Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.41 Billion |

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 1.66 Billion |

| Growth Rate (2026 - 2031) | 2.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Mattress Market Analysis by Mordor Intelligence

The United Kingdom mattress market size was valued at USD 1.41 billion in 2025 and estimated to grow from USD 1.45 billion in 2026 to reach USD 1.66 billion by 2031, at a CAGR of 2.74% during the forecast period (2026-2031). A mature demand base underpins steady replacement cycles, even as raw-material cost inflation and tighter Competition and Markets Authority (CMA) oversight pressure margins. Growth pockets are opening around foam technology upgrades, hospitality refurbishment ahead of major 2028 tourism events, and sustainability-linked procurement policies that reward low-carbon designs. Online bed-in-a-box brands continue to reshape shopper expectations through long trial periods and compressed shipping, prompting traditional retailers to accelerate omnichannel upgrades. Heightened consumer awareness of sleep quality, a build-to-rent (BTR) housing boom, and rising demand for pressure-relief models among aging households round out the principal growth catalysts.

Key Report Takeaways

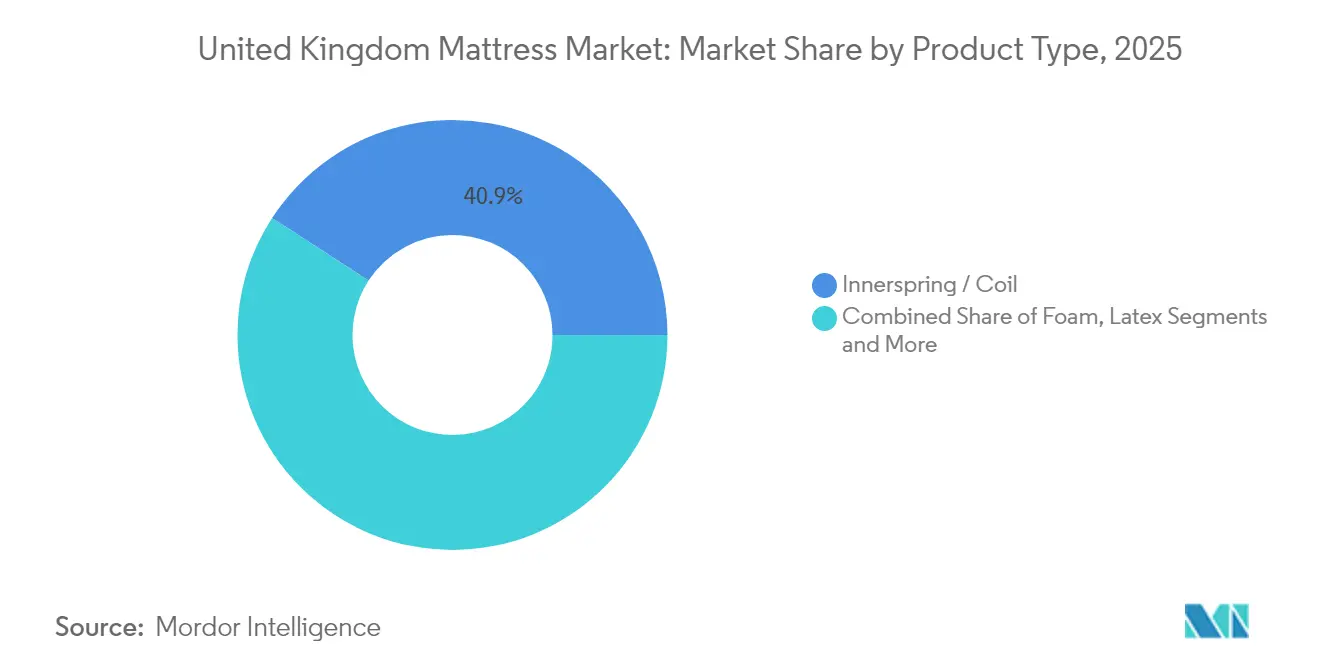

- By product type, innerspring mattresses led with 40.85% of United Kingdom mattress market share in 2025, while foam variants are on track to post the fastest 3.02% CAGR through 2031.

- By mattress size, king-size units captured 37.12% of the United Kingdom mattress market size in 2025, whereas queen-size formats are projected to expand at a 3.46% CAGR between 2026 and 2031.

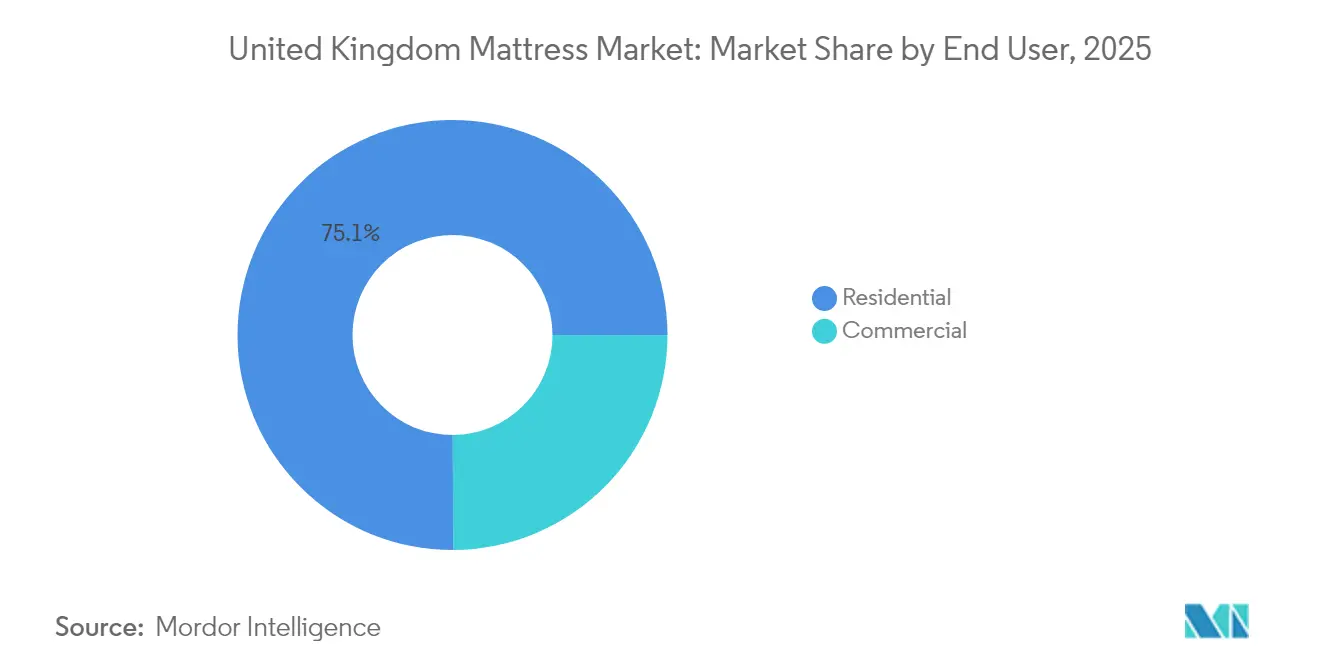

- By end user, residential applications accounted for 75.05% share of the United Kingdom mattress market size in 2025; the commercial segment is advancing at a 3.79% CAGR through 2031.

- By distribution channel, B2C retail commanded 71.62% of the United Kingdom mattress market size in 2025, whereas online platforms are projected to expand at a 3.48% CAGR through 2031

- By geography, England held 40.88% share of the United Kingdom mattress market size in 2025, and Scotland is forecast to record the highest 4.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently high replacement demand driven by UK homeowners' renovation cycles | +0.8% | England, Scotland, Wales | Medium term (2-4 years) |

| Proliferation of e-commerce bed-in-a-box brands reshaping buying behaviour | +0.6% | Global, concentrated in urban areas | Short term (≤ 2 years) |

| Hospitality re-furbishment surge ahead of major 2028 UK tourism events | +0.4% | England, Scotland | Short term (≤ 2 years) |

| ESG-linked procurement by large retailers favouring low-carbon mattresses | +0.3% | Global, EU compliance focus | Long term (≥ 4 years) |

| Build-to-Rent furnishing schemes and mattress-subscription models unlocking recurring demand | +0.5% | London, Manchester, Birmingham | Medium term (2-4 years) |

| Ageing-in-place drives uptake of pressure-relief home-care mattresses | +0.7% | England, Wales, aging demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistently High Replacement Demand Driven by UK Homeowners’ Renovation Cycles

British homeowners continue to postpone mattress replacements well beyond the seven-year guideline, leaving pent-up demand that releases when households renovate, relocate, or invest in wellness upgrades. The Travelodge UK Mattress Census notes that 31% of adults sleep on mattresses beyond the recommended lifespan and 10% keep them up to 20 years, even though 43% report discomfort and 20% experience morning aches[1]Source: Travelodge, “UK Mattress Census,” travelodge.co.uk. Property transactions typically trigger a mattress upgrade within 18 months, ensuring a steady rhythm of replacement sales. Post-pandemic emphasis on the bedroom as a restorative retreat further elevates sleep-quality spending. Consumer-education campaigns by retailers and the National Bed Federation underline the health costs of over-aged sleep surfaces, creating long-run replacement tailwinds.

Proliferation of E-commerce Bed-in-a-Box Brands Reshaping Buying Behavior

Direct-to-consumer innovators such as Emma Sleep, Simba, and Eve Sleep command roughly 5% of the United Kingdom mattress market, having broken the showroom dependency by compressing foam mattresses into easily delivered boxes and backing sales with 90- to 365-day trials[2]Source: The Guardian, Sarah Butler, “Mattress Start-ups Shake Up UK Bed Market,” theguardian.com. Convenience, price transparency, and friction-free returns resonate with digital natives, and analysts project the online cohort’s share could quadruple within three years. Traditional retailers have responded by rolling out their own-brand boxed ranges, upgrading websites, and offering click-and-collect. Yet customer-acquisition costs above 30% of revenue challenge e-commerce profitability, fueling consolidation moves such as Simba’s 2025 sale to Sleep Country. CMA scrutiny of online urgency tactics now obliges clearer pricing, nudging bed-in-a-box firms toward sustainable growth models.

Hospitality Refurbishment Surge Ahead of Major 2028 UK Tourism Events

Hotel chains are bringing forward mattress-replacement programs to enhance guest satisfaction ahead of landmark sports and cultural gatherings scheduled for 2028. Premier Inn plans to operate 97,000 rooms by 2028/29, up from 83,000 in 2025, and specifies Silentnight’s medium-firm Mattress 2.0 for its refreshed estates[3]Source: Whitbread PLC, “Premier Inn Expansion Plans,” whitbread.co.uk. Branded operators gained share after an independent-hotel contraction of 4% since 2019, concentrating procurement with a handful of contract manufacturers. Mattress makers benefit from five- to seven-year hospitality replacement cycles that dwarf household volumes, while specification standards push suppliers toward durable, flame-retardant, and environmentally certified designs. The hospitality uplift therefore provides a sizeable, time-bound volume spike that overlaps with wider ESG imperatives.

ESG-Linked Procurement by Large Retailers Favoring Low-Carbon Mattresses

Retailers are embedding carbon-reduction targets into vendor scorecards, creating measurable advantages for manufacturers able to certify low-emission supply chains. Marks & Spencer cut Scope 1 and 2 emissions 33% from the 2016/17 baseline and aims for net-zero across its value chain by 2040, prompting suppliers to design mattresses that exceed existing eco-labels. Silentnight has attained Carbon Neutral+ status and redesigned contract ranges for easier recycling, aligning with North London Waste Authority pilots that diverted 51,000 mattresses from landfill in eight months. ESG alignment not only wins tenders but also defends margins when consumers trade up to sustainable options. Over time, circular-economy legislation is expected to make reparability and recyclability table stakes for market access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-inflation in polyurethane & steel springs squeezing mid-tier margins | -0.5% | Global supply chains affecting UK | Short term (≤ 2 years) |

| Heightened CMA scrutiny of online discounting tactics dampening flash-sale volumes | -0.3% | England, online-focused brands | Short term (≤ 2 years) |

| Second-hand/grey-market influx from large-scale refurb projects cannibalising first-sales | -0.4% | England, Scotland, urban centers | Medium term (2-4 years) |

| Stricter UK fire-retardant chemical limits raising reformulation costs for foam producers | -0.2% | England, Wales, manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Inflation in Polyurethane & Steel Springs Squeezing Mid-Tier Margins

Foam costs face upward pressure amid a planned Carpenter-Recticel merger that would consolidate one of only three UK producers and risk price hikes in comfort foam supply, according to CMA concerns[4] Source: Competition and Markets Authority, “Carpenter-Recticel Merger Inquiry,” gov.uk. January 2025 producer-price data showed input prices virtually flat while output prices crept up 0.3%, illustrating manufacturers’ limited headroom to absorb raw-material spikes. Mid-tier brands lack the premium pricing power of luxury labels and the scale efficiencies of mass-market players, so margin compression is acute. Steel-coil prices, governed by volatile global scrap and energy costs, further strain innerspring models, which still account for 41.29% of sales. Manufacturers, therefore, accelerate vertical integration or lean toward hybrid and foam lines with lower metal intensity.

Heightened CMA Scrutiny of Online Discounting Tactics Dampening Flash-Sale Volumes

The CMA filed High Court proceedings against Emma Sleep in October 2024 for countdown timers and reference prices that misrepresented genuine savings, undermining the urgency tactics central to flash-sale volume lifts. New powers from April 2025 permit fines of up to 10% of global turnover for unfair-practice breaches, forcing online sellers to overhaul promotions. Bed-in-a-box firms, heavily reliant on limited-time offers to trigger conversions, now face higher marketing spend and slower sales spikes, diluting the channel’s growth premium. Traditional retailers with everyday-value positioning feel less impact, narrowing the competitive gap. Transparent pricing and third-party certifications emerge as trust signposts shaping future digital conversions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Innerspring Dominance Faces Foam Innovation

In 2025, innerspring units secured 40.85% share of the United Kingdom mattress market size through consumer familiarity with coil support and perceived longevity. Foam lines, however, hold the growth crown at a 3.02% CAGR, buoyed by memory-foam refinements that address heat retention and durability complaints. Hybrid models blending coils with foam comfort layers gain traction among shoppers seeking balanced support, while latex remains a premium eco-niche. Manufacturers are improving flexible polyurethane foam’s resilience and airflow, with EUROPUR research highlighting advancements that extend usable life and enhance ergonomic conformity. Compliance with BS 7177 fire-safety requirements affects all types, but foam producers shoulder added reformulation costs to replace restricted flame-retardants, lifting average selling prices.

Foam’s ascendancy intertwines with the bed-in-a-box phenomenon because compressibility favors all-foam cores. As e-commerce adoption widens, foam suppliers secure scale leverage and invest in low-VOC chemistries that appeal to ESG-driven buyers. In contrast, innerspring lines leverage differentiated coil counts and zoning to maintain relevance, especially within traditional showroom environments. Marketing now stresses hybrid comfort benefits such as edge support and temperature neutrality. Altogether, innovation paths diverge: foam specialists chase material science gains, while coil manufacturers focus on optimizing steel-usage efficiency and recyclability.

By Mattress Size: King-Size Leadership with Queen-Size Momentum

King-size mattresses dominated with 37.12% market share in 2025, reflecting UK housing trends toward larger bedrooms and consumer willingness to invest in premium sleep experiences. Queen-size variants are experiencing the fastest growth at 3.46% CAGR through 2031, driven by urban apartment living constraints that balance space optimization with comfort preferences. Double-size mattresses maintain steady demand in guest rooms and smaller accommodations, while single-size options serve children's rooms and budget-conscious consumers. Custom and specialty sizes address niche requirements, including extra-long variants for tall individuals and bespoke dimensions for unique bed frames.

Housing stock evolution underpins shifting size preferences. High-density city projects constrain room dimensions, channeling incremental demand toward queen formats. Conversely, suburban expansions with generous layouts preserve king-size preeminence. Manufacturing efficiency favors standard sizing, yet bespoke extra-long orders are rising among taller demographics. Retailers increasingly market split-firmness king models to address partner comfort mismatches, blending luxury cues with personalization.

By End User: Residential Stability with Commercial Acceleration

Residential applications maintained 75.05% market share in 2025, reflecting the sector's fundamental role as the primary mattress consumption driver through household replacement cycles and new home furnishing. Commercial segments are growing faster at 3.79% CAGR through 2031, propelled by hospitality sector expansion, healthcare facility upgrades, and Build-to-Rent sector development. The commercial growth trajectory reflects institutional purchasing patterns that prioritize durability, fire safety compliance, and bulk procurement advantages over individual consumer preferences.

Healthcare facilities purchase pressure-relief surfaces to mitigate pressure-ulcer incidence affecting roughly 412,000 UK patients every year. Pressure-management technology — alternating-air cells, viscoelastic foams — increasingly migrates into home-care segments as aging-in-place gains policy backing. Hospitality operators, by contrast, emphasize brand-standard consistency, using mattress quality as a differentiator in online guest reviews. BTR owners adopt service contracts with built-in replacement cycles, expanding recurring revenue streams for compliant manufacturers.

By Distribution Channel: Retail Dominance with Digital Integration

B2C retail channels commanded 71.62% market share in 2025 while growing at 3.48% CAGR through 2031, demonstrating the sector's successful adaptation to omnichannel consumer preferences. Mass merchandisers benefit from high-volume purchasing power and broad geographic coverage, while specialty mattress stores maintain relevance through expert consultation and product demonstration capabilities. Online channels have fundamentally reshaped consumer behavior, with bed-in-a-box brands leveraging direct-to-consumer models that bypass traditional retail markups and enable trial periods impossible in physical stores.

Project-based B2B channels serve hotels, hospitals, and furnished-housing schemes. Buyers require detailed compliance paperwork, flame-retardant certification, ESG disclosures, and recyclability statements, creating entry barriers that favor established brands. The National Bed Federation (NBF) introduced a retailer-support package that promotes NBF-approved labels, acting as a quality filter that reassures consumers and project buyers alike. As CMA enforcement stiffens, transparent online pricing and friction-less in-store experience converge into a unified customer journey.

Geography Analysis

England continues to anchor the United Kingdom mattress market with a 40.88% share because of its population density, retail saturation, and robust build-to-rent pipeline. London drives premium hybrid adoption, while concurrent affordability sensitivities in northern counties maintain a strong base for mid-range innerspring models. The CMA’s promotional-pricing clampdown disproportionately affects England-centric online players, nudging some traffic back to in-store environments. Simultaneously, region-wide ESG goals stimulate low-carbon product lines and recycling partnerships with local authorities. Regional variations within England reflect economic disparities, with southern markets demonstrating premium product preference while northern regions show greater price sensitivity and promotional responsiveness.

Scotland’s 4.01% CAGR expectation to 2031 rests on Edinburgh’s expanding financial services sector, Glasgow’s urban renewal schemes, and an influx of tourists heading to cultural festivals. Hotel chains retrofit guest rooms with medium-firm, recyclable models to meet brand-standard upgrades ahead of 2028. The devolved government promotes circular-economy agendas that incentivize mattress recyclability, benefiting compliant manufacturers with clear carbon accounting frameworks. Aberdeen’s energy workforce supports discretionary spending on premium beds, cushioning regional demand against commodity-price swings. Energy sector employment stability, particularly in Aberdeen and surrounding areas, supports premium mattress purchases despite broader economic headwinds affecting other UK regions.

Wales and Northern Ireland share smaller but strategically important slices of the United Kingdom mattress market. Cross-border shopping corridors expose Welsh consumers to English promotional calendars, while Cardiff’s rising student housing stock boosts twin and double-size volumes. Northern Ireland’s dual alignment with UK and Republic of Ireland standards encourages a competitive landscape rich in euro-denominated online offers, tightening margins for local brick-and-mortar outlets. Both regions see healthcare modernization projects that stipulate pressure-relief mattresses, supporting specialized contract lines.

Competitive Landscape

Market structure is moderately fragmented: no brand claims a double-digit share, and the top five holds major market share in 2024. Dreams, Silentnight, and Tempur Sealy lead through scale, multi-format retail networks, and proprietary sleep-diagnostics tools. Bed-in-a-box rivals, Emma Sleep, Simba, Eve Sleep, together reached roughly 5% market share by parlaying home trials and subscription-based replacement schemes. Rising customer-acquisition costs and new CMA penalties reshape economics, prompting Simba’s 2025 takeover by Sleep Country, a Canadian operator seeking cross-border expansion synergies.

Technology adoption sets competitive borders. Dreams rolled out “Sleepmatch” pressure-mapping kiosks, boosting conversion and cutting returns; Harrison Spinks operates vertically integrated spring and natural-fiber plants, shielding itself from steel and cotton price shocks. Luxury labels Hypnos and Vispring leverage royal warrants and handcrafted narratives to defend price premiums. ESG credentials increasingly sway both retail listings and contract tenders: Silentnight’s Carbon Neutral+ badge positions it favorably with environmentally conscious chains. Meanwhile, the National Bed Federation’s audit program screens suppliers, raising quality expectations and impeding low-cost, non-compliant imports.

White-space opportunities revolve around healthcare pressure-management surfaces, circular-economy models, and recurring-revenue subscriptions. NHS data indicates 412,000 patients endure pressure ulcers annually, underlining unmet need for advanced support surfaces. Mattress-collection and recycling schemes piloted by local authorities encourage manufacturers to design for disassembly and reclaimable components. Corporate wellness programs increasingly include nap rooms furnished with high-spec mattresses, representing a nascent but promising B2B segment. As competition intensifies, differentiation will hinge on transparent ESG metrics, adaptive service models, and AI-driven comfort personalization.

United Kingdom Mattress Industry Leaders

Dreams

Silentnight Group

Tempur Sealy UK

Emma – The Sleep Company

Simba Sleep

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tempur unveiled new mattress and bed ranges at the Design Museum in London, slated for July rollout and priced to broaden the customer base.

- February 2025: Emma Sleep opened its first standalone store outside London, reinforcing its shift toward a hybrid retail model.

- January 2025: Simba Sleep was acquired by Sleep Country, with an upfront payment and earn-outs tied to international expansion milestones.

United Kingdom Mattress Market Report Scope

A mattress is a large, usually rectangular pad supporting a lying person. It is designed to be used as a bed or on a bed frame as part of a bed. The United Kingdom Mattress Market is segmented by type (innerspring mattress, memory foam mattress, latex mattress, and others), application (residential and commercial), and distribution channel (online and offline). The report offers market sizes and forecasts for the United Kingdom Mattress Market in value (USD) for all the above segments.

By Product Type

| Innerspring / Coil |

| Foam (including memory foam) |

| Latex |

| Hybrid |

| Other Mattress Types |

By Mattress Size

| Single-size Mattress |

| Double-size Mattress |

| Queen-size Mattress |

| King-size Mattress |

| Custom & Specialty Sizes |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B/Project |

By Geography

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product Type | Innerspring / Coil | |

| Foam (including memory foam) | ||

| Latex | ||

| Hybrid | ||

| Other Mattress Types | ||

| By Mattress Size | Single-size Mattress | |

| Double-size Mattress | ||

| Queen-size Mattress | ||

| King-size Mattress | ||

| Custom & Specialty Sizes | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

How large is the United Kingdom mattress market in 2026?

The United Kingdom mattress market size stands at USD 1.45 billion in 2026.

What is the expected growth rate for mattresses sold in the UK?

Industry revenue is projected to advance at a 2.74% CAGR through 2031.

Which product type sells most in UK bedding stores?

Innerspring mattresses lead with 40.85% market share as of 2025.

Which UK region is seeing the fastest growth in mattress sales?

Scotland is forecast to grow the quickest, at a 4.01% CAGR to 2031.

What factors are boosting commercial mattress demand?

Hotel refurbishment ahead of 2028 events and build-to-rent furnishing cycles propel commercial purchases at a 3.79% CAGR.

Page last updated on: