Hybrid Fiber Coaxial Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

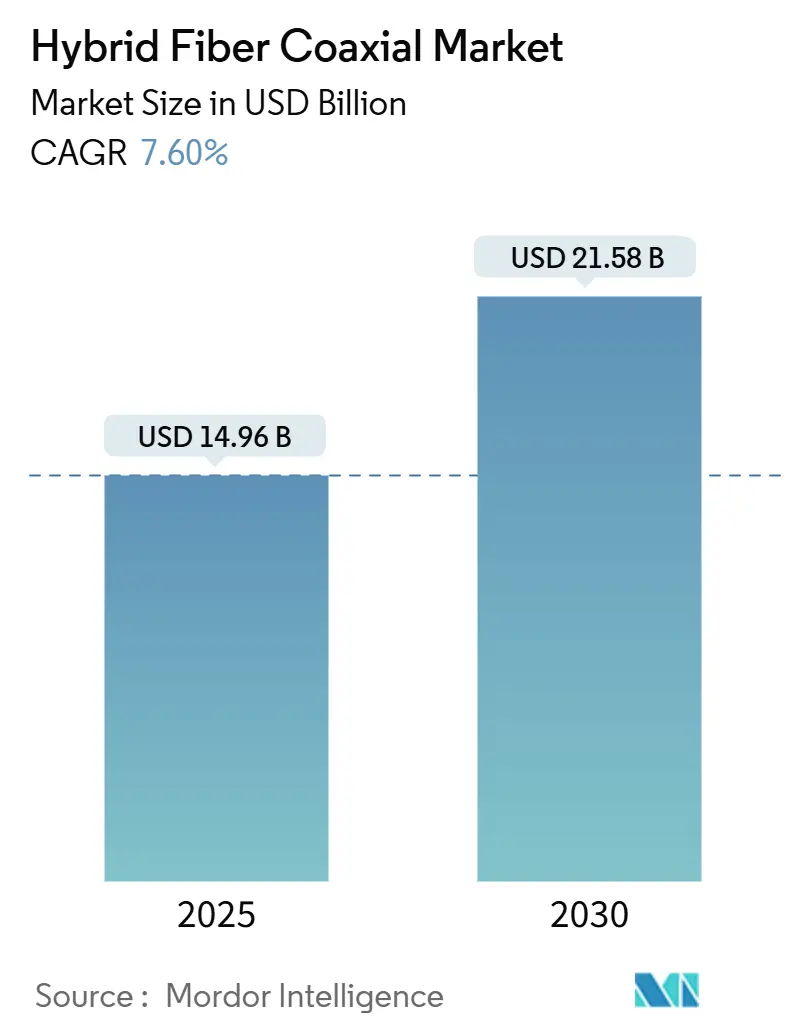

| Market Size (2025) | USD 14.96 Billion |

| Market Size (2030) | USD 21.58 Billion |

| Growth Rate (2025 - 2030) | 7.60% CAGR |

| Fastest Growing Market | South America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Fiber Coaxial Market Analysis by Mordor Intelligence

The Hybrid Fiber Coaxial market size is valued at USD 14.96 billion in 2025 and is projected to reach USD 21.58 billion by 2030, growing at a 7.60% CAGR during the forecast period. Cable operators are extending the life of existing plant through DOCSIS 4.0 upgrades, node+0 designs and GaN amplifier deployments that reduce maintenance costs and boost upstream capacity. Government broadband subsidies in the United States, European Union and parts of Asia are influencing technology choice, allowing HFC upgrades in high-cost areas where full fiber deployments remain uneconomical. Operators are also integrating edge-compute capabilities to monetize low-latency services for enterprises and content providers. Meanwhile, semiconductor shortages and stricter energy-efficiency mandates create supply-chain and regulatory headwinds that shape upgrade timelines.

Key Report Takeaways

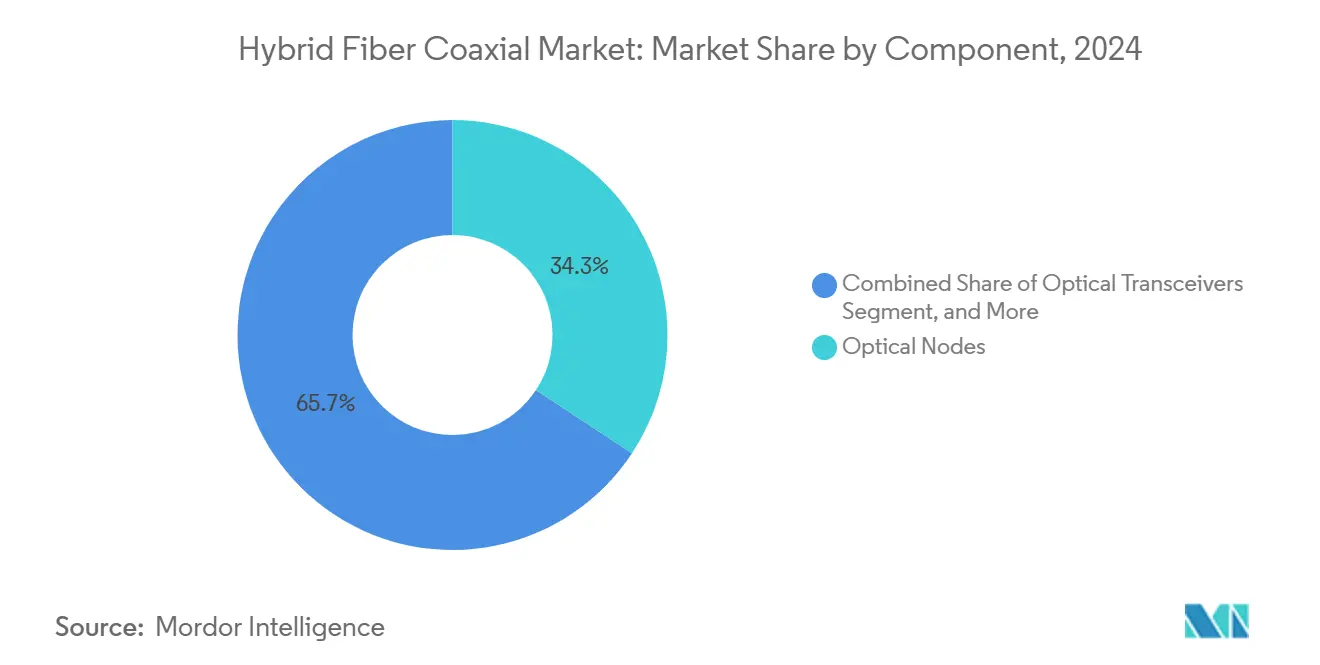

- By component, Optical Nodes led with 34.27% of Hybrid Fiber Coaxial market share in 2024, while RF Amplifiers recorded the fastest growth at a 7.96% CAGR through 2030.

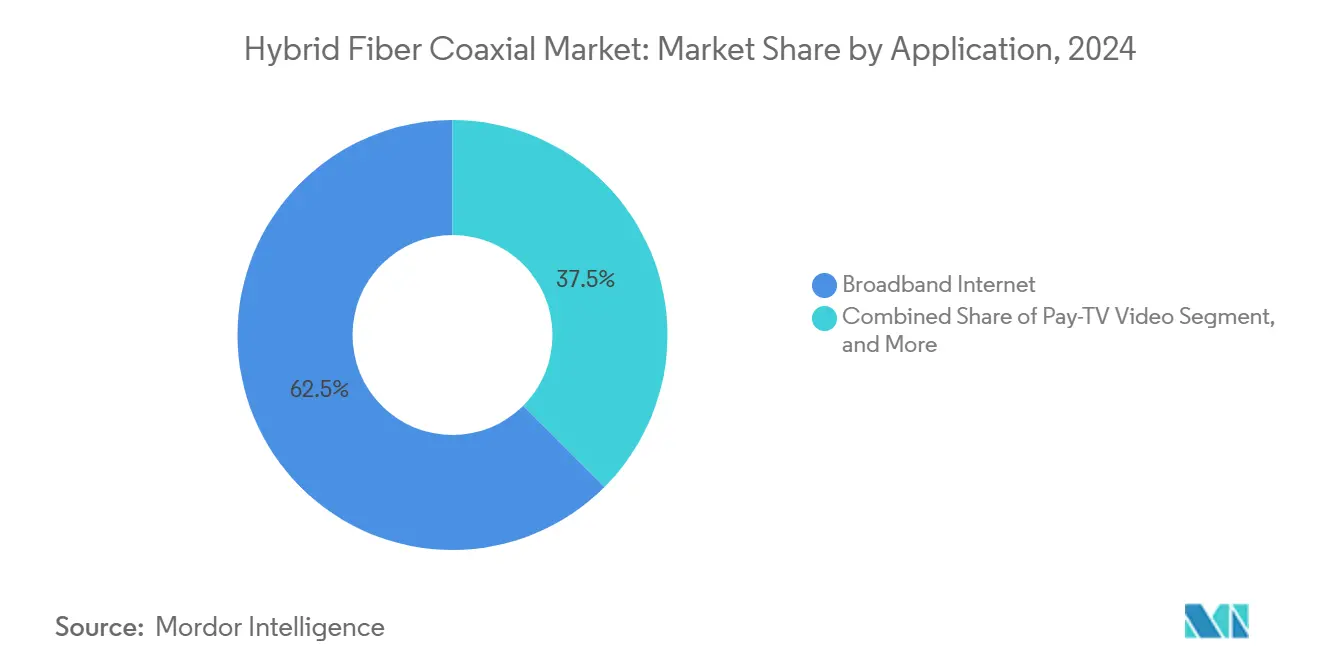

- By application, Broadband Internet accounted for 62.51% share of the Hybrid Fiber Coaxial market size in 2024 and Enterprise Services are projected to expand at an 8.89% CAGR through 2030.

- By end-user, Residential users represented 71.27% of Hybrid Fiber Coaxial market share in 2024, while Government and Education segment is forecasting 9.11% CAGR to 2030.

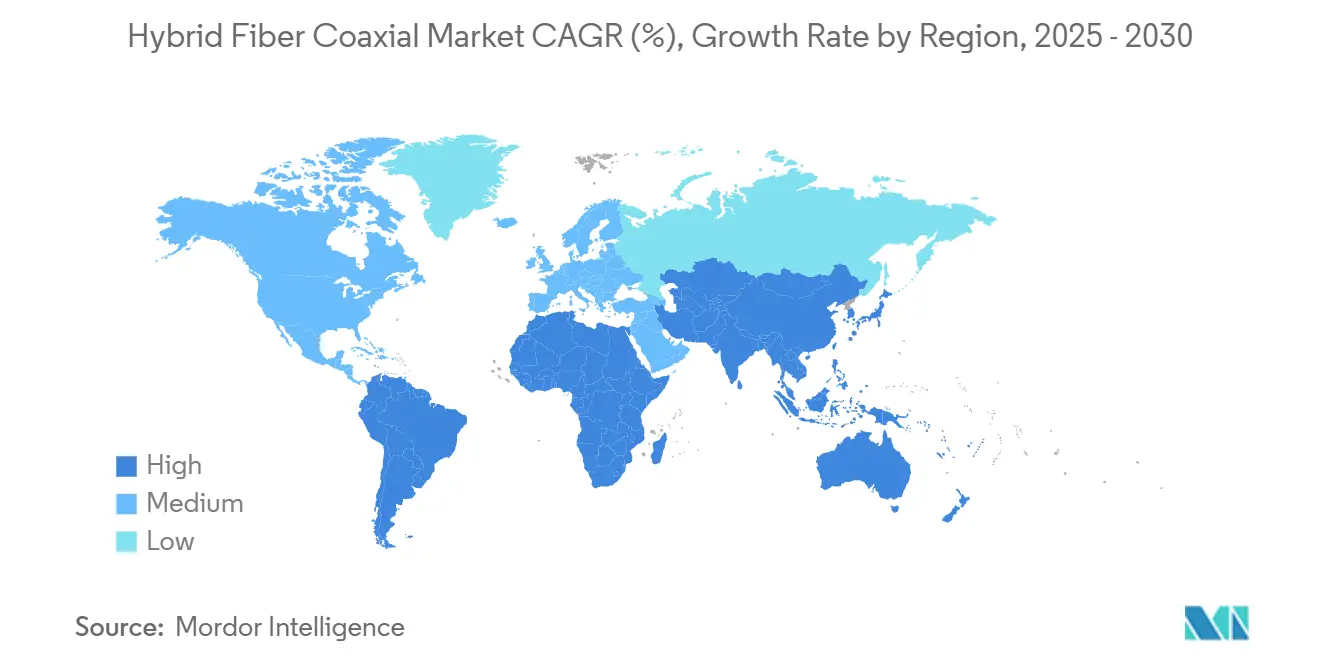

- By geography, North America contributed 38.87% share of the Hybrid Fiber Coaxial market size in 2024 and South America is expected to post the quickest regional growth at an 8.34% CAGR to 2030.

Global Hybrid Fiber Coaxial Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DOCSIS 4.0 roll-outs accelerating node+0 architecture adoption | +1.8% | North America and EU, selective Asia-Pacific | Medium term (2-4 years) |

| Surge in DOCSIS-based gigabit broadband demand in emerging Asia | +1.2% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Government rural broadband subsidy waves in the US and EU | +0.9% | North America and EU | Short term (≤ 2 years) |

| Cable MSO edge-compute integration for low-latency services | +0.7% | Global, early gains in North America | Medium term (2-4 years) |

| Energy-efficient GaN amplifier deployments lowering OPEX | +0.6% | Global | Medium term (2-4 years) |

| Re-use of existing coax plant vs. FTTH CAPEX parity tipping-point | +0.5% | Global, dense urban cores | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

DOCSIS 4.0 roll-outs accelerating node+0 architecture adoption

Cable operators are scaling DOCSIS 4.0 to deliver symmetric multi-gigabit speeds while preserving legacy coaxial investments. Comcast has introduced the technology across 10 markets and plans to cover 63 million locations using more than 160,000 distributed access nodes. [1]Jeff Baumgartner, “Comcast ready to hit the accelerator on DOCSIS 4.0,” lightreading.com The Broadcom-Charter-Comcast unified chipset targets 25 Gbps capability over 3 GHz spectrum, integrating AI-driven optimization that eases field management. Node+0 eliminates cascaded amplifiers between the fiber node and each premise, cutting maintenance and energy costs. Successful adoption rests on GaN amplifier availability and workforce training because legacy LDMOS devices cannot handle extended spectrum. These steps allow HFC networks to compete with FTTH in urban areas where trenching costs exceed USD 1,000 per home passed.

Surge in DOCSIS-based gigabit broadband demand in emerging Asia

Broadband consumption is rising sharply across emerging Asian economies, and governments are modernizing cable networks as a cost-conscious alternative to fiber. China’s broadband budget already surpassed USD 323 billion and continues to fund DOCSIS 3.1 and early DOCSIS 4.0 pilots in tier-2 cities. The Asian Development Bank’s 2025 policy report highlights rural-urban digital gaps and positions HFC as a bridge technology. India and several Southeast Asian countries favor HFC upgrades to bypass right-of-way challenges linked to greenfield fiber. Price-sensitive consumers benefit from shared coaxial infrastructure in multi-dwelling units, while regulators increasingly recognize HFC as an eligible platform for universal-service subsidies.

Government rural broadband subsidy waves in the US and EU

The USD 42.45 billion BEAD program includes provisions for HFC upgrades in extremely high-cost areas, an approach echoed by several U.S. states supplementing federal grants. Europe’s Gigabit Infrastructure Act streamlines permits and encourages infrastructure reuse under a EUR 174 billion connectivity plan. Co-ops and municipal utilities are leveraging these funds to modernize coax networks, trimming deployment timelines from 18 to 6 months. “Build America, Buy America” sourcing rules further incentivize domestic HFC equipment purchases, creating short-term demand spikes for U.S. vendors.

Cable MSO edge-compute integration for low-latency services

Operators are transforming fiber-deep networks into distributed computing fabrics. Comcast’s Open Edge platform, deployed at nearly 200 sites, forms a content delivery layer that cuts latency for streaming and gaming traffic. The company’s Janus initiative virtualizes core functions using AI to anticipate congestion. Similar moves by Cox Communications reduce fault-resolution times from 45 minutes to 45 seconds. Enterprise use-cases AI inferencing, AR and IoT drive incremental revenue, strengthening HFC competitiveness against all-fiber rivals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid FTTH over-build in dense urban cores | -1.4% | Global, developed markets | Medium term (2-4 years) |

| Tightened power-consumption standards for outside-plant amps | -0.8% | North America and EU | Short term (≤ 2 years) |

| Limited DOCSIS talent pool delaying field upgrades | -0.6% | Global | Medium term (2-4 years) |

| Supply-chain shortages of high-spec RF passive components | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid FTTH over-build in dense urban cores

Municipal broadband and competitive fiber providers are installing FTTH in high-density zones, eroding HFC’s core revenue base. Fiber’s unlimited bandwidth and symmetric speeds appeal to households streaming 4K video, cloud gaming and remote work. EU policy now mandates fiber-ready building standards, and the BEAD program ranks fiber ahead of other media for future proofing. [2]ISE Staff, “Powering the Plant: HFC versus FTTH,” isemag.comOperators must decide between DOCSIS 4.0 defense of urban clusters or shifting capital to suburban and rural markets. Falling fiber construction costs reinforce the threat as HFC upgrade expenses climb with spectrum expansion and amplifier replacement.

Tightened power-consumption standards for outside-plant amps

Energy directives in the EU and several U.S. states limit permissible power draw for telecom gear, complicating high-frequency HFC designs. GaN amplifiers enable 1.8 GHz spectrum but consume more power than legacy solutions, conflicting with operators’ sustainability pledges. [3]Jeff Baumgartner, “Cable Nodes Becoming a Choke Point,” lightreading.com Node+0 removes cascaded amps yet concentrates higher-powered devices at the node, triggering upgrades to local power feeds and cooling. Added power management can raise per-node costs by USD 500–1,000 and may redirect budgets toward inherently more efficient fiber builds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Optical Nodes underpin migration flexibility

Optical Nodes accounted for 34.27% share of Hybrid Fiber Coaxial market size in 2024. These devices provide the fiber-coax demarcation that dictates speed, latency and upgrade agility. Fiber-deep rollouts shorten coax runs, prompting demand for modular nodes with software-defined controls that ease remote re-tuning. RF Amplifiers post the fastest 7.96% CAGR as operators adopt GaN devices to unlock extended spectrum and node+0 patterns. Integrated vendors bundling optical, RF and management software gain advantage as operators seek single-invoice procurement. Coaxial Cable, Passives and Customer-Premises Equipment remain replacement-driven but benefit from DOCSIS 4.0 modem cycles and Wi-Fi 6E adoption.

Component integration is reshaping supply chains. CommScope’s acquisition of Casa Systems’ virtual CMTS assets concentrates intellectual property and enables end-to-end offers. GaN costs are higher yet acceptable due to OPEX savings from fewer field amplifiers, while predictive maintenance built into smart nodes reduces truck rolls. These factors sustain capital allocation to node and amplifier upgrades through 2030.

By End-User: Residential base, institutional momentum

Residential customers provided 71.27% of Hybrid Fiber Coaxial market share in 2024, fueled by pandemic-anchored streaming habits and multi-device households. Government and Education segment is the fastest grower at 9.11% CAGR, reflecting stimulus-backed digital transformation. Rural school upgrades under the U.K.’s Gigabit Connectivity Scheme showcase how HFC meets dense-user concurrency needs without new trenching. Health agencies exploring telemedicine favor symmetric bandwidth and centralized management. Commercial and SMB users sustain steady growth as hybrid work requires dependable upstream and VPN capabilities.

Institutional buyers value proven uptime and remote provisioning in DOCSIS networks. Their procurement rules often demand mature standards and broad vendor support, factors currently favoring HFC over nascent fiber offerings inz many suburban and ex-urban districts.

By Application: Broadband dominates, enterprise surges

Broadband Internet commanded 62.51% share of Hybrid Fiber Coaxial market size in 2024. Streaming video, cloud collaboration and gaming depend on reliable downstream throughput, reinforcing this segment. Enterprise Services, while smaller, project the highest 8.89% CAGR as MSOs layer managed security, SD-WAN and edge compute atop connectivity. Comcast Business’ tie-up with Starlink illustrates diversification into satellite resiliency packages that complement terrestrial HFC links. Pay-TV Video continues secular decline yet remains a cash-flow stream via IPTV overlays. Voice-over-Cable persists within bundled offers, especially in cost-sensitive markets.

Growth in enterprise apps hinges on HFC’s symmetrical upgrade path. DOCSIS 4.0 upstream gains facilitate AI inferencing at the edge, remote robotic control and massive IoT packet bursts, creating higher-margin services beyond commodity broadband.

Geography Analysis

North America held 38.87% Hybrid Fiber Coaxial market share in 2024. Aggressive DOCSIS 4.0 roadmaps by Comcast and Charter, plus the USD 42.45 billion BEAD program that reimburses HFC upgrades in high-cost rural zones, underpin regional momentum. Canada’s technology-neutral rules encourage cable-fibre coexistence, while Mexico’s cost-sensitive consumers accept coax upgrades over new fiber builds. Established supply chains and skilled labor accelerate equipment turnover, making the region a global reference site for DOCSIS 4.0 validation.

South America represents the fastest regional expansion with an 8.34% CAGR to 2030. Brazil’s National Broadband Plan supports competitive infrastructure, enabling cable operators to revitalize coax plant instead of duplicating fiber. Argentina and Andean nations value HFC’s lower capital intensity amid currency volatility. Rising streaming adoption among urban middle classes amplifies data demand, while subsidies target network gaps in underserved zones.

Europe shows divergent signals: the EUR 174 billion Gigabit Infrastructure Act pushes deep fiber, yet permits HFC modernization where premises costs exceed EUR 3,000. MSOs in Germany, Spain and parts of Eastern Europe deploy DOCSIS 4.0 selectively, keeping coax competitive until fiber depreciation cycles close. Asia-Pacific remains mixed. China’s historic USD 323 billion broadband investment fuels DOCSIS pilots in dense areas lacking viable FTTH economics. India and Southeast Asia pursue cost-effective coax upgrades to sidestep right-of-way hurdles. The Middle East and Africa adopt HFC for rapid urban coverage where scarce fiber manpower slows roll-outs.

Competitive Landscape

Hybrid Fiber Coaxial equipment supply is moderately concentrated. CommScope, Cisco, Harmonic and a few others bundle optical nodes, amplifiers and CPE into integrated portfolios, limiting multi-vendor complexity. CommScope’s USD 2.1 billion wireless divestiture and Casa Systems asset purchase sharpen its DOCSIS focus. Cisco leverages AI-enhanced routing to embed edge compute orchestration, gaining 29% product order growth in FY2025.

Competitive advantage hinges on DOCSIS 4.0 readiness and GaN amplifier roadmaps. Broadcom’s chipset collaboration with Charter and Comcast illustrates vertically aligned innovation that can exclude rivals lacking spectrum-extension IP. Patent filings concentrate on AI-driven capacity prediction and dynamic spectrum allocation, signifying the shift from hardware prowess to software intelligence. New entrants emerge in SDN and edge-platform domains, but entrenched vendors retain scale economies and long-running service contracts that keep switching costs high.

Supply-chain volatility remains a wildcard. Semiconductor shortages, particularly of high-spec passive components, force operators to stagger upgrades and test multi-sourcing. Energy-consumption limits may favor vendors with efficient GaN designs or hybrid optical-electrical nodes. Overall, pricing discipline prevails as differentiation centers on performance, lifecycle cost and software automation rather than sticker discounts.

Hybrid Fiber Coaxial Industry Leaders

CommScope Holding Company Inc. (ARRIS Solutions)

Cisco Systems Inc.

Harmonic Inc.

Casa Systems Inc.

Teleste Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: T-Mobile signed 5G MVNO agreements with Comcast and Charter for enterprise mobility services launching in 2026.

- June 2025: Comcast Business partnered with Starlink to add satellite backup to enterprise offers.

- April 2025: Harmonic recorded Q1 2025 revenue of USD 133.1 million and returned to GAAP profitability.

- February 2025: CommScope reported Q4 2024 revenue of USD 1.17 billion, up 26.6% year over year, and finalized a USD 2.1 billion wireless divestiture to focus on connectivity solutions.

Global Hybrid Fiber Coaxial Market Report Scope

| Optical Transceivers |

| Optical Nodes |

| RF Amplifiers |

| Coaxial Cable and Passives |

| Customer-Premises Equipment (CPE) |

| Residential |

| Commercial and SMB |

| Government and Education |

| Broadband Internet |

| Pay-TV Video |

| Voice-over-Cable (VoC) |

| Enterprise Services (Business/Data Backhaul) |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Component | Optical Transceivers |

| Optical Nodes | |

| RF Amplifiers | |

| Coaxial Cable and Passives | |

| Customer-Premises Equipment (CPE) | |

| By End-User | Residential |

| Commercial and SMB | |

| Government and Education | |

| By Application | Broadband Internet |

| Pay-TV Video | |

| Voice-over-Cable (VoC) | |

| Enterprise Services (Business/Data Backhaul) | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

How fast is the Hybrid Fiber Coaxial market expected to grow through 2030?

The market is projected to expand from USD 14.96 billion in 2025 to USD 21.58 billion in 2030, representing a 7.60% CAGR.

Which component category currently holds the largest share of HFC spending?

Optical Nodes lead with 34.27% share in 2024 because they are the pivotal fiber-coax interface that dictates network performance.

What is driving DOCSIS 4.0 adoption among North American cable operators?

Demand for symmetric multi-gigabit tiers, government subsidies that permit HFC in high-cost zones, and node+0 architecture benefits accelerate DOCSIS 4.0 roll-outs.

Which application segment is forecast to grow the quickest?

Enterprise Services are projected to post an 8.89% CAGR as operators integrate edge compute and managed networking solutions.

Why are GaN amplifiers important to future HFC upgrades?

GaN devices enable spectrum extension to 1.8–3 GHz, support node+0 topologies and reduce long-term maintenance, despite higher upfront cost and power draw.

Which region is expected to be the fastest growing for HFC by 2030?

South America, supported by urbanization and subsidy programs, is forecast to register an 8.34% CAGR during the period.

Page last updated on: