Heterogeneous Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 160.17 Billion |

| Market Size (2031) | USD 430.52 Billion |

| Growth Rate (2026 - 2031) | 21.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heterogeneous Computing Market Analysis by Mordor Intelligence

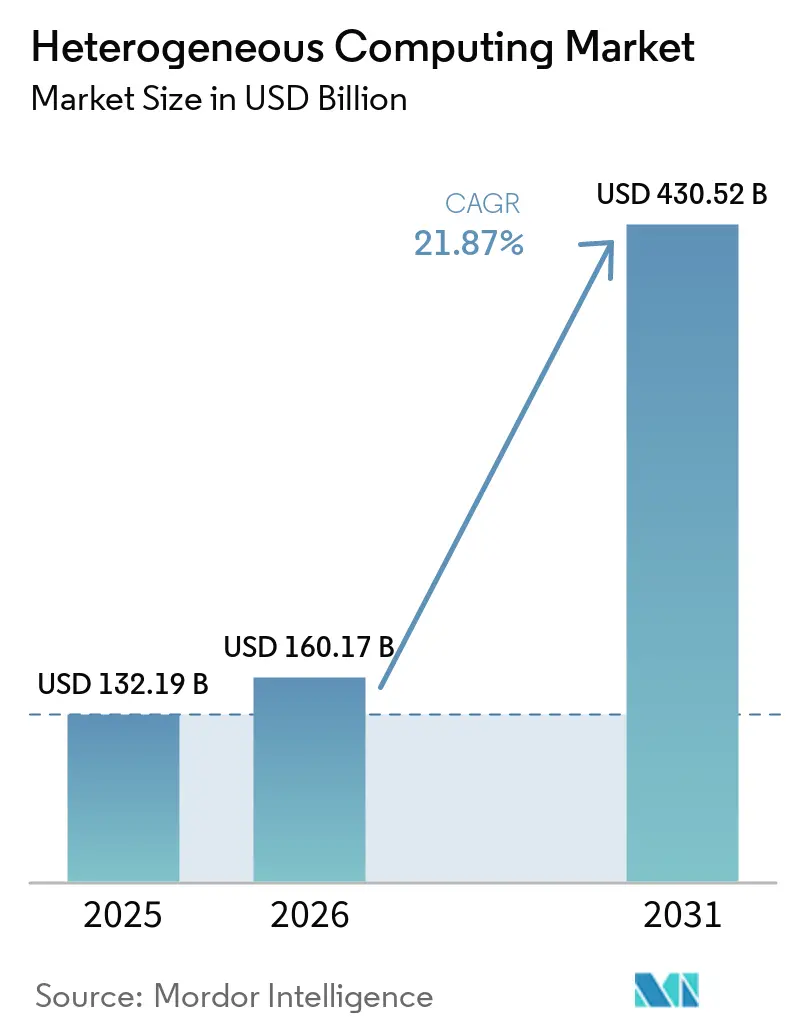

The Heterogeneous Computing Market size is expected to increase from USD 132.19 billion in 2025 to USD 160.17 billion in 2026 and reach USD 430.52 billion by 2031, growing at a CAGR of 21.87% over 2026-2031. Growth is being supported by a clear move away from single-architecture systems toward platforms that combine CPUs, GPUs, ASICs, FPGAs, and DSPs within the same computing environment. That shift is gaining speed because modern AI workloads now need training, inference, data processing, and simulation to run together with tighter control over latency, cost, and power use. Procurement is also becoming more durable because enterprise demand is being reinforced by public investment in sovereign AI infrastructure, national supercomputing programs, and policy support for semiconductor capacity. Competitive pressure is rising across hardware, software, and systems design as vendors try to tie silicon, memory, packaging, and orchestration tools into one usable stack. The strongest opening for growth sits in platforms that can coordinate mixed processors well, lower deployment friction, and meet stricter requirements around energy efficiency, data control, and real-time performance.

Key Report Takeaways

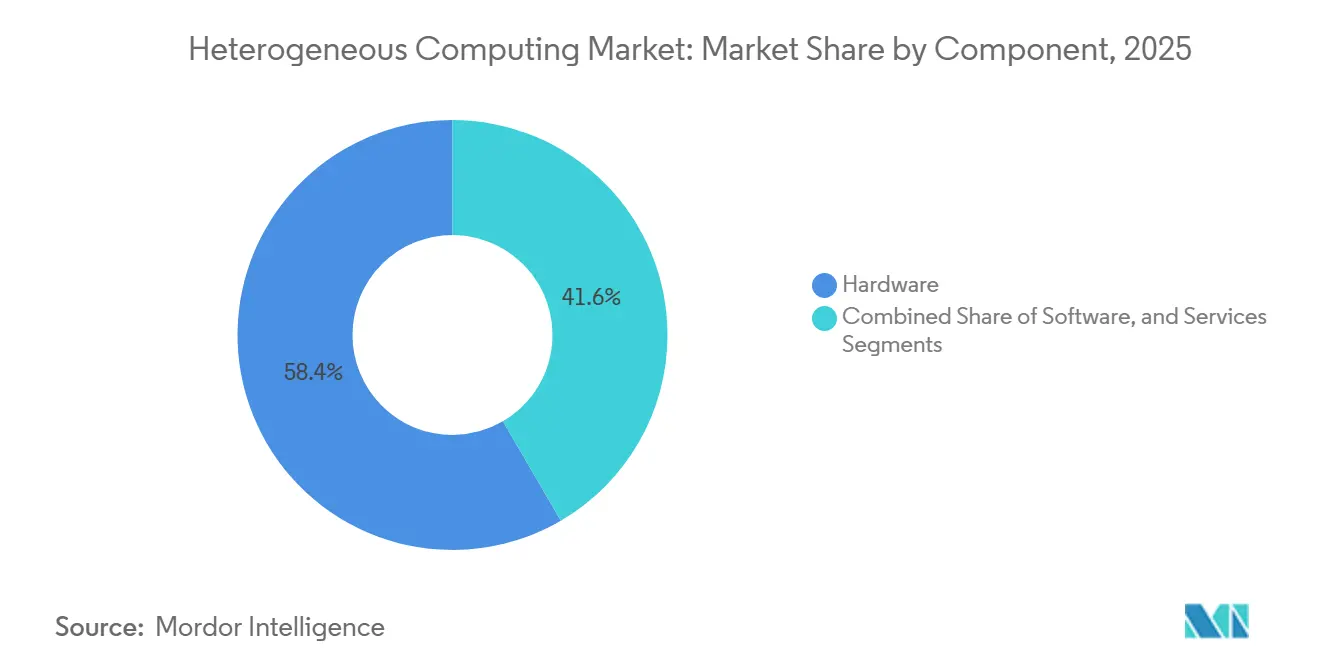

- By component, hardware held 58.41% of the heterogeneous computing market in 2025, while software is projected to expand at a 23.16% CAGR through 2031.

- By deployment mode, on-premises held 50.48% of the market in 2025, while cloud is projected to grow at a 22.78% CAGR through 2031.

- By processor type, GPU accounted for 35.42% of the market in 2025, while ASIC are projected to advance at a 22.54% CAGR through 2031.

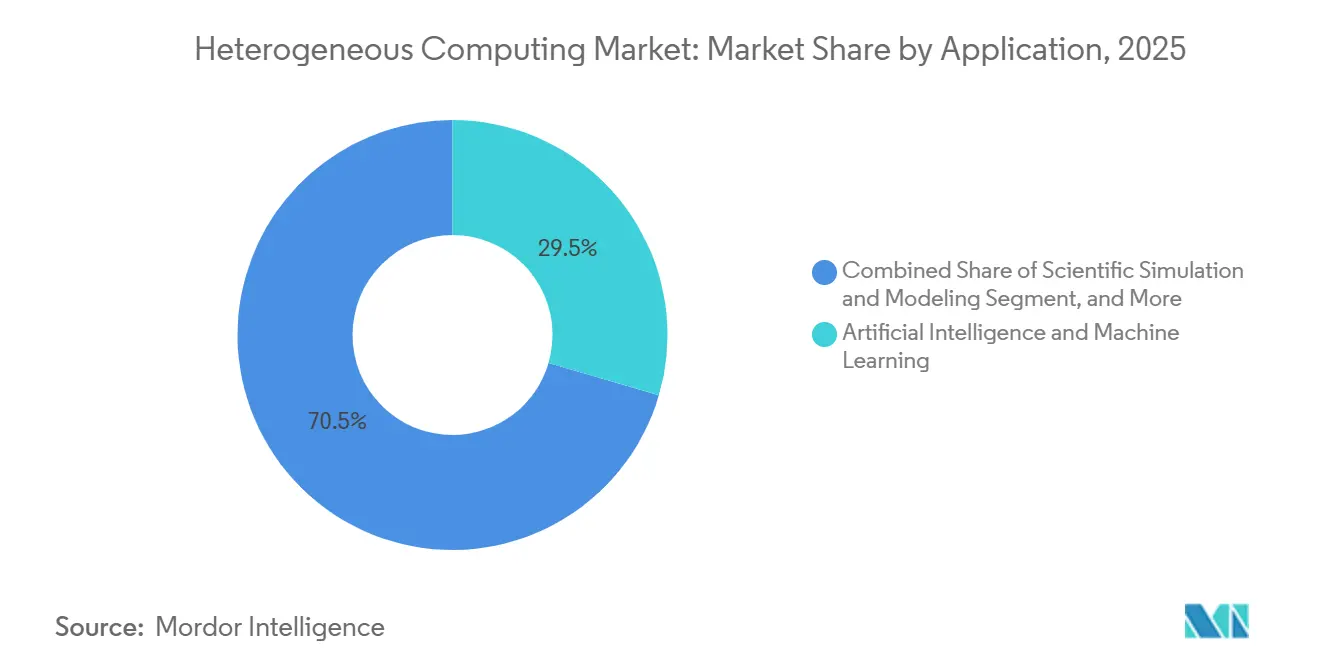

- By application, artificial intelligence and machine learning held 29.53% of the market in 2025 and are projected to grow at a 22.69% CAGR through 2031.

- By end user, enterprises represented 41.57% of the market in 2025, while the government and public sector are projected to expand at a 22.91% CAGR through 2031.

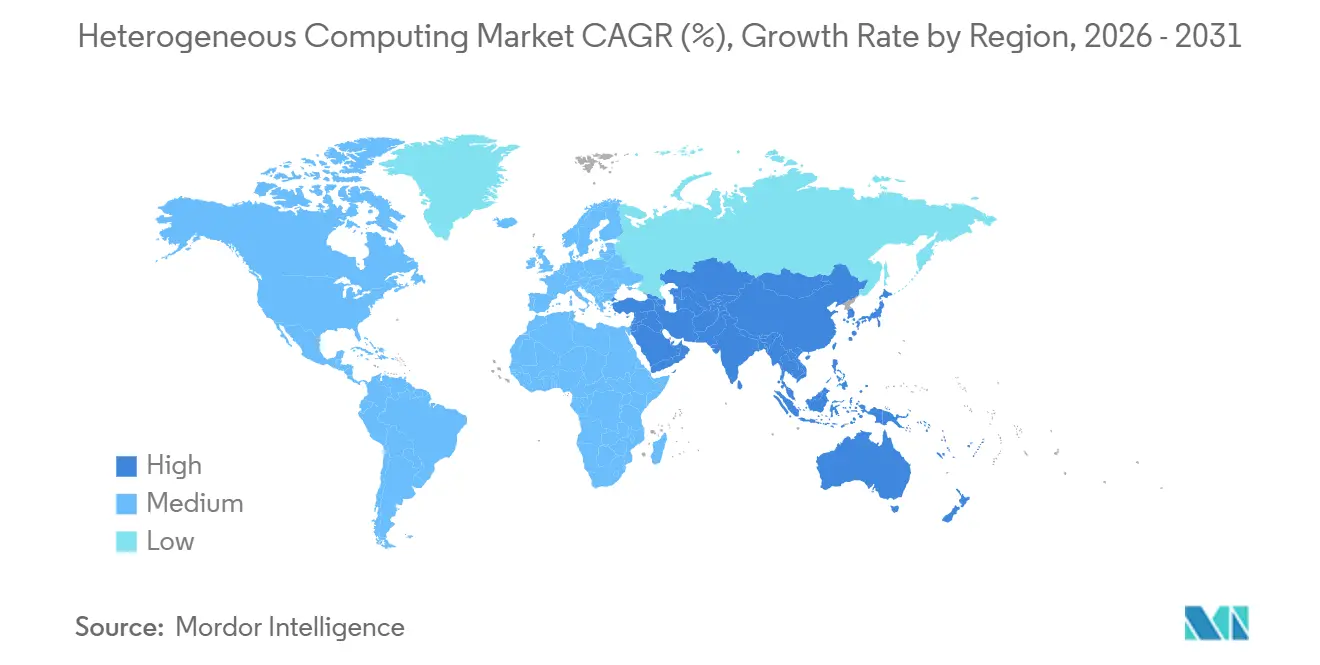

- By geography, North America held 40.83% of the heterogeneous computing market in 2025, while Asia-Pacific is projected to grow a 22.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heterogeneous Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Generative AI and Large Language Model Workloads | +5.5% | Global, concentrated in North America and the Asia-Pacific | Short term (≤ 2 years) |

| Growing Need for Parallel Processing in AI Training and Inference | +4.2% | Global, core in North America and Asia-Pacific data center clusters | Short term (≤ 2 years) |

| Expansion of Sovereign AI and National Compute Infrastructure | +3.5% | Global, led by North America, Europe, Asia-Pacific, the Middle East and Africa | Medium term (2-4 years) |

| Shift Toward Energy-Efficient and Performance-per-Watt Architectures | +2.8% | Global, accelerated in Europe and Asia-Pacific | Medium term (2-4 years) |

| Growth of Multimodal and Real-Time Analytics Workloads | +1.9% | North America, Europe, East Asia | Medium term (2-4 years) |

| Edge-to-Cloud Orchestration for Low-Latency Compute | +1.6% | Global, with highest traction in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Generative AI and Large Language Model Workloads

Generative AI workloads are the strongest near-term force driving the heterogeneous computing market, pushing buyers to combine dense training accelerators with hardware optimized for high-volume inference. Large language models do not create demand solely through model training; they also impose a lasting serving burden that increases token throughput, memory access, and latency requirements long after deployment begins. That is making single-processor strategies less practical, since one architecture rarely delivers the best mix of performance, utilization, and power efficiency across the full AI workflow. Google’s TPU 8t and TPU 8i launch in April 2026 clearly showed this split, with one design tuned for large-scale training and the other for concurrent inference and lower network latency.[1]Google Cloud, “TPU 8t and TPU 8i Technical Deep Dive,” Google Cloud Blog, cloud.google.com The heterogeneous computing market is therefore being shaped by platforms that can integrate different accelerator profiles rather than by raw chip speed alone. Vendors that can align silicon, interconnect, memory, and software around those needs are moving closer to repeat enterprise adoption.

Growing Need for Parallel Processing in AI Training and Inference

The growing need for parallel processing is widening the role of the heterogeneous computing market beyond hyperscale AI and into simulation, research, finance, and industrial computing. These workloads increasingly depend on coordinated processing across CPUs, GPUs, and specialized accelerators because no single device class handles every stage efficiently. Amazon’s Graviton5 design, introduced in 2026 with a 4-chiplet structure, 420 GB/s inter-chiplet bandwidth, and stronger machine learning inference performance, showed that even CPU-class products are now being redesigned around parallel AI behavior. The same pattern is visible in software, where AMD’s first 3-GPU heterogeneous submission in MLPerf Inference 6.0 highlighted how orchestration across different processor resources can become a direct performance lever. Academic work also supports this direction, with research published in Scientific Reports showing that learning-based scheduling on hybrid cloud-edge systems improves service quality by dynamically matching workloads to available hardware. As a result, the heterogeneous computing market is moving toward system-level optimization, where the value lies in how processors work together rather than in isolated chip specifications.

Expansion of Sovereign AI and National Compute Infrastructure

Sovereign AI programs are creating a second demand pillar for the heterogeneous computing market that is not dependent solely on private enterprise spending cycles. Governments are now moving from general AI policy to direct compute procurement, which gives the market a steadier multi-year pipeline for servers, accelerators, and related software layers. Canada took a similar step in April 2026, launching the AI Sovereign Compute Infrastructure Program to build Canadian-owned AI-optimized high-performance systems under a structured national strategy. These moves matter because they support demand for heterogeneous systems in research, public administration, and strategic infrastructure, even when commercial spending becomes more selective. The heterogeneous computing market is therefore gaining a more durable base, with policy frameworks also shaping supply chain qualification, localization priorities, and long-horizon investment timing.

Shift Toward Energy-Efficient and Performance-Per-Watt Architectures

Energy efficiency has become a central buying criterion in the heterogeneous computing market because AI clusters now consume enough power that operating cost can undermine the value of incremental speed gains. This is shifting product roadmaps away from peak throughput alone and toward designs that deliver better output within fixed power, cooling, and facility limits. NVIDIA’s Vera CPU platform is one example, with the company reporting higher density and stronger performance-per-watt than x86-based racks through a design aimed at AI factory workloads. Intel’s 18A-P process results, presented at the 2026 VLSI Symposium, pointed in the same direction by showing higher performance at iso-power or lower power at iso-performance through changes at the transistor and power-delivery levels. Research in Nature Machine Intelligence also showed that algorithm-hardware co-design can sharply increase throughput while improving energy efficiency by more than 5-fold, reinforcing the importance of tight hardware-software coupling. For the heterogeneous computing market, that means efficiency leadership is becoming a condition for deployment in large facilities, not just a feature for better margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity for Heterogeneous System Design and Validation | -3.5% | Global, particularly limiting in South America and Middle East and Africa | Medium term (2-4 years) |

| Scarcity of Parallel Programming and Hardware-Software Co-Design Talent | -2.8% | Global, most acute in Europe and South America | Long term (≥ 4 years) |

| Thermal and Power Delivery Constraints in Dense Compute Environments | -2.0% | Global, constraining in markets with aging grid infrastructure | Medium term (2-4 years) |

| Supply Chain Dependence on Advanced Nodes, HBM, and Packaging Capacity | -1.8% | Global, concentrated in East Asia supply chain nodes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity for Heterogeneous System Design and Validation

High capital intensity remains a major brake on the heterogeneous computing market because multi-processor systems require far more validation work than single-architecture deployments. Cost pressure appears at every stage, including silicon design, board development, interconnect tuning, memory integration, software compatibility testing, and system qualification. That burden is hardest on mid-sized enterprises and emerging-market operators that cannot spread engineering costs across very large, stable compute volumes. The result is a market where adoption can cluster among hyperscalers, large enterprises, and public institutions that have clearer workload visibility and stronger balance sheets. Advanced packaging requirements add another layer of cost and execution risk, narrowing the number of suppliers able to support production-scale deployment.

Scarcity of Parallel Programming and Hardware-Software Co-Design Talent

Talent scarcity is also limiting the pace of the heterogeneous computing market because effective deployment depends on engineers who can work across processors, software frameworks, and memory hierarchies simultaneously. The challenge goes beyond basic accelerator programming, since teams also need to profile workloads, allocate tasks across hardware types, and optimize data movement under real operating constraints. When that talent is missing, installed hardware is harder to use effectively, utilization rates remain lower, and the return on investment becomes less convincing for the next procurement cycle. Vendors that simplify orchestration and build stronger training pipelines are likely to face fewer adoption delays than those that rely solely on hardware benchmarks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Anchors Scale as Software Accelerates Monetization

Hardware accounted for 58.41% of the heterogeneous computing market in 2025, underscoring how strongly current spending still leans toward accelerator purchases, servers, memory, and supporting infrastructure. The largest near-term revenue pool remained tied to GPU-dense data center expansion, where buyers continued to prioritize access to computing capacity before focusing on full software standardization. That spending pattern also reflected timing, since large hardware rollouts reached commercial scale faster than orchestration and scheduling software could be monetized across broad enterprise environments. The heterogeneous computing market, therefore, entered 2026 with hardware still carrying the largest share of recognized value, even though long-term differentiation is moving higher in the stack.

GPU, FPGA, ASIC, and CPU products all expanded their installed base, but GPUs drove the largest absolute revenue contribution because they remained central to both training and many inference tasks. AMD’s Instinct MI430X, presented for scientific and AI workloads with 432 GB of HBM4 memory and 19.6 TB/s bandwidth, illustrated how hardware suppliers are trying to widen their role across research and commercial AI at the same time.[2]Advanced Micro Devices, Inc., “AMD Instinct MI430X Powers the Next Wave of AI and Science,” AMD, amd.com Software is projected to grow at a 23.16% CAGR from 2026 to 2031, which makes it the fastest-growing component and points to increasing value in orchestration frameworks, schedulers, abstraction layers, and memory management tools. Services continue to matter because many customers still need integration support to operate mixed environments with fewer deployment errors. Within the heterogeneous computing industry, this mix suggests that hardware is still the entry point for spending, while software and services are becoming the main path to recurring revenue and tighter customer retention.

By Deployment Mode: On-Premises Resilience Against a Cloud-Dominated Forecast

On-premises accounted for 50.48% of the heterogeneous computing market in 2025, underscoring that local infrastructure remained the largest deployment base despite heavy cloud investment. That position reflected the installed footprint of enterprise GPU clusters, university systems, and national laboratory environments that had already absorbed several years of capital spending. The segment also benefited from practical constraints, since real-time inference workloads often require lower latency than distant cloud regions can consistently deliver. Data control requirements added further support for local deployment, especially in finance, healthcare, and government settings, where model weights, training data, and sensitive outputs are subject to stricter handling rules.

Cloud is projected to grow at a 22.78% CAGR through 2031, making it the fastest-growing deployment mode in the heterogeneous computing market. This growth is being driven by hyperscaler investment in mixed GPU and ASIC environments that allow customers to access specialized processors without upfront capital commitments. Hybrid deployment is expanding beyond that trend, as enterprises route workloads between local and cloud resources based on latency, compliance, and cost conditions rather than using one environment for every task. The coexistence of a leading on-premises base and a faster-growing cloud segment suggests that the heterogeneous computing market is not following a one-way migration path. Instead, workload placement is becoming more selective, which sustains demand for deployment flexibility across the broader heterogeneous computing industry.

By Processor Type: GPU Holds Structural Lead as Custom Silicon Narrows the Gap

GPU held 35.42% of the heterogeneous computing market share in 2025, which kept it in the lead among processor categories because it still offered the strongest balance of programmability, ecosystem depth, and training performance. That leadership remained important in environments where buyers wanted one accelerator class that could support both established AI workflows and newer inference needs without a full redesign of tools and operating practices. NVIDIA’s Vera Rubin platform, announced in June 2026 with tightly linked Rubin GPUs and Vera CPUs, showed how GPU-centered systems are also being pushed deeper into scientific computing and complex simulation use cases. CPUs, FPGAs, and DSPs continued to fill specialized roles across orchestration, reconfigurable processing, and real-time signal processing, keeping processor diversity central to the heterogeneous computing market rather than peripheral to it.

ASIC is projected to grow at a 22.54% CAGR through 2031, making it the fastest-growing processor type as hyperscalers continue to back purpose-built inference silicon. The appeal is clear in production-serving environments, where high-volume inference rewards better cost-per-token, tighter power control, and workload-specific tuning. Growth in ASICs does not remove the role of GPUs evenly, because training and exploratory development still favor broad programmability while steady inference can justify dedicated silicon. Samsung’s February 2026 shipment of the first commercial HBM4 stack on a 4 nm base die underscored how memory and packaging advances are becoming critical to the next wave of accelerator performance. For the heterogeneous computing market, the processor landscape is becoming more layered, with GPUs keeping a structural lead while custom silicon expands faster in tightly defined deployment cases.

By Application: AI and Machine Learning Consolidates Demand Across the Compute Stack

Artificial intelligence and machine learning accounted for 29.53% of the heterogeneous computing market in 2025, making it the largest application and the strongest source of current demand. That share reflected the scale of spending behind large-scale model training and the ongoing infrastructure load created as those models move into production inference. The segment is projected to grow at a 22.69% CAGR through 2031, so the same application that led the market in 2025 is also expected to remain the fastest-growing major use case through the forecast period. This continuity matters because it focuses product roadmaps, channel investment, and platform competition on AI serving, model development, and data movement rather than on a rotating mix of unrelated workloads.

Data center and cloud computing remained the next major application group, supported by hyperscaler capacity build-outs that underpin commercial AI services. Scientific simulation and modeling formed a separate demand pool where high-memory accelerators, CPUs, and FP64-capable systems stayed important for climate, materials, and life science workloads. Edge computing is also gaining ground in the heterogeneous computing market as organizations look for lower-latency inference at the point of use rather than routing every workload back to centralized infrastructure. Research in Discover Computing reported end-to-end latency of 39 to 52 milliseconds with 48% bandwidth savings in a low-latency intelligent edge design, which supports the case for more distributed accelerator deployment. Automotive and autonomous systems are expanding in parallel because higher levels of autonomy depend on mixed-sensor processing across several specialized compute blocks, which keeps application diversity broad even while AI and machine learning remain dominant.

By End User: Enterprise Scale Anchored by Government-Led Acceleration

Enterprises accounted for 41.57% of the heterogeneous computing market share in 2025, giving them the largest end-user position. Their lead came from the scale and breadth of AI infrastructure programs in hyperscale cloud, finance, healthcare, and industrial operations, where computing now supports production workflows rather than experimental pilots. Enterprise buying also tends to favor integrated platforms that reduce engineering burden, which benefits suppliers that can combine silicon, software, services, and support under a single operating model. That made reliability, ecosystem depth, and deployment simplicity nearly as important as raw accelerator specifications in many purchasing decisions across the heterogeneous computing market.

The government and public sector are projected to grow at a 22.91% CAGR through 2031, which makes it the fastest-growing end-user group. This rise is tied directly to sovereign AI programs, national computing strategies, and public investment in research and defense infrastructure that require local control over advanced compute assets. Research institutes and academia remained important because they often adopt next-generation heterogeneous designs early, especially when those systems support both scientific simulation and AI research. Telecommunications and network operators are also moving deeper into the heterogeneous computing market as they apply AI to network optimization, 5G core processing, and low-latency services. NVIDIA’s AI Grid reference design, presented at GTC 2026, reflected that direction by targeting distributed intelligence and coordinated computing across different infrastructure layers.

Geography Analysis

North America held 40.83% of the heterogeneous computing market in 2025, and that lead rested on its deep concentration of hyperscale data centers, advanced AI developers, and defense-linked computing programs. The United States remained the core of this position because its policy stance and commercial infrastructure continued to support the fast deployment of AI clusters and related semiconductor capacity. The January 2025 executive order on advancing U.S. leadership in AI infrastructure showed that federal policy was already aligning build-out speed, supply security, and permitting direction around large-scale compute expansion. Canada strengthened the regional picture in April 2026 by launching its AI Sovereign Compute Infrastructure Program to support Canadian-owned AI-optimized high-performance systems.[3]Government of Canada, “Canada Launches National Initiative to Build Large-Scale AI Supercomputing Capacity,” Canada.ca, canada.ca In the heterogeneous computing market, that combination of private scale and public support kept North America ahead on both installed capacity and near-term procurement momentum.

Asia-Pacific is projected to grow at a 22.36% CAGR through 2031, making it the fastest-growing region in the heterogeneous computing market. The region’s growth is being supported by government compute programs, rising domestic chip ambitions, and its central role in memory, packaging, and broader semiconductor supply chains. This matters because many of the core enabling technologies for heterogeneous systems, including advanced packaging and high-bandwidth memory, are concentrated in Asia-Pacific production networks. That concentration can speed deployment for local buyers while also tying regional growth to global demand for accelerators, servers, and supporting components. The heterogeneous computing market is therefore likely to see Asia-Pacific strengthen both as a demand center and as a supply-side backbone for future system scaling.

Europe remained an important part of the heterogeneous computing market because public policy and industrial modernization are pushing AI infrastructure into more sectors. The United Kingdom’s June 2026 AI Hardware Plan stood out because it paired compute capacity spending with support for domestic chip firms and technical skills development. South America and Middle East and Africa were earlier-stage regions in 2026, but the market direction there was still improving as governments and institutions evaluated sovereign compute capacity and local AI infrastructure needs. These regions face higher barriers around capital intensity, power systems, and engineering availability, which means adoption may move in steps rather than at the same pace seen in North America or Asia-Pacific. Even so, the heterogeneous computing market has room to deepen in these regions when public programs, telecom modernization, and enterprise AI deployment become more coordinated.

Competitive Landscape

The heterogeneous computing market remained moderately fragmented at the platform level in 2026, with a small group of vendors controlling the broadest accelerator ecosystems, while competition stayed more dispersed across subsystems and specialized architectures. NVIDIA kept the widest position because it combined strong GPU demand with a mature software stack and systems-level reach across AI deployment environments. AMD remained the most credible scaled alternative in data center accelerators, keeping the second-source strategy relevant for large buyers seeking greater supply flexibility and pricing leverage. The market was also becoming more layered because merchant chip vendors now compete not only with each other, but also with hyperscalers that are designing internal silicon for targeted workloads. This is why the heterogeneous computing market is being shaped as much by ecosystem control and integration quality as by any single processor benchmark.

A major strategic move came in September 2025 when NVIDIA invested USD 5 billion in Intel, and the two companies agreed to develop NVIDIA-custom x86 CPUs for data centers and x86 SoCs that integrate NVIDIA RTX GPU chiplets for PCs. That agreement signaled closer fusion between processor classes that had long been purchased and optimized more separately.[4]Intel Corporation, “Intel and NVIDIA to Jointly Develop AI Infrastructure and Personal Computing Products,” Intel Newsroom, intel.com Intel also expanded its role in April 2026 through a strategic collaboration with SambaNova Systems to build a reference architecture that combines Xeon 6 CPUs, GPUs, and SambaNova reconfigurable dataflow units for agentic AI models. These moves showed that leading vendors are trying to control more of the system path, from host processing and acceleration to software compatibility and inference flow. In the heterogeneous computing market, competitive advantage is increasingly tied to how well vendors coordinate multiple processor types for production use instead of treating them as standalone products.

Startups and specialized challengers are still influencing direction, but the stronger competitive signal comes from companies that can translate technical differentiation into deployable platforms. Google’s publication of TPU 8t and TPU 8i specifications in April 2026 reinforced the pressure on merchant suppliers by showing how custom internal silicon can be split more precisely between training and inference demands. AMD’s MLPerf Inference 6.0 results also showed that software-led orchestration across heterogeneous GPU configurations is becoming a practical differentiator rather than a laboratory exercise. The heterogeneous computing market therefore remains open to new entrants in targeted niches, but scale, software maturity, and integration depth still favor established players with broad value chain coverage.

Heterogeneous Computing Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Qualcomm Incorporated

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA announced the Vera Rubin NVL4 platform on June 22, 2026, delivering over 7 exaflops of AI compute and 5 petaflops of FP64 performance for science workloads; systems from Dell Technologies, GIGABYTE, HPE, and Supermicro are expected in Q4 2026.

- June 2026: Intel Foundry presented silicon results for its 18A-P process node at the VLSI Symposium, demonstrating 9% higher performance at iso-power or 18% lower power at iso-performance versus Intel 18A, enabled by gate-all-around transistors and backside power delivery technology.

- June 2026: Advanced Micro Devices, Inc. acquired Mext Corp., a flash memory optimization startup, on June 15, 2026. AMD plans to integrate Mext's technology into its data center portfolio to reduce AI deployment costs and address memory supply constraints in large-scale AI workloads.

- April 2026: The Government of Canada launched the AI Sovereign Compute Infrastructure Program on April 15, 2026, initiating a call for applications for Canadian-owned AI-optimized high-performance computing systems. The program is backed by budgets announced in Canada's 2024 and 2025 federal budgets under the Canadian Sovereign AI Compute Strategy.

Global Heterogeneous Computing Market Report Scope

The heterogeneous computing market refers to the integration of different types of processors, such as CPUs, GPUs, and FPGAs, within a single system to optimize performance and energy efficiency. The study examines market trends, growth drivers, challenges, and opportunities during the forecast period.

The Heterogeneous Computing Market Report is Segmented by Component (Hardware, Software, and Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Processor Type (CPU, GPU, FPGA, ASIC, DSP, and Other Processor Types), Application (Artificial Intelligence and Machine Learning, Data Center and Cloud Computing, Scientific Simulation and Modeling, Edge Computing, Automotive and Autonomous Systems, and Other Applications), End User (Enterprises, Government and Public Sector, Research Institutes and Academia, Telecommunications and Network Operators, and Other End Users), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| On-Premises |

| Cloud |

| Hybrid |

| Central Processing Unit (CPU) |

| Graphics Processing Unit (GPU) |

| Field-Programmable Gate Array (FPGA) |

| Application-Specific Integrated Circuit (ASIC) |

| Other Processor Types |

| Artificial Intelligence and Machine Learning |

| Data Center and Cloud Computing |

| Scientific Simulation and Modeling |

| Edge Computing |

| Automotive and Autonomous Systems |

| Other Applications |

| Enterprises |

| Government and Public Sector |

| Research Institutes and Academia |

| Telecommunications and Network Operators |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Processor Type | Central Processing Unit (CPU) | |

| Graphics Processing Unit (GPU) | ||

| Field-Programmable Gate Array (FPGA) | ||

| Application-Specific Integrated Circuit (ASIC) | ||

| Other Processor Types | ||

| By Application | Artificial Intelligence and Machine Learning | |

| Data Center and Cloud Computing | ||

| Scientific Simulation and Modeling | ||

| Edge Computing | ||

| Automotive and Autonomous Systems | ||

| Other Applications | ||

| By End User | Enterprises | |

| Government and Public Sector | ||

| Research Institutes and Academia | ||

| Telecommunications and Network Operators | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and forecast for the heterogeneous computing market?

The heterogeneous computing market was worth USD 132.19 billion in 2025, stands at USD 160.17 billion in 2026, and is forecast to reach USD 430.52 billion by 2031 at a 21.87% CAGR.

What is driving demand for heterogeneous computing systems?

The main demand drivers are generative AI, large language model inference, parallel processing needs, sovereign AI infrastructure programs, and rising pressure to improve performance-per-watt.

Which component leads revenue in heterogeneous computing?

Hardware led with 58.41% share in 2025 because current spending is still centered on accelerators, servers, memory, and related infrastructure. Software is projected to grow at the fastest CAGR of 23.16% through 2031.

Why do on-premises still matter when the cloud is growing quickly?

On-premises held 50.48% of the market in 2025 because low-latency applications and data control rules still favor local infrastructure. Cloud is still expanding quickly, with a projected 22.78% CAGR through 2031.

Which processor type is growing fastest?

GPU remained the largest processor type with 35.42% share in 2025, while ASIC is projected to grow fastest at a 22.54% CAGR as hyperscalers keep investing in purpose-built inference silicon.

Which region offers the strongest growth outlook?

North America led with 40.83% share in 2025, but Asia-Pacific is projected to grow fastest at a 22.36% CAGR through 2031 because of public compute programs and its role in semiconductor supply chains.

Page last updated on: