Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

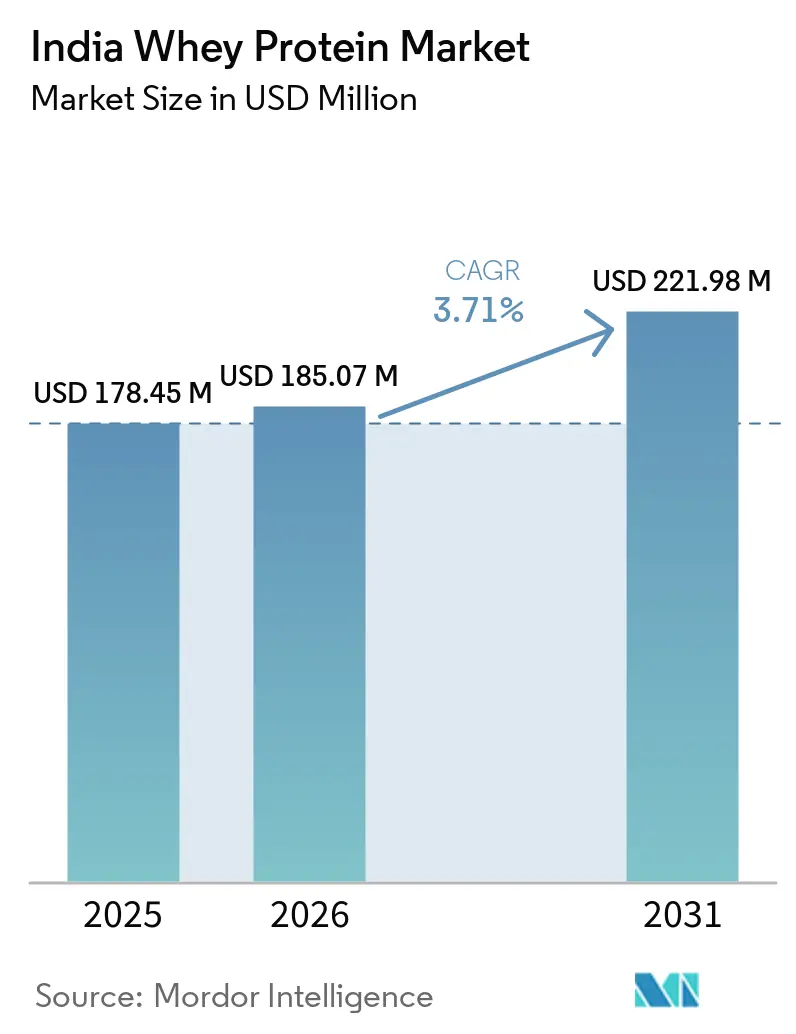

| Base Year Market Size (2025) | USD 178.45 Million |

| Market Size (2026) | USD 185.07 Million |

| Market Size (2031) | USD 221.98 Million |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Whey Protein Market Analysis by Mordor Intelligence

India whey protein market size in 2026 is estimated at USD 185.07 million, growing from 2025 value of USD 178.45 million with 2031 projections showing USD 221.98 million, growing at 3.71% CAGR over 2026-2031. The market's growth is driven by increasing health consciousness among consumers, a rising preference for protein-rich diets, and the expanding fitness and wellness industry in the country. Additionally, the growing adoption of whey protein in various applications, including dietary supplements, functional foods, and beverages, is further fueling market demand. The market also benefits from advancements in product formulations and the introduction of innovative flavors and formats, catering to diverse consumer preferences. The forecast period is expected to witness sustained growth as manufacturers focus on expanding their distribution networks and enhancing product accessibility across urban and rural areas.

Key Report Takeaways

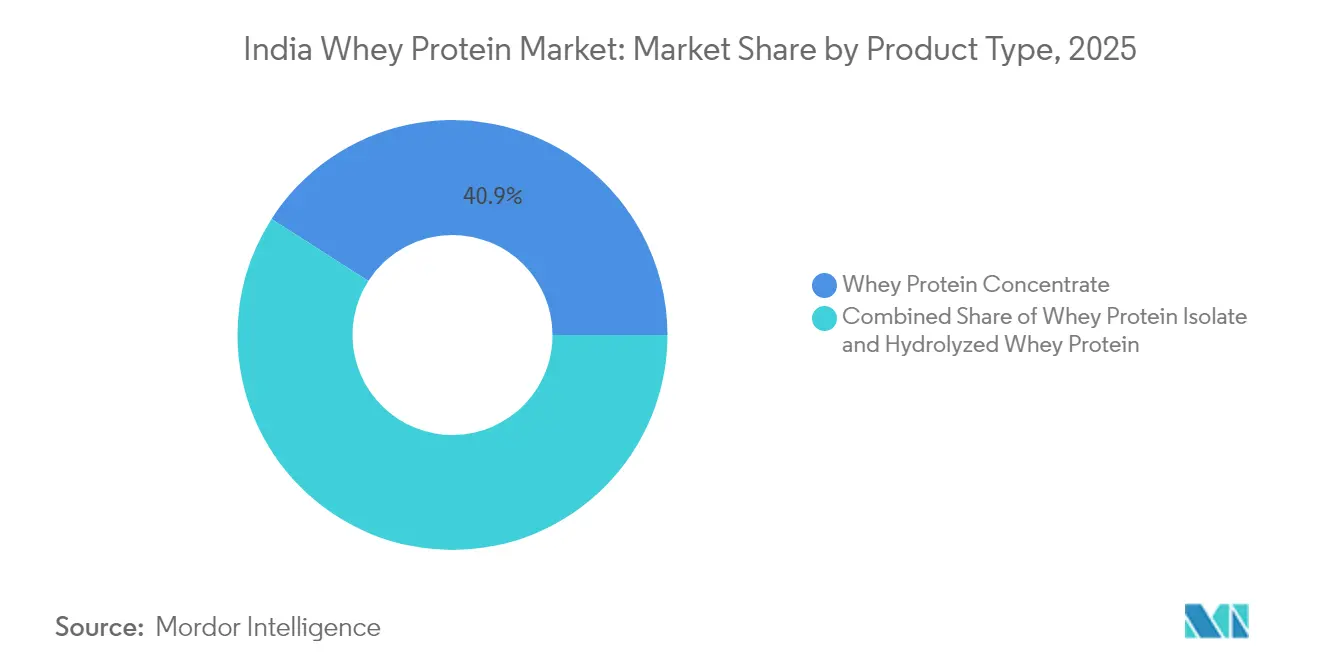

- By product type, whey protein concentrate commanded 40.92% of the India whey protein market share in 2025, whereas whey protein isolate is projected to post the fastest 5.93% CAGR through 2031.

- By category, the mass segment held 73.10% revenue share in 2025, but premium products are advancing at a 4.72% CAGR to 2031.

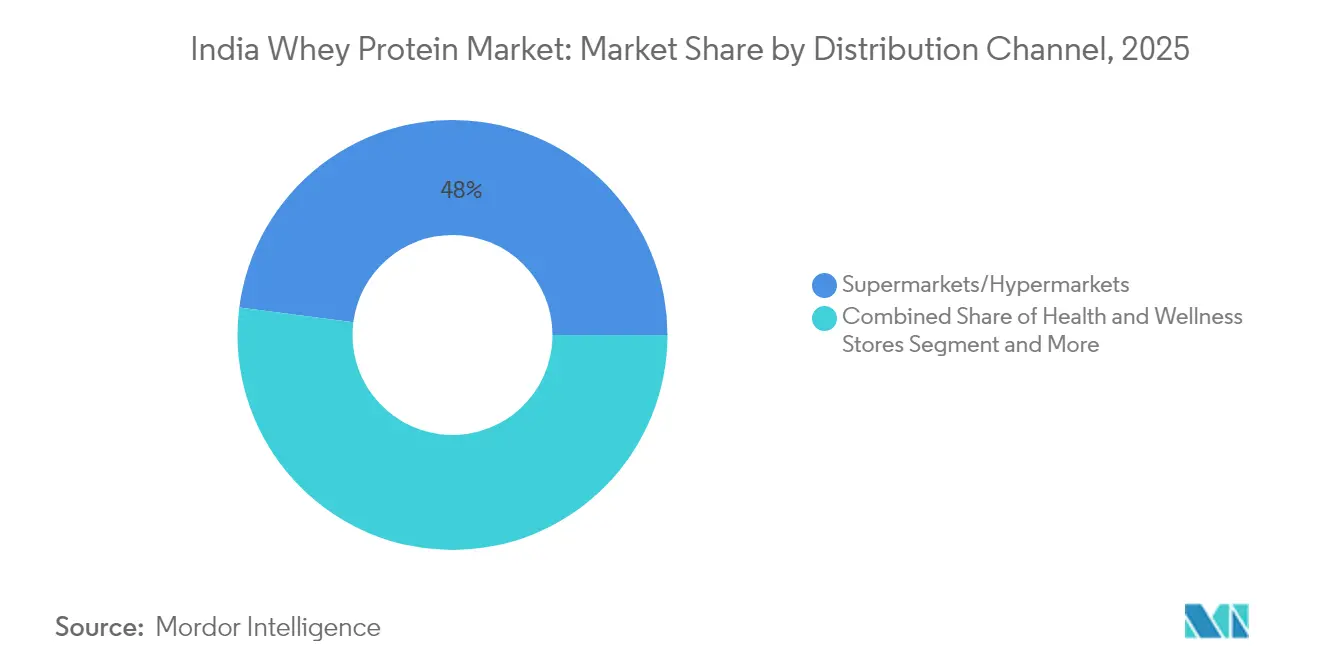

- By distribution channel, supermarkets and hypermarkets led with a 47.96% share in 2025, while online retail is forecast to expand at a 5.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Whey Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising sports and gym culture among millennials and gen z | +0.8% | National, with concentration in Tier-1 cities | Medium term (2-4 years) |

| Growing awareness of protein deficiency in indian diets | +1.2% | National, stronger in urban areas | Long term (≥ 4 years) |

| Expansion of E-commerce and D2C health-nutrition brands | +0.6% | National, led by metro markets | Short term (≤ 2 years) |

| Increasing adoption of whey in infant-nutrition formulas | +0.4% | National, premium urban segments | Long term (≥ 4 years) |

| Government PLI incentives for dairy-protein processing | +0.7% | National, manufacturing hubs priority | Medium term (2-4 years) |

| Surge in female recreational-fitness participation | +0.5% | Urban India, expanding to Tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising sports and gym culture among millennials and gen z

The rising sports and gym culture among Millennials and Gen Z is a significant driver of the India whey protein market. According to the Ministry of Youth Affairs and Sports, the government has been actively promoting fitness initiatives, such as the Fit India Movement, which institutionalizes fitness culture through age-appropriate protocols recommending 30-60 minutes of moderate-to-vigorous physical activity daily [1]Source: Ministry of Youth Affairs and Sports, "Fitness Protocols and Guidelines for 18+ to 65 Years", yas.nic.in. This has encouraged young individuals to adopt healthier lifestyles. Additionally, digital fitness adoption accelerated post-COVID, with fitness apps experiencing significant increases in user engagement. This shift has created educated consumers who understand the role of protein in muscle recovery and performance. The transition from traditional Indian fitness practices to modern gym culture has further driven demand for scientifically-formulated nutrition products, positioning whey protein as an essential rather than optional supplementation. The growing trend is expected to continue driving the market during the forecast period.

Growing awareness of protein deficiency in indian diets

The growing awareness of protein deficiency in Indian diets is a significant driver of the India whey protein market. This deficiency has made whey one of the fastest-adopted supplements within the overall India Protein landscape. A large portion of the Indian population suffers from inadequate protein intake due to dietary habits that rely heavily on carbohydrates and fats. This deficiency has led to increased health concerns, including weakened immunity, muscle loss, and other related issues. As a result, consumers are actively seeking protein-rich alternatives to address these nutritional gaps. Whey protein, known for its high bioavailability and complete amino acid profile, has emerged as a preferred choice among health-conscious individuals. Additionally, government initiatives and campaigns by health organizations to promote balanced diets and protein consumption are further fueling the demand for whey protein products in the country. This trend is expected to drive market growth during the forecast period.

Expansion of e-commerce and D2C health-nutrition brands

The expansion of e-commerce platforms and the rise of direct-to-consumer (D2C) health-nutrition brands are significant drivers of the India whey protein market. The increasing penetration of the internet and smartphones has enabled consumers to access a wide range of whey protein products online, offering convenience and variety. E-commerce platforms provide detailed product descriptions, customer reviews, and competitive pricing, which influence purchasing decisions. Additionally, D2C brands leverage digital marketing strategies and social media platforms to directly engage with consumers, building brand loyalty and trust. These brands often focus on offering high-quality, customized, and innovative whey protein products tailored to specific consumer needs, such as fitness enthusiasts and health-conscious individuals. The seamless integration of e-commerce and D2C channels has significantly contributed to the growth of the whey protein market in India, making these products more accessible to a broader audience.

Government PLI incentives for dairy-protein processing

With a focus on dairy products, the Production Linked Incentive (PLI) scheme has allocated a substantial INR 10,900 crore for food processing. This move is set to bolster manufacturing incentives, particularly for whey protein production [2]Source: Ministry of Food Processing Industries, "From Farm to Retail: Make in India’s push for Food Processing Excellence", pib.gov.in. By March 2025, the PLI scheme had successfully drawn in investments totaling INR 1.61 lakh crore across various sectors. This influx not only led to a remarkable production value of INR 14 lakh crore but also resulted in the creation of 11.5 lakh jobs. Such outcomes underscore the government's unwavering commitment to enhancing domestic manufacturing capabilities. Furthermore, the scheme offers a 50% reimbursement on international marketing expenses. This reimbursement is capped at either 3% of annual sales or INR 50 crore, empowering Indian whey protein manufacturers to bolster their global competitiveness while simultaneously expanding domestic capacity. By 2024, the food processing sector saw 171 active participants benefiting from the PLI, highlighting a robust industry response to the government's incentives. These supportive policies not only lower capital investment hurdles and operational costs but also position domestic players to effectively compete with imports and enhance their export potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import dependence and volatile whey prices | -0.9% | National, affecting all market segments | Short term (≤ 2 years) |

| Rising popularity of plant-based protein alternatives | -0.7% | Urban India, premium segments | Medium term (2-4 years) |

| Stringent FSSAI compliance and testing costs | -0.4% | National, manufacturing operations | Long term (≥ 4 years) |

| Limited cold-chain for RTD whey beverages | -0.3% | National, rural and semi-urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High import dependence and volatile whey prices

In 2025, India is set to import 23,000 MT of whey protein, marking a 20% jump from 2024 figures. This surge makes the Indian market susceptible to global price swings and disruptions in the supply chain [3]Source: United States Department of Agriculture, "Dairy and Products Annual", apps.fas.usda.gov . Even with an impressive annual milk production of 240 million tonnes, India finds itself contributing to less than 0.5% of the global dairy export pie. Its foothold in the lucrative whey product segment pales in comparison to the US, which boasts a 6.7% share in global exports. The US has voiced its apprehensions at the WTO, spotlighting India's newly minted dairy import certificate mandates. These requirements could muddle the import process and inflate compliance expenses for overseas suppliers. Domestically, India grapples with hurdles: a dearth of investment in cheese and whey processing, soaring production costs, and lapses in quality compliance. These challenges stymie the scaling up of domestic manufacturing. Furthermore, fluctuations in global whey prices reverberate through Indian consumer pricing. This volatility introduces demand elasticity hurdles, curbing market growth, especially when import costs surge.

Rising popularity of plant-based protein alternatives

The rising popularity of plant-based protein alternatives poses a significant restraint to the growth of the whey protein market in India. Consumers are increasingly shifting towards plant-based options due to growing health consciousness, dietary preferences, and ethical considerations. The perception of plant-based proteins as healthier and more sustainable compared to animal-derived proteins, including whey, is driving this trend. Additionally, the expanding availability of plant-based protein products, coupled with aggressive marketing strategies by manufacturers, is further intensifying competition for whey protein. This shift in consumer preference is challenging the whey protein market to innovate and adapt to changing demands, potentially impacting its growth trajectory during the forecast period. Furthermore, plant-based protein alternatives, such as soy, pea, and almond proteins, are gaining traction due to their versatility and compatibility with various dietary restrictions, including vegan and lactose-intolerant diets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Isolate Drives Premium Positioning

Whey Protein Concentrate continues to dominate the India Whey Protein Market, holding a significant 40.92% market share in 2025. This dominance is attributed to its affordability and widespread availability, making it a preferred choice among cost-conscious mass consumers. The concentrate segment caters to a broad audience, including individuals seeking basic protein supplementation for general health and fitness. Its relatively lower price point compared to isolates makes it accessible to a larger demographic, particularly in price-sensitive markets. However, the segment faces challenges from increasing consumer awareness about lactose intolerance and the growing demand for cleaner, more refined protein options.

Whey Protein Isolate, on the other hand, is experiencing robust growth, with a projected CAGR of 5.93% through 2031, significantly outpacing the overall market growth. This segment benefits from rising consumer sophistication and a willingness to invest in premium products that offer higher protein content and reduced lactose levels. The isolate segment is particularly appealing to fitness enthusiasts and health-conscious consumers who prioritize cleaner nutritional profiles and superior quality. Additionally, the increasing awareness of lactose intolerance in India further drives demand for isolates, as they cater to individuals seeking protein supplements with minimal lactose content. This growing preference for isolates highlights a clear market bifurcation between cost-driven and quality-focused consumer segments.

By Category: Premium Gains Despite Mass Dominance

The mass category continues to dominate the Indian whey protein market, accounting for a substantial 73.10% market share in 2025. This dominance can be attributed to its affordability and widespread availability, making it accessible to a larger consumer base. The mass segment caters primarily to price-sensitive consumers, including fitness enthusiasts, gym-goers, and individuals seeking basic protein supplementation to meet their dietary needs. Its strong presence in both urban and rural areas further reinforces its market leadership, supported by extensive distribution networks, competitive pricing strategies, and the availability of locally manufactured products. Additionally, the mass category benefits from the increasing penetration of e-commerce platforms, which have made these products more accessible to consumers across various regions of the country.

In contrast, the premium category is witnessing significant growth, with a projected CAGR of 4.72% through 2031. This growth reflects the evolving preferences of Indian consumers, who are increasingly prioritizing quality, brand reputation, and advanced formulations in their protein supplementation choices. The premium segment appeals to a niche audience, including health-conscious individuals, professional athletes, and fitness enthusiasts who are willing to invest in high-quality products with superior nutritional profiles. Factors such as rising disposable incomes, greater awareness of health and fitness, and the influence of global trends are driving the expansion of this segment in the Indian whey protein market.

By Distribution Channel: Digital Commerce Reshapes Access

Supermarkets and Hypermarkets continue to dominate the India whey protein market, holding a substantial 47.96% market share in 2025. These traditional retail channels remain a preferred choice for consumers due to their widespread presence, convenience, and the ability to physically inspect products before purchase. Additionally, supermarkets and hypermarkets often offer promotional deals and discounts, further attracting price-sensitive buyers. Their role in the supply chain remains critical, as they provide a platform for both established brands and new entrants to reach a broad consumer base. Despite the growing popularity of online retail, these channels are expected to maintain their relevance by adapting to changing consumer preferences and enhancing in-store experiences.

Online retail, on the other hand, is experiencing rapid growth in the India whey protein market, with a projected CAGR of 5.04% through 2031. This growth reflects a fundamental shift in consumer purchasing behavior, driven by the increasing penetration of smartphones, improved internet connectivity, and the convenience of doorstep delivery. Online platforms also enable consumers to access a wider variety of products, compare prices, and read reviews, which significantly influence purchasing decisions. Furthermore, the rise of health-conscious consumers and the growing trend of personalized nutrition have led to an increased demand for niche and premium whey protein products, which are more readily available online. As a result, online retail is emerging as a key channel, complementing traditional retail rather than completely displacing it.

Geography Analysis

India's whey protein market remains predominantly domestic, shaped by a unified regulatory framework and distribution networks. Tier-1 cities like Delhi-NCR, Mumbai, Bangalore, and Chennai dominate the landscape, driven by higher disposable incomes, a burgeoning fitness culture, and heightened health awareness. These urban centers serve as key hubs for premium whey protein consumption, with consumers in these regions showing a preference for branded and high-quality products. The presence of organized retail chains and e-commerce platforms further facilitates the availability and accessibility of whey protein products in these cities.

Consumption patterns and price sensitivity vary significantly across regions. Northern states, such as Punjab and Haryana, exhibit a higher acceptance of dairy-based supplements, attributed to the region's strong dairy consumption culture and familiarity with milk-based products. In contrast, southern markets, including Tamil Nadu and Kerala, are witnessing a growing inclination towards plant-based alternatives, driven by dietary preferences and increasing veganism. Additionally, the Maharashtra government's subsidies to dairy farmers, in response to procurement price protests, underscore regional policy disparities that influence both raw material costs and manufacturing dynamics. Such policies can create cost advantages or challenges for manufacturers operating in specific states, impacting the overall market competitiveness.

Rural and semi-urban markets grapple with cold chain infrastructure challenges, limiting the distribution of ready-to-drink whey beverages. These areas face logistical hurdles due to inadequate refrigeration facilities, which are essential for maintaining the quality of perishable products. As a result, manufacturers are focusing on shelf-stable powder formulations to achieve wider market reach. Powdered whey protein products offer longer shelf life and easier storage, making them more suitable for distribution in regions with infrastructure constraints. Furthermore, the growing penetration of e-commerce in rural areas is gradually improving product accessibility, although challenges related to awareness and affordability persist.

Competitive Landscape

Companies in the India whey protein market are actively prioritizing geographical and operational expansions to address the increasing demand for whey protein products across various regions. With the growing awareness of health and fitness among consumers, companies are strategically enhancing their production capabilities to cater to this rising demand. By investing in advanced manufacturing facilities and adopting innovative production techniques, they aim to ensure a consistent supply of high-quality whey protein products. These efforts not only help companies meet the current market requirements but also position them to handle future demand surges effectively.

In addition to production enhancements, companies are streamlining their supply chain operations to improve efficiency and reduce costs. By optimizing logistics, warehousing, and distribution networks, they ensure timely delivery of products to consumers and retailers. Many companies are also forming strategic partnerships with local distributors and e-commerce platforms to expand their reach and penetrate untapped markets. These collaborations enable them to establish a strong foothold in key regions, ensuring better accessibility of their products to a wider consumer base. Furthermore, companies are leveraging digital platforms and online sales channels to tap into the growing e-commerce market in India, which has become a significant driver of growth for the whey protein market.

Furthermore, companies are leveraging their regional expansions to sharpen their competitive edge and capitalize on emerging growth opportunities in the India whey protein market. By focusing on key regions with high growth potential, they aim to strengthen their market presence and gain a larger share of the market. Many players are also investing in marketing and promotional activities to build brand awareness and attract health-conscious consumers. These efforts include collaborations with fitness influencers, sponsorships of health and wellness events, and targeted advertising campaigns. Additionally, companies are emphasizing research and development to innovate and introduce new products that align with consumer trends, such as plant-based protein blends and organic whey protein options.

India Whey Protein Industry Leaders

-

Parag Milk Foods Ltd

-

Gujarat Cooperative Milk Marketing Federation

-

Glanbia PLC

-

Bright Lifecare Pvt. Ltd.

-

GNC Holdings, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nutrabay has launched BioAbsorb, featuring the ProDiFi blend, a patent-pending mix of probiotics, digestive enzymes, and dietary fiber. This formulation enhances digestion, nutrient absorption, and protein processing. BioAbsorb uses 100% Crossflow Microfiltered Whey Concentrate, offering a cleaner protein profile with minimal fat and lactose through a chemical-free filtration process.

- May 2025: GNC, a global leader in nutritional supplements, has launched its newest product in India: the GNC Pro Performance 100% Whey + Keto Surge. Offered in a chocolate flavor, GNC 100% Whey + Keto Surge is available in convenient 1-pound, 2-pound, and 4-pound size variants. Consumers can purchase it on GNC India's website, as well as on platforms like Amazon, Flipkart, Healthcare, Myntra, Hyugalife, and in select offline stores.

- October 2023: In a strategic move, Keventers has partnered with Myprotein, a prominent online sports nutrition brand, to launch a Butterscotch-flavored whey protein. This collaboration aims to cater to fitness enthusiasts across India, assisting them in reaching their fitness aspirations while savoring a novel flavor. The newly introduced Keventers Butterscotch Whey Protein comes in two sizes: 500g and 1kg, priced at INR 2,599 and INR 4,399, respectively.

- February 2023: Fast & Up, an Indian brand specializing in active nutrition, has unveiled its latest product: Fast & Up Fusion Tech Protein. This innovative formulation stands out as India's inaugural clinically tested blend of whey and plant protein. Featuring the Faster Sustained Absorption Formula (FSA), it promises superior protein delivery, double the absorption rate, and benefits like enhanced muscle growth and quicker recovery, all while being budget-friendly.

India Whey Protein Market Report Scope

Whey protein, also known as whey isolate, is a compound of proteins extracted from whey, a liquid material produced as a byproduct of cheese production.

The Indian whey protein market is segmented by product type and application. By product type, the market is segmented into whey protein concentrate, whey protein isolate, and hydrolyzed whey protein. Based on application, the market is segmented into sports and performance nutrition, infant formula, and functional or fortified food.

The market sizing has been done in value terms in USD and for volume terms in volume in tons for all the abovementioned segments.

By Product Type

| Whey Protein Concentrate |

| Whey Protein Isolate |

| Hydrolyzed Whey Protein |

By Category

| Mass |

| Premium |

By Distribution Channel

| Online Retail |

| Supermarkets and Hypermarkets |

| Health and Wellness Stores |

| Other Distribution Channels |

| By Product Type | Whey Protein Concentrate |

| Whey Protein Isolate | |

| Hydrolyzed Whey Protein | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Online Retail |

| Supermarkets and Hypermarkets | |

| Health and Wellness Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the India whey protein market in 2026?

The India whey protein market size is USD 185.07 million in 2026 with a 3.71% CAGR to 2031.

Which product type grows fastest within Indian whey supplements?

Whey protein isolate posts the quickest 5.93% CAGR thanks to higher purity and low lactose levels.

What share do supermarkets hold in whey protein sales?

Supermarkets and hypermarkets account for 47.96% of 2025 sales, leading all channels.

How do government incentives support domestic whey production?

The PLI scheme reimburses up to 50% of qualifying expenses and lowers capital costs for new dairy-protein plants.

Page last updated on: