Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.11 Billion |

| Market Size (2026) | USD 18.77 Billion |

| Market Size (2031) | USD 22.41 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

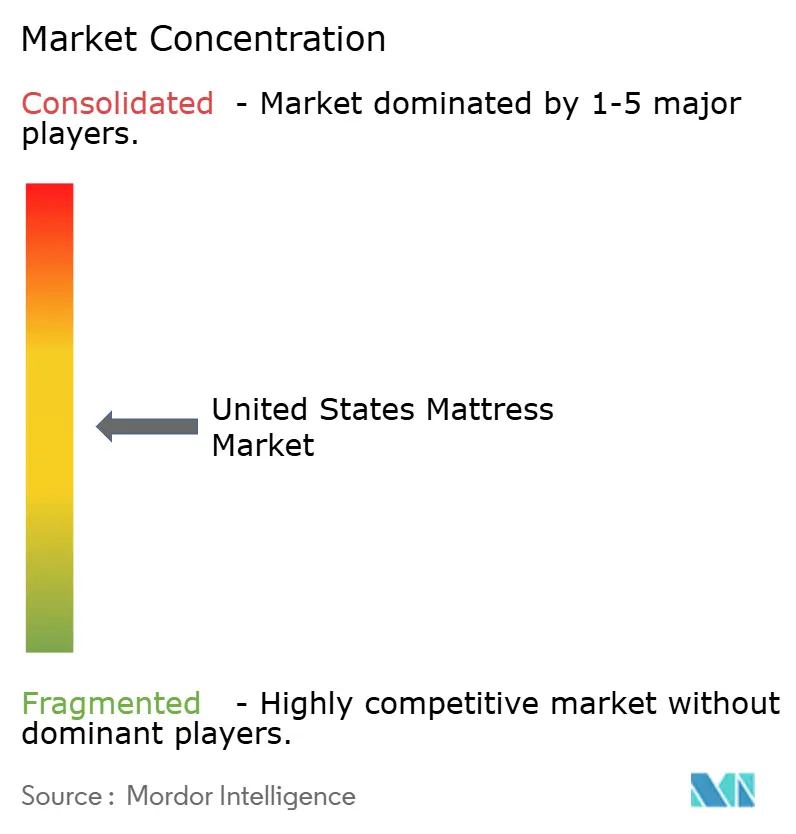

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Mattress Market Analysis by Mordor Intelligence

The United States Mattress Market size is expected to grow from USD 18.11 billion in 2025 to USD 18.77 billion in 2026 and is forecast to reach USD 22.41 billion by 2031 at 3.62% CAGR over 2026-2031.

Demand now hinges more on replacement cycles, housing construction, and technology-focused sleep upgrades than on first-time purchases. Wellness-centric positioning, smart features, and on-shore manufacturing investments are redefining competitive advantages across the United States mattress market, while consolidation and federal scrutiny temper unchecked expansion. Elevated input costs and stringent disposal regulations pose near-term headwinds, but demographic shifts and product innovation sustain a steady medium-term outlook for the US mattress market.

Key Report Takeaways

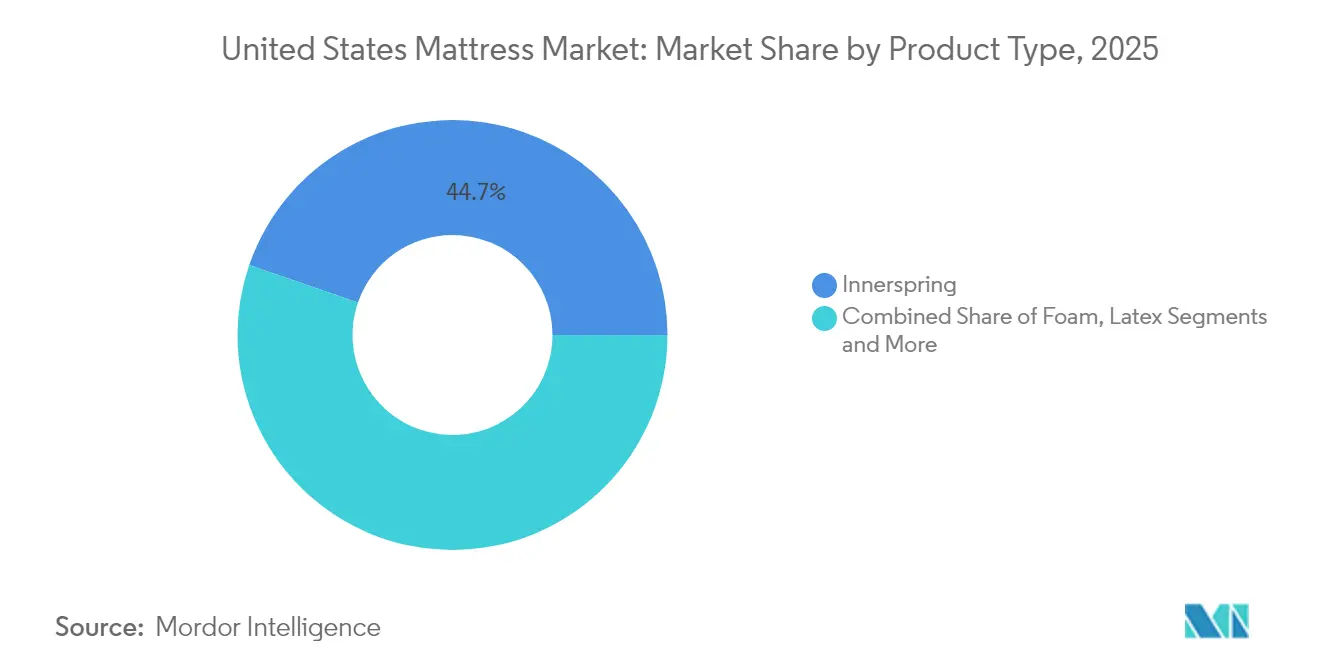

- By product type, innerspring held the lead with 44.72% of the United States mattress market share in 2025, while foam, including memory foam, is projected to expand at a 4.30% CAGR through 2031.

- By mattress size, queen models commanded 44.65% of the United States mattress market size in 2025 and are set to grow at a 3.74% CAGR to 2031.

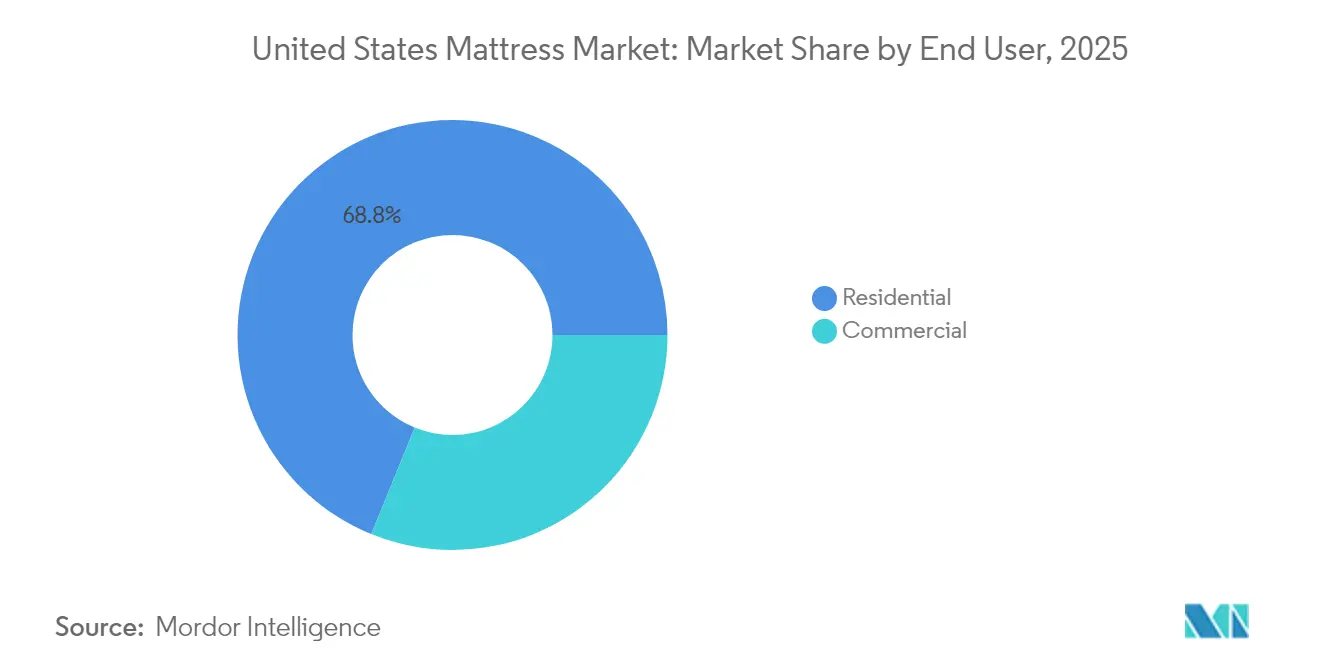

- By end user, the residential segment accounted for 68.84% of the US mattress market size in 2025 and is forecast to advance at a 3.88% CAGR through 2031.

- By distribution channel, B2C retail, including online and specialty stores, captured 64.58% of the US mattress market share in 2025 and is on track for a 3.96% CAGR growth to 2031.

- By geography, the Southeast led with 23.42% of the USA mattress market share in 2025, while the West region recorded the fastest 4.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising housing starts & home-furnishing spend | +0.8% | National, with concentration in Southeast and West | Medium term (2-4 years) |

| Rapid proliferation of "bed-in-a-box" D2C model | +0.6% | National, strongest in urban Northeast and West Coast | Short term (≤ 2 years) |

| Growing incidence of back-pain driving premium mattress demand | +0.5% | National, higher adoption in affluent Northeast and West | Long term (≥ 4 years) |

| Product innovation in memory-foam & hybrid constructions | +0.4% | National, with premium segment concentration in Northeast | Medium term (2-4 years) |

| Anti-dumping duties boosting on-shore production | +0.3% | National, manufacturing concentration in Southeast and Midwest | Long term (≥ 4 years) |

| Integration of sleep-data platforms with wellness insurers | +0.2% | National, early adoption in tech-forward West Coast markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Housing Starts & Home-Furnishing Spend

Single-family housing starts are projected at 1.01 million units in 2025[1]Source: National Association of Home Builders, “Housing Forecast 2025,” nahb.org. New homeowners typically replace mattresses within 18 months, creating a reliable volume pipeline for the United States mattress market. Remodeling outlays are increasing 5% annually, further lifting premium replacement demand. Equity gains correlate with a higher willingness to upgrade to smart or hybrid models rather than standard innerspring units. Consumer confidence surveys show 71% of potential buyers are ready to pay mortgage premiums above prevailing rents, signaling sustained furnishing expenditure. These dynamics particularly favor the memory-foam and hybrid sub-segments that promise better pressure relief and climate control.

Rapid Proliferation of “Bed-in-a-Box” D2C Model

Direct-to-consumer brands have rewritten distribution economics by collapsing supply chains and eliminating showroom overheads. Online interest in mattress buying rose from 27% in 2016 to 47% in 2020. An average online ticket of USD 303 on Amazon contrasts sharply with USD 1,194 in traditional stores, demonstrating margin reallocation rather than compression. Free 365-night trials and expedited white-glove delivery have neutralized tactile-testing barriers. Established manufacturers such as Serta Simmons launched dedicated online-only lines in 2025, underlining the D2C playbook’s endurance. Regional fulfillment centers now achieve two-day delivery across most metropolitan ZIP codes, meeting consumer immediacy expectations.

Growing Incidence of Back-Pain Driving Premium Mattress Demand

Chronic back-pain prevalence and a population with a median age surpassing 39 years are pushing older cohorts toward orthopedic features. Sleep Number’s 360® smart series generated USD 732.4 million, 36.7% of its 2024 revenue, at an average sell-out price of USD 2,700, more than double the market median. HSAs and FSAs now reimburse medically justified sleep products, effectively subsidizing premium purchases[2]Source: Internal Revenue Service, “HSA/FSA Eligible Medical Expenses,” irs.gov. Pressure-mapping tools offer objective firmness recommendations, replacing subjective showroom trials. Insurers piloting sleep-data integrations report reduced musculoskeletal claims, reinforcing willingness to reimburse connected beds. These factors expand high-margin slices of the United States mattress market.

Product Innovation in Memory-Foam & Hybrid Constructions

Gel-infused foams and phase-change covers mitigate historic heat-retention complaints without sacrificing contouring comfort. Hybrid designs marry pocketed coils with adaptive foams for optimal edge support plus pressure relief. At CES 2024, DeRUCCI’s T11 Pro Smart Mattress introduced AI-driven respiratory monitoring, foreshadowing the next wave of sleep tech. BASF’s new chemical-recycling loop for polyurethane curtails landfill waste and slashes virgin feedstock reliance, aligning with state recycling mandates[3]Source: BASF, “Circular Polyurethane Solutions,” basf.com. IoT sensors facilitating automatic firmness adjustments underline convergence between bedding and health analytics ecosystems. The integration of IoT sensors for sleep tracking and automatic firmness adjustment represents the convergence of traditional bedding with health technology platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material (foam & steel) price volatility | -0.7% | National, manufacturing concentration in Southeast and Midwest | Short term (≤ 2 years) |

| Market saturation & longer replacement cycles | -0.5% | National, most pronounced in mature Northeast markets | Long term (≥ 4 years) |

| FTC scrutiny of Tempur-Sealy/Mattress Firm deal | -0.3% | National, with focus on competitive retail markets | Medium term (2-4 years) |

| Stricter disposal rules for polyurethane foam | -0.2% | Regional, implemented in California, Connecticut, Oregon, Rhode Island | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material (Foam & Steel) Price Volatility

Supply chain disruptions have created unprecedented cost pressures, with foam prices increasing 50% and steel coil materials experiencing similar inflation, while container shipping costs surged from USD 3,400 to over USD 10,000 per container. Steel coil costs traced a similar trajectory. Successive price increases throughout 2024 kept revenue stable but risked demand elasticity. Producers with diversified domestic suppliers mitigated shocks, unlike smaller firms reliant on spot imports. Tariffs on Canadian and Mexican steel, plus residual levies on Chinese foam, further pressure cost structures. Margin compression is likely to linger until commodity indices normalize. Companies with diversified supply chains and domestic sourcing capabilities gain competitive advantages, while smaller manufacturers face existential pressures from sustained input cost inflation.

Market Saturation & Longer Replacement Cycles

Improved durability extends ownership from 7 years to as long as 10 years, limiting unit velocity. Industry shipments slipped 22% from 2021-2023. Population aging and decelerating household formation mean fewer first-time buyers. Congressional Budget Office models show annual housing starts sliding to 0.78 million by 2044-2053[4]Source: Congressional Budget Office, “Long-Term Housing Outlook,” cbo.gov. Higher average selling prices partly offset slower volumes, but true expansion depends on unlocking wellness features that justify mid-cycle upgrades. Premium segment growth partially offsets unit decline through higher average selling prices, but total addressable market expansion faces mathematical limits in mature regions. Delayed purchase patterns observed in 2024 suggest pent-up demand could provide temporary relief in 2025, though underlying replacement cycle extension represents a permanent structural shift requiring industry adaptation strategies focused on value-added services rather than volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Innerspring Resilience Amid Innovation

Innerspring mattresses held 44.72% of the United States mattress market share in 2025, underscoring the value placed on edge support and bounce among older buyers. Foam products, especially memory foam, are projected to grow at a 4.30% CAGR through 2031, the highest within the US mattress market. Hybrid adaptations combining coils and advanced foams are narrowing the performance gap, encouraging incumbents to pivot portfolios. Latex maintains a premium niche, appealing to eco-conscious consumers with natural material preferences.

Aging demographics still gravitate toward firmer feel and easier ingress, sustaining core innerspring demand. Conversely, newly formed households—often in smaller urban dwellings opt for roll-packed foam units that simplify delivery. Smart variants overwhelmingly use foam cores because embedded sensors and actuators integrate more readily into homogeneous material structures. Consequently, manufacturers segment marketing, traditional support for legacy buyers, cooling foams and sleep-tracking hybrids for tech-savvy cohorts, maximizing cross-selling. Foam segment leadership in growth rates indicates successful resolution of historical heat retention issues through gel infusion and phase-change materials, while innerspring manufacturers increasingly adopt hybrid approaches to maintain relevance in evolving market dynamics.

By Mattress Size: Queen Dominance Reflects Housing Trends

Queen-size captured 44.65% of the United States mattress market in 2025 and is forecast to expand at a 3.74% CAGR, the fastest among all sizes. Urban condos and suburban master bedrooms are routinely designed around queen dimensions, reinforcing default demand. King sizes command prestige positioning in luxury housing, while twin and full serve youth and hospitality turnover channels. Custom and specialty sizes cater to niche applications, including RV markets, adjustable bed frames, and therapeutic requirements, though volumes remain limited compared to standard configurations.

Smart launches typically roll out in queen formats first, leveraging the highest installed base for network effects. The universality of queen sizing simplifies supply-chain SKUs and marketing spend. Even as replacement cycles lengthen, queen refresh volumes remain resilient because married and cohabiting couples prioritize comfort upgrades earlier than single sleepers in smaller beds. The size category's stability suggests limited disruption potential from alternative configurations, with growth driven primarily by replacement cycles and new household formation rather than consumer switching between size preferences.

By End User: Residential Wellness Focus Drives Growth

Residential buyers represented 68.84% of the USA mattress market size in 2025 and are advancing at a 3.88% CAGR. Remote and hybrid work increases time spent at home, turning sleep environments into productivity assets. HSAs and FSAs now reimburse medically indicated sleep solutions, effectively subsidizing premium models. Commercial segments—hospitality, healthcare, student housing- demand robust durability and flame compliance, but grow at a slower clip due to capital-budget cycles. Commercial applications serve hospitality, healthcare, and institutional markets with different performance requirements emphasizing durability, infection control, and standardized comfort levels rather than personalization features prioritized by residential consumers.

Smart innovation remains a residential story in the USA mattress market: adjustable lumbar zones, temperature regulation, and partner-specific firmness settings cater to individualized comfort. Commercial properties, in contrast, prioritize price, uniformity, and warranty simplicity. Nonetheless, healthcare facilities begin piloting pressure-relief hybrid models to reduce patient ulcer incidence, signaling niche medical adoption. Commercial segment growth remains constrained by standardized procurement processes and cost-focused purchasing decisions, though healthcare applications increasingly recognize therapeutic benefits of advanced mattress technologies for patient outcomes and recovery acceleration.

By Distribution Channel: Retail Evolution Toward Experience

B2C retail dominated the US mattress market with a 64.58% share in 2025, propelled by omnichannel convergence. Brick-and-mortar specialty chains merge in-store trials with virtual configuration tools, while online platforms extend 365-night returns. Amazon commands 20%-unit volume, leveraging same-day Prime delivery in dense metros. Traditional furniture stores lose footing, prompting co-location with mattress galleries to recapture foot traffic. Other distribution channels, including furniture stores and department stores, serve complementary roles, though their market share continues declining as consumers gravitate toward specialized mattress retailers and online platforms.

Retailers invest in interactive showrooms using VR posture mapping and sensor-based pressure visualization, converting exploration into higher ASPs. Direct-to-consumer startups continue scaling warehouse-showroom hybrids for last-mile efficiency. B2B channels trail because bulk purchasers negotiate longer contracts and procure via project tenders rather than transactional buys. The distribution landscape increasingly favors omnichannel approaches, where consumers research online but complete purchases through preferred channels, requiring manufacturers to maintain consistent pricing and product availability across multiple touchpoints.

Geography Analysis

The Southeast’s 23.42% share anchors its leadership within the United States mattress market. Factory expansions by Palmetto Pedic and Malouf shorten supply chains and align with anti-dumping relief. Younger demographics and retiree migrations alike support first-time and replacement purchases, sustaining volume stability despite elongated cycles. Climate-responsive textiles, cooling gels and moisture-wicking top layers, resonate with humid conditions, spurring specialized SKUs. Climate considerations drive regional preferences toward cooling technologies and moisture-wicking materials that address high humidity conditions prevalent throughout the Southeast.

The West will outpace national CAGR at 4.07% through 2031. Technology workforce expansion in California and Washington correlates with higher discretionary spend on connected sleep systems. Eight Sleep’s dynamic thermal management beds find particularly strong traction here, as quantified-self culture permeates consumer habits. Elevated real-estate costs limit bedroom sizes, prompting prioritization of premium quality over furniture quantity. California's implementation of PFAS regulations for mattresses establishes precedent for environmental standards that may influence national product development priorities.

Northeast states show low-single-digit growth, but high ASPs in the US mattress market. Older housing stock and colder winters heighten interest in thermal-retentive foams and dual-zone heating layers. Urban fulfillment constraints champion bed-in-a-box logistics; elevator-friendly roll formats simplify high-rise deliveries. The Midwest multiples its role as both buyer and logistical hub, benefitting from central geographic shipping lanes. The Southwest mirrors Sun Belt migration patterns, yet water scarcity pushes builders toward smaller footprints, indirectly reinforcing queen-size preference. Regional preferences increasingly reflect climate adaptation, with cooling technologies gaining traction in warmer markets and thermal regulation features appealing to temperature-variable regions, suggesting opportunities for geographic product specialization strategies.

Competitive Landscape

Completion of the Tempur Sealy–Mattress Firm merger in February 2025 created Somnigroup International, marrying the largest U.S. manufacturer with the largest specialty retailer. Post-deal market share exceeds 32%, but divestitures and consent decrees cap potential dominance. Sleep Number commands the premium adjustable-air niche and holds 36.7% of its revenue in connected products, leveraging 800+ patents. Casper, Purple and Nectar pursue scale through D2C storytelling and omnichannel pop-ups. The competitive landscape increasingly favors companies with omnichannel capabilities and vertical integration advantages, as evidenced by Mattress Warehouse's expansion plans targeting 650 stores by 2027 and Ashley Home's acquisition of Resident Home (Nectar, DreamCloud brands) to combine retail strength with e-commerce expertise.

Material innovators occupy fertile white space. BASF’s circular polyurethane program and DeRUCCI’s AI mattresses exemplify R&D pathways beyond price competition. Retailers such as Mattress Warehouse plan to reach 650 stores by 2027 while integrating e-commerce APIs for localized inventory. Strategic moves include Ashley Home acquiring Resident Home to blend physical and online strength. Competitive intensity hinges on technology integration, cost control and regulatory reflexes. Technology adoption patterns suggest that companies successfully integrating sleep data platforms with wellness insurance coverage will capture premium market segments, while traditional manufacturers face pressure to innovate beyond commodity product offerings or risk margin compression from low-cost imports and D2C competition.

United States Mattress Industry Leaders

Tempur Sealy International

Serta Simmons Bedding

Sleep Number Corp.

Purple Innovation

Resident (Nectar)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Tempur Sealy completed its USD 5 billion acquisition of Mattress Firm, forming Somnigroup International and divesting 176 stores to satisfy FTC conditions.

- February 2025: Malouf relocated all mattress manufacturing to the United States, citing anti-dumping incentives and supply-chain agility.

- January 2025: E.S. Kluft debuted Aireloom hybrid lines at Winter Las Vegas Market, expanding luxury offerings.

- January 2025: South Bay unveiled three new mattress collections at Las Vegas Market, targeting mid-tier growth.

United States Mattress Market Report Scope

A mattress is a soft rectangular pad large enough to support a person lying on it. It is used as a bed or as part of the bed frame. The United States mattress market is segmented by type, size, end user, and distribution. The market by type is further segmented into innerspring, memory foam, latex, and other types. The market by size is segmented into single-size, double-size, queen-size, and king-size mattresses. The market by the end-user is segmented into residential and commercial. The market by distribution channel is divided into offline (specialty stores, multi-brand stores, others) and online. For all the above segments, the market size regarding value (USD) during the forecast period is provided.

By Product Type

| Innerspring / Coil |

| Foam (including memory foam) |

| Latex |

| Hybrid |

| Other Mattress Types |

By Mattress Size

| Single-size Mattress |

| Double-size Mattress |

| Queen-size Mattress |

| King-size Mattress |

| Custom & Specialty Sizes |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B/Project |

By Geography

| Northeast |

| Midwest |

| Southeast |

| Southwest |

| West |

| By Product Type | Innerspring / Coil | |

| Foam (including memory foam) | ||

| Latex | ||

| Hybrid | ||

| Other Mattress Types | ||

| By Mattress Size | Single-size Mattress | |

| Double-size Mattress | ||

| Queen-size Mattress | ||

| King-size Mattress | ||

| Custom & Specialty Sizes | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | Northeast | |

| Midwest | ||

| Southeast | ||

| Southwest | ||

| West | ||

Key Questions Answered in the Report

How large is the United States mattress market in 2026?

The United States mattress market size totals USD 18.77 billion in 2026.

What is the projected CAGR for U.S. mattress sales through 2031?

Revenue is on track to grow at a 3.62% CAGR between 2026 and 2031.

Which segment is growing fastest within U.S. mattress sales?

Foam, including memory-foam, posts the highest 4.30% CAGR through 2031.

Which U.S. region shows the strongest mattress demand growth?

The West region leads with a 4.07% CAGR thanks to tech-driven incomes and smart-bed adoption.

Page last updated on: