Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

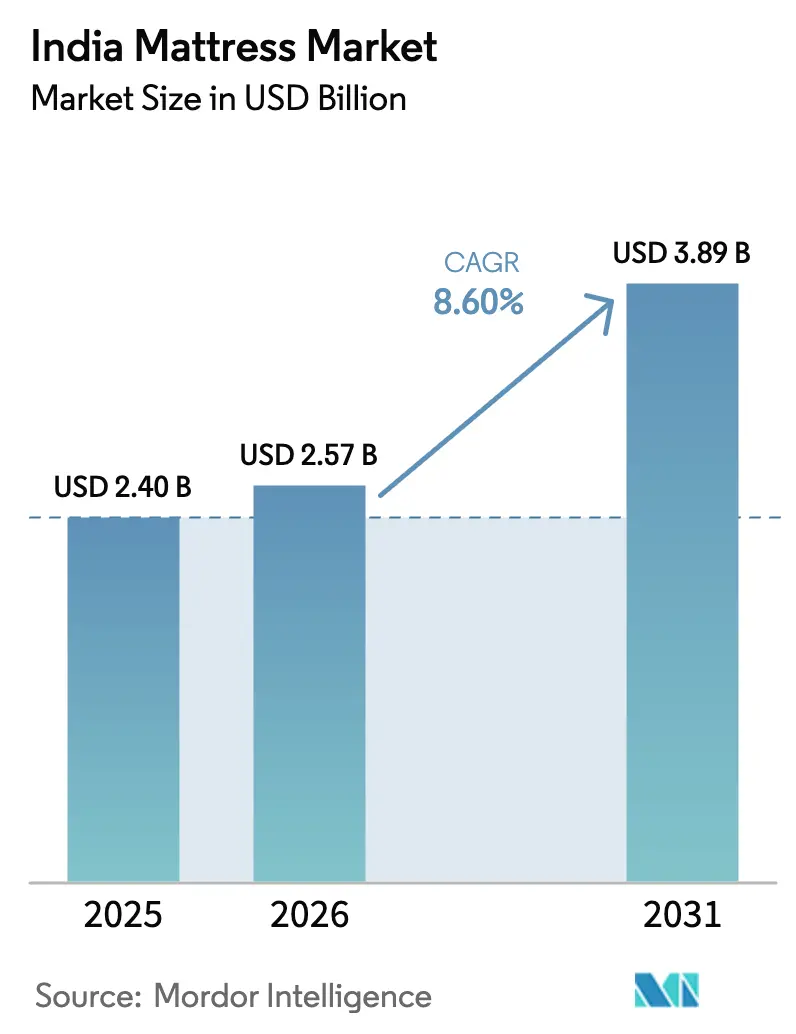

| Base Year Market Size (2025) | USD 2.40 Billion |

| Market Size (2026) | USD 2.57 Billion |

| Market Size (2031) | USD 3.89 Billion |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Mattress Market Analysis by Mordor Intelligence

The India mattress market size is projected to expand from USD 2.40 billion in 2025 and USD 2.57 billion in 2026 to USD 3.89 billion by 2031, registering a CAGR of 8.60% between 2026 to 2031. Government housing schemes, including the 11.8 million homes sanctioned under PMAY-Urban by November 2024, are sustaining first-time purchase and replacement cycles. In 2025, residential sales in India’s top eight cities totaled 3.48 lakh units, a 1% year-on-year decline. Despite rising prices, demand remained stable, with NCR witnessing a 19% price increase, followed by Hyderabad (13%), Bengaluru (12%), and Mumbai and Chennai (7%). Key drivers of housing demand included reduced home loan interest rates, strong economic growth, and lower inflation, which collectively supported market stability during the year. The National Housing Bank logged housing loans outstanding at INR 33.53 lakh crore (USD 402 billion) in September 2024, 14% higher than a year earlier, underscoring strong mortgage-led spending on household essentials. Urban millennials with rising disposable incomes are gravitating toward smart, health-tracking mattresses, while real-estate developers’ premium offerings fuel demand for king-size variants.

Key Report Takeaways

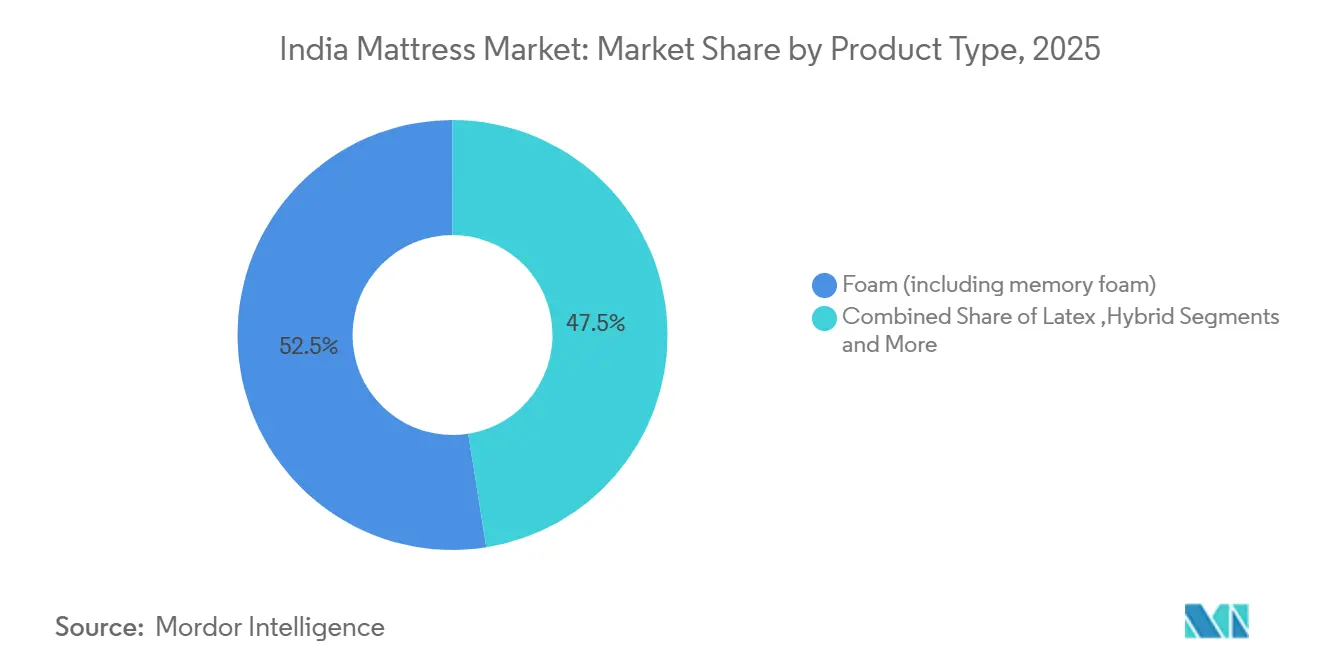

- By product type, foam (including memory foam) led with 52.51% of the India mattress market size in 2025; hybrid mattresses are forecast to expand at a 9.04% CAGR through 2031.

- By mattress size, queen-size held 33.78% of the India mattress market share in 2025, whereas king-size units are expected to post an outsized 8.92% CAGR to 2031.

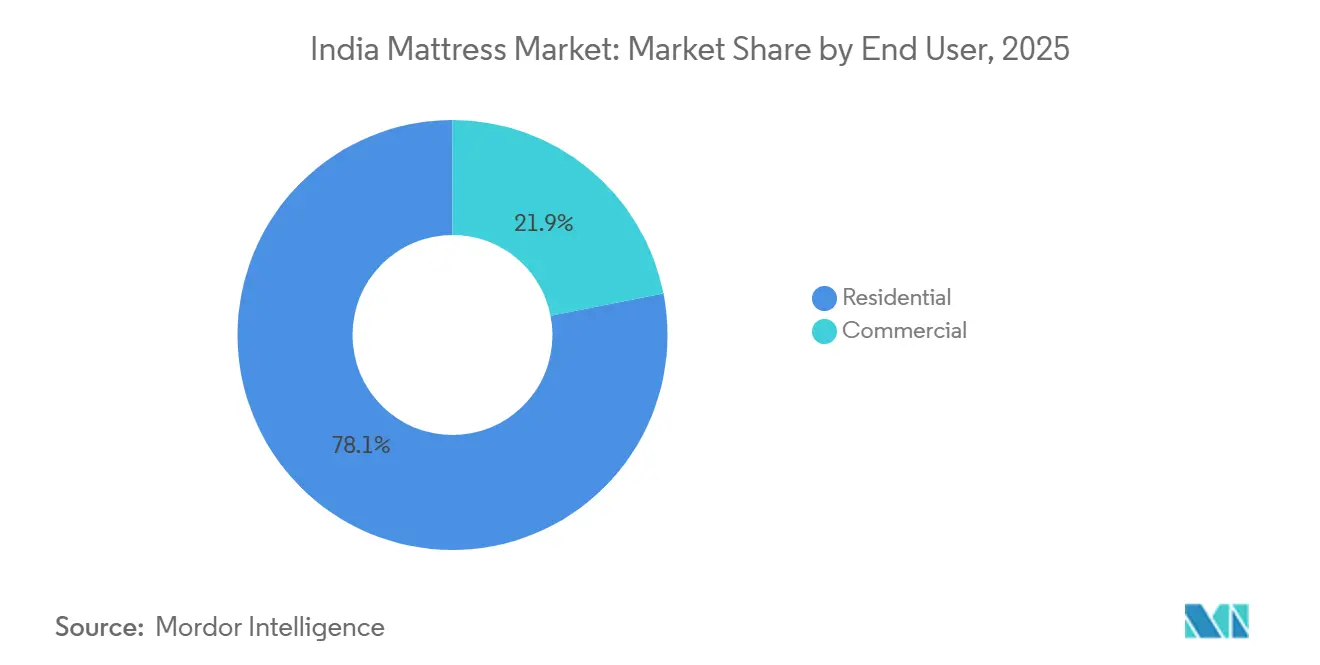

- By end user, residential demand accounted for 78.09% of the India mattress market size in 2025, while the commercial segment is projected to grow at a 10.06% CAGR during 2026-2031.

- By distribution channel, B2C/Retail commanded 72.48% of the India mattress market share in 2025, and is advancing at a 10.89% CAGR to 2031.

- By Geography, North India captured 29.81% of the India mattress market geographic share in 2025; South India is anticipated to be the fastest-growing region, registering a 9.39% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Initiatives promoting sleep-health awareness, endorsed by medical professionals | 1.8% | National, with early gains in metros (Mumbai, Delhi, Bengaluru, Chennai) | Medium term (2-4 years) |

| Growth in disposable income levels among urban millennial demographics | 2.1% | Tier-I and Tier-II cities, spillover to Tier-III | Long term (≥ 4 years) |

| Development and expansion of organized furniture retail networks | 1.5% | South and West India, expanding to North and East | Medium term (2-4 years) |

| Accelerated urbanization alongside a thriving real estate market | 2.3% | National, concentrated in the top 8 cities and PMAY-U beneficiary regions | Long term (≥ 4 years) |

| Increased e-commerce penetration in Tier-II and Tier-III cities | 1.4% | Tier-II and Tier-III cities across all regions | Short term (≤ 2 years) |

| Robust hospitality infrastructure pipeline driven by the G20 tourism agenda | 0.9% | National, with concentration in Delhi-NCR, Mumbai, Bengaluru, Goa, Rajasthan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Initiatives Promoting Sleep-Health Awareness, Endorsed by Medical Professionals

In India, Apollo Hospitals screened more than 10,000 individuals for sleep disorders during World Sleep Day 2024, linking poor sleep to diabetes and hypertension [1]Source: Apollo Hospitals, “World Sleep Day 2024 Initiative,” apollohospitals.com. Such medical validation is transforming mattress shopping into a preventive-health decision rather than a mere replacement purchase. Brands are responding to this trend in recent years, particularly during 2024–2025, with Sleepwell’s “Sleep Moksha” campaign highlighting productivity gains from quality sleep, while Duroflex has partnered with orthopedic clinics to recommend memory-foam products for back-pain relief. New products such as Sleepwell’s Fitrest line, which was introduced around September 2024 with Acuprofile technology and backed by a 25-year warranty, emphasize durability as a health differentiator in mattress innovation. Certification marks, CertiPUR-US for foam safety and OEKO-TEX 100 for textile purity, are now prominently displayed by Sunday Mattress on its Belgian-latex models to build consumer trust.

Growth in Disposable Income Levels among Urban Millennial Demographics

Home Credit India reported a 35% rise in EMI-based mattress purchases in 2024, with average ticket sizes increasing from INR 12,000 to INR 18,000 (USD 144–216). Easy financing allows millennials to trade up to mid-premium offerings featuring memory foam, hybrid cores, or IoT sensors. Market leaders target this cohort with technology-enabled products such as Wakefit’s Zense mattress, priced at INR 44,999 (USD 540) and equipped with temperature regulation and sleep-stage tracking. Social-media-driven promotions, for example, The Sleep Company’s INR 1 crore (USD 116,939) mattress giveaway that attracted more than 6,000 participants, is adding aspirational appeal to big-ticket sleep products [2]Source: ADGULLY, "The Sleep Company gives away around INR 1 Crore worth of free mattresses", https://archive.adgully.com/the-sleep-company-gives-away-around-inr-1-crore-worth-of-free-mattresses-149904.html. Mortgage data reinforce the trend, with middle- and high-income borrowers accounting for 61% of housing loans, and their larger homes typically accommodating king-size beds.

Accelerated Urbanization Alongside a Thriving Real Estate Market

India’s Economic Survey 2024–25, published by the Government of India, Ministry of Finance (Department of Economic Affairs), projects housing demand to reach 93 million units by 2036, driven by an urban population expected to hit 50% by 2050. [3]Source: Business Standard, “Economic Survey Highlights Real Estate Boom,” business-standard.com . Residential sales in the top eight cities soared 33% year-on-year to 4.1 lakh units in 2023, and first-quarter 2024 volumes rose another 41%. Each new dwelling triggers furniture spending, with mattresses typically absorbing 8–12% of the initial interior budget. National Housing Bank (NHB) in 2024 data show outstanding housing loans of USD 402 billion, with 39% in economically weaker segments, fueling affordable foam sales, and 44% in middle-income brackets, where memory-foam and hybrid products dominate [4]Source: Ministry of Finance, "National Housing Bank releases report on Trends and Progress of Housing in India 2024", https://www.pib.gov.in/PressReleasePage.aspx?PRID=2110726. Metro rail expansion 1,010 km in operation across 23 cities and 980 km under construction, is already concentrating housing demand along new corridors in Bengaluru, Hyderabad, and Delhi-NCR, as reported by the Ministry of Housing and Urban Affairs (MoHUA), Government of India, in 2024.

Development and Expansion of Organized Furniture Retail Networks

Specialty retailers, such as Peps Industries and Duroflex, continue to expand their footprint. Peps operates 35 Great Sleep Stores and 4,400 multi-brand partner outlets across Tamil Nadu alone, while Sleep Company aims to expand to 150 stores by March 2025. Store-based experiences, including in-store sleep consultants and trial zones, complement digital channels and justify premium pricing. Organized chains also unlock financing tie-ups, extended warranties, and BIS-certified assortments, mitigating the price advantage of the informal sector. Consumer confidence in branded stores has improved since 2023–2024 in South India, where retail density is highest, driven by consistent in-store experience, standardized pricing, and better after-sales service, and this confidence is now spreading to northern and eastern regions as large chains replicate these proven store formats. Vertical integration during 2023–2025, exemplified by Sheela Foam’s acquisition of Kurlon and its equity participation in Furlenco, has further strengthened organized players by improving control over product quality, supply chains, and inventory management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated product costs driven by the 18% GST rate | -1.2% | National | Long term (≥ 4 years) |

| Market fragmentation is fostering unorganized players with low-cost alternatives | -1.6% | National, more pronounced in Tier-III and Tier-IV towns | Medium term (2-4 years) |

| Persistent volatility in polyurethane and latex raw material prices | -0.9% | National, affects all organized manufacturers | Short term (≤ 2 years) |

| Limited infrastructure for mattress recycling is hindering sustainability | -0.4% | National, with urban waste management gaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Product Costs Driven by the 18% GST Rate

Mattresses attract an 18% GST, unchanged for a decade, adding INR 900 (USD 11) to a typical entry-level price tag of INR 5,000 (USD 60) and discouraging price-sensitive buyers. Repeated industry petitions to reduce the rate to 12%, the slab applied to most furniture, have been rejected on revenue grounds, sustaining the cost disadvantage for organized brands. Smaller players absorb compliance costs through tighter margins, while unregistered manufacturers sidestep taxation altogether and undercut branded products by up to 30%. Sheela Foam and Century combat the tax wedge by launching economy sub-brands and promoting EMI plans through Home Credit India, whose EMI-based mattress purchases grew 35% in 2024. Nevertheless, persistent taxation pressure remains a long-term obstacle to expanding penetration in rural and semi-urban India.

Market Fragmentation is Fostering Unorganized Players with Low-Cost Alternatives

Informal mattress makers dominate Tier-III and Tier-IV markets, often operating without BIS certification or GST compliance. Their price advantage is 20–30% below branded equivalents, making them the default choice for many budget-constrained consumers. Organized companies respond with differentiation strategies such as BIS marking, extended warranties, and 100-night trial programs, which illustrate a level of quality assurance that unbranded products cannot match. Retail education campaigns showcase the long-term benefits of certified materials and proper spinal support, albeit adoption is gradual. As e-commerce platforms expand, consumer reviews and return policies expose the deficiencies of low-grade substitutes, nudging wary buyers toward branded options. Yet, until certification enforcement tightens, fragmentation will sustain downward price pressure on the India mattress market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Foam Products Propel Innovation Across the Market

Foam (including memory foam) dominated the Indian mattress market size in 2025, securing a 52.51% share, while hybrid mattresses are anticipated to grow at a 9.04% CAGR through 2031, driven by their combination of spring support and foam comfort. Wakefit’s Zense, launched in June 2024 at INR 44,999 (USD 540), offers remote temperature regulation and sleep-stage tracking, making connected features accessible beyond ultra-premium price points. PU foam continues to dominate with a 49.74% share in 2024, supported by its wide availability across Peps’ 4,400 partner outlets in Tamil Nadu and over 900 Godrej Interio stores nationwide. Latex options marketed for breathability and allergen resistance find strong uptake in humid South India, where Sunday Mattress prices its Belgian-latex range between INR 25,000 and INR 45,000 (USD 300–540). Pocketed-spring hybrids like Century’s Sleepables combine motion isolation with roll-pack convenience, channeling online demand that previously shunned coil constructions. BIS standards (IS 14239 - PU foam, IS 11356 - latex) help organized brands differentiate on certified safety and durability, though enforcement remains uneven nationwide.

Growth prospects hinge on premiumization and health-tracking trends, with market leaders investing in R&D and patent licensing. Wakefit’s integration of app-driven algorithms parallels global wellness gadgets, signaling that connected sleep solutions will reshape consumer expectations over the next five years. Economical PU foam retains mass appeal, especially in replacement cycles among lower-income households taking advantage of PMAY-Urban subsidies. Latex and hybrid products will benefit from climatic comfort preferences and hospitality demand for durability. Collectively, innovation, certification, and affordability will dictate product-mix evolution in the India mattress market.

By Mattress Size: Queen-Size Mattresses Lead, While King-Size Records Growth

Queen-size mattresses commanded 33.78% of revenue in 2025, fitting typical 2-BHK city apartments, but king-size units are projected to post an outsized 8.92% CAGR through 2031 due to a low base and growing luxury-housing stock. NHB data indicate that middle- and high-income borrowers account for 61% of recent housing loans, and their larger master bedrooms routinely adopt king-size beds. Emma Sleep and Springwel now customise dimensions up to 84 inches for affluent buyers who prioritise comfort and room aesthetics. Single-size items remain staples for children’s rooms and hostels, but incremental upgrades to double-size at marginal price differences are eroding their share. Roll-pack distribution enables couriers to deliver double and queen formats into Tier-II towns, where Meesho’s 45% surge in transacting users underscores latent demand.

King-size proliferation mirrors premiumisation in the India mattress market: larger homes, higher disposable incomes, and aspirational lifestyles converge to make oversized beds a status symbol. Manufacturers thus bundle premium foams and smart sensors to justify higher price tags. Conversely, entry-level shoppers gravitate toward single and double formats priced below INR 8,000 (USD 96), often through online flash sales. Mass retailers educate buyers on space planning to reduce size-selection errors, bolstering repeat purchase satisfaction. Size preferences will henceforth segment the market along income and dwelling-type strata.

By End User: Commercial Demand Strengthens Amid Hospitality Sector Expansion

Residential consumers provided 78.09% of India's mattress market size in 2025, yet the commercial category, hotels, hospitals, and hostels, will expand at a 10.06% CAGR through 2031, outpacing household demand. India’s hospitality sector is expected to rise, supported by a USD 4.51 billion hotel development pipeline. Star-rated hotels favour standardised pocketed-spring mattresses for motion isolation, and Peps Industries capitalises on its Restonic license to secure long-term procurement contracts. Hospitals upgrade to waterproof, antimicrobial surfaces. Emma Sleep’s Latex II targets this niche, meeting infection-control norms. Student hostels and co-living spaces also scale bulk purchases, leveraging subscription models from platforms such as Furlenco, 35% owned by Sheela Foam, to manage capex.

Household demand remains pivotal, with PMAY-Urban completions triggering bundled furnishings that allocate 8–12% of budgets to bedding. First-time buyers in economically weaker segments often choose PU-foam or coir products under INR 8,000 (USD 96), whereas middle-income homeowners allocate INR 15,000–30,000 (USD 180–360) to memory-foam hybrids. Rental and subscription models cater to mobile young professionals, offering entry-level pricing at INR 148 per month for a single mattress in Chennai. Over the forecast period, commercial procurement cycles will shorten from seven to five years as hotels refresh inventory to meet international sleep-quality benchmarks.

By Distribution Channel: Online Channels Drive Transformation in Retail Distribution

B2C/Retail held a 72.48% share in 2025, and is advancing at a 10.89% CAGR through 2031. Wakefit and The Sleep Company both generate more than 60% of sales online while aggressively adding stores to offer hybrid experiences, targeting 242 and 150 outlets, respectively, by FY 2028. Godrej Interio’s 900-plus-store network cross-sells mattresses to furniture customers, aiming to reach INR 300 crore in revenue by 2028. Centuary’s Sleepables, sold exclusively on Amazon, Flipkart, and Pepperfry, targets a 200% revenue jump and 200,000 units in two years.

Mass-merchandiser struggles and Pepperfry’s distress sale, despite 195 stores, highlight the importance of private-label differentiation and supply-chain efficiency. Tier-II and Tier-III penetration accelerates through platforms like Meesho, eroding the unorganised sector’s hold by exposing buyers to certified brands at transparent prices. For B2B buyers, Project channels maintain a steady share due to lengthy tender cycles and relationship-driven procurement. Omnichannel strategies will shape competitive positioning in India's mattress market over the coming years.

Geography Analysis

North India commanded 29.81% of the India mattress market size in 2025, the highest regional share, supported by 1 million PMAY-Urban houses approved as of October 2025. The region favours memory-foam and orthopaedic models because colder winters and higher back-pain incidence influence purchasing criteria, a trend amplified after Sheela Foam merged Sleepwell and Kurlon through its acquisition. Metro-rail corridors, approximately 1,010 km operational and over 900 km under construction, are catalyzing transit-oriented suburbs such as Noida, Gurgaon, and Ghaziabad, tightening delivery radii for organized brands. Middle- and high-income borrowers now represent 61% of housing loans, and their larger 3-bedroom homes routinely specify king-size beds, raising the premium tier’s India mattress market size within the northern cluster. As a result, retailers allocate incremental floor space to high-margin king and smart mattresses in Delhi and Chandigarh showrooms to capture the upswing.

South India is projected to post the fastest regional growth at a 9.39% CAGR between 2026 and 2031, aided by the nation’s highest housing-credit share of 35.4% and unparalleled retail density, with Peps alone running 82 exclusive Great Sleep Stores and 4,000 multi-brand outlets in Tamil Nadu. Peps’ 2025 Tamil Nadu-only lineup, featuring 93% biodegradable Comfort mattresses, underscores the region’s receptivity to eco-labelled goods. Humid weather influences demand for breathable latex and hybrid mattresses, with Sunday Mattress's OEKO-TEX® certified Latex Plus range (approximately INR 30,000–40,000) and Emma Sleep's waterproof hybrids positioned as premium innovative offerings. Higher per-capita disposable income in Bengaluru, Chennai, and Hyderabad fuels uptake of connected products such as Wakefit’s Zense at INR 44,999 and The Sleep Company’s SensAI at up to INR 279,000, expanding the region’s share of the technology-enabled India mattress market. Omnichannel roll-outs by digital natives reinforce brand visibility, positioning South India as the launch pad for next-generation sleep solutions.

West India, anchored by Mumbai and Pune, leverages affluent demographics and a mature store network. East India offers the widest headroom: its 6.9% share of national housing credit in March 2024 signals latent demand that is now unlocked by metro projects in Kolkata and Bhubaneswar and Tier-II urbanization in Patna, Ranchi, and Guwahati. Wakefit and The Sleep Company are first movers beyond their southern bases, banking on lower competitive intensity to scale quickly. Tier-II cities in North and West India, such as Jaipur, Surat, and Nagpur, are also witnessing faster organized retail penetration as brands replicate proven formats, expanding the India mattress market share in formerly underserved pockets. Collectively, geographic disparities in credit flow, climate, and infrastructure shape a multi-speed growth map that rewards agile, region-specific strategies.

Competitive Landscape

Consolidation and digital disruption co-exist in the India mattress market. Wakefit, profitable and raising INR 1,400 crore via a December 2025 IPO, leverages D2C logistics, in-house roll-pack technology, and the Zense smart range to court tech-savvy buyers. The Sleep Company, with FY 2024 revenue of INR 335 crore, differentiates through SmartGRID polymer and immersive store experiences, capturing media attention with India’s biggest mattress giveaway event.

Peps Industries combines its Restonic license and 300,000-unit annual spring-mattress capacity to target INR 1,000 crore revenue within five years. Duroflex plans an IPO within 24 months and 23 new outlets by FY 2026, underlining confidence in premiumisation. Godrej Interio capitalises on a 900-store network to cross-sell mattresses, targeting INR 300 crore sales by 2028. Centuary’s online-only Sleepables launch demonstrates logistical innovation and taps into Amazon, Flipkart, and Pepperfry ecosystems. Certification - IS 14239, IS 7888, and IS 15907 act as a competitive moat, meeting rising consumer expectations for safety and longevity.

Competitive strategy increasingly revolves around omnichannel reach, R&D-led product differentiation, and scalable manufacturing. Top players invest in backward integration to hedge against raw-material volatility, while digital natives focus on user experience and data analytics. Market concentration remains moderate as unorganised players still supply vast rural markets, yet with the organised share rising, competition among formal brands intensifies. Continued M&A and IPO pipelines suggest further consolidation as firms raise capital to sustain marketing and innovation outlays.

India Mattress Industry Leaders

-

Sheela Foam Ltd

-

Kurlon Enterprises

-

Duroflex Pvt Ltd

-

Peps Industries

-

Wakefit Innovations

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Peps Industries aims to double its number of exclusive Peps Great Sleep stores from its current network of over 94 outlets, strengthening its direct retail footprint across India. Alongside expanding its exclusive store count, the company is also focusing on boosting exports, indicating a strategic move to grow both domestic retail presence and international sales.

- June 2025: The Sleep Company reached a major growth milestone with the launch of its 150th store, strengthening its position as India’s fastest-growing comfort-tech brand. The expansion reflects the company’s rapid retail growth across multiple cities and its continued focus on experiential stores showcasing its proprietary SmartGRID® sleep technology.

- February 2025: Peps Industries launched a new range of luxurious mattresses, including the Peps Comfort, Peps Supreme, and Peps Restonic Memory Foam collections, in the Bengaluru market as part of its product innovation drive. These new offerings are designed to meet evolving consumer needs for enhanced sleep comfort and quality using advanced materials and technology.

India Mattress Market Report Scope

A mattress is a rectangular cushion made of durable fabric filled with plush material or a system of coiled springs utilized for sleeping on a bed. A supportive mattress enables individuals to achieve a restful night's sleep consistently. A complete background analysis of the Indian Mattress Market, comprising emerging trends by segments and regional markets, key market players, market dynamics, and market overview, is covered in the report.

The India Mattress Market is segmented by product type, mattress size, end-user, distribution channels, and geography. By product type, the market is segmented as innerspring mattress, foam mattress, latex mattress, hybrid mattress, and others (gel, air beds, and celliant-infused mattress). By mattress size, the market is segmented into single-size, double-size, king-size, queen-size, custom & specialty. By end-user, the market is segmented into residential and commercial. By distribution channel, the market has the following segments: B2C/retail (mass merchandisers, specialty stores, online, and other), B2B/Project. The report offers market size and forecasts for the India Mattress Market in value (USD) for all the above segments.

By Product Type

| Innerspring / Coil |

| Foam (including memory foam) |

| Latex |

| Hybrid |

| Other Mattress Types |

By Mattress Size

| Single-size Mattress |

| Double-size Mattress |

| Queen-size Mattress |

| King-size Mattress |

| Custom & Specialty Sizes |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B/Project |

By Geography

| North India |

| West India |

| South India |

| East India |

| By Product Type | Innerspring / Coil | |

| Foam (including memory foam) | ||

| Latex | ||

| Hybrid | ||

| Other Mattress Types | ||

| By Mattress Size | Single-size Mattress | |

| Double-size Mattress | ||

| Queen-size Mattress | ||

| King-size Mattress | ||

| Custom & Specialty Sizes | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | North India | |

| West India | ||

| South India | ||

| East India | ||

Key Questions Answered in the Report

What is the current value of the India mattress market?

The market is valued at USD 2.57 billion in 2026 and is forecast to reach USD 3.89 billion by 2031 at an 8.60% CAGR.

Which product segment is growing fastest?

Hybrid mattresses are projected to grow at a 9.04% CAGR, driven by health-tracking features and rising disposable incomes.

Why are king-size mattresses surging in demand?

Premium housing trends, larger master bedrooms, and higher middle-income buying power are fueling an anticipated 8.92% CAGR for king-size units between 2026 and 2031.

Which distribution channel is expanding the quickest?

B2C/Retail is advancing at a 10.89% CAGR, aided by roll-pack logistics and deeper smartphone penetration.

How does the GST rate affect prices?

The 18% GST adds INR 900 to an INR 5,000 mattress, making branded products costlier and encouraging price-sensitive buyers to opt for unorganised alternatives.

How big is the commercial opportunity for hotel mattresses?

The commercial segment is expected to expand at a 10.06% CAGR through 2031, backed by 105 hotel projects in the pipeline and broader hospitality expansion.

Page last updated on: