Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

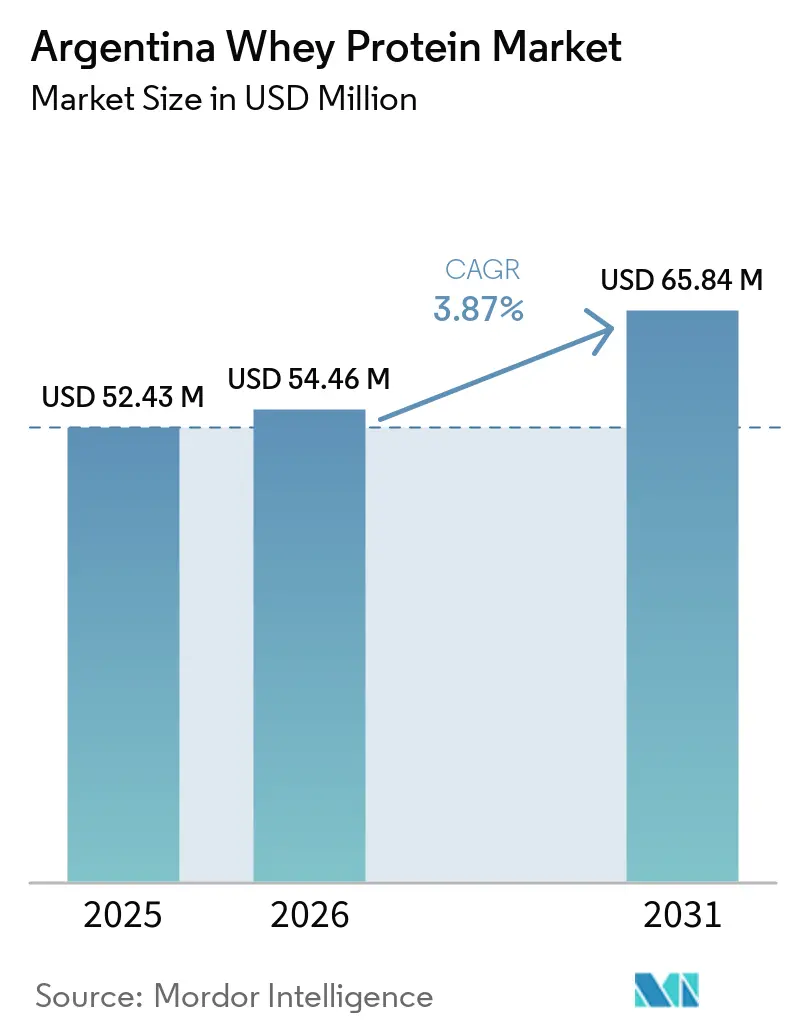

| Base Year Market Size (2025) | USD 52.43 Million |

| Market Size (2026) | USD 54.46 Million |

| Market Size (2031) | USD 65.84 Million |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

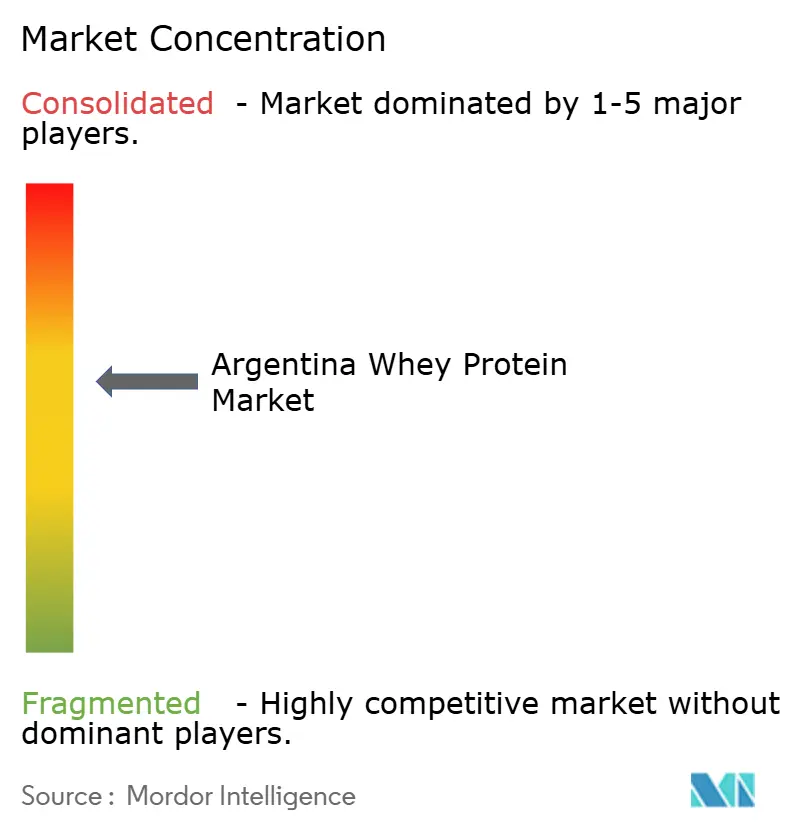

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Whey Protein Market Analysis by Mordor Intelligence

The Argentina whey protein market size is expected to grow from USD 52.43 million in 2025 to USD 54.46 million in 2026 and is forecast to reach USD 65.84 million by 2031 at 3.87% CAGR over 2026-2031. This growth trajectory is particularly noteworthy given Argentina's complex macroeconomic landscape, where the country experienced a significant inflation rate of 211.4% in 2023. While these inflationary pressures pose challenges for businesses, they simultaneously create strategic advantages for protein manufacturers who can leverage currency devaluation to enhance their market position. The market's measured expansion reflects its evolution into a more mature phase, where industry leaders are strategically shifting their focus from pure volume growth to developing and marketing value-added products. This strategic pivot becomes especially relevant considering the recent challenges in Argentina's dairy sector, which witnessed a substantial 13% reduction in production during the first half of 2024, prompting companies to adapt their business models and explore innovative product offerings to maintain competitive advantages [1]Source: U.S. Department of Agriculture, “Argentina: Dairy and Products Annual,” fas.usda.gov .

Key Report Takeaways

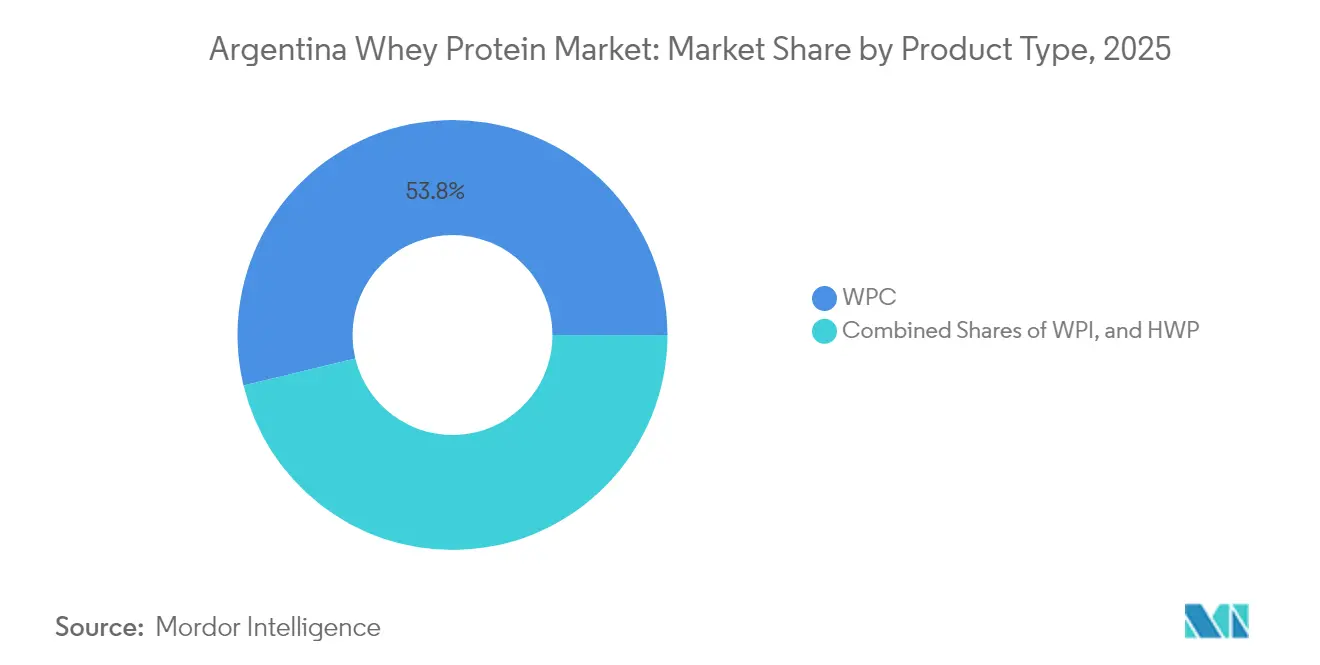

- By product type, whey protein concentrate led with 53.78% of the Argentina whey protein market share in 2025; hydrolyzed whey protein is projected to post a 5.62% CAGR through 2031.

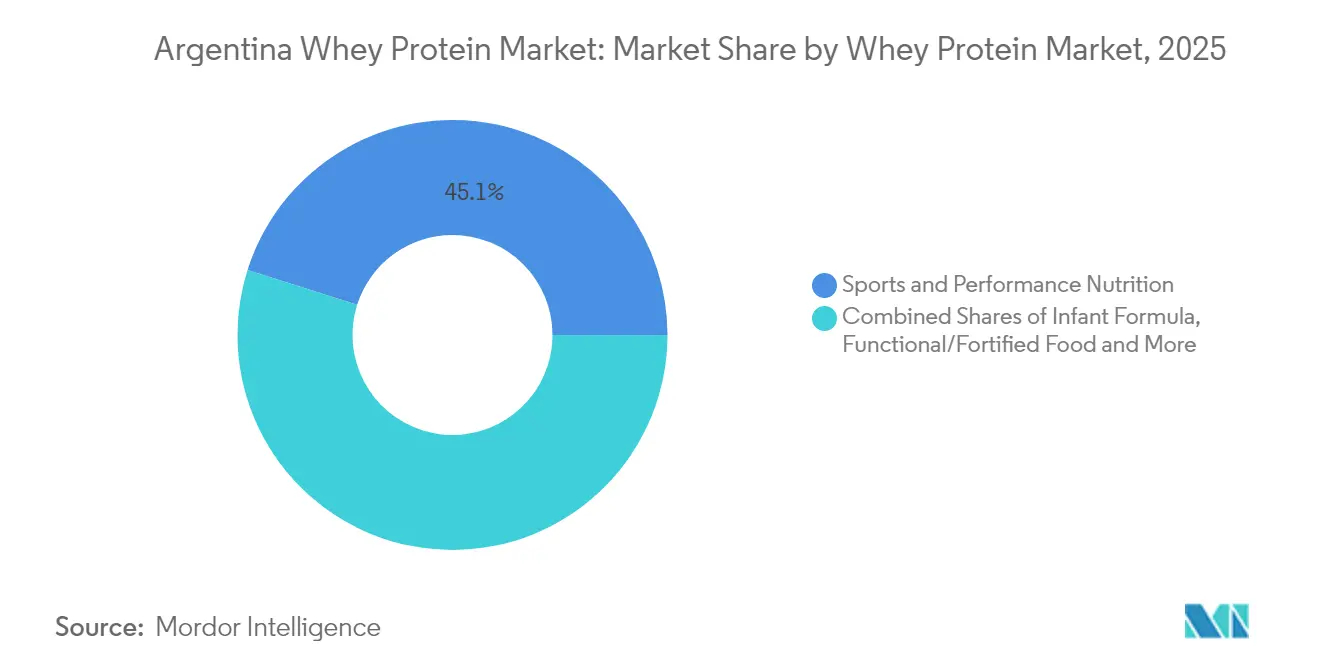

- By application, sports and performance nutrition captured 45.12% revenue share in 2025, while functional/fortified food is forecast to advance at a 5.43% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Whey Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of fitness activities | +1.2% | National, concentrated in Buenos Aires, Córdoba, Santa Fe | Medium term (2-4 years) |

| Product innovation and new flavors/formats by brands | +0.8% | National, with premium segments in urban centers | Short term (≤ 2 years) |

| Growing popularity of sports nutrition products | +1.0% | National, stronger in metropolitan areas | Medium term (2-4 years) |

| Preference for clean-label and natural products | +0.7% | National, led by higher-income demographics | Long term (≥ 4 years) |

| Increasing use in infant formula and pediatric nutrition | +0.4% | National, regulated by ANMAT standards | Long term (≥ 4 years) |

| Expansion of distribution networks | +0.6% | National, focusing on pharmacy and supermarket chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Fitness Activities

Argentina's fitness industry demonstrates remarkable resilience and continued expansion despite prevailing economic challenges, primarily fueled by heightened health consciousness and an expanding array of accessible training alternatives. The sports nutrition market draws substantial strength from the country's deeply embedded fitness culture, particularly evident in urban regions where both gym memberships and home fitness equipment sales maintain robust performance. In the aftermath of the COVID-19 pandemic, consumers have notably increased their health-related investments, even while navigating economic uncertainties, reflecting a fundamental shift in spending priorities. The government's strategic allocation of resources toward public sports infrastructure, combined with the increasing popularity of functional fitness programs, has created a robust ecosystem that amplifies demand for protein supplements. ANMAT's comprehensive regulatory framework ensures stringent safety standards for sports nutrition products, fostering consumer confidence and providing a solid foundation for sustained market expansion [2]Source: Argentina National Government, “What is ANMAT?” argentina.gob.ar.

Product Innovation and New Flavors/Formats by Brands

Manufacturers are strategically transforming their product portfolios to meet evolving consumer preferences, with significant investments in advanced product development capabilities focused on ready-to-drink formats and specialized hydrolysates. In November 2024, Arla Foods Ingredients demonstrated this market responsiveness by introducing Lacprodan® DI-3092, a specialized whey protein hydrolysate containing 10 grams of protein per 100ml, specifically engineered for medical nutrition applications. The industry's innovation trajectory has broadened beyond traditional sports nutrition, with manufacturers actively developing functional food products such as whey-enriched yogurts incorporating caseinomacropeptide to promote dental health benefits. Companies are making substantial progress in enhancing taste profiles and minimizing the characteristic bitterness of hydrolyzed products, addressing a significant barrier to widespread consumer adoption. This commitment to product improvement aligns with the growing consumer demand for transparent ingredient lists and clean-label formulations, as demonstrated by the significant market shift where 68% of Argentine food products now feature vegan/vegetarian labeling [3]Source: Argentine Nutrition Society, “Logos, Symbols And Legends Present On Packaged Food Labels,” revistasan.org.ar.

Growing Popularity of Sports Nutrition Products

The Argentine sports nutrition market has undergone a significant transformation, evolving from its niche bodybuilding roots to become an integral part of mainstream wellness and active lifestyle segments. This shift reflects changing consumer perceptions, as Argentinians increasingly recognize protein supplements as fundamental components of their recovery routines and overall health maintenance programs, moving away from the singular focus on muscle development. The market's accessibility has improved substantially through expanded distribution channels, with products now readily available in pharmacy chains and supermarkets, complementing traditional supplement specialty stores. The industry has experienced notable growth driven by increased female participation in fitness activities and a surge in endurance sports enthusiasts, both demographics requiring consistent protein supplementation for optimal recovery. Additionally, healthcare professionals have played a crucial role in market expansion by educating the public about protein's significance in healthy aging, effectively broadening the consumer base beyond young athletes to include health-conscious individuals across various age groups.

Preference for Clean-Label and Natural Products

The whey protein market is experiencing a significant transformation as consumers increasingly prioritize products with transparent ingredient lists and natural formulations. Health-conscious individuals are demonstrating a willingness to pay higher prices for products they perceive as cleaner and more natural, aligning with broader food industry shifts toward minimal processing. Manufacturers face the technical challenge of maintaining product functionality while removing artificial additives, particularly in flavoring and preservation systems. In response, companies are making substantial investments in developing natural flavor alternatives and pursuing organic certifications, despite the complex regulatory requirements associated with organic claims. Organizations that successfully demonstrate product purity and ingredient sourcing transparency to their increasingly knowledgeable consumer base are gaining competitive advantages in the marketplace.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for plant-based proteins rising among vegans and vegetarians | -0.9% | National, concentrated in urban areas | Medium term (2-4 years) |

| Allergies and lactose intolerance in some consumers | -0.5% | National, with 0.8% APLV prevalence | Long term (≥ 4 years) |

| High cost compared to plant-based and alternative proteins | -1.1% | National, affecting price-sensitive segments | Short term (≤ 2 years) |

| Inconsistent quality and adulteration concerns | -0.6% | National, requiring enhanced regulatory oversight | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preference for Plant-Based Proteins Rising Among Vegans and Vegetarians

The rising popularity of plant-based diets among Argentina's consumers, especially urban millennials and Gen Z, presents significant market challenges for whey protein manufacturers. This dietary transformation is driven by a combination of environmental consciousness and health considerations, supported by the increasing presence of plant protein alternatives across supermarkets, specialty stores, and e-commerce platforms. These alternatives now feature improved taste profiles and textures that effectively compete with traditional dairy-based products. Consumer concerns about dairy farming's environmental impact and animal welfare practices further strengthen this shift towards plant-based options. Despite these challenges, whey protein continues to maintain its strong market presence in sports nutrition and performance-focused segments, where its scientifically proven superior amino acid composition and higher bioavailability make it the preferred choice for consumers prioritizing optimal nutritional benefits over other considerations.

High Cost Compared to Plant-Based and Alternative Proteins

The persistent inflationary environment in Argentina has fundamentally altered consumer behavior, with price sensitivity becoming a dominant factor in purchasing decisions across all market segments. While whey protein offers superior nutritional benefits, its premium pricing structure compared to plant-based alternatives presents significant market penetration challenges, particularly among budget-conscious consumers who struggle to justify the additional expense despite the product's functional advantages. The situation is further complicated by Argentina's ongoing currency instability, which directly impacts the costs of imported specialized ingredients and packaging materials. This economic landscape has created a complex operational environment where manufacturers must carefully navigate between maintaining profitable margins and ensuring their products remain accessible to consumers. As a result, companies with established local production facilities have gained a competitive advantage, while businesses capable of implementing vertical integration strategies or achieving substantial economies of scale in domestic operations are better positioned to capture market opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Concentrate Dominance Faces Hydrolysate Innovation

Whey Protein Concentrate (WPC) dominates the Argentine market with a substantial 53.78% share in 2025, establishing itself as the preferred choice across diverse applications. This dominance stems from its versatile nature and competitive pricing structure, which resonates particularly well with cost-conscious Argentine consumers who seek quality protein supplements without significant financial burden.

In the evolving protein landscape, Hydrolyzed Whey Protein (HWP) demonstrates remarkable growth potential with a projected CAGR of 5.62% through 2031. This growth trajectory is underpinned by its superior digestibility characteristics and increasing adoption in medical nutrition applications. Meanwhile, Whey Protein Isolate (WPI) maintains its strategic position in the market by offering a balanced solution for consumers who demand higher protein concentration but find hydrolysate prices prohibitive. This market segmentation clearly illustrates the distinction between mainstream applications, where concentrates remain the primary choice, and the expanding specialized market segment where hydrolysates are gaining significant traction.

By Application: Sports Nutrition Leadership Challenged by Functional Foods

The Sports and Performance Nutrition segment continues to command a substantial 45.12% market share in 2025, demonstrating its strong position in the protein supplements industry. Meanwhile, the Functional and Fortified Food applications segment is experiencing robust growth at a 5.43% CAGR, as consumers increasingly incorporate protein-enriched products into their daily diets.

This market evolution reflects a significant transformation in consumer behavior, where protein supplementation has transitioned from being primarily associated with athletic performance to becoming an integral part of everyday wellness routines. The Infant Formula segment, while maintaining consistent growth, operates under rigorous regulatory frameworks, with manufacturers adhering to comprehensive guidelines set by the Argentine Ministry of Health and international Codex Alimentarius standards to ensure product safety and quality.

Geography Analysis

Argentina's market demonstrates distinct regional consumption patterns that vary significantly across its diverse geographical landscape. The metropolitan area of Buenos Aires and its surrounding regions emerge as the primary consumption hub, driven by the population's higher purchasing power and growing health consciousness. This trend particularly manifests in urban areas where consumers increasingly prioritize nutritional value. The Pampas region, historically recognized as Argentina's dairy production center, provides manufacturers with substantial operational advantages for local production and processing activities. However, despite abundant access to raw materials, the region faces notable infrastructure limitations that restrict potential capacity expansion.

The country's vast geographical expanse presents substantial distribution challenges, particularly in bridging the economic divide between urban centers and rural areas. This situation has prompted the government to implement Decree 35/2025, which marks a significant shift in food industry regulations . The decree effectively streamlines import and export procedures, creating a more accessible market environment for international suppliers while simultaneously opening new opportunities for domestic manufacturers to expand their global reach.

Argentina's economic trajectory remains closely intertwined with the effectiveness of government policies and the stability of commodity markets. The agricultural sector continues to face exposure to unpredictable weather patterns and fluctuations in global market conditions. The dairy industry's pressing need for infrastructure modernization presents both significant challenges and valuable opportunities for whey protein manufacturers looking to enhance their processing capabilities. While SENASA's regulatory framework effectively maintains product quality standards essential for both domestic consumption and export market participation, the associated compliance requirements often place considerable financial pressure on smaller-scale producers, affecting their operational sustainability.

Competitive Landscape

The Argentina whey protein market demonstrates a moderate level of concentration, where established multinational corporations operate alongside local dairy enterprises to capture market share. Companies that have integrated dairy processing operations into their business model hold significant competitive advantages. These advantages manifest through operational cost efficiencies and the ability to maintain consistent quality standards - benefits that companies relying solely on imports find challenging to replicate. The technological advancement in this market primarily revolves around processing innovations, with companies investing in sophisticated hydrolysis and filtration systems that not only enable distinct product offerings but also help optimize production costs.

The market presents substantial opportunities in specialized segments, particularly in medical nutrition and functional foods. These areas require significant regulatory compliance and clinical validation investments, creating natural barriers that protect companies willing to make these commitments. Innovation continues to shape the market landscape, as exemplified by companies like Vivici, which has successfully developed whey protein through precision fermentation techniques, demonstrating the possibility of commercial production without traditional dairy inputs.

Business success in this market largely depends on organizations' capabilities to effectively navigate Argentina's complex regulatory environment while maintaining financial efficiency in an economy prone to inflation. The recent implementation of ANMAT's enhanced labeling requirements has introduced a dual dynamic - while creating compliance hurdles, it also opens new opportunities for companies that can effectively position themselves in the clean-label segment. This regulatory evolution has become a critical factor in shaping competitive strategies and market positioning.

Argentina Whey Protein Industry Leaders

Arla Foods Ingredients

Saputo Inc.

Hilmar Cheese Company

Fonterra Co-Operative Group

Royal FrieslandCampina

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Arla Foods Ingredients has launched a new whey protein hydrolysate ingredient designed to improve taste and nutritional compliance in medical nutrition products. The hydrolysate offers rapid nutrient absorption with minimal bitterness, enhancing patient experience and recovery.

- August 2024: Fonterra is investing AUD 75 million to expand its Studholme site in southern Canterbury, New Zealand, to increase production of high-value functional proteins for medical and sports nutrition applications.

- April 2024: Arla Foods Ingredients signed an agreement to acquire Volac’s Whey Nutrition business, aiming to use Volac’s Felinfach site in Wales as a global hub to enhance their product offerings in performance, health, and food sectors. The acquisition, completed in late 2024 after regulatory approval, strengthens Arla's position in the whey nutrition market and expands its global supply chain

Argentina Whey Protein Market Report Scope

Argentina whey protein market is fragmented with the presence of various players. The major players are adopting different strategies such as product innovation, merger, and acquisitions to meet the growing demand of consumers. The major players engaged in the distribution of whey protein across the region are Fonterra Co-operative Group Limited, Arla Foods Ingredients, Carbery Group, and Hilmar Ingredients among others.

By Product Type

| Whey Protein Concentrate (WPC) |

| Whey Protein Isolate (WPI) |

| Hydrolyzed Whey Protein (HWP) |

By Application

| Sports and Performance Nutrition |

| Infant Formula |

| Functional/Fortified Food |

| Beverage |

| Others |

| By Product Type | Whey Protein Concentrate (WPC) |

| Whey Protein Isolate (WPI) | |

| Hydrolyzed Whey Protein (HWP) | |

| By Application | Sports and Performance Nutrition |

| Infant Formula | |

| Functional/Fortified Food | |

| Beverage | |

| Others |

Key Questions Answered in the Report

What is the current value of the Argentina whey protein market?

The Argentina whey protein market size is USD 54.46 million in 2026.

How fast is the category expected to grow in Argentina?

It is projected to register a 3.87% CAGR, reaching USD 65.84 million by 2031.

Which product type commands the largest share?

Whey protein concentrate leads with 53.78% share in 2025, driven by cost-effective versatility.

Which application segment is expanding quickest?

Functional and fortified foods are forecast to post a 5.43% CAGR thanks to mainstream consumer uptake.

How are regulations affecting market entry?

Decree 35/2025 and updated ANMAT labeling rules streamline import procedures yet require transparent ingredient disclosures, favoring compliant brands.

Page last updated on: