Hydrogen Fuel Cell Vehicle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

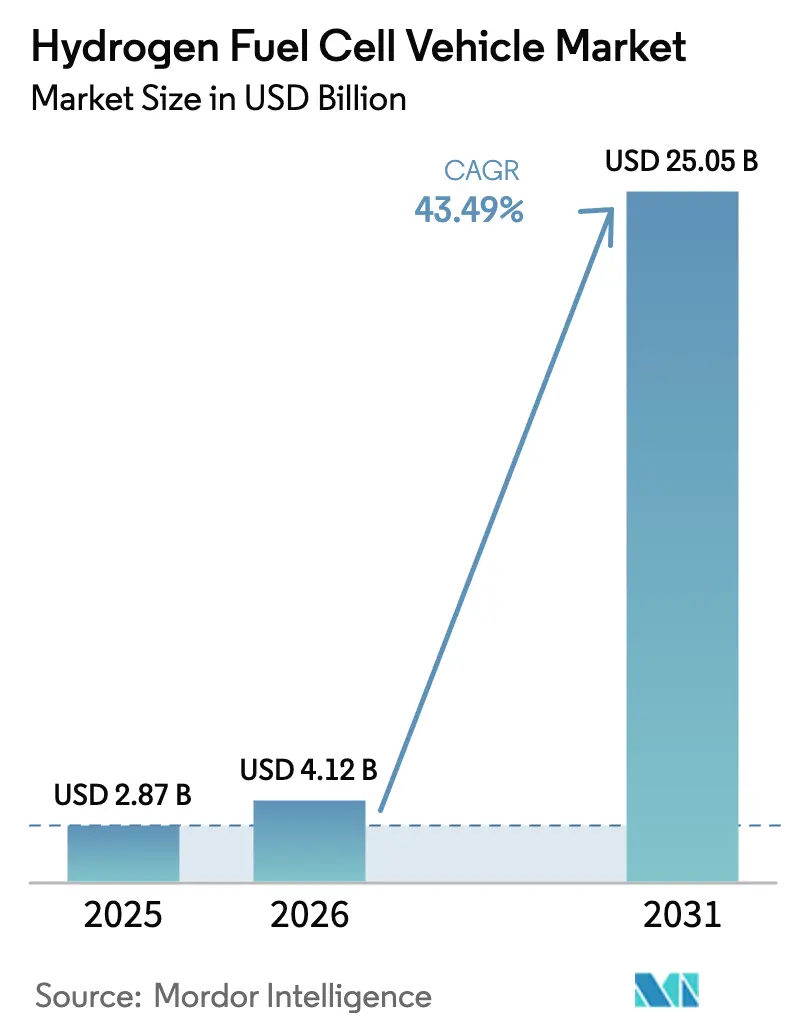

| Market Size (2026) | USD 4.12 Billion |

| Market Size (2031) | USD 25.05 Billion |

| Growth Rate (2026 - 2031) | 43.49% CAGR |

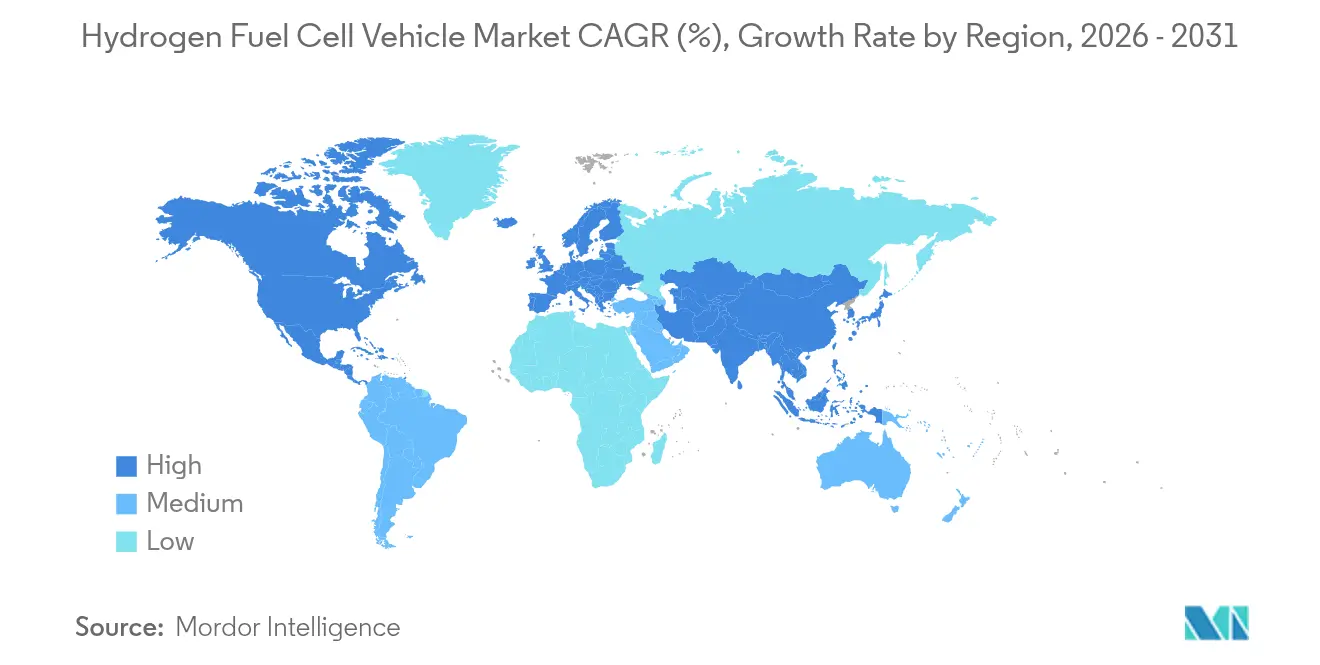

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

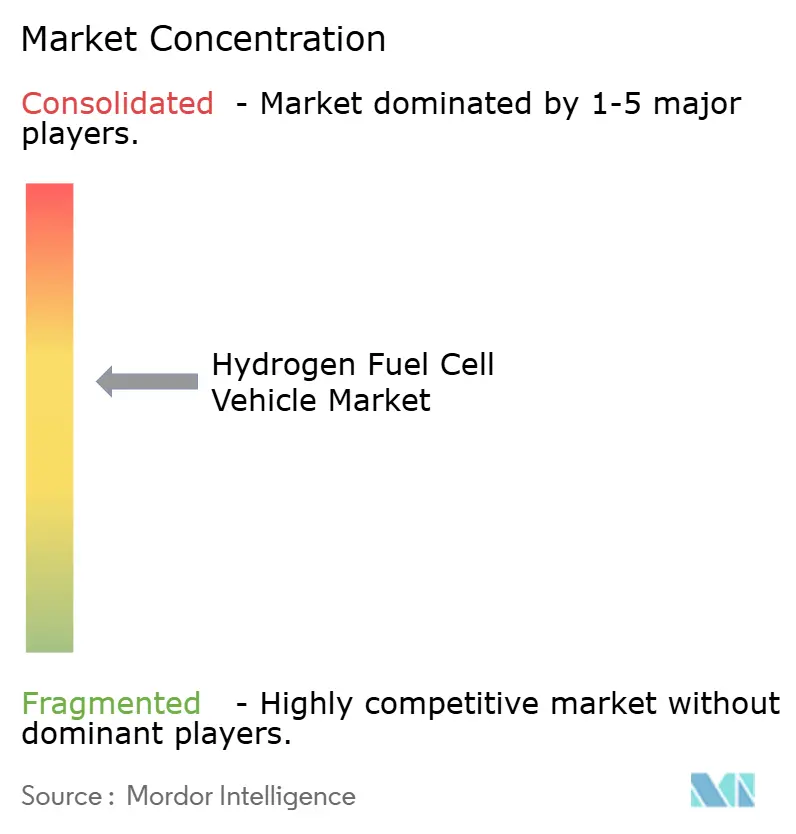

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrogen Fuel Cell Vehicle Market Analysis by Mordor Intelligence

Hydrogen Fuel Cell Vehicle Market size market size in 2026 is estimated at USD 4.12 billion, growing from 2025 value of USD 2.87 billion with 2031 projections showing USD 25.05 billion, growing at 43.49% CAGR over 2026-2031. Stacking cost breakthroughs that pushed proton-exchange membrane fuel cell (PEMFC) systems below USD 600 /kW in 2024 underpin the new commercial reality. Tight zero-emission-vehicle quotas, especially for heavy-duty fleets in the European Union, China, and a dozen U.S. states, are compelling fleet owners to adopt hydrogen powertrains faster than originally forecast. Extensive green-hydrogen corridors funded by Brussels, Beijing, and Tokyo increase refueling access every quarter, cutting range anxiety and bolstering residual values.

Key Report Takeaways

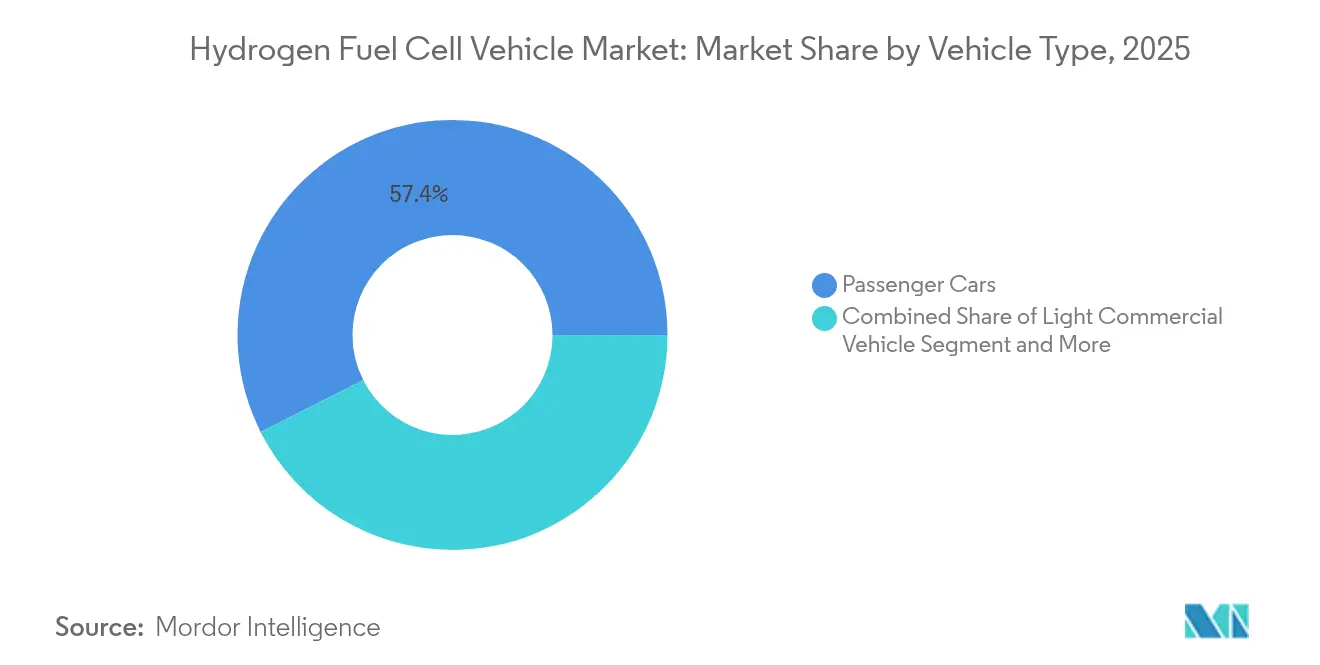

- By vehicle type, passenger cars led 57.44% of the hydrogen fuel cell market share in 2025; medium and heavy commercial vehicles are forecast to advance at a 46.47% CAGR through 2031.

- By technology, PEMFC systems accounted for 72.48% of the hydrogen fuel cell vehicle market size 2025 and are expected to climb at a 42.95% CAGR between 2026 and 2031.

- By driving range, 251-500 mile models captured 51.62% of the hydrogen fuel cell vehicle market share in 2025, whereas vehicles exceeding 500 miles are projected to expand at a 44.38% CAGR to 2031.

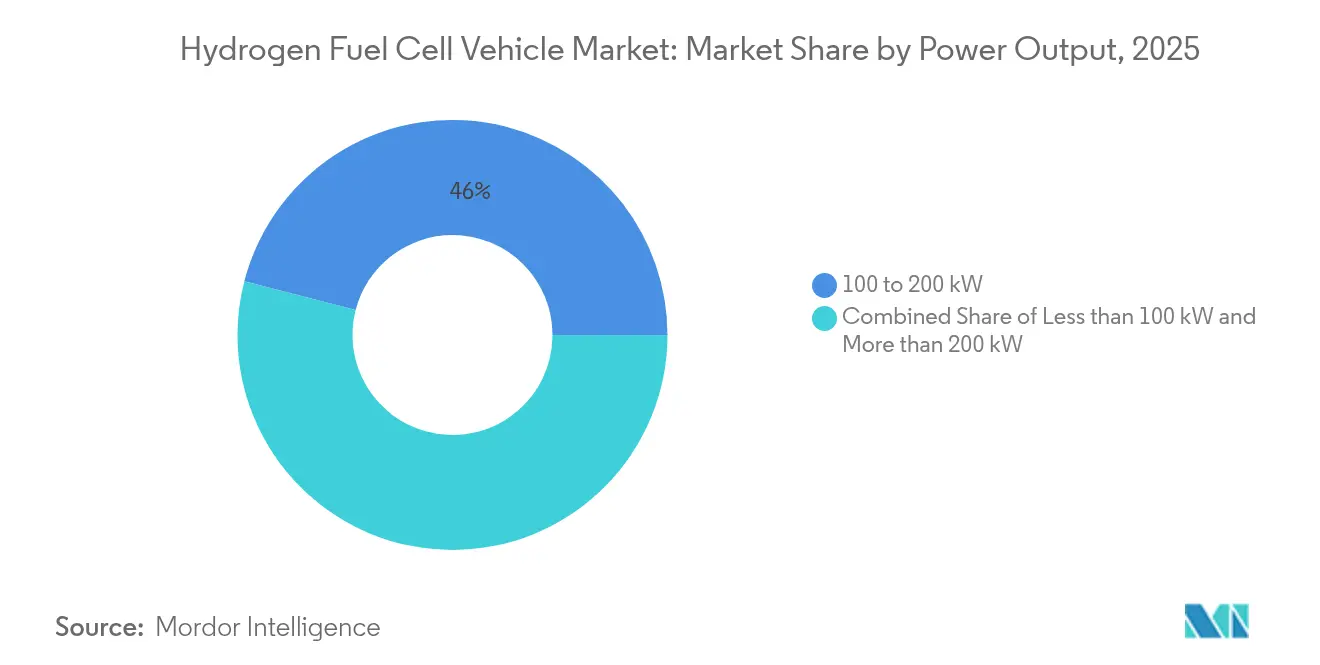

- By power output, the 100-200 kW class represented 45.98% of the hydrogen fuel cell vehicle market size 2025; systems above 200 kW will grow at a 44.92% CAGR through 2031.

- By end-use ownership, private buyers dominated with 64.05% market share in 2025, while logistics and freight operators will register the fastest growth at 44.10% CAGR to 2031.

- By geography, Asia Pacific held 42.88% of global revenue in 2025; it also records the highest regional CAGR at 40.35% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Hydrogen Fuel Cell Vehicle Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Decarbonization Mandates | +10.5% | Global, with early gains in EU, California, China | Medium term (2-4 years) |

| Falling USD/kW of PEMFC Stacks Below USD600 | +8.1% | Global | Short term (≤ 2 years) |

| Rapid Scale-up of Green-Hydrogen Refueling | +7.7% | EU core, China, spill-over to North America | Long term (≥ 4 years) |

| Renewable-Curtailment-Linked Hydrogen Offtake Contracts | +4.9% | Middle East and Africa, Australia, Chile, with export to Asia-Pacific & EU | Long term (≥ 4 years) |

| Port and Airport Zero-Emission Fleet Programs | +4.1% | Global coastal regions, major transport hubs | Medium term (2-4 years) |

| On-Board Ammonia-to-H2 Cracking Prototypes | +3.1% | North America & EU, Asia-Pacific adoption following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Decarbonization Mandates & ZEV Quotas

The European Union now requires 45% CO₂ reduction for new heavy-duty vehicles by 2030 and 90% by 2040. California’s Advanced Clean Fleets rule obliges drayage fleets to turn fully zero-emission by 2035, while 12 additional U.S. states mirror the mandate. China’s 2060 carbon-neutrality pledge underpins large-scale subsidies for fuel-cell trucks, and the Renewable Energy Directive III creates upstream demand for green hydrogen. Such converging regulations are recalibrating fleet procurement models toward compliance first, cost second.

Falling USD /kW of PEMFC Stacks Below USD 600 Driven by Pt-Loading Cuts

Platinum-alloy catalysts guided by machine-learning models now double activity and durability. Toyota’s third-generation stack trims platinum loading by 35%, boosting fuel efficiency by 20% and slicing total stack cost to USD 585 /kW in 2024.[1]Toyota Motor Corporation, “Fuel Cell System Gen 3 Technical Briefing,” global. Toyota The advance hits the industry’s commercial viability threshold and immediately feeds larger OEM order books, accelerating cost-down curves through volume manufacturing.

Rapid Scale-Up of Green-Hydrogen Refueling Corridors in EU & China

The Alternative Fuels Infrastructure Regulation insists on hydrogen stations every 200 km along the TEN-T core network by 2031. Germany already operates 86 public stations, which is equal to 46% of Europe’s network, and Brussels committed EUR 1 billion to extend corridors to ports and industrial hubs.[2]Federal Ministry for Digital & Transport (Germany), “Hydrogen Refueling Station Network Update,” bmdv.bund.de China targets 1,200 stations by 2025, concentrating on industrial clusters that host long-haul freight routes, ensuring high utilization from day one.

Port & Airport Zero-Emission Fleet Programs

Ports from Los Angeles to Hamburg deploy fuel-cell drayage trucks, yard tractors, and ground-support equipment that refuel in five minutes while maintaining payload limits. Centralized operations provide anchor demand, letting infrastructure investors secure bankable throughput contracts. Airports leverage industrial-gas know-how to handle hydrogen safely, offering a blueprint for other hub-and-spoke fleets.

Restraints Impact Analysis of Hydrogen Fuel Cell Vehicle Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO Gap vs BEVs in Light-Duty Segment | -8.3% | Global, particularly pronounced in passenger car markets | Short term (≤ 2 years) |

| Sparse Fueling Infrastructure | -6.7% | Global, most severe in rural and secondary markets | Medium term (2-4 years) |

| PGMs Supply-Chain Tightness and Price Volatility | -5.2% | Global, concentrated impact in South Africa & Russia sourcing | Medium term (2-4 years) |

| Investor Shift Toward H2-ICE and E-fuels | -4.1% | EU & North America, with spillover to developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High TCO Gap vs BEVs in Light-Duty Segment

Hydrogen costs USD 8-12 per kilogram today, translating to per-mile expenses roughly double those of equivalent BEVs that recharge at home overnight. Fuel-cell car acquisition prices sit 50-100% above comparable electric models, and second-hand values remain uncertain. Until fuel prices drop and stack lifetimes hit 200,000 hours, fleet operators will keep hydrogen cars mainly in high-utilization niches.

Sparse Fueling Infrastructure Outside Early Adopter Clusters

Europe counted more than 150 open stations in May 2024, versus 600,000 plus public EV chargers. California’s active station count experienced a slight dip. Utilization rates under 30% deter investors, especially in rural corridors where payback exceeds 10 years. Station capex of USD 1-2 million still relies on subsidies, limiting roll-outs to government-backed zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Hydrogen Fuel Cell Vehicle Market Segment Analysis

By Vehicle Type:

Commercial Vehicles Drive Market TransformationMedium and heavy commercial vehicles grew from a small base to command 46.47% CAGR between 2026 and 2031, even though passenger cars retained a 57.44% share in 2025. The hydrogen fuel cell vehicle market size for trucks and buses reached USD 1.03 billion in 2025, reflecting strong demand from logistics players seeking lower refueling downtime and higher payload versus battery options. Hyundai expanded annual bus production capacity from 500 to 3,100 units, signaling industry confidence in high-mileage duty cycles. Operators operating fixed routes now benefit from depot refueling, which secures volume and improves station economics. Passenger cars remain important but infrastructure-constrained, with buyers in California, Tokyo, and Shanghai, where networks exist.

A second wave of adoption emerges as OEMs deploy modular fuel-cell platforms for vans and 44-ton tractors. Toyota’s strategy shift toward fleet-focused platforms underscores where value lies: predictable, intensive routes that leverage hydrogen’s energy density. The hydrogen fuel cell vehicle market, therefore, witnesses commercial fleets turbo-charging volume, allowing passenger-car economies of scale to catch up post-2030.

By Technology:

PEMFC Dominance Amid Emerging AlternativesProton exchange membrane stacks captured 72.48% of 2025 revenue and will maintain a 42.95% CAGR to 2031. This momentum keeps the hydrogen fuel cell vehicle market on a single dominant architecture, allowing suppliers to reduce cost through shared tooling. Solid oxide options remain limited by 700 °C operating temperatures, while alkaline cells are relegated to forklifts and niche material-handling roles. BMW and Toyota’s joint 2026 stack promises 30% higher power density, reinforcing the incumbents’ lead.

Continued breakthroughs in ultra-low-platinum catalysts, ionomer membranes with higher proton conductivity, and bipolar plate stamping push PEMFC costs down annually. Manufacturers explore hybrid powertrains pairing PEMFCs with small batteries to handle transient peaks, a strategy extends stack life and eases thermal management demands. Competing chemistries must therefore carve out highly specialized use cases, ensuring PEMFC technology sets the mainstream pace inside the hydrogen fuel cell vehicle market.

By Driving Range:

Long-Range Applications Accelerate GrowthModels spanning 251-500 miles held 51.62% of global deliveries in 2025, a sweet spot that matches daily freight loops and intercity coach distances. Yet, vehicles capable of more than 500 miles post a 44.38% CAGR as cryo-compressed storage tested by Lawrence Livermore National Laboratory boosts onboard density up to 165%. The hydrogen fuel cell vehicle market size for extended-range units is forecast to reach USD 8.44 billion in 2031, buoyed by long-haul truck mandates in Europe’s TEN-T corridors.

Urban applications requiring ≤250 miles rely on base-return logistics. Fleets operating such vehicles appreciate centralized refueling and steady stack loads, achieving 96% uptime compared with 88% for BEV counterparts that need multiple charging sessions. As infrastructure fills gaps along cross-country routes, OEM line-ups will likely migrate toward larger tanks and heavier loads to displace diesel in the longest hauls.

By Power Output:

High-Power Systems Enable Commercial ApplicationsThe 100-200 kW bracket accounted for 45.98% of 2025 shipments, serving most passenger cars and light trucks. Systems over 200 kW, however, will log a 44.92% CAGR because heavy-duty tractors, multi-axle buses, and vocational trucks require sustained high power. Cellcentric’s automated line in Weilheim targets 10,000 units annually above 230 kW, leveraging in-house membrane-electrode-assembly coating to cut per-stack cost by 18%.

Meanwhile, sub-100 kW units power forklifts, airport tugs, and refrigerated trailers. Specialists in this field refine durability under partial-load cycles, a key differentiator. The hydrogen fuel cell vehicle market thus bifurcates into high-volume, high-power modules for freight plus smaller bespoke stacks for material handling. Modular stack designs let OEMs mix two 120 kW units to meet a 240 kW rating, simplifying inventory and service training.

By End-Use Ownership:

Fleet Operators Lead AdoptionPrivate consumers still represented 64.05% of cars on the road in 2025, driven by early-adopter appeal in Japan, South Korea, and California. Yet logistics and freight operators will accelerate at 44.10% CAGR, reflecting hydrogen’s economic edge when high daily mileage amortizes capex quickly. DHL’s 2025 Saudi Arabian pilot covers a 1,000-km corridor between Riyadh and Dammam, gathering data on total cost of ownership at desert temperatures.

Public-sector fleets—police cruisers in Tokyo, shuttle buses in Hamburg—continue to de-risk technology for wider commercial adoption. They also unlock station sharing, giving private haulers reliable uptime today. As depreciation schedules favor multi-shift fleets, lease financiers roll out index-linked hydrogen supply contracts, lowering per-mile volatility for operators inside the hydrogen fuel cell vehicle market.

Geography Analysis

APAC Hydrogen Fuel Cell Vehicle Market

Asia Pacific serves as the nucleus of the hydrogen fuel cell vehicle market. The region controlled 42.88% of global revenue in 2025 and retained a 40.35% CAGR through 2031. China already has more than 6,500 fuel-cell trucks on the road, and plansto produce 1 million units by 2035. Its local governments subsidize up to around USD 55,000 per heavy truck and reimburse station operators per kilogram, guaranteeing the ecosystem's cash flow. Japan’s fuel-cell strategy dovetails automotive production with water-electrolysis exports, creating an end-to-end domestic value chain. South Korea’s Hyundai leverages around two fifth of the global vehicle share to anchor supplier capacity, and India’s National Green Hydrogen Mission seeds truck pilots along the Delhi-Mumbai freight corridor.

North America Hydrogen Fuel Cell Vehicle Market

North America ranks second, with California remaining the bellwether as it enforces drayage conversion deadlines. The Section 45V clean hydrogen tax credit pays up to USD 3/kg for low-carbon production, cutting retail pump prices in pilot hubs. Ballard’s USD 160 million Texas plant will supply up to 3 GW of MEA annually from 2026, reinforcing local content requirements that unlock further subsidies. Canada uses abundant hydroelectric power to feed electrolyzers in British Columbia and Quebec, while Mexico positions its industrial parks for export-ready fuel-cell truck assembly.

Europe and GCC Hydrogen Fuel Cell Vehicle Market

The EU’s EUR 6.9 billion state-aid package funds 119 refueling clusters, and the European Hydrogen Bank’s first auction awarded EUR 800 million in offtake contracts. Germany hosts almost 100 public stations, France follows just behind, and the Netherlands connects Rotterdam to the German Ruhr valley by 2027. Nordic countries add long-range pilots on the E6 artery from Oslo to Trondheim. Beyond the continent, Gulf states transform low-cost solar into competitive hydrogen exports; Saudi Arabia’s advanced logistics projects will eventually spur domestic vehicle adoption.

Competitive Landscape

Competition sits at a moderate concentration level. Toyota, Hyundai, and Honda draw on decades of stack R&D and vehicle integration know-how. They cooperate where volumes are subscale, evidenced by the 2025 BMW-Hyundai-Toyota Hydrogen Transport Forum that harmonizes standards across heavy-duty platforms. European truck makers like Daimler and Volvo embed Cellcentric stacks, while U.S. newcomers like Nikola focus on bundled truck-plus-fuel leasing models.

Cost reduction and durability remain the battlegrounds. UCLA’s 2025 breakthrough doubled catalyst life to 200,000 hours, a milestone rapidly licensed by four Tier-1 suppliers. Cummins and MAN explore hydrogen internal combustion engines (H2-ICE) for faster regulatory compliance, using existing driveline architecture for the 2027 product roll-out. Chinese players Yutong and Weichai leverage local incentives to scale domestically, then pivot to Southeast Asian export markets. Start-ups specializing in ammonia cracking, lightweight composite tanks, or cryo-compressed storage vie for niche segments, hoping to be acquired once OEMs finalize their 2030 supply chains.

Strategic moves increasingly combine manufacturing scale with forward-fuel contracting. Hyundai’s Ulsan hub will integrate electrolyzer output to guarantee green fuel, while Daimler Truck’s Würzburg expansion consolidates stack machining, bipolar-plate stamping, and module testing under one roof. This vertical integration protects IP, lowers cost, and secures ESG-compliant supply lines for institutional investors scrutinizing Scope 3 emissions.

Hydrogen Fuel Cell Vehicle Industry Leaders

Daimler AG

Honda Motor Co., Ltd.

SAIC Motor Corporation

Toyota Motor Corporation

Hyundai Motor Group

- *Disclaimer: Major Players sorted in no particular order

Hydrogen Fuel Cell Vehicle Market Companies Covered in this Report

- Toyota Motor Corporation

- Hyundai Motor Group

- Honda Motor Co., Ltd.

- Daimler Truck

- Nikola Corporation

- Ballard Power Systems

- Cummins Inc.

- Plug Power Inc.

- Robert Bosch GmbH

- Weichai Power

- SAIC Motor Corporation

- BYD FCEV

- Yutong Bus Co.

- Foton Motor

- Kenworth (PACCAR)

- BMW AG

- AUDI AG

- General Motors

- Renault Group

- Riversimple

Recent Industry Developments in Hydrogen Fuel Cell Vehicle Market

- June 2025: Daimler Truck expanded its Würzburg facility to boost hydrogen and battery-electric production capacity.

- May 2025: Sinotruk and Toyota signed a cooperation pact to accelerate fuel-cell commercial-vehicle deployment in China.

- May 2025: DHL and Hyperview agreed to pilot hydrogen trucks on key Saudi Arabian freight corridors.

- March 2025: Hyundai Motor confirmed a new fuel-cell production plant in Ulsan scheduled for mass output in 2028.

Hydrogen Fuel Cell Vehicle Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the hydrogen fuel cell vehicle market as all new on-road passenger cars and light, medium, or heavy-duty commercial vehicles in which a fuel-cell stack converts compressed hydrogen into electricity for traction. Propulsion batteries are treated as auxiliaries, not scope drivers.

Scope Exclusions: Vehicles powered by hydrogen internal-combustion engines, off-road machines, rail, marine, aerospace platforms, and refueling equipment are excluded.

Segments Covered in This Report

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicle

- Medium and Heavy Commercial Vehicle

- By Technology

- Proton Exchange Membrane Fuel Cell (PEMFC)

- Phosphoric Acid Fuel Cell (PAFC)

- Solid Oxide Fuel Cell (SOFC)

- Alkaline Fuel Cell (AFC)

- By Driving Range

- Less than or equal to 250 Miles

- 251 – 500 Miles

- More than 500 Miles

- By Power Output

- Less than 100 kW

- 100 – 200 kW

- More than 200 kW

- By End-Use Ownership

- Private / Personal

- Public & Government Fleet

- Logistics / Freight Operators

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Egypt

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews with automakers, stack vendors, fleet operators, and station developers across Asia, North America, and Europe let us verify deployment counts, average selling prices, refill economics, and duty cycles.

These conversations close the gaps left by secondary work and fine-tune model assumptions.

Desk Research

We begin by mapping fleet totals, station roll-outs, and hydrogen price curves from open sources such as the International Energy Agency, IRENA, the U.S. DOE Alternative Fuels Data Center, and the European Alternative Fuels Observatory.

Trade statistics from UN Comtrade and Eurostat clarify cross-border component flows, while peer-reviewed journals outline stack cost trajectories.

Next, policy papers and incentive catalogs reveal national zero-emission mandates. Company filings and reputable press add launch timelines.

According to Mordor analysts, paid resources like Marklines and Dow Jones Factiva augment competitive and financial intelligence.

The sources named illustrate our coverage, yet many additional references support every datapoint.

Market-Sizing & Forecasting

We build a top-down and bottom-up hybrid model.

National vehicle-parc data, new-registration shares, and refueling-station density yield the first cut, which we cross-check with sampled supplier revenues and channel feedback.

Key variables like average stack power rating, retail hydrogen price per kilogram, country-level clean-transport incentives, and battery-to-stack energy ratio feed a multivariate regression, while scenario analysis adjusts for policy or infrastructure delays.

Where supplier roll-ups miss startup activity, weighted estimates bridge the shortfall.

Data Validation & Update Cycle

We screen outputs against independent sales trackers and fuel-cell shipment tallies before a senior review.

Reports refresh each year, with interim updates whenever policy or technology shifts materially alter adoption curves.

How Mordor Intelligence's Hydrogen Fuel Cell Vehicle Market Size Compares to Other Published Estimates

Published estimates often diverge because firms draw different scope lines, assume static prices, or refresh infrequently.

Mordor's disciplined focus on fuel-cell-only drivetrains, live price inputs, and annual recalibration limits such drift. Key gap drivers elsewhere include excluding trucks and buses, bundling demonstrator units, or mixing infrastructure revenue with vehicle sales.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.87 B (2025) | Mordor Intelligence | - |

| USD 0.20 B (2024) | Global Consultancy A | Passenger cars only, limited primary checks, biennial refresh |

| USD 1.92 B (2023) | Global Consultancy B | Constant 2022 prices, bundles prototypes, trend extrapolation |

| USD 2.56 B (2024) | Industry Association C | Mixes vehicle and infrastructure revenue, unclear currency basis |

These contrasts show why Mordor's annually updated, variable-rich baseline offers decision-makers a balanced and transparent midpoint between narrow counts and optimistic roll-ups.

Key Questions Answered in the Report

What is the current size of the hydrogen fuel cell vehicle market?

The market stands at USD 4.12 billion in 2026 and is projected to reach USD 25.05 billion by 2031, driven by a 43.49% CAGR.

Which region leads hydrogen vehicle adoption?

Asia Pacific controls 42.88% of global revenue, with China, Japan, and South Korea leading the way in infrastructure and fleet deployment.

Why are commercial vehicles adopting hydrogen faster than passenger cars?

High mileage and tight zero-emission mandates make hydrogen’s quick refueling and longer range economically attractive for trucks and buses, while TCO still favors BEVs in typical car use.

How many hydrogen refueling stations does Europe plan to install?

EU rules mandate a public station at least every 200 km on core corridors by 2031, supported by EUR 6.9 billion in state aid.

What cost milestone unlocked large-scale commercialization?

Cutting the cost of the PEMFC stack below USD 600 /kW in 2024 met the auto industry’s target for viable mass production, spurring OEM rollout schedules.

Which technology dominates the hydrogen fuel cell vehicle industry?

PEMFC systems had a 72.48% market share in 2025 and will keep the lead thanks to superior power density, mature supply chains, and ongoing catalyst cost reductions.

Page last updated on: