Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

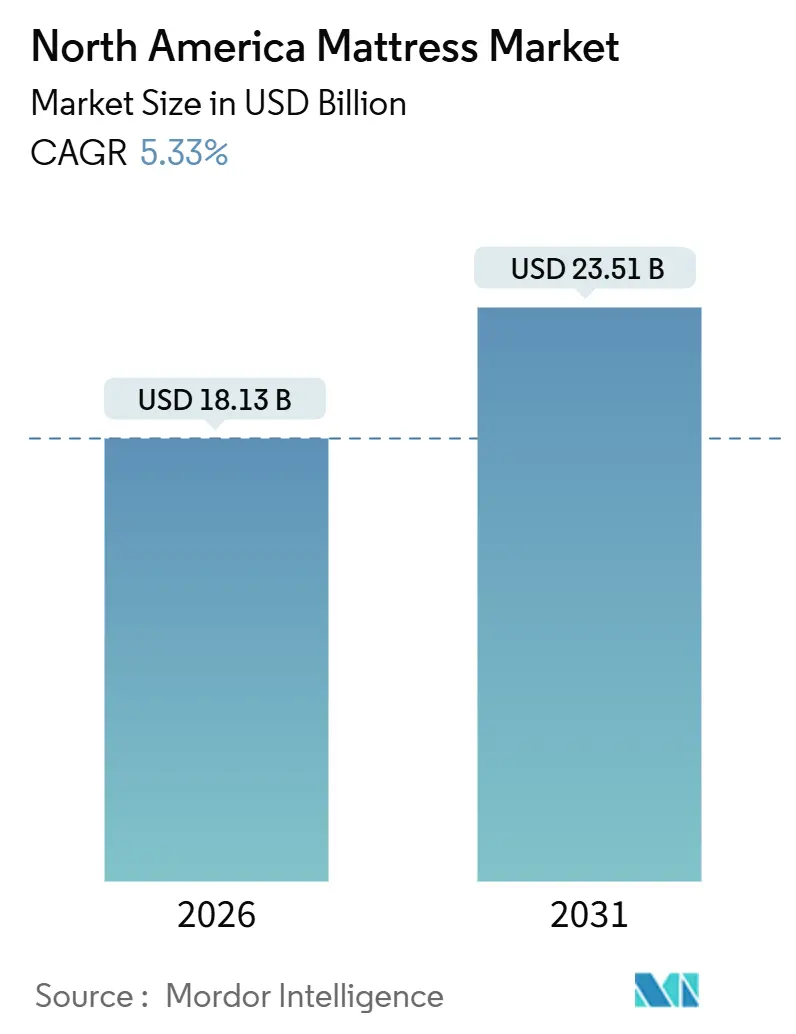

| Market Size (2026) | USD 18.13 Billion |

| Market Size (2031) | USD 23.51 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

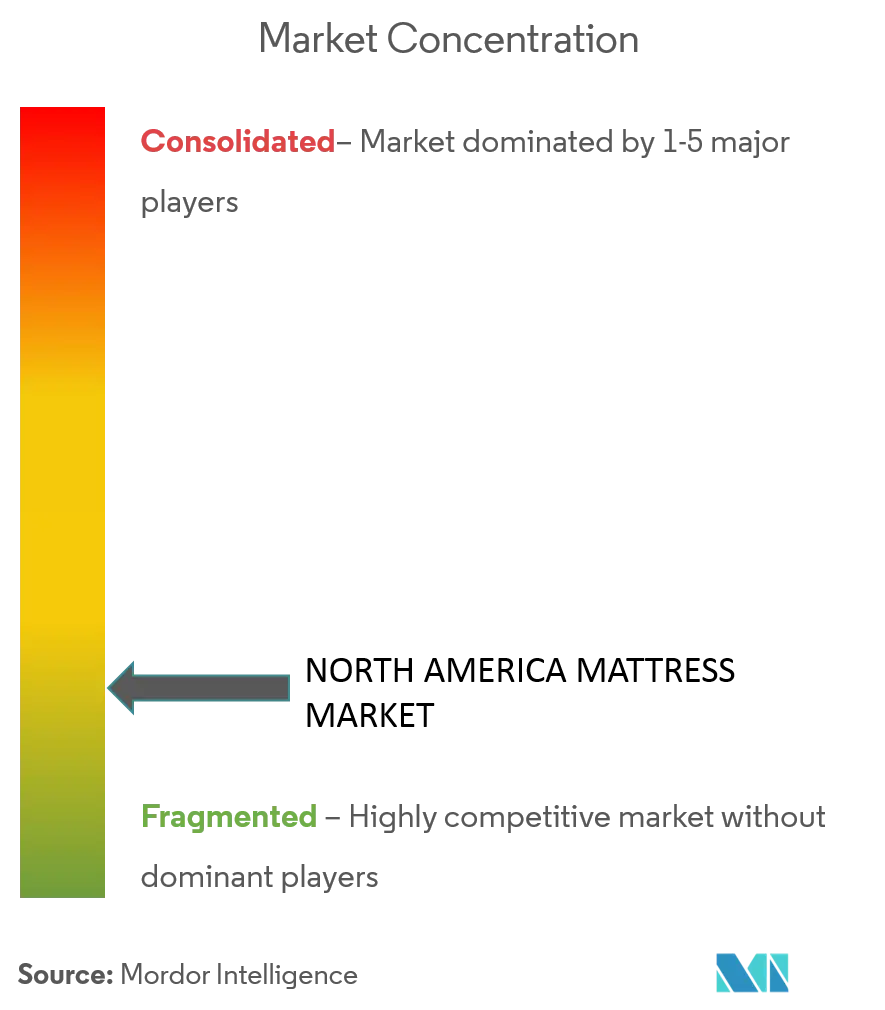

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Mattress Market Analysis by Mordor Intelligence

The North America mattress market size was USD 18.13 billion in 2026 and is projected to reach USD 23.51 billion by 2031, reflecting a 5.33% CAGR through the forecast period. Growth in the North America mattress market is being shaped by a multi-year pivot to premium comfort technologies, vertically integrated retail models, and accelerating sustainability mandates that influence product design and end-of-life programs. The rebound from a 2024 demand trough is uneven across channels, but scale players have used new product launches and advertising to restore pricing power and capture share in higher-value categories. Extended producer responsibility programs continue to expand, increasing recycling fees and compliance complexity, which favours brands with domestic operations and circular-design roadmaps. Meanwhile, consumer health priorities and sleep-tech adoption sustain demand for smart features, cooling innovation, and adjustable bases in the North America mattress market.

Key Report Takeaways

- By product type, innerspring led with 43.22% of the North America mattress market share in 2025, while foam products, including memory foam, are forecast to expand at a 6.46% CAGR through 2031.

- By mattress size, queen-size accounted for 47.61% of the North America mattress market share in 2025 and is projected to post a 5.98% CAGR through 2031, marking the strongest trajectory among sizes.

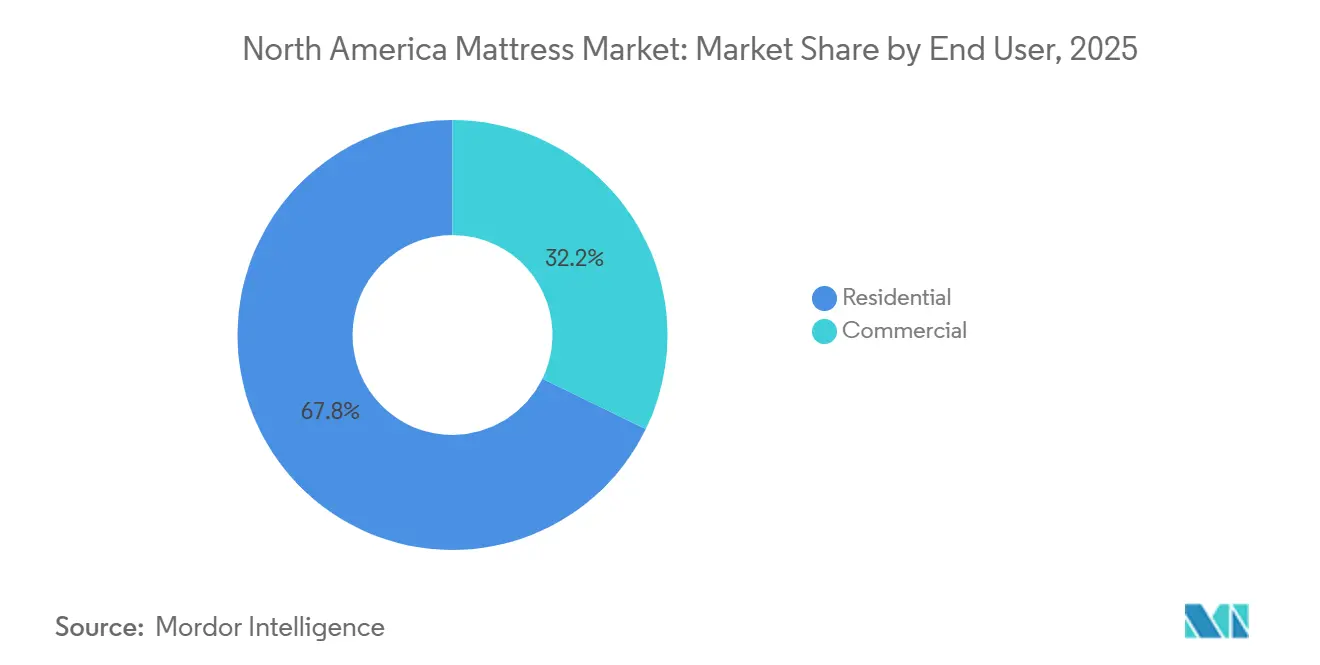

- By end user, the residential segment held 67.82% of the North America mattress market share in 2025 and is set to grow at a 6.05% CAGR through 2031.

- By distribution channel, B2C retail captured 65.23% of the North America mattress market share in 2025 and is forecast to register a 6.18% CAGR through 2031.

- By geography, the United States accounted for 81.49% of the North America mattress market share in 2025, while Canada is projected to post the fastest 5.61% CAGR through 2031, underscoring divergent baselines and growth drivers across the North America mattress market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of back pain & sleep disorders | +0.9% | United States, Canada | Medium term (2-4 years) |

| Growth of online "mattress-in-a-box" DTC brands | +0.7% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Premiumization via hybrid & memory-foam models | +1.1% | United States, Canada | Long term (≥ 4 years) |

| Hospitality renovation & new hotel projects | +0.5% | United States primary, Canada secondary | Medium term (2-4 years) |

| ESG-driven demand for recyclable mattresses | +0.6% | California, Oregon, Connecticut, Rhode Island, Massachusetts; expanding nationally | Long term (≥ 4 years) |

| Smart mattresses in elder-care facilities | +0.4% | United States, early adoption in Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Back Pain & Sleep Disorders Drives Replacement Cycles and Premium Purchases

Chronic pain has increased among United States adults, rising from 20.0% in 2019 to 24.3% in 2023, with back pain the most common complaint and a major contributor to nighttime discomfort and poor sleep quality. Sleep disorders have broad economic and health impacts, with insufficient sleep, insomnia, and sleep apnea weighing on productivity and household well-being across the North America mattress market. These combined conditions push consumers toward mattresses that provide better support, cooling, and pressure relief, while also shortening replacement cycles among those who experience persistent pain. Brands have responded with line refreshes and targeted technologies, including advanced cooling, zoned support systems, and bases that adjust firmness and positioning to reduce strain on the spine and hips. The product narrative is shifting from commodity bedding to wellness-oriented solutions, which supports pricing power and sustained upgrade demand in the North America mattress market. As health-aware households link sleep quality to productivity and longevity, this driver continues to underpin premium purchases even as economic conditions fluctuate.

Growth of Online "Mattress-in-a-Box" DTC Brands Disrupts Traditional Retail Economics

Digital-first brands normalized long trial periods and simplified delivery, reducing showroom overhead while pushing the broader retail ecosystem toward hybrid online-offline journeys in the North America mattress market. Scaled players have deepened direct-to-consumer sales and integrated online platforms with large store networks to give shoppers both tactile validation and doorstep convenience. New product cycles show the channel’s resilience, with Purple’s Rejuvenate 2.0 demonstrating strong direct response while also expanding wholesale floor presence to capture shoppers who prefer in-store consultations. As omnichannel options expand, brands are rebalancing media spend, strengthening supply chains for fast home delivery, and aligning boxable designs with parcel and LTL networks to safeguard margins. This evolution reshapes the North America mattress market by migrating value toward vertically integrated models that manage manufacturing, merchandising, and last-mile fulfilment within one platform. The resulting mix enables broader assortments, price-point coverage, and consistent brand storytelling across digital and physical touchpoints.

Premiumization Via Hybrid & Memory-Foam Models Elevates Average Transaction Values

New launches emphasize cooling, pressure relief, and motion isolation, which resonates with health-conscious households in the North America mattress market. Tempur Sealy refreshed its Sealy Posturepedic lineup in January 2025 and introduced TEMPUR-ActiveBreeze in January 2024 to broaden coverage from entry to premium segments with stronger innovation and brand pull[1]Tempur Sealy, “Newsroom - Product Launches and Corporate Announcements,” Tempur Sealy Newsroom, tempursealy.com. Sleep Number advanced the category’s temperature management narrative with its ClimateCool capability and continued to position adjustable bases and biometric insights as value-adding companions to the mattress purchase[2]leep Number Corporation, “Sleep Number Introduces ClimateCool Smart Bed: Actively Cools and Effortlessly Adjusts for Deeper, More Comfortable Sleep,” Sleep Number Investor Relations, ir.sleepnumber.com. . As consumers pair mattresses with smart bases and app-connected sleep tools, basket sizes expand, and attachment rates rise within higher-margin assortments in the North America mattress market. The premium tier also benefits from omnichannel placement, as premium shoppers often validate firmness, responsiveness, and edge support in-store before activating flexible online fulfilment options. These elements together support durable price realization and contribute to the category’s long-term CAGR uplift.

ESG-Driven Demand for Recyclable Mattresses Shapes Product Design and Supply Chains

Extended producer responsibility programs have expanded in scope and fees, with California, Connecticut, Rhode Island, and Oregon operating mattress recycling programs, and Massachusetts enforcing a disposal ban that shifts end-of-life practices toward recycling. California’s fee is set to increase to USD 18 per unit starting April 2026, while Oregon’s program fee is USD 22.50 per unit, and these changes raise planning needs for brands allocating return logistics and recycling support in the North America mattress market. California recycled 1.56 million mattresses in 2024, demonstrating that 75–90% of materials can be recovered when systems are set up for scale and convenience[3]Mattress Recycling Council, “Bedding Industry’s California Mattress Recycling Program Reaches New Milestones in Ninth Year,” mattressrecyclingcouncil.org. As compliance costs increase, design-for-disassembly practices and material transparency become more central to product roadmaps and marketing claims in the North America mattress market. Companies with regional manufacturing investments and clear material sourcing can better align with circularity requirements, as illustrated by Essentia’s 2026 United States plant opening that strengthens North American production for organic and low-emission constructions. As state programs mature, early movers that standardize recoverable constructions can benefit from operational predictability and brand credit with sustainability-minded consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polyurethane foam & steel prices | -0.8% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Supply-chain freight cost inflation | -0.5% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Landfill bans are raising the recycling compliance cost | -0.3% | California, Connecticut, Rhode Island, Oregon, Massachusetts | Medium term (2-4 years) |

| Fiberglass fire-barrier scrutiny & recall risk | -0.4% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Polyurethane Foam & Steel Prices Compress Manufacturer Margins

Raw material volatility limits pricing flexibility, especially when consumer demand sits below historical averages, and buyers are sensitive to price increases in the North America mattress market. The 2024 United States sales decline, with total mattress and stationary foundation sales falling 7.7% to USD 9.2 billion and units dropping to 36.5 million, reduced throughput and curbed the ability of smaller producers to offset cost spikes through volume leverage. These conditions amplify the advantage of scale and vertical integration, as large platforms can coordinate foam, spring, and assembly inputs across facilities and adjust mix to manage cost exposure. Upstream component suppliers provide another buffer for integrated players that align procurement, logistics, and product design across divisions to mitigate volatility within the North America mattress market. Smaller manufacturers face tighter working capital conditions when input costs rise faster than wholesale price revisions, which can constrain new product cycles and limit marketing support during peak selling periods. In this environment, product simplification, fewer SKUs, and targeted upgrades become more common near term to protect margins and stabilize factory utilization.

Landfill Bans Raising Recycling Compliance Cost Challenge Smaller Market Participants

State-level extended producer responsibility mandates and disposal bans in several states elevate both per-unit fees and administrative reporting requirements, which increase cost-to-serve for brands operating national assortments. California’s fee increases to USD 18 per unit in April 2026, while Oregon operates at USD 22.50 per unit, and the Massachusetts disposal ban adds planning requirements for retailers and e-commerce sellers serving that state in the North America mattress market. Recycling infrastructure varies by region, and limited capacity can create bottlenecks that complicate take-back programs during peak buying seasons, raising service-level risks. These conditions reward products designed for disassembly and clear material labelling, which simplifies recovery and improves downstream value from steel, foam, and fibre streams. Larger brands are better positioned to harmonize compliance, logistics, and consumer communications across state lines in the North America mattress market. As the circular economy becomes a stronger policy focus, producers that update constructions for recyclability can reduce long-run compliance cost intensity and improve customer experience at end-of-life.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Foam Gains Velocity While Innerspring Defends Volume Share

Innerspring mattresses held 43.22% of revenue in 2025, reflecting deep distribution in traditional retail and broad price accessibility, while foam offerings, including memory foam, are forecast to post a 6.46% CAGR through 2031, the fastest trajectory within the product mix in the North America mattress market. This mix highlights the steady role of coils in mass and commercial channels alongside the momentum of engineered foams that deliver pressure relief and motion isolation aligned with health and wellness needs. Premium hybrids that blend coil support with foam comfort layers reinforce the upgrade path for consumers who want a bouncier response and stronger edge performance in the North America mattress market. Line refreshes at scale, such as the all-new Sealy Posturepedic family introduced in January 2025, ensure coverage from entry to premium while spotlighting innovations in support systems and cooling materials. Smart base attachments and targeted cooling innovations continue to raise average selling prices and strengthen the perceived value of performance-focused configurations across the North America mattress market.

Leading brands are balancing factory throughput and SKU complexity by centring on high-velocity constructions and rationalizing low-rotation items where needed. In parallel, specialty suppliers and organic-focused producers are strengthening domestic production footprints to mitigate tariff and compliance risks, as seen in Essentia’s new Florida facility serving North American demand. Performance marketing by premium brands emphasizes cooling ranges, breathable textiles, and adjustable support to differentiate from commodity foam builds in the North America mattress market. As consumers weigh durability against price, foam and hybrid models with demonstrable comfort benefits are resonating, while established coil producers continue to defend volume share through value lines and hospitality placements. This balance suggests ongoing premiumization in the North America mattress industry while preserving the role of coils in value and commercial tiers that prioritize longevity and compliance.

By Mattress Size: Queen-Size Dominance Reflects Household Demographics and Bedroom Dimensions

Queen-size models led with a 47.61% share in 2025 and are projected to post a 5.98% CAGR through 2031, reflecting the best fit for typical household needs and retail floor dynamics in the North America mattress market. King-size retains a strong position among larger households and buyers with more space, though queen remains the default in many store assortments and DTC lineups. Single and double sizes maintain relevance for children’s rooms and guest spaces, with pricing strategies that balance affordability and basic comfort. Custom and specialty sizes, including split king formats, serve sleepers who want independent firmness and adjustable positioning paired with smart bases for personalized sleep in the North America mattress market. Packaging and home delivery also align well with queen and king sizes, supporting efficient fulfilment through parcel, LTL, or scheduled delivery networks.

Smart features and accessories reinforce size selection, as couples often prioritize dual-zone climate control and individualized support that favour split formats on adjustable foundations. Retailers are streamlining inventory by focusing on fast-moving queen configurations, while maintaining key king and specialty options to preserve attachment opportunities for premium buyers. E-commerce imagery, comparison tools, and virtual consultations complement in-store testing for size and comfort validation in the North America mattress market. Brands are also curating bedding and base bundles by size to simplify decision-making and to protect margins with value-added packages. This approach supports consistent consumer experiences across channels while coordinating supply chains around the highest volume formats.

By End User: Residential Segment Commands Share Yet Commercial Hospitality Provides Stability

Residential customers accounted for 67.82% of 2025 revenue and are projected to grow at a 6.05% CAGR through 2031, reflecting the central role of replacement cycles, household formation, and wellness-driven upgrades in the North America mattress market. The consumer shift toward cooling, pressure relief, and smart features supports higher average selling prices when paired with bases and accessories. Commercial buyers stabilize factory loads with batch procurement, formal specifications, and compliance checks that reward suppliers with coordinated component, assembly, and logistics capabilities. Senior living and healthcare facilities are testing connected solutions for monitoring and fall-risk reduction, improving outcomes, and aligning with value-based care objectives in the North America mattress market. This mix of consumer-led upgrades and institutional refreshes underpins steady demand across economic cycles.

Hospitality projects and chain standards also influence product roadmaps, with emphasis on durability, cleanability, and fire-code compliance that translates to consumer confidence. The rise of smart bases and app-connected insights creates new opportunities to extend value beyond the mattress in both residential and commercial environments. Brands with broad price coverage can serve entire portfolios from select-service hotels to premium suites, while aligning production with seasonal peaks in the North America mattress market. As households continue to prioritize sleep health and comfort, the residential segment remains the core growth engine, with commercial contracts offering counter-cyclical predictability and margin diversification. The result is a more stable blend of revenue streams that supports sustained investment in product innovation and omnichannel execution.

By Distribution Channel: B2C Retail Expands Fastest Yet Omnichannel Integration Blurs Boundaries

B2C retail captured 65.23% share in 2025 and is forecast to grow at a 6.18% CAGR through 2031, reflecting ongoing strength in direct-to-consumer e-commerce and specialty retail in the North America mattress market. Specialty chains provide tactile validation for premium shoppers, while online platforms excel at trial periods, delivery convenience, and assortment breadth. Large integrated operators are synchronizing store and digital experiences to create seamless shopping that supports both high-touch consultations and quick home delivery. Purple’s expansion within Mattress Firm illustrates how brands are combining wholesale floor presence with DTC-led innovation cycles to diversify traffic sources and reduce channel risk in the North America mattress market. Boxable designs continue to favour parcel and LTL networks, while unboxed premium models rely on scheduled delivery and white-glove services to protect the customer experience.

B2B project channels remain critical for hospitality and institutional buyers, where consistency, compliance, and service-level agreements define supplier selection. Vertically integrated retail platforms that can align merchandising, inventory, and last-mile delivery capture scale benefits and tighter feedback loops for product improvement. Retail media and performance marketing sharpen audience targeting, while in-store diagnostics and sleep consultations guide shoppers through comfort preferences in the North America mattress market. Returns and exchanges are streamlined through unified systems that link online orders with store networks to reduce reverse-logistics costs. The net effect is a channel landscape that rewards brands and retailers that remove friction and adapt assortments to consumer and commercial use cases across regions.

Geography Analysis

The United States accounted for 81.49% of regional revenue in 2025, reflecting the largest installed base and broad channel coverage across specialty retail, mass e-commerce, and brand-owned stores in the North America mattress market. Canada is projected to post the fastest 5.61% CAGR through 2031, reflecting steady household demand and increasing adoption of digital-first sleep solutions. After a 2024 downturn in the United States, where total mattress and stationary foundation sales fell 7.7% to USD 9.2 billion, and units declined to 36.5 million, activity in late 2025 and 2026 has been supported by product resets and integrated retail platforms, improving service levels and marketing reach. Product innovation and advertising from scaled platforms help normalize pricing and promote upgraded materials, cooling, and smart features that broaden appeal for wellness-minded buyers in the North America mattress market. Regulatory oversight of fire barriers and recycling accelerates compliance initiatives, which favour brands with domestic manufacturing, transparent materials, and robust quality systems.

Canada’s performance benefits from resilient demand drivers and rising omnichannel penetration, as consumers lean into comfort upgrades, smart bases, and shorter delivery windows. Locally relevant assortments that emphasize clean materials and durable constructions resonate with households that value long product life and clear certifications. Organic-focused brands are expanding manufacturing capacity within North America to support cross-border availability, which also helps manage policy shifts and improves lead times for Canadian shoppers. Retailers continue to refine unified commerce features that link online discovery with store trials and coordinated delivery across provinces to meet service expectations in the North America mattress market. The focus on localized service and transparent materials supports steady upgrades and replacement cycles without sacrificing convenience.

Mexico remains the smallest market by value within the region, yet it is strategically important for supply chains and near-term growth opportunities in localized production. Partnerships between brands and component suppliers support cross-border consistency in innerspring systems, foams, and assemblies that must meet United States and Canadian standards. As digital channels progress, boxable designs and simplified checkout processes help reach consumers across urban centres while traditional merchants continue to serve regional clusters. The broader North America mattress market benefits from regionalized manufacturing and component availability, which improves speed-to-market and resilience during periods of demand swings. Over time, these supply-side strengths are likely to support more consistent assortment planning and product refresh cadence across the three countries. Local execution and dependable service remain essential, especially as consumers expect immediate availability and easy returns for larger home goods.

Regulatory Landscape

In the United States, mattress sets are governed by the U.S. Consumer Product Safety Commission (CPSC) flammability standard 16 CFR Part 1633 (open-flame), which specifies performance-based heat-release limits and shapes compliance testing, labeling, and documented quality systems for both domestic producers and importers. Canada regulates mattresses under the Canada Consumer Product Safety Act through the Mattresses Regulations (SOR/2016-183), which reference national test methods (CAN/CGSB-4.2 No. 27.7-2023), making flammability performance a baseline requirement for market access.

Trade and end-of-life rules also affect operating decisions. U.S. trade measures, including Section 301 tariff actions updated in 2024 with staged implementation dates beginning January 1, 2025 and January 1, 2026 for covered China-origin products, add cost and sourcing complexity for imported mattress components and finished goods. On the sustainability side, state-level extended producer responsibility and disposal restrictions (for example, California, Connecticut, Rhode Island, and Oregon programs, and Massachusetts disposal requirements) increase reporting and per-unit fee planning, which pushes brands toward clearer material declarations and take-back readiness.

Value Chain Analysis

The value chain starts with upstream petrochemical and metal inputs, mainly polyols and isocyanates for polyurethane foam, steel wire and coil systems, textiles, and adhesives. Component fabrication then converts these inputs into foam, spring units, and covers and quilting, before final assembly into innerspring, foam, hybrid, and latex mattresses. Supply-side volatility has been a recurring input risk, highlighted by a March 2026 outage affecting polyol production at a LyondellBasell facility in Pasadena, Texas. The disruption tightened foam availability, triggered allocation dynamics and price pressure through mattress manufacturing, and reinforces the need for multi-sourcing, buffering, and in-house foam capabilities.

Downstream, the market splits between B2C retail (specialty stores, mass merchants, and online) and B2B or project channels (hospitality and institutions), where last-mile execution is a key cost and service determinant due to bulky freight and damage sensitivity. Retailers and buying groups have been formalizing freight and data-layer partnerships to stabilize delivery and inventory availability, including Nationwide Marketing Group's freight program with J.B. Hunt launched in April 2025 and Mattress Firm's final-mile partnership with Freightlined announced in September 2025. These efforts tend to favor platforms that can connect demand signals, inventory, and transport execution while managing returns and exchanges efficiently.

Competitive Landscape

The competitive landscape of the North America mattress market is consolidating as scale players extend vertical control and omnichannel reach. Tempur Sealy completed the acquisition of Mattress Firm in February 2025 and adopted the corporate name Somnigroup International, creating a unified platform that spans foam, innerspring, assembly, wholesale, e-commerce, and the largest specialty retail network in the United States[4]Somnigroup, “Tempur Sealy Successfully Completes Acquisition of Mattress Firm,” Somnigroup Newsroom, somnigroup.com. The combined platform positions Somnigroup as a category anchor with enhanced capabilities to manage product cycles and service levels in the North America mattress market. Competitors are responding with targeted innovation, selective store expansion, and partnerships that extend their floor presence in high-traffic retail environments. These moves sharpen differentiation while reinforcing the importance of reliable delivery and after-sales service.

Purple Innovation broadened its retail footprint within Mattress Firm, more than doubling its slot count to strengthen traffic capture and conversion in 2026, while striking a supply agreement that leverages Somnigroup’s assembly and logistics network for select lines. Sleep Number continued to deepen its technology leadership through connected beds and temperature management while earning the top spot in J.D. Power’s 2025 United States Mattress Satisfaction Study for both in-store and online purchases. Premium and organic-focused brands invested in North American manufacturing to ensure stable supply and shorter lead times, as highlighted by Essentia’s new United States facility announced for 2026. These strategies help sustain differentiation as consumers increasingly seek performance, sustainability, and dependable service in the North America mattress market.

Product innovation and partnerships also play a central role in competitive positioning. Tempur Sealy launched extensive product updates across key brands and introduced new cooling capabilities with TEMPUR-ActiveBreeze to attract premium buyers. Strategic supplier arrangements between Mattress Firm, Purple, and Leggett & Platt broadened the assortment across price points and components, supporting both value and premium segments in stores and online. Marketing partnerships that highlight sleep performance, such as Saatva’s collaboration with Team USA and LA28, reinforce brand trust and expand reach to new audiences in the North America mattress market. Leadership changes at technology-forward brands, including a new CEO and CFO at Sleep Number in 2025, underscore the importance of execution in omnichannel operations and product development during the next phase of category recovery. Across the field, manufacturers and retailers are aligning around fewer, stronger SKUs, expanded cooling options, and integrated delivery to sustain momentum.

North America Mattress Industry Leaders

Serta Simmons Bedding LLC

Tempur Sealy International Inc.

Sleep Number Corporation

Kingsdown Inc.

Corsicana Mattress Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

End-of-life compliance requirements continue to create whitespace for retailer-ready take-back and recycling enablement, particularly in states operating mattress recycling programs and in California where the recycling fee is scheduled to move to USD 18 per unit from April 2026. This environment supports mattress recycling-as-a-service partnerships that combine consumer communication, compliant pickup workflows, and consolidated reporting for national and regional sellers that need consistent processes across jurisdictions.

On the supply and product side, vertical integration and differentiated materials are emerging as a practical response to foam and logistics volatility, with multiple capacity and capability moves across North America. Examples include DeLandis Sleep adding a new foam-pouring line in May 2025 at its Houston facility, Americanstar starting in-house foam production in February 2026 in Waco, and Leesa launching GreenFlex in June 2026, a plant-based polyol foam produced in-house at its Arizona site and positioned as USDA Certified Biobased. In parallel, premium smart and modular architectures are moving beyond pilot concepts into commercial offerings, including 2026 launches featuring biometric sensing, pressure mapping, and serviceable modular designs. These developments align with the report's focus on AI-driven personalized sleep diagnostic platforms and higher-value attachments such as adjustable bases.

Recent Industry Developments

- June 2026: Sleep Number entered into an asset purchase agreement to combine with Sleep Country Canada. The move expands Sleep Number's addressable footprint in North America through a large Canadian retail platform and adds a new lever for omnichannel distribution and service coverage.

- March 2025: Somnigroup International announced that Mattress Firm signed new supplier arrangements with Purple Innovation and Leggett & Platt covering mattresses, foundations, and other bedding products across multiple price points. These agreements strengthen assortment control inside the largest U.S. specialty mattress retailer and tighten supplier-to-retail execution through a vertically integrated platform.

- May 2024: Serta Simmons Bedding launched the Beauty Sleep and Serta Classic collections. The introductions refreshed value and mid-tier lineups for broad retail placement, supporting traffic conversion in price-sensitive segments while keeping national brands active during a volatile demand period.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the North America mattress market as the value of new mattresses sold across the United States, Canada, and Mexico through consumer retail and project channels, covering common construction types used for sleep and rest applications.

Scope exclusions: This sizing excludes mattress toppers, pillows, sheets, and other bedding accessories, along with used and refurbished mattress resale.

Segmentation Overview

- By Product Type

- Innerspring / Coil

- Foam (including memory foam)

- Latex

- Hybrid

- Other Mattress Types

- By Mattress Size

- Single-size Mattress

- Double-size Mattress

- Queen-size Mattress

- King-size Mattress

- Custom & Specialty Sizes

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Mass Merchandisers

- Specialty Mattress Stores (including exclusive brand outlets)

- Online

- Other Distribution Channels

- B2B/Project

- B2C/Retail

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public series that help explain the demand pool and the supply movement behind mattress sales. Sources used include, for example, US Census Bureau housing indicators and retail indicators, Bureau of Economic Analysis consumer spending data, US International Trade Commission trade tables, and US Census Bureau Foreign Trade statistics on imports and exports.

We also referenced Statistics Canada household expenditure tables, the Government of Canada trade data portal, and Mexico's INEGI datasets where applicable to confirm macro direction and cross-country differences. In addition, we reviewed company filings, investor presentations, and association websites to track channel changes and pricing context. Where public data was too aggregated, we used paid subscription sources for company financials and news plus an import-export shipment-level database to validate revenue direction and product flow patterns. These sources are illustrative, and many other public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, component suppliers, retailers, and commercial buyers so channel mix and pricing logic could be checked against actual selling conditions. We also validated differences across the United States, Canada, and Mexico by testing assumptions on replacement cycles, online versus store conversion, and project demand from hospitality and other commercial uses.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 35% | |

| Smaller Players: 16% | Managers: 53% |

Market-Sizing & Forecasting

Our model starts from a top-down view where housing turnover, household formation, and durable-goods consumption are used to rebuild the replacement and first-time purchase pool. We then convert that pool into value using observed price bands and channel mix. Results are subsequently checked with selective bottom-up approximations, such as sampled average selling price (ASP) by type and size combined with volume signals from retailers and manufacturer commentary, before final totals are adjusted.

Key inputs included home sales and moves (common purchase triggers), replacement cycle timing by use, the online versus offline share shift, and mix movement across foam, innerspring or coil, hybrid, latex, and other constructions. We also tracked promotion intensity and freight sensitivity because these can shift realized ASP even when unit demand is stable. For forecasting, scenario analysis was applied so base expectations on consumption and housing could be stress-tested against faster or slower pricing normalization, and then cross-checked with expert views gathered in interviews.

When bottom-up checks were incomplete for smaller formats or niche size categories, gaps were handled through conservative mix assumptions derived from retailer assortment patterns, then re-tested with primary feedback so the long tail was not overstated.

Data Validation & Update Cycle

Outputs were validated through multiple checks, including reconciling implied units against realistic replacement behavior and comparing value growth with independent signals like retail sales direction and trade flow changes. Any large variance by country, channel, or type was flagged, and follow-up calls were triggered when expert feedback did not align with model math.

Before sign-off, the model and assumptions go through step-by-step analyst review so inputs, conversions, and currency handling stay consistent across the time series. Reports are refreshed annually, with interim updates when material events affect pricing, channel operations, or cross-border supply. Right before delivery, an analyst completes a fresh review pass so clients receive the latest updated view.

Mordor Intelligence's North America Mattress Market Estimate Compared With Other Published Estimates

Published market sizes for mattresses in North America often do not line up because the scope line is drawn differently, and because pricing, channel coverage, and timing assumptions are not always treated the same way. Some estimates lean more on retail sell-through value, while others are shaped by production and trade signals, which can pull totals apart.

The table shows a spread around the 2026 value, and under Mordor Intelligence's scope only new mattresses sold through B2C retail and B2B project channels across the United States, Canada, and Mexico are counted, while mattress toppers and other bedding accessories sit outside scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.13 B (2026) | |

| Industry Association A | USD 16.90 B (2026) | This type of estimate can run lower when value is inferred mainly from domestic shipments and factory-gate pricing, which can miss imported finished mattresses and can understate retail markups in omnichannel sales. |

| Trade Journal B | USD 20.40 B (2026) | This type of figure can trend higher when the count extends into related sleep products or when retail ASP growth is applied uniformly despite promotion cycles and mix shifts by construction type and size. |

Looking across the three figures, the key driver behind the gap is what gets counted as a mattress sale and how selling price is built up from channel realities. By tying demand to housing and replacement signals, then pressure-testing ASP and mix through interviews, we keep the total traceable to clear steps that can be repeated year after year.

Key Questions Answered in the Report

What is the current size and expected growth of the North America mattress market?

The North America mattress market size was USD 18.13 billion in 2026 and is forecast to reach USD 23.51 billion by 2031, implying a 5.33% CAGR over the period.

Which product categories are leading and growing fastest in North America?

Innerspring led with 43.22% share in 2025, while foam, including memory foam, is expected to post the fastest growth at a 6.46% CAGR through 2031 as premium comfort features gain traction.

How are channels evolving for mattress purchases in North America?

B2C retail held 65.23% of revenue in 2025 and is projected to grow at a 6.18% CAGR, supported by integrated online and specialty store experiences that improve selection and delivery convenience.

What factors are driving technology adoption in North American bedding?

Health concerns and sleep optimization are pushing adoption of cooling, adjustability, and biometric tracking, with connected platforms and smart bases expanding basket size and perceived value.

How do recycling and EPR programs affect the bedding category in North America?

State programs impose per-unit fees and reporting, such as California’s USD 18 fee from April 2026 and Oregon’s USD 22.50 fee, which encourage design-for-disassembly and coordinated take-back programs.

Which geography leads and which is growing fastest within North America?

The United States accounted for 81.49% of revenue in 2025, while Canada is projected to post the fastest 5.61% CAGR through 2031 based on current trajectories.

Page last updated on: