Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

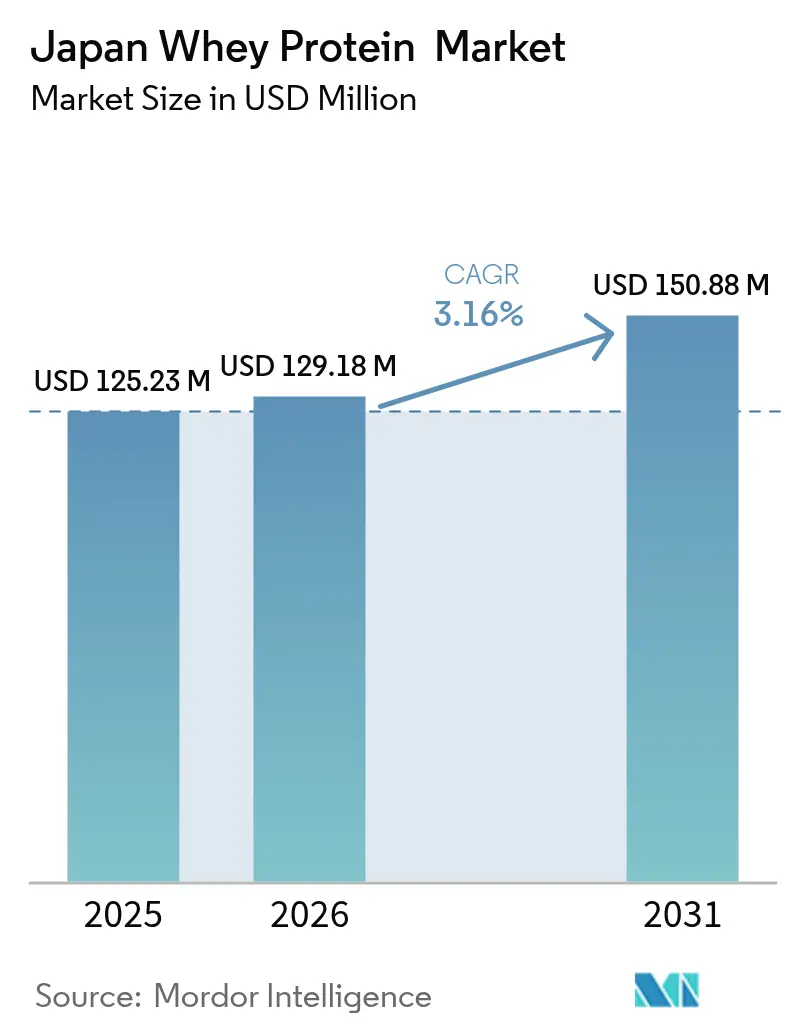

| Base Year Market Size (2025) | USD 125.23 Million |

| Market Size (2026) | USD 129.18 Million |

| Market Size (2031) | USD 150.88 Million |

| Growth Rate (2026 - 2031) | 3.16% CAGR |

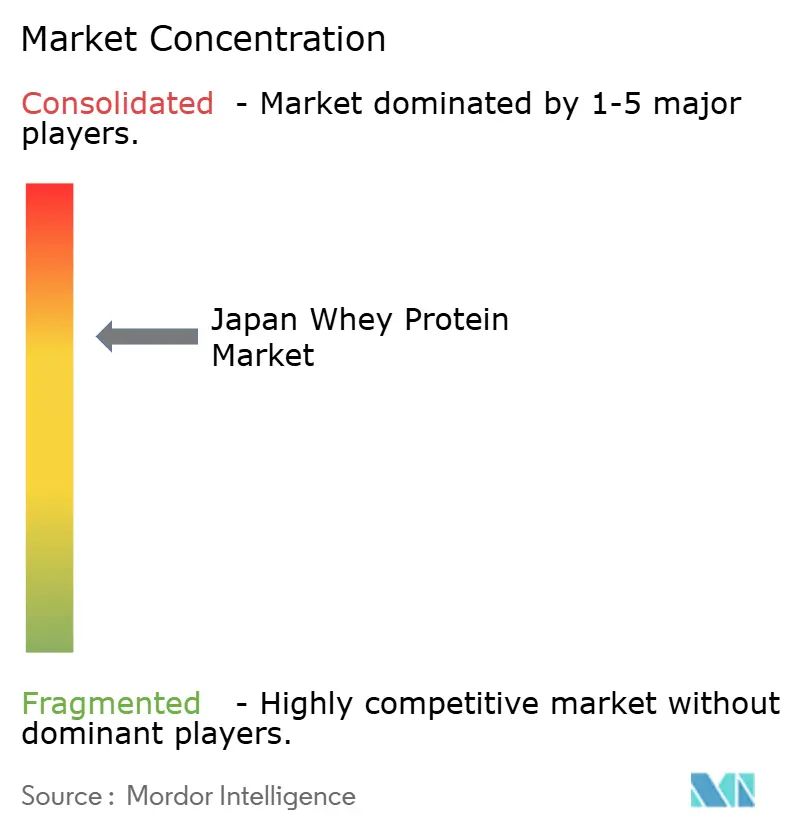

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Whey Protein Market Analysis by Mordor Intelligence

Japan whey protein market size in 2026 is estimated at USD 129.18 million, growing from 2025 value of USD 125.23 million with 2031 projections showing USD 150.88 million, growing at 3.16% CAGR over 2026-2031. Japan's aging population, particularly individuals aged 65 and older, is driving a shift in demand from traditional sports nutrition products to medical foods specifically designed to address sarcopenia (age-related muscle loss). This demographic shift is influencing product preferences, with daily consumption increasingly centered around ready-to-drink beverages, single-serve stick packs, and high-protein bakery items. These products align with the convenience-store shopping habits prevalent in Japan and offer the added benefit of portion control. Retailers are responding to these evolving consumer needs by broadening their protein product assortments, particularly targeting female and senior shoppers. As a result, suppliers who can deliver high-purity whey protein isolates combined with clean-label sweeteners are securing the most shelf space and gaining a competitive edge. However, Japan's heavy reliance on imports remains a critical factor in the market. Global producers supply advanced filtration grades of whey protein that local dairies are unable to produce, ensuring a steady demand for imported products. At the same time, this dependency introduces challenges, as fluctuations in currency exchange rates and rising freight costs create pricing uncertainties for both suppliers and retailers.

Key Report Takeaways

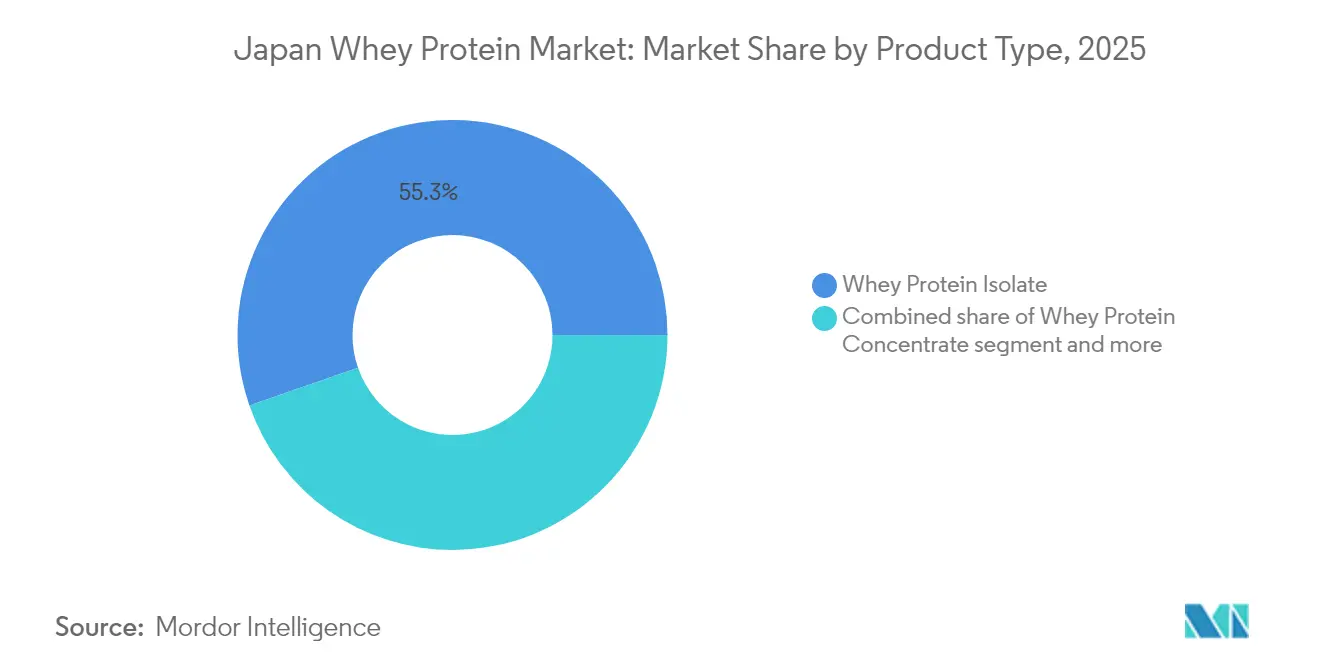

- By product type, whey protein isolate held 55.32% of the Japanese whey protein market share in 2025. While whey protein isolate is projected to expand at a 3.72% CAGR through 2031.

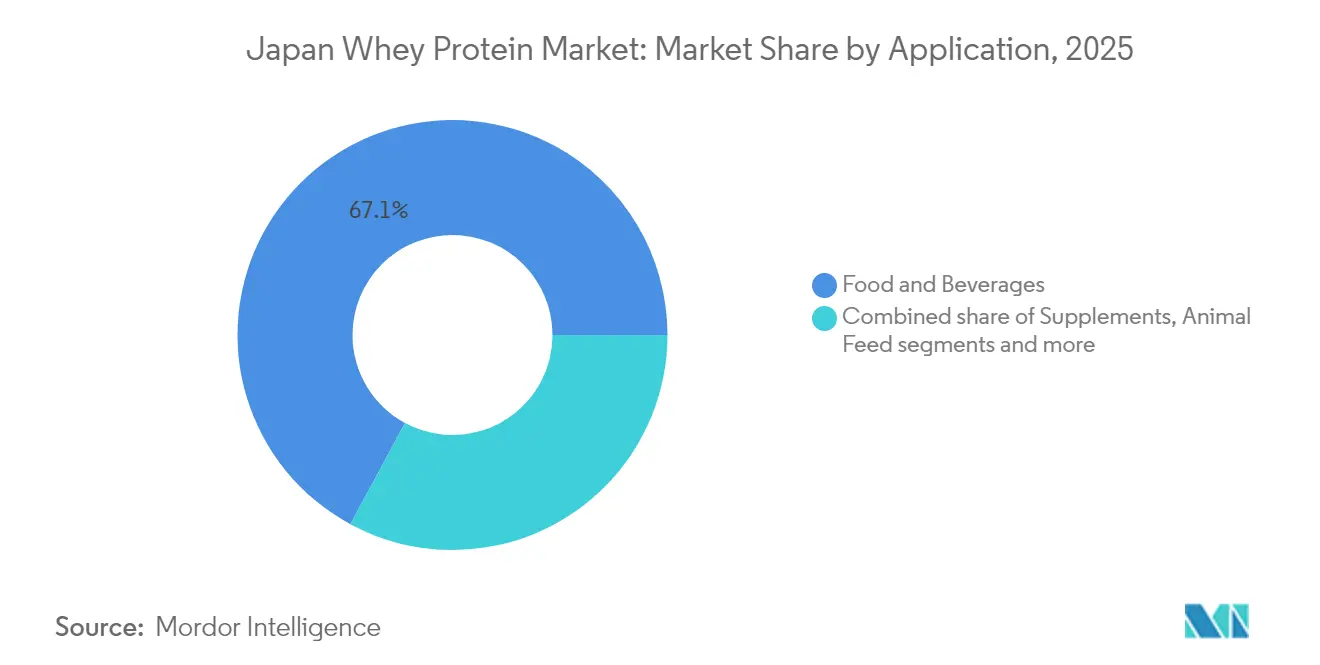

- By application, food and beverages accounted for 67.12% of the Japanese whey protein market size in 2025. While supplements are forecast to register a 3.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Whey Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-protein ingredients in end products | +0.6% | National, concentrated in Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Health and fitness trends boosting protein needs | +0.5% | National, with higher penetration in urban centers | Short term (≤ 2 years) |

| Expansion of sports nutrition and protein categories | +0.4% | National, Olympics legacy driving participation | Medium term (2-4 years) |

| High-purity isolate differentiation by leading brands | +0.3% | National, premium retail channels | Long term (≥ 4 years) |

| Premium and clean-label positioning | +0.3% | National, female and senior demographics | Medium term (2-4 years) |

| Product innovation and flavor localization | +0.2% | National, convenience-store distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing demand for high-protein ingredients in end products

Protein fortification has expanded from niche sports supplements to mainstream food categories, such as ready-to-eat meals, breakfast cereals, and snack bars. Whey's neutral flavor and heat stability make it the top choice for savory applications, including protein-enriched ramen and miso soup bases, where soy protein's beany notes can interfere with traditional taste profiles. The Ministry of Health, Labour and Welfare's 2024 update to nutrition labeling rules has reduced the requirement for "high protein" claims from 15 grams to 12 grams per 100 grams, effectively lowering formulation costs for mid-tier brands. Bakery applications remain underutilized, as whey protein concentrate can replace wheat flour in bread formulations without affecting crumb structure. However, adoption has been slow due to procurement inertia and limited technical support from ingredient distributors. With growing demand for protein-enriched products, such as high-protein yogurts, nutrition bars, ready-to-drink shakes, and fortified snacks, food and beverage manufacturers are increasingly using whey protein ingredients to meet high-protein claims. In 2024, packaged food products in Japan containing animal-derived protein ingredients recorded a total volume sales of 41.7 thousand tonnes, according to Agriculture and Agri-Food Canada [1]Source: Agriculture and Agri-Food Canada, "Plant-based protein food and drink trends in Japan", agriculture.canad.ca .

Health and fitness trends boosting protein needs

In 2024, Japan reported 2.88 million fitness club members, as stated by the Ministry of Economy, Trade and Industry [2]Source: Ministry of Economy, Trade and Industry, "Current survey of selected service industries", meti.go.jp. This demographic change is transforming protein marketing strategies: brands now focus on promoting skin elasticity, hair health, and metabolic support rather than muscle growth. Meiji's "Savas for Women" line, updated in 2024 to include collagen peptides along with whey isolate, quickly captured the female sports nutrition market within six months of its launch. This success reflects a key insight: Japanese consumers regard protein supplements as a means of preventive healthcare, aligning with the cultural principle of "mibyō," which emphasizes managing health before disease onset. The increasing use of GLP-1 receptor agonists for weight management has also driven demand for high-protein, low-carbohydrate meal replacements that help preserve lean mass during calorie restriction. Whey hydrolysates have gained popularity within this segment due to their faster gastric emptying and reduced satiety effects. On the regulatory side, the Foods with Function Claims system remains supportive, allowing muscle-maintenance claims based on existing literature reviews and eliminating the need for the extensive clinical trials required for FOSHU approval.

Expansion of sports nutrition and protein categories

In 2024, Japan's Ministry of Internal Affairs and Communications reported that 77.4% of the population actively participated in sports activities [3]Source: Ministry of Internal Affairs and Communications, "Survey on sports", soumu.go.jp. This notable increase in recreational sports engagement, including a rise in marathon registrations and gym memberships, is projected to sustain its momentum through 2025. The growing interest in fitness and physical well-being has significantly boosted the demand for performance-enhancing products, particularly whey protein supplements. To cater to this rising demand, manufacturers are focusing on developing innovative product formats, which has led to an increase in ingredient procurement from whey suppliers to support an expanded portfolio of stock-keeping units (SKUs). Furthermore, flavor innovations have moved beyond the conventional vanilla and chocolate options, with locally inspired flavors such as matcha, yuzu, and sakura gaining popularity. These unique flavors are helping domestic brands differentiate themselves from imported competitors. Additionally, the adoption of digital supply chains has streamlined the sourcing process, enabling whey suppliers to handle larger, recurring orders efficiently while ensuring a more predictable demand pattern.

High-purity isolate differentiation by leading brands

Whey protein isolate, with its 90% protein content and less than 1% lactose, holds a premium position that concentrate formulations cannot achieve. The brand's success lies in its transparent labeling, where each serving clearly specifies leucine content and BCAA ratios. This approach appeals to knowledgeable consumers who value protein quality over quantity for driving muscle protein synthesis. Advances in membrane filtration technology have enabled cross-flow microfiltration to deliver high protein purity with minimal denaturation. This method preserves bioactive fractions, such as lactoferrin and immunoglobulins, which are typically lost during concentrate processing. These functional peptides support immune health claims under Japan's Foods with Function Claims framework, creating a regulatory advantage that commodity suppliers find difficult to overcome. Additionally, isolates' superior solubility is critical for clear-beverage applications. Ready-to-drink (RTD) protein waters depend on isolates to maintain clarity and prevent sedimentation throughout their shelf life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from plant-based proteins | -0.5% | National, urban centers with vegan adoption | Medium term (2-4 years) |

| Lactose intolerance and dairy sensitivity | -0.4% | National, affecting up to 80% of population to varying degrees | Short term (≤ 2 years) |

| Dairy price volatility | -0.3% | National, import-dependent supply chain | Short term (≤ 2 years) |

| Market maturity in core sports segments | -0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying competition from plant-based proteins

Soy protein isolates and pea protein concentrates are gaining traction in cost-sensitive applications, where whey’s functional benefits, such as solubility, neutral flavor, and a complete amino acid profile, are less critical compared to the cost per gram of protein. This trend is most evident in the USD 5-10 per kilogram price range, where whey concentrate directly competes with textured soy protein, and brand loyalty is relatively weak. Improvements in pea protein, such as reduced off-flavors through enzymatic debittering and enhanced solubility via microencapsulation, have made it a viable option for beverage applications that were previously exclusive to whey. In Japan, the environmental narrative is influential, with consumers increasingly considering carbon footprints when selecting packaged foods. Consequently, the market is experiencing a gradual decline in whey’s default status in new product development, particularly among startups unencumbered by legacy formulations or supplier relationships.

Lactose intolerance and dairy sensitivity

Japanese adults experience lactase non-persistence, a genetic condition that reduces the ability to digest lactose after weaning, though the severity of symptoms varies. Whey protein isolates, which contain less than 1% lactose, effectively address this issue. However, many consumers avoid all dairy-based ingredients due to prior negative experiences with milk or cheese, reflecting a gap between perception and scientific reality. This disconnect limits market growth, particularly in elderly nutrition, where digestive comfort is a priority. Hydrolyzed whey, produced through enzymatic pre-digestion that breaks proteins into smaller peptides, enables faster absorption and minimizes bloating. Nevertheless, its higher cost confines its use primarily to medical nutrition. Additionally, Japan's Food Labeling Act does not require lactose content disclosure for protein supplements, leaving consumers reliant on voluntary "lactose-free" claims, which lack standardized criteria. Educational campaigns promoting the low lactose content of isolates have shown limited success, indicating that addressing this challenge may require innovative approaches, such as lactose-free certification programs, rather than relying solely on marketing efforts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Isolate Purity Commands Premium

In 2025, whey protein isolate accounted for 55.32% of the market value and is expected to grow at a 3.72% CAGR through 2031, surpassing both concentrate and hydrolysate variants. The isolate's market leadership is driven by its high protein purity and low lactose content. These characteristics not only support premium market positioning but also address the lactose sensitivity common among many Japanese consumers. Advances in membrane filtration, particularly cross-flow microfiltration, have enabled the preservation of bioactive fractions like lactoferrin and immunoglobulins. These components, often lost in earlier processing methods, now allow brands to substantiate immune-support claims under the Foods with Function Claims framework.

Whey protein concentrate, although less pure, remains a cost-effective option for bakery and ready-to-eat products. In these applications, functional properties such as emulsification and water binding are more critical than protein density. Hydrolyzed whey protein, which is enzymatically broken down into smaller peptides, serves niche markets like medical nutrition and infant formulas that require rapid absorption and hypoallergenicity. However, its bitter taste and higher price limit broader adoption. The varying growth rates across the segment are influenced by formulation economics: isolates offer a solubility advantage essential for clear, ready-to-drink (RTD) beverages and single-serve stick packs. While the concentrate's slower growth reflects commoditization pressures, particularly as plant-based alternatives challenge its cost-performance benefits in bulk applications, the hydrolysate's specialized market focus protects it from direct competition. Nevertheless, its volume remains restricted by its limited use cases and the complex regulatory requirements for infant formula approvals, which necessitate multi-year clinical validation under MHLW standards.

By Application: Supplements Outpace Food Fortification

In 2025, food and beverages accounted for 67.12% of the market share, highlighting the extensive use of whey in products such as ready-to-drink protein shakes, high-protein bread, breakfast cereals, and dairy alternatives. Bakery applications utilize whey concentrate as a replacement for wheat flour while preserving the desired crumb structure. However, adoption has been slow due to procurement challenges and limited technical support from ingredient distributors. Beverages, particularly clear protein waters that require isolates for transparency and shelf stability, represent the fastest-growing subcategory within food applications. Additionally, ready-to-eat meal kits and snacks are incorporating whey to meet "high protein" labeling requirements.

Supplements are expected to grow at a 3.89% CAGR through 2031, the highest growth rate among applications. This growth is primarily driven by nutrition sachets for the elderly and leucine-enriched formulations designed to prevent sarcopenia. With 29.3% of Japan's population now over 65, as reported by the Statistics Bureau of Japan in 2024, formulation priorities are shifting from muscle growth to addressing frailty, supported by clinical evidence emphasizing the importance of protein intake for seniors. Baby food and infant formula, governed by strict MHLW compositional standards, are experiencing stable but slow growth, largely due to Japan's declining birth rate. Meanwhile, the sports and performance nutrition segment is expanding its reach to recreational athletes and weekend enthusiasts, who consume smaller portions but prefer higher-margin retail channels. In the personal care sector, while applications are still emerging, whey hydrolysates are gaining traction. Their film-forming and moisturizing properties make them valuable actives in hair-care products, particularly for addressing protein damage, a common concern among Japanese women who frequently color their hair. Lastly, animal feed applications, especially whey permeate in livestock rations, show potential for high volumes but face margin pressures due to fluctuating commodity soy meal prices.

Geography Analysis

In metropolitan areas such as Tokyo, Osaka, and Nagoya, the combination of dense retail networks and higher disposable incomes significantly contributes to the volume of premium isolated purchases. Urban shoppers in these cities are highly responsive to new flavors and clean-label trends, providing brands with an ideal environment to test products before launching them nationwide. Additionally, the higher concentration of gyms in these urban centers sustains a consistent demand for protein powders, with casual athletes frequently purchasing these products through clubs, drugstores, and online platforms.

In contrast, regional prefectures exhibit a slower adoption rate; however, convenience stores in these areas continue to stock the same ready-to-drink (RTD) product ranges. This approach ensures widespread product exposure without requiring additional investments in separate distribution networks. In rural regions, older consumers tend to prefer sachets and jellies, which are primarily marketed through pharmacy chains. This distribution channel not only commands higher per-unit prices but also benefits from reduced freight costs. Furthermore, the demographic shift toward an aging population in these areas suggests that demand for medical nutrition products could surpass that of sports nutrition formats.

Import logistics are heavily concentrated through Tokyo Bay and Osaka ports, which handle the majority of inbound whey protein shipments. This concentration creates a significant inventory risk at these two key nodes. To mitigate risks associated with earthquakes, suppliers have started maintaining safety stocks by storing buffer inventories in inland depots located around Nagoya. Moreover, currency hedging decisions are typically made in these hubs, and fluctuations in the yen have an immediate and widespread impact on wholesale pricing across the country.

Competitive Landscape

The Japan whey protein market exhibits moderate consolidation; top suppliers such as Fonterra Co-operative Group Limited, Glanbia Plc, Meiji Co., Ltd., Morinaga Milk Industry Co., Ltd., and Arla Foods amba collectively hold a significant share of the ingredient volume, reflecting a moderately consolidated market structure. However, the finished consumer product segment remains highly fragmented, driven by the proliferation of private-label and niche brands. Competitive dynamics in this market are distinctly bifurcated. Global ingredient suppliers focus on offering advanced technical services, forming co-manufacturing partnerships, and ensuring supply chain reliability to maintain their market position. On the other hand, Japanese consumer brands prioritize securing retail shelf space, tailoring flavors to local preferences, and leveraging their established brand heritage to safeguard end-product margins and sustain consumer loyalty.

Significant white-space opportunities exist in the market, particularly in the development of cosmetic-grade hydrolysates for hair care formulations and in animal feed applications. In the latter, whey permeate remains underutilized compared to soy meal, despite its superior amino-acid bioavailability, which positions it as a high-potential alternative. The competitive landscape features a mix of global ingredient suppliers and local formulation partners, all vying for dominance across both raw ingredients and finished products. This dynamic environment includes active participation from large multinational corporations and domestic players, with strategies often tailored to align with regional consumer preferences and distribution networks.

Technological advancements are increasingly setting apart the frontrunners from the rest. Glanbia's foray into membrane filtration, achieving 92% protein purity with minimal denaturation, not only safeguards bioactive fractions like lactoferrin and immunoglobulins, pivotal for immune-health claims, but also erects a regulatory barrier against commodity suppliers. Meanwhile, Arla's "Grass to Glass" initiative, tracing each batch back to specific European farms, has become essential for premium branding in Japan's discerning market. This has put pressure on smaller entities to either match such investments or concede the premium segment to larger multinationals. On the horizon, precision-fermentation startups are pioneering animal-free whey proteins through microbial expression, yet they face a 3-5 year commercialization timeline and navigate the still-unclear regulatory landscape under Japan's novel-food framework.

Japan Whey Protein Industry Leaders

-

Glanbia Plc

-

Fonterra Co-operative Group Limited

-

Arla Foods amba

-

Morinaga Milk Industry Co., Ltd.

-

Meiji Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Kentai launched BioActive Whey, a premium protein powder enriched with maslinic acid. This triterpenoid compound is recognized for its anti-inflammatory and metabolic advantages, catering to consumers desiring more than just standard protein benefits.

- April 2023: Arla Foods Ingredients, headquartered in Denmark, introduced Nutrilac and ProteinBoost, two cutting-edge whey protein products leveraging patented microparticulate technology. This innovative launch addresses the surging global demand for high-quality protein, particularly in the Japanese market. These versatile products find application in a wide range of dairy and sports nutrition products, including yogurt, desserts, and dairy beverages.

Japan Whey Protein Market Report Scope

By Product Type

| Whey Protein Concentrate |

| Whey Protein Isolate |

| Hydrolyzed Whey Protein |

By Application

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Dairy and Dairy Alternative Products | |

| RTE/RTC Food Products | |

| Snacks | |

| Personal Care and Cosmetics | |

| Supplements | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition | |

| Personal Care and Cosmetics | |

| Others |

| By Product Type | Whey Protein Concentrate | |

| Whey Protein Isolate | ||

| Hydrolyzed Whey Protein | ||

| By Application | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Dairy and Dairy Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

| Personal Care and Cosmetics | ||

| Others | ||

Key Questions Answered in the Report

How large is Japan’s whey protein demand in 2026?

The Japan whey protein market size is USD 129.18 million in 2026 with a projected USD 150.88 million by 2031 at 3.16% CAGR.

Which product type leads sales?

Whey protein isolate dominates with 55.32% value share in 2025 and is forecast to expand at 3.72% CAGR.

What application category is growing the fastest?

Supplements, especially elderly-focused sachets, are set to grow at 3.89% CAGR through 2031.

Why do imports matter so much?

Imports make up 60% of supply, and currency swings plus freight costs strongly influence domestic pricing and margins.

Page last updated on: