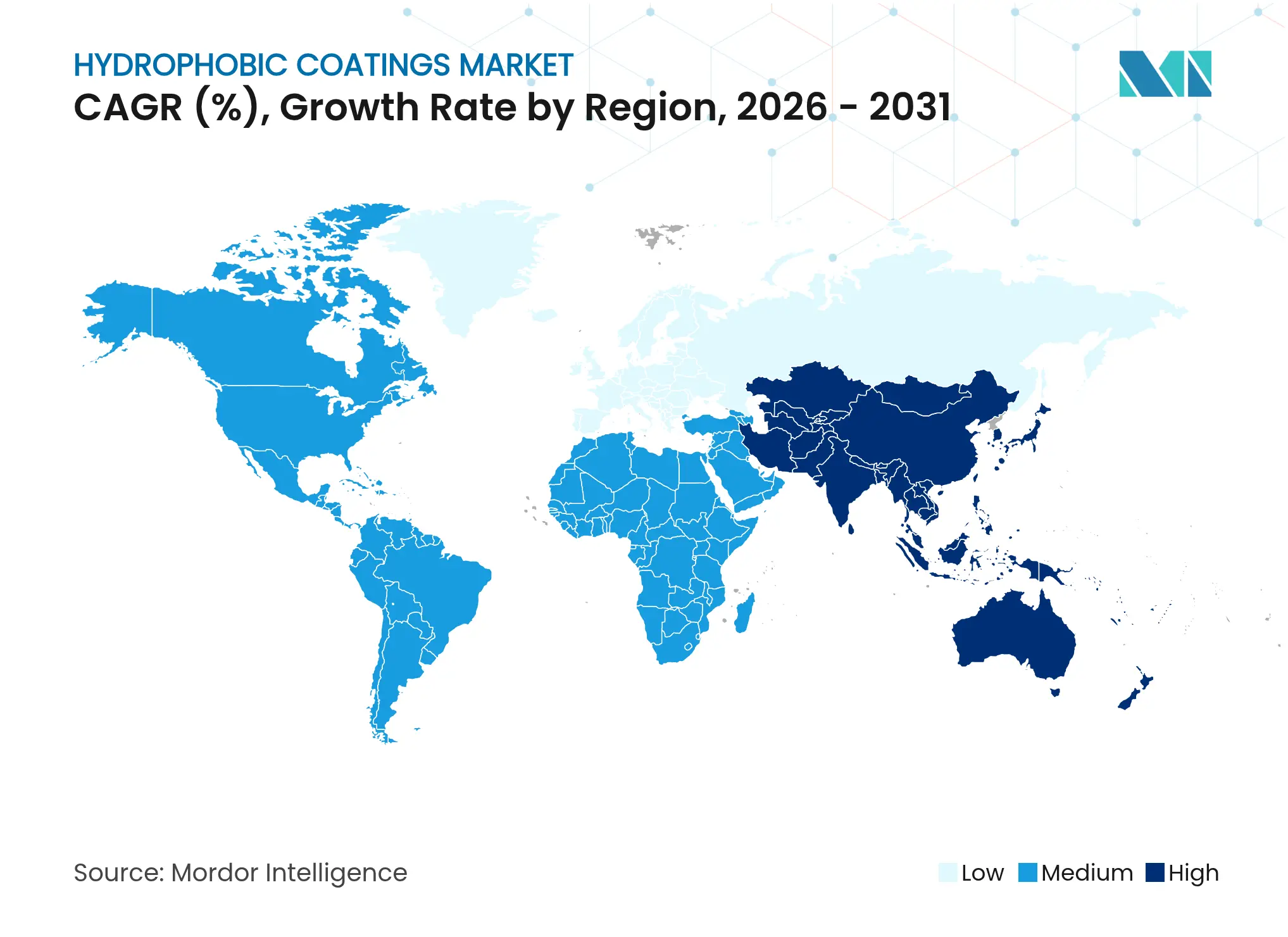

Asia-Pacific retained 47.66% revenue share in 2025, driven by China’s manufacturing scale, India’s infrastructure pipeline, and Japan’s material-science prowess. Government mandates that public buildings meet green-construction benchmarks have boosted uptake of low-VOC hydrophobic products. Electronics contract manufacturers across the region specify sub-micron waterproof layers to secure export contracts from global smartphone brands. Continued capacity additions in Southeast Asian solar module plants sustain demand for self-cleaning PV coatings that increase plant uptime.

North America stands as a technological bellwether. The United States cultivates high-performance aerospace and defense applications, where superhydrophobic anti-icing layers reduce operational costs for airlines and military fleets. Canada’s phased PFAS prohibition elevates domestic demand for fluorine-free chemistries, compelling regional suppliers to accelerate the qualification of silicone and polyurethane alternatives. Mexico’s automotive export hubs integrate hydrophobic treatments in electric-vehicle battery enclosures, reinforcing cross-border supply chains for raw materials and application equipment.

Europe balances strict environmental policy with industrial competitiveness. The European Chemicals Agency proposal to restrict over 10,000 PFAS substances has triggered a rush among formulators to validate bio-based replacements. Germany’s automotive Tier-1 suppliers co-develop graphene-reinforced water-borne top-coats that satisfy both corrosion-resistance and paint-shop emission targets. Nordic nations’ preference for circular-economy models stimulates demand for biodegradable hydrophobic barriers in packaging, pushing innovation toward cellulose-based solutions. The hydrophobic coatings market is thus experiencing geographically diverse pull factors that collectively sustain global growth momentum.

Market Concentration

The hydrophobic coatings market exhibits moderate fragmentation. Multinational incumbents such as 3M, PPG Industries, AkzoNobel, and BASF leverage economies of scale and global distribution, yet must navigate rising compliance costs linked to PFAS phase-outs. BASF’s plan to divest its USD 6.8 billion coatings arm illustrates the strategic recalibration underway as energy prices and regulatory scrutiny tighten margins. Capital allocation is shifting from commodity segments toward high-value specialty niches where bespoke hydrophobic formulations command pricing power.

Specialized nanocoating firms occupy agile positions, often targeting niche applications like IPX8-level electronics waterproofing or anti-icing aerospace surfaces. Aculon’s supply agreement with Henkel to embed NanoProof technology in mobile devices exemplifies the pattern of vertical collaboration that extends technology reach while giving OEMs a single-source solution. Intellectual-property moat building has intensified; the past 24 months saw a sharp rise in patents covering micro- and nano-texture fabrication processes that achieve high contact angles with minimal fluorine content.

Bio-based innovators are also gaining ground. Start-ups using vegetable-oil-derived polyols or peptide-functionalized cellulose report progress in achieving water contact angles above 110° while meeting end-of-life compostability metrics. These entrants often partner with packaging converters or apparel brands seeking PFAS-free labels. As a result, the competitive arena is gradually tilting toward firms that can combine material science ingenuity with credible sustainability narratives.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The hydrophobic coatings market report includes:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.