Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

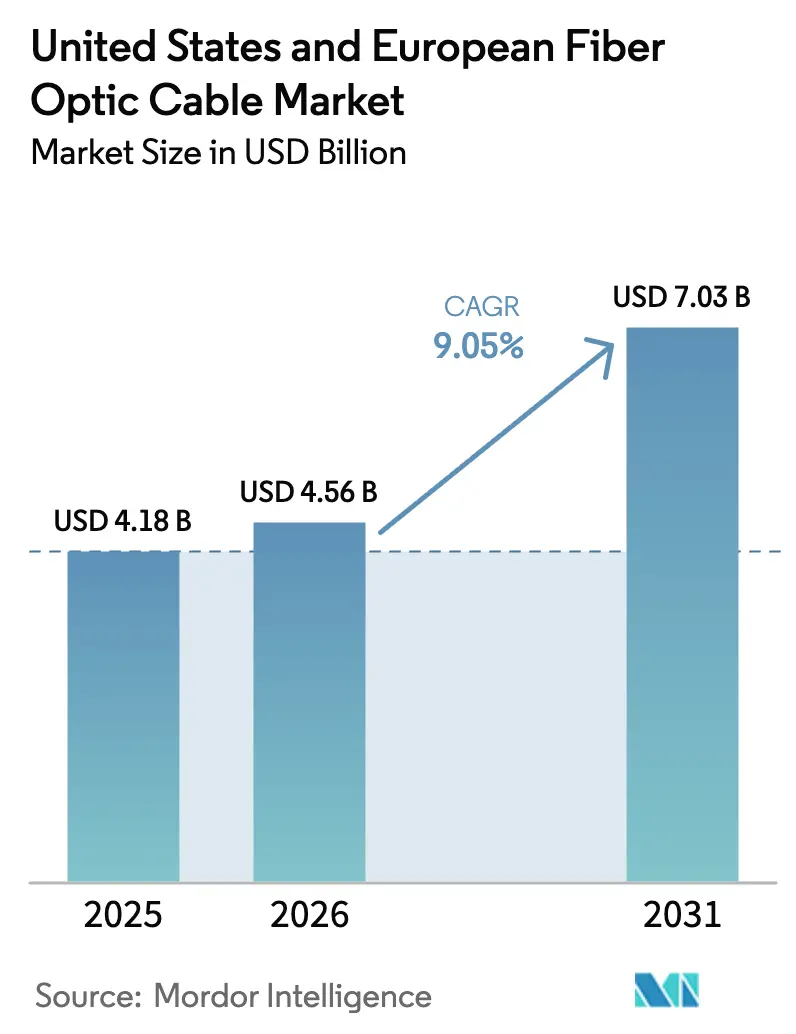

| Base Year Market Size (2025) | USD 4.18 Billion |

| Market Size (2026) | USD 4.56 Billion |

| Market Size (2031) | USD 7.03 Billion |

| Growth Rate (2026 - 2031) | 9.05% CAGR |

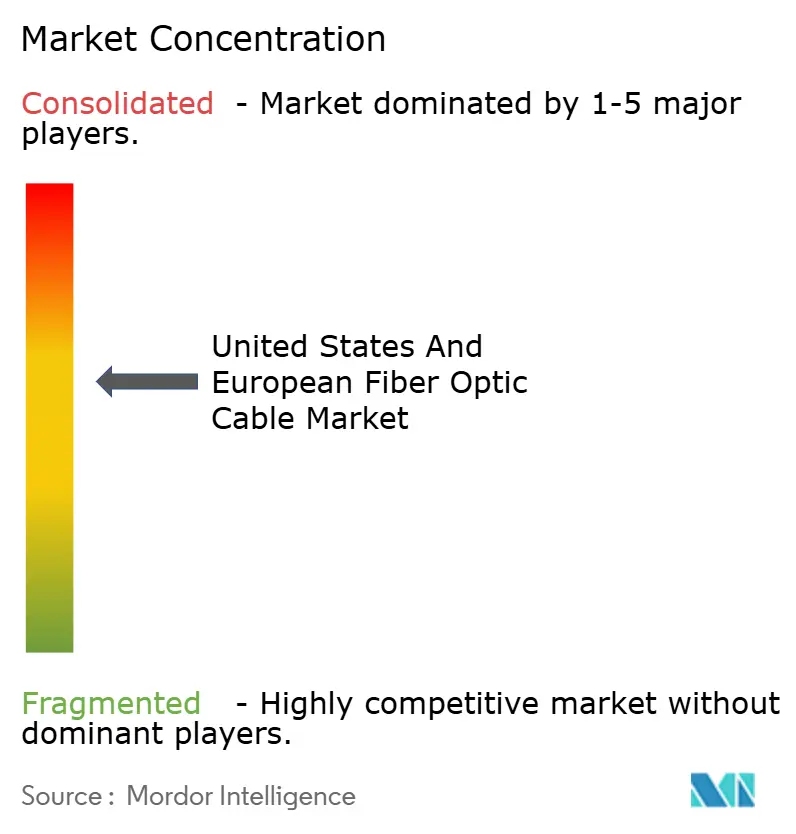

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States And European Fiber Optic Cable Market Analysis by Mordor Intelligence

The United States and European Fiber Optic Cable Market size in 2026 is estimated at USD 4.56 billion, growing from 2025 value of USD 4.18 billion with 2031 projections showing USD 7.03 billion, growing at 9.05% CAGR over 2026-2031. Accelerated 5G densification, government broadband stimulus, and AI-centric hyperscale data centers are synchronizing spending cycles, driving long-haul, metro, and in-building deployments. Stimulus packages such as the USD 42.45 billion BEAD program and the European Union’s Digital Decade plan deliver clear long-term demand visibility, while neutral-host and utility dark-fiber models unlock incremental opportunities for manufacturers able to supply specialty assemblies. Submarine investments by hyperscalers, including Meta’s Project Waterworth, are catalyzing technical shifts toward ultra-low-loss G.654.E fibers, and a persistent shortage of skilled splice technicians is tightening project timelines but sustaining pricing power for integrators with turnkey field services.

Key Report Takeaways

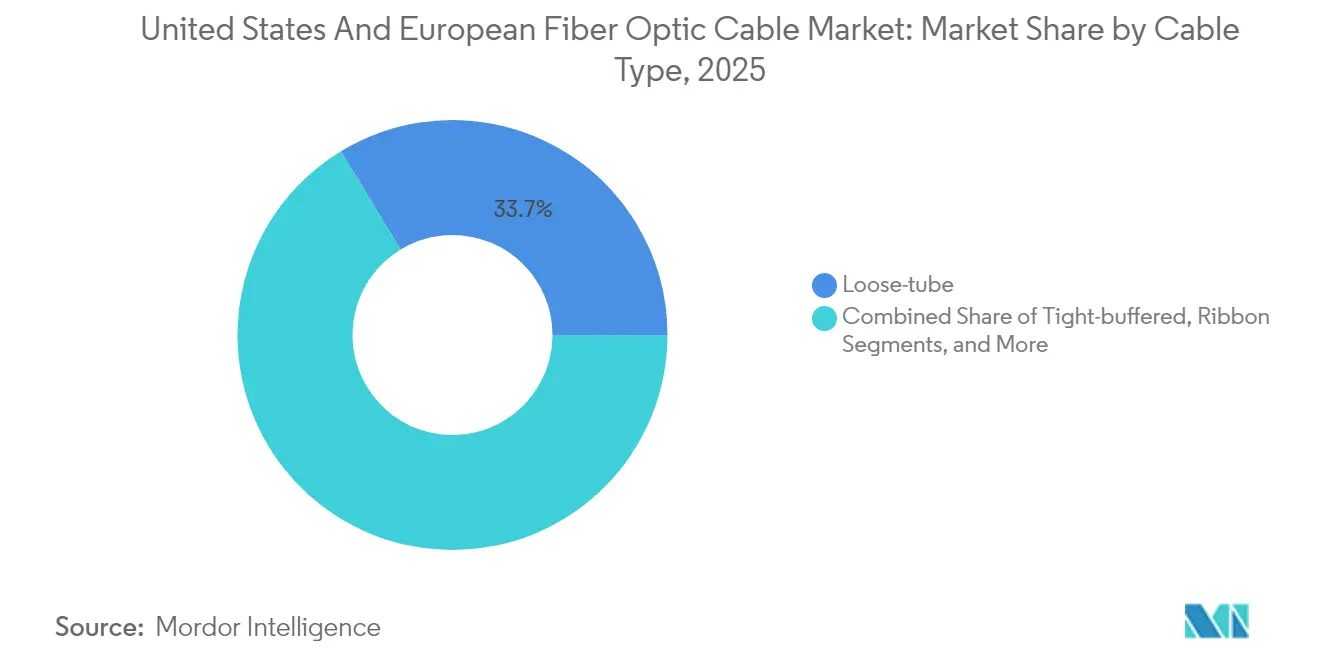

- By cable type, loose-tube products captured 33.68% revenue share of the fiber optic cable market in 2025; tight-buffered variants are forecast to advance at a 9.54% CAGR through 2031.

- By mode, single-mode solutions held 60.92% of the fiber optic cable market share in 2025, whereas multi-mode offerings posted the highest projected CAGR of 9.41% during 2026-2031.

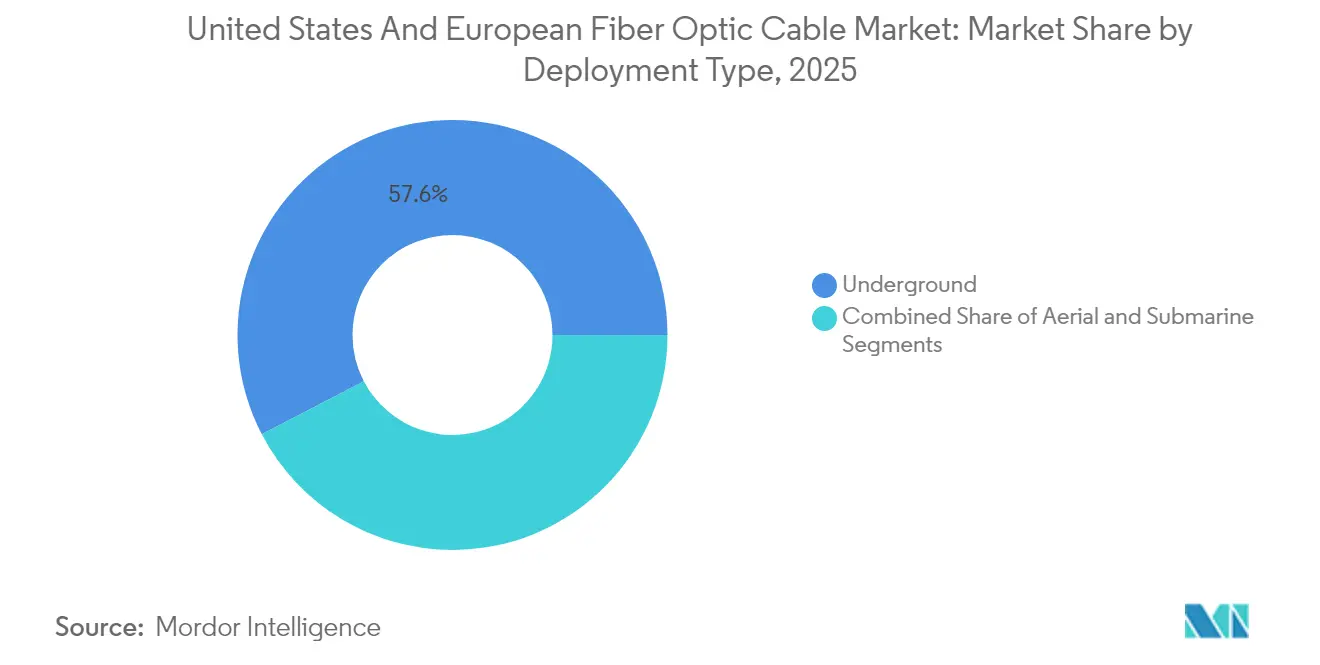

- By deployment type, underground installations accounted for 57.64% of the fiber optic cable market size in 2025; submarine systems are positioned to grow at a 9.78% CAGR through 2031.

- By end-user industry, telecommunications dominated with a 65.71% share in 2025, and it is expanding at a 9.95% CAGR outlook through 2031.

- By country, the United States led with 38.12% of the total 2025 value and is forecast to expand at a 10.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States And European Fiber Optic Cable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging data traffic and cloud workloads | +2.1% | North American and EU hyperscale clusters | Medium term (2-4 years) |

| Accelerated FTTH and 5G rollout investments | +1.8% | EU39 nations, US rural corridors | Medium term (2-4 years) |

| Government broadband stimulus (US BEAD/EU Digital Decade) | +1.5% | United States, Germany, France, Italy, Spain | Short term (≤ 2 years) |

| Adoption of ultra-low-loss single-mode fibers | +1.2% | Global subsea and long-haul routes | Long term (≥ 4 years) |

| Open-RAN neutral-host densification needs dark fiber | +0.9% | Dense urban areas in US and EU | Medium term (2-4 years) |

| Utility-owned fiber commercialization for grid modernization | +0.8% | North America, Northern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Data Traffic and Cloud Workloads

Hyperscale data centers dedicated to AI training clusters are consuming high-density ribbon assemblies at an unprecedented pace, reflecting east-west traffic patterns that copper links cannot support. Meta’s Project Waterworth and Amazon’s Ireland-US cable exemplify multibillion-dollar commitments to private backbone infrastructure that prioritize 400 G and 800 G optical lanes. Connector lead times exceed 16 weeks for MPO/MTP formats, illustrating a tightening supply environment that strengthens the hand of vertically integrated suppliers [1]CABLExpress Editorial Team, “Navigating the MTP/MPO Component Shortage with CABLExpress,” cablexpress.com. Ultra-low-loss G.654.E fibers are gaining traction because they reduce regeneration sites across ocean spans, thereby decreasing the total cost of ownership for cloud operators. As a result, manufacturers capable of delivering specialty tight-buffered and ribbon designs optimized for AI workloads secure premium pricing while broadening recurring services revenue from on-premise moves, adds, and changes.

Accelerated FTTH and 5G Rollout Investments

EU39 fiber coverage rose to 74.6% by September 2024, with Germany adding 3.8 million premises and the United Kingdom passing 4.2 million during that period. Competitive overbuilds by Delta Fibre, Open Dutch Fibre, and KPN’s Glaspoort drove the Netherlands to an 88% household coverage milestone. In parallel, millimeter-wave 5G densification depends on dark-fiber backhaul to small-cell clusters, prompting mobile network operators to co-deploy FTTH and 5G assets to amortize trenching costs. Infrastructure sharing and neutral-host tower models lower barriers for alternative operators, while multitenant data centers leverage the same conduit systems to integrate meet-me rooms. This convergence accelerates order pipelines for cable makers that maintain modular product portfolios adaptable to both aerial and underground pathways.

Government Broadband Stimulus Programs

The USD 42.45 billion BEAD initiative prioritizes fiber-first build plans, effectively sidelining fixed-wireless proxies in federally funded US rural deployments. Parallel Digital Decade policies mandate universal gigabit access across the European Union by 2030, complemented by Germany’s EUR 1.2 billion Gigabitförderung 2.0 grants and France’s successive national rollouts. Build America Buy America content provisions protect domestic cable plants, granting incumbents such as Prysmian’s North American factories preferred supplier status. State broadband offices’ milestone-based disbursement schedules improve cash-flow predictability, allowing cable producers to optimize furnace utilization rates and negotiate longer quartz supply contracts. Collectively, these programs underpin a predictable multi-year revenue runway for US and European manufacturers with compliant product credentials.

Adoption of Ultra-Low-Loss Single-Mode Fibers

G.654.E designs deliver attenuation below 0.16 dB/km, extending repeater spacing to 100 km on subsea routes while supporting 100G/λ coherent modulation [2]Molex Engineering, “Smarter Data Center Scaling with High-Density Connectors,” molex.com. As Meta, Google, and AWS pursue private transatlantic links, ultra-low-loss specifications become baseline requirements, prompting suppliers to invest in advanced vapor-deposition preform lines. Similar upgrades spill into terrestrial long-haul builds where Tier-1 carriers aim to slash amplifier expenditures. Early adopters command a pricing premium supported by quantifiable capex savings at the network-owner level. The technical barrier narrows the vendor field to a handful of players with proprietary doping profiles and tight furnace-temperature control, reinforcing existing market concentration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High civil-works and right-of-way costs | -1.4% | Dense urban cores in US and Western Europe | Short term (≤ 2 years) |

| Competition from fixed-wireless and satellite | -0.8% | Rural spots, low-density districts | Medium term (2-4 years) |

| Skilled labor shortage for splicing | -0.6% | Global, acute in North America | Medium term (2-4 years) |

| Volatility in glass-preform supply chain | -0.5% | China, Japan, US manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Civil-Works and Right-of-Way Costs

Underground construction reached USD 18.25 per foot in 2024, a 12% leap attributed to labor inflation and lengthy permitting cycles in dense metros [3]Fiber Broadband Association & Cartesian, “U.S. Fiber Construction Cost Study 2024,” fiberbroadband.org. Civil works represent up to 80% of project budgets, compelling operators to pursue micro-trenches and conduit reuse strategies. Aerial placement, priced at USD 6.55 per foot, remains attractive but faces European mandates for burial to preserve streetscapes. These dynamics tilt the playing field toward incumbents holding legacy pole-attachment rights and pre-existing ducts, deterring greenfield overbuilds and moderating competitive intensity in mature ZIP codes.

Competition from Fixed-Wireless and Satellite Broadband

Starlink surpassed 4 million subscribers by 2025, validating low-Earth-orbit broadband for low-density locales where fiber penetration is economically prohibitive. Concurrently, 5G fixed wireless delivers gigabit throughput in suburban clusters using existing macro tower footprints, compressing payback periods compared with trench-based FTTH. While latency and capacity ceilings persist for satellite and wireless modalities, they still siphon off the most price-sensitive residential subscribers, lowering penetration projections for select rural fiber projects. Cable manufacturers mitigate risk by targeting enterprise, wholesale, and dark-fiber leases where fiber’s deterministic performance remains irreplaceable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cable Type: Tight-Buffered Lines Up Indoor Upside

Loose-tube designs maintained a 33.68% revenue lead within the fiber optic cable market in 2025, owing to moisture-blocked constructions ideal for outdoor ducts and aerial spans. This segment capitalizes on government-funded rural builds, where extended temperature swings demand gel-filled or dry-core loose-tube formats for long-term reliability. Demand ties closely to statewide broadband grants that prioritize buried networks over wireless substitutes, enabling predictable furnace loading at domestic facilities owned by incumbents.

Hyperscale and colocation operators, however, are accelerating procurement of tight-buffered assemblies that demonstrate a 9.54% CAGR to 2031, reflecting growing intra-data-hall deployments where bend-insensitive jacketing and 900-µm coatings reduce installation time. Port counts per rack have tripled in AI clusters, and ribbonized tight buffers ease mass-fusion splicing to pre-terminated MPO trunks, attracting price premiums amid ongoing connector shortages. As GPU expansion favors multi-tenant buildings located near renewable energy, the cable mix skews toward flame-retardant plenum ratings, prompting vendors to retool jacketing lines for lower-toxicity compounds.

By Mode: Multi-Mode Reclaims Short-Reach Relevance

Single-mode solutions controlled 60.92% of 2025 revenue, given their long-haul reach and future-proof bandwidth for FTTH, metro, and subsea backbones. Government subsidies cement single-mode dominance for access loops where 1 Gbps services are baseline. Operators deploy standard G.652.D or bend-tolerant G.657.A2 cores to extend the life cycles of new plant investments.

Multi-mode fiber volumes are set for a 9.41% CAGR through 2031 as OM4/OM5 variants support 400G SR8 and 800G SR4 lanes inside hyperscale leaf-spine fabrics. Parallel-optic architectures limit reach to 150 m but slash transceiver costs, reclaiming share in data halls. Vendors respond with graded-index profiles optimized for 850 nm VCSEL sources that improve modal dispersion, tightening spec tolerances. The trend lifts overall volume for short-reach jumpers, enhancing factory utilization rates between long-haul campaign runs and helping buffer revenue cyclicality inherent in carrier capex cycles.

By Deployment Type: Subsea Systems Lift Growth Premium

Underground construction held 57.64% of 2025 spending because most EU jurisdictions mandate buried new builds for safety and aesthetics. Municipal dig-once rules and conduit-sharing policies reduce incremental costs, yet labor shortages push project timelines beyond statutory disbursement milestones in select German Länder, incentivizing micro-trenching and HDD techniques. Service providers focus on duct standardization to streamline fiber-sensing upgrades for grid and traffic management in future smart-city pilots.

Submarine builds post the fastest 9.78% CAGR through 2031, propelled by hyperscale content providers bypassing carrier consortium models. Meta’s Project Waterworth and Google’s Nuvem adopt 24-fiber pairs with space-division multiplexing that drive composite pull tensions above legacy limits, demanding new steel-wire armoring compositions. Cable yards in the United States and France accelerate G.654.E qualification to meet post-quantum encryption overhead, while European bankers expand green-bond frameworks covering subsea sustainability metrics, thus diversifying funding sources for future Atlantic and Nordic routes.

By End-User Industry: Telcos Remain Anchor Tenant

Telecommunications accounted for 65.71% of 2025 revenue and is projected to post a 9.95% CAGR, underwritten by dual-track FTTH and 5G backhaul plans targeting symmetrical gigabit experiences. Subsidies lower hurdle rates, allowing regional ISPs to pre-order multi-year fiber volumes that stabilize factory lines and justify quartz furnace expansions. Incumbent telcos also upgrade inter-central-office rings to 800G ZR+ pluggable optics, stimulating demand for ultra-low-loss trunks already qualified for subsea use, thereby spreading R&D amortization across segments.

Utilities, defense agencies, manufacturers, and medical OEMs diversify the customer base, capturing incremental volumes in high-margin specialty niches. Grid-modernization grants let electric companies commercialize surplus fibers along transmission corridors, creating new dark-fiber revenues and sparking orders for armored OPGW cables. Defense ministries specify hermetically sealed tactical reels resistant to electromagnetic pulses, while minimally invasive surgical devices integrate biocompatible silica strands for real-time imaging. These pockets cushion cyclical swings in carrier capex and support sustained R&D around coating chemistries and geometry tolerances.

Geography Analysis

The United States commanded a 38.12% share of 2025 spending with a 10.46% CAGR outlook, reflecting the fiber-first orientation of the BEAD program and the Build America Buy America preference for domestic sources. Hyperscale clusters in Virginia, Oregon, and Texas trigger continuous pull orders for pre-terminated trunks, while Midwestern rural electrification cooperatives leverage USDA loans to wire underserved counties. Domestic manufacturers benefit from stable quartz sourcing contracts and an on-shored preform ecosystem that insulates them from Asian export controls on high-purity silica.

Germany is Europe’s largest single market, fueled by EUR 1.2 billion Gigabitförderung 2.0 grants that shorten payback periods for altnets expanding into second-tier cities. The United Kingdom trails closely, adding 4.2 million premises in 2024 amid aggressive competition between CityFibre, Openreach, and Virgin Media O2, which accelerates duct leasing opportunities for dark-fiber specialists. France, Italy, and Spain deliver steady contributions via national broadband strategies aligned with the EU connectivity toolbox that streamlines permitting and mandate conduit sharing.

Smaller European economies, the Netherlands, Austria, Switzerland, and Nordic states, show above-average penetration owing to high GDP per capita and municipal ownership models that reinvest returns into incremental rural runs. The Netherlands’ 88% household coverage milestone raises marginal deployment costs as operators tackle complex brownfield builds in historic city centers. Nordic utilities exploit long rights-of-way along power corridors for bundled OPGW, while Swiss carriers harness existing rail rights-of-way to lower civil-works costs. Collectively, these geographies maintain robust demand for specialty outdoor ribbons, snow-shedding jacketing, and low-temperature bend-insensitive cores.

Competitive Landscape

Prysmian Group’s USD 950 million purchase of Encore Wire expands its North American installation accessories and copper cable footprint, positioning the firm to bundle electrical wire with fiber bundles in BEAD-funded projects. Nokia’s 2025 acquisition of Infinera forms a USD 2.4 billion optical entity with combined coherent transceiver and subsea repeater assets, enabling bundled bids on turnkey submarine and terrestrial long-haul contracts. Belden, CommScope, and Corning deepen vertical integration across jacketing compounds, fiber draw towers, and factory-terminated assemblies, raising entry barriers for niche rivals.

Technology differentiation now centers on producing ultra-low-loss G.654.E cores and MPO-16/24 high-density connectors validated to IEC 61754-7 specs. Proprietary vapor-axial deposition furnaces guard intellectual property and demand capital intensity, reinforcing moderate market concentration. Supply-side risks linger around helium shortages for draw towers and fluctuating germanium prices used as dopants, but integrated players mitigate exposure through multi-year supply agreements. Skilled-labor shortages in field splicing intensify demand for plug-and-play modules, favoring companies with factory pre-termination capabilities and nationwide technician networks.

White-space growth appears in medical, defense, and power-utility niches where stringent certifications (ISO 13485, MIL-DTL-38999, IEEE Std 1596) permit premium pricing. AFL and Clearfield target these segments with hermetic coatings and hardened terminals, capturing value beyond commodity long-haul strands. Meanwhile, European players partner with local construction firms to ensure Build-and-Transfer contract compliance, bundling warranty services that lock in annuity-like maintenance fees.

United States And European Fiber Optic Cable Industry Leaders

Prysmian Group

Corning Inc.

Nexans SA

CommScope Holding Company Inc.

Furukawa Electric Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Meta unveiled Project Waterworth, a transatlantic cable exceeding USD 2 billion that will employ ultra-low-loss G.654.E fibers.

- February 2025: Nokia finalized the acquisition of Infinera, creating a sizeable optical networking vendor with expanded subsea competencies.

- January 2025: Prysmian Group completed the acquisition of Encore Wire for USD 950 million, broadening its North American portfolio and strengthening bid eligibility for BEAD contracts.

- January 2025: Amazon Web Services confirmed a USD 1.5 billion Ireland-to-US subsea link focused on dedicated cloud connectivity.

United States And European Fiber Optic Cable Market Report Scope

Fiber optic technology transmits data by highly flexible, transparent extruded glass or plastic fiber. Fibre optic cables incorporate glass threads as thin as human hair, sending messages modulated into light waves. Although these cables are made of glass, they are highly durable and malleable.

The United States and European Fiber Optic Cable Market is segmented by end-user industry (telecommunication, power utilities, defence/military, industrial, and medical) and by country (United States, Germany, Austria, Switzerland, and the Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Cable Type

| Loose-tube |

| Tight-buffered |

| Ribbon |

| Armoured |

By Mode

| Single-mode |

| Multi-mode |

By Deployment Type

| Underground |

| Aerial |

| Submarine |

By End-user Industry

| Telecommunications |

| Power Utilities |

| Defense and Military |

| Industrial and Manufacturing |

| Medical |

By Country

| United States |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Austria |

| Switzerland |

| Rest of Europe |

| By Cable Type | Loose-tube |

| Tight-buffered | |

| Ribbon | |

| Armoured | |

| By Mode | Single-mode |

| Multi-mode | |

| By Deployment Type | Underground |

| Aerial | |

| Submarine | |

| By End-user Industry | Telecommunications |

| Power Utilities | |

| Defense and Military | |

| Industrial and Manufacturing | |

| Medical | |

| By Country | United States |

| Germany | |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Austria | |

| Switzerland | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the United States and European fiber optic cable market in 2026?

The fiber optic cable market size across these two regions is valued at USD 4.56 billion in 2026.

What is the forecast CAGR for regional fiber deployments through 2031?

Aggregate revenue is expected to grow at a 9.05% CAGR between 2026 and 2031.

Which cable type is growing fastest?

Tight-buffered designs aimed at data center interiors post the highest 9.54% CAGR forecast to 2031.

Why are ultra-low-loss single-mode fibers gaining attention?

G.654.E fibers lower attenuation below 0.16 dB/km, cutting the number of repeaters in long-haul and subsea links and reducing total system cost.

How do government broadband programs influence demand?

The U.S. BEAD and EU Digital Decade initiatives supply multi-year funding that guarantees volume commitments, improving factory utilization rates for cable producers.

Which country leads spending within the studied regions?

The United States holds 38.12% of 2025 regional revenue and continues to outpace Europe, supported by hyperscale data center builds and fiber-first subsidies.

Page last updated on: