Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

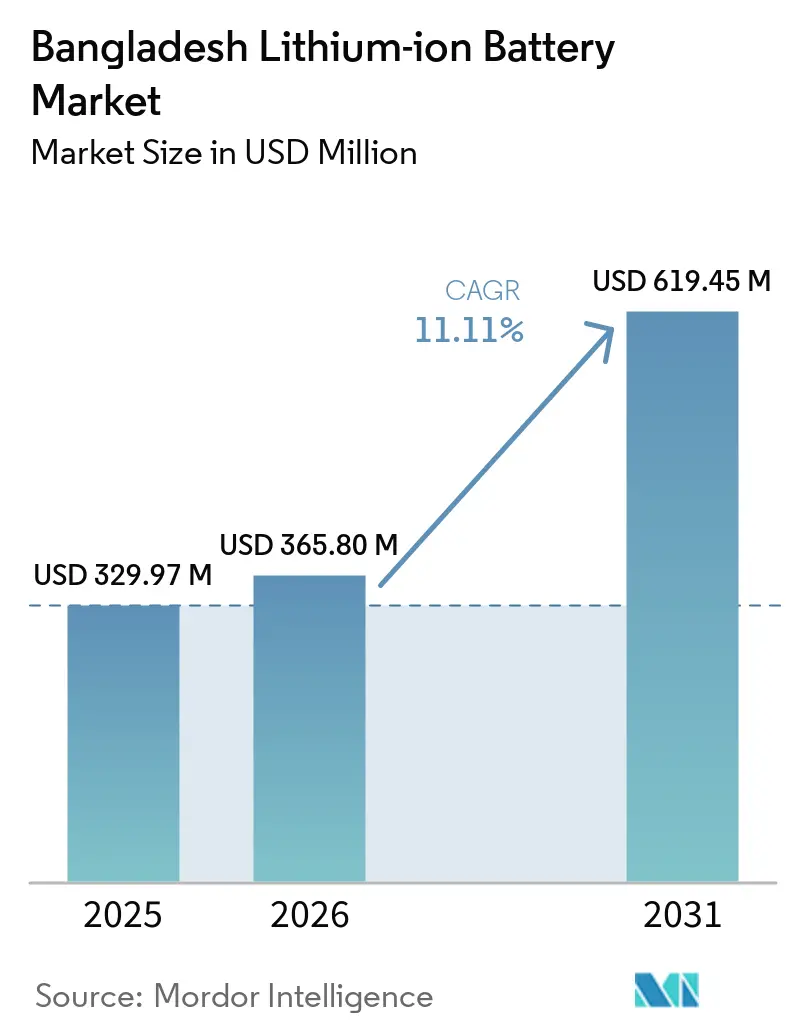

| Base Year Market Size (2025) | USD 329.97 Million |

| Market Size (2026) | USD 365.80 Million |

| Market Size (2031) | USD 619.45 Million |

| Growth Rate (2026 - 2031) | 11.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Lithium-ion Battery Market Analysis by Mordor Intelligence

The Bangladesh Lithium-ion Battery Market size is projected to be USD 329.97 million in 2025, USD 365.80 million in 2026, and reach USD 619.45 million by 2031, growing at a CAGR of 11.11% from 2026 to 2031.

Robust policy support, notably the June 2025 duty cut on battery raw materials, is accelerating the migration from lead-acid to lithium-ion across an estimated 2-4 million electric two- and three-wheelers. Falling global cell prices, the legalization of battery-run autorickshaws, and the rapid build-out of battery-swapping networks are catalyzing formal investment from local conglomerates and Chinese suppliers. Parallel momentum in telecom tower backup systems, cold-chain logistics, and distributed aquaculture micro-grids is broadening use cases and reinforcing demand resilience. Despite these tailwinds, grid instability, supply-chain dependence on China, and a lack of domestic safety standards temper near-term returns on stationary storage projects.

Key Report Takeaways

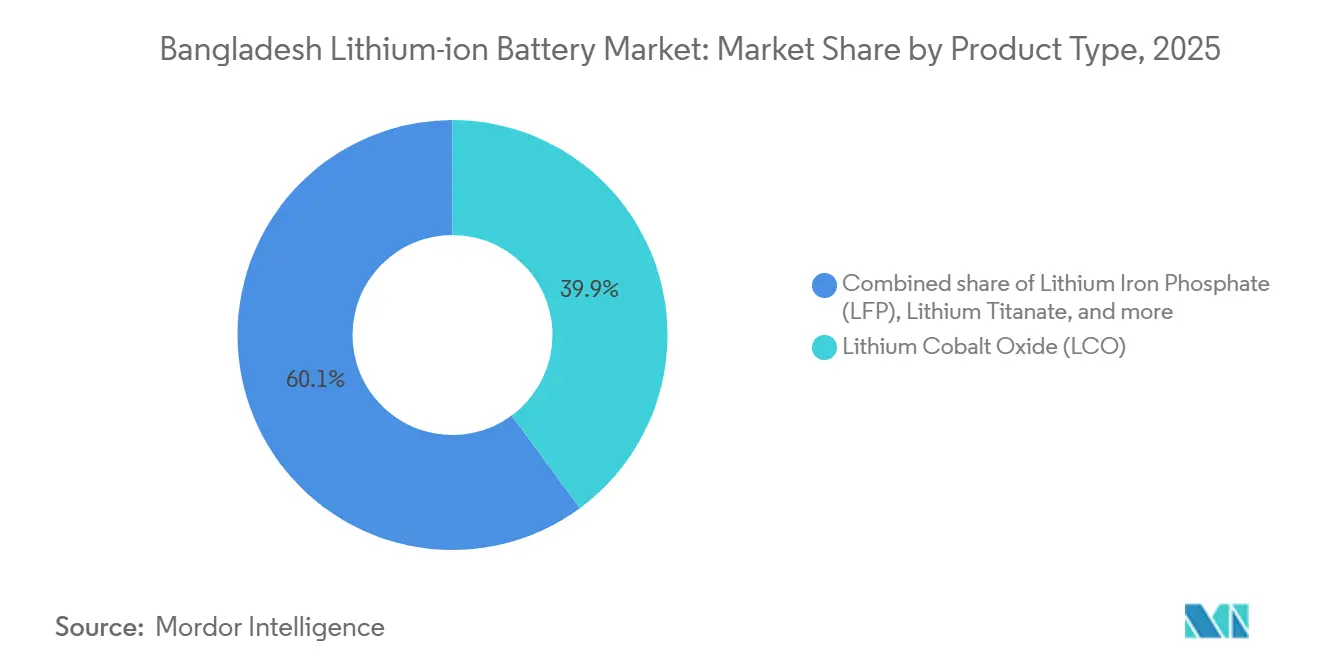

- By product type, lithium cobalt oxide led with 39.9% of Bangladesh's lithium-ion battery market share in 2025, while lithium iron phosphate is projected to expand at a 20.8% CAGR through 2031.

- By form factor, cylindrical cells accounted for 45.4% of the Bangladesh lithium-ion battery market in 2025; pouch cells are expected to grow at 22.7% CAGR over the forecast period.

- By power capacity, the 3,000-10,000 mAh range captured 34.1% of the Bangladesh lithium-ion battery market size in 2025; the above-60,000 mAh bracket is expected advance at a 23.9% CAGR.

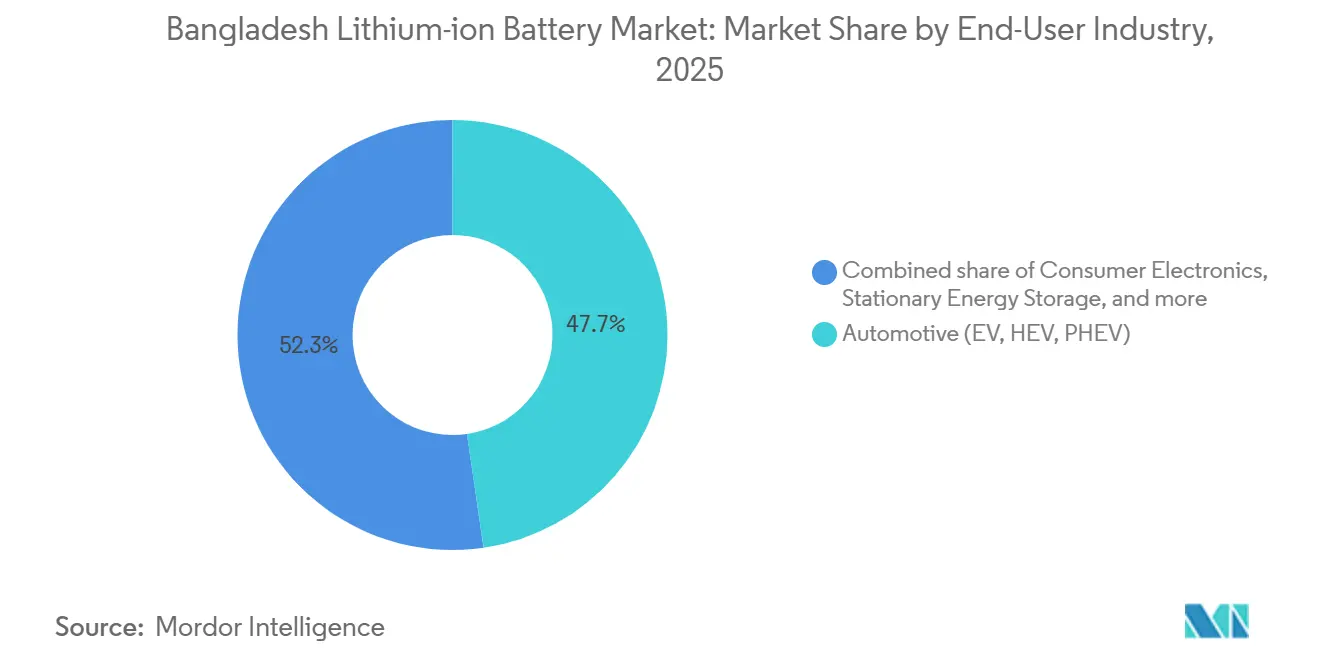

- By end-use industry, automotive held 47.7% revenue share in 2025 and is expected to grow at a 14.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Lithium-ion Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid e-two/three-wheeler adoption | 4.20% | National, Dhaka, Chittagong, Sylhet | Short term (≤ 2 years) |

| Government EV & Solar Home System incentives | 3.10% | National, policy set in Dhaka | Medium term (2-4 years) |

| Falling global cell $/kWh prices | 2.50% | Global pass-through to Bangladesh | Short term (≤ 2 years) |

| Telecom tower battery-swap programs | 1.80% | Urban and peri-urban tower sites | Medium term (2-4 years) |

| Dhaka-centric e-commerce cold-chain demand | 0.60% | Dhaka, spillover to Chittagong | Long term (≥ 4 years) |

| Off-grid shrimp-farm micro-grids | 0.40% | Coastal Khulna, Satkhira, Cox’s Bazar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid E-Two/Three-Wheeler Adoption Drives Volume Demand

Bangladesh hosts 2-4 million battery-powered rickshaws, yet over 80% still use lead-acid batteries in 2024, incurring annual replacements of roughly 4 million units.[1]A.S.M. Mominul Hasan, “Electric Rickshaw Charging Stations as Distributed Energy Storages for Integrating Intermittent Renewable Energy Sources: A Case of Bangladesh,” Energies, mdpi.com Nationwide legalization of battery-run autorickshaws in May 2024 eliminated regulatory uncertainty, enabling organized manufacturers to enter with lithium-ion packs that last 3-5 years. Tianneng Battery’s January 2026 supply agreement with Rahimafrooz targets 4 million e-trikes and illustrates how Chinese cell makers leverage local distributors to meet surging replacement demand.[2]TBS Report, “Import duty on raw materials for e-bikes, lithium batteries reduced from 80% to 1%,” The Business Standard, tbsnews.net As formalization compresses the replacement cycle, value shifts from disposable lead-acid units to durable lithium-ion systems financed through swap subscriptions and installment credit.

Government EV & Solar Home System Incentives Lower Entry Barriers

The June 2025 cut of customs duty on lithium battery inputs to 1% reversed a cumulative levy exceeding 70%, sacrificing BDT 1,000 crore in annual revenue to spur domestic assembly. By neutralizing the price gap between imported packs and local builds, the policy draws investment from Huawei and Walton, whose planned 1 GWh plant exemplifies mid-stream value capture. Closing loopholes that previously allowed refurbished battery imports curbs quality risks and encourages standardized packs that carry warranties, accelerating trust among fleet operators.

Falling Global Cell $/kWh Prices Accelerate Substitution

Global pack prices fell 20-30% in 2024, with LFP enjoying a 30% cost edge over NMC chemistries.[3]International Energy Agency, “Global EV Outlook 2025,” iea.org In Bangladesh, where 100% of cells are imported, and 80% originate from China, these declines translate directly into retail savings. A 48 V 40 Ah LFP pack priced at BDT 50,000-60,000 in 2025 delivers a 40-50% total-cost-of-ownership benefit over five years compared with lead-acid arrays. Tiger New Energy’s battery-as-a-service platform monetizes that differential by billing per swap and redeploying end-of-life packs into second-life stationary uses.[4]Gulf News, “Harvard duo powers Bangladesh's rickshaws with battery startup,” gulfnews.com

Telecom Tower Battery-Swap Programs Expand Stationary Storage

EDOTCO’s migration of 17,000 towers to lithium-ion and its July 2025 MoU with Tiger New Energy highlight telecom infrastructure as an anchor for large-format cell demand. LFP cells rated for 3,000+ cycles cut tower backup replacements by a factor of ten versus lead-acid. The Bangladesh Energy Regulatory Commission’s plan for a dedicated swapping tariff could let stations earn grid-service income, improving internal rates of return by 3-5 percentage points and supporting nationwide rollout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited local raw-material supply | -2.80% | National, all assemblers | Long term (≥ 4 years) |

| Grid instability affecting ESS ROI | -1.20% | Industrial zones, rural areas | Medium term (2-4 years) |

| High upfront CAPEX for EV OEMs | -1.90% | Organized manufacturers | Medium term (2-4 years) |

| Fire-safety regulatory gaps | -0.70% | Dense urban warehouses | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Local Raw-Material Supply Exposes Import Dependency

Bangladesh relies entirely on imported lithium, cobalt, and graphite, with China accounting for more than 80% of inputs. Lead times of 60-90 days hamper working-capital cycles, while India’s USD 2.4 billion cell incentive scheme diverts regional capacity. Without upstream policy support, local assemblers remain price-takers, vulnerable to geopolitical shocks such as potential Chinese export controls on battery-grade carbonate.

Grid Instability Affecting ESS ROI

Daily load-shedding of 500-1,500 MW in 2024 produced voltage swings of ±0.5 Hz, undermining inverter efficiency and accelerating battery degradation. For rooftop solar and telecom backup systems, erratic grid frequency shortens expected lifespans and elongates payback periods beyond five years. Until distribution upgrades materialize, investors may delay large-format storage despite policy incentives, slowing the Bangladesh lithium-ion battery market’s penetration into commercial and industrial segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LFP Chemistry Gains on Cost and Safety

Lithium cobalt oxide secured 39.9% of 2025 demand, anchored in smartphones and laptops that prize energy density. By contrast, lithium iron phosphate is forecast to post a 20.8% CAGR, capturing mobility and telecom applications where thermal stability and low cost prevail. The Bangladesh lithium-ion battery market size for LFP packs used in e-rickshaws is projected to more than triple between 2025 and 2031, underpinned by Huawei-Walton capacity expansions.

Suppliers such as Pylon Technologies promote 15-year LFP modules for tower backup, advancing the Bangladesh lithium-ion battery market as operators pursue maintenance-free assets. NMC retains a niche in imported premium EVs, while NCA, LMO, and LTO remain minor. Should global LFP oversupply persist, domestic assemblers may see their Bangladesh lithium-ion battery market share surpass 50% by 2028.

By Form Factor: Pouch Cells Gain in Automotive Conversions

Cylindrical formats held 45.4% in 2025, benefiting from mature 18650 and 21700 supply chains. Pouch cells, however, are registering a 22.7% CAGR as automotive converters value the 10-15% weight reduction achieved in 48 V packs. The Bangladesh lithium-ion battery market size for pouch-based packs is expected to rise sharply once Walton’s 80,000-unit line reaches full capacity in 2027.

Supply-chain risk offsets performance gains; pouch cells require custom tooling, inflating minimum orders. Larger assemblers with direct CATL contracts enjoy secure flow, while small workshops remain wedded to cylindrical imports from Shenzhen distributors. Prismatic cells fill a middle ground in telecom and cold-storage ESS.

By Power Capacity: Large-Format Cells Capture ESS and Fleet Demand

In 2025, 3,000-10,000 mAh cells commanded 34.1% due to smartphones and small e-bike packs. Above-60,000 mAh cells, mainly 280 Ah LFP units, are expected to climb at 23.9% CAGR as swap stations and tower backups scale. The Bangladesh lithium-ion battery market size for large-format modules could approach one-third of the total value by 2031 if Tiger New Energy hits its 2,000-station target.

Swapping mitigates slow-charge constraints by relocating charging to grid-connected depots, allowing 60-80 Ah packs that extend range to 150-180 km per swap. Rural micro-grid projects are also embracing 14 kWh arrays assembled from EVE LF280K cells that arrive through gray-market channels, highlighting ongoing supply informality.

By End-Use Industry: Automotive Segment Anchors Demand

Automotive captured 47.7% in 2025 and will grow at 14.3% CAGR as rickshaw formalization, fleet electrification, and ride-hailing platforms coalesce. The Bangladesh lithium-ion battery market size for automotive packs is forecast to exceed USD 300 million by 2031, supported by battery-as-a-service subscriptions that lower entry barriers.

Consumer electronics remain resilient, yet their growth moderates as replacement cycles lengthen. Stationary energy storage, industrial tools, and marine collectively remain below 15%, but tower backup upgrades and donor-funded fishing-vessel pilots offer upside. Parallel supply chains emerge: branded cells for organized OEMs and commodity imports for informal assemblers, each with distinct risk profiles.

Geography Analysis

Dhaka and Chittagong generate roughly 70% of Bangladesh's lithium-ion battery market demand. Dhaka’s 20 million residents sustain 1-1.5 million battery rickshaws and lead e-commerce cold-chain electrification, while Chittagong processes all cell imports and hosts the first 100 swap stations. Secondary cities such as Sylhet, Khulna, and Rajshahi witness accelerating two-wheeler adoption, though informality dominates distribution.

Coastal Khulna, Satkhira, and Cox’s Bazar anchor off-grid aquaculture pilots that deploy solar-plus-storage systems targeting 52% dissolved-oxygen gains in shrimp ponds, illustrating high willingness to pay where grid access is erratic. Suppliers tailor IP55-rated LFP modules to withstand humidity, commanding price premiums that offset low volumes.

Battery-swap rollouts follow a hub-and-spoke pattern: dense urban hubs achieve 200-300 swaps daily, recovering capital in 12-18 months, while rural spokes see 30-50 swaps and three-year paybacks. Urban-rural disparity may persist until policy incentives equalize economics or removable-battery models evolve to bridge the range gap.

Competitive Landscape

Chinese suppliers control about 80% of cell imports, anchoring a moderate-to-highly fragmented ecosystem. Dongjin Group’s USD 44 million Dhaka plant, launched in 2016, now claims more than 60% of local consumer battery volume. Local assemblers, Rahimafrooz, BASE Technologies, Navana Batteries, Karacus Energy, SARBS Communications, compete on distribution and after-sales, leveraging legacy lead-acid channels.

Global majors such as Samsung SDI, LG Energy Solution, CATL, BYD, and Panasonic Energy serve Bangladesh through regional hubs in India and Singapore. Samsung’s 6 GWh Bangalore plant (2025) and LG’s 40 GWh Gujarat complex (2026) prioritize automotive OEM contracts, leaving mass-market rickshaw segments largely to Chinese cell makers like EVE Energy.

Strategic white space lies in battery-as-a-service, second-life deployment, and recycling. Tiger New Energy’s ADB-backed swap business exemplifies a recurring-revenue pivot. Recycling capacity is absent, presenting an opening for regional specialists such as ACE Green Recycling to collect retired packs. Technology differentiation is shifting toward cloud-connected battery management systems that enable predictive analytics and secure 10-15% price premiums through service contracts.

Bangladesh Lithium-ion Battery Industry Leaders

BASE Technologies Ltd.

Rahimafrooz Energy Services

Samsung SDI (imports)

Navana Batteries

Karacus Energy Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Tianneng Battery and Rahimafrooz formed a strategic supply partnership targeting 4 million three-wheelers.

- July 2025: Tiger New Energy signed an MoU with EDOTCO to provide swappable LFP packs for 17,000 telecom towers.

- May 2025: Dhaka North City Corporation began shutting illegal battery-rickshaw workshops and mandated BUET-certified designs.

- April 2025: EVE Energy completed a 50 GWh LFP expansion, increasing LF280K exports that flow into Bangladesh’s off-grid solar systems.

Bangladesh Lithium-ion Battery Market Report Scope

A Li-ion battery, or lithium-ion battery, is a rechargeable battery composed of lithium-ion cells that contain lithium ions that move from the negative electrode through an electrolyte to the positive electrode during discharge and back when charging.

The Bangladesh Lithium-ion Battery Market Report is Segmented by Product Type (Lithium Cobalt Oxide (LCO), Lithium Iron Phosphate (LFP), Lithium Nickel Manganese Cobalt (NMC), Lithium Nickel Cobalt Aluminium (NCA), Lithium Manganese Oxide (LMO), and Lithium Titanate(LTO)), Form Factor (Cylindrical, Prismatic, and Pouch), Power Capacity (Up to 3,000 mAh, 3,000-10,000 mAh, 10,000-60,000 mAh, and Above 60,000 mAh), and End-use Industry (Automotive (EV, HEV, PHEV), Consumer Electronics, Industrial and Power Tools, Stationary Energy Storage, Aerospace and Defense, and Marine). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

By Product Type

| Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt (NMC) |

| Lithium Nickel Cobalt Aluminium (NCA) |

| Lithium Manganese Oxide (LMO) |

| Lithium Titanate (LTO) |

By Form Factor

| Cylindrical |

| Prismatic |

| Pouch |

By Power Capacity

| Up to 3,000 mAh |

| 3,000 to 10,000 mAh |

| 10,000 to 60,000 mAh |

| Above 60,000 mAh |

By End-use Industry

| Automotive (EV, HEV, PHEV) |

| Consumer Electronics |

| Industrial and Power Tools |

| Stationary Energy Storage |

| Aerospace and Defense |

| Marine |

| By Product Type | Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) | |

| Lithium Nickel Manganese Cobalt (NMC) | |

| Lithium Nickel Cobalt Aluminium (NCA) | |

| Lithium Manganese Oxide (LMO) | |

| Lithium Titanate (LTO) | |

| By Form Factor | Cylindrical |

| Prismatic | |

| Pouch | |

| By Power Capacity | Up to 3,000 mAh |

| 3,000 to 10,000 mAh | |

| 10,000 to 60,000 mAh | |

| Above 60,000 mAh | |

| By End-use Industry | Automotive (EV, HEV, PHEV) |

| Consumer Electronics | |

| Industrial and Power Tools | |

| Stationary Energy Storage | |

| Aerospace and Defense | |

| Marine |

Key Questions Answered in the Report

How large is the Bangladesh lithium-ion battery market in 2026?

It is valued at USD 365.80 million, on track for an 11.11% CAGR through 2031.

Which chemistry is growing fastest in Bangladesh?

Lithium iron phosphate is expanding at a 20.8% CAGR due to its cost and safety advantages.

Why are battery-swapping stations important for Bangladesh?

They cut upfront costs for drivers, improve battery lifecycle economics, and can earn grid-service revenue under a proposed BERC tariff.

What share does automotive hold in Bangladeshi demand?

Automotive accounted for 47.7% in 2025 and remains the anchor end-use segment.

How exposed is Bangladesh to import risk for battery materials?

The country imports 100% of lithium, cobalt, and graphite, mainly from China, making supply security a strategic concern.

Which cities drive the most lithium-ion demand?

Dhaka and Chittagong together generate about 70% of national demand, supported by dense populations and logistics hubs.

Page last updated on: