Protein Hydrolysates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.17 Billion |

| Market Size (2031) | USD 6.67 Billion |

| Growth Rate (2026 - 2031) | 9.81% CAGR |

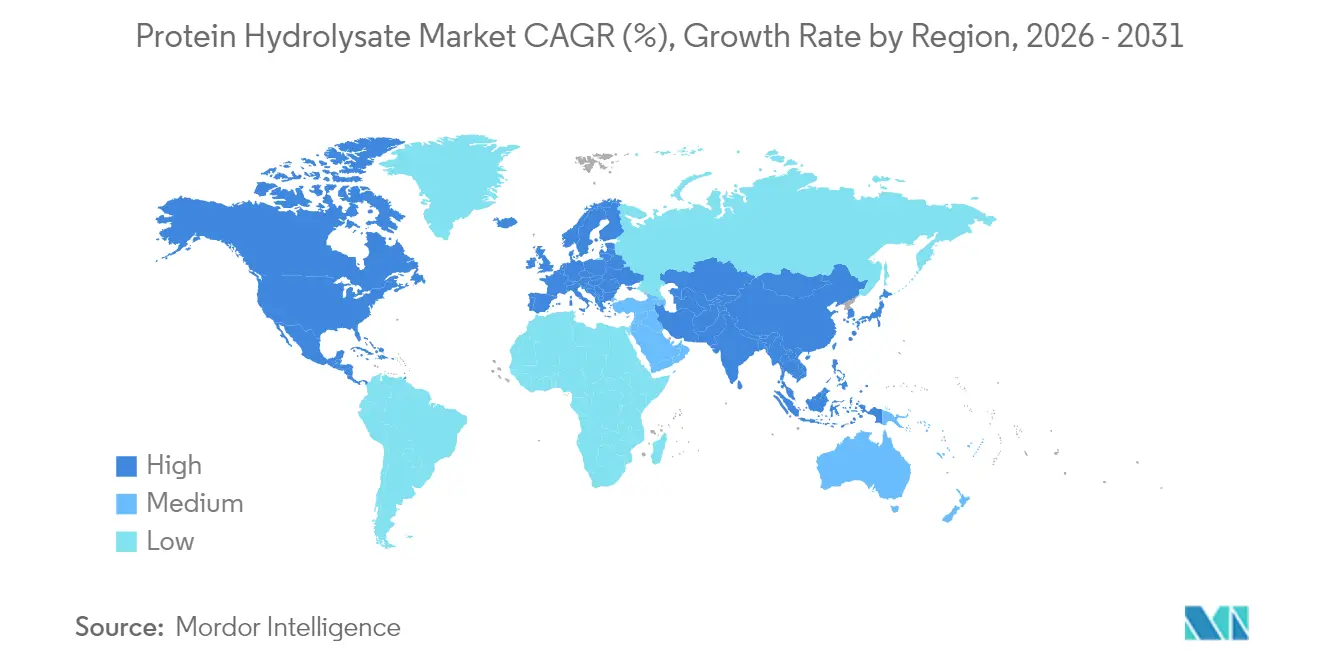

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Protein Hydrolysates Market Analysis by Mordor Intelligence

The protein hydrolysates market size was valued at USD 3.8 billion in 2025 and estimated to grow from USD 4.17 billion in 2026 to reach USD 6.67 billion by 2031, at a CAGR of 9.81% during the forecast period (2026-2031). The widening use of hydrolyzed proteins in infant formula, sports recovery beverages, and specialized clinical nutrition reinforces growth. Strong regulatory alignment in North America and Europe, paired with rising disposable incomes across Asia-Pacific, stimulates demand for tailored peptides that deliver proven bioavailability while meeting clean-label expectations. Technological progress—including precision fermentation, ultrasonic pretreatment, and enzyme immobilization—reduces bitterness and improves functional attributes, supporting new product launches that attract brand investment. Manufacturers also benefit from global moves toward allergen-friendly and sustainable proteins, as plant-derived hydrolysates gain traction in dairy alternatives and clear drink formats.

Key Report Takeaways

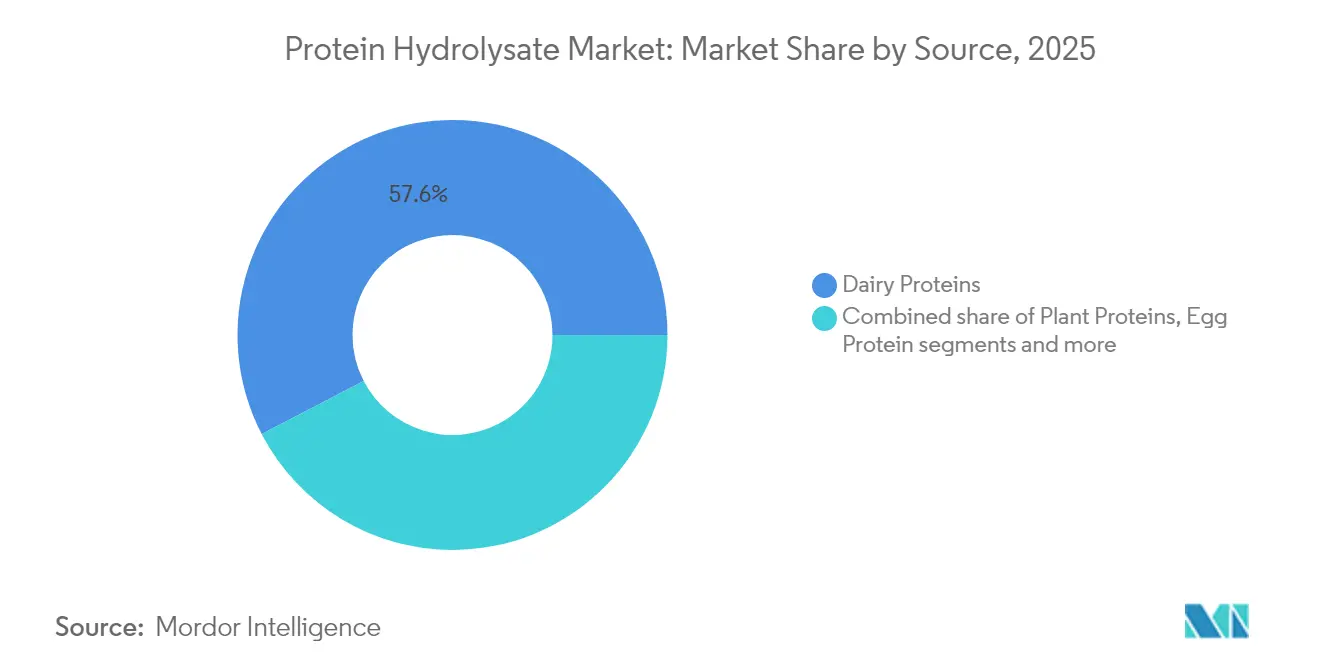

- By source, dairy protein accounted for 57.62% of the protein hydrolysates market share in 2025, while plant protein is projected to expand at a 10.63% CAGR to 2031.

- By degree of hydrolysis, medium-DH products held 47.58% share of the protein hydrolysates market size in 2025; high-DH offerings are expected to grow at an 11.72% CAGR through 2031.

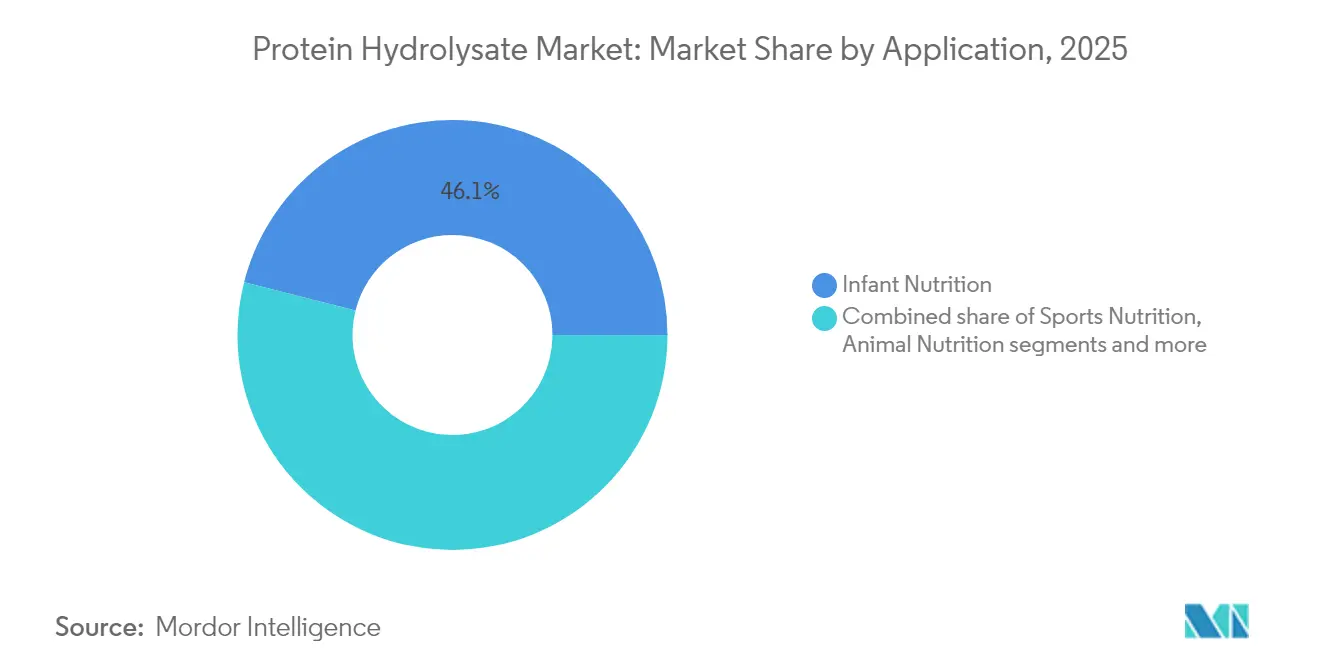

- By end-use, infant nutrition dominated with a 46.05% share in 2025; sports nutrition is forecast to log the fastest 13.02% CAGR during 2026-2031.

- By geography, Asia-Pacific dominated the market with 38.05% share in 2025; the Middle East and Africa are projected to expand at a 11.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Hydrolysates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift in Demand Toward Hydrolyzed Proteins in Infant Nutrition | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Sports‐Recovery Brands Incorporating High-DH Peptides in RTD Formats | +1.8% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Increasing Demand for Clean-Label Plant-Based Hydrolysates | +1.5% | Global, led by North America and Northern Europe | Medium term (2-4 years) |

| Technological Innovation in Protein Hydrolysis | +1.3% | Global, with Research and Development centers in North America and Europe | Long term (≥ 4 years) |

| Increased Application in Pet and Animal Nutrition | +1.1% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Demand for Protein-Enriched Functional Food and Beverages | +0.9% | Global, with premium segments in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift in Demand Toward Hydrolyzed Proteins in Infant Nutrition

Regulatory approval momentum accelerates adoption of protein hydrolysates in infant nutrition, exemplified by Arla Foods Ingredients' FDA clearance for four whey protein hydrolysates in July 2024, strengthening confidence in the protein hydrolysates market, marking the first such authorization for allergy management applications [1]Source: U.S. Food and Drug Administration, "FDA confirms Arla Foods Ingredients’ whey protein hydrolysates can be used in infant formula", www.fda.gov The FDA's updated infant formula nutrient requirements review signals potential expansion of hydrolysate specifications beyond current protein efficiency ratio standards. Clinical evidence demonstrates that extensively hydrolyzed formulas reduce allergic reaction incidence in high-risk infants by up to 50% compared to standard formulations, driving pediatrician recommendations and parental preference shifts. India's Food Safety and Standards Authority permits protein hydrolysates in milk and cereal-based complementary foods, expanding addressable markets in price-sensitive regions. Manufacturing complexity increases as producers must demonstrate protein biological quality equivalent to casein while maintaining palatability, requiring specialized enzymatic processing capabilities that favor established players with R&D resources.

Sports‐Recovery Brands Incorporating High-DH Peptides in RTD Formats

Sports-recovery brands are increasingly incorporating high-degree hydrolysis (High-DH) peptides into ready-to-drink (RTD) formats, driving growth in the protein hydrolysate market. High-DH peptides are known for their rapid absorption and enhanced bioavailability, making them ideal for post-workout recovery. These peptides help in faster muscle repair and reduce recovery time, which aligns with the growing consumer demand for convenient and effective sports nutrition solutions. The adoption of RTD formats further caters to the on-the-go lifestyle of modern consumers, offering a practical and efficient way to meet their protein intake requirements. This trend highlights the evolving preferences in the protein hydrolysates market, where innovation in product formats and functionality plays a critical role in market expansion.

Increasing Demand for Clean-Label Plant-Based Hydrolysates

As manufacturers strive for clean-label positioning, they face the challenge of eliminating synthetic additives without compromising protein functionality. This necessitates the use of advanced enzymatic hydrolysis techniques that safeguard amino acid profiles. The increasing demand for clean-label plant-based hydrolysates is a significant driver of the protein hydrolysates market, as consumers increasingly prioritize transparency, sustainability, and natural ingredients in their food and beverage choices. Plant-based hydrolysates, in particular, align with the growing consumer preference for vegan and vegetarian diets, further boosting their adoption. Additionally, clean-label plant-based hydrolysates cater to the rising demand for allergen-free and easily digestible protein sources, making them a preferred choice across various applications, including infant nutrition, sports nutrition, and clinical nutrition. Research from CBI, the Ministry of Foreign Affairs, indicates that clean-label products are set to rise from 52% of portfolios in 2021 to over 70% in 2025 and 2026 [2]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities," www.cbi.eu, highlighting the growing importance of clean-label solutions in the protein hydrolysates market.

Technological Innovation in Protein Hydrolysis

Recent advances in enzymatic processing have transformed protein hydrolysates production across the protein hydrolysates market through specific enzyme selection and reaction condition optimization. Novozymes' Savinase protease enables a controlled degree of hydrolysis, reducing bitterness while maximizing bioactive peptide formation. The combination of ultrasonic pretreatment with dual oxidase systems enhances whey protein crosslinking and thermal stability by 25%, making protein hydrolysates suitable for heat-sensitive applications, according to MDPI research. Magnetic cross-linked cell aggregates (CLCAs) decrease processing costs by 40% while maintaining 70% enzyme activity after five reaction cycles, making hydrolysates viable for price-sensitive applications, as reported by Microbial Cell Factories. Fonterra and DSM's Vivici joint venture has achieved commercial production levels of beta-lactoglobulin through precision fermentation, eliminating the need for livestock inputs. The integration of artificial intelligence enables real-time optimization of hydrolysis parameters, reducing batch variations and ensuring consistent yields across different production scales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Off-Notes and Bitterness Restrict Adoption of Protein Hydrolates Ingredients | -1.9% | Global, particularly in consumer-facing applications | Short term (≤ 2 years) |

| Price Volatility of Raw Materials | -1.6% | Global, with acute impact in commodity-dependent regions | Short term (≤ 2 years) |

| Stringent Regulations around Health Claims, Labeling, and Usage | -1.2% | Global, with varying intensity by jurisdiction | Medium term (2-4 years) |

| High Cost of Processing and Ingredient Isolation | -0.8% | Global, affecting smaller manufacturers disproportionately | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Off-Notes and Bitterness Restrict Adoption of Protein Hydrolates Ingredients

The protein hydrolysates market faces significant restraints due to the off-notes and bitterness associated with protein hydrolysate ingredients. These sensory drawbacks often impact the overall taste profile of end products, making them less appealing to consumers. As a result, manufacturers encounter difficulties in incorporating these ingredients into food and beverage formulations without compromising flavor. This challenge limits the widespread adoption of protein hydrolysates across the protein hydrolysates market, particularly in applications where taste is a critical factor. Additionally, the bitterness and off-notes pose challenges in product development, as masking these undesirable attributes often requires additional processing or the use of flavor enhancers, which can increase production costs. This further restricts the market's growth potential, especially in cost-sensitive segments. Addressing these issues remains a priority for market players aiming to expand the use of protein hydrolysates across various industries within the protein hydrolysates market, including functional foods, dietary supplements, and infant nutrition.

Price Volatility of Raw Materials

The protein hydrolysates market faces a significant restraint due to the price volatility of raw materials. The costs of essential raw materials used in the production of protein hydrolysates, such as milk, soy, and other protein sources, are subject to frequent fluctuations. These price changes are influenced by various factors, including unpredictable weather conditions, supply chain disruptions, geopolitical tensions, and changes in agricultural policies. Such volatility directly impacts the production costs for manufacturers, making it challenging to maintain consistent pricing for end products. Additionally, the fluctuating raw material prices can lead to reduced profit margins for manufacturers, further hindering market growth. This instability in raw material costs poses a critical challenge for stakeholders in the protein hydrolysates market, as it affects both the supply chain and the overall market dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Dairy Faces Plant-Protein Disruption

In 2025, dairy proteins accounted for a significant 57.62% share of the protein hydrolysates market revenue, highlighting their established presence driven by mature supply chains and well-understood regulatory frameworks. Whey hydrolysates, derived from by-products of the cheese industry, have gained traction due to their high nutritional value and functional benefits, making them a preferred choice in sports nutrition and infant formula. Additionally, casein variants have carved a niche in clinical nutrition, where their ability to provide the desired viscosity and slow digestion properties makes them ideal for specialized dietary needs. The versatility and widespread applications of dairy proteins continue to reinforce their dominance in the market.

On the other hand, plant proteins are emerging as a rapidly growing segment within the protein hydrolysates market, with a projected CAGR of 10.63% from 2026 to 2031. This growth is fueled by increasing consumer demand for sustainable and plant-based alternatives, driven by rising health consciousness and environmental concerns. Plant protein hydrolysates, derived from sources such as soy, pea, and rice, are gaining popularity due to their hypoallergenic properties and suitability for vegan and vegetarian diets. Their applications span across functional foods, beverages, and dietary supplements, positioning them as a key growth driver in the market. The robust growth trajectory of plant proteins reflects their potential to reshape the protein hydrolysate landscape in the coming years.

By Degree of Hydrolysis: High-DH Products Drive Innovation

Medium-DH ranges (10-25%) accounted for 47.58% of the demand in the protein hydrolysates market in 2025. These ranges effectively balance digestibility and flavor, making them highly suitable for mainstream applications such as infant formulas and functional foods. Medium-DH protein hydrolysates are particularly favored in these segments due to their ability to provide essential nutrients while maintaining a palatable taste, which is crucial for consumer acceptance. Their versatility and compatibility with various formulations further enhance their demand in the protein hydrolysates market.

High-DH solutions, with degrees of hydrolysis exceeding 25%, are projected to grow at an impressive 11.72% CAGR across the protein hydrolysates market during the forecast period. This growth is primarily driven by their application in sports nutrition and clinical feeding, where rapid nitrogen absorption is critical. High-DH protein hydrolysates are preferred in these segments due to their ability to deliver quick and efficient protein uptake, which is essential for muscle recovery and medical nutrition. As the demand for specialized nutrition continues to rise, the adoption of high-DH solutions is expected to expand significantly.

By End-Use Application: Sports Nutrition Accelerates Beyond Infant-Formula Leadership

In 2025, the protein hydrolysates market witnessed significant traction in the infant nutrition segment, capturing 46.05% of the market share. This growth was primarily driven by strong medical endorsements and an increasing willingness among the middle class to invest in specialized allergy-managed formulas. Reformulated standards in the segment now emphasize higher protein quality scores, which have elevated the demand for hydrolysates in premium stock-keeping units (SKUs). These hydrolysates, known for their enhanced digestibility and reduced allergenic potential, are becoming a preferred choice for parents seeking optimal nutrition for their infants.

In the sports nutrition segment, the protein hydrolysates market is experiencing robust growth, with a CAGR of 13.02%. This expansion is fueled by the increasing adoption of active lifestyles and the growing preference for convenient, ready-to-drink (RTD) and clear beverage formats. These formats require fully soluble peptides, which hydrolysates effectively provide, ensuring superior mixability and functionality. The demand for hydrolysates in sports nutrition is further supported by their rapid absorption and ability to aid muscle recovery, making them a popular choice among fitness enthusiasts and athletes. As consumers continue to prioritize health and performance, the sports nutrition segment is expected to remain a key driver of growth in the protein hydrolysates market.

Geography Analysis

In 2025, the Asia-Pacific region secures a commanding 38.05% share of the protein hydrolysates market, driven by a surge in protein awareness, the rise of a middle class, and an increasing shift towards Western dietary habits emphasizing protein supplementation. China and Indonesia emerged as the top global importers of whey powders, with import values reaching USD 811.09 million and USD 209.53 million, respectively, as reported by ITC Trade Map. Japan enforces stricter regulations on dairy, requiring comprehensive documentation for products fortified with probiotics. At the same time, Indonesia's BPOM Regulation No. 10 of 2024 introduces specific labeling requirements for health supplements, with a particular emphasis on protein hydrolysates.

The Middle East and Africa emerge as the fastest-growing regions, boasting an impressive 11.05% CAGR from 2026 to 2031. This surge is largely attributed to heightened concerns over protein deficiencies and a burgeoning awareness of the benefits of nutritional supplementation, especially in urban locales with increasing disposable incomes. The U.S. Meat Export Federation highlights the vast potential for affordable protein sources in African markets. However, it's worth noting that constraints in purchasing power confine the adoption of premium products to a select niche segment.

North America and Europe collectively represent mature markets for the protein hydrolysates market, driven by well-established health and wellness trends and a strong focus on fitness and dietary supplementation. In North America, the United States leads the market, supported by high consumer awareness and the widespread availability of protein-based products. The region also benefits from ongoing innovations in protein hydrolysate formulations, catering to diverse consumer preferences. Meanwhile, Europe sees steady growth, underpinned by increasing demand for clean-label and plant-based protein hydrolysates. Regulatory frameworks in both regions, such as the FDA guidelines in the United States and EFSA regulations in Europe, ensure product quality and safety, further bolstering consumer confidence.

Competitive Landscape

The protein hydrolysates market demonstrates a moderate concentration level, with competition driven by both established dairy processors and emerging biotechnology firms. Established players leverage vertical integration to optimize their supply chains and reduce costs, giving them a competitive edge. These companies in the protein hydrolysates industry, including Arla Foods Ingredients, Fonterra, and Glanbia, benefit significantly from economies of scale in raw material procurement and their long-standing relationships with customers. Their ability to maintain consistent product quality and supply reliability further strengthens their market position.

However, the protein hydrolysates market is witnessing a shift as new entrants focus on innovative approaches to processing and sourcing, challenging the dominance of traditional players. Emerging biotechnology firms are differentiating themselves by exploring alternative protein sources and employing advanced processing technologies to meet evolving consumer demands. Disruption in the market is increasingly driven by precision fermentation companies, which bypass traditional agricultural inputs entirely. These companies are introducing innovative solutions that challenge the conventional production methods of protein hydrolysates. By leveraging cutting-edge fermentation technologies, they are creating high-quality, sustainable protein alternatives that appeal to environmentally conscious consumers. This shift is forcing established players to adapt and innovate to maintain their competitive edge. While traditional dairy processors still hold a significant share of the market, the growing influence of precision fermentation companies is reshaping the competitive landscape and creating new opportunities for collaboration and growth.

Strategic partnerships between established market leaders and technology innovators are becoming a key trend in the protein hydrolysates market. These collaborations aim to combine the strengths of traditional dairy expertise with the technological advancements of emerging firms. A notable example is the joint venture between Fonterra and DSM's Vivici, which integrates Fonterra's extensive dairy knowledge with DSM's fermentation capabilities to produce animal-free whey proteins. Such partnerships not only accelerate innovation but also enable companies to address the increasing demand for sustainable and alternative protein solutions. As the market evolves, these alliances are expected to play a crucial role in shaping the future of the protein hydrolysates industry.

Protein Hydrolysates Industry Leaders

-

Fonterra Co-operative Group Limited

-

Kerry Group plc

-

Arla Foods AMBA

-

Archer Daniels Midland Company

-

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Arla Foods Ingredients has launched Lacprodan DI-3092, a new whey protein hydrolysate, targeting challenges in peptide-based medical nutrition. This ingredient boasts 10g of protein per 100ml, a figure the company claims is "significantly higher" than the typical 6-7g in similar products.

- August 2024: Fonterra is set to bolster its Studholme facility on New Zealand's South Island, focusing on ramping up production of premium protein ingredients. This initiative underscores the company's ambition to fortify its foothold in the international dairy arena. With a hefty investment of USD 47.13 million, the expansion underscores Fonterra's dedication to harnessing its prowess in dairy science and innovation.

- October 2023: Angel Yeast Co., Ltd unveiled a range of innovative biotechnology products at the 2023 CPHI Exhibition in Spain. Among the showcased items were the ultrafiltration yeast extract FM888, yeast protein hydrolysate FP108, soy protein hydrolysate FP408, along with cell wall, yeast protein, β-glucan, and several other key offerings.

Global Protein Hydrolysates Market Report Scope

Hydrolyzed protein is a solution derived from the hydrolysis of a protein into its component amino acids and peptides. The global protein hydrolysate market is segmented by source, form, application, and geography. By source, the market is segmented into plant and animal. By form, the market is bifurcated into dry and liquid forms. Based on the application, the market is segmented into sports nutrition, dietary supplements, food products, and others. The geographical analysis includes regions such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Animal Protein | Dairy Protein | Whey |

| Casein & Caseinates | ||

| Egg Protein | ||

| Gelatin and Collagen | ||

| Other Animal Proteins | ||

| Plant Protein | Soy | |

| Pea | ||

| Wheat | ||

| Rice | ||

| Potato | ||

| Hemp | ||

| Others |

| Low DH ( <10 %) |

| Medium DH (10-25 %) |

| High DH (>25 %) |

| Infant Nutrition |

| Sports Nutrition |

| Clinical and Medical Nutrition |

| Specialized Food and Beverage |

| Animal Nutrition |

| Personal Care and Cosmetics |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Animal Protein | Dairy Protein | Whey |

| Casein & Caseinates | |||

| Egg Protein | |||

| Gelatin and Collagen | |||

| Other Animal Proteins | |||

| Plant Protein | Soy | ||

| Pea | |||

| Wheat | |||

| Rice | |||

| Potato | |||

| Hemp | |||

| Others | |||

| By Degree of Hydrolysis | Low DH ( <10 %) | ||

| Medium DH (10-25 %) | |||

| High DH (>25 %) | |||

| By End-Use Application | Infant Nutrition | ||

| Sports Nutrition | |||

| Clinical and Medical Nutrition | |||

| Specialized Food and Beverage | |||

| Animal Nutrition | |||

| Personal Care and Cosmetics | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current size of the protein hydrolysates market?

The protein hydrolysates market is worth USD 4.17 billion in 2026.

How fast will the protein hydrolysates market grow through 2031?

It is projected to expand at a 9.81% CAGR, reaching USD 6.67 billion by 2031.

Which source category leads the protein hydrolysates market?

Dairy protein hydrolysates command 57.62% market share, though plant proteins are growing faster.

Why are high-degree hydrolysates important for sports nutrition?

High-DH peptides offer quicker amino-acid absorption, supporting rapid muscle recovery and enabling clear RTD beverage formulations.

Page last updated on: