Embedded Computing Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 124.01 Billion |

| Market Size (2031) | USD 187.02 Billion |

| Growth Rate (2026 - 2031) | 8.55% CAGR |

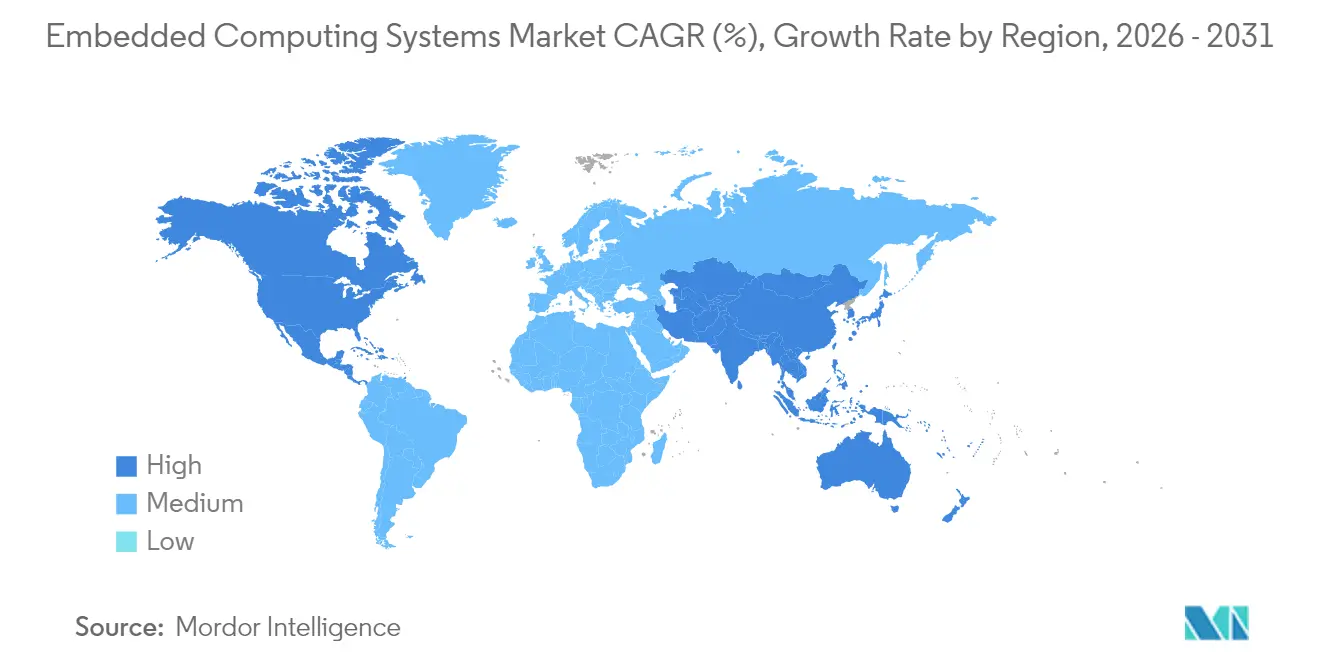

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

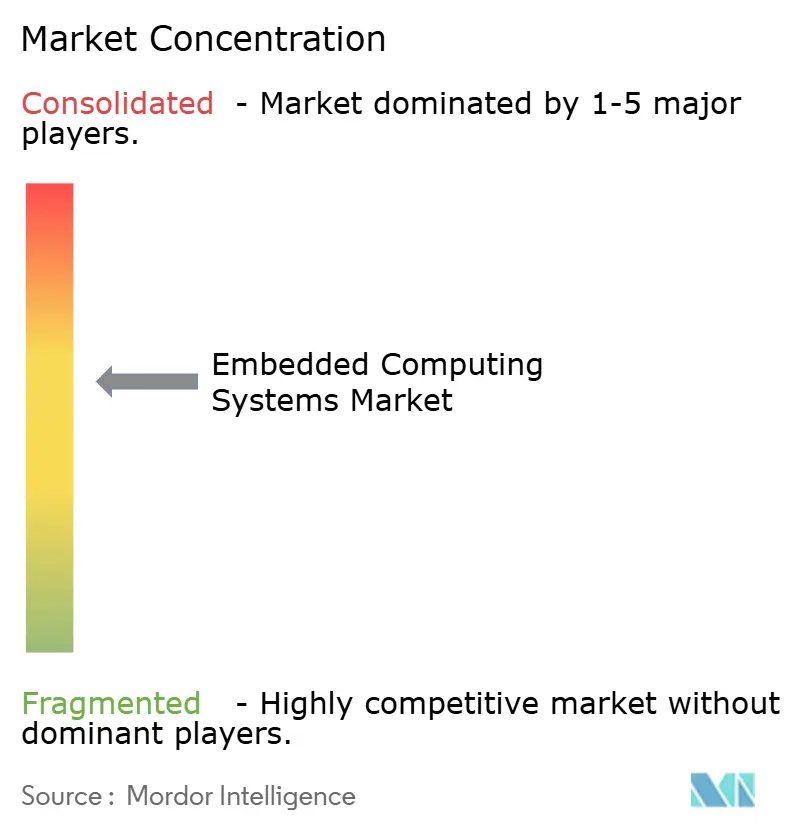

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embedded Computing Systems Market Analysis by Mordor Intelligence

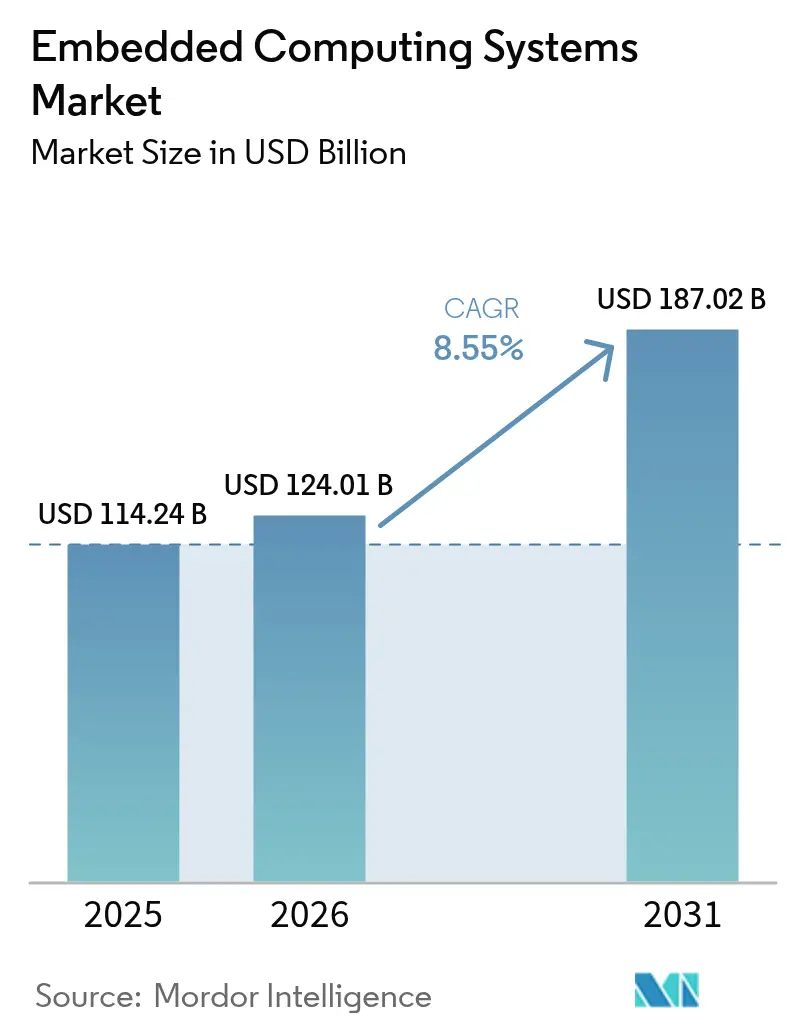

The embedded computing systems market size is expected to grow from USD 114.24 billion in 2025 to USD 124.01 billion in 2026 and is forecast to reach USD 187.02 billion by 2031 at 8.55% CAGR over 2026-2031. Rapid migration from general-purpose processors toward application-specific SoCs, tighter convergence of sensing, processing, and actuation, and the need for deterministic decision loops underpin this growth trajectory. Industrial automation remains the largest demand center, yet the highest incremental value stems from edge AI inference that eliminates cloud round-trip latency. Hardware still generates most sales, but value is shifting to software layers-real-time operating systems, middleware, container runtimes-that monetize device fleets long after initial deployment. Regionally, the center of gravity continues moving to Asia Pacific, where China and India leverage policy tools to localize control-system production and attract multinational electronics investors. Architectural competition is intensifying; while ARM held a majority of 2024 shipments, RISC-V is expanding as a royalty-free alternative that major auto and cloud buyers favor for domain-specific acceleration.

Key Report Takeaways

- By end user, industrial automation led with 36.05% revenue share in 2025; edge AI deployments within factories are advancing at an 11.02% CAGR through 2031.

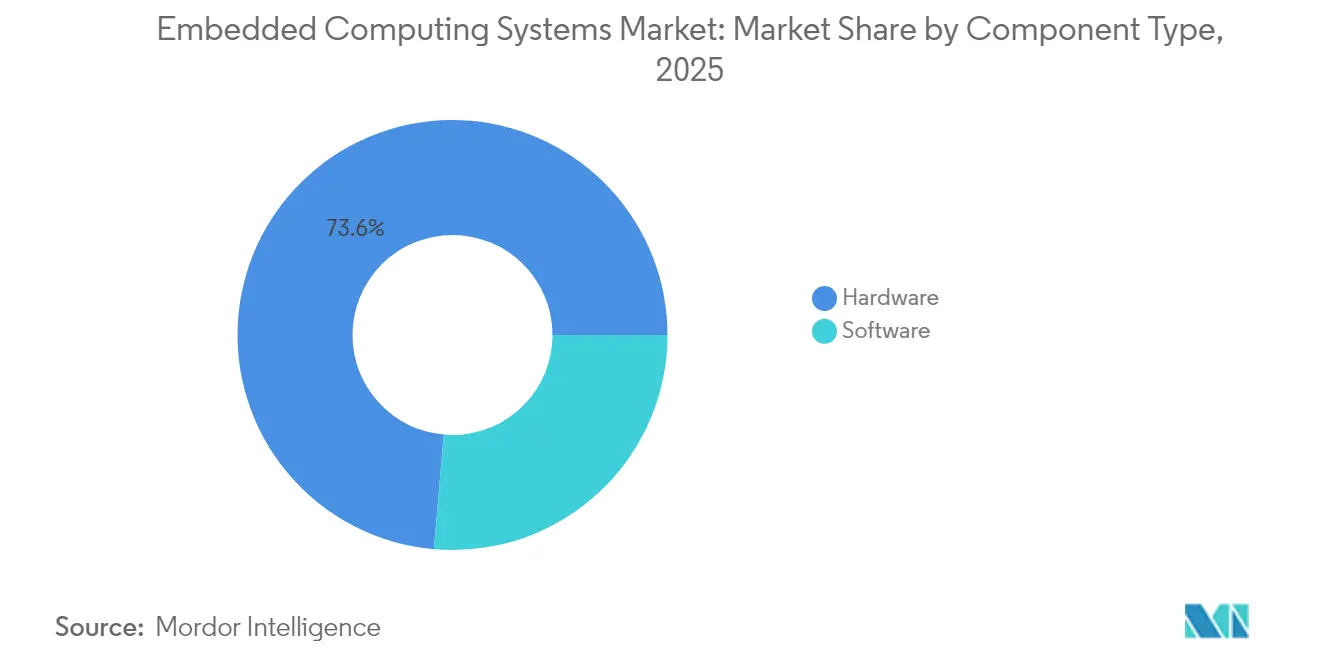

- By component, software is forecast to expand at a 10.05% CAGR to 2031, overtaking hardware’s 73.62% 2025 base.

- By architecture, RISC-V is the fastest-growing instruction set at an 10.73% CAGR even as ARM retained 50.25% embedded computing systems market share in 2025.

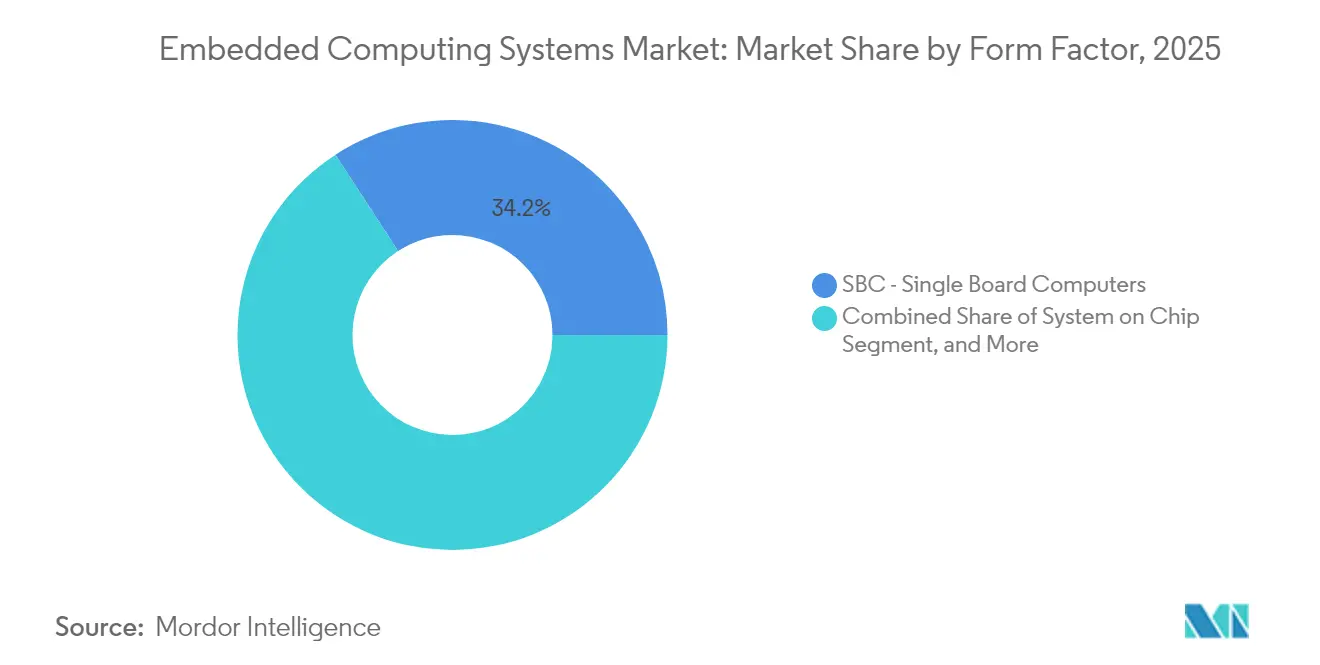

- By form factor, system-on-chip modules will widen their contribution, growing at a 10.08% CAGR to 2031, while single-board computers accounted for 34.16% of the 2025 embedded computing systems market size.

- By geography, Asia Pacific generated 45.96% of 2025 sales and is set to climb at a 12.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Embedded Computing Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing investments in industrial automation | +1.8% | Global with APAC core spill-over to Europe | Medium term (2–4 years) |

| Rising demand in consumer electronics due to size and power constraints | +1.5% | Global led by North America and APAC | Short term (≤ 2 years) |

| Proliferation of Internet of Things devices | +1.2% | Global | Medium term (2–4 years) |

| Growing adoption of electric vehicles requiring embedded controllers | +1.0% | North America, Europe, China | Long term (≥ 4 years) |

| Edge AI co-design reducing latency costs in smart manufacturing | +1.3% | APAC core, North America, spill-over to Europe | Medium term (2–4 years) |

| Government security certification mandates driving trusted-execution architectures | +1.1% | North America, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Investments in Industrial Automation

Factory owners are leaving relay logic behind and installing programmable controllers that accept over-the-air firmware, predictive-maintenance analytics, and sub-100-millisecond fail-safe loops. Orders for Siemens SIMATIC edge devices rose 22% YoY in 2024, with buyers citing bandwidth savings from local time-series inference.[1]Siemens AG, “Q4 2024 Earnings Presentation,” siemens.com Schneider Electric’s June 2024 Modicon refresh embedded ARM Cortex-A53 cores capable of containerized IEC 61131-3 code beside Python, merging OT and IT tasks on one board.[2]Schneider Electric, “EcoStruxure Expansion 2024,” se.com Falling industrial PC prices mean machine builders redirect budgets toward compute and software subscriptions. Meeting IEC 61508 safety targets increases upfront validation effort yet locks users into multi-year service contracts, widening vendor moats.

Edge AI Co-Design Reducing Latency Costs in Smart Manufacturing

Manufacturers now embed tensor accelerators in PLCs to classify defects or tweak tool paths on the fly. NVIDIA’s Jetson Orin NX ships 100 TOPS INT8 within 10 W envelopes, enabling 200 parts per minute vision assembly lines. Intel’s 2024 majority stake in SiFive’s auto unit underscores a pivot to royalty-free cores optimized for matrix math, replacing legacy DSPs in gateways. Hardware-model co-design boosts throughput-per-watt by three to five times versus general ARM implementations, extending battery field life and lowering ownership cost.

Growing Adoption of Electric Vehicles Requiring Embedded Controllers

Battery electric vehicles need distributed compute for pack management, traction inverters, and ADAS. Infineon’s automotive MCU revenue climbed 18% YoY in 2024 as EV platforms consumed two-to-three times more silicon than combustion peers. Texas Instruments’ August 2024 TMS320F28P55x integrates 16-bit ADCs sampling 4 MSPS to keep motor torque loops deterministic at 10 µs. Zonal architectures cut wiring but raise compute density per node, and regulatory over-the-air mandates force secure boot chains and redundant partitions, increasing silicon bills 15%-20%.

Government Security Certification Mandates Driving Trusted Execution Architectures

U.S. federal agencies now procure only FIPS 140-3 validated modules featuring tamper-evident cases and side-channel-resistant crypto. Microchip’s SAM L11 achieved EAL5+ in July 2024, adding hardware random-number generation and secure key stores for smart-meter rollouts. ARM TrustZone partitions secure and non-secure worlds; adoption by Qualcomm, NXP, and Renesas isolates safety code from general workloads. Compliance extends development cycles 12-18 months and favors suppliers that can bankroll penetration tests, raising entry barriers for new entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limitations in deployment in harsh environments | -0.8% | Oil and gas, mining, global | Short term (≤ 2 years) |

| High initial integration costs for legacy equipment | -0.6% | North America, Europe | Medium term (2–4 years) |

| Cybersecurity vulnerabilities in connected devices | -0.9% | Global | Short term (≤ 2 years) |

| Global shortage of advanced packaging for embedded SoCs | -1.2% | Global, supply in Taiwan and South Korea | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Vulnerabilities in Connected Devices

Sixty-eight percent of surveyed industrial controllers still run unpatched real-time operating systems with remote-code-execution flaws, according to a March 2024 CISA advisory.[3]CISA, “Industrial Control Systems Advisory,” cisa.gov SAE’s updated J3061 guide urges vehicle ECUs to integrate hardware security modules and intrusion detection. Air-gapping brownfield assets remains common, yet segmentation boxes add latency and complexity. Multi-tier supply chains lack a unified disclosure framework, slowing patch rollout because firmware source code sits with multiple IP holders.

Global Shortage of Advanced Packaging for Embedded SoCs

Fan-out wafer-level capacity is oversubscribed until late 2025, driving 40-week lead times for sub-10 mm z-height packages, per TSMC’s January 2025 earnings call. Designers either accept thicker stacks that violate mechanical envelopes or revert to wire-bond multichip modules that degrade gigahertz signal integrity. Samsung’s planned USD 17 billion packaging fab will not open until 2026, leaving a two-year gap that disproportionately strains low-volume OEMs unable to secure allocation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Software Monetization Outpaces Commodity Hardware

Hardware captured 73.62% of 2025 sales, led by industrial PCs, HMIs, and rugged gateways. Yet software revenue will grow 10.05% annually, eclipsing hardware by 2031 as OEMs decouple value from silicon. Wind River’s VxWorks now runs on more than 2 billion devices, offering POSIX compliance for Linux application portability. Microsoft’s Azure Sphere bundles a Cortex-M4 with a managed security service, and its installed base expanded 35% in 2024 as appliance makers embraced automatic patching. Industrial PCs still dominate brownfields because of legacy I/O needs, but edge servers tailored for inference, like Dell’s PowerEdge XR series, are proliferating in factories that cannot tolerate cloud latency. Software subscription models hedge against commodity pricing erosion that plagues hardware, prompting silicon vendors to acquire OS vendors to secure recurring revenue streams.

Software’s ascent underscores a qualitative shift in the embedded computing systems market. OEMs increasingly bill customers for container runtimes, update orchestration, and diagnostics dashboards. Per-device license fees translate into higher lifetime value than one-time board sales, a pattern echoed in adjacent markets such as PLC licensing. As abstraction layers thicken, developers focus on ML model deployment pipelines rather than register-level coding, allowing broader talent pools to build applications. This democratization accelerates feature velocity yet raises long-term maintenance complexity, boosting demand for curated Linux distros and real-time hypervisors.

By Architecture: RISC-V’s Royalty-Free Momentum

ARM held 50.25% of 2025 shipments, a testament to its mature compiler stacks and IP catalog. Still, RISC-V cores are forecast to post an 10.73% CAGR to 2031 as auto makers and hyperscalers adopt customizable ISA extensions. SiFive’s Performance P870 scores 15 SPECint2017 per watt, aligning with high-end industrial gateway requirements. Intel’s strategic stake in SiFive broadens foundry demand for its 18A node, helping anchor the open ISA in safety-critical domains. x86 retains a corner of the embedded computing systems industry in rackmount edge servers where binary compatibility simplifies workload migration. However, power envelopes that exceed 25 W limit x86 adoption in fanless enclosures common on factory walls.

Digital signal processors survive in audio and RF niches but lose share as vendors fuse DSP extensions into general cores. FPGAs remain vital in prototyping and low-volume avionics, with AMD-Xilinx Zynq UltraScale+ blending ARM clusters with programmable logic for convolution acceleration. ASIC economics make sense only for million-unit runs, given 7-nm mask costs above USD 10 million. Toolchain fragmentation looms as each RISC-V vendor adds proprietary vector or bit-manipulation sets, prompting RISC-V International to prioritize baseline compliance tests that preserve cross-platform portability.

By Form Factor: SoC Modules Push Miniaturization

Single-board computers captured 34.16% of 2025 value, favored for plug-and-play I/O adaptability. Raspberry Pi’s Compute Module 4 shipped over 3 million units, serving building-automation and signage needs within a 55 mm × 40 mm footprint. Yet system-on-chip modules will grow at a 10.08% CAGR, consolidating compute, memory, and connectivity in one package to satisfy battery-device power budgets. NXP’s i.MX 8M Plus packs a quad-core Cortex-A53, a 2.3 TOPS NPU, and a Cortex-M7 into a 14 mm × 14 mm die, enabling handheld barcode scanners to run vision models without external accelerators.

COM Express, SMARC, and Qseven standards help distributors manage inventory, but proliferating pinouts fragment the ecosystem. Rackmount systems keep relevance in telecom and data-center edges; Advantech’s MIC-7700 supports Intel Xeon-D and dual 10-GbE for network-function virtualization. Legacy PC/104 boards remain entrenched in defense platforms requiring 15-year lifecycles and radiation-hardened parts. Surface-mount adoption yields thinner profiles but complicates field repair because BGA rework needs x-ray inspection, pushing operators toward hot-swap redundancy over board-level servicing.

By End User: Automation Dominant, Healthcare Rising

Industrial automation contributed 36.05% of 2025 revenue as discrete manufacturers embedded controllers for motion, vision, and condition monitoring. Edge AI installations in these factories are projected to rise 11.02% annually, reallocating analytics from cloud to line side. Automotive ranks second, driven by electric vehicles whose embedded compute nodes exceed 30 per car, according to Tesla’s 2024 annual report. Healthcare grows steadily as FDA cybersecurity guidance requires secure boot and patch management for infusion pumps and diagnostic systems.

Retail deploys vision-enabled kiosks and shelf robots to curb shrink and shorten checkout queues. Consumer smart-home devices crave ultra-low standby power; Qualcomm’s QCS4290 integrates Wi-Fi 6E, Bluetooth 5.2, and a Hexagon DSP within 3 W envelopes. Aerospace and defense continue to demand radiation-tolerant parts and DO-178C software certification, narrowing supplier pools. Telecom base stations rely on embedded processors for line-rate encryption and QoS policing, where Intel Atom C3000 remains a reference. Energy, transportation, and building automation round out the landscape, tied to smart-grid upgrades and carbon-reporting mandates.

Geography Analysis

Asia Pacific delivered 45.96% of the 2025 embedded computing systems market revenue and will expand at a 12.45% CAGR to 2031, the fastest of any region. China’s “New Quality Productive Forces” policy targets a 30% drop in imported PLC reliance by 2027, funneling subsidies to local integrators such as Inovance and Hollysys. India’s production-linked incentive program commits INR 738 billion (USD 8.9 billion) to electronics lines over six years, attracting Foxconn and Pegatron to Tamil Nadu and Karnataka. Japan pivots from consumer to automotive microcontrollers; Renesas’ Q3 2024 MCU shipments rose 14% YoY. South Korea’s foundry leadership makes it a linchpin for SoC supply even though its domestic automation base is smaller. Australia and New Zealand see steady demand from mining IoT and agritech, where satellite links cover remote operations.

North America generated about 27.85% of 2025 revenue. The CHIPS and Science Act allocates USD 52 billion to domestic semiconductor capacity, bringing embedded MCU production onshore for defense and critical infrastructure. Canada’s auto-tier suppliers and telecom OEMs rely on BlackBerry QNX for safety-critical OS kernels. Mexico’s near-shoring boom in automotive and consumer electronics lifts demand for bilingual HMIs that satisfy USMCA content rules.

Europe contributed roughly 21.70% of 2025 sales. Germany, France, and Italy dominate industrial automation and EV supply chains. The EU Machinery Regulation effective January 2027 requires cybersecurity risk assessments for every new machine, compelling embedded vendors to secure CE marking. divergence after Brexit raises compliance costs for exporters. Spain and Italy emphasize renewable energy embedded controllers as Iberdrola and Enel digitize distributed assets.

South America, the Middle East, and Africa collectively hold under 5% share but offer long-term upside. Petrobras specifies IECEx Zone 1 controllers for subsea gear. Dubai’s RTA awarded 2024 contracts for V2X-enabled traffic systems RTA.AE. South Africa automates ore sorting with rugged vision systems, while Kenya pilots IoT crop sensors despite patchy cellular coverage.

Regulatory Landscape

Embedded computing systems are increasingly shaped by horizontal cybersecurity and safety compliance regimes that apply to "products with digital elements" and connected industrial and consumer devices. In the European Union, the Cyber Resilience Act (Regulation (EU) 2024/2847) entered into force in December 2024. It tightens secure-by-design requirements, vulnerability handling, and documentation expectations for CE-marked embedded products, pushing suppliers toward SBOM-ready development and post-market monitoring processes. In parallel, the Radio Equipment Directive cybersecurity provisions via Regulation (EU) 2022/30 became applicable on August 1, 2025, raising the compliance bar for embedded platforms that include radio interfaces used in IoT gateways, HMIs, and smart-home devices.

Standards and conformity infrastructure are also moving through 2026, shaping how vendors demonstrate process maturity and software lifecycle control. ISO/IEC/IEEE 12207:2026 was published in April 2026 to provide a software life cycle process framework for embedded software integrated into larger systems, and the European Commission issued Commission Implementing Decision (EU) 2026/901 to list standards supporting the General Product Safety Regulation (EU) 2023/988. These updates reinforce procurement preferences for certified development processes and traceable update practices in sectors already anchored to functional safety and security requirements (including IEC 61508-driven validation in industrial automation and secure module procurement rules such as FIPS 140-3 in US federal purchasing).

Value Chain Analysis

The value chain for embedded computing systems spans IP and software stacks (CPU/GPU/accelerator IP, RTOS, middleware, toolchains), semiconductor manufacturing (fabless design, foundries, advanced packaging), and board and module manufacturing (SBCs, COMs, industrial PCs, edge servers). It continues through system integration into end-user equipment across industrial automation, automotive, healthcare, telecom, and consumer devices. Distribution and after-sales software operations, including device management, OTA updates, security patching, and lifecycle services, increasingly influence long-tail profitability as vendors monetize fleet management and compliance maintenance beyond initial hardware shipment.

Supply-side friction remains concentrated around foundry allocation and advanced packaging availability, which affects lead times for compact SoCs and AI-capable modules used at the edge. The report context points to oversubscribed fan-out wafer-level capacity through late 2025, extending lead times for low z-height packages, and broader industry commentary entering 2026 points to capacity constraints at leading foundries and a shift toward longer-term supply agreements to secure commitments. In response, OEMs and module vendors are pushed toward design-for-supply-chain practices such as multi-sourcing, wider approved vendor lists, and modular form factors (COM Express, SMARC, Qseven) that enable faster substitution of compute building blocks when specific SoCs, memory, or packaging options are constrained.

Competitive Landscape

The top ten providers earned about 55% of 2024 revenue, making the embedded computing systems market moderately concentrated. Intel, NXP, Renesas, NVIDIA, and Qualcomm vie on performance-per-watt and functional-safety credentials. Board vendors such as Advantech, Kontron, and Axiomtek differentiate with extended temperature ratings and 10-year lifecycle guarantees. AMD’s 2022 acquisition of Xilinx merges adaptive compute into CPU roadmaps, while Intel’s SiFive stake secures RISC-V IP. White-space remains in sub-1 W edge AI and ISO 13849-certified cobot modules. Community boards from Raspberry Pi and BeagleBoard convert maker adoption into industrial follow-ons by offering hardened versions.

Patent filings concentrate on heterogeneous chiplet packaging and secure boot. NXP devoted USD 1.8 billion to R&D in 2024, focusing on hardware security modules for ISO 21434 auto compliance. IEEE and IEC harmonize Ethernet-based fieldbus protocols, curbing vendor lock-in. Hardware makers increasingly bundle real-time OS licenses; Qualcomm pairs INTEGRITY RTOS with Snapdragon Auto to guarantee deterministic ADAS scheduling.

Supplier rivalry also centers on supply-chain resilience. Firms with guaranteed advanced packaging allocations gain pricing power during shortages. Smaller RISC-V licensors fragment the ISA but simultaneously spur tool innovation, benefitting developers who can swap cores without rewriting applications. Overall, the embedded computing systems industry shows healthy competition balanced by high entry barriers in safety certification and long-tail software maintenance.

Embedded Computing Systems Industry Leaders

Arm Ltd.

Axiomtek Co. Ltd.

Congatec AG

Dell Technologies Inc.

Fujitsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Cybersecurity compliance is creating a platform opportunity for embedded computing systems, particularly in Europe where the Cyber Resilience Act entered into force in December 2024 and introduces vulnerability handling and documentation obligations across product lifecycles. Vendors that productize secure development, SBOM generation, and update orchestration can turn compliance work into repeatable embedded platforms and service layers for industrial automation, healthcare devices, and connected machinery procurement programs that already require auditable security and safety practices.

Edge AI also continues to open whitespace for higher-value embedded modules and systems that integrate dedicated acceleration within tight power and thermal envelopes, especially for factory vision, robotics, and rail or transport surveillance endpoints. Market evidence in 2026 includes new edge-AI-focused embedded processor and compute introductions from major suppliers, including AMD introducing its Ryzen AI Embedded portfolio in January 2026 and starting production shipments of the Ryzen AI Embedded P100 Series in July 2026, and NVIDIA introducing Jetson Thor computers for robotics and edge AI agent development in July 2026. With AI-capable silicon, modular compute form factors, and certified secure development processes, the opportunity shifts toward reusable embedded platforms deployed across device fleets and maintained over multi-year lifecycles.

Recent Industry Developments

- June 2026: Congatec received IEC 62443-4-1:2018 certification from TUeV NORD for its embedded building blocks development processes. The certification formalizes secure development lifecycle controls that help OEM customers shorten supplier qualification cycles in industrial automation and other critical infrastructure segments where process evidence is required for procurement.

- March 2026: Espressif Systems unveiled the ESP32-S31, a dual-core RISC-V SoC integrating Wi-Fi 6, Bluetooth 5.4, and hardware-accelerated security. The launch strengthens the low-power, multi-protocol connectivity layer for embedded IoT endpoints, supporting deployments where on-device security features and standards-based wireless connectivity are procurement checkboxes.

- November 2024: NXP launched the ISO 26262 ASIL-D-certified i.MX 95 with an NPU and a Cortex-M7 real-time core aimed at sub-1 ms control loops. The device raises the performance and safety baseline for automotive and industrial embedded platforms by combining AI acceleration with deterministic real-time capability in a safety-oriented design.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the embedded computing systems market covers purpose-built computing hardware and the supporting software used inside equipment to perform dedicated functions, often under real-time or near real-time needs, across major commercial and industrial end uses.

Scope exclusions: We exclude general-purpose PCs, consumer smartphones, and stand-alone cloud hosting services that are not sold as part of an embedded computing system.

Segmentation Overview

- By Component Type

- Hardware

- Industrial PC

- HMI

- Edge Servers

- Other Hardwares

- Software

- Hardware

- By Architecture

- RISC

- CISC

- ARM

- DSP

- FPGA

- ASIC

- By Form Factor

- COM - Computer on Module

- SBC - Single Board Computers

- System on Chip

- Rackmount Embedded Systems

- Other Form Factors

- By End User

- Automotive

- Industrial Automation

- Healthcare

- Retail

- Consumer and Smart Home

- Aerospace and Defense

- Telecommunications

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the value chain and to anchor the model to trackable signals such as chip shipments, industrial production, and electronics trade flows. Public sources were reviewed, including US Census trade data, Eurostat, the World Semiconductor Trade Statistics releases, ITU telecom indicators, and standards or regulatory publications that spell out device requirements for safety-critical uses.

We also screened company annual reports and investor decks to understand product mix shifts, pricing pressure, and where embedded boards and modules are being adopted faster. Where needed, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to validate timelines and technology direction. The sources listed here are illustrative, and many other public and paid references were also consulted for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with supply-side roles (product, sales, and engineering) and demand-side users across automotive, industrial automation, telecom, and aerospace and defense, so assumptions could be tested where desk sources were thin. Because this is a global market, inputs were checked across APAC, EMEA, and the Americas, and we re-contacted experts when pricing, form-factor mix, or architecture adoption appeared to move faster than expected.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 42% |

| Mid tier: 53% | Functional/Unit leaders: 31% | EMEA: 34% |

| Smaller Players: 20% | Managers: 53% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where electronics production and trade data are used to reconstruct the addressable embedded compute demand pool, and then it is filtered by adoption in key equipment types. The totals are then checked with selective bottom-up approximations, such as sampled average selling price by form factor multiplied by estimated shipment volumes, plus supplier-side revenue direction from filings and interviews.

Key model inputs include shipment trends for industrial and automotive electronics, the mix shift across SBCs, COMs, and system-on-chip designs, the pace of edge AI workload adoption, architecture mix changes (such as ARM and RISC style adoption), and regional manufacturing output indicators that influence build rates. For forecasting, scenario analysis was used to reflect different paths for semiconductor supply conditions, equipment demand cycles, and price erosion, and the final path was aligned to the operating case most experts described as likely. Where bottom-up coverage is incomplete, gaps are handled through penetration assumptions by end-use equipment category, and those assumptions are revisited if interview feedback suggests a mismatch.

Data Validation & Update Cycle

Validation is done by comparing the model outputs against independent signals, such as semiconductor shipment direction, electronics export trends, and end-market equipment production indicators, and then reviewing variances that do not align. If a region or application shows an abrupt jump, we re-check conversion steps, currency timing, and the assumed mix of boards, modules, and software before sign-off.

A multi-step analyst review is followed so inputs, formulas, and written logic match, and any unusual movements are explained in simple terms. Reports are refreshed annually, and interim updates are made when major events materially change demand or pricing. Before delivery, a final pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Embedded Computing Systems Market Estimate Compared With Other Published Estimates

Published market sizes for embedded computing systems can look different even when the topic name is similar, because each source draws the boundary around what counts as embedded compute and how software is treated. Differences also come from base-year timing, currency conversion choices, and whether a source takes a more conservative or a more aggressive outlook.

In this market, the biggest drivers tend to be whether broader semiconductor content is included, how edge AI acceleration is priced into ASP movement, and whether adjacent services are bundled into the same total. Reporting year also matters, since a one-year shift can change the number when semiconductor supply tightness or price erosion is happening at the same time.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 114.24 B (2025) | |

| Industry Publisher A | USD 119.38 B (2025) | The estimate appears to use a broader embedded computing definition that can pull in a wider component set, and it applies a longer forecast window where near-term pricing changes are smoothed. |

| Research Portal B | USD 130.70 B (2025) | The figure likely includes a wider technology and solution scope, and it may roll in services alongside hardware and software, which lifts the 2025 total versus a tighter product boundary. |

The table shows a spread around the same 2025 year, and in Mordor Intelligence's model the total is limited to embedded computing systems hardware and the supporting embedded software, rather than counting broader semiconductor content or packaged services as part of the same market value. With that scope fixed, the model stays easier to audit because the inputs are tied to observable production, trade, and adoption indicators that can be rechecked each refresh cycle.

Key Questions Answered in the Report

How large is the embedded computing systems market in 2026?

The embedded computing systems market size is USD 124.01 billion in 2026.

What is the expected growth rate for embedded computing platforms toward 2031?

Revenue is projected to grow at a 8.55% CAGR, reaching USD 187.02 billion by 2031.

Which region is expanding fastest in embedded controllers?

Asia Pacific leads with a 12.45% CAGR to 2031, powered by policy incentives in China and India.

Why is software revenue outpacing hardware in embedded deployments?

OEMs increasingly monetize real-time operating systems, middleware, and update services, which scale better than one-time board sales.

How are electric vehicles influencing embedded compute demand?

Battery electric cars integrate two-to-three times more controllers than combustion models to manage packs, inverters, and ADAS functions.

What architecture trend challenges ARM’s dominance?

RISC-V cores are gaining ground due to royalty-free licensing and custom extension flexibility, growing at an 10.73% CAGR.

Page last updated on: