Field Programmable Gate Array (FPGA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

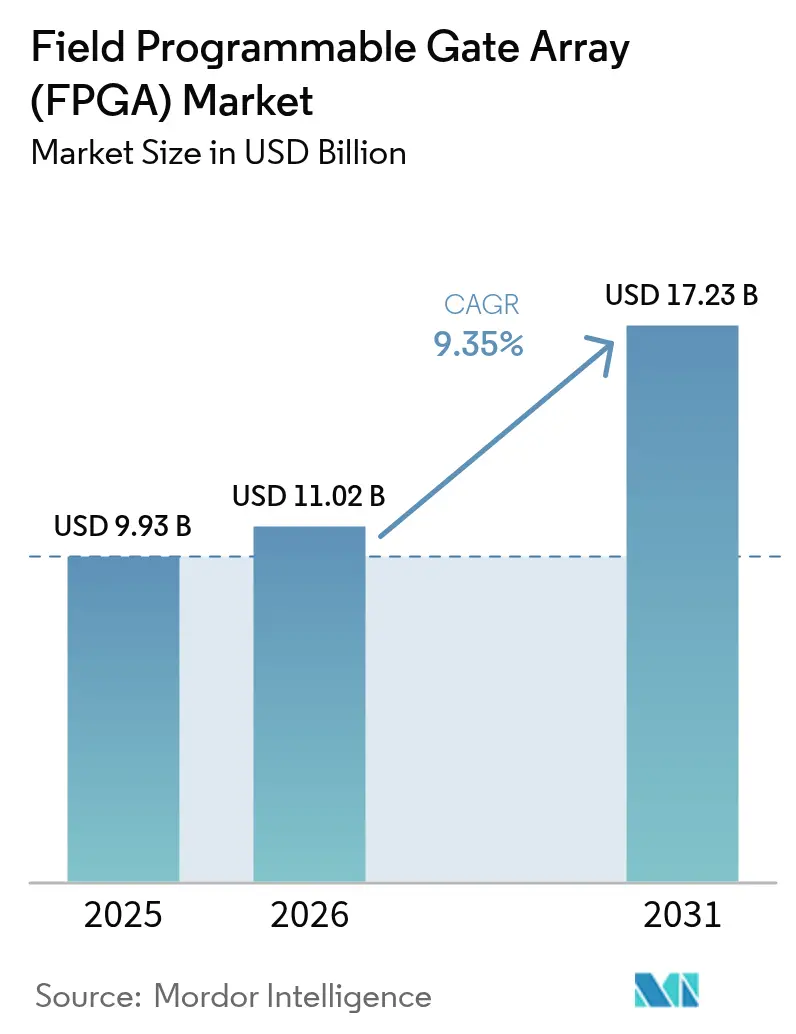

| Market Size (2026) | USD 11.02 Billion |

| Market Size (2031) | USD 17.23 Billion |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Field Programmable Gate Array (FPGA) Market Analysis by Mordor Intelligence

The Field programmable gate array (FPGA) market size is expected to increase from USD 9.93 billion in 2025 to USD 11.02 billion in 2026 and reach USD 17.23 billion by 2031, growing at a CAGR of 9.35% over 2026-2031. Demand is shifting toward reconfigurable logic as cloud operators refine AI inference pipelines, mobile-network providers scale 5G Open RAN overlays, and automakers adopt software-defined powertrains. Vendors that master chiplet integration at 7-nanometer nodes are widening performance per watt advantages at the high end, while flash-based devices keep expanding in industrial and automotive designs that require instant-on operation. Supply risk linked to export controls has spurred indigenous innovation in China, yet it has also tightened Western inventories, allowing premium pricing on advanced parts. Competitive differentiation now hinges more on tool-chain ease of use and certified IP cores than on raw logic density alone.

Key Report Takeaways

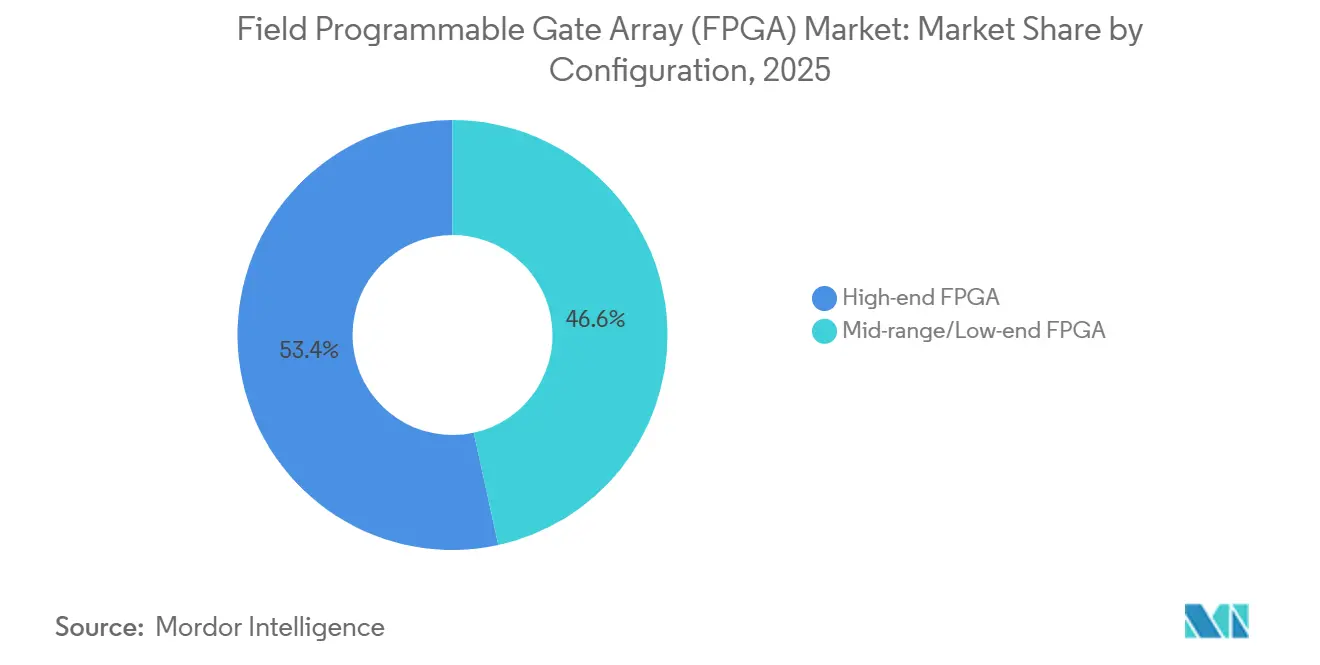

- By configuration, high-end FPGAs led with 53.41% of revenue in 2025, mid-range and low-end devices are projected to expand at an 11.80% CAGR through 2031.

- By architecture, SRAM-based designs captured 71.23% of share in 2025, flash-based alternatives are progressing at a 9.47% CAGR to 2031.

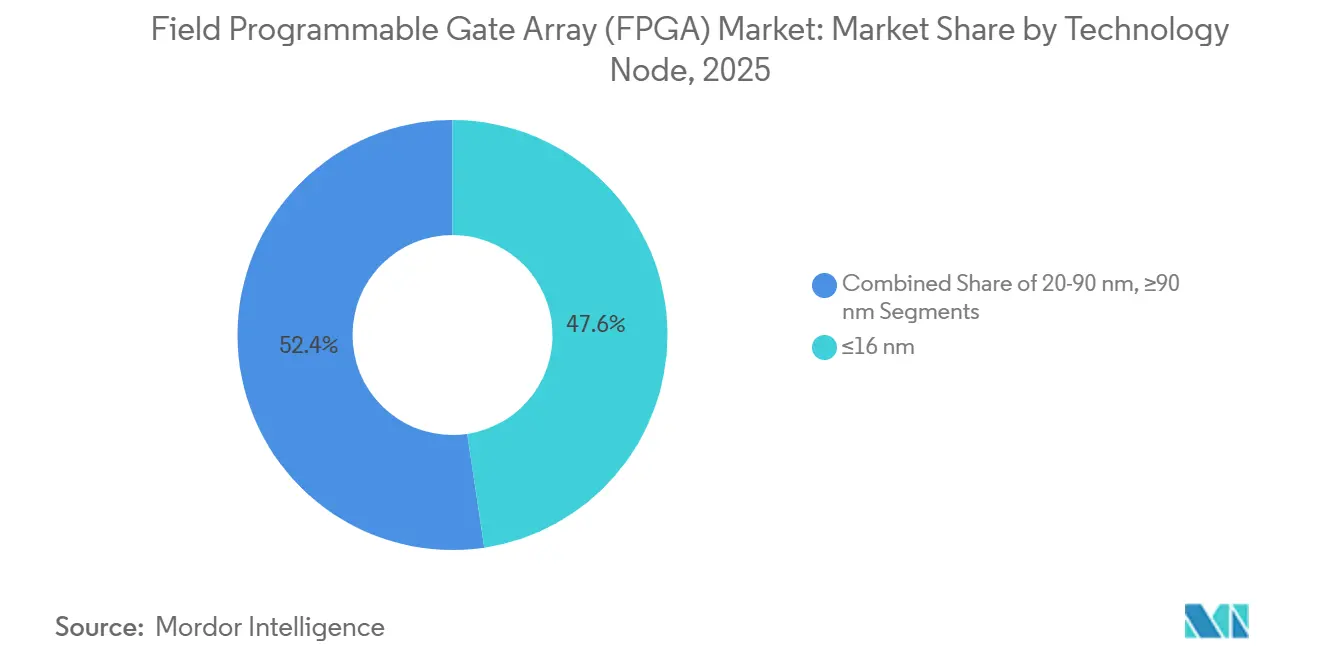

- By technology node, sub-16-nanometer shipments represented 47.64% volume in 2025,that cohort is expected to advance at a 12.71% CAGR between 2026-2031.

- By end market, automotive applications are forecast to grow at 12.88% during 2026-2031, the fastest among all verticals, data centers retained the largest slice at 35.92% of 2025 demand.

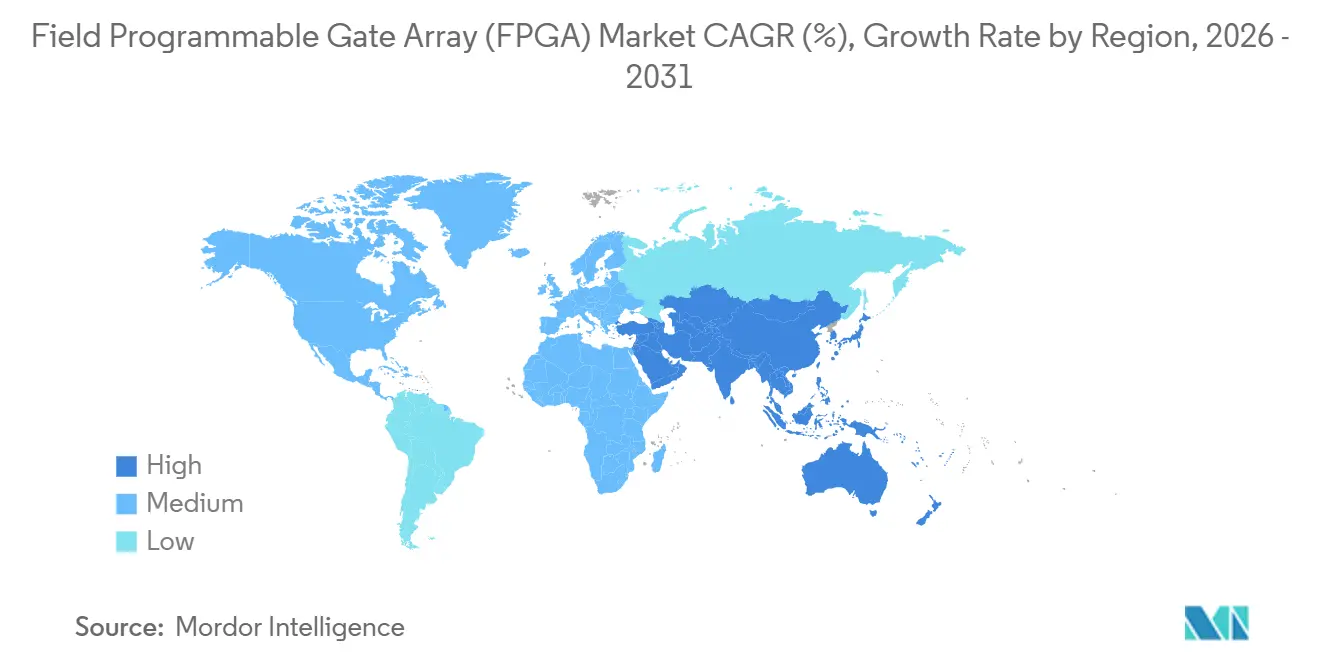

- By geography, Asia-Pacific accounted for 46.83% revenue in 2025 and should post an 11.49% CAGR through 2031, North America and Europe jointly contributed nearly 46% of 2025 spending, buoyed by hyperscale and defense programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Field Programmable Gate Array (FPGA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge-AI Inference Demand in Hyperscale Data Centers | +2.1% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| 5G ORAN Shift Requiring Re-programmable Logic in Radios | +1.8% | Global, with early adoption in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Rapid Prototyping Needs for ASIC/SoC Shrink Cycles (≤ 7 nm) | +1.5% | Global, led by North America and Asia-Pacific design hubs | Medium term (2-4 years) |

| Functional Safety Compliance in Automotive (ISO 26262) | +1.4% | Global, strongest in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Radiation-Tolerant Designs for New-Space Constellations | +0.9% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Chinese EV Power-train OEMs Adopting eFPGAs for Motor Control | +0.7% | Asia-Pacific, primarily China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Edge-AI Inference Demand In Hyperscale Data Centers

Operators keep replacing fixed-function accelerators with reconfigurable fabric that can adjust to evolving quantization, pruning, and sparsity techniques in foundation models. Microsoft Azure’s Maia 200 integrates adaptive compute tiles to handle dynamic batching and model rotation tasks that would otherwise require a hardware refresh.[1]Microsoft Azure, “Maia 200 AI accelerator integrates adaptive compute,” azure.microsoft.com IBM validated a similar approach when its Spyre platform paired POWER10 with Agilex-7 devices, reaching sub-millisecond latency on fraud-detection pipelines. Regional data sovereignty mandates in the European Union and India favor locally hosted inference nodes, prompting cloud builders to adopt FPGAs that can be retargeted for country-specific compliance logic. As generative AI frameworks iterate on a quarterly cadence, the Field programmable gate array (FPGA) market benefits from reduced risk of silicon obsolescence. Tool-chain enhancements that expose high-level compilers to data-scientists further accelerate adoption.

5G ORAN Shift Requiring Re-programmable Logic In Radios

Open RAN architects rely on FPGAs to implement continually evolving fronthaul interfaces while supporting dynamic spectrum sharing, massive MIMO, and low-latency beam steering. Rakuten Mobile’s commercial launch validated Agilex-7 throughput at 100 Gbps eCPRI.[2]Intel, “Agilex FPGA enables Rakuten Open RAN,” intel.com MaxLinear’s Sierra platform mixes embedded ARM cores with mid-range fabric so operators can cover sub-6 GHz and millimeter-wave bands on one hardware bill of materials. Qualcomm added eFPGA blocks to its X100 accelerator, signaling migration of reconfigurable logic onto single dies. These deployments shorten radio replacement cycles from five years to in-place software upgrades, expanding the Field programmable gate array (FPGA) market footprint across macro-cell and small-cell equipment.

Rapid Prototyping Needs For ASIC/SoC Shrink Cycles

Mask costs at 5 nm surpass USD 50 million per tape-out, so design teams run early-stage verification on high-end FPGAs, trimming bring-up time by half. Alchip documented an eight-month reduction for a customer emulating a 5 nm AI processor. [3]Alchip Technologies, “2024 annual report,” alchip.com AMD’s Versal Premium with integrated 112 Gbps transceivers allows chiplet developers to test Universal Chiplet Interconnect Express links in-situ before committing to silicon. The ability to toggle configuration images in minutes rather than redo wafers in months sharpens the Field programmable gate array (FPGA) market edge within semiconductor IP development flows, especially where safety or security testing demands exhaustive corner-case coverage impossible on early silicon.

Functional Safety Compliance In Automotive (ISO 26262)

Vehicle platforms are consolidating dozens of electronic control units into zonal and domain controllers that must meet ASIL-D reliability targets. Flash-based PolarFire SoCs guarantee deterministic boot within microseconds, avoiding the vulnerability window of SRAM architectures in fail-operational systems. GOWIN’s GW5A-25 earned TÜV SÜD certification, giving automakers a domestically sourced component for body electronics. Cadence tools automate safety monitor insertion, reducing certification effort by roughly one-third. As electric vehicles grow software content, over-the-air updates require hardware redundancy that reconfigurable logic supplies, broadening the Field programmable gate array (FPGA) market appeal among tier-1 suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| US-EU Export Controls on High-performance FPGAs to China | -1.6% | Global, most acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Volatility in 300 mm Foundry Capacity Allocation | -1.2% | Global, concentrated in Asia-Pacific foundry ecosystems | Medium term (2-4 years) |

| Higher Static Power Consumption vs. Dedicated ASIC | -0.8% | Global, particularly in data center and automotive use | Long term (≥ 4 years) |

| High Licensing Costs for Proprietary Design Toolchains | -0.6% | Global, affecting small and medium enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

US-EU Export Controls On High-performance FPGAs To China

Rules enacted in October 2024 block devices with bandwidth above 600 GBps or over 1 000 DSP slices, removing Versal Premium and Agilex 9 from Chinese catalogs. AMD’s 2024 annual filing flagged a USD 400 million revenue gap because of the restrictions. The European Union mirrored restrictions in January 2025, increasing license complexity. Chinese OEMs accelerated domestic procurement, pushing combined shipments from GOWIN, Anlogic, and Pango to 2.3 million units in 2025. While the policy constrains near-term growth, it also stimulates regional alternatives, fragmenting the Field programmable gate array (FPGA) market landscape.

Volatility In 300 mm Foundry Capacity Allocation

Leading foundries channel capital to smartphone processors and AI GPUs, leaving fewer wafers for programmable logic. TSMC earmarked 65% of its USD 40 billion 2025 capital plan for 3 nm and 5 nm expansions, pushing 16 nm lines to 85% utilization and adding 16-week lead times. Intel Foundry Services reserved 20% of Arizona Fab 52 for its own FPGA business, shrinking external access and forcing smaller vendors to seek higher-priced slots at GlobalFoundries or UMC. Supply swings inflate average selling prices and compel OEMs to dual-source designs, slowing conversion cycles and dampening the Field programmable gate array (FPGA) market CAGR in mid-range and low-end tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Configuration: High-end Dominance, Cost-optimized Momentum

High-end devices captured 53.41% of 2025 revenue, anchored by data-center acceleration cards and 5G radio units that require massive parallelism and multi-hundred-gigabit transceivers. Vendors command premium pricing because hardened Ethernet, PCIe Gen5, and AES-256 engines reduce board-level parts count, lowering total solution cost despite higher device ASPs. Automotive adoption of adaptive compute acceleration platforms for advanced driver-assistance systems sustains volume at leading nodes, while aerospace customers rely on radiation-tolerant siblings. The Field programmable gate array (FPGA) market thus continues to treat flagship fabric as strategic infrastructure.

Mid-range and low-end categories are gaining volume at an 11.80% CAGR through 2031. Flash-based architectures with sub-1-watt power draw fit machine-vision gateways, predictive-maintenance sensors, and automotive camera modules, enabling local AI inference within tight thermal envelopes. Lattice’s CertusPro-NX and other instant-on parts offer logic density sufficient for sensor fusion while shrinking bill-of-materials costs. EU biometrics rules favor on-device processing, further lifting demand. As learning curves flatten and pre-validated IP libraries expand, cost-sensitive sectors bring new entrants into the Field programmable gate array (FPGA) market, diversifying revenue away from hyperscale customers.

By Architecture: SRAM Hegemony, Flash Resilience

SRAM-based designs held 71.23% share in 2025, reflecting deep IP ecosystems, high logic density, and mature high-level synthesis flows that map data-center AI kernels with minimal RTL intervention. Quartus Prime and Vitis tool suites streamline C++ and Python workloads, cutting adoption friction for software teams. Telecom operators favor SRAM FPGAs for fronthaul baseband and network slicing since extra watts are offset by 5G capacity gains.

Flash-based fabric is advancing at 9.47% through 2031 as deterministic boot times, single-event-upset immunity, and lower standby leakage align with functional-safety and industrial control mandates. Microchip’s PolarFire SoC integrates a RISC-V cluster that boots immediately after power restoration, protecting safety-critical zones such as steering and braking. Radiation-hardened anti-fuse parts stay niche but vital in space payloads that must survive >300 kRad doses, sustaining a specialized slice of the Field programmable gate array (FPGA) market size even if unit shipments remain modest.

By Technology Node: Leading-edge Acceleration

Sub-16-nanometer devices accounted for 47.64% of 2025 volume and are forecast to climb at 12.71% CAGR. Chiplets stitched together with 2.5D silicon interposers allow high-bandwidth memory stacks to share a single package with logic dies, delivering terabyte-per-second throughput for LLM serving. Agilex 5 adds Embedded Multi-die Interconnect Bridge channels, proving heterogeneous integration at commercial scale. Lower dynamic power per logic element lets hyperscalers densify accelerator racks without breaching datacenter cooling envelopes, strengthening demand inside the Field programmable gate array (FPGA) market.

Mature 20-90 nm nodes persist in industrial drives, medical imaging, and avionics where qualification cycles outlast process innovation. Stable supply, lower mask costs, and integrated analog peripherals make these nodes attractive despite bigger die footprints. Devices at ≥90 nm remain indispensable in defense systems that prioritize one-time-programmable security and 15-year support contracts. Consequently, the Field programmable gate array (FPGA) market share of legacy nodes erodes slowly, cushioning vendors against foundry demand swings.

By End Market: Automotive Velocity

Data centers generated 35.92% of 2025 revenue, with hyperscale spending on AI inference, smart-NICs, and network function virtualization absorbing high-end parts. Automotive demand, however, is projected to be the fastest grower at 12.88% CAGR, as over-the-air upgrade strategies and zonal electronics pivot hardware toward reconfigurable logic to avoid multiple microcontroller versions. Telecommunications stays the second-largest application by value, with Open RAN and private-5G small cells deploying programmable fabric for protocol agility. Industrial automation, robotics, and medical equipment broaden the Field programmable gate array (FPGA) market size by embedding flexible signal-processing pipelines that adapt to future-proof connectivity standards.

Aerospace and defense secure long-term contracts for anti-fuse and radiation-hard FPGAs in satellite payloads and radar. Consumer wearables adopt low-power fabric for sensor aggregation in augmented-reality glasses and smartwatches. Test and measurement vendors integrate programmable logic to lengthen instrument lifespans via firmware updates. Collectively, these verticals diversify the Field programmable gate array (FPGA) market and mitigate dependence on hyperscale capex cycles.

Geography Analysis

Asia-Pacific led with 46.83% revenue in 2025 and will likely sustain an 11.49% CAGR. Chinese firms shipped 2.3 million domestic units after export controls, taking 12% regional share despite node limitations. India’s rollout of 150 000 Open RAN radios in 2025, under a Production-Linked Incentive scheme, pulled in Agilex 7 and Versal AI Edge boards to process fronthaul and beamforming workloads. Japan’s automakers embedded flash-based PolarFire SoCs into electric-vehicle zone controllers, compensating for ASIL-D complexity with instant-on performance. These dynamics ensure the Field programmable gate array (FPGA) market remains anchored in Asia even as geopolitical factors reshape supply deep inside the region.

North America supplied roughly 28% revenue in 2025, propelled by hyperscale AI investment and defense modernization that mandates U.S.-origin parts. The Department of Defense selected radiation-tolerant fabric for satellite communications and unmanned platforms, underpinning multi-year procurement visibility. Silicon Valley start-ups embrace eFPGA IP blocks for custom SoCs, reinforcing domestic design-service revenue streams. As tool-chains converge on oneAPI and Python front-ends, North American customers unlock greater code portability between CPUs, GPUs, and reconfigurable logic, expanding the Field programmable gate array (FPGA) market adoption base.

Europe contributed about 18% of 2025 spending, with Germany, France, and Italy foregrounding automotive electrification and factory automation. The Chips Act earmarked EUR 43 billion for semiconductor subsidies, including FPGA pilot lines expected post-2027. Industrial machinery manufacturers integrate Time-Sensitive Networking capabilities, leaning on deterministic latency in flash-based devices. Space agencies contracted PolarFire radiation-hardened variants for the Galileo constellation, bolstering regional supply security. South America, the Middle East, and Africa combined for under 8% share, yet infrastructure modernizations in telecom and oil-field automation keep the Field programmable gate array (FPGA) market footprint global.

Competitive Landscape

AMD and Intel jointly controlled roughly 55-60% of 2025 revenue, but the market remains only moderately concentrated as new entrants leverage national subsidies and IP licensing. AMD bundles Versal ACAP with EPYC CPUs under the Vitis platform, letting data-scientists deploy AI kernels in high-level languages and shortening dev cycles by nearly half. Intel positions oneAPI across CPUs, GPUs, and FPGAs, enabling code reuse and easing workload migration for cloud-native developers. These ecosystem investments raise switching costs and defend margins even while unit prices face discount pressure.

Lattice Semiconductor dominates low-power edge niches using sub-1-watt instant-on fabric and Arm cores, unlocking design wins in camera modules and IoT gateways that attract less interest from larger rivals. Chinese suppliers undercut headline pricing by up to 30%, leveraging domestic sourcing mandates, yet process lag at 28 nm narrows their appeal to industrial and automotive edge boards. eFPGA licensors Flex Logix and Achronix penetrate automotive radar and base-band ASICs, sidestepping the board-level cost and latency of discrete components. This strategy diversifies the Field programmable gate array (FPGA) market toward IP-centric business models.

Strategic moves revolve around vertical integration, geographic risk mitigation, and regulatory compliance. Intel expanded a design center in Malaysia to rebalance supply lines away from China. AMD completed socket-level integration of Versal fabric with EPYC processors, slashing data movement latency by 60% in inference workloads. Microchip secured a USD 150 million ESA contract for Galileo navigation satellites, showing that space-grade orders reward certified radiation tolerance. As functional-safety and cybersecurity certifications grow decisive, vendors offering pre-validated libraries can shave 6-12 months from automotive qualification schedules, providing critical time-to-market leverage in the Field programmable gate array (FPGA) market.

Field Programmable Gate Array (FPGA) Industry Leaders

Advanced Micro Devices, Inc.

Lattice Semiconductor Corporation

QuickLogic Corporation

Intel Corporation

Achronix Semiconductor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Intel Corporation announced a USD 300 million expansion of its Penang, Malaysia, FPGA design center, adding 500 engineers to focus on Agilex 9 and Open RAN reference designs.

- January 2026: AMD finalized integration of Versal ACAP into the EPYC 9005 roadmap, enabling same-socket heterogeneous computing for latency-sensitive inference tasks.

- December 2025: Lattice Semiconductor and Arm Holdings pre-integrated Cortex-M33 processors into CertusPro-NX fabric to target ultra-low-power industrial and automotive gateways.

- November 2025: Microchip Technology won a USD 150 million European Space Agency contract for radiation-hardened PolarFire FPGAs destined for Galileo Second Generation satellites.

Global Field Programmable Gate Array (FPGA) Market Report Scope

FPGAs are prefabricated silicon instruments that can be electrically programmed in the field to become almost any type of digital circuit or system. They are an array of configurable logic blocks (CLBs) linked together by programmable interconnects. After manufacturing, they can be reprogrammed to meet the needs of the desired application or functionality.

The Field Programmable Gate Array Report is Segmented by Configuration (High-end FPGA, Mid-range/Low-end FPGA), Architecture (SRAM-based, Flash-based, Anti-fuse), Technology Node (≥90 nm, 20-90 nm, ≤16 nm), End Market (Data Center, Telecommunications, Automotive, Industrial, Aerospace, Consumer, Medical), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Value (USD).

| High-end FPGA |

| Mid-range/Low-end FPGA |

| SRAM-based FPGA |

| Flash-based FPGA |

| Anti-fuse FPGA |

| ≥90 nm |

| 20-90 nm |

| ≤16 nm |

| Data Center and Cloud Computing |

| Telecommunications and 5G Infrastructure |

| Automotive (ADAS, Electrification) |

| Industrial Automation and Robotics |

| Aerospace and Defense (Avionics, SATCOM) |

| Consumer Electronics and Wearables |

| Test, Measurement and Medical Devices |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Configuration | High-end FPGA | |

| Mid-range/Low-end FPGA | ||

| By Architecture | SRAM-based FPGA | |

| Flash-based FPGA | ||

| Anti-fuse FPGA | ||

| By Technology Node | ≥90 nm | |

| 20-90 nm | ||

| ≤16 nm | ||

| By End Market | Data Center and Cloud Computing | |

| Telecommunications and 5G Infrastructure | ||

| Automotive (ADAS, Electrification) | ||

| Industrial Automation and Robotics | ||

| Aerospace and Defense (Avionics, SATCOM) | ||

| Consumer Electronics and Wearables | ||

| Test, Measurement and Medical Devices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the Field programmable gate array (FPGA) market?

The market stood at USD 9.93 billion in 2025 and is projected at USD 11.02 billion for 2026.

Which vertical will grow fastest for FPGAs over 2026-2031?

Automotive electronics, led by advanced driver-assistance and battery-management units, is forecast to expand at 12.88% CAGR.

Why are hyperscalers favoring FPGAs for AI inference?

Reconfigurable logic adapts to evolving model architectures without the re-spin costs of ASICs, delivering sub-millisecond latency in dynamic workloads.

How will export controls affect global FPGA supply?

Restrictions on high-performance parts to China limit near-term shipments but also stimulate domestic alternatives, adding regional diversity to supply chains.

Which architecture is gaining share in functional-safety designs?

Flash-based FPGAs offer instant-on operation and single-event-upset resilience, making them attractive for ASIL-D automotive zones and industrial control loops.

What manufacturing node captures nearly half of today’s FPGA shipments?

Processes at or below 16 nm comprised 47.64% of 2025 volume, driven by data-center and 5G radio deployments.

Page last updated on: