Hybrid Work Hardware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

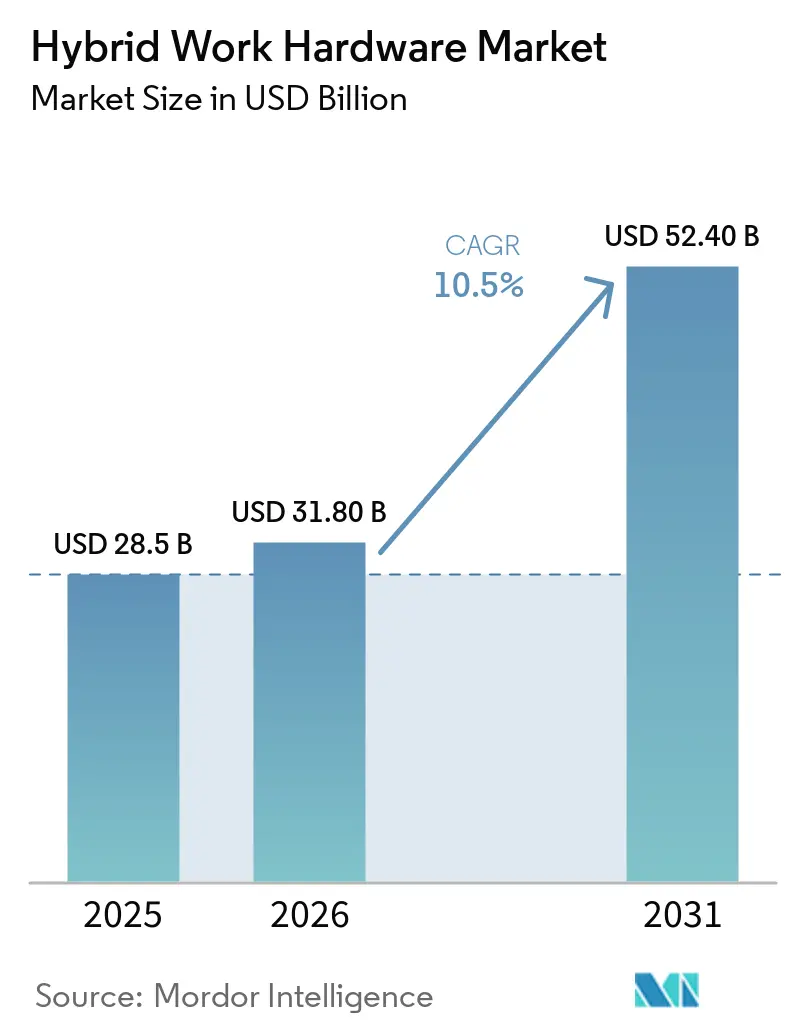

| Market Size (2026) | USD 31.80 Billion |

| Market Size (2031) | USD 52.40 Billion |

| Growth Rate (2026 - 2031) | 10.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Work Hardware Market Analysis by Mordor Intelligence

The Hybrid Work Hardware market size is expected to increase from USD 28.50 billion in 2025 to USD 31.80 billion in 2026 and reach USD 52.40 billion by 2031, growing at a CAGR of 10.50% over 2026-2031. Enterprises are now embedding collaboration endpoints into capital budgets, shifting from stop-gap webcam purchases toward room-grade infrastructure that enables equitable participation for on-site and remote employees. Procurement leaders are standardizing on AI-ready cameras and soundbars that promise long support lifecycles, while bring-your-own-meeting (BYOM) policies expand the addressable base by allowing staff to leverage existing laptops as soft codecs. Component shortages in early 2025 exposed supply-chain fragility, prompting vendors to dual-source silicon and prequalify alternative firmware images to avoid prolonged backorders. Competitive dynamics are intensifying as incumbents bundle hardware with cloud licenses, using ecosystem lock-in to defend margins even as white-box manufacturers race to commoditize standalone peripherals.

Key Report Takeaways

- By product type, computing devices led with 32.25% of the hybrid work hardware market share in 2025, while video conferencing and meeting room systems are forecast to expand at a 12.8% CAGR through 2031.

- By organization size, large enterprises accounted for 68.46% of 2025 expenditure, yet small and medium-sized enterprises are projected to grow at a 12.24% CAGR over 2026-2031.

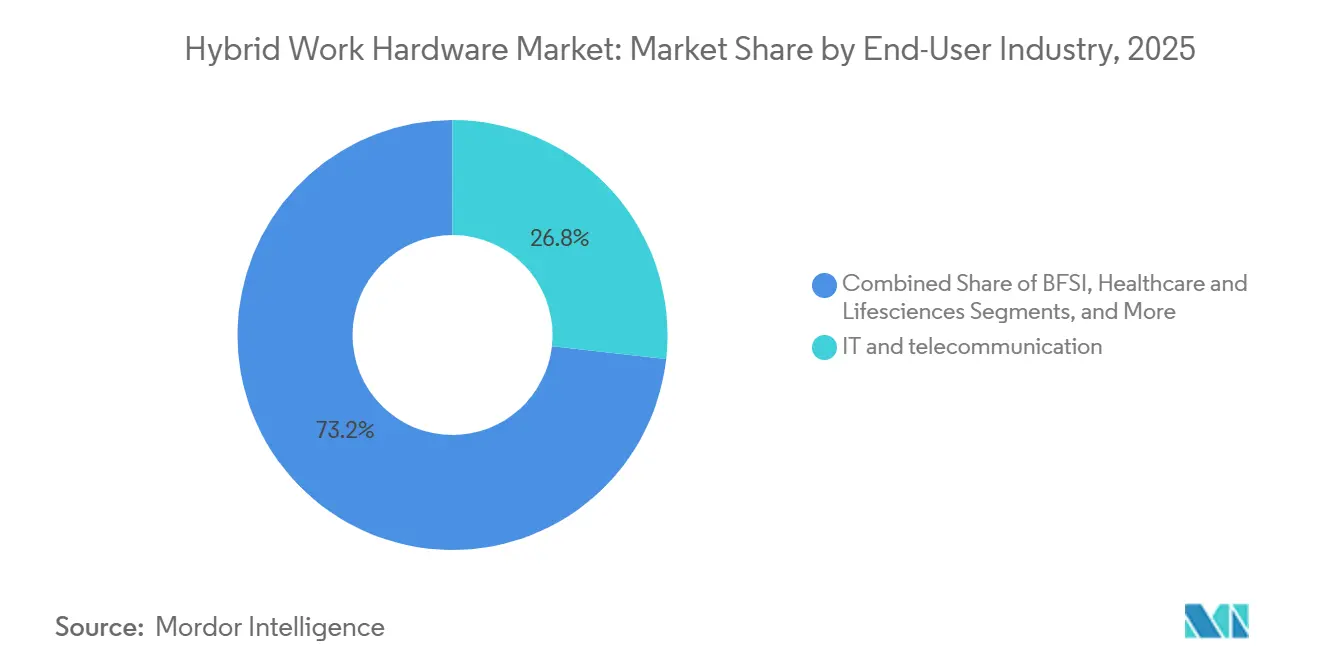

- By end-user industry, the IT and telecommunications sector accounted for 26.78% of 2025 deployments, whereas education is advancing at a 13.24% CAGR through 2031.

- By distribution channel, offline channels retained 65.80% revenue share in 2025, but online procurement is rising at a 12.86% CAGR during the forecast period.

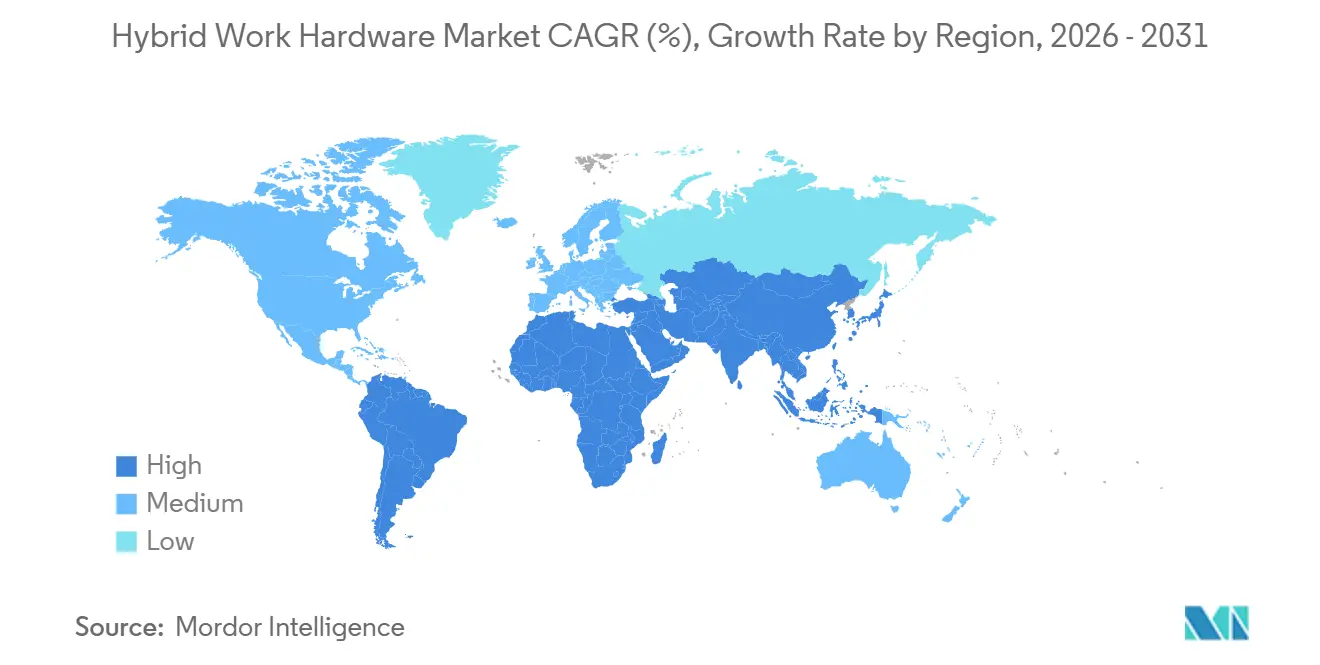

- By geography, North America commanded 36.46% of 2025 revenue, while Asia-Pacific is on track for a 12.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hybrid Work Hardware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bring Your Own Meeting Policies | +2.8% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Surge in Video Conferencing Adoption | +2.4% | Global | Medium term (2-4 years) |

| Upgrades to Conference Rooms | +2.1% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| AI-Powered Meeting Equity Features | +1.6% | North America, Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Expansion of High-Speed Broadband and 5G | +1.2% | Asia-Pacific core, Middle East, Africa emerging | Long term (≥ 4 years) |

| Tax Incentives for Remote Work Equipment | +0.4% | United States, Canada, select European nations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Bring Your Own Meeting Policies

BYOM policies shorten hardware refresh cycles because employees can connect personal laptops to USB speakerphones and auto-framing cameras without proprietary codecs, bypassing complex IT provisioning. Owl Labs reported that 63% of hybrid workers in 2025 favored BYOM layouts that mirror familiar desktop interfaces.[1]Owl Labs, “The State of Hybrid Work 2025,” OWLLABS.COM The preference aligns with the 12.8% CAGR expected for conference-room systems as firms replace fixed boxes with software-agnostic soundbars. Samsung, Cisco, and Logitech countered the trend in February 2026 by unveiling pre-integrated bundles that promise zero-touch deployment, an ecosystem play that trades openness for administrative simplicity. Organizations embracing modular BYOM still gain leverage when renegotiating SaaS contracts because hardware remains decoupled from licensing terms, preserving optionality in the 2028-2030 refresh window.

Surge in Video Conferencing Adoption Post Pandemic

Although webcam penetration peaked by 2024, spending persists as first-wave endpoints reach end of life and users demand 4K optics, neural noise suppression, and edge-based analytics. Logitech’s Rally AI cameras, launched in January 2026, embed dedicated processors that execute speaker tracking locally, mitigating cloud round-trip latency and satisfying data-sovereignty mandates in healthcare and finance.[2]Logitech, “Rally AI Camera,” LOGITECH.COM University lecture-hall retrofits costing USD 8,000-15,000 per room underpin education’s double-digit CAGR, with ceiling-mounted arrays enabling asynchronous playback for students in distant time zones. Appliance-style offerings, like Crestron’s Collab Compute, package compute, touch control, and licensing into one SKU, reducing bill-of-materials complexity and accelerating deployment CRESTRON.COM.

Upgrades to Conference Rooms for Hybrid Collaboration

Meeting-equity metrics now inform renovation budgets, shifting focus from cosmetic AV facelifts to environmental factors that balance visual and audio parity between in-room and remote participants. UCToday’s 2025 checklist noted that 72% of hybrid sessions fail when off-site attendees cannot hear sidebar exchanges, prompting the adoption of 360-degree cameras and ceiling mic grids. Crestron’s early access to Teams Rooms APIs lets its touch panels trigger lighting scenes and motorized shades, justifying USD 12,000-25,000 per-room premiums that were once viewed as discretionary. As enterprises hard-code HVAC and lighting events into meeting workflows, switching to alternate control ecosystems requires costly script rewrites, effectively stretching replacement cycles to seven years.

Rising Demand for AI-Powered Meeting Equity Features

Machine-learning functions, including live transcription, language translation, sentiment cues, and adaptive beamforming, are evolving from premium differentiators to baseline check-boxes. Zoom embedded its AI Companion directly in certified hardware in 2024, avoiding cloud exposure that violates HIPAA and GDPR. Google’s 2025 Gemini rollout added live translation across 40 languages to Meet endpoints. Premium tiers now include on-device neural silicon, creating a widening performance gap versus entry webcams that offload burden to host CPUs, reducing battery life on ultraportables. Education’s 13.24% CAGR is partially driven by AI lecture-capture solutions that auto-index keywords, enabling searchable repositories and offsetting the need for dedicated videography staff.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and Data Privacy Concerns | −1.4% | Global, heightened scrutiny in Europe and North America | Short term (≤ 2 years) |

| Budget Constraints for Small and Medium Businesses | −1.2% | Global, acute pressure in emerging markets | Medium term (2-4 years) |

| Environmental Regulations on Display Materials | −0.6% | Europe, spillover to North America and Asia-Pacific | Long term (≥ 4 years) |

| Component Shortages in Audio Chipsets | −0.5% | Global, supply-chain concentration in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and Data Privacy Concerns in Collaborative Devices

Always-on cameras and microphones expand the attack surface that malicious actors exploit through firmware implants and man-in-the-middle attacks. AVIXA’s 2024 survey indicated 58% of IT leaders delayed hardware rollouts until vendors proved ISO 27001-certified manufacturing and secure boot chains.[3]AVIXA, “Cybersecurity in AV: 2024 Industry Survey,” AVIXA.ORG Enterprises now specify Trusted Platform Modules and auto-patch utilities, adding USD 100-200 per endpoint yet averting potential GDPR fines equal to 4% of annual turnover. The trend elevates incumbent brands that publish CVE disclosures and fund bug-bounty programs, while penalizing white-box entrants with opaque supply chains.

Budget Constraints for Small and Medium Businesses

SMBs allocate only 3-5% of revenue to IT, according to Digital Origin’s 2025 spending analysis. A USD 2,500 conferencing bar competes with payroll or inventory investments, pushing many firms to refurbished webcams or software echo-cancellation that erodes call quality. Although the United States and Canadian tax codes allow companies to expense up to USD 2,500 of remote-work gear per employee in 2025, limited accounting staff means many SMBs fail to claim the benefit. Vendors are responding with hardware-as-a-service options that spread costs into predictable monthly fees, supporting the 12.24% CAGR forecast for SMB uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Video Conferencing Systems Outpace Computing Devices

Hybrid Work Hardware market size leadership in 2025 rested with computing devices, which held a 32.25% share, yet video conferencing systems are poised for faster expansion at a 12.8% CAGR through 2031. Computing endpoints have commoditized, with average business-laptop prices dropping 8% in 2025 as component spec sheets homogenized. Peripherals bridge the gap, exemplified by Jabra PanaCast’s on-device DSPs that reduce cloud latency, while networking and connectivity hardware, such as Wi-Fi 6E routers, ensure bandwidth symmetry for multi-stream meetings. Collaboration boards and interactive whiteboards are ascending in education and healthcare, where touch-enabled annotation brings remote cohorts into room-based workflows. Ancillary categories like ergonomic lighting kits grow more slowly but round out holistic hybrid-work bundles.

Across the forecast horizon, enterprises will redirect capital from refreshed notebooks toward conference-room modernization, a shift accelerated by BYOM, as one smart bar can serve an entire team rather than multiple laptops per employee. Hybrid Work Hardware market share is therefore poised to rebalance toward shared-space infrastructure, especially as vendors collapse compute, control, and connectivity into single SKUs such as Crestron’s Collab Compute. The greater margin resident in integrated room solutions grants vendors budget to embed neural accelerators, effectively raising the technology bar for late-comer competitors.

By Organization Size: SMEs Narrow the Gap

The hybrid Work Hardware market size is skewed toward large enterprises, with 68.46% in 2025, leveraging global contracts, bulk discounts, and in-house AV teams. Small and medium-sized enterprises, while resource-constrained, are projected to post a 12.24% CAGR, gradually narrowing the gap through 2031. The inflection stems from USB-based bars that require no specialist integrators, allowing office managers to install endpoints in under an hour. Financing models also level the playing field with HP, Dell, and Lenovo, which are now pricing laptops, monitors, and peripherals as monthly subscriptions, aligning with SMB cash-flow realities.

Large enterprises will continue controlling the premium tier, negotiating bundles of hardware, SaaS licenses, and five-year managed-services addenda. However, many have begun adopting flexible procurement practices that mirror consumer e-commerce, demanding transparent SKU-level pricing and next-day delivery, similar to what SMBs enjoy. As BYOM proliferates, the support burden falls from centralized IT to employees, reducing the staffing advantage historically enjoyed by large firms, although governance requirements such as zero-trust device posture still favor well-resourced organizations.

By End-User Industry: Education Surges Ahead

The IT and telecommunication vertical dominated deployments at 26.78% in 2025, naturally adopting advanced AV stacks given its technical fluency. Education, however, claims the fastest runway with a 13.24% CAGR, catalyzed by lecture-capture retrofits that blend in-person and remote attendance. Universities now specify ceiling microphone arrays that auto-isolate speakers and AI cameras that pan across classrooms, lessening the need for videography crews. Healthcare mirrors this momentum by installing telemedicine suites that comply with HIPAA, demanding medical-grade displays and encrypted video streams.

BFSI institutions remain conservative, prioritizing firmware-signed devices and on-premise key management to avoid regulatory penalties. Retailers and consumer brands deploy meeting hardware in distribution hubs for virtual product launches, though adoption rates trail knowledge-centric sectors. Government agencies emphasize accessibility compliance, which prolongs procurement cycles but yields multi-year contracts once wrapped. Manufacturing rounds out the landscape with ruggedized endpoints capable of filtering machinery noise, while media and entertainment studios adopt broadcast-quality cameras for low-latency remote production, a niche commanding high selling prices.

By Distribution Channel: Online Gains Ground

Offline integrator sales captured 65.80% of revenue in 2025 because enterprises still value site surveys, acoustic tuning, and hands-on demos before awarding six-figure contracts. Online channels, however, are accelerating at a 12.86% CAGR as e-catalog portals package hardware, cloud licenses, and managed services onto a single invoice, an approach that resonates with resource-constrained buyers. CANCOM’s marketplace, for instance, lets administrators order monitors alongside Microsoft 365 subscriptions, then manage both through a unified dashboard.[4]CANCOM, “E-Business – English – CANCOM eBusiness,” CANCOM.COM

Hybrid Work Hardware market share is expected to tilt incrementally toward online as virtual showrooms mature, using augmented-reality previews and AI-driven SKU recommendations to close the tactile gap. Nonetheless, high-complexity projects, such as multi-room headquarters retrofits, for example, will likely remain offline to leverage white-glove services that justify higher margins. A hybrid sales architecture is emerging: online marketplaces embed concierge chat, while traditional resellers launch web storefronts, blurring historic channel distinctions.

Geography Analysis

North America accounted for 36.46% of the Hybrid Work Hardware market revenue in 2025, underpinned by Fortune 500 refresh cycles and tax deductions for home-office equipment. The region benefits from mature fiber backbones and pervasive Wi-Fi 6E rollouts, ensuring that full-resolution 4K streams rarely downgrade. State and provincial grants further subsidize equipment for public-sector employees, broadening addressable demand beyond corporate headquarters. Yet cybersecurity regulations, such as the California Privacy Rights Act, increase compliance costs, nudging buyers toward established brands with documented vulnerability disclosure programs.

Asia-Pacific is on course for a 12.62% CAGR, the fastest worldwide. Government-funded 5G expansion in Singapore, India, and Japan removes latency bottlenecks and supports real-time, multi-participant whiteboarding. India’s Production-Linked Incentive scheme for electronics attracts contract manufacturing from Logitech and Yealink, lowering import duties and shortening logistical lead times. Japanese employers, facing demographic labor shortages, embrace hybrid work models to tap non-urban talent pools; this shift drives high demand for compact, apartment-friendly conferencing bars rather than large-format displays prevalent in U.S. home offices. Simultaneously, local brands leverage linguistic localization and culturally specific UI cues to edge out Western incumbents.

Europe’s growth lags because environmental mandates increase compliance costs. The November 2025 sunset of the RoHS exemption for cadmium-based quantum dots forced vendors to invest USD 50-100 per display in re-qualification testing.[5]TÜV Rheinland, “EU - Ecodesign Requirements for Electronic Displays,” TUV.COM Middle Eastern buyers shift toward hardware-encrypted drives to meet national data-sovereignty laws, a behavior Kingston flagged in its November 2025 regional storage report. Africa remains nascent due to patchy broadband, yet pilot programs in South Africa and Kenya prove that solar-powered conference kits can function on sub-5 Mbps links, hinting at latent upside once infrastructure matures. South American adoption fluctuates with currency volatility; Brazil’s hybrid-work incentives spur demand in bull cycles, whereas import restrictions in Argentina create gray-market channels for refurbished gear.

Competitive Landscape

The Hybrid Work Hardware market shows moderate concentration; the top five vendors, such as Logitech, Cisco, Microsoft, HP, and Lenovo, control a substantial share. Market leaders pursue ecosystem lock-in, AI feature acceleration, and channel leverage. The February 2026 Samsung-Cisco-Logitech alliance bundles Rally AI cameras, Webex licenses, and Samsung displays under a single part number, collapsing procurement friction but also tying customers to three-party renewal cycles. Crestron, after joining Microsoft’s Device Ecosystem Program in 2025, differentiates with environmental automation, folding lighting, and shades to meet control and command USD 12,000-25,000 room premiums.

Regional challengers like DTEN and Yealink seize share in Asia-Pacific by offering Teams-certified kits at 30% discounts relative to Western equivalents, an advantage enabled by local production and streamlined distribution. However, intensifying cybersecurity audits raises the compliance bar in favor of incumbents with transparent CVE roadmaps. Technology remains the battleground; vendors embed neural engines in cameras and microphones to process audio and video locally, neutralizing latency and privacy concerns associated with cloud-dependent algorithms. Component droughts that throttled audio DSP supply in early 2025 prompted dual-sourcing arrangements and smaller modular SKUs that can ship partial configurations, illustrating how supply resilience has become a core competitive differentiator.

Looking ahead, ruggedized endpoints tailored for factory floors, medical-grade cameras for telemedicine, and ultra-low bandwidth codecs for emerging markets represent fertile niches. Large players may acquire specialists to close gaps, while startups will rely on vertical expertise and rapid firmware iteration to outmaneuver broad-portfolio incumbents. Channel convergence is likely, with integrators launching self-service portals and e-commerce giants adding white-glove installation tiers, blurring historic lines between offline and online sales.

Hybrid Work Hardware Industry Leaders

Logitech International S.A.

Cisco Systems, Inc.

HP Inc.

Lenovo Group Limited

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Samsung Electronics, Cisco Systems, and Logitech International formalized a strategic partnership to pre-integrate Logitech Rally AI cameras with Cisco Webex software and Samsung interactive displays, slashing installation time to under two hours per room.

- January 2026: Logitech launched the Rally AI Camera series with on-device neural processors that execute real-time framing and noise suppression, addressing latency concerns in healthcare and finance deployments.

- January 2026: Crestron Electronics unveiled the Collab Compute appliance, bundling a Teams Rooms license, touch controller, and compute module in one USD 3,500 SKU to streamline branch-office rollouts.

- November 2025: The European Union terminated RoHS exemption 39(a) for cadmium-based quantum dots, compelling display vendors to adopt cadmium-free formulations and adding USD 50-100 per unit in compliance testing.

Global Hybrid Work Hardware Market Report Scope

The Hybrid Work Hardware Market comprises revenues generated from the sale and deployment of physical IT equipment designed to enable seamless work across remote, office, and hybrid environments. This includes computing devices, peripherals, collaboration tools, video conferencing systems, networking hardware, and related accessories that support distributed workforce productivity and connectivity.

The Hybrid Work Hardware Market Report is Segmented by Product Type (Computing Devices, Peripherals and Accessories, Collaboration Hardware, Video Conferencing and Meeting Room Systems, Networking and Connectivity Hardware, and Other Product Types), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-user Industry (IT and Telecommunication, BFSI, Healthcare, Retail and Consumer Goods, Education, Government and Public Sector, Manufacturing, Media and Entertainment, and Other Industry Verticals), Distribution Channel (Offline, and Online), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Computing Devices |

| Peripherals and Accessories |

| Collaboration Hardware |

| Video Conferencing and Meeting Room Systems |

| Networking and Connectivity Hardware |

| Other Product Types |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| IT and Telecommunication |

| BFSI |

| Healthcare and Lifesciences |

| Retail and Consumer Goods |

| Education |

| Government and Public Sector |

| Manufacturing |

| Media and Entertainment |

| Other Industry Verticals |

| Offline |

| Online |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Product Type | Computing Devices | |

| Peripherals and Accessories | ||

| Collaboration Hardware | ||

| Video Conferencing and Meeting Room Systems | ||

| Networking and Connectivity Hardware | ||

| Other Product Types | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-user Industry | IT and Telecommunication | |

| BFSI | ||

| Healthcare and Lifesciences | ||

| Retail and Consumer Goods | ||

| Education | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Other Industry Verticals | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Hybrid Work Hardware market by 2031?

The market is forecast to reach USD 52.40 billion by 2031, growing at a 10.5% CAGR over 2026-2031.

Which product category is expected to grow the fastest through 2031?

Video conferencing and meeting room systems, with a projected 12.8% CAGR, outpace other hardware types.

Why is education adopting hybrid-work hardware so rapidly?

Universities retrofit lecture halls with AI-powered cameras and microphone arrays, fueling a 13.24% CAGR as they support global student cohorts and asynchronous learning.

How are small and medium businesses financing hardware purchases?

Vendors now offer hardware-as-a-service subscriptions that convert upfront capital costs into predictable monthly fees, aligning with SMB cash-flow constraints.

What regions present the highest growth potential?

Asia-Pacific leads with a projected 12.62% CAGR, driven by government-backed 5G rollouts and local manufacturing incentives.

Page last updated on: