Europe Sustainable Mattress Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

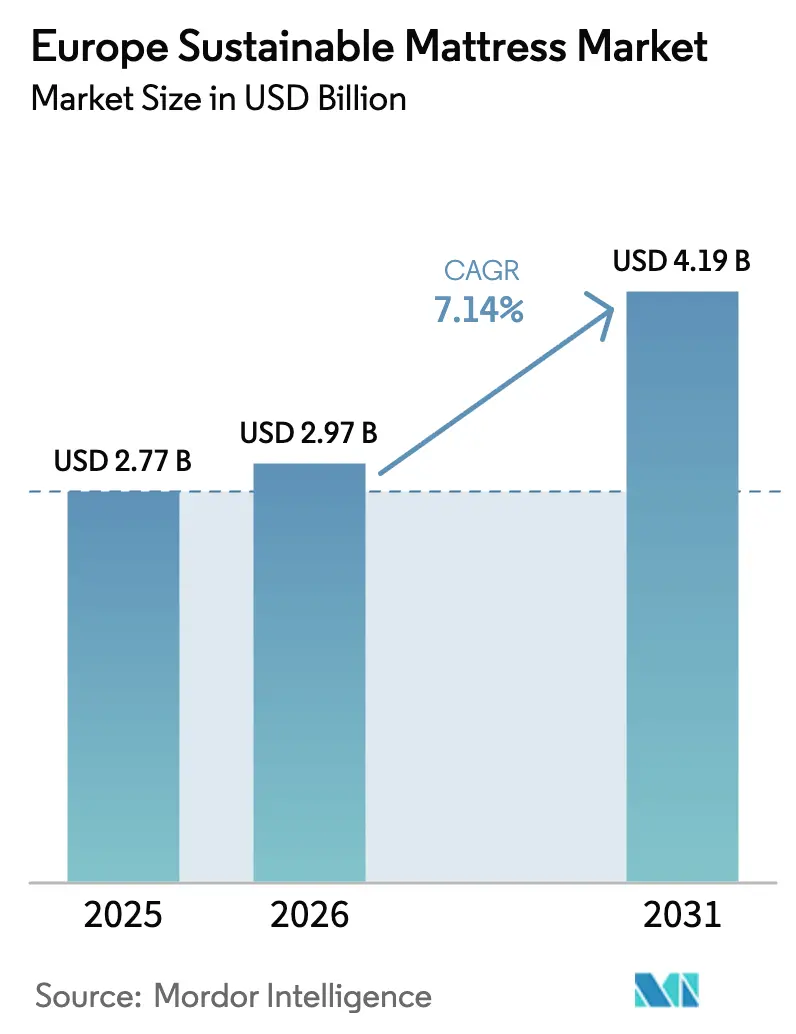

| Base Year Market Size (2025) | USD 2.77 Billion |

| Market Size (2026) | USD 2.97 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

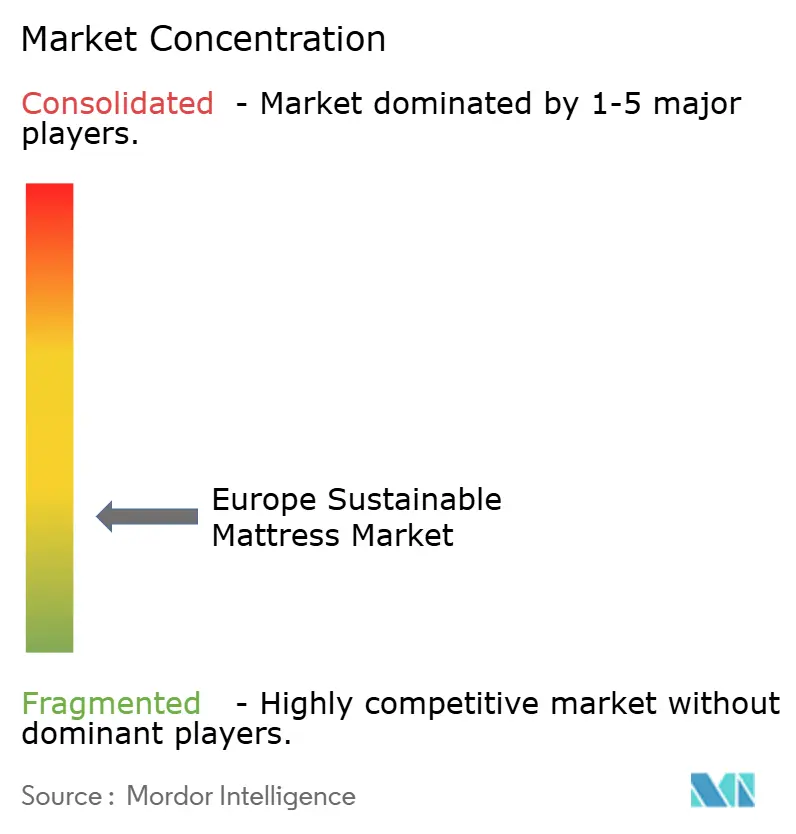

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Sustainable Mattress Market Analysis by Mordor Intelligence

The Europe sustainable mattress market size is expected to grow from USD 2.77 billion in 2025 to USD 2.97 billion in 2026 and is forecast to reach USD 4.19 billion by 2031 at 7.14% CAGR over 2026-2031. Demand accelerates as the Ecodesign for Sustainable Products Regulation (ESPR) mandates digital product passports for mattresses from 2027, pushing producers to disclose full life-cycle data [1]European Parliament and Council, “Ecodesign for Sustainable Products Regulation Text,” europarl.europa.eu . Consumer appetite for transparent, low-impact products, premium spending on sleep wellness, and the rise of bed-in-a-box logistics collectively lift the sustainable mattress market above broader bedding growth rates. Germany’s mature recycling infrastructure and strong purchasing power anchor regional demand, while Spain records the quickest adoption amid a younger, eco-focused demographic profile. Natural latex leads material choices thanks to durability and biodegradability, yet upcycled latex captures momentum as chemical-recycling pilots scale across Germany and the Netherlands. Commercial buyers in healthcare and hospitality accelerate orders to meet ESG targets, giving the B2B direct channel double-digit growth. Ongoing consolidation—exemplified by Tempur Sealy’s USD 5 billion Mattress Firm deal—signals tightening competition even as the broader competitive field remains fragmented.

Key Report Takeaways

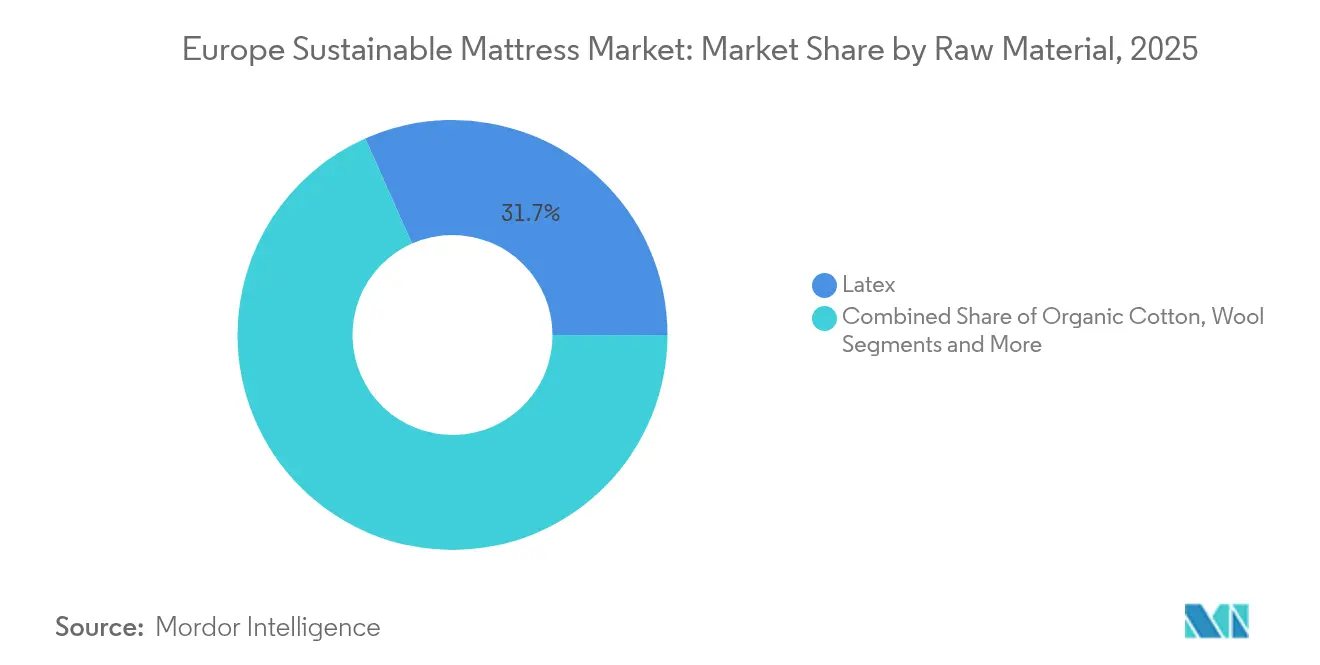

- By raw material, latex captured 31.65% of the sustainable mattress market share in 2025, while other raw materials are projected to advance at a 11.7% CAGR through 2031.

- By size, queen-size mattresses led with 39.20% revenue share in 2025; king-size mattresses are forecast to expand at a 8.55% CAGR to 2031, underscoring premiumization.

- By end-user, residential purchases accounted for 76.25% of the sustainable mattress market size in 2025, yet commercial demand is growing at 8.1% CAGR on the back of ESG-led procurement.

- By distribution channels, retail channels led with 82.10% revenue share in 2025; B2B direct sales posted the quickest pace at 10.35% CAGR, outstripping the overall sustainable mattress market.

- By geography, Germany held 26.60% of the regional sustainable mattress market in 2025, while the United Kingdom is poised for the fastest 11.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Sustainable Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Environmental Awareness Among European Consumers | +1.2% | Germany and the Nordics strongest | Medium term (2-4 years) |

| Stringent EU Circular-Economy & Ecolabel Policies | +1.8% | EU-wide, early BENELUX adoption | Long term (≥ 4 years) |

| Premiumisation & Wellness-Oriented Spending On Sleep Products | +1.5% | Western Europe's core, spreading south | Short term (≤ 2 years) |

| Expansion Of D2C E-Commerce Logistics & “Bed-In-A-Box” Models | +1.1% | The UK and Germany are leading | Medium term (2-4 years) |

| Breakthrough Chemical-Recycling Pilots For PU Mattress Foam | +0.9% | Germany and the Netherlands pilots | Long term (≥ 4 years) |

| ESG-Driven Procurement In Healthcare & Hospitality Chains | +0.7% | Major EU metro areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Environmental Awareness Among European Consumers

Europeans consider sustainability important and are buying eco-friendly products, indicating a shift toward low-impact goods. Eighty-six percent of Europeans consider sustainability important, and 29% actively purchase eco-friendly products, indicating a shift toward low-impact goods. Mattress decisions carry added weight because of long replacement cycles and intimate health links, letting brands translate environmental storytelling into palpable value. QR-code product passports and material origin disclosures resonate strongly with digital-native buyers. Austria’s public-sector push to cut healthcare carbon footprints reinforces the trend, pulling sustainable choices into residential channels.

Stringent EU Circular-Economy & Ecolabel Policies

The Ecodesign for Sustainable Products Regulation (ESPR) makes mattresses an early priority, obligating digital passports that record composition, recyclability, and end-of-life routes by 2027. Producers such as Aquinos Bedding plan to tag 1 million units via QR and RFID to pre-empt the deadline. EU Ecolabel certification, covering more than 102,000 products, confers brand distinction yet imposes documentation costs that favour scale operators' environment. France, Belgium, and the Netherlands require certified recycling for discarded mattresses, stimulating downstream infrastructure investment. From July 2026, large enterprises may no longer destroy unsold stock, catalyzing circular designs across the value chain.

Premiumisation & Wellness-Oriented Spending On Sleep Products

Consumers increasingly link sleep to holistic wellness, explaining the rapid 9.0% CAGR for king-size units through 2030. Higher disposable income segments are prepared to pay premiums for natural latex, organic cotton, and ethically sourced wool. Contract hotel buyers echo the pattern, adopting foam-free mattresses that support both guest comfort and carbon targets. As wellness budgets trump other discretionary categories, sustainable mattress market values continue climbing despite inflation. The commercial share uptick illustrates institutional willingness to translate health benefits into procurement policy.

Expansion Of D2C E-Commerce Logistics & “Bed-In-A-Box” Models

Compressed-foam technology allows home delivery through parcel networks, slashing transport emissions and packaging waste. Direct channels grew 10.9% CAGR as brands bypass intermediaries and supply chain layers. Emma Sleep’s Westfield London flagship blends online speed with tactile trial, birthing hybrid commerce. E-commerce buyers also demand sustainable packaging, pushing brands to adopt recycled cardboard and water-based inks. Regulatory scrutiny tightens on marketing claims, seen in the UK Competition and Markets Authority’s case against Emma Sleep, signalling an era of stricter oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Premium Vs Conventional Mattresses | -1.4% | Price-sensitive markets: Southern & Eastern Europe | Short term (≤ 2 years) |

| Volatile Pricing & Supply Of Natural Latex / Organic Fibres | -0.8% | Global supply chains are affecting all EU markets | Medium term (2-4 years) |

| Complex Multi-Material Construction Limits Recyclability | -0.6% | EU-wide, particularly affecting circular-economy initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Premium Vs Conventional Mattresses

Retail tags for sustainable lines sit 40-60% above synthetic foam models, creating affordability tension in price-sensitive regions. The gap stems from costlier inputs, ecolabel audits, and sub-scale runs. Purchase intent surveys show enthusiasm outrunning real conversion when budgets tighten. Financing plans and entry-level models target fence-sitters, yet maintaining margins while lowering ticket prices remains difficult. Economic headwinds, therefore, dampen near-term acceleration in the sustainable mattress market.

Volatile Pricing & Supply of Natural Latex / Organic Fibres

Climate-related yield swings pushed latex prices up to 45% in 2024, compressing manufacturer margins[2]BASF, “Chemical Recycling of Mattress Foams,” basf.com. Natural latex and organic cotton are subject to sharp price swings because their supply depends on weather patterns, farming yields, and geopolitical stability in key producing regions. Certified organic cotton faces similar pressure; less than 1% of global cotton acreage meets organic standards, so even small production shocks ripple quickly through prices. These fluctuations force European mattress makers to carry larger inventories and lock in long-term contracts, tying up more working capital than synthetic inputs with steadier pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Latex Leadership Drives Innovation

Latex commanded 31.65% of the sustainable mattress market share in 2025, reflecting consumer trust in its durability, breathability, and antimicrobial qualities. Upcycled latex is forecast to climb as chemical-recycling processes from Aarhus University enter commercial production, recovering feedstock at industrial yields. The sustainable mattress market size for latex-based units is projected to widen in line with regulatory preferences for biodegradable content. Wool maintains an eco-friendly niche as buyers value moisture control and thermal regulation. Coconut fibre and hemp fill plant-based propositions, whereas Liège University’s biobased polyurethane foams introduce isocyanate-free alternatives that cure in under two minutes.

Demand patterns vary across Europe. Nordic consumers, who post longer replacement cycles, gravitate to latex because of durability. Southern markets on tighter budgets prefer blended constructions that temper cost without sacrificing ecolabel eligibility. Suppliers adopt multi-material layering designed for easier disassembly, supporting future recycling mandates while preserving comfort profiles. Leading producers also integrate QR-enabled passports that disclose exact latex origin, verifying sustainable forestry and fair-labour compliance.

By Size: King-Size Growth Reflects Premiumisation

Queen units held 39.20% of volume in 2025, benefiting from standardised European bed frames and urban floor-space limits. The sustainable mattress market size for queen offerings remains sizable through 2031, even as king models surge. King formats show 8.55% CAGR because affluent buyers associate a larger surface area with superior sleep wellness. Northern European homes, which feature bigger bedrooms, accelerate the shift. Manufacturers reinforce king uptake with bundling promotions that pair mattresses with adjustable slatted bases made from certified timber, enhancing perceived value.

Single and double mattresses attract students and city dwellers with compact rooms. The segment retains relevance amid mounting urbanization, yet grows modestly compared to premium sizes. Custom dimensions cater to high-end renovation projects and accessible-housing retrofits, providing a small but steady revenue stream. BekaertDeslee’s Balance cover technology tailors stretch and breathability ratios to specific thicknesses, illustrating innovation even within traditional size lines.

By End-User: Commercial Acceleration Drives Growth

Residential customers contributed 76.25% of 2025 revenue, mirroring personal buying habits and multi-year replacement rhythms. Digital natives lean on influencer reviews and third-party ecolabel badges for decision support, rewarding transparent brands. The sustainable mattress market size in residential channels continues to climb, though at a slower pace than commercial. Hospitals and hotels chart an 8.1% CAGR as procurement teams embed carbon metrics into tender criteria. Hypnos offers foam-free hospitality ranges that meet durability and recyclability benchmarks.

ESG compliance compels facilities to document carbon savings, catalyzing demand for mattresses with recycled steel springs and biodegradable fiber layers. Commercial life-cycle costing models, recognizing lower disposal fees and longer service intervals, further justify higher upfront expenditure. Supplier contracts increasingly specify end-of-life take-back, creating annuity-style relationships that stabilize revenue streams for manufacturers.

By Distribution Channel: Direct Sales Transformation

B2C/Retail channels outlets still hold an 82.10% share thanks to showroom trials and high-touch sales staff. Yet online channels accelerate as bed-in-a-box formats solve legacy freight constraints. The sustainable mattress market size captured via pureplay e-commerce is poised to double between 2025 and 2030 as free returns and virtual sleep consultations reduce purchase friction. Direct manufacturer-to-business sales grow even faster at 10.35% CAGR, reflecting institutional buyers’ preference for traceable supply and bulk-order pricing.

Brands employ omnichannel tactics such as pop-up stores and mobile testing labs to bridge tactile and digital experiences. IKEA’s USD 1 billion recycling investment underpins reverse-logistics programs that let consumers return used units during new purchases, fostering loyalty while securing recyclable feedstock. Expect blended commerce formats to dominate future shopping journeys as regulation and consumer ethics align.

Geography Analysis

Germany contributes the largest 26.60% sustainable mattress market share in 2025, a position reinforced by the country’s 69% municipal-waste recycling rate that supplies a ready framework for mattress take-back and material recovery. German buyers value third-party labels, allowing EU Ecolabel products to command meaningful price premiums and fund further eco-design upgrades. BASF’s Brandenburg plant recovers polyols from discarded polyurethane foams, underscoring local prowess in chemical-recycling technology that feeds directly into the sustainable mattress market size for latex-hybrid and foam models. A mature retail base lets brands pilot mattress-as-a-service subscriptions, testing circular revenue streams while meeting the ESPR’s 2027 digital-passport deadline. Combined, these factors keep German growth steady even as penetration levels plateau at the high end of the regional curve.

The United Kingdom registers the fastest 11.21% CAGR through 2031, fueled by strong e-commerce logistics and rising wellness spending despite post-Brexit regulatory divergence. Emma Sleep’s Westfield London showroom blends tactile trials with D2C fulfilment and signals mainstream acceptance of bed-in-a-box formats that cut transport emissions. Regulatory vigilance is tightening in parallel; the Competition and Markets Authority’s case against Emma Sleep over discount claims underscores higher compliance expectations and should raise overall product-quality benchmarks. Hospitality chains such as Hypnos Contract Beds promote 100% foam-free, sustainable ranges, expanding commercial demand and lifting the sustainable mattress market size in the UK’s hotel segment. Tailored standards that mesh domestic needs with EU methodologies help sustain buyer confidence in ecolabels even as rules evolve locally. BENELUX countries are early adopters of digital product passports and closed-loop models such as RetourMatras, enabling higher collection rates and lower landfill fees. Nordic buyers pay the highest premiums and favour Nordic Swan-certified models, reflecting a mature sustainability culture.

Competitive Landscape

Industry structure remains fragmented even after Tempur Sealy’s USD 5 billion Mattress Firm acquisition that added more than 3,000 retail outlets to its portfolio. Large incumbents pursue horizontal deals to gain omnichannel reach and sustainability skills. IKEA’s Ingka Group committed USD 1 billion to European recycling plants, securing feedstock and strengthening brand credibility. Direct-to-consumer challengers such as Emma Sleep and Simba build differentiation on B Corp status and carbon-neutral logistics, trading scale for agility.

Vertical integration is a rising theme. Harrison Spinks cultivates its own hemp and flax, reducing input volatility while broadcasting farm-to-bed transparency. Technology partnerships matter as well; RAMPF Group supplies recycled polyols from PET waste, lowering Scope 3 emissions for mattress brands. Recticel’s PUReSmart initiative explores chemical recycling consortiums to pool R&D budgets and speed commercialisation. As ESG reporting becomes mandatory across Europe, certification prowess and circular-economy execution will separate leaders from laggards.

Europe Sustainable Mattress Industry Leaders

Emma Sleep GmbH

Tempur Sealy International Inc.

Hilding Anders International AB

Silentnight Group

Leggett & Platt Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Heimtextil introduced a “Sleep & Meet” zone for its 2026 fair to showcase sustainable production and recycling partnerships with Matratzen-Industrie e.V.

- February 2025: RetourMatras, backed by IKEA, launched an automated line that recycles 80% of mattress materials in the Netherlands.

- January 2025: IKEA’s Ingka Group earmarked USD 1 billion for mattress and plastic recycling assets.

- May 2024: Emma Sleep opened its first physical store in London’s Westfield mall.

Europe Sustainable Mattress Market Report Scope

Sustainable mattresses are made with organic materials that are grown without harmful chemicals. They are also made from biodegradable and consciously sourced materials like natural latex, organic cotton, and sustainably developed fabrics like tencel and Wwol.

The European sustainable mattress market is segmented by product, end-user, raw material, distribution channel, and geography. By product, the market is segmented into innerspring, memory foam, latex, and other products. By size, the market is segmented into single, double, queen, and king. By end user, the market is segmented into residential and commercial. By raw material, the market is segmented into organic cotton, wool, natural latex, and upcycled latex. By distribution channel, the market is segmented into specialty stores, furniture stores, direct, and online. By geography, the market is segmented into the United Kingdom, Spain, Germany, Italy, France, and the rest of Europe.

The report offers market size and forecasts in value (USD) for all the above segments.

| Organic Cotton |

| Wool |

| Latex |

| Other Raw Materials (coconut fiber, hemp, etc.) |

| Single |

| Double |

| Queen |

| King |

| Other Sizes |

| Residential |

| Commercial |

| B2B/Directly from the Manufacturers | |

| B2C/Retail Consumers | Specialty Bedding and Mattress Stores |

| Multi-brand Stores/Home Centers | |

| Online | |

| Other Distribution Channels |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Raw Material | Organic Cotton | |

| Wool | ||

| Latex | ||

| Other Raw Materials (coconut fiber, hemp, etc.) | ||

| By Size | Single | |

| Double | ||

| Queen | ||

| King | ||

| Other Sizes | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2B/Directly from the Manufacturers | |

| B2C/Retail Consumers | Specialty Bedding and Mattress Stores | |

| Multi-brand Stores/Home Centers | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size of Europe’s sustainable mattress market?

The sustainable mattress market stands at USD 2.97 billion in 2026 and is projected to reach USD 4.19 billion by 2031 at a 7.14% CAGR.

Which material leads the sustainable mattress market share?

Latex is the top material with 31.65% share in 2025 because of its durability, breathability, and biodegradability.

Why are king-size sustainable mattresses growing faster than other sizes?

Premiumisation and wellness spending drive a 8.55% CAGR for king-size units as consumers seek larger sleep surfaces for better comfort.

How are EU regulations shaping the sustainable mattress industry?

The Ecodesign for Sustainable Products Regulation will require digital product passports by 2027, pushing manufacturers toward full transparency and recyclability.

Which sales channel is expanding most rapidly?

B2B direct sales to healthcare and hospitality buyers show the highest 10.35% CAGR, supported by ESG procurement mandates.

What limits growth in price-sensitive regions?

High premiums over conventional mattresses and volatile costs for natural inputs deter adoption in Southern and Eastern Europe despite rising interest in sustainability.

Page last updated on: