Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.09 Billion |

| Market Size (2026) | USD 5.24 Billion |

| Market Size (2031) | USD 6.08 Billion |

| Growth Rate (2026 - 2031) | 3.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Mattress Market Analysis by Mordor Intelligence

Japan Mattress Market size in 2026 is estimated at USD 5.24 billion, growing from 2025 value of USD 5.09 billion with 2031 projections showing USD 6.08 billion, growing at 3.02% CAGR over 2026-2031.

This steady expansion rests on Japan’s demographic reality as the world’s first super-aged society, the premiumization of sleep products, and the widening corporate view that restorative rest underpins workforce productivity. An aging cohort exceeding 29% of the population is pushing demand for pressure-relief technologies, while e-commerce adoption enables data-rich, customized buying journeys that once required in-store trials. Large-scale hotel upgrades tied to the Osaka-Kansai Expo 2025 add a parallel commercial demand wave that supplements household replacement cycles[1]Source: Statistics Bureau, “Current Population Estimates as of October 1, 2024,” STAT.GO.JP. . Currency weakness has lifted imported latex costs, yet legacy brands wield resilient supply networks that cushion margin pressure. Stringent recycling rules elevate disposal fees, lengthening replacement cycles but also driving design shifts toward modular, recyclable builds. Collectively, these drivers and frictions anchor a predictable yet opportunity-rich trajectory for the Japan mattress market.

Key Report Takeaways

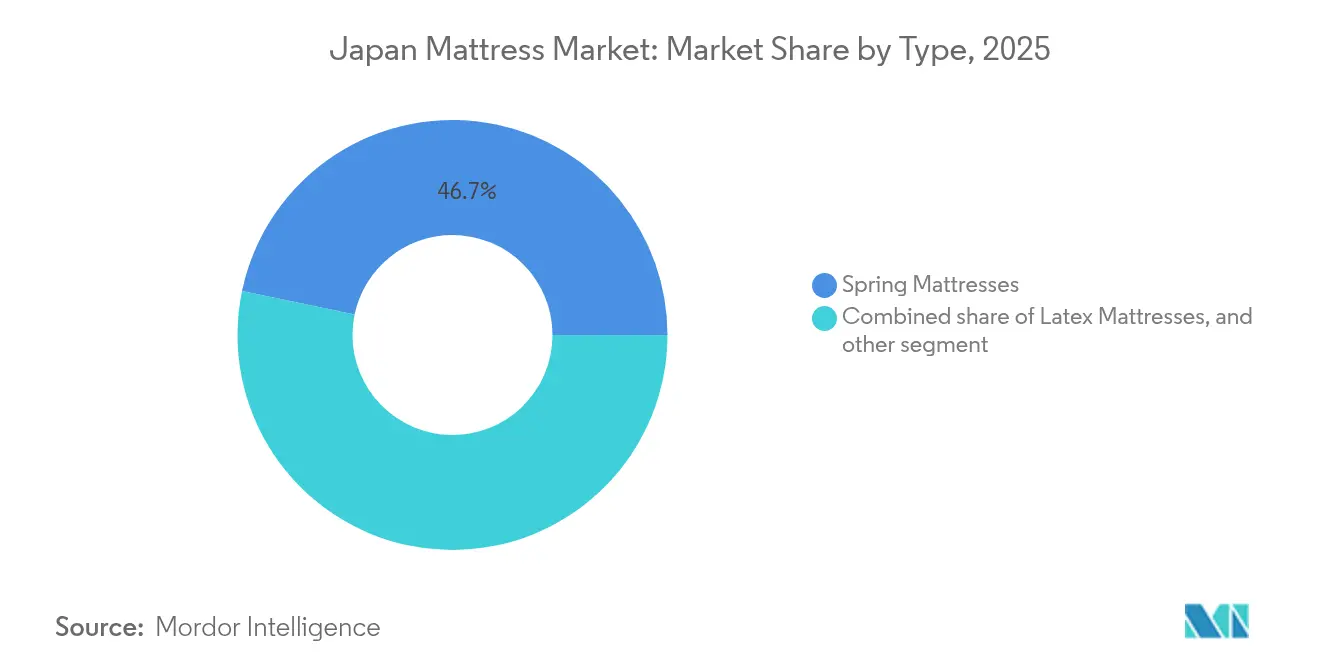

- By type, spring mattresses led with 46.72% of Japan mattress market share in 2025, while memory foam is advancing at an 7.72% CAGR to 2031.

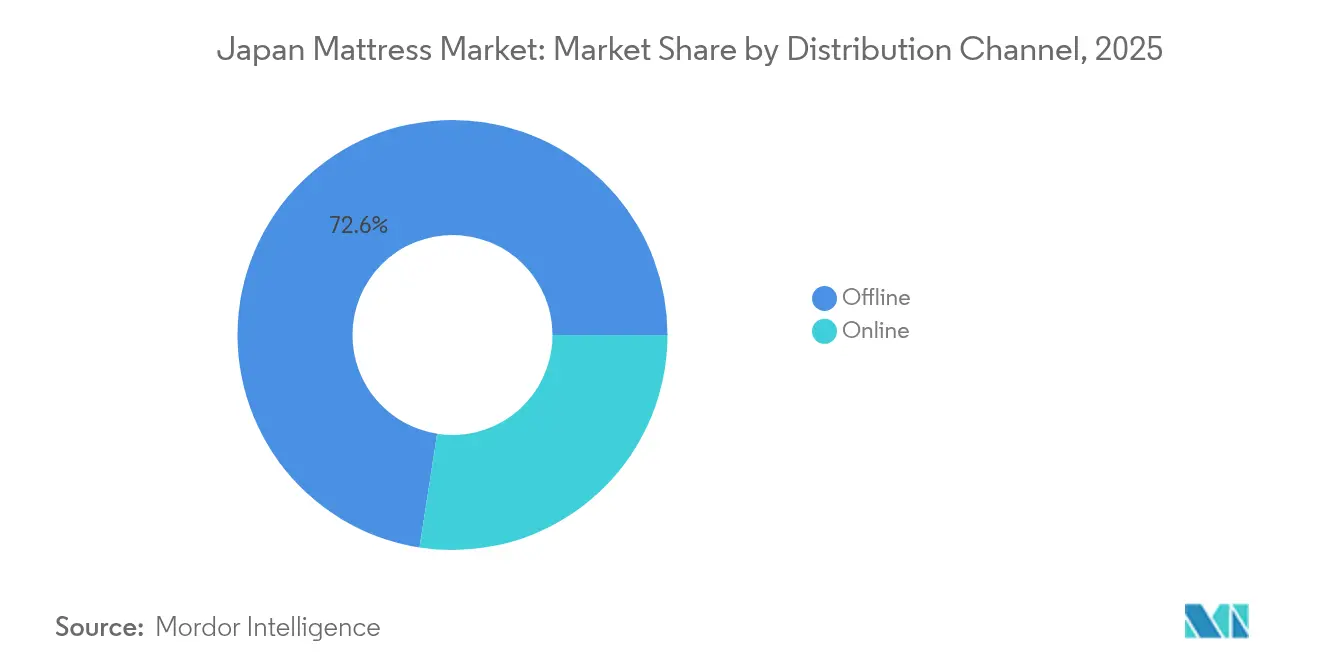

- By distribution channel, offline accounted for 72.55% of the Japan mattress market size in 2025, whereas online is the fastest-growing route at 11.85% CAGR through 2031.

- By end user, residential applications held 81.10% share of Japan mattress market size in 2025, and the commercial segment is projected to expand at 6.94% CAGR between 2026-2031.

- By region, Kanto commanded 35.95% of Japan's mattress market share in 2025, while Kyushu & Okinawa show the highest forecast CAGR at 6.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated aging population demanding pressure-relief bedding | +1.0% | National, rural prefectures | Long term (≥ 4 years) |

| Rising e-commerce penetration in furniture & interiors | +0.8% | Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| Hotel refurbishment boom ahead of Osaka–Kansai Expo 2025 | +0.4% | Kansai, Chubu, Chugoku | Short term (≤ 2 years) |

| Corporate sleep-health programs boosting bulk procurement | +0.3% | Major business districts | Medium term (2-4 years) |

| AI-enabled 3D body-scanning retail experience | +0.2% | Urban centers | Medium term (2-4 years) |

| Surging inbound tourism fostering futon-to-mattress conversions | +0.3% | Tourist destinations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Aging Population Demanding Pressure-Relief Bedding

Japan’s baby-boomer wave is crossing age 75, lifting the elderly population to nearly 22 million and intensifying needs for medical-grade pressure relief. Health expenditures are projected to reach JPY 89 trillion (USD 605.4 billion) by 2040, and policymakers view restorative sleep as a preventive-care lever[2]Source: Shotaro Kinoshita, “Updating the Japanese Healthcare System,” JMA.JP.. Insurers such as Sompo incorporate AI sensors in senior facilities, turning sleep data into actionable care insights. Mattress makers now bundle geriatric ergonomics with smart monitoring to migrate purchases from discretionary to health-essential budgets. Firms that certify products under Japan’s emerging medical-device guidelines gain priority in reimbursements, tightening links between bedding and healthcare. The demographic surge, therefore, transforms product messaging from comfort to clinically validated support, widening the premium ceiling.

Rising E-Commerce Penetration in Furniture & Interiors

Japan’s BtoC online sales hit JPY 24.8 trillion (USD 168.7 billion) in 2024, posting 9.23% growth and lifting furniture’s digital share by 25% year over year[3]Source: Ministry of Economy, Trade and Industry, “FY 2023 E-Commerce Market Survey,” METI.GO.JP. . AI-driven 3D visualization now lets shoppers virtually test firmness, and 51% of users plan repeat usage, proving that virtual showrooms can close sensory gaps. Direct-to-consumer entrants bypass store markups, apply dynamic pricing, and funnel savings into R&D on cooling foams and odor-resistant covers. The digital channel favors memory-foam and hybrid categories because their value proposition rests on spec sheets rather than tactile trial. Logistics partners refine vacuum-roll packaging that fits narrow elevators, solving a decisive last-mile hurdle in dense Japanese cities. As same-day delivery expands outside megacities, online conversion rates climb, moving the Japan mattress market from showroom-centric to algorithm-guided.

Corporate Sleep-Health Programs Boosting Bulk Procurement

Japanese employees average only 6 hours 22 minutes of sleep on work nights, a figure companies now treat as a productivity gap. Programs combining wearables and nutrition aim to lift cognitive output, and bulk mattress upgrades form the hardware backbone. Since 2022 the ZAKONE corporate community has grown to 240 member firms advocating sleep-first HR policies[4]Source: Meikippu Co., “3D Silhouette Real Purchase Experience,” PRTIMES.JP. . Enterprises bargain for standardized SKUs that simplify facility-wide replacement and support five-year depreciation schedules. Suppliers responding with dashboard analytics on aggregated sleep scores create a feedback loop that ties mattress specs to KPIs. This B2B path circumvents retail margins and stabilizes revenue through multi-year contracts, reshaping channel economics inside the Japan mattress market.

AI-Enabled 3D Body-Scanning Retail Experience Driving Premium Upgrades

Showa Nishikawa’s 3D Body Fitting System maps posture, converts it to sleep posture data, and recommends optimal firmness within minutes. The tech has spread from Tokyo flagships to regional stores, bringing personalized fitting to consumers who usually rely on floor samples. Retailers report conversion rates rising 30% for shoppers who complete scans, with average selling prices increasing because recommended SKUs skew premium. Online platforms mirror this by inviting users to upload body metrics for algorithmic sizing. As accuracy improves, return rates decline, mitigating a historical barrier to online mattress sales. Brands offering scan-based warranties lock customers into their ecosystem, creating recurring revenue for toppers and accessories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High real-estate costs limiting bedroom size & king-size demand | -0.6% | Tokyo, Osaka | Long term (≥ 4 years) |

| Price-sensitive senior segment delaying replacement cycles | -0.4% | Rural prefectures | Medium term (2-4 years) |

| High import duties raising premium mattress prices | -0.5% | Nationwide | Medium term (2–4 years) |

| Declining average household size reducing multi-bed purchases | -0.3% | Urban centers (e.g., Tokyo, Yokohama) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Real-Estate Costs Limiting Bedroom Size & King-Size Demand

The average Japanese home size has shrunk to 92 square meters, a 30-year low that restricts space for large beds. Micro-apartments dominate new urban builds, compelling residents to choose semi-double mattresses or foldable futons. Hotels, facing identical space economics, specify slimmer profile mattresses to free walking clearance, muting ASP growth. Brands answer with rollable cores and modular layering, yet profit margins thin because compact units use less material. Retail floor sets increasingly feature storage-bed hybrids that trade height for under-bed drawers, altering design priorities. Space scarcity, therefore, imposes a structural ceiling on premium expansion even as per-unit technology costs climb.

Price-Sensitive Senior Segment Delaying Replacement Cycles

Seniors on fixed pensions face yen-driven inflation that raised household costs by JPY 90,000 (USD 612.24) in 2024. Disposal fees under the Home Appliance Recycling Law further discourage frequent mattress renewals. Resulting cycles stretch beyond 10 years, limiting unit sell-through despite the rising headcount of older consumers. Manufacturers pursue durability claims and reversible designs to reassure budget-focused buyers, but prolonged lifecycles slow revenue velocity. Subscription-based rental models target care homes yet remain nascent. Unless pension reforms lift disposable income, upgrade prompts will hinge on medical prescriptions rather than lifestyle aspirations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Memory Foam Disrupts Traditional Spring Dominance

Spring mattresses maintained 46.72% share of Japan mattress market size in 2025 on the back of cultural leaning toward firm support. Memory foam, posting an 7.72% CAGR, benefits from pressure-relief attributes that cater to the aging demographic and corporate wellness programs that prioritize spine alignment. Latex continues as a niche, challenged by import-cost hikes amid yen volatility but defended by environmental appeal to eco-conscious households. Hybrid and air-fiber designs sit in the “other” bucket and ride a health-performance narrative popular among athletes, further diversifying consumer options. Showa Nishikawa’s AI-driven fitting showcases how technology underpins foam’s ascent by de-risking comfort uncertainty, while spring remains resilient in value-oriented segments and multi-generational homes that equate firmness with longevity.

Upgrades in hospital beds and senior facilities lean toward viscoelastic layers, embedding memory foam deeper into healthcare procurement streams. Spring makers innovate with zoned coils that mimic foam contouring without sacrificing bounce, but they face rising steel costs that compress margins. Retail merchandising now groups products by “sleep outcome” rather than material, subtly steering shoppers toward foam for pain relief narratives. Durability studies published by domestic testing institutes debunk early sag myths, boosting consumer confidence in foam. This shift in perception solidifies foam’s role as a credible alternative and positions it to capture incremental gains as ergonomic literacy spreads.

By Distribution Channel: Digital Transformation Accelerates Despite Offline Dominance

Offline distribution channel captured 72.55% of Japan mattress market share in 2025 because tactile assessment still resonates with local purchasing culture. Yet online channels are accelerating at a 11.85% CAGR as pandemic-era digital fluency meets AI-enabled visualization that narrows the sensory deficit. Furniture chains pivot to “phygital” models, allowing shoppers to book store visits after completing online pre-fits, thereby shortening in-store dwell time and upselling add-ons through app reminders. Pure-play e-tailers package mattresses in high-density rolls that comply with condominium delivery protocols, unlocking urban penetration at lower fulfilment cost. Influencer-led live commerce spotlights unboxing ease, countering discomfort over self-assembly and driving impulse purchases in younger cohorts.

Corporate procurement increasingly transacts via secure portals where HR and facility managers download spec sheets, upload floor plans, and receive fleet-wide price quotes within hours. This digitized workflow trims cycle times and reduces the need for regional distributor layers, pressuring traditional wholesale margins. Compliance integrations that auto-populate recycling certificates help online sellers meet legal disclosures, enhancing transparency. As product databases gain meta-tags for stiffness, heat dissipation, and rebound rate, search algorithms push curated bundles, nudging average order values upward. These converging elements accelerate the channel pivot even as showroom culture endures among older shoppers.

By End User: Commercial Segment Emerges as Growth Engine

Residential buyers drove 81.10% of Japan mattress market size in 2025, guided by replacement triggers and lifestyle upgrades. The commercial user base, however, is set to grow fastest at 6.94% CAGR, buoyed by hotel refurbishments and enterprise wellness schemes. Hospitality operators upgrading ahead of Expo 2025 demand standardized SKUs that meet global fire and hygiene codes, fostering volume deals favoring coil-on-coil and pocket spring variants known for durability. Hospitals and elderly-care centers increasingly specify alternating-pressure surfaces within therapeutic mattresses, blending medical compliance with comfort. Corporate dormitories incorporate mid-range hybrids that balance edge stability with storage-bed compatibility, reflecting space constraints yet prioritizing employee rest.

Commercial product lifecycles adhere to tighter replacement schedules due to branding and safety audits, lifting unit velocity relative to households. Service offerings such as on-site sanitation and replacement rentals diversify revenue streams for manufacturers aiming to secure recurring income. Regulatory oversight is stringent in healthcare environments, obliging suppliers to maintain documentation on antimicrobial fabrics and formaldehyde emissions. Compliance-ready firms thus enjoy reduced bid friction, capturing share in public procurement rosters. Events such as Expo 2025 create proof-of-concept showcases that ripple through regional hotel chains, sustaining momentum beyond the event window.

Geography Analysis

Japan’s mattress demand pulses through its economic geography in three tiers. The Kanto megalopolis leads with 35.95% in absolute sales owing to corporate density, affluent households, and early adoption of sleep-health benefits. However, real-estate compression pushes shoppers toward slimmer profiles, moderating ASP growth despite premium features. Kansai’s hotel refurbishment spree injects a near-term boom, raising commercial share and spotlighting expo-related procurement consortia that negotiate volume discounts with domestic brands. Kyushu & Okinawa outpace all regions in CAGR with 6.55% terms as tourism-driven lodging expands and local governments subsidize accommodation upgrades to stimulate regional economies. Northern regions witness demand stabilization, with specialty eco-tourism lodges sustaining a modest pipeline, while local aging accelerates pressure-relief mattress uptake.

Urban centers across all regions show higher penetration of AI-based body-scan retail tools, translating to faster migration toward memory foam and hybrid formats. E-commerce adoption correlates with broadband coverage, granting suburban Chubu districts unexpected growth pockets that close the digital gap with metropolises. Corporate wellness roll-outs follow headquarters footprints, explaining Kanto’s disproportionate share of B2B orders. Conversely, rural prefectures pivot toward budget lines under fixed-income pressure, reinforcing regional SKU segmentation based on affordability. Finally, regional waste-management ordinances compel manufacturers to tailor end-of-life logistics, with stricter prefectures driving earlier product redesign toward modular recyclability.

Competitive Landscape

The Japan mattress market shows moderate concentration, with the top manufacturers holding holding a significant portion of overall revenue in 2024. Long-established domestic players like Nishikawa Co. and France Bed Holdings rely on their century-old brand heritage and extensive retail networks across the country. Meanwhile, Tempur Sealy Japan has positioned itself in the premium memory foam segment, using experiential flagship stores and hotel collaborations to highlight its expertise in pressure-relief technology. Direct-to-consumer insurgents such as Koala Sleep Japan exploit agile supply chains, social-influencer marketing, and 120-night trial policies to undercut legacy pricing. Competitive vectors have shifted from coil count wars toward data-backed sleep outcomes, with companies integrating IoT sensors, analytics dashboards, and subscription maintenance.

Firms incapable of certifying under recycling directives face margin erosion from disposal levies, nudging the field toward eco-design competition. Import cost volatility pushes multinational brands to localize production, reinforcing domestic supply chains and hedging currency swings. Consolidation chatter intensifies as mid-tier manufacturers explore mergers to fund R&D on smart mattresses, although antitrust regulators maintain vigilance to guard consumer choice. Overall, strategic emphasis on health positioning, sustainability, and digital personalization underpins competitive narratives more than raw material or price wars.

Japan Mattress Industry Leaders

Nishikawa Co., Ltd.

France Bed Holdings Co., Ltd.

Nitori Holdings Co., Ltd.

Airweave Inc.

Tempur Sealy Japan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Taiwan’s Sleepy Tofu opens its first permanent Japanese store, Sleepy Tofu House, in Minami Aoyama in May 2025, offering immersive, home-like comfort retail experiences.

- March 2025: Nellify, Japan’s premier luxury mattress brand, debuts in the U.S., offering unmatched comfort with high coil count craftsmanship, featuring a 365-night trial and presale discount.

Japan Mattress Market Report Scope

A mattress is a large, usually rectangular pad for supporting a lying person. It is designed to be used as a bed or on a bed frame as part of a bed. The mattress is one of the most widely demanded products as people are adopting urbanization.

The Japan mattress market is segmented by type, distribution channel, and end-user. By type, the market is sub-segmented into spring mattresses, memory foam mattresses, latex mattresses, and other mattresses. By distribution channel, the market is sub-segmented into online and offline. By end-user, the market is sub-segmented intocommercial and residential. The report offers the market sizes and forecasts for all the above segments in value (USD).

By Type

| Spring Mattresses |

| Memory Foam Mattresses |

| Latex Mattresses |

| Other Mattresses |

By Distribution Channel

| Online |

| Offline |

By End User

| Residential |

| Commercial |

By Region

| Hokkaido |

| Tohoku |

| Kanto |

| Chubu |

| Kansai |

| Chugoku |

| Shikoku |

| Kyushu & Okinawa |

| By Type | Spring Mattresses |

| Memory Foam Mattresses | |

| Latex Mattresses | |

| Other Mattresses | |

| By Distribution Channel | Online |

| Offline | |

| By End User | Residential |

| Commercial | |

| By Region | Hokkaido |

| Tohoku | |

| Kanto | |

| Chubu | |

| Kansai | |

| Chugoku | |

| Shikoku | |

| Kyushu & Okinawa |

Key Questions Answered in the Report

What is the projected value of the Japan mattress market in 2031?

The market is forecast to reach USD 6.08 billion by 2031, expanding from USD 5.24 billion in 2026 and growing from USD 5.09 billion in 2025 at a 3.02% CAGR.

Which mattress type is growing fastest in Japan?

Memory foam is advancing at an 7.72% CAGR between 2026-2031 due to its pressure-relief characteristics suited to an aging population.

Why are online mattress sales accelerating in Japan?

AI-powered 3D visualization, streamlined delivery of vacuum-rolled units, and direct-to-consumer pricing are driving a 11.85% CAGR in online channels.

How will Expo 2025 influence mattress demand?

Hotel refurbishments tied to Expo 2025 in Osaka are triggering bulk procurement of premium mattresses, temporarily boosting commercial segment growth.

Page last updated on: