Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.72 Billion |

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Mattress Market Analysis by Mordor Intelligence

The Australia mattress market size is expected to increase from USD 1.72 billion in 2025 to USD 1.78 billion in 2026 and reach USD 2.12 billion by 2031, growing at a CAGR of 3.56% over 2026-2031. Growth in the Australian mattress market is supported by premiumization, stronger compliance with pricing transparency rules, and a broader consumer focus on sleep wellness, which sustains upgrades rather than replacement-only behavior. Online bed-in-a-box models continue to expand reach through risk-reversal trials and parcel logistics, while purpose-built student accommodation pipelines add steady institutional demand that anchors multi-year orders. State-level construction cycles shape local opportunities, with Western Australia’s eight-year high in completions adding fresh bedroom demand in line with greenfield growth corridors. Net overseas migration and interstate flows into Queensland and Western Australia reinforce these patterns, which keep the Australian mattress market closely linked to household formation in those states[1]https://www.abs.gov.au/statistics/people/population/national-state-and-territory-population/latest-release..

Key Report Takeaways

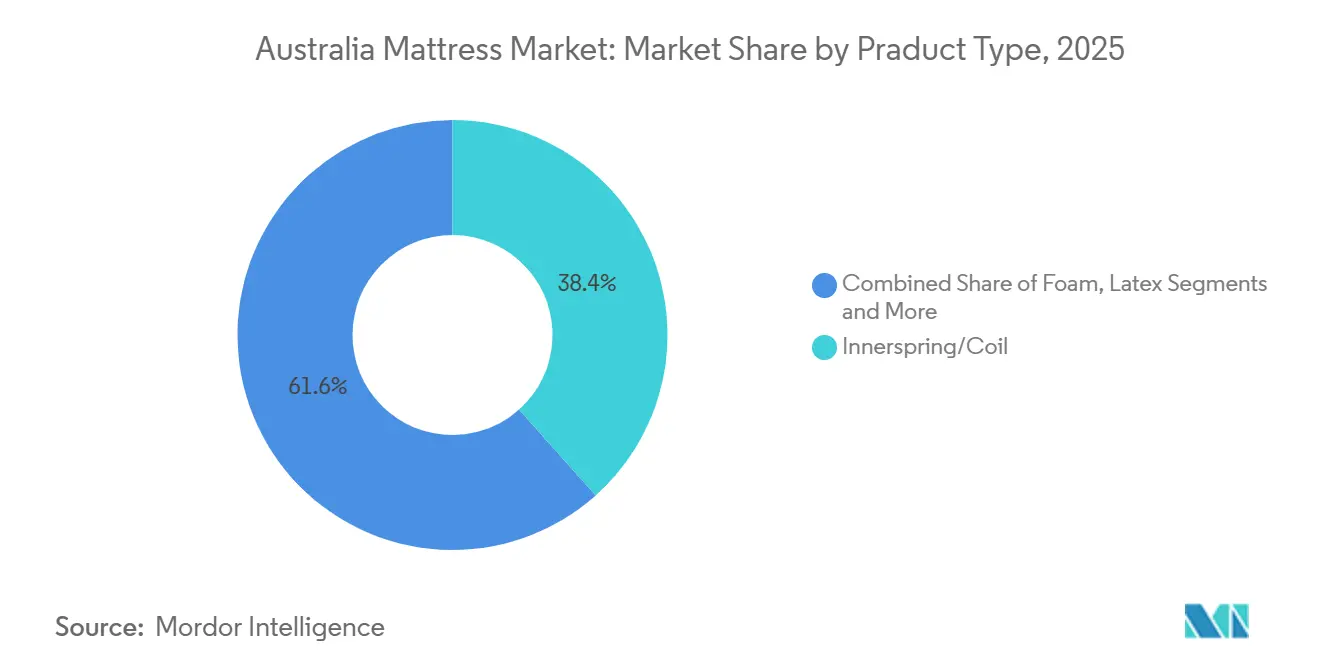

- By product type, innerspring/coil led with 38.4% of the Australia mattress market share in 2025, while hybrid designs are forecast to expand at a 5.92% CAGR through 2031.

- By mattress size, queen-size held 36.8% of the Australia mattress market share in 2025, and king-size is projected to grow at a 5.44% CAGR to 2031.

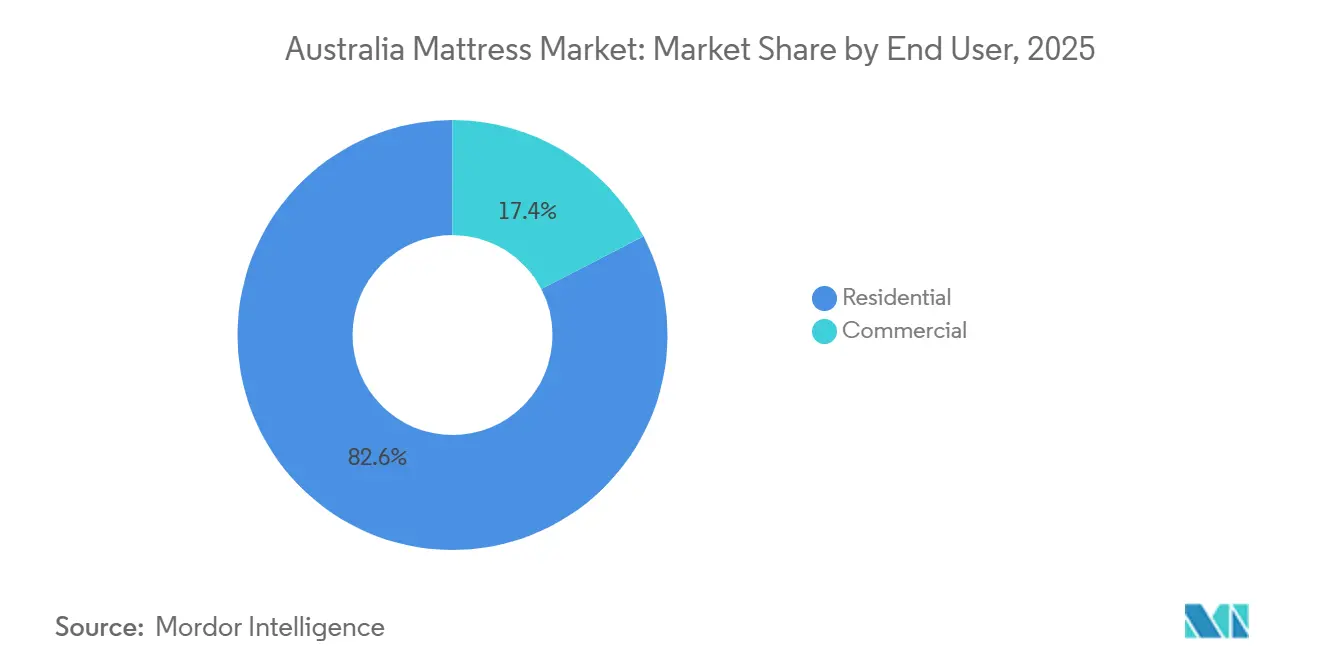

- By end user, residential accounted for 82.6% of the Australia mattress market share in 2025, while commercial is set to record a 4.48% CAGR through 2031.

- By distribution channel, B2C/retail held 88.9% of the Australia mattress market share in 2025, and online within B2C is expected to post a 6.35% CAGR to 2031.

- By geography, New South Wales accounted for 31.7% of the Australia mattress market share in 2025, while Queensland is the fastest-growing state at a projected 4.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing Formation and Replacement Cycles Intensify | +0.9% | National, with early gains in NSW, QLD, WA | Medium term (2-4 years) |

| Bed-In-A-Box Adoption Lifts Online Penetration | +1.2% | National, strongest in metro areas | Short term (≤ 2 years) |

| Population Growth and Interstate Migration Hotspots Elevate Bedroom Demand | +0.8% | Queensland, Western Australia, select regional corridors | Medium term (2-4 years) |

| Stewardship Scheme Scale-Up and Landfill Levies Accelerate Replacements | +0.3% | National, led by Victoria and the NSW council, mandates | Long term (≥ 4 years) |

| Institutional Procurement Shifts to Certified, Low-VOC, Recyclable Mattresses | +0.5% | BTR and PBSA clusters in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Sleep Health and Back Pain Awareness Prioritize Demand | +0.9% | National, strongest in metro areas with aging demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Housing Formation and Replacement Cycles Intensify

National supply underperformed underlying household formation in 2024 and 2025, as completions trailed the number of new dwellings implied by population growth, which maintained a structural shortfall. The National Housing Supply and Affordability Council reported 177,000 completions in 2024 and estimated annual demand for 223,000 dwellings, underscoring a persistent supply gap that feeds replacement and upgrade cycles within existing housing stock[2]https://geca.slantstaging.com.au/wp-content/uploads/2022/10/GECA-Standard-Guide-Furniture-Fittings-Foam-Mattresses.pdf. Net overseas migration added 305,600 people in the year to June 2025, which lifted bedroom demand and supported sales in corridors where new households form. As rooms in established homes are repurposed for flexible use, consumers favor larger formats and enhanced support systems for longevity, which aligns with the projected 5.44% CAGR for king-size mattresses to 2031. Western Australia demonstrates new-supply momentum, with 22,602 completions in fiscal 2024-25, up 25.1% year over year, adding to first-purchase demand alongside replacement cycles in undersupplied rental markets[3]. Vendors are aligning assortments around queen and king sizes in fast-growing corridors in Queensland and Western Australia, which reinforces a shift toward premium hybrids as households prioritize comfort and durability over entry price.

Bed-in-a-Box Adoption Lifts Online Penetration

The Australia mattress market benefits from bed-in-a-box adoption, which compresses freight and enables convenient delivery, and from in-home trials that shift evaluation from showrooms to bedrooms. Online penetration inside B2C is expected to remain the fastest-growing channel, with online sales within B2C projected to post a 6.35% CAGR through 2031, supported by risk-reversal propositions and standardized delivery workflows. The Australia Competition and Consumer Commission’s June 2025 enforcement against misleading strike-through prices in the category heightened attention to transparent promotions and truthful urgency claims across websites and apps. Brands now lean on verifiable material certifications and clear specification sheets to maintain consumer trust amid stronger compliance expectations, helping stabilize value as promotional intensity moderates[4]https://geca.slantstaging.com.au/wp-content/uploads/2022/10/GECA-Standard-Guide-Furniture-Fittings-Foam-Mattresses.pdf. Parcel-based compression and doorstep delivery remain core efficiencies, yet execution depends on disciplined returns handling and transparent trial disclosures that balance consumer experience with cost control. The Australia mattress market continues to blend direct-to-consumer convenience with selective showrooming by major retailers, which permits tactile testing while preserving online service advantages in delivery and returns.

Population Growth and Interstate Migration Hotspots Elevate Bedroom Demand

Australia’s population reached 27.61 million in June 2025, with annual growth of 420,100 driven by net overseas migration of 305,600, which sustains new household formation and bedroom demand[3]https://www.wa.gov.au/government/media-statements/Cook%20Labor%20Government/Western-Australian-housing-completions-continue-to-gather-pace-20251015. Queensland recorded net interstate migration gains of 21,595 over the period, while Western Australia gained 10,288, shifting a larger share of housing and furnishing purchases toward these states. This movement favors mattress purchases tied to first-time setups and relocations, which supports sustained volumes for the Australian mattress market even as overall growth remains measured. Western Australia’s elevated completions add to this effect by increasing first-purchase bedroom sets in newly delivered homes, while existing households continue to replace aging units under multi-occupant use. Queensland’s demographic profile combines a growing older cohort with steady family formation, which maintains interest in comfort-forward specifications and low-VOC materials for sensitive occupants. Developers and institutional buyers reference eco labels such as GECA and OEKO-TEX Standard 100 during fit-out procurement, which influences material and foam choices for mattresses sold into new residential supply.

Sleep Health and Back Pain Awareness Premiumizes Demand

In Australia, mattress purchases are increasingly being viewed as an investment in preventive health rather than simple commodity replacements. This shift is supported by clinical evidence that highlights the connection between sleep quality, chronic disease management, and productivity. Queensland’s aging population exemplifies this trend, with 17.2% of residents aged 65 and older in 2024, compared to 11.9% in 2004. This demographic shift has led to a higher prevalence of conditions such as osteoarthritis and degenerative disc disease, which are closely linked to aging. Addressing these issues, the Australian Physiotherapy Association emphasizes the benefits of medium-firm hybrid mattresses with zoned lumbar support. These mattresses have been shown to reduce morning stiffness by 30-40%, offering significant relief for individuals suffering from these conditions. As awareness grows regarding the role of sleep in overall health, consumers are increasingly prioritizing mattresses that cater to specific health needs. This trend reflects a broader understanding of the importance of quality sleep in managing chronic conditions and enhancing daily productivity. By investing in mattresses designed for optimal support and comfort, Australians are taking proactive steps toward improving their long-term health and well-being, particularly in regions like Queensland, where the aging population is steadily increasing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Opacity and Heavy Discounting Compress Average Selling Prices | -0.6% | National, most acute in online-first brands | Short term (≤ 2 years) |

| Reverse Logistics and Hygiene Rules Inflate Online Return Costs | -0.4% | National, disproportionate in rural and remote areas | Medium term (2-4 years) |

| Imported Components and Foam Chemical Price Volatility | -0.3% | National, affects foam and latex segments | Medium term (2-4 years) |

| Limited Mattress Recycling Throughput and Contamination Constraints | -0.2% | National infrastructure gaps in QLD and WA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Opacity and Heavy Discounting Compress Average Selling Prices

Opaque pricing practices in Australia mattress retail face stronger enforcement to reduce the use of artificial markdowns and countdown timers. In June 2025, the ACCC reported that Emma Sleep admitted to misleading sale price representations for dozens of products, triggering compliance reviews across the category and highlighting legal risks from perceived perpetual promotions. This shift is prompting brands to move toward simpler everyday pricing, recalibrate their discount cadence, and substantiate comparative claims. Clear communication, consistent price governance, and verifiable performance attributes now carry more weight in defending value in the Australia mattress market than reliance on high headline markdowns. Materials and safety certifications offer another route to sustain price realization by signaling quality and traceability across foam and textile inputs. Over time, this rebalancing is expected to support steadier margins while aligning promotional practices with consumer law, benefiting manufacturers and retailers that invest early in robust compliance systems.

Reverse Logistics and Hygiene Rules Inflate Online Return Costs

Generous trial policies create reverse logistics obligations that vendors must manage in line with hygiene and safety standards. Returned mattresses that show signs of use cannot be resold as new, so companies rely on donation or recycling programs, which require coordination and often yield little revenue. The Australia Bedding Stewardship Council reports wide national coverage for mattress recycling and continues to expand approved recycler capacity, strengthening take-back pathways for brands that prioritize sustainability in the Australia mattress market. Soft Landing, a leading recycler, dismantles mattresses at scale and notes that contamination can still divert some units to landfill, underscoring the need for careful collection and triage processes. These realities push online sellers to tighten return terms, clarify pickup eligibility, and forge partnerships with stewardship networks to control cost while meeting customer expectations. As online volumes rise, transparent and well-governed return workflows will operate as a competitive differentiator as much as a cost center across the Australia mattress market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Designs Engineer Market-Share Gains Through Measurable Ergonomic Superiority

Innerspring and coil mattresses commanded 38.4% of the Australia mattress market share in 2025, while hybrid designs are projected to grow at a 5.92% CAGR through 2031, which outpaces the broader Australia mattress market. The engineering behind leading hybrid centers focuses on higher coil counts and zoned support, which improve pressure relief and motion isolation compared with standard innersprings. Sleep Republic’s flagship hybrid features 2,500 individually wrapped pocket springs and a five-zone support system that goes beyond typical coil counts and zoning to deliver measurable ergonomic support. Foam-based options remain important in the Australia mattress market, yet buyers increasingly seek low-VOC assurances and recognized labels that verify input safety and emissions. Natural latex alternatives, such as Peace Lily’s latex and hybrid models, appeal to consumers who want renewable materials and long service lives under extended warranties.

Commercial procurement reinforces the hybrid trend, as operators value a balance of durability and comfort in multi-tenant properties. Student accommodation and large residential projects emphasize medium-firm hybrids with credible eco-labels to reduce complaints and align sustainability mandates in tenders, thereby improving lifecycle performance. The Australia mattress industry is adapting by embedding certifications into product roadmaps and by publishing specification sheets that simplify due diligence for institutional buyers. Tighter scrutiny of marketing claims further encourages vendors to promote demonstrable performance features over subjective comfort language, which supports sustained gains for hybrids with validated designs.

By Mattress Size: King-Size Growth Tracks Suburban Greenfield Sprawl and Work-From-Home Permanence

Queen-size beds held 36.8% of the Australia mattress market share in 2025, while king-size variants are forecast to grow at a 5.44% CAGR through 2031 as households invest in larger formats. Suburban greenfield development favors larger master suites, which support wider mattress adoption to reduce partner disturbance and improve comfort while preserving usable space for multi-purpose bedroom layouts. Western Australia’s eight-year high in dwelling completions illustrates how new housing supply creates first-purchase bedroom needs that often include larger master-suite layouts. Hybrid work arrangements also drive demand for spacious, comfortable bedroom setups, keeping interest in king-size configurations visible across metro and fast-growing regional markets in the Australia mattress market. Buyers who prioritize sleep quality often allocate more of the furnishing budget to the master bedroom than to guest rooms or occasional spaces, which favors upgrades to wider sizes.

Commercial specifications shape a different mix. Purpose-built student accommodation emphasizes single and king-single formats to maximize room counts, and planned PBSA additions through mid-decade sustain that requirement. Build-to-rent operators typically prefer queen sizes to optimize floor plans in one and two-bedroom units, which maintains healthy throughput for standard dimensions that fit most layouts in Australia’s major cities. The Australia mattress market continues to be segmented by household type and property format, with large families and downsizers alike using size upgrades to improve comfort and reduce partner disturbance. Retailers and brands support this shift by presenting clear size guides, firmness options, and compatibility notes for bases and frames to reduce returns and improve satisfaction.

By End User: Commercial Demand Accelerates as Build-to-Rent and Purpose-Built Student Accommodation Institutionalize Australia Rental Housing

Residential purchases accounted for 82.6% of unit volume in 2025, while commercial demand is expected to expand at a 4.48% CAGR through 2031 as institutional procurement grows. Commercial buyers in the Australia mattress market favor standardization by firmness and certification, which lowers complaint rates, streamlines maintenance, and supports ESG reporting. Purpose-built student accommodation brings consistent demand for single and king-single mattresses, and multi-year pipelines across key university cities underpin predictable order cycles. Procurement teams increasingly specify low-VOC foam and verified textile inputs to meet institutional sustainability commitments, guiding product design toward certified materials.

The Australia mattress industry also sees greater involvement from professional landlords and developers who value nationwide warranty service and consistent fulfillment standards. Vendors that can document performance through durability testing and zoned support designs win tenders that weigh lifecycle cost over initial price alone. Recycling and take-back partnerships with stewardship networks help projects address end-of-life obligations at scale, which increasingly appear in tender criteria and building certifications. These factors collectively support a shift toward medium-firm hybrids in commercial settings, where comfort, durability, and compliance carry equal weight in purchase decisions.

By Distribution Channel: Online Bed-in-a-Box Brands Disrupt Traditional Retail’s Negotiated-Discount Model but Face Return-Cost Headwinds

B2C and retail accounted for 88.9% of sales in 2025, and online within B2C is projected to post a 6.35% CAGR through 2031 as risk-reversal trials and parcel-based logistics improve access and convenience. This segment commanded the largest share of the Australia mattress market in 2025, and its online subsector continues to grow faster than store-led formats as retailers merge e-commerce with curated showrooms. Consumers benefit from clearer spec sheets, digital consultations, and selection tools that personalize fit across size and firmness, which helps offset the absence of extended in-store testing. Major retailers complement online service with broad assortments and pickup options that reduce delivery friction, supporting a hybrid experience that aligns with how Australians now research and buy sleep products.

The channel’s next phase centers on cost governance and compliance. Returns handling and hygiene protocols require disciplined operations and transparent trial terms that reflect real-world logistics across metropolitan and regional postcodes. Partnerships with stewardship networks are increasingly important to keep end-of-life material out of landfill and to meet public and private sustainability expectations. Pricing transparency enforcement also reshapes digital promotion calendars, encouraging consistent value presentation and reducing legal exposure for brands that sell direct to consumers. Taken together, these shifts make service reliability and compliance core differentiators in the Australia mattress market, alongside comfort and material innovation.

Geography Analysis

New South Wales accounted for a 31.7% share of the Australia mattress market size in 2025, reflecting Greater Sydney’s large population base and ongoing household formation. Metropolitan density and steady retrofit activity sustain replacement cycles across established suburbs, which keeps demand stable even as affordability pressures shape relocation decisions. Population trends and overseas arrivals in Sydney support continuous flows of first-time setups and upgrades, sustaining the category’s baseline. Retail networks in NSW also reflect the category’s premiumization, with broad availability of hybrids and certified materials that align with health and wellness preferences among urban buyers.

Queensland is forecast to be the fastest-growing state at a 4.62% CAGR through 2031, supported by strong net interstate gains and steady international arrivals. Net interstate migration of 21,595 into Queensland and sustained net overseas migration reinforce new household formation, which fuels bedroom setups across detached housing and medium-density formats. The state’s demographic profile includes an aging cohort alongside family formation, which sustains demand for comfort-focused specifications across queen and king sizes. PBSA pipelines anchored in Brisbane and the southeast carry consistent orders for single- and king-single mattresses, and procurement criteria increasingly include credible eco-labels that reduce complaints and align with institutional ESG goals.

Western Australia’s upswing in completions adds a second growth focal point in the Australia mattress market. The state delivered 22,602 dwellings in fiscal 2024-25, up 25.1% year over year, aligning first-time buyer demand with replacement cycles in undersupplied rental markets. Interstate inflows add to this momentum, expanding the addressable base for queen- and king-size beds tied to new master suites. Stewardship networks continue to expand their coverage of recyclers across states, supporting end-of-life management and helping lower barriers to replacement decisions in regional areas. Across other jurisdictions, ACT, South Australia, Tasmania, and the Northern Territory contribute a steady base demand shaped by public-sector employment, university populations, and modest new-build activity, with retailers aligning mix and certification choices to local buyer profiles in the Australia mattress market.

Competitive Landscape

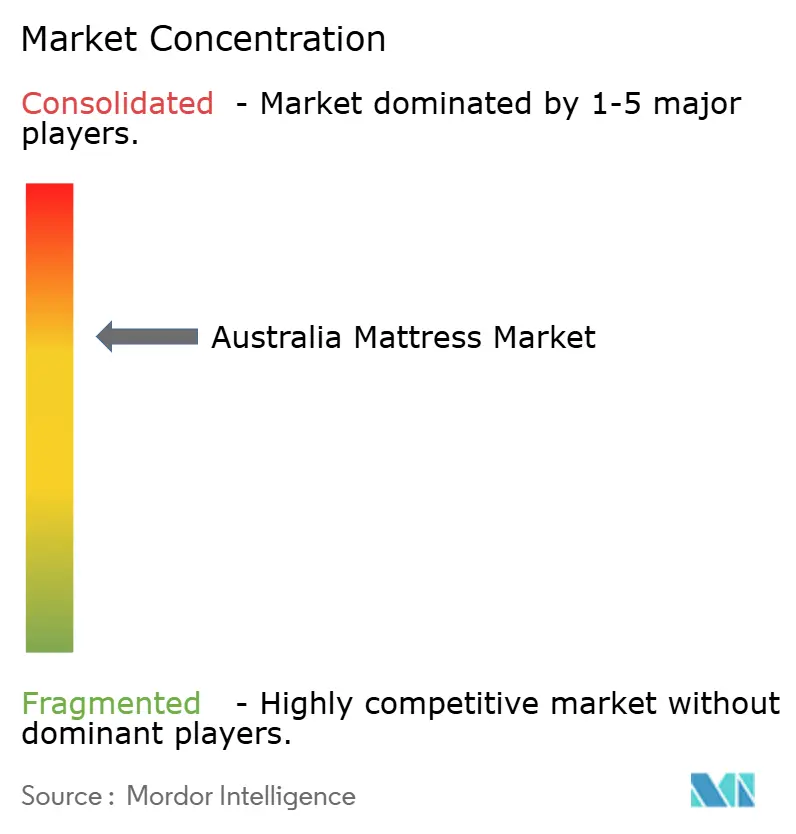

The Australia mattress market remains moderately concentrated around established brands that anchor large retail networks and licensed ranges, while direct-to-consumer entrants add fragmentation in urban channels. Pricing transparency enforcement has become a structural factor in strategy and communications, underscoring the importance of accurate promotions and verifiable claims across every channel. Brands are shifting investment toward certified materials, product testing, and customer experience improvements that preserve value and reduce costly returns, which supports stable share positions for companies that execute consistently. Institutional buyers favor vendors that can document performance and service at a national scale, which narrows consideration sets in tenders and strengthens incumbents with proven fulfillment.

Product engineering is an active battleground. Sleep Republic differentiates through 2,500 pocket springs and five-zone support, which gives it a clear positioning on measurable ergonomics and durability that resonates with buyers who want evidence-based comfort. Natural latex specialists such as Peace Lily address sustainability and longevity preferences, and extended warranties reinforce the total-cost-of-ownership message for customers who value material traceability. Major retailers deploy selection tools and curated assortments to counter one-size-fits-most claims from online-only brands, blending showroom testing with digital convenience to protect their share in the Australia mattress market. Certification frameworks, particularly GECA and comparable textile and foam standards, help vendors defend pricing and reduce returns related to emissions or material sensitivities.

Circular economic initiatives continue to expand, which supports a shift from disposal to stewardship in the category. The Australia Bedding Stewardship Council increases recycler participation and provides public guidance, simplifying take-back programs for brands and retailers. Soft Landing scales dismantling and processing nationwide, providing vendors with an ethical, often local outlet for returns that cannot be resold as new. Together, these platforms let companies codify end-of-life processes into customer journeys and tender responses, creating additional differentiation beyond comfort and price. The Australia mattress market, therefore, rewards firms that pair disciplined compliance and credible sustainability with engineered comfort, thereby stabilizing brand equity and deepening trust across consumer and institutional segments.

Australia Mattress Industry Leaders

Sealy of Australia

A.H. Beard

SleepMaker

Koala

Tempur Australia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Serta announced to expand its international footprint with a new licensing agreement with A.H. Beard for Australia and New Zealand. The partnership between the Serta Simmons Bedding brand and A.H. Beard, the 125-year-old, family-held mattress manufacturer based in Padstow, New South Wales, Australia,

- March 2025: Sealy Posturepedic Australia launched a multi-channel campaign for its Acclaim mattress, emphasizing "comfort fused with technology" through TV commercials, digital assets, and CGI animations showcasing React® Support, FlexCase™, and CoreSupport systems.

- February 2025: Tempur Sealy International completed its USD 5 billion acquisition of Mattress Firm, the largest mattress specialty retailer in the U.S., following a favorable U.S. District Judge ruling against the FTC's attempt to block the transaction.

- January 2025: Vispring opened its first flagship showroom in Melbourne, showcasing handcrafted premium natural-material beds priced from USD 5,361-20,104 (AUD 8,000-30,000), tapping ultra-high-net-worth demand in Toorak, South Yarra, and Brighton, where median dwelling values exceed USD 2.0 million (AUD 3 million), and buyers prioritize artisanal provenance over price optimization.

Australia Mattress Market Report Scope

The mattress is one of the most widely demanded products as people adopt urbanization. A complete background analysis of the Australia Mattress Market includes an assessment of the economy, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles covered in the report.

The Australia mattress market is segmented by type, distribution channel, and end-user. By type, the market is sub-segmented into spring mattresses, memory foam mattresses, latex mattresses, and other mattresses. By distribution channel, the market is sub-segmented into online and offline. by end-users, the market is sub-segmented into commercial and residential. The report offers the market sizes and forecasts for all the above segments in value (USD).

By Product Type

| Innerspring / Coil |

| Foam (including memory foam) |

| Latex |

| Hybrid |

| Other Mattress Types |

By Mattress Size

| Single-size Mattress |

| Double-size Mattress |

| Queen-size Mattress |

| King-size Mattress |

| Custom & Specialty Sizes |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B/Project |

By Geography

| New South Wales |

| Victoria |

| Queensland |

| Rest of Australia |

| By Product Type | Innerspring / Coil | |

| Foam (including memory foam) | ||

| Latex | ||

| Hybrid | ||

| Other Mattress Types | ||

| By Mattress Size | Single-size Mattress | |

| Double-size Mattress | ||

| Queen-size Mattress | ||

| King-size Mattress | ||

| Custom & Specialty Sizes | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | New South Wales | |

| Victoria | ||

| Queensland | ||

| Rest of Australia | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Australian mattress market?

The Australian mattress market size is USD 1.72 billion in 2025 and is projected to reach USD 2.12 billion by 2031 at a 3.56% CAGR (2026-2031).

Which product types are gaining the most traction in Australia?

Hybrids are growing fastest with a 5.92% CAGR through 2031, while innerspring and coil mattresses remain the largest by share.

Which state shows the fastest growth for mattress demand?

Queensland is the fastest-growing state with a projected 4.62% CAGR through 2031, supported by strong interstate migration.

How are online channels shaping purchasing behaviors in Australia?

Online within B2C is the fastest-growing route with a 6.35% CAGR, driven by bed-in-a-box models, clear specs, and risk-reversal trials.

What certifications matter most to institutional buyers in Australia?

Commonly referenced eco-labels include GECA and comparable foam and textile standards, which help meet ESG and low-VOC expectations in tenders.

Page last updated on: