Hybrid Mattress Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

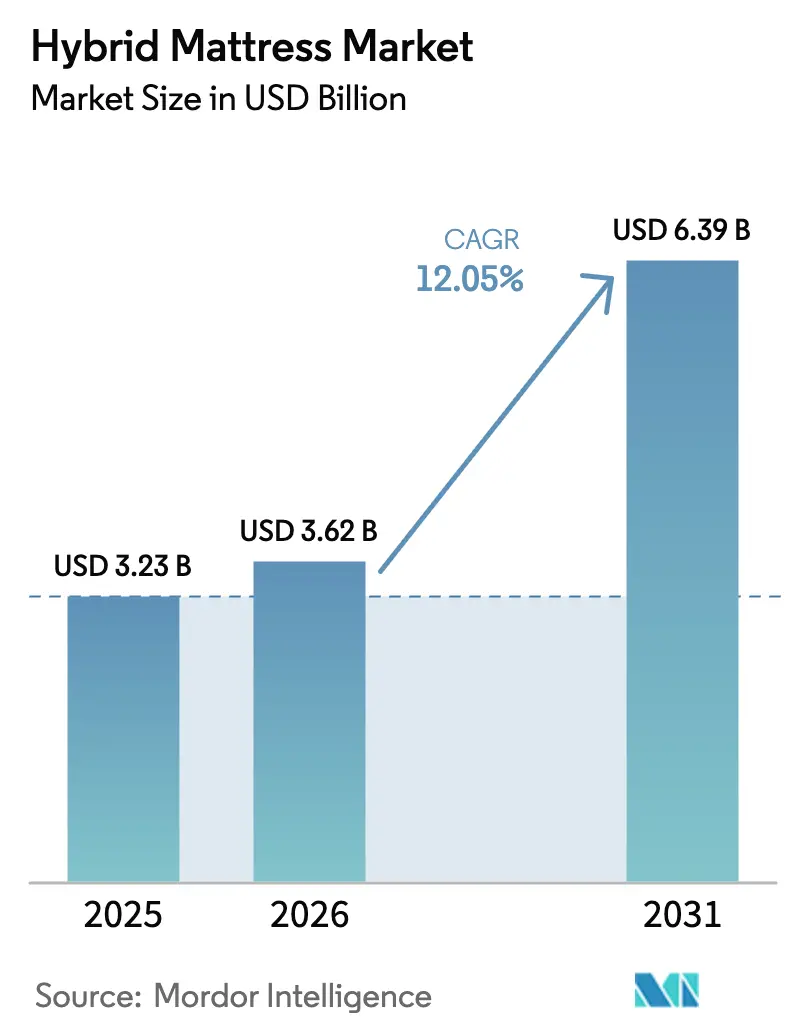

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 6.39 Billion |

| Growth Rate (2026 - 2031) | 12.05% CAGR |

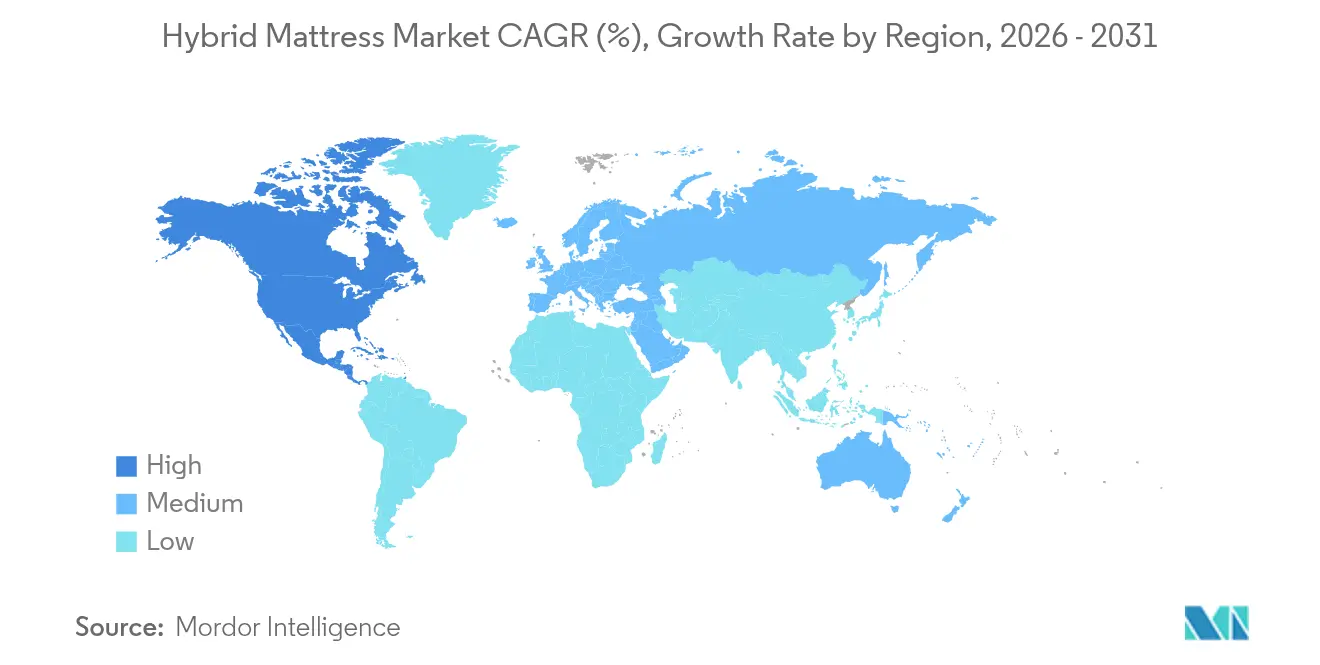

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Mattress Market Analysis by Mordor Intelligence

The hybrid mattress market size was valued at USD 3.23 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 6.39 billion by 2031, at a CAGR of 12.05% during the forecast period (2026-2031). Demand remains resilient because hybrid construction pairs familiar coil support with evolving foam and micro-coil layers, delivering balanced pressure relief and bounce that many consumers have struggled to find in single-material beds. Premium wellness positioning, a pronounced shift toward direct-to-consumer e-commerce, and rapid feature innovation—such as active cooling, bio-based foams, and app-linked sleep tracking—reinforce the category’s pull even as overall furniture spending softens. Trade actions on imported mattresses, together with volatile petrochemical inputs, elevate cost pressure, but vertically integrated suppliers protect margins by controlling upstream foam output and final-mile logistics. Merger activity—most notably Tempur Sealy’s purchase of Mattress Firm—compresses retail shelf space, yet simultaneously unlocks large-scale omnichannel efficiencies that smaller direct-to-consumer brands can mimic only through partnerships.

Key Report Takeaways

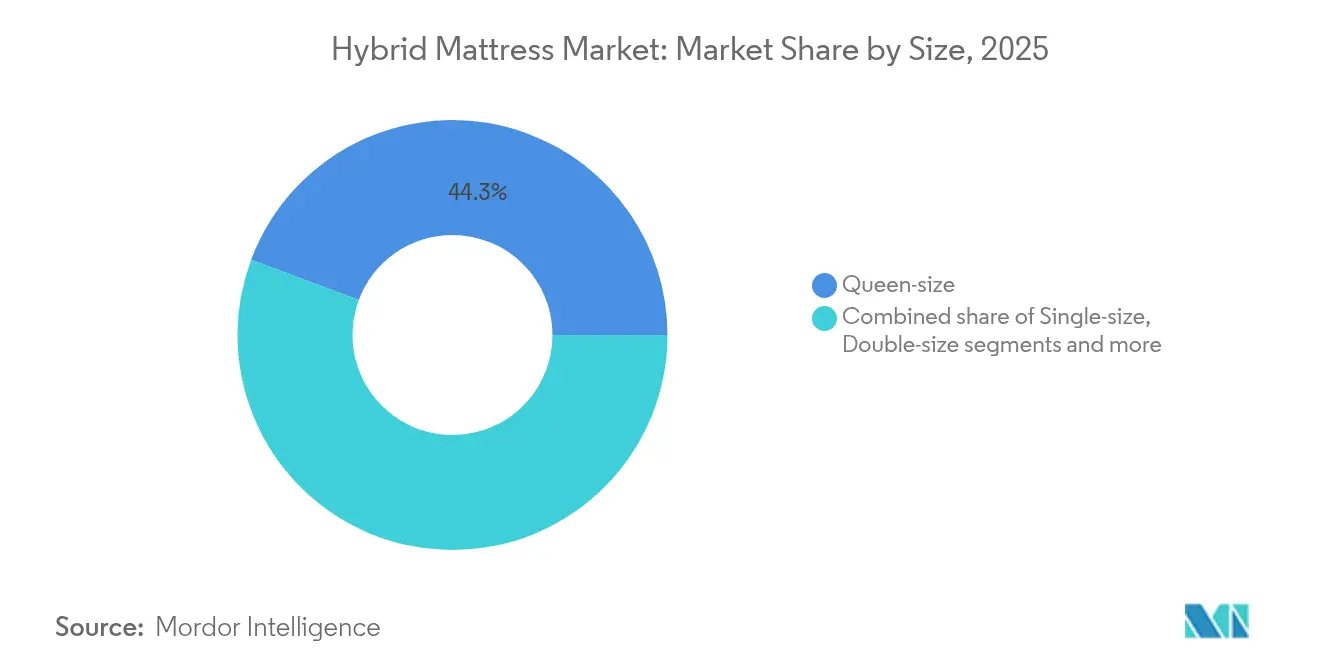

- By size, queen-size accounted for 44.30% revenue share of the hybrid mattress market in 2025; King-size is on track to expand at a 13.75% CAGR through 2031.

- By price range, the premium tier commanded 39.40% share of the hybrid mattress market size in 2025, while the mid-range tier is forecast to grow at 13.25% CAGR to 2031.

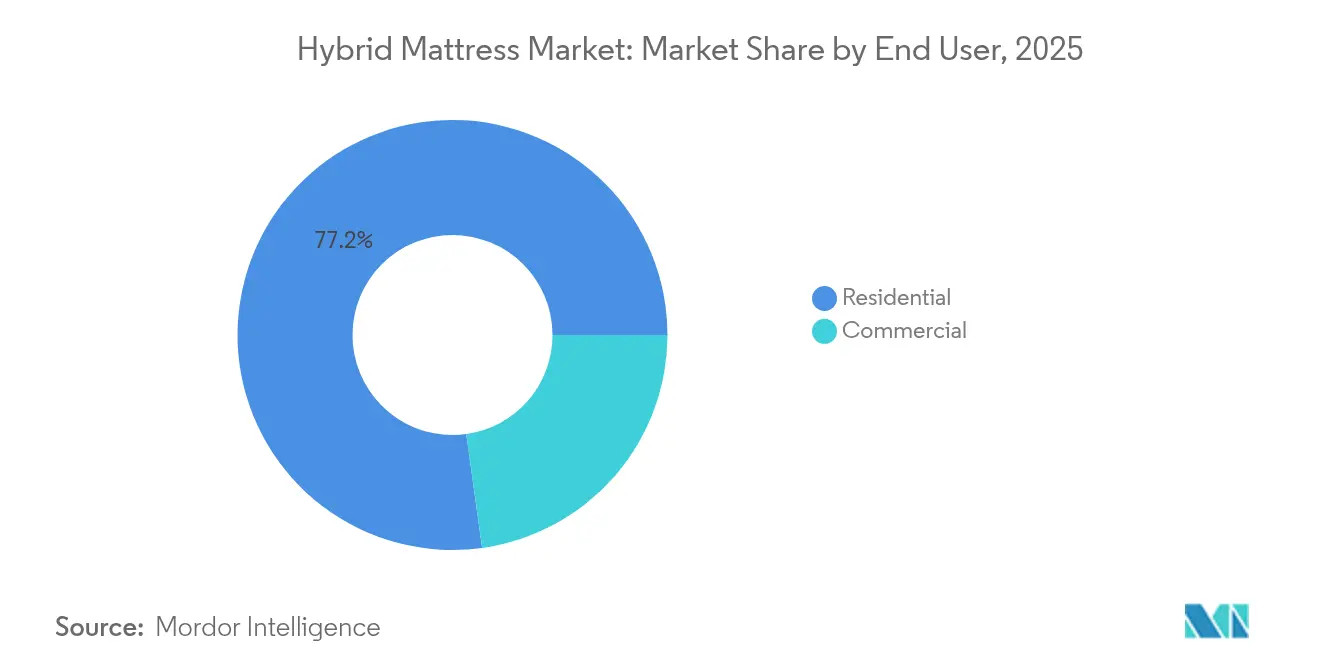

- By end user, residential buyers represented 77.20% of the hybrid mattress market share in 2025; commercial buyers are advancing at a 8.85% CAGR.

- By distribution channel, B2C retail held 79.10% share of the hybrid mattress market size in 2025, with online sales inside this channel accelerating at 14.8% CAGR.

- By geography, North America led with a 32.60% revenue share in 2025; Asia-Pacific is advancing at a 14.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hybrid Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Focus on Sleep Quality & Wellness | +3.2% | Global, strongest in North America & EU | Medium term (2-4 years) |

| Expansion of D2C E-Commerce Mattress Brands | +2.8% | Global, fastest in APAC | Short term (≤ 2 years) |

| Housing Renovation Boom in Key Urban Clusters | +2.1% | North America & EU core; APAC spill-over | Medium term (2-4 years) |

| Smart-Sensor & Phase-Change Cooling Integration | +1.9% | NA & EU first adopters | Long term (≥ 4 years) |

| Modular, Fully-Recyclable Hybrid Designs Gain Policy Tailwinds | +1.4% | EU leadership; NA following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Focus on Sleep Quality & Wellness

Consumers increasingly frame a mattress purchase as a health investment rather than a furniture swap, and hybrid engineering supports that narrative by combining ergonomic coil zoning with pressure-relieving foam that stabilizes spinal alignment. Sleep Number’s university-validated ClimateCool smart bed, which actively cools each side by up to 15 degrees, exemplifies how wellness science now anchors product value propositions. Marketing directed at menopausal sleepers seeking thermal regulation, athletes monitoring recovery, and knowledge workers combating fatigue broadens the buyer pool. The resulting willingness to pay for tangible wellness gains shields average selling prices against inflation in petrochemical foams. Demand elasticity, therefore, tilts toward performance over cost, sustaining premium tier momentum even in price-sensitive climates.

Expansion of D2C E-Commerce Mattress Brands

Direct-to-consumer challengers deploy compressed-roll shipping and 100-night trials to bypass traditional bedding showrooms, capturing shoppers who prefer digital discovery and doorstep delivery. Their feedback loops—every online review, chatbot exchange, and return questionnaire—feed rapid design iterations, allowing brands to debut upgraded hybrid builds within months rather than years. The sub-channel’s 15.2% CAGR inside overall B2C retail shows that even high-ticket sleep products can migrate online when friction is removed. Yet reverse-logistics costs from bulky returns erode margins, prompting experiments with charitable donation rerouting and consolidated pick-up hubs. Companies mastering that back-end efficiency gain a durable cost edge while sustaining generous trial policies that underpin sales growth.

Housing Renovation Boom in Key Urban Clusters

A post-pandemic desire to upgrade living spaces, coupled with extended remote-work patterns, is driving an upswing in bedroom remodels. Mattresses are replaced midway through these projects, not merely at end-of-life, compressing replacement cycles and favoring premium hybrids pitched as centerpieces of holistic sleep sanctuaries. In major North American metros, renovation spending has outpaced new-home starts, shielding unit volumes from cooling real-estate transactions[1]William Blair & Company, “U.S. Home Renovation Trend Snapshot,” williamblair.com. Europe mirrors the trend as homeowners retrofit energy-efficient windows and leverage tax credits that free discretionary funds for interior comforts. While macro-uncertainty could slow future DIY budgets, professional remodel pipelines booked through 2026 suggest that near-to-mid-term bedding demand retains structural support.

Smart-Sensor & Phase-Change Cooling Integration

Hybrid frameworks readily accommodate embedded thermistors, air channels, or PCM (phase-change material) gel layers without sacrificing coil resilience, allowing vendors to market “smart surface” benefits over legacy innersprings. Connected modules stream rest-quality data to mobile apps where users visualize heart-rate variability and deep-sleep minutes, building brand stickiness through daily engagement[2]Sleep Number Corporation, “ClimateCool Smart Bed Launch,” sleepnumber.com. The hardware can also flag sagging early, letting firms monetize replacement toppers or service plans while extending core mattress life. Active cooling technology is especially valued in hot-and-humid APAC cities with limited central air conditioning; passive PCM draws energy only from body heat and meets EU eco-design rules. Over time, integration costs are expected to fall as sensors scale, making smart hybrids the category norm rather than the luxury exception.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Petro-Chemical Foam Input Prices | -2.1% | Global; acute in APAC | Short term (≤ 2 years) |

| Hybrid Price Premium Vs. Legacy Innerspring | -1.8% | Emerging markets & rural NA | Medium term (2-4 years) |

| Rising Reverse-Logistics Cost of E-Commerce Returns | -1.3% | Global; high in NA & EU | Short term (≤ 2 years) |

| Tightening Flammability Rules Restricting Certain Foams | -0.9% | Global; strictest in NA & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Petro-Chemical Foam Input Prices

Polyol and MDI supply shocks, tied to crude-oil swings and refinery outages, can widen cost spreads by double digits in a single quarter. Because hybrids employ thicker foam comfort layers than legacy innersprings, exposure is magnified, particularly for mid-range SKUs where end-price flexibility is narrow. U.S. antidumping duties on mattresses from India, Kosovo, Mexico, and Spain add further cost layers and compel supply-chain rerouting to tariff-exempt plants [3]U.S. Department of Commerce, “Mattresses From India, Kosovo, Mexico, and Spain: Antidumping Duties,” federalregister.gov. Integrated mattress makers with captive foam lines hedge better, while assemblers dependent on spot purchasing risk margin erosion. The resulting squeeze is pushing some niche players toward consolidation talks or private-label pivots merely to secure stable feedstock.

Hybrid Price Premium Vs. Legacy Innerspring

Even as awareness rises, consumers in lower-income regions still compare ticket prices first, and hybrids average 15-30% higher shelf prices than conventional coils. Value-engineering—lower-density foams or simplified perimeter rails—closes part of this gap, yet performance trade-offs can threaten brand credibility. The mid-range segment’s 13.6% CAGR shows progress, but many first-time buyers remain sceptical of long-term durability claims without physical test beds. Rural North American shoppers, often served by promotional furniture outlets, continue to favor bargain coil mattresses bundled with bedroom sets, delaying hybrid penetration. If macro-inflation persists, down-trading back to basic beds could undercut sales forecasts despite superior hybrid comfort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size: King-Size Upshift in Consumer Preferences

Queen-size, accounting for 44.30% of 2025 sales, shows slower unit gains as empty-nesters and higher-income couples upgrade sleeping quarters. King-size variants lead volume growth at a 13.75% CAGR, easily outpacing the hybrid mattress market. They benefit from dual-zone cooling, motion isolation for partners, and wellness marketing that frames extra surface area as essential to deep sleep. Double and Single formats retain footholds in urban apartments and youth bedrooms, but their mixture share slips marginally each year as space-efficient storage beds make larger frames feasible. California King and bespoke dimensions serve luxury homes and hospitality suites, with hotel chains emphasizing plush King hybrids in upgraded room categories to justify higher nightly rates.

Demand for larger sizes pushes upstream coil suppliers to refine edge-support systems that remain stable under heavier loads, and logistics teams adapt packaging to fit standard door widths without costly white-glove setups. Retail showrooms allot more floor space to King displays, nudging consumers to “size up” via visual comparison. Online configurators that overlay mattress footprints on virtual bedrooms reinforce the scale upgrade trend. As households treat sleep space like square footage insurance against restless nights, the premium for bigger hybrids appears justified, propelling mix-shift-driven revenue even amidst flat unit shipments.

By Price Range: Mid-Range Democratization

Premium hybrids controlled 39.40% of the hybrid mattress market size in 2025, buoyed by sensor-driven upgrades and health-backed marketing. The mid-range, however, demonstrates the fastest trajectory, expanding 13.25% annually as component costs fall and production lines achieve scale economies. Manufacturers trim extras—Bluetooth speakers, under-bed lighting—and instead highlight core hybrid benefits that meet mainstream budgets without stripping essential performance. Economy SKUs remain critical for emerging markets but expose brands to razor-thin margins when MDI prices spike or tariffs rise. As financing apps normalize monthly instalments, many shoppers leapfrog the economy and land in mid-range territory, reinforcing democratization.

Product managers now deliberately design “good-better-best” step-ups, ensuring each rung delivers recognizably higher foam density or coil count to avoid cannibalizing premium lines. Promotional events timed around housing-move seasons lock in incremental share gains. Yet brand custodians must protect premium aura by reserving cutting-edge cooling algorithms, bio-based comfort layers, and extended warranties for the top slate. If they fail, mid-range cannibalization could erode flagship margins, an outcome some category veterans encountered in television and smartphone markets.

By End User: Commercial Awakening

Residential buyers still command 77.20% of hybrid mattress sales owing to entrenched replacement cycles and ongoing urban household formation. Commercial demand, growing 8.85% annually, is catalysed by hotel groups that now advertise sleep programs—pillow menus, circadian lighting, and hybrid beds—to secure five-star review scores. Healthcare facilities adopt pressure-relief hybrids for post-surgery wards, citing reduced bedsore incidence in internal audits. Corporate apartments and extended-stay brands integrate mid-range hybrids to extend product life beyond 200 guest-night cycles, reducing capital-expense turnover relative to traditional contract beds. These institutional customers value durability certifications and rapid bulk-swap services more than consumer-style aesthetics.

Volume contracts often stipulate flame-barrier verifications and anti-microbial fabric treatments, pushing vendors to maintain comprehensive compliance dossiers or risk bid disqualification. Commercial buyers also bargain for rapid lead times, benefiting suppliers with multi-region assembly hubs. While payment terms stretch beyond consumer cash sales, steady order cadence cushions revenue volatility tied to retail seasonality.

By Distribution Channel: Online, Re-writes Retail

The B2C channel’s 79.10% dominance reflects mattress buyers’ reticence toward third-party contract procurement and the enduring allure of showroom testing. Within B2C, however, online sales clock a 14.8% CAGR as compressed packaging, real-time delivery tracking, and buy-now-pay-later plans dissolve barriers to at-home mattress discovery. Legacy specialty chains answer with hybrid e-commerce portals and augmented-reality preview tools that overlay mattress firmness onto avatars. Tempur Sealy’s takeover of Mattress Firm unites a broad physical network with mature e-commerce assets, providing scale to negotiate carrier contracts and share customer data across channels. Smaller D2C labels experiment with mobile show vans and micro-pop-ups inside malls, giving tactile validation without lumbering into full lease commitments.

B2B distribution tackles specification-heavy commercial accounts, where procurement officers issue RFQs and lean on decades-old supplier relationships. Hybrid adoption rises once vendor reps demonstrate coil-count longevity under high turnover usage; yet, purchase cycles are slow, and bid windows occur only once or twice a year. Consequently, B2C remains the headline growth engine shaping brand narratives and marketing spend.

Geography Analysis

North America contributes 32.60% of the hybrid mattress market’s 2025 revenues, anchored by deep consumer familiarity with boxed-bed D2C models and higher disposable income that absorbs premium up-charges. Innovation pipelines—like Sleep Number’s Climate Cool series—keep existing buyers in upgrade cycles and defend price ladders against promotion-driven rivals. Housing mobility, while cooling with higher mortgage rates, still sparks replacement purchases when owners relocate or remodel. Canada offers incremental upside via U.S. brand spill-over, but local flammability codes impose extra labelling, nudging some suppliers to establish regional fulfilment centres. Mexico, despite antidumping duties on U.S. imports, leverages domestic foam plants to produce hybrids for its expanding middle class, insulating local demand from trade skirmishes.

Asia-Pacific shows the fastest 14.05% CAGR to 2031, fuelled by swelling middle classes in India, Indonesia, and Vietnam who equate sleep quality with modern lifestyles. Duroflex’s planned IPO underlines investor conviction that Indian domestic demand can sustain double-digit revenue growth without relying on export arbitrage . China, already the world’s biggest mattress base by units, is gradually shifting from commodity foam builds to mid-range hybrids as urban dwellers upgrade. Japanese and South Korean shoppers embrace app-linked features and appreciate motion isolation in small apartments, steering them toward premium SKUs. Southeast Asian climate conditions elevate interest in breathable latex-coil hybrids, compelling brands to adjust foam chemistries for hot, humid nights. Europe, though slower growing, carves a niche around sustainability imperatives. Germany and France adopt modular hybrids that score well on lifecycle-assessment indices, securing incentives under eco-label procurement programs. Eastern Europe offers fresh territory as rising wages enable discretionary furniture upgrades; however, fragmented language and certification regimes demand localized marketing collateral and service networks. Brexit’s customs paperwork complicates cross-Channel shipments, driving some EU brands to house U.K. inventory in leased warehouses to sidestep border delays. The Middle East and Africa, presently a small share, exhibit hotel refurb activity in Gulf tourism hubs, suggesting commercial seeding that could spill into residential adoption over the next decade.

Competitive Landscape

The hybrid mattress market exhibits moderate concentration. Tempur Sealy’s USD 5 billion takeover of Mattress Firm closed in February 2025, forming Somnigroup International, a vertically integrated heavyweight that controls product design all the way to last-mile delivery. Serta Simmons, emerging from a 2023 restructuring, reinvests in gel-grid hybrids to reclaim showroom floor share. Sleep Number maintains a technology edge, funneling roughly 5% of sales into R&D that produced its adjustable Climate Cool platform. Pure-play D2C companies—Casper, Purple, Emma Sleep—roll out pop-up stores to cut return rates, while local champions such as Kurl-on and Duroflex defend price-sensitive Indian metros with factory-direct tactics.

Supply-chain strategy now defines competitiveness. Brands controlling foam pouring mitigate raw-material price swings, whereas asset-light assemblers rely on short-term spot buys that expose margins. Regulatory proficiency acts as another moat; multinational incumbents fund in-house burn labs to certify every SKU ahead of shifting flammability rules, whereas small entrants risk recalls like Nap Queen’s 2024 fiasco. Collaboration is also on the rise: Dow’s comfort-rating protocol with GoodBed could standardize marketing claims, lessening information asymmetry and favoring players who genuinely deliver pressure-relief scores.

Market segmentation is solidifying into three clusters. The premium wellness tier hosts sensor-rich offerings and commands the highest margin; the mid-range balances coil counts against essential cooling foams; the entry tier fights over price points. Competitive intensity is greatest in the middle, where overlapping price bands meet channel-blurring distribution. Successful firms tailor portfolio differentiation—warranties here, recycled fabrics there—while avoiding cannibalization of higher trim lines. Failure to manage that ladder could squeeze gross profit, a dynamic already visible in quarterly filings from mid-sized D2C firms.

Hybrid Mattress Industry Leaders

Tempur Sealy International

Serta Simmons Bedding

Sleep Number Corp.

Purple Innovation

Casper Sleep Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Duroflex filed for an IPO, targeting plant capacity expansion in Kerala and new mid-range hybrid lines for India’s tier-2 cities.

- February 2025: Tempur Sealy International completed its USD 5 billion acquisition of Mattress Firm, forming Somnigroup International Inc., and announced immediate integration of e-commerce, POS data, and logistics platforms.

- January 2025: Dow and GoodBed launched the first industry-wide scientific testing protocol for mattress comfort, encompassing pressure mapping and thermal dissipation metrics.

- October 2024: Sleep Number debuted ClimateCool, a smart hybrid that lowers each side’s surface temperature by up to 15 degrees and syncs with a proprietary app for sleep-stage analytics.

Global Hybrid Mattress Market Report Scope

A hybrid mattress is the combination of two or more support systems, usually memory foam layers, along with an innerspring system, to offer a balance of comfort, support, and durability. The goal of a hybrid mattress is to create a sleep surface that addresses the shortcomings of individual materials while maximizing their benefits, resulting in a comfortable and supportive sleeping experience. The hybrid mattress market forecast is segmented by application, distribution channel, and geography. By applications, the market is segmented into household and commercial. By distribution channels, the market is segmented into offline and online. And by geography, the market is segmented into Asia-Pacific, North America, Europe, South America, Middle East and Africa, and the Rest of the World. The reports offer the market sizing and forecasts for the hybrid mattress market in value (USD) for all the above segments.

| Single-size |

| Double-size |

| Queen-size |

| King-size |

| Other Sizes |

| Economy |

| Mid-Range |

| Premium |

| Residential |

| Commercial |

| B2B/Directly from the Manufacturers | |

| B2C/Retail Channels | Specialty Bedding and Mattress Stores |

| Multi-brand Stores/Home Centers | |

| Online | |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Aisa-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Size | Single-size | |

| Double-size | ||

| Queen-size | ||

| King-size | ||

| Other Sizes | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2B/Directly from the Manufacturers | |

| B2C/Retail Channels | Specialty Bedding and Mattress Stores | |

| Multi-brand Stores/Home Centers | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Aisa-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size of the hybrid mattress market?

The hybrid mattress market stands at USD 3.62 billion in 2026.

How fast will the hybrid mattress market grow by 2031?

It is forecast to expand at a 12.05% CAGR, reaching USD 6.39 billion.

Which region currently holds the largest hybrid mattress market share?

North America leads with 32.60% of global revenues in 2025.

Why are King-size hybrids growing faster than other mattress sizes?

Consumers seek larger sleep surfaces that support dual-zone cooling and motion isolation, producing a 13.75% CAGR for King-size models.

How important are online channels in hybrid mattress sales?

Online purchases inside B2C retail are growing 14.8% annually, reshaping how consumers research and buy mattresses.

What is the biggest operational challenge for direct-to-consumer mattress brands?

High reverse-logistics expenses from bulky product returns threaten profitability despite strong sales growth.

Page last updated on: