Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

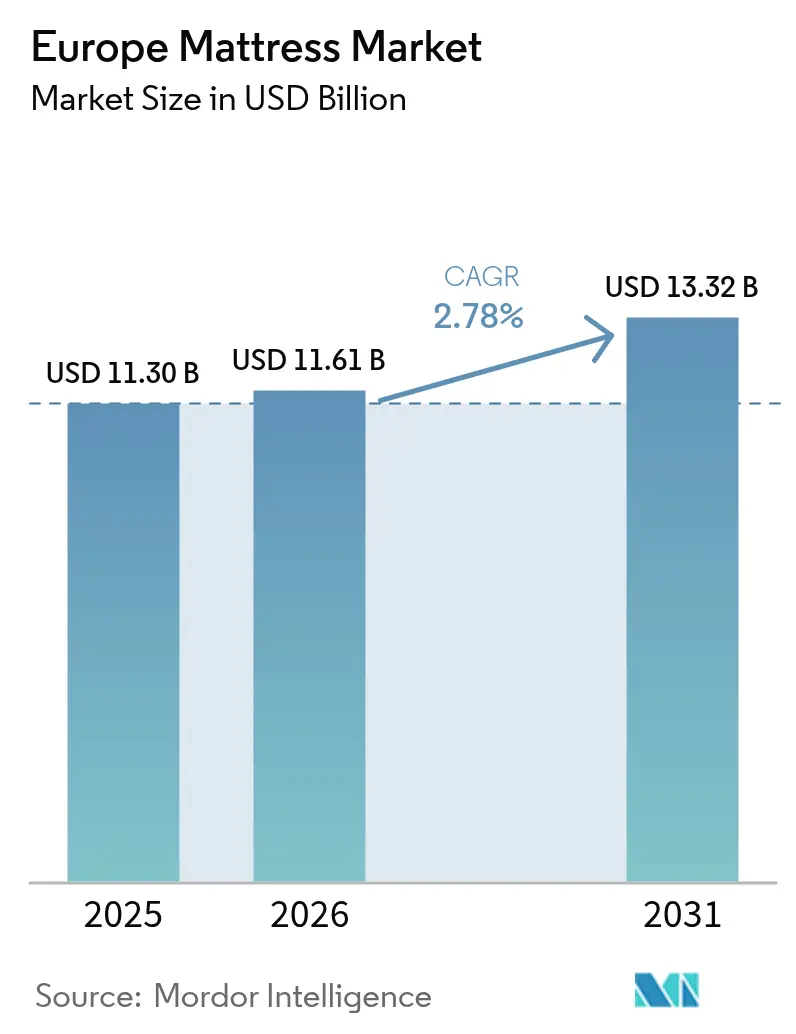

| Base Year Market Size (2025) | USD 11.30 Billion |

| Market Size (2026) | USD 11.61 Billion |

| Market Size (2031) | USD 13.32 Billion |

| Growth Rate (2026 - 2031) | 2.78% CAGR |

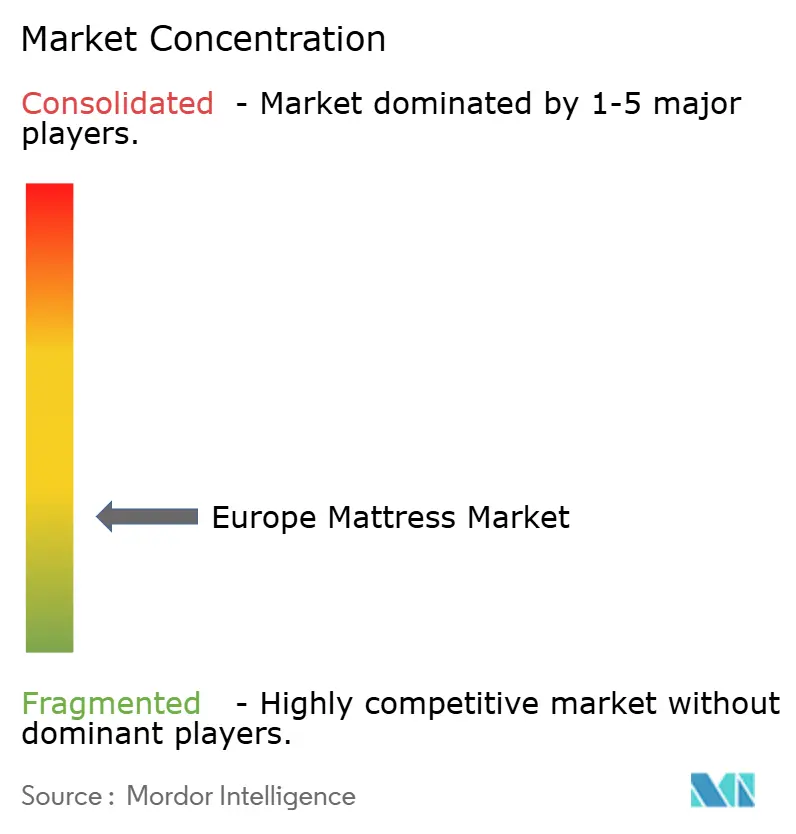

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mattress Market Analysis by Mordor Intelligence

Europe mattress market size in 2026 is estimated at USD 11.61 billion, growing from 2025 value of USD 11.30 billion with 2031 projections showing USD 13.32 billion, growing at 2.78% CAGR over 2026-2031. Moderate yet consistent expansion is underpinned by premiumization, demographic aging, stringent circular-economy rules, and the rapid maturation of online direct-to-consumer (D2C) channels. Mature household penetration in Western Europe is steering growth toward replacement demand, value-added features, and smart sleep technologies. Regulatory levers, including the Ecodesign for Sustainable Products Regulation (ESPR) and Extended Producer Responsibility (EPR) frameworks, are reshaping product development and end-of-life strategies. Competitive intensity is rising as incumbents embrace omnichannel models while digital-native challengers scale across borders. Opportunities cluster around orthopaedic innovations, hospitality refurbishment cycles, and circular business models that cut costs and satisfy tightening environmental mandates.

Key Report Takeaways

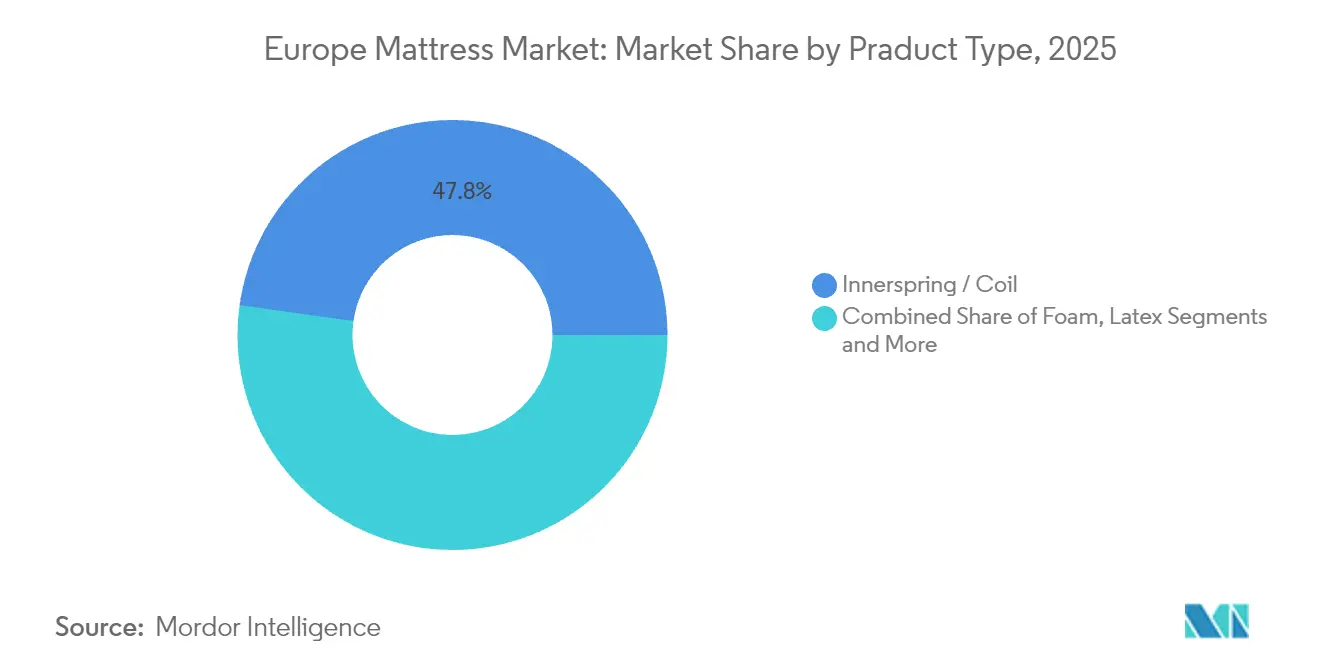

- By product type, innerspring/coil designs generated 47.78% of Europe mattress market share in 2025; hybrid mattresses are projected to post the fastest 4.22% CAGR through 2031.

- By size, queen-size accounted for 34.71% of the Europe mattress market size in 2025, whereas king-size is forecast to expand at 3.52% CAGR to 2031.

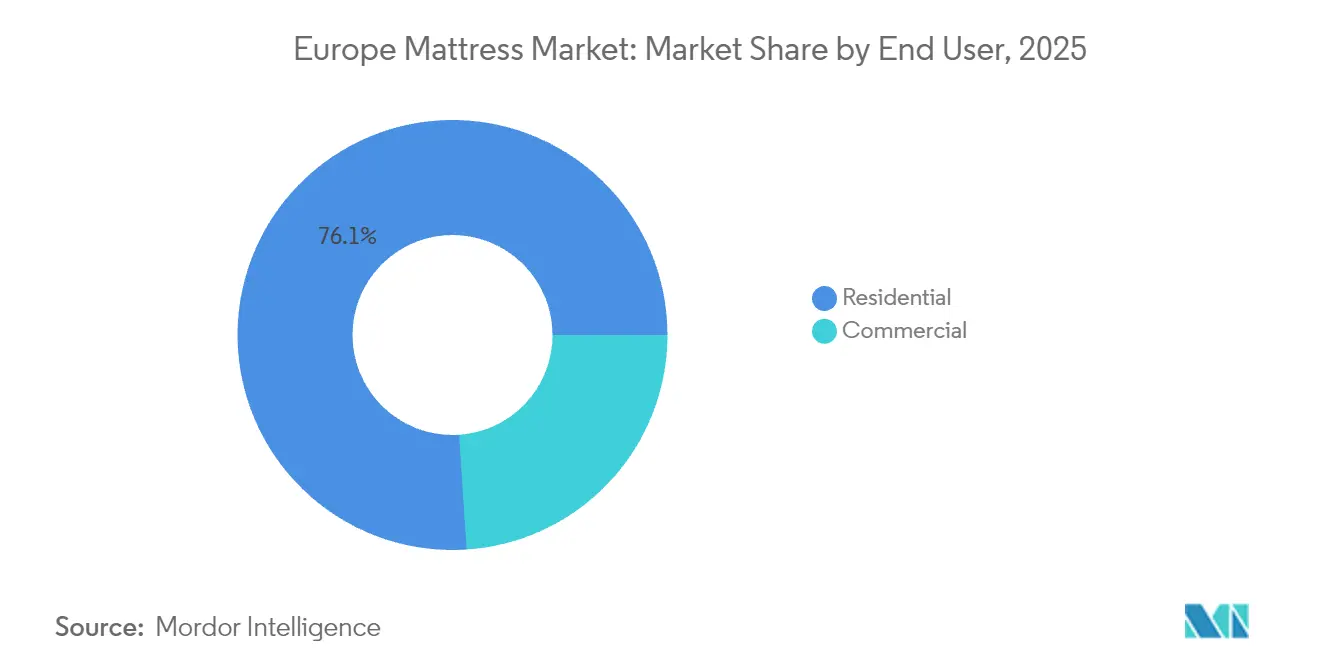

- By end user, residential customers held 76.05% revenue share in 2025, while commercial procurement is expected to advance at a 3.98% CAGR through 2031.

- By Distribution Channel, B2C/Retail held 70.88% revenue share in 2025, while B2C/Retail is expected to grow at a 3.86% CAGR through 2031.

- By geography, Germany led with 17.96% sales in 2025; Spain is predicted to record the highest 4.48% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for premium & luxury mattresses | +0.7% | Western Europe, Nordics, BENELUX | Medium term (2-4 years) |

| Rapid shift toward online D2C “bed-in-a-box” sales | +0.6% | UK, Germany, France, Spain | Short term (≤ 2 years) |

| Ageing population spurring orthopaedic & therapeutic need | +0.8% | Italy, Portugal, Germany, Nordics | Long term (≥ 4 years) |

| Hospitality refurbishment cycles driving bulk replacement | +0.5% | Southern Europe, UK, DACH | Short term (≤ 2 years) |

| EU circular-economy rules accelerating recyclable designs | +0.4% | EU-wide | Medium term (2-4 years) |

| Emergence of European smart-sleep tech integration | +0.2% | Western Europe, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Premium & Luxury Mattresses

Affluent households and boutique hospitality chains continue to trade up, favoring advanced materials, certified sustainability, and tailored ergonomics[1]Source: European Bedding Industries’ Association, “Annual Report 2025,” ebia.eu. Segment resilience is reinforced by wellness-centric consumer mindsets, with traceable supply chains and carbon-neutral labeling becoming table stakes. Manufacturers are vertically integrating to secure premium foam grades and artisanal upholstery, locking in margins and raising entry barriers. Retailers are curating experiential showrooms where in-store diagnostics match sleepers with bespoke builds. As premium penetration deepens, late-cycle demand shifts from mass propositions to differentiated wellness narratives.

Rapid Shift Toward Online D2C “Bed-in-a-Box” Sales

Digital-first disruptors lowered purchase friction through free trials, compressed packaging, and border-agnostic logistics. Pandemic-era adoption has endured, with omnichannel hybrids emerging—Emma’s flagship in London demonstrates that physical storefronts amplify digital funnels. Cost-effective last-mile networks and algorithmic personalization sharpen competitive edges, yet the General Product Safety Regulation (GPSR) amplifies compliance overheads for web-only sellers[2]Source: European Commission, “General Product Safety Regulation (EU) 2023/988,” single-market-economy.ec.europa.eu. Data-rich feedback loops accelerate product iteration cycles, allowing D2C brands to refresh line-ups quarterly, far faster than traditional catalog rotations.

Ageing Population Spurring Orthopaedic & Therapeutic Products

EU residents aged 65+ formed 21.6% of the population in 2024 and will expand steadily, concentrating in Italy, Portugal, and Germany. Clinical guidelines emphasize zoned support and pressure redistribution, lifting orthopaedic mattress uptake across home-care and assisted-living channels. Hospital purchasing consortia are embedding stringent evidence-based specifications that favor products validated by sleep-science research. Long-term care operators add antimicrobial fabrics and moisture management to mitigate infection risks. These factors secure durable demand even as broader household replacement cycles lengthen. The European Bedding Industries' Association (EBIA) is actively shaping standards in this space, ensuring that new products meet evolving clinical and consumer needs.

Hospitality Refurbishment Cycles Driving Bulk Replacement

Tourism rebound and brand repositioning spur capital expenditure in Southern Europe, the UK, and DACH, translating into multi-property mattress tenders every 7-10 years. ESG metrics now sit alongside comfort criteria; as a result, suppliers offering low-VOC foams, recyclability guarantees, and smart sleep analytics win preferred-vendor status. Co-development of proprietary models for flagship hotels cements longer contracts and co-marketing rights. Suppliers, however, must navigate project delays tied to macroeconomic swings or regulatory approvals, necessitating agile manufacturing slots and buffer inventory. Strategic partnerships between mattress manufacturers and hospitality groups are becoming more common, enabling co-development of bespoke solutions and joint marketing initiatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market saturation in Western Europe curbing first-time sales | -0.5% | Western Europe | Medium term (2-4 years) |

| Volatile polyurethane & latex prices squeezing margins | -0.4% | EU-wide | Short term (≤ 2 years) |

| Upcoming EPR fees raising end-of-life costs | -0.3% | EU-wide | Medium term (2-4 years) |

| Carbon-border tariffs inflating input costs | -0.2% | EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Market Saturation in Western Europe Curbing First-Time Sales

Household mattress ownership approaches 1.07 units per dwelling in Germany, France, and the Netherlands, trimming headroom for new transactions. Growth pivots to premium upgrades, smart add-ons, and subscription replacements that smooth cash outlays. Small regional makers face consolidation pressure as retail real estate rationalizes. The shift intensifies competition for share-of-wallet against adjacent wellness products such as adjustable bases and sleep trackers. Brands, therefore, refine loyalty programs and recycling to lock in repeat purchase cycles.

Volatile Polyurethane & Latex Prices Squeezing Manufacturer Margins

Flexible polyurethane foam spot prices swung by 23% between Q2’24 and Q1’25, driven by geopolitics and energy costs, while natural latex remains exposed to currency swings and climate impacts in Southeast Asia[3]Source: EUROPUR, “Flexible PU Foam Market Trends 2025,” europur.org. Mattress makers hedge with multi-year supply contracts, diversify toward recycled or bio-based foams, and re-engineer bill-of-materials for lower density ratings. ESPR-mandated material disclosures add administrative expense but incentivize innovation in circular feedstocks. Coupled with EPR fees that fund end-of-life programs, input volatility continues to compress gross margins until scale efficiencies offset cost spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Designs Drive Next-Gen Demand

Hybrid models are the fastest risers, advancing at a 4.22% CAGR from 2026-2031, buoyed by the fusion of coil responsiveness with foam contouring. Hybrid share gains leverage young households’ desire for balanced comfort and hotter sleepers’ need for airflow. In the commercial sphere, hotels adopt hybrids to heighten guest reviews while meeting durability benchmarks. The Europe mattress market size for hybrids is expected to reach USD 4.45 billion by 2031, equivalent to 33.10% of category revenue. Sensor-enabled hybrids capable of sleep-stage reporting, temperature modulation, and maintenance alerts further distinguish premium tiers, strengthening brand lock-in.

Foam and latex remain vital niche categories. Viscoelastic foam supports healthcare pressure-relief applications, whereas natural latex attracts eco-conscious buyers. Innerspring/coil formats preserve a 47.78% share, underlining the residual demand for budget comfort and firm feel preferences. Regulatory emphasis on recyclability accelerates coil-foam separable constructions, reducing disassembly labor and diverting tonnage from landfill. The segment's success is increasingly dependent on manufacturers' ability to balance performance, sustainability, and cost-effectiveness while meeting evolving regulatory requirements.

By Mattress Size: King-Size Gains on Queen-Size Leadership

Queen-size holds the lion’s 34.71% share, aligning with standard European bed frames and hospitality bedding protocols. However, king-size growth accelerates to 3.52% CAGR as rising disposable incomes and larger dwelling footprints in the Nordics and Germany accommodate upsizing. The Europe mattress market size for king-size units will exceed USD 3.34 billion by 2031, supported by couples seeking enhanced personal space and luxury hoteliers upgrading suites. Logistics hurdles—bulkier freight and higher last-mile costs—are countered through vacuum-roll compression and white-glove delivery.

Single and double formats cater to student housing, first apartments, and elder-care facilities, preserving volume albeit at lower average selling prices. Custom lengths for healthcare bariatric beds and super-king options in ultra-luxury resorts introduce SKUs that challenge operational complexity yet deliver margin uplift. The growth in king-size demand is also driving innovation in adjustable bases and smart bedroom ecosystems, as consumers seek integrated sleep solutions. Market players are investing in flexible manufacturing capabilities that can efficiently produce multiple size categories while maintaining quality consistency across their product portfolios.

By End User: Commercial Segment Outpaces Residential Dominance

Residential channels still command 76.05% of 2025 demand, but commercial procurement—hotel, healthcare, student housing, and senior living—will expand at 3.98% CAGR. Group tenders frequently bundle mattresses with adjustable bases, toppers, and occupancy-sensor software, lifting deal values. Compliance protocols covering fire safety, hygiene, and circularity raise specification sophistication, benefiting suppliers with testing labs and accredited documentation. Commercial buyers sign multi-year maintenance and recycling agreements, anchoring recurring revenue even as initial volumes fluctuate.

Retailers adjust merchandising to spotlight commercial-grade SKUs for consumer purchase, capitalizing on rising interest in hospitality-level comfort at home. Meanwhile, growth in private medical clinics and assisted living builds in Spain and Italy injects incremental demand for therapeutic and pressure-care variants. The integration of IoT sensors and fleet management systems is emerging in premium commercial applications, enabling proactive maintenance and performance monitoring. Manufacturers are developing specialized sales teams and technical support capabilities to serve the unique needs of commercial buyers, including site surveys, installation services, and ongoing maintenance programs.

By Distribution Channel: B2C/Retail Channels Remain Growth Engine

Omnichannel strategies keep B2C at a 70.88% revenue share, with a 3.86% CAGR through 2031. Online D2C remains the discovery gateway; nonetheless, conversion improves when tactile trialing and instant pickup options are available. Specialty mattress boutiques highlight diagnostics pods, AI mattress fitters, and in-store sleep consultations to justify premium tickets. Furniture chains scale their webshops, funneling traffic via augmented reality room renders and “click-to-collect” modules at warehouses. General Product Safety Regulation (GPSR) compliance nudges both clicks and bricks to embed QR-code passports detailing material origins and recyclability.

Project/B2B channels cultivate hotel and healthcare procurement desks, often operating under framework agreements that standardize pricing across multiple countries. Distributors employing circular collection schemes and refurbishment centers win EPR-conscious tenders, especially in BENELUX and the Nordics where landfill restrictions bite earliest. Regulatory compliance is becoming a key differentiator in retail channels, with consumers increasingly seeking products that meet environmental and safety standards. The growth of social commerce and influencer marketing is opening new customer acquisition channels, particularly for D2C brands targeting younger demographics.

Geography Analysis

Germany contributed 17.96% of 2025 revenue, driven by affluent households, a sizable therapeutic need base, and early adoption of circular economy mandates. Domestic producers shorten lead times by clustering supplier networks inside the country, mitigating import exposure under the Carbon Border Adjustment Mechanism (CBAM). Consumers associate German-made mattresses with engineering rigor and durability, sustaining premium pricing even during economic softness. German retailers are leading the adoption of omnichannel strategies, combining traditional furniture stores with online platforms and specialized mattress boutiques.

Spain is the Europe mattress market’s fastest grower, projected at 4.48% CAGR, underpinned by tourism bounce-back and refurbishments across the Costa del Sol, Balearics, and Canary Islands. Spanish factories ramp capacity not only for domestic hospitality but also for export runs into North Africa and Latin America along historic trade corridors. Younger demographics favor king-size and smart-sleep bundles, while hospitality brands pivot toward eco-labeled products to satisfy EU funding conditionalities. Regional manufacturers are expanding production capacity to serve both domestic and export markets, particularly in North Africa and Latin America. The growth of vacation rental properties and boutique accommodations is creating new demand for mid-range and premium mattresses. Spain's relatively young demographic profile compared to Northern European countries is supporting demand for larger mattress sizes and innovative product features.

France shows steady mid-single-digit growth, distinguished by strong brand loyalty and preference for domestically produced goods protected by origin labeling. Specialty chains dominate distribution, educating shoppers on artisanal upholstery and bio-based latex credentials. Italy remains Europe’s luxury nucleus, with 24.3% of residents aged 65+, lifting orthopaedic lines and boutique manufacturers steeped in craft heritage. BENELUX markets exhibit high saturation yet lead on circular initiatives; manufacturers pilot mattress leasing and take-back schemes that guarantee recycling rates above 85%. The Netherlands adopts IoT-embedded mattresses at twice the EU average, reflecting tech-savvy consumers and wellness insurance incentives. Nordic countries—Denmark, Sweden, Norway—support premium price points through high purchasing power and environmental stringency, pushing suppliers toward life-cycle analysis and carbon-negative models.

Competitive Landscape

The Europe mattress market is highly fragmented, with the top five players accounting for a limited share of the market in 2024. Tempur Sealy, IKEA Group, and Hilding Anders leverage vertically integrated foam pouring, spring engineering, and global sourcing to compress costs and ensure supply security. Emma – The Sleep Company and Simba Sleep exemplify D2C prowess, turning customer analytics into rapid SKU refreshes and localized marketing blitzes. Tempur Sealy’s 2025 acquisition of Mattress Firm deepens European omnichannel reach and improves distribution node density[4]Source: Tempur Sealy International, “Investor Presentation Q2 2025,” investor.tempursealy.com. The European Bedding Industries' Association (EBIA) has become a critical forum for industry collaboration on standards and best practices, particularly regarding ESPR compliance and circular economy initiatives.

Strategic themes pivot on omnichannel synergy, circular design, and smart-sleep differentiation. Leading incumbents co-design proprietary models with Marriott, Accor, and NHS trusts, securing multi-year replacement cycles. Disruptors file patents on modular zip-off comfort layers and AI-driven pressure mapping, embedding upgradable components that lengthen product life and recurrent revenue. Compliance costs for ESPR digital product passports drive smaller rivals toward joint ventures or exit, accelerating consolidation. The competitive dynamics are increasingly influenced by sustainability credentials, with companies investing in life cycle assessments, carbon footprint reduction, and circular business models to meet both regulatory requirements and consumer expectations.

Technology adoption accelerates: the HEKA AI mattress earned 2025 SleepTech accolades for machine-learning-based sleep-stage adjustment, reflecting the market’s appetite for blended hardware-software propositions. ESG imperatives shape procurement scoring; early movers publishing cradle-to-gate carbon footprints and third-party verified recycling rates win share in government-backed projects. Supply-chain resilience investments, dual-sourcing critical foams, near-shoring latex compounding, buffer volatility yet raise capital intensity barriers. The emergence of subscription and rental models, particularly among younger consumers, is creating new competitive dynamics and forcing traditional players to reconsider their business models and value propositions.

Europe Mattress Industry Leaders

Hilding Anders

Tempur Sealy International Inc.

IKEA Group

Recticel NV/SA

Pikolin Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Emma – The Sleep Company launched IoT-enabled sleep monitoring devices that synchronize with its premium mattress line.

- May 2025: Recticel unveiled advanced acoustic and thermal regulation foams for bedding applications, targeting premium and healthcare segments.

- May 2025: Tempur Sealy finalized the acquisition of Mattress Firm, bolstering European logistics and storefront coverage.

- May 2024: Emma – The Sleep Company opened its first physical D2C store in London, extending its digital footprint into experiential retail.

Europe Mattress Market Report Scope

Mattresses are the primary bedding component, either directly on a bed frame or as a standalone bed. Factors such as the mattress's initial craftsmanship, material composition, and even the sleepers' weight and preferred sleeping styles can significantly impact the bed's overall durability.

European Mattress Manufacturers Market is segmented by type (innerspring mattress, memory foam mattress, latex mattress, and others), end-user (residential and commercial), distribution channel (online and offline), and Geography (United Kingdom, Spain, Germany, Italy, France, and rest of Europe). The market size and forecasts are provided regarding value (USD) for all the above segments.

By Product Type

| Innerspring / Coil |

| Foam (including memory foam) |

| Latex |

| Hybrid |

| Other Mattress Types |

By Mattress Size

| Single-size Mattress |

| Double-size Mattress |

| Queen-size Mattress |

| King-size Mattress |

| Custom & Specialty Sizes |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B/Project |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product Type | Innerspring / Coil | |

| Foam (including memory foam) | ||

| Latex | ||

| Hybrid | ||

| Other Mattress Types | ||

| By Mattress Size | Single-size Mattress | |

| Double-size Mattress | ||

| Queen-size Mattress | ||

| King-size Mattress | ||

| Custom & Specialty Sizes | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the Europe mattress market in 2026?

The market stands at USD 11.61 billion in 2026 and is projected to reach USD 13.32 billion by 2031.

Which product type is growing fastest across Europe?

Hybrid mattresses lead growth with a forecast 4.22% CAGR through 2031 due to their blend of coil support and foam comfort.

What drives commercial mattress demand after the pandemic?

Hotel refurbishments and healthcare upgrades are renewing bulk orders, pushing the commercial segment toward a 3.98% CAGR.

Why are king-size mattresses gaining popularity?

Rising disposable incomes and larger bedroom footprints in Northern Europe encourage consumers to trade up to king-size formats.

How do EU regulations influence mattress manufacturing?

ESPR, EPR, and GPSR rules require recyclable designs, digital product passports, and enhanced safety documentation, raising compliance stakes.

Page last updated on: