Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

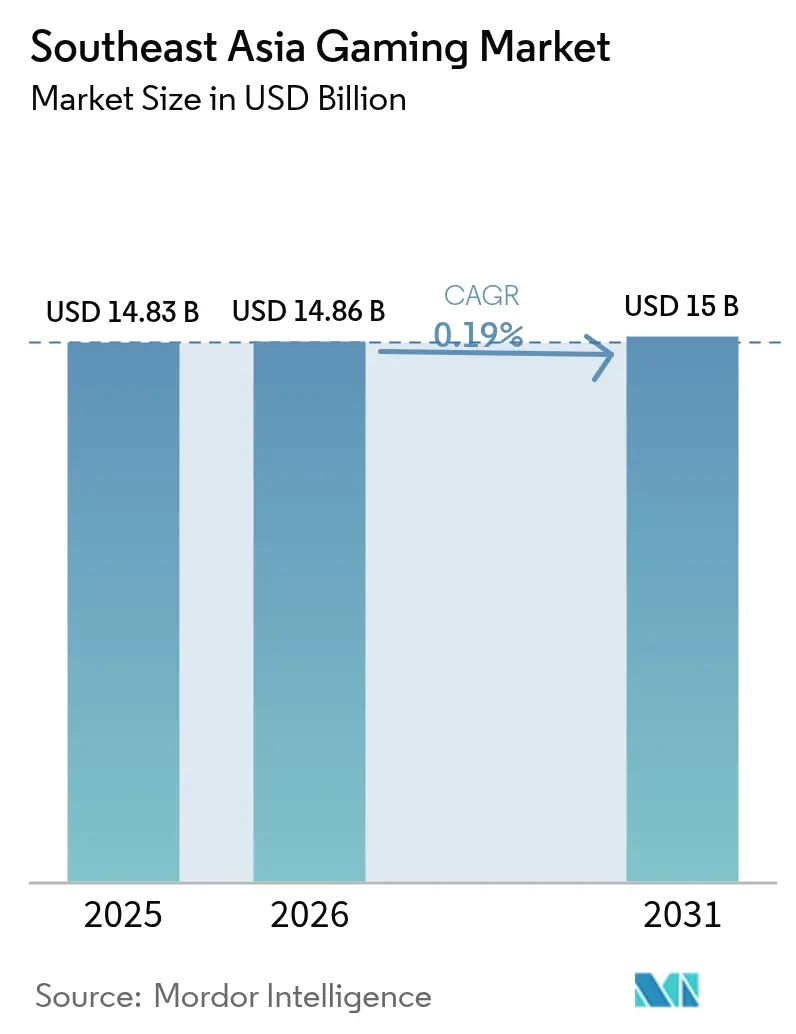

| Base Year Market Size (2025) | USD 14.83 Billion |

| Market Size (2026) | USD 14.86 Billion |

| Market Size (2031) | USD 15 Billion |

| Growth Rate (2026 - 2031) | 0.19% CAGR |

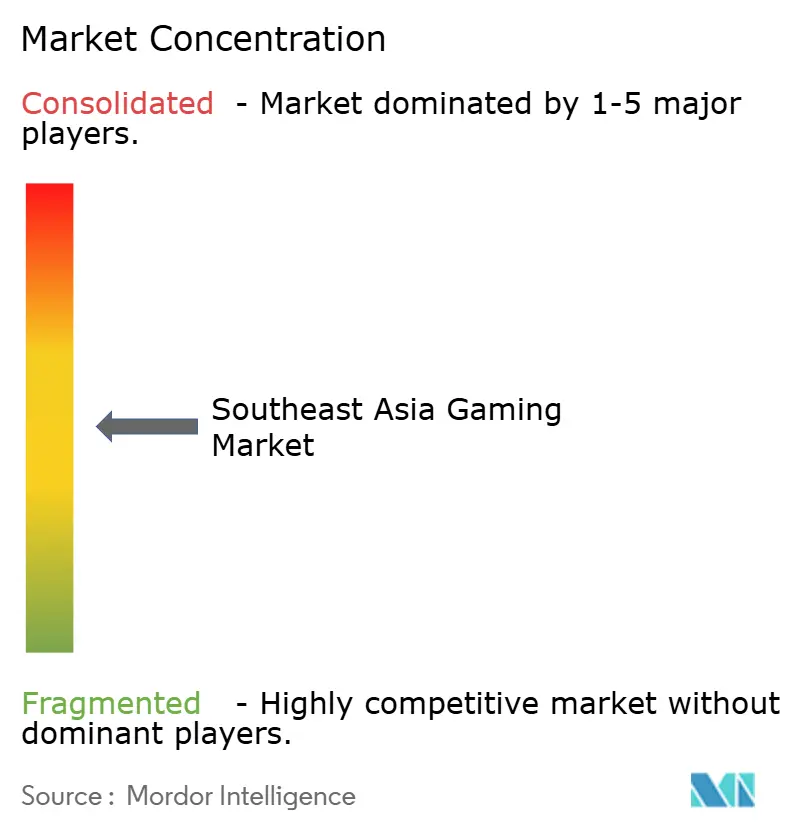

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Gaming Market Analysis by Mordor Intelligence

Southeast Asia gaming market size in 2026 is estimated at USD 14.86 billion, growing from 2025 value of USD 14.83 billion with 2031 projections showing USD 15 billion, growing at 0.19% CAGR over 2026-2031. Robust user engagement continues, yet saturated addressable audiences, tightening regulations, and currency volatility restrain top-line expansion. Mobile titles retain primacy as 5G coverage improves playability and cloud-based delivery, but low-spec devices cap average revenue per user and limit premium content uptake. Localized payment ecosystems anchored in digital wallets and carrier billing reduce friction for micro-transactions and help offset credit-card under-penetration. Intensifying rivalry among regional champions such as Garena and global publishers, including Tencent and NetEase, accelerates content localization, esports sponsorship, and hybrid monetization experiments. Government esports programs and tax incentives spur professionalization, though compliance costs and content-approval delays temper immediate returns.

Key Report Takeaways

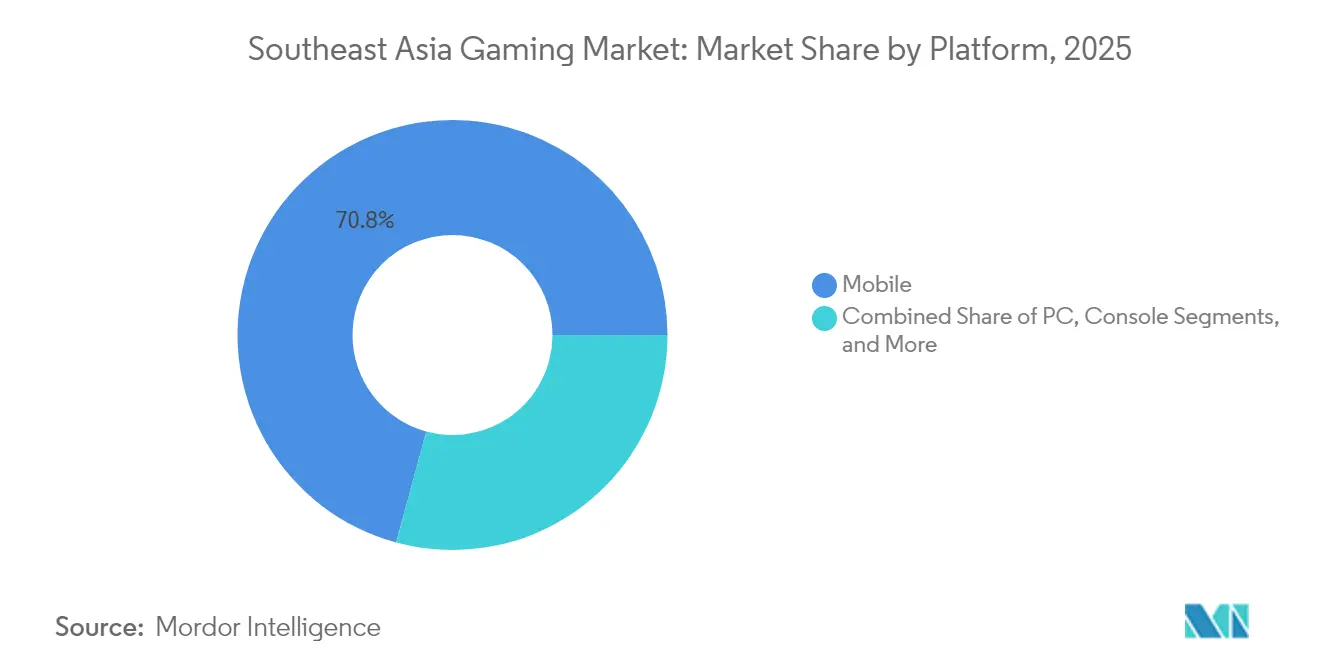

- By platform, mobile accounted for 70.78% of the Southeast Asia gaming market share in 2025. Cloud gaming is projected to expand at a 0.95% CAGR between 2026-2031.

- By revenue model, free-to-play held 75.62% share of the Southeast Asia gaming market size in 2025. Subscription services post the fastest growth at a 1.20% CAGR through 2031.

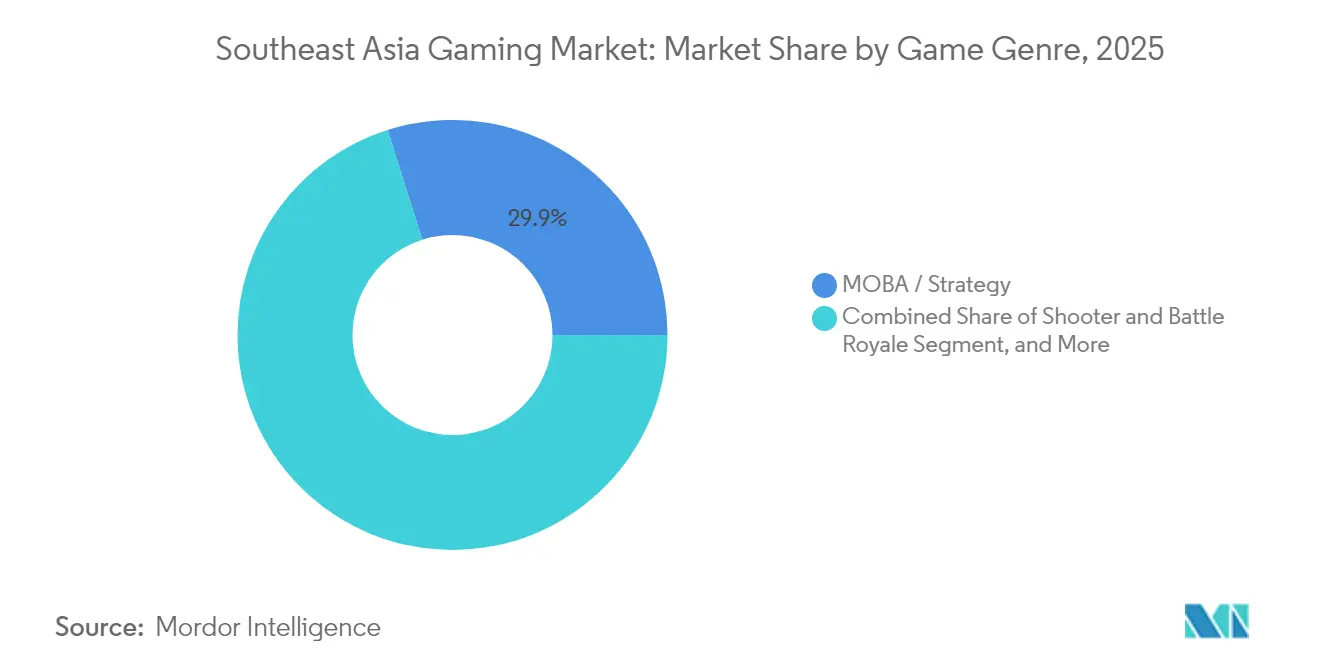

- By game genre, MOBA and strategy commanded 29.88% of the Southeast Asia gaming market size in 2025, while simulation and sports are advancing at a 0.43% CAGR.

- By country, Indonesia led with 29.45% of the Southeast Asia gaming market share in 2025; Thailand records the highest projected CAGR at 0.59% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Gaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mobile-internet penetration and affordable smartphones | +0.8% | Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| 5G rollout enabling low-latency competitive gaming | +0.6% | Singapore, Malaysia, Thailand | Medium term (2-4 years) |

| Increasing adoption of digital wallets and carrier billing | +0.5% | Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Government support for esports and tax incentives | +0.4% | Thailand, Malaysia, Indonesia | Long term (≥ 4 years) |

| Emergence of out-of-app alternative distribution channels | +0.3% | Global | Short term (≤ 2 years) |

| Surging cloud-gaming cafés in tier-2 SEA cities | +0.2% | Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Mobile-Internet Penetration and Affordable Smartphones

Indonesia achieved 99.4% smartphone adoption among internet users by 2024, with 96% of players favoring mobile titles. Budget Android devices priced below USD 150 broadened gamer demographics, bringing Vietnam’s user base to 54 million and sustaining 9% annual growth. Publishers respond by optimizing asset size, frame rates, and battery consumption to accommodate entry-level hardware, ensuring reach but limiting premium graphics and monetization depth. Lightweight builds cut data costs and improve playability on 3G fallback connections, reinforcing the Southeast Asia gaming market’s mobile-first orientation. Yet low disposable income segments restrain in-app purchase intensity, keeping ARPU below USD 15 across most markets. Device vendors collaborating with telcos on gaming-bundled data plans aim to elevate engagement and nudge users toward higher-end handsets.

5G Rollout Enabling Low-Latency Competitive Gaming

Malaysia’s 5G network covered 80.2% of the population by December 2024, boosting median download speeds to 105.36 Mbps from 45.57 Mbps a year earlier. Singapore ranks among Asia’s fastest for mobile throughput, while Thailand’s 5G footprint spans over 90% of urban centers.[1]Staff Reporter, “5G Availability High Amongst APAC Markets,” Asian Telecom, asiantelecom.com Low-latency connectivity cuts lag to sub-30 ms, a threshold critical for MOBA and battle-royale esports. TM Global deployed edge facilities to shrink server round-trips, demonstrating 40% latency reduction in pilot cloud-gaming sessions. Telcos bundle data-free game passes and co-host tournaments to popularize 5G services. Rural coverage gaps and spectrum-auction delays in Indonesia temper uniform gains, but government digital-inclusion mandates aim to close disparities by 2027.

Increasing Adoption of Digital Wallets and Carrier Billing

TrueMoney, GrabPay, and Boost collectively exceed 120 million active wallets region-wide, with game credit top-ups among the top three use cases in Thailand and Malaysia.[2]DigitalEdge, “Fintech: Digital Wallets Driving User-Centric Finance,” The Edge Malaysia, theedgemalaysia.com Average in-game basket sizes rise 64% when buy-now-pay-later options are available, signaling latent spending capacity once friction barriers fall. Direct carrier billing still processes over 25% of micro-transactions in the Philippines, serving unbanked users, though operator fees above 25% compress publisher margins. Regulatory pushes for interoperable QR standards and caps on wallet fees support broader payment choice, benefiting the Southeast Asia gaming market as platforms diversify monetization away from sole reliance on Google Play and App Store rails.

Government Support for Esports and Tax Incentives

Thailand’s 2021 recognition of esports as a professional sport unlocked access to the Sports Authority fund, channeling USD 2.9 million into athlete development by 2025. Malaysia earmarked RM 10 million (USD 2.4 million) for esports infrastructure, matched by private sponsorship from telcos and hardware vendors.[3]Dealessandri Marie, “Esports Professionally Recognised in Thailand,” GamesIndustry.biz, gamesindustry.biz Indonesia’s Presidential Regulation 19/2024 coordinates ministries to raise domestic developer share and eases foreign-talent visas, targeting USD 40 million annual private investment. These programs legitimize gaming careers, expand event calendars, and attract global tournament IP such as Valorant Masters Bangkok 2025. Lengthy budget disbursement cycles and shifting political priorities may stagger timelines, yet the policy tailwind remains positive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-spec device base limits high-fidelity titles | -0.4% | Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Stringent content regulations and approval delays | -0.3% | Vietnam, Indonesia, Malaysia | Long term (≥ 4 years) |

| Volatile local currencies hurt IAP pricing | -0.2% | Indonesia, Philippines, Thailand | Short term (≤ 2 years) |

| Rising digital-payment fraud and chargebacks | -0.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low-Spec Device Base Limits High-Fidelity Titles

Entry-level smartphones with 3 GB RAM or less still account for 52% of handsets in Indonesia and the Philippines. Developers invest in asset-streaming and adaptive-resolution technology to maintain playability, but visual downgrades dilute potential for premium cosmetics and season-pass upselling. Testing matrices encompass over 600 device models, inflating QA budgets by up to 35%. The constraint sustains dominance of casual and hyper-casual genres, keeping average session times under 30 minutes and depressing ad-view CPMs. Hardware upgrades will occur gradually as income levels rise, but near-term monetization upside remains capped.

Stringent Content Regulations and Approval Delays

Vietnam’s Ministry of Information and Communications revoked 104 G1 licenses by November 2024 for non-compliance, extending go-to-market timelines to six-plus months.[4]Vietnam+, “Vietnam Seeks to Tap Into Game Industry’s Huge Potential,” vietnamplus.vn Indonesia blocked access to Steam and Epic Games Store in 2022 over registration issues, underscoring enforcement capabilities. Malaysia’s Film Censorship Board retains broad discretionary powers that have led to game bans on religious-sensitivity grounds. These hurdles raise legal costs and encourage partnerships with local publishers versed in compliance. Iterative live-ops updates can trigger re-review, complicating seasonal content release pacing and hampering the Southeast Asia gaming market’s agility relative to global peers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Strength Spurs Cloud Crossover

Mobile titles generated 70.78% of 2025 revenues, confirming the Southeast Asia gaming market dependence on handheld devices. The segment still posts mid-single-digit user growth as rural smartphone diffusion progresses, but monetization intensity plateaus. Cloud gaming, although only 1.8% of revenue, records the fastest 0.95% CAGR, benefitting from 5G rollouts and edge-compute partnerships. The Southeast Asia gaming market size for cloud services is projected to surpass USD 365 million by 2031, translating to 2.43% of overall spend. Hybrid models allowing session hand-off between mobile and cloud strengthen retention. PC café revenue slips amid higher electricity prices, yet cafés reposition as esports arenas, drawing sponsorship from peripheral brands. Console adoption lags due to USD 400+ hardware pricing and limited official distribution channels, though gray-market imports feed niche enthusiast communities.

Hardware subsidies tied to telco contracts and cloud-streamed console libraries attempt to lower the entry barrier. Content strategy increasingly revolves around cross-platform progression, letting players grind on mobile and enjoy premium visuals in the café or at home. Publishers leverage cloud-rendered demos to market upcoming mobile ports, reducing APK download friction and highlighting flagship experiences that were previously inaccessible to low-spec device owners.

By Revenue Model: Subscriptions Gain Traction Amid Free-to-Play Plateau

Free-to-play accounted for 75.62% of the Southeast Asia gaming market size in 2025, with gacha, season passes, and cosmetic bundles anchoring spend. However, payer conversion rates hover at 6–8%. Subscription passes such as Garena Booyah and Apple Arcade post a 1.20% CAGR, surpassing USD 426 million by 2031. Bundles offering ad-free gameplay, exclusive skins, and monthly currency stipends enhance perceived value, especially when priced below USD 4. Carrier-billed weekly pass variants attract unbanked users. In-game advertising grows alongside regional digital-ad spending but faces viewability trade-offs during competitive sessions.

Regulators scrutinize loot-box mechanics, pushing publishers to disclose odds and cap spending, which may marginally depress high-spender activity. Consequently, developers diversify toward battle-pass and cosmetic subscriptions. The Southeast Asia gaming market share for premium pay-to-play titles remains under 3% given price sensitivity, yet remastered legacy IPs enjoy nostalgia-driven spikes. Web3 play-to-earn activity cools after speculative token declines, but select guild-run scholarship models persist in the Philippines.

By Game Genre: MOBA Primacy Meets Simulation Surge

MOBA and strategy titles held 29.88% of 2025 revenue, led by Mobile Legends: Bang Bang, which generated USD 45 million regionally during January-April 2024. The Southeast Asia gaming market size for MOBA is projected to contract marginally as newer genres take share, but esports-driven engagement keeps monetization robust. Simulation and sports exhibit 0.43% CAGR, propelled by localized football licenses and life-sim titles featuring regional cultural motifs. Shooter and battle-royale franchises maintain stickiness through frequent cosmetic drops and influencer-backed tournaments, though user churn rises with content fatigue. Role-playing games gain footing via cross-media collaborations with anime properties popular among Gen Z.

Cross-genre hybrids emerge: MOBA-auto-battler mashups and shooter-RPG blends create differentiated loops to combat saturation. Developers localize language packs and celebrity voice-overs to deepen emotional resonance. Educational game sub-genres begin exploring ad-funded freemium paths in Thailand’s school sector. The genre diversification underscores evolving taste profiles as disposable incomes rise and as cloud-streamed fidelity broadens palate.

Geography Analysis

Indonesia anchors the Southeast Asia gaming market with a 29.45% stake, leveraging its vast population and 96% mobile preference to generate USD 4.38 billion in 2026 revenue. Presidential Regulation 19/2024 sets objectives to lift local developer revenue share and to streamline import duties on gaming hardware. Yet 2022 platform blocks highlight regulatory unpredictability that can upend foreign publisher planning. Telcos partner with Tencent Cloud to pilot edge nodes in Java and Sulawesi, eyeing 40% latency reduction for multiplayer titles.

Thailand’s projected 0.59% CAGR brings its revenue to USD 2.62 billion by 2031, driven by 5G coverage, esports grants, and high social-media penetration that amplifies influencer campaigns. State-backed tournaments funnel prize pools that exceed USD 5 million annually, stimulating semi-pro circuits. Payment-gateway regulation caps merchant fees at 1.5%, encouraging micro-transaction experimentation.

Vietnam’s gaming user base surpassed 54 million in 2024, and the government outlines a USD 1 billion ambition by 2030. However, G1 licensing reviews and content screening prolong launch timelines. Local studios such as VNG and Hiker Games secure co-publishing deals with Korean and Chinese IP owners to mitigate compliance risk.

Malaysia and Singapore share advanced infrastructure. Malaysia’s nationwide network modernization, 44% complete in 2024, readies 7,200 5G-capable sites. Singapore’s Infocomm Media Development Authority supports cloud-gaming pilots within its Media Industry Digital Plan, offering rebates on GPU cloud hours. The Philippines leverages a 76 million mobile-first population, with telco Smart’s Giga Arena esports platform surpassing 1 million registered gamers in 2025. Emerging markets such as Cambodia and Laos show double-digit gamer growth but contribute under 3% of regional spend due to limited payment rails and political uncertainties.

Competitive Landscape

The Southeast Asia gaming market remains fragmented; the top five publishers collectively hold roughly 28% share, indicating moderate concentration. Sea Limited’s Garena leads through localized operations and flagship Free Fire, which posted 70% quarter-over-quarter download growth in Indonesia during 2024. Tencent leverages WeChat Pay integrations and partnerships with Malaysian telcos to reduce payment friction. NetEase expands via local joint ventures and Thai-language dubbing studios, while Activision Blizzard licenses Call of Duty Mobile through Garena to capitalize on existing distribution.

Content localization depth differentiates regional players: Bahasa voice-overs, cultural holiday events, and Muslim-friendly cosmetic items lift engagement during Ramadan. Cloud infrastructure investments become competitive moats; TM Global and Tencent Cloud court publishers with SLA-backed sub-40 ms latency. Blockchain integration experiments continue, illustrated by play-to-own cosmetics trials in Singapore, but mainstream adoption stays cautious.

Strategic moves in 2024-2025 illustrate rivalry escalation. NCSOFT created NCV Games with Vietnam’s VNG to publish Lineage 2M across six markets, tapping VNG’s Zalo payment network. TM Global’s March 2025 Edge Gaming launch positions Malaysia as a cloud-gaming hub. Tencent opened a Jakarta creator campus providing motion-capture facilities to indie studios, aiming to secure early access to breakout IP. Esports event operators ESL and Mineski expand arena footprints, deepening sponsorship inventory.

Southeast Asia Gaming Industry Leaders

IGG Inc.

Nintendo Co., Ltd.

Asiasoft Corporation Public Company Limited

Sony Group Corporation

Com2uS Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TM Global debuted Edge Gaming, bringing edge nodes to Malaysia for sub-30 ms latency cloud play.

- March 2025: Sky Mavis revealed Axie Infinity: Atia’s Legacy MMO with pre-registration open and alpha tests planned for summer 2025, leveraging Ronin sidechain to expand its ecosystem.

- February 2025: Indonesia projected IDR 24.88 trillion gaming revenue as Regulation 19/2024 accelerates developer incentives and mobilizes USD 40 million annual private funding.

- January 2025: Honor of Kings surpassed USD 1 billion global revenue after its 2024 SEA launch, underscoring the region’s strategic role.

Southeast Asia Gaming Market Report Scope

Asia-Pacific holds the largest share globally in the gaming market, while Southeast Asia generates the largest revenue. The online population in Southeast Asia is rapidly rising, mostly due to increased mobile device use. Almost two-thirds of the gaming population in Greater Southeast Asia are engaged in e-sports. Owing to this trend, the region is also becoming the fastest-growing gaming market in the world.

The Southeast Asian gaming market is segmented by platform (PC, console, mobile) and geography (Indonesia, Malaysia, Singapore, Thailand, and the Rest of Southeast Asia). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Platform

| Mobile |

| PC |

| Console |

| Cloud/Game-Streaming |

By Revenue Model

| Free-to-Play (F2P) |

| Premium / Pay-to-Play |

| Subscription |

| In-Game Advertising |

| Hybrid and Web3 / Play-to-Earn |

By Game Genre

| MOBA / Strategy |

| Shooter and Battle Royale |

| Role-Playing Games (RPG) |

| Casual and Puzzle |

| Simulation and Sports |

| Other Game Genre |

By Country

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By Platform | Mobile |

| PC | |

| Console | |

| Cloud/Game-Streaming | |

| By Revenue Model | Free-to-Play (F2P) |

| Premium / Pay-to-Play | |

| Subscription | |

| In-Game Advertising | |

| Hybrid and Web3 / Play-to-Earn | |

| By Game Genre | MOBA / Strategy |

| Shooter and Battle Royale | |

| Role-Playing Games (RPG) | |

| Casual and Puzzle | |

| Simulation and Sports | |

| Other Game Genre | |

| By Country | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large is the Southeast Asia gaming market in 2026?

It is valued at USD 14.86 billion, with a forecast to reach USD 15 billion by 2031 at a 0.19% CAGR.

Which platform leads spending among gamers in Southeast Asia?

Mobile titles dominate, accounting for 70.78% of 2025 revenue and retaining growth momentum as 5G coverage expands.

Why is Thailand considered the region’s fastest-growing gaming country?

Government recognition of esports, 5G rollout, and hosting premier events like Valorant Masters underpin its 0.59% CAGR outlook through 2031.

What revenue model shows the most upside beyond free-to-play?

Subscription passes are the fastest-growing, increasing at a 1.20% CAGR as they offer bundled perks and predictable cash flows.

How are payment preferences shaping monetization?

Rising digital-wallet and carrier-billing adoption lowers friction for micro-transactions, boosting average basket sizes and payer conversion rates.

Page last updated on: