Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 34.66 Billion |

| Market Size (2031) | USD 46.91 Billion |

| Growth Rate (2026 - 2031) | 6.26% CAGR |

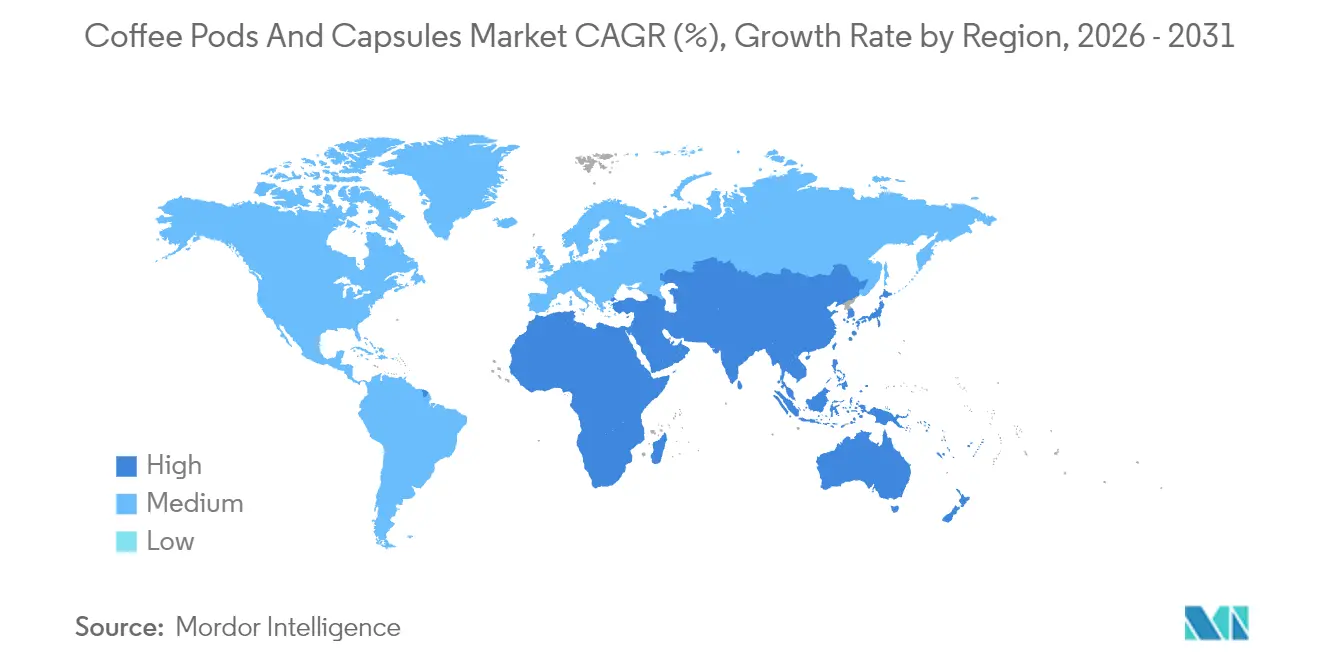

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

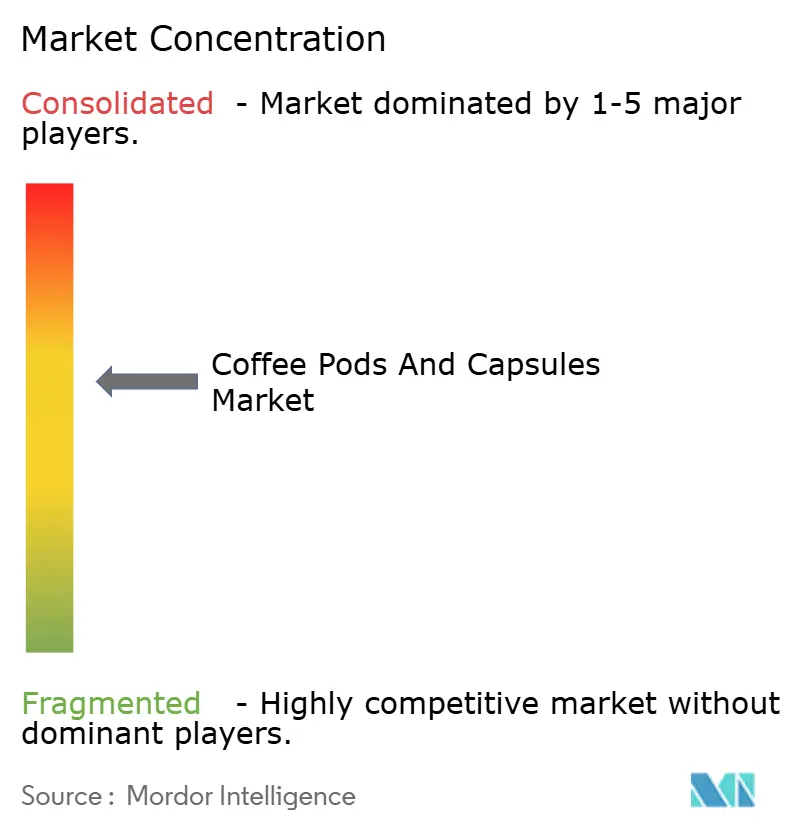

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coffee Pods And Capsules Market Analysis by Mordor Intelligence

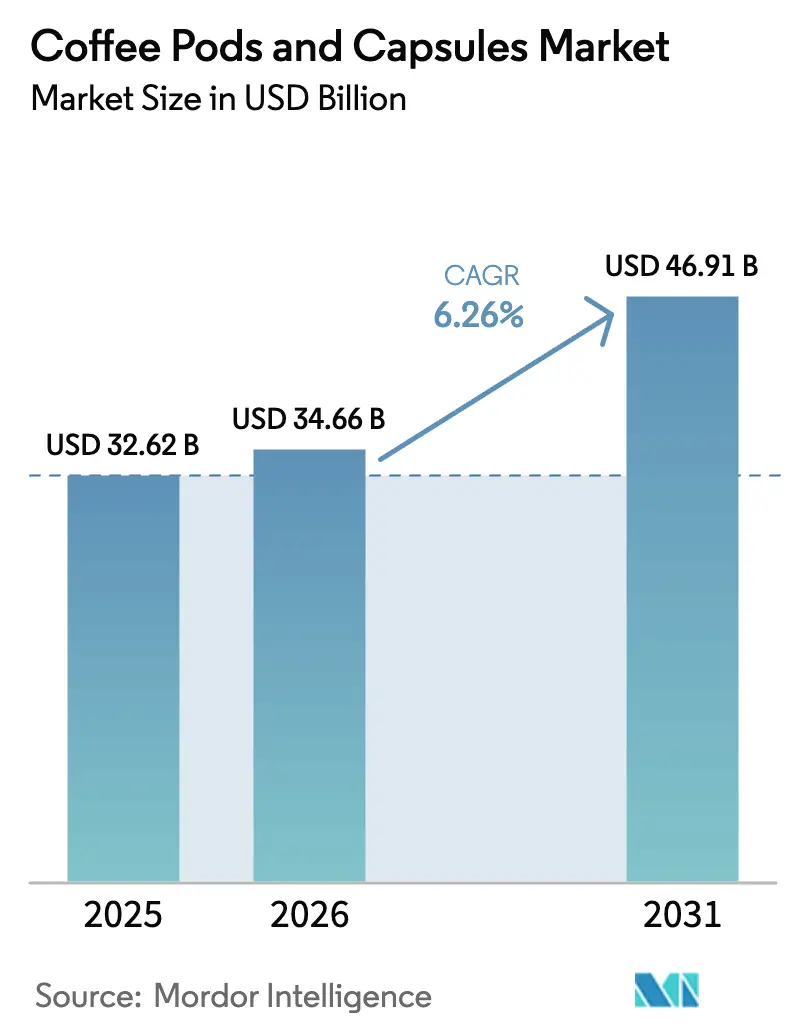

The coffee pods and capsules market size is expected to grow from USD 32.62 billion in 2025 to USD 34.66 billion in 2026 and is forecast to reach USD 46.91 billion by 2031 at 6.26% CAGR over 2026-2031. Driven by a surge in household demand for premium coffee, a swift expansion of machine installations, and private-label initiatives from retailers, the market is witnessing notable growth. The increasing preference for convenience and high-quality coffee products among consumers has further fueled this demand. As premiumization aligns with sustainability, product innovation is increasingly leaning towards specialty blends and eco-friendly formats, such as recyclable pods and biodegradable packaging. In response to stringent regulations and a commitment to flavor integrity, companies are turning to aluminum and compostable solutions, which not only meet environmental standards but also preserve the quality of the coffee. While global brands are actively seeking alliances, mergers, and acquisitions to bolster their scale and counter the challenge posed by nimble newcomers, the competitive intensity remains at a moderate level, with established players focusing on maintaining their market share and shelf presence.

Key Report Takeaways

- By product type, capsules led with 51.88% share in 2025, while pods are projected to grow at a 6.63% CAGR through 2031.

- By category, conventional coffee commanded an 82.96% share in 2025; organic variants are advancing at a 7.29% CAGR to 2031.

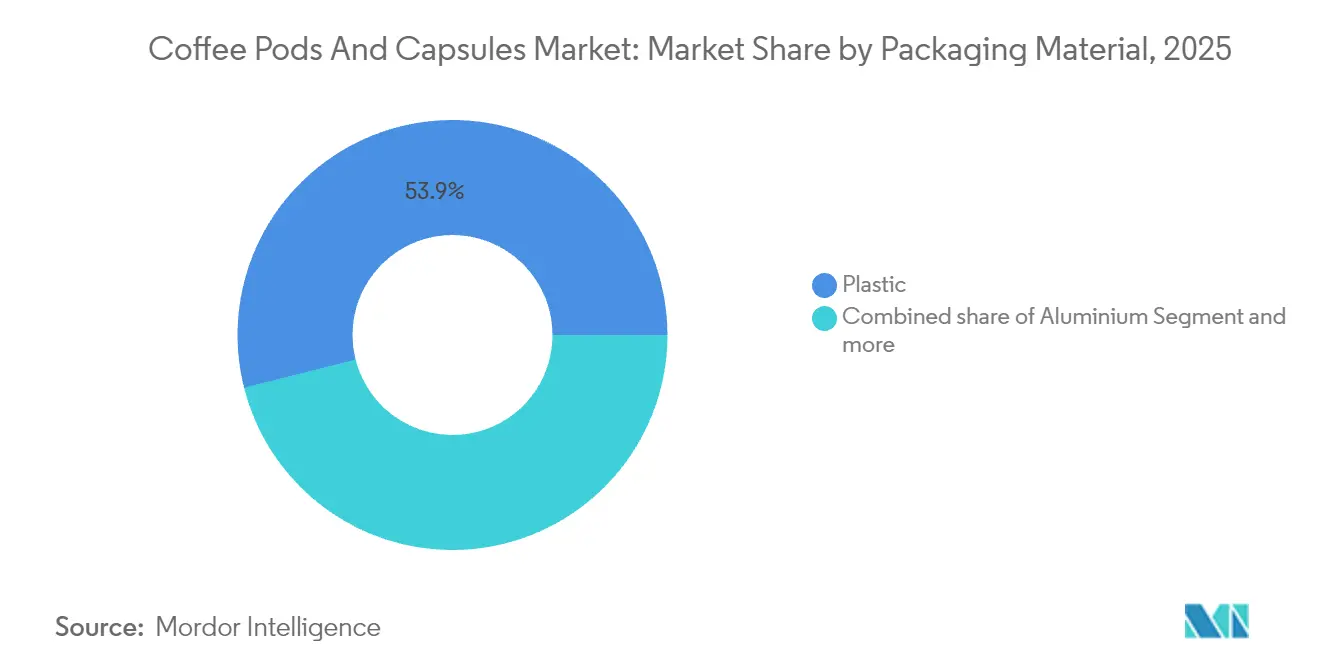

- By packaging material, plastic retained a 53.94% share in 2025, whereas aluminum formats are set to expand at a 6.82% CAGR to 2031.

- By distribution channel, off-trade accounted for a 62.35% share in 2025; on-trade is forecast to log a 6.61% CAGR between 2026-2031.

- By geography, Europe captured a 36.21% share in 2025, while Asia-Pacific is expected to post the fastest 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coffee Pods And Capsules Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation and demand for specialty single-serve coffee | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing Household consumption | +1.5% | Global, with early gains in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Rapid expansion of closed-system machine install base | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Mainstream retailers adding private-label capsules | +0.9% | North America and Europe, expanding to Latin America | Short term (≤ 2 years) |

| Patented compostable pod materials reaching commercial scale | +0.6% | EU regulatory zones, expanding globally | Long term (≥ 4 years) |

| Corporate Scope-3 mandates driving office-coffee capsule demand | +0.5% | North America and EU corporate hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization and demand for specialty single-serve coffee

Driven by consumers' willingness to pay a premium for specialty coffee experiences, the market is expanding beyond its traditional commodity roots. This trend is evident as artisanal roasters team up with capsule manufacturers, introducing limited-edition flavors that fetch a 30-40% premium over standard offerings. These collaborations not only enhance product differentiation but also cater to a growing segment of consumers seeking unique and high-quality coffee experiences. A prime example is Nestlé's partnership with Starbucks, which not only capitalizes on brand equity to support higher price points but also broadens its market reach beyond conventional coffeehouses. By leveraging Starbucks' established reputation and Nestlé's distribution network, this collaboration has successfully tapped into the premium coffee segment. This wave of premiumization not only fortifies established players' competitive edges but also paves the way for craft coffee brands to venture into the single-serve arena, offering them a platform to compete with larger players. Furthermore, the pivot towards specialty offerings is spurring technological advancements in brewing systems, with manufacturers crafting machines that adeptly extract optimal flavors from these premium coffee blends. These innovations aim to enhance the consumer experience by ensuring that the quality of specialty coffee is preserved and maximized during the brewing process.

Increasing household consumption

As remote work cements its place in corporate culture, home coffee consumption is on the rise, shifting demand from commercial outlets to residential homes. Globally, coffee consumption jumped by 5% year-over-year, outstripping the 3% growth seen in the U.S. This trend is evident in 11 out of 12 major countries, highlighting a widespread shift in consumer behavior. The shift underscores a growing appetite for at-home brewing solutions that match coffeehouse standards, driven by the increasing time spent at home and the desire for premium coffee experiences without leaving the house. Households are increasingly favoring pod-based systems over traditional methods, drawn by their consistency, convenience, and quicker preparation times. This transition from commercial to home consumption is prompting a rethink in supply chains and a push for packaging innovations, now tailored for retail rather than bulk foodservice. Additionally, manufacturers are focusing on enhancing product offerings to cater to evolving consumer preferences, such as eco-friendly pods and customizable brewing options.

Rapid expansion of closed-system machine install base

Proprietary brewers, bolstered by hardware subsidies, are locking consumers into compatible capsules, ensuring a steady and predictable revenue stream for manufacturers. Keurig's K-Round platform, leveraging CoffeeB's compostable technology, not only showcases the growth of a machine-led ecosystem but also addresses environmental concerns by reducing waste and promoting sustainability. This approach highlights the industry's focus on balancing innovation with ecological responsibility while catering to consumer demand for environmentally friendly products. The swiftest gains in the install base are observed in the urbanizing markets of Asia-Pacific, driven by increasing disposable incomes, rapid urbanization, and a growing preference for convenient, premium coffee solutions that align with evolving consumer lifestyles, environmental awareness, and the desire for high-quality, sustainable products.

Mainstream retailers adding private-label capsules

These private-label products cater to environmentally conscious consumers, aligning with the growing demand for eco-friendly packaging solutions. Additionally, these offerings allow supermarkets to differentiate themselves in a competitive market by addressing sustainability concerns. Meanwhile, contract packers like Euro Caps churn out high volumes, enabling supermarkets to offer competitive pricing and exerting pricing pressure on branded competitors. This strategy becomes particularly popular during economic downturns, as consumers prioritize value while still desiring convenience. By offering sustainable and cost-effective options, supermarkets aim to capture a larger share of the market while addressing consumer preferences for both affordability and environmental responsibility. Furthermore, the combination of sustainability and affordability helps supermarkets build brand loyalty, as shoppers increasingly favor retailers that align with their values.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-grade refill capsules | -0.8% | Global, with concentration in price-sensitive markets | Short term (≤ 2 years) |

| Intensifying pushback on single-use plastics | -0.6% | EU regulatory zones, expanding to North America | Medium term (2-4 years) |

| Aluminium price volatility squeezing margins | -0.4% | Global packaging supply chains | Short term (≤ 2 years) |

| EU "Right-to-Repair" rules threatening machine lock-in | -0.3% | European Union member states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and low-grade refill capsules

Unauthorized refills undermine brand trust and diminish cup quality. Testing by SGS revealed a 10% mislabeling rate in products labeled as “100% Arabica,” highlighting significant authenticity concerns. Such mislabeling not only misleads consumers but also poses risks to the reputation of premium coffee brands. While budget-friendly imitations attract price-sensitive consumers, they risk damaging machines and altering taste profiles, leading to potential long-term dissatisfaction among users. In a bid to safeguard their intellectual property, brands are turning to QR codes and pursuing legal actions. QR codes allow consumers to verify product authenticity, while legal actions aim to deter counterfeiters. However, enforcing these measures proves difficult in the fragmented landscape of retail, where counterfeit products often circulate through complex and unregulated supply chains.

Intensifying pushback on single-use plastics

The production of billions of plastic pods annually, with only a small percentage being recycled, fuels consumer outrage amid rising environmental concerns and heightened awareness of plastic waste's ecological impact. In response, EU directives strongly advocate for compostable formats, compelling manufacturers to overhaul their material choices to align with stringent sustainability goals and regulatory compliance. This shift necessitates substantial changes in supply chains as they adapt to incorporate new polymers, requiring investments in research, development, and infrastructure upgrades. These rising transition costs place considerable pressure on profit margins, a challenge that is expected to persist until production volumes reach economies of scale, enabling cost efficiencies and broader adoption of sustainable materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Capsules lead through convenience innovation

In 2025, capsules dominated the global coffee pods and capsules market, capturing 51.88% of the segment. Their airtight design not only preserves the coffee's aroma but also ensures precise dosing for each brew. The growth of the capsule segment is closely linked to the rising demand for single-serve coffee machines. Manufacturers are now focusing on making their products compatible with these machines and developing proprietary extraction profiles to enhance flavor consistency. Innovations in capsule materials are also noteworthy; for instance, Keurig recently introduced compostable K-Rounds, moving away from traditional plastic casings, showcasing the industry's shift towards eco-friendliness. In commercial settings, hard pods are preferred for their durability during high-volume use, while households lean towards capsules for their convenience and prolonged freshness. The competitive landscape is driven by technological innovations and brand differentiation, with companies aiming to elevate the coffee experience, irrespective of the hardware used.

On the other hand, coffee pods are the fastest-growing segment, with projections of a 6.63% CAGR through 2031. This surge is largely attributed to a growing consumer preference for sustainable options. Paper-based pods, favored by eco-conscious consumers as alternatives to plastic and aluminum, have seen a notable uptick in adoption. In response to these market shifts, manufacturers are blending the sustainability of pods with the convenience of capsules, challenging traditional category boundaries. This approach enables commercial entities to utilize hard pods for their robustness, while households are gravitating towards soft pods that align with curbside composting initiatives. Such adaptability is driving market growth, catering to both home users and foodservice establishments. Competitive strength in the pod arena is bolstered by unique extraction technologies that ensure rich flavor profiles, even as the focus on environmental responsibility grows among consumers.

By Category: Organic variants accelerate despite conventional dominance

Conventional coffee pods and capsules command a dominant 82.96% share of the global market. Their leadership is bolstered by well-established supply chains and cost advantages, making them easily accessible to both manufacturers and consumers. Thanks to extensive distribution networks and standardized production practices, these conventional options enjoy consistent availability and stable pricing across various regions. Retailers' familiarity with these formats, coupled with broad consumer acceptance, reinforces their market dominance. Major brands leverage economies of scale, simplifying operations and efficiently catering to large-scale demand. Despite rising sustainability concerns, conventional SKUs still occupy prime shelf space globally, a testament to enduring purchasing habits and competitive pricing. Furthermore, the ability of conventional coffee pods and capsules to cater to a wide range of consumer preferences, including flavor variety and compatibility with popular coffee machines, strengthens their foothold in the market. Their affordability compared to premium or niche alternatives also ensures their appeal to cost-conscious consumers, further solidifying their position.

On the other hand, organic coffee pods and capsules are the market's rising stars, with projections pointing to a robust 7.29% CAGR, outpacing the overall market growth. While organic SKUs hold a smaller slice of the market, their premium pricing bolsters supplier margins, even at reduced volumes. Certifications like Fair Trade and Rainforest Alliance not only foster consumer trust but also align with retailer sourcing policies, boosting organic products' visibility. In Europe, regulatory backing and clear labeling amplify awareness and accessibility of organic offerings. Take Starbucks, for instance: with 98.2% of its beans sourced through C.A.F.E. Practices, the brand's sustainability commitment directly enhances its market value. However, operational challenges, like supply segregation and certification audits, pose entry hurdles, benefiting established players adept in compliance. Moreover, a surge in health consciousness across the Asia-Pacific is expanding the audience for chemical-free, single-serve coffee, propelling the organic segment's growth. The increasing demand for transparency in product sourcing and the growing preference for environmentally friendly packaging further contribute to the segment's expansion. Additionally, the ability of organic coffee pods and capsules to cater to niche markets, such as vegan or allergen-free consumers, enhances their appeal and positions them as a premium choice for health-conscious buyers.

By Packaging Material: Aluminum gains amid sustainability transition

Plastic formats dominate the coffee pods and capsules market, commanding 53.94% of sales. Their lead is primarily due to cost efficiency and swift manufacturing, making them the preferred choice for many producers. These advantages facilitate large-scale production and affordability, resonating with both manufacturers and consumers. The established supply chains and versatile design options further bolster plastic's widespread adoption. Even amidst rising environmental concerns, plastic's efficiency in meeting high demand cements its market stronghold, balancing performance with cost-effectiveness.

Conversely, aluminum-based coffee pods and capsules are the market's fastest-growing segment, boasting a projected CAGR of 6.82% through 2031. This surge is driven by heightened consumer awareness of aluminum's closed-loop recyclability, marking it as a sustainable packaging choice. The expanding market size for aluminum pods is also a response to regulatory pressures, pushing for recyclable materials in line with directives like the EU’s Right to Repair Directive 2024/1799. Furthermore, aluminum's superior barrier properties extend coffee freshness, reinforcing its premium market stance. Manufacturers, such as MZB-USA, are ramping up production, churning out tens of millions of Nespresso-compatible aluminum capsules yearly. Meanwhile, compostable resin alternatives are appealing to eco-conscious consumers, and as industrial composting infrastructure advances, these materials could seize a larger market share, highlighting the interplay between environmental performance and product quality.

By Distribution Channel: Off-trade dominance faces on-trade recovery

In 2025, off-trade channels dominated the coffee pods and capsules market, capturing 62.35% of total volumes. This trend mirrors a resurgence in foodservice and an expansion of workplace coffee programs, driven by corporate sustainability mandates. The rise in at-home coffee consumption, coupled with the ubiquitous presence of supermarkets and retail outlets, underpins this dominance. These off-trade channels not only provide convenience but also grant consumers easy access to a diverse array of coffee pods and capsules. Online subscriptions have further strengthened this segment, fostering repeat purchases and enticing customers with exclusive product launches. The broad availability of coffee products in retail spaces cements off-trade channels as the go-to choice for many, reinforcing their market leadership. Additionally, the stability and scale of these channels offer manufacturers reliable distribution and revenue streams.

On the other hand, on-trade channels are emerging as the fastest-growing segment, projected to grow at a 6.61% CAGR. This growth is fueled by cafés, offices, and hotels upgrading their coffee equipment, coinciding with a resurgence in travel and corporate activities. As businesses invest in premium brewing technologies to elevate experiences, the on-trade market size is set for a notable uptick. A prominent trend is the blending of channels: coffee shops are now retailing branded capsules directly, while grocery chains are adding in-store tasting bars, merging retail with hospitality. Brands face the challenge of synchronizing pricing and promotions across off-trade and on-trade platforms to prevent sales cannibalization and optimize market reach. Additionally, robust logistics systems are vital for balancing the intricacies of smaller e-commerce orders with larger foodservice shipments, ensuring harmonious growth across all channels.

Geography Analysis

In 2025, Europe, bolstered by its rich coffee culture and established recycling networks, commanded a dominant 36.21% share of the market. The EU Deforestation Regulation, a testament to policy leadership, incentivizes companies to maintain traceable supply chains, ensuring sustainable sourcing practices. Germany, the UK, and France stand out as primary hubs, where specialty single-serve products enjoy premium shelf space due to high consumer demand for quality and convenience. While the EU's Right-to-Repair mandates might challenge machine exclusivity by allowing third-party repairs, they simultaneously pave the way for enhanced service revenue streams as companies adapt to offer maintenance and support services.

Asia-Pacific is poised to lead with a robust 7.05% CAGR through 2031. In China, urban consumers are propelling a 20% annual growth in cold-coffee adoption, driven by changing lifestyles and preferences for ready-to-drink beverages. Nestlé is eyeing an expansion of the Starbucks capsule range into India, aiming to tap into the burgeoning middle-class demographic, which increasingly seeks premium and convenient coffee options. While Japan and South Korea ensure consistent sales due to their established coffee-drinking habits, it's the rising disposable incomes in Southeast Asia, coupled with growing urbanization, that promise significant growth opportunities for market players.

North America boasts a solid revenue foundation, thanks to the entrenched Keurig ecosystems and proactive corporate sustainability efforts. Yet, with looming plastic-waste regulations echoing European standards, suppliers are being nudged towards recyclable and compostable materials, which could reshape packaging strategies across the region. South America, while capitalizing on origin marketing to highlight the unique qualities of locally sourced coffee, grapples with income volatility that dampens the premium segment's growth, as affordability remains a concern for many consumers. In the Middle East and Africa, markets, especially in the Gulf Cooperation Council countries, are witnessing steady growth, driven by increasing Western dietary influences, a growing preference for premium coffee products, and robust household incomes that support discretionary spending.

Regulatory Landscape

In the European Union, the Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, entered into force on 11 February 2025 and applies from 12 August 2026. The regulation explicitly classifies single-serve coffee units, including soft pads/bags and rigid beverage capsules, as packaging, bringing them under packaging compliance obligations and Extended Producer Responsibility (EPR) reporting in member states.

PPWR tightens design-for-environment requirements that affect materials used in pods and capsules. Soft, permeable single-serve units must be industrially compostable under EN 13432 by 12 February 2028, and packaging must meet recyclability requirements by 2030 (with further performance expectations tied to recyclability at scale by 2035). In the United States, capsule components are regulated as Food Contact Substances under the FD&C Act. When materials are not already authorized, companies must maintain appropriate FDA Food Contact Notifications demonstrating reasonable certainty of no harm for the intended conditions of use.

Value Chain Analysis

The value chain spans green coffee sourcing (including certified and segregated organic supply), roasting and grinding, capsule and pod component manufacturing (aluminum foils, specialty plastics/biopolymers, paper filters and lidding), high-speed filling and sealing, then multi-channel distribution through off-trade retail, e-commerce subscriptions, and on-trade/office programs. Leading brands frequently combine centralized, highly automated roasting and filling with direct-to-consumer logistics and branded recycling or take-back programs, supported by vertical integration and closed-system ecosystems. Private-label growth also increases the role of contract fillers and third-party component suppliers.

Upstream, specialized component suppliers and converters shape performance and compliance by enabling barrier protection, precision dosing, and compatibility across proprietary brewers. Input costs, notably aluminum, can tighten margins. Consolidation among capsule component providers is visible as companies seek scale and R&D depth, exemplified by Datwyler acquiring a 51% stake in Capsul’Invest SA and Brain Corp SA (Capsul’in) in December 2025, and Alupak acquiring Spain-based ALUCAPS in October 2024. From 12 August 2026, EU PPWR packaging obligations and EPR reporting add new compliance workstreams across the chain, increasing emphasis on mono-material designs, recycled-content integration, and end-of-life partnerships with local collection and recycling systems.

Competitive Landscape

Top players command a moderate market concentration. Nestlé's USD 7.15 billion partnership with Starbucks amplifies its global capsule reach, seamlessly blending robust distribution with a prestigious brand. This collaboration allows Nestlé to leverage Starbucks' strong consumer loyalty while expanding its presence in the premium coffee segment. Meanwhile, JAB Holding, by consolidating assets under JDE Peet’s, aims to harness procurement synergies and bolster its bargaining stance with retailers. This strategy not only strengthens its supply chain efficiency but also enhances its ability to negotiate favorable terms with key retail partners.

Strategically, the focus is on proprietary brewers, ensuring consistent capsule purchases. Companies are not just subsidizing hardware; they're embedding in-home IoT features that track consumption and streamline re-ordering. These IoT-enabled brewers provide consumers with convenience while fostering brand loyalty through automated replenishment systems. Innovations in sustainability are emerging as pivotal competitive arenas. For instance, Keurig's CoffeeB licensing agreement empowers partners to sidestep aluminum and plastic, championing a strong waste-reduction narrative. This initiative aligns with growing consumer demand for environmentally friendly solutions, positioning Keurig as a leader in sustainable practices.

Retailers are ramping up competition with private-label capsules that mimic premium quality but at reduced prices. This move has pushed branded suppliers to amplify their research and development efforts and dive deeper into experiential marketing. By focusing on unique flavor profiles and immersive brand experiences, these suppliers aim to differentiate themselves in an increasingly crowded market. Additionally, emerging regional players are carving out niches by presenting locally sourced specialty beans in formats that align with market demands. These players capitalize on consumer preferences for authenticity and regional flavors, offering a competitive edge in specific geographic markets.

Coffee Pods And Capsules Industry Leaders

Keurig Dr Pepper Inc.

Starbucks Corporation

Nestlé SA

JAB Holding Companies

Luigi Lavazza SpA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Packaging compliance and circularity execution are creating demand for material redesign, local collection partnerships, and compliant compatible-capsule manufacturing. The EU PPWR (Regulation (EU) 2025/40), applicable from 12 August 2026, brings single-serve units under packaging rules and hard deadlines. Industrial compostability requirements for soft, permeable units by 12 February 2028 and recyclability requirements by 2030 are pushing brands and retailers to rebalance portfolios toward aluminum, compostable formats, and designs intended to fit real-world sorting and recycling systems.

Operational opportunities are also emerging around regional capacity and recycling access. In March 2026, Keurig Dr Pepper partnered with Circular Materials to accept K-Cup beverage pods in Ontario Blue Box recycling as programs transition to a peelable lid design, illustrating how EPR-linked infrastructure can expand the addressable market for recyclable single-serve formats. On the supply side, Nestle announced in July 2026 a THB 23 billion (approximately CHF 563 million) investment to build an AI-enabled Nescafe manufacturing facility and distribution center in Samut Prakan, Thailand. This supports the case for newer, regionally optimized production hubs that can support a broader mix of formats (including single-serve) and faster replenishment across domestic and export channels.

Recent Industry Developments

- June 2026: Keurig Dr Pepper announced plans to spin off its coffee business into a standalone company, temporarily named Global Coffee Co., following the April 1, 2026 close of the JDE Peet's acquisition. The structure consolidates branded pods, brewers, and licensing partnerships under a dedicated entity that can prioritize single-serve platform strategy and portfolio integration across regions.

- November 2025: Keurig launched Keurig Coffee Collective, its first branded coffee line, using a Refined Grind approach designed to increase ground density in pods. The introduction strengthens vertical participation in pod content and differentiation, adding another branded option alongside licensed offerings in the K-Cup ecosystem.

- October 2024: Alupak acquired Spain-based ALUCAPS to expand its aluminum capsule capabilities and broaden its packaging offering for single-serve coffee. The acquisition supports larger-scale supply for compatible capsules and reinforces investment into aluminum formats as sustainability and recyclability requirements tighten in key markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers portioned coffee products sold as pods and capsules that are used in compatible single serve brewers for home and out of home consumption, with revenues captured at the point of sale across channels.

Scope exclusions: It does not include coffee machines, spare parts, or non-coffee beverages sold for the same brewers.

Segmentation Overview

- By Product Type

- Pods

- Soft Coffee Pods

- Hard Coffee Pods

- Capsules

- Pods

- By Category

- Conventional

- Organic

- By Packaging Material

- Plastic

- Aluminium

- Compostable/Biodegradable

- By Distribution Channel

- On Trade

- Off Trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand context and the supply context, so the model stays tied to observable consumption and trade signals. We refer to public sources such as USDA coffee statistics, International Coffee Organization releases, UN Comtrade and national customs tables for coffee and packaging related flows, Eurostat retail and price series where relevant, and national food safety or packaging regulators for rule changes that affect materials and labeling.

To make the market model usable by geography and channel, we also review company filings, annual reports, investor presentations, and reputable press coverage for assortment, channel moves, and pricing cues. When needed, paid subscriptions for company financials and news, patent databases for packaging formats, and shipment level import export databases are used to validate assumptions on volumes and material shifts. The sources listed above are illustrative and not exhaustive, and many other references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary inputs are used to pressure test what the desk signals suggest, especially around pricing, channel mix, and how quickly new formats are replacing older ones. We spoke with a spread of stakeholders across brand owners, co-manufacturers, retailers, foodservice distributors, packaging participants, and coffee buyers, and then we balanced views across APAC, EMEA, and the Americas so one region did not over influence the global total.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 43% |

| Mid tier: 57% | Functional/Unit leaders: 36% | EMEA: 35% |

| Smaller Players: 14% | Managers: 52% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic that meet in the middle and are reconciled to one clean number. On the top-down side, coffee consumption indicators and single serve penetration signals are combined with channel splits to reconstruct the addressable demand pool for pods and capsules, and then it is converted into value using observed price ladders by format.

The model uses practical inputs that can be refreshed each year, including the installed base growth of compatible brewers, the share shift between pods and capsules, packaging material mix changes (plastic, aluminum, compostable), average pack sizes and unit counts, and on trade versus off trade share movement as home consumption patterns evolve. Where public data is thin for a country, gaps are handled using proxy markets with similar coffee culture and retail structure, followed by interview based correction.

For forecasting, scenario analysis is used and the year by year path is guided by variables that respondents consistently point to, such as pricing progression, adoption of recyclable formats, and retail and online channel expansion. Totals are then corroborated with selective bottom-up approximations like sampled assortment checks, typical unit price times estimated unit movement, and supplier side capacity commentary, and adjustments are made when the two views do not align.

Data Validation & Update Cycle

Validation is handled through triangulation across independent signals, followed by structured variance checks at region and global levels. We look for outliers such as unrealistic price jumps, sudden channel mix swings, or growth rates that are not supported by brewer penetration and retail turnover, and these items are reviewed before sign off.

Findings pass through multi step analyst reviews, and re contacts are triggered when a material mismatch appears between the model and what suppliers or channel participants report. Reports are refreshed annually, with interim updates when there are major events like regulatory shifts on packaging materials or sharp commodity driven price moves. Before delivery, an analyst performs a fresh review pass so clients receive the latest updated view.

Mordor Intelligence's Coffee Pods and Capsules Market Size Versus Other Published Estimates

Published market sizes for pods and capsules often do not match because the included formats, pricing basis, and time period assumptions vary across publishers. Some figures also mix in adjacent single serve products, or they use a different point in the value chain for revenue capture, which changes the final number.

Retail price series, format level mix shifts (pods versus capsules), and brewer installed base checks are the evidence points used to keep Mordor Intelligence aligned to pods and capsules sell-through only, with coffee machines kept outside scope and channel markups treated consistently by region.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 32.62 B (2025) | |

| Global Consultancy A | USD 43.18 B (2025) | This estimate appears to treat pods and capsules as a broader coffee segment with different revenue capture assumptions, which can pull in a wider set of single serve items and higher average selling prices. |

| Industry Research Group B | USD 40.85 B (2025) | The coverage looks similar at a high level, but differences commonly come from how out of home demand is counted, which channel pricing basis is used for value conversion, and the assumed pace of premiumization in mature markets. |

The table indicates that the main differences are driven by scope edges and pricing mechanics rather than a disagreement on underlying demand direction. When inputs are tied back to clear signals and refreshed each year, the resulting size range becomes easier to reconcile across regions and channels.

Key Questions Answered in the Report

How large is the coffee pods and capsules market in 2026?

It stands at USD 34.66 billion and is projected to reach USD 46.91 billion by 2031.

Which product type leads the segment?

Capsules lead with a 51.88% share in 2025, driven by airtight construction and machine compatibility.

What packaging material is growing fastest?

Aluminium capsules are forecast to expand at a 6.82% CAGR through 2031 as recyclability gains favor

Which region will record the highest growth?

Asia-Pacific is expected to post a 7.05% CAGR between 2026-2031 on the back of urbanization and rising incomes.

What is the key environmental trend shaping the sector?

The transition to compostable and recyclable materials is accelerating in response to regulations and consumer sustainability demands.

Page last updated on: