Submarine Optical Fiber Cable Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

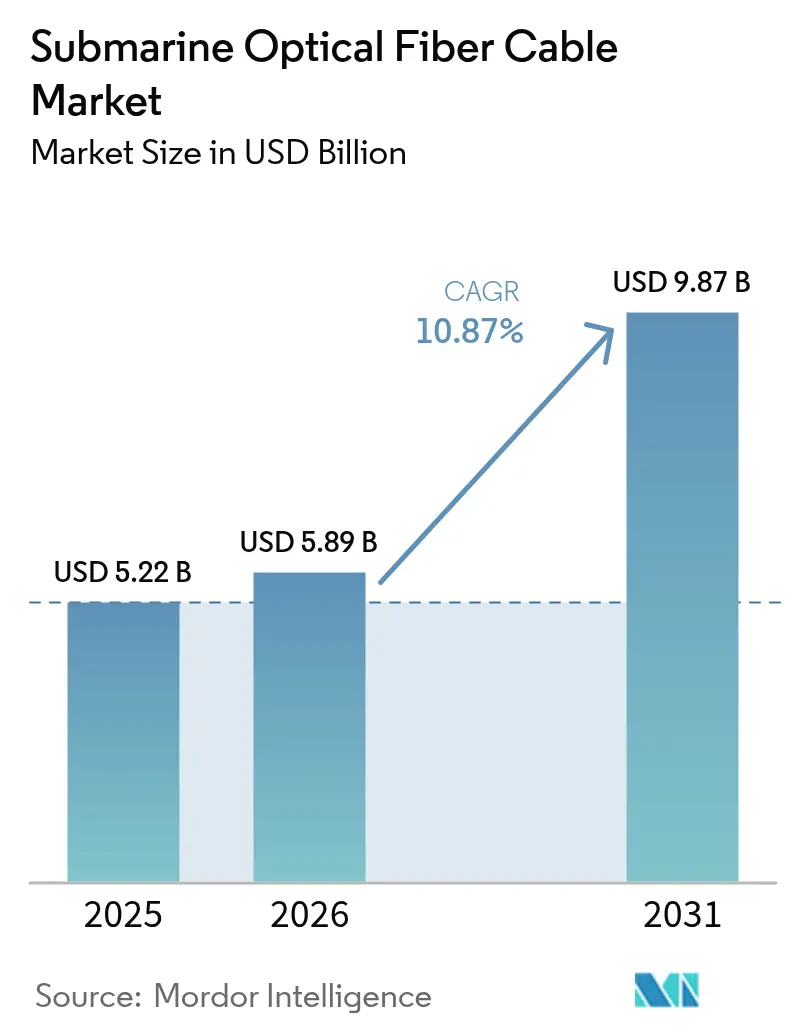

| Market Size (2026) | USD 5.89 Billion |

| Market Size (2031) | USD 9.87 Billion |

| Growth Rate (2026 - 2031) | 10.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Submarine Optical Fiber Cable Market Analysis by Mordor Intelligence

The Submarine Optical Fiber Cable Market size is projected to be USD 5.22 billion in 2025, USD 5.89 billion in 2026, and reach USD 9.87 billion by 2031, growing at a CAGR of 10.87% from 2026 to 2031.

A shift toward privately owned, high-capacity systems is redefining the global connectivity fabric as hyperscale cloud platforms bypass congested carrier-neutral routes, lock in predictable bandwidth costs, and meet the latency requirements of artificial-intelligence applications. Operators are extending cable life through 800 GbE upgrades that raise wavelength rates fourfold while deferring disruptive refurbishments. Demand for rapid-response repair fleets has intensified after a rise in cable-cut incidents, and auxiliary marine services are now expanding faster than hardware sales. Innovation in multi-core and space-division-multiplexing (SDM) fiber points to a long-term capacity roadmap able to support 680 Tbit-s systems demonstrated in 2025

Key Report Takeaways

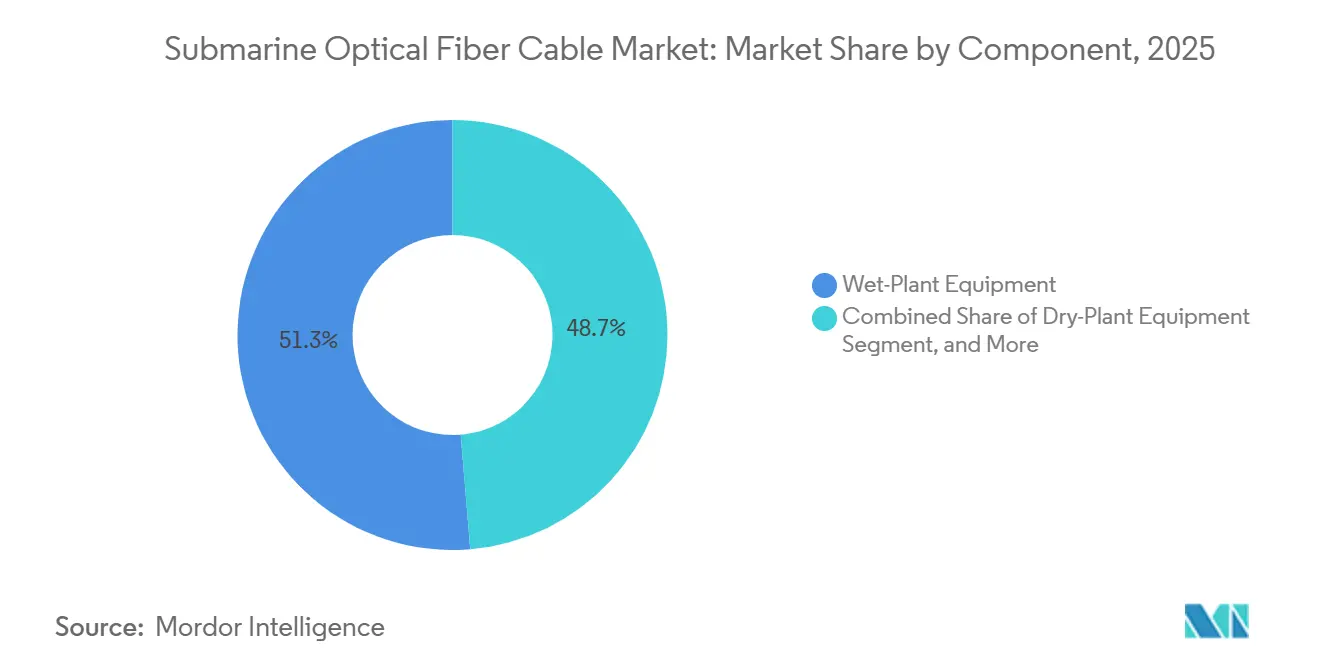

- By component, wet-plant equipment led with 51.32% revenue share in 2025, while auxiliary and marine services are accelerating at an 11.69% CAGR to 2031.

- By cable type, single-mode fiber accounted for 66.32% of the submarine optical fiber cable market share in 2025, whereas SDM/multi-core architectures are projected to grow at a 11.43% CAGR through 2031.

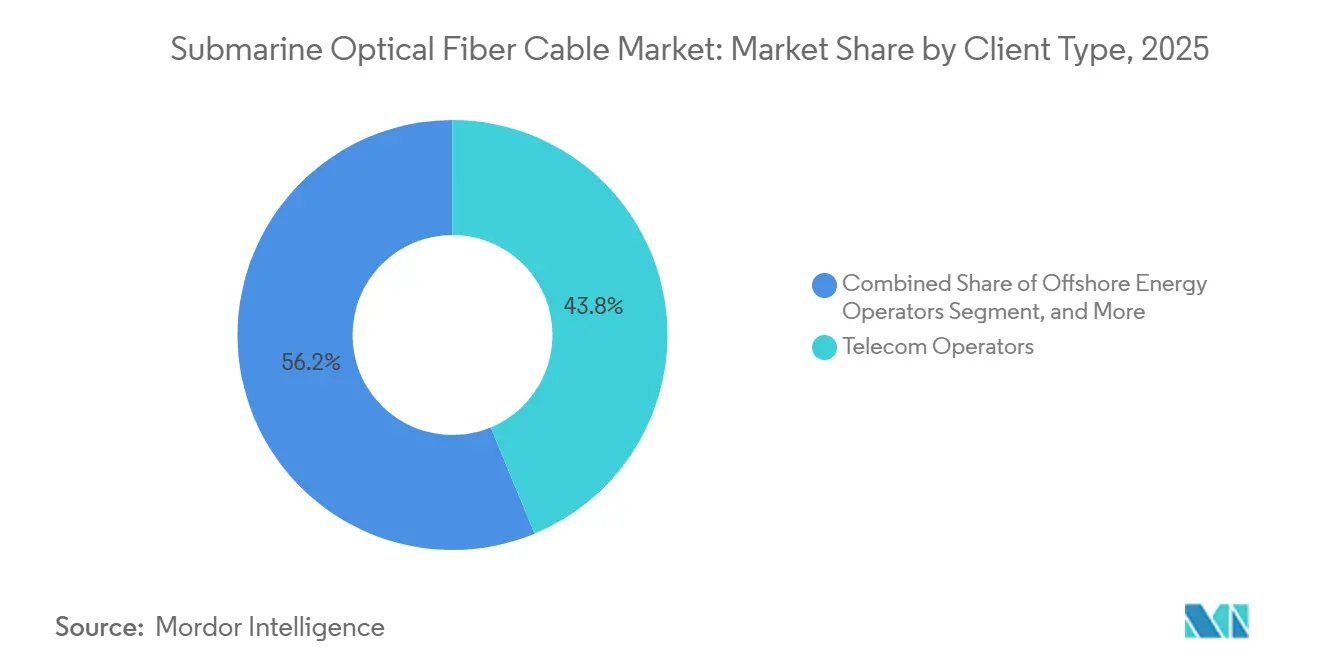

- By client type, telecom operators accounted for 43.76% of revenue in 2025, yet content and hyperscale cloud providers represent the fastest-growing segment, with an 11.84% CAGR to 2031.

- By capacity design, 16-60 Tbit-s systems commanded 49.19% of the submarine optical fiber cable market share in 2025, while systems rated above 60 Tbit-s are projected to log the fastest growth at an 11.37% CAGR through 2031.

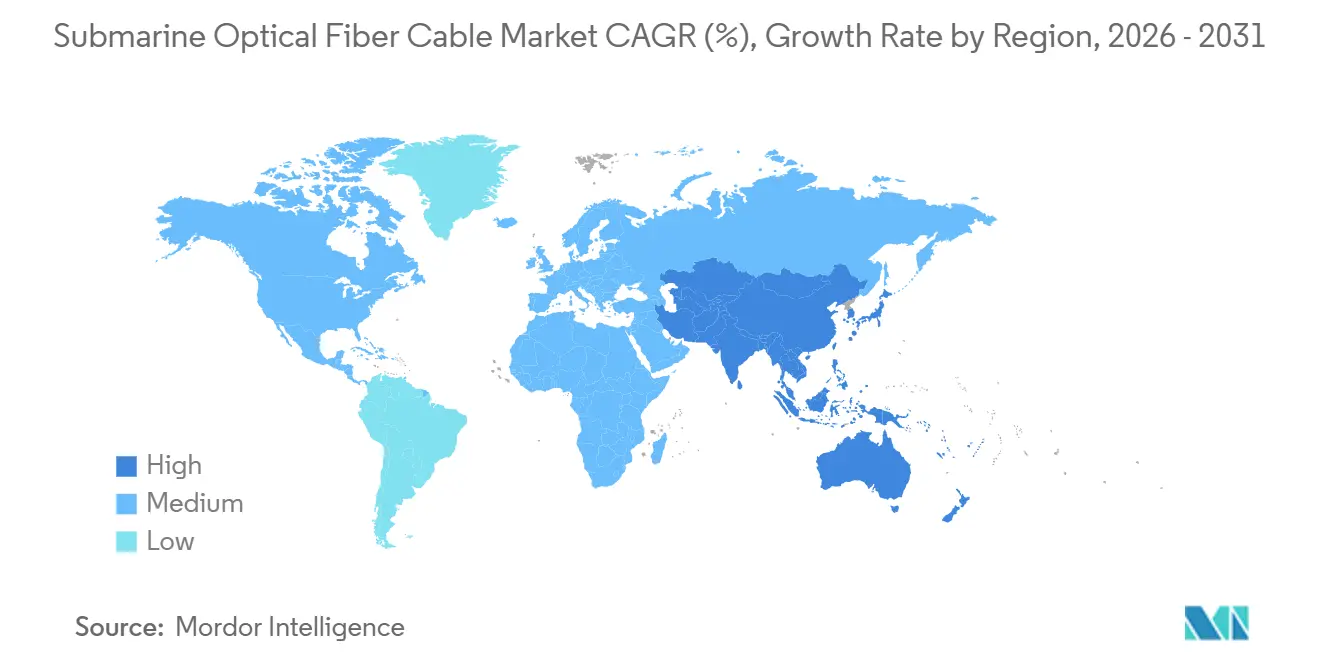

- By geography, Asia-Pacific generated 33.21% of 2025 revenue, while Africa is forecast to advance at a 11.83% CAGR driven by new hyperscale-backed cables.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Submarine Optical Fiber Cable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale Cloud and OTT Investment in Private Cables | +2.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rapid 400 GbE and 800 GbE Upgrade Cycle Among Carriers | +2.3% | Middle East and Asia-Pacific | Short term (≤ 2 years) |

| Growing Smartphone Penetration and Rising Internet Bandwidth Demand | +1.9% | Asia-Pacific, Africa, South America | Long term (≥ 4 years) |

| Increasing Fiber Connectivity in Emerging Regions | +1.6% | Africa, South America, Southeast Asia | Long term (≥ 4 years) |

| Push Toward Low-Latency Trans-polar Routes | +1.2% | Arctic corridors | Medium term (2-4 years) |

| Offshore Wind Farms Adopting Hybrid Power-Data Cables | +0.9% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud and OTT Investment in Private Cables

Content platforms now commission the majority of new trans-oceanic systems. Meta’s 2Africa and Waterworth programs together exceed 90,000 km of route length and secure end-to-end ownership, eliminating bandwidth-lease negotiations.[1]Meta Platforms, “Introducing Waterworth, Our Longest Subsea Cable System,” meta.com Google activated the Dhivaru link between Singapore and the Maldives in 2025 to ensure low-latency replication for AI model training. Amazon obtained landing rights in Ireland for a 100 Tbit-s trans-Atlantic route scheduled for 2027. These moves channel multi-billion-dollar capital flows directly to fiber manufacturers, reshaping supplier power dynamics. Telecom groups respond by repositioning as wholesale landlords rather than end-to-end owners.

Rapid 400 GbE and 800 GbE Upgrade Cycle Among Carriers

Coherent pluggable optics let operators quadruple wavelength throughput on legacy cables. Omantel proved the economics in 2025 by lifting each channel to 800 Gbps with Ciena’s WaveLogic 6 and deferring a USD 200 million rip-and-replace project by at least five years.[2]Ciena Corporation, “WaveLogic 6 Powers Omantel 800 Gb s Upgrade,” ciena.com Altibox has already validated 1.6 Tbit-s single-wavelength trials, hinting at commercial adoption before 2028. Adoption of ITU-T G.654.E low-attenuation fiber in 60% of 2025 tenders further extends span lengths, lowering amplifier counts and operating power budgets.

Growing Smartphone Penetration and Rising Internet Bandwidth Demand

Asia-Pacific monthly mobile data usage climbed to 120 exabytes in 2025, driven by 5G rollouts in India and Indonesia, lifting average per-user consumption above 20 GB.[3]GSMA Intelligence, “Mobile Data Traffic Outlook 2026,” gsma.com Video streaming and cloud gaming dominate traffic and rely on subsea fiber for 99% of intercontinental bandwidth. New assets, such as SEA-ME-WE-6, added 126 Tbit-s to India in 2025, yet even with even utilization, it still peaks at 70%. The shift from text to video means demand now grows faster than subscriber numbers, requiring continuous capacity augmentation even in saturated smartphone markets.

Increasing Fiber Connectivity in Emerging Regions

African and South American governments are joining forces to co-finance subsea projects, aiming to sidestep the high costs of satellite backhauls. In 2024, Nigeria's Equiano made its debut, bringing a whopping 144 Tbit/s of capacity and slashing wholesale prices by 40% in just half a year. Meanwhile, Brazil's Seabras-2 route not only reduced latency to Europe but also spurred the establishment of new content-delivery nodes. While multilateral lenders step in to fill funding gaps, especially when commercial returns extend beyond 7 years, the GDP gains from digital-service exports more than make up for it.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Maintenance and Repair-Ship Costs | −1.4% | Global, remote routes | Short term (≤ 2 years) |

| Growing Investment in LEO Satellite Constellations | −1.1% | Rural North America, Africa, island nations | Medium term (2-4 years) |

| Geopolitical Cable-Landing Permit Delays | −0.8% | South China Sea, Red Sea, Baltic Sea | Short term (≤ 2 years) |

| Fiber-Optic Theft and Vandalism in Shallow Waters | −0.5% | Mediterranean, Malacca Strait, West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Maintenance and Repair-Ship Costs

Deep-water repairs typically range from USD 1 million to 3 million. This cost is influenced by daily vessel charter rates, which hover between USD 0.1 million and 0.3 million, and the unpredictable nature of multi-week weather windows. With only 60 dedicated repair ships available globally, the industry faces significant bottlenecks, especially when multiple vessels encounter faults simultaneously. In 2025, insurers responded to these challenges by increasing premiums by as much as 30% for corridors deemed high-risk. In light of these rising costs and potential downtimes, operators have begun pre-booking standby contracts. While this strategy adds an extra 5-8% to their project budgets, it significantly mitigates the risk of extended downtimes.

Growing Investment in LEO Satellite Constellations

SpaceX’s Starlink exceeded 7,000 satellites by 2025 and delivers 25-50 ms latency, narrowing the performance gap with some subsea paths.[4]SpaceX, “Starlink Network Statistics,” spacex.com Rural consumers, facing the high costs of fiber backhaul, are increasingly turning to satellite broadband, even if each satellite manages only a few tens of gigabits. In response, subsea operators, feeling the pinch of price pressures in these less populated areas, are shifting their focus. They're now emphasizing enterprise-grade Service Level Agreements (SLAs) – a feature that satellites have yet to fully offer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Marine Services Gain Share as Protection Needs Rise

The submarine optical fiber cable market size for wet-plant equipment stood at USD 2.67 billion in 2025, equal to 51.32% of overall revenue, as repeaters and branching units remain the single largest cost block. Yet auxiliary and marine services are growing at 11.69% annually because operators in conflict-prone corridors purchase round-the-clock repair coverage and seabed route audits. That service-centric shift increases recurring revenue and cushions suppliers against the lumpiness of turnkey hardware contracts.

Dry-plant equipment, namely optical line terminals and monitoring platforms, faces commoditization as hyperscalers demand open architectures that disaggregate transport electronics from wet-plant vendors. Smaller niches, including distributed acoustic sensing units that repurpose the fiber itself as a vibration sensor, have emerged after National Grid’s 2024 deployment proved 15% turbine-downtime savings for offshore wind projects. Across components, suppliers diversify into hybrid power-data cables to tap an adjacent USD 500 million addressable pool by 2030.

By Cable Type: SDM and Multi-core Architectures Approach Commercial Readiness

Single-mode designs held 66.32% of 2025 revenue, but multi-core and SDM fiber posted the highest growth at 11.43% as NEC’s 22-core demonstration reached 680 Tbit-s on a single fiber pair. Early deployments remain inside data-center campuses, yet splicing-cost declines to below USD 10,000 per joint, anticipated by 2027, will unlock long-haul adoption. The ITU-T G.654.E low-attenuation specification underpins most new tender documents, enabling amplifier spacing of 400 km and trimming repeater counts by 40% versus legacy G.652.D.

Multimode fiber persists for short offshore-platform hops under 10 km but continues to cede share as single-mode prices fall. Suppliers funnel R&D toward hollow-core variants that promise sub-latency propagation and could complement SDM in the next decade if manufacturing yields stabilize.

By Client Type: Hyperscalers Reshape Demand Patterns

Telecom operators still accounted for 43.76% of 2025 spend, but their share will erode as Meta, Google, Amazon, and Microsoft adopt end-to-end ownership models that bypass wholesale bandwidth markets. Content and cloud providers logged an 11.84% CAGR and already sponsor more than half of announced trans-Pacific projects. Government research networks maintain stable but modest volumes, as exemplified by NORDUnet’s Polar Connect lane, which delivered 10 Tbit/s for Arctic science in 2025.

Offshore energy producers increasingly request custom SLAs that integrate power-cable telemetry. Equinor deployed a 100 Gbps link to its Johan Sverdrup platform in 2024, confirming that real-time reservoir analytics lower personnel exposure and lift uptime. Suppliers now market modular kits that adapt to both hyperscale mega-projects and boutique industrial deployments.

By Capacity Design: Ultra-High Ratings Become Baseline

More than half of new RFPs in 2025 demanded ≥60 Tbit/s systems to future-proof against 8K video, XR collaboration, and AI cluster replication. The submarine optical fiber cable market size for the >60 Tbit-s class is projected to climb at an 11.37% CAGR, while <16 Tbit-s proposals have virtually disappeared from global tenders. Coherent-pluggable progress lets designers meet 60 Tbit-s with only 12 fiber pairs running 800 Gb/s wavelengths, cutting diameter and easing right-of-way congestion.

Because incremental fiber-pair additions during initial lay cost only 10-15% of total capex, CFOs now favor maximum initial capacity to avoid multi-year permitting cycles for mid-life expansion. The practice elevates up-front capital intensity but extends economic lifespan to 20-25 years, aligning depreciation with revenue trajectories.

Geography Analysis

Asia-Pacific led the submarine optical fiber cable market with 33.21% revenue in 2025, driven by the SEA-ME-WE-6’s Mumbai landing and Japan’s USD 300 million JUNO route, which secures disaster-recovery links for Tokyo enterprises. China’s manufacturers remain active but face political headwinds in Australia and the United States, rerouting traffic through Singapore and Hong Kong to comply with national-security screening requirements.

Africa delivers the fastest growth at 11.83% CAGR through 2031. Meta’s 2Africa system now spans the continent with 180 Tbit-s of capacity across 33 landings, slashing wholesale Mbps prices by double digits in Nigeria, Kenya, and South Africa. Lower tariffs stimulate local data-center builds and cloud on-ramp deployments that were impossible under satellite-backed terabit ceilings.

North America sees steady replacement demand as early-2000s cables reach end of life and are upgraded to 800 GbE wavelengths. Europe’s permitting cycle grew longer after Brexit split licensing regimes for cross-Channel landings, while strict EU environmental reviews add 12-18 months to Mediterranean routes. South America diversifies away from its Miami choke point via Brazil-Portugal links such as Seabras-2, creating alternate corridors that lower single-point-failure risk. Middle Eastern traffic remains transit-heavy; operators now deploy Red Sea protection loops to hedge against disruption, and insurers levy higher premiums on Suez passages. Emerging trans-polar routes promise 30% latency cuts between Asia and Europe once Far North Fiber’s 14,000 km link activates in late 2026..

Competitive Landscape

Three vendors, Alcatel Submarine Networks, SubCom, and HMN Technologies, control roughly 60% of global manufacturing capacity, rendering the arena moderately consolidated. Alcatel’s Blue-Raman amplification lengthens repeater spacing to 500 km and trims hardware outlays 15% on ultra-long hauls. SubCom focuses on Arctic-capable vessels and won the USD 500 million Arctic Way contract linking Norway to Alaska in 2027. HMN serves Chinese-financed corridors across the South China Sea and the Indian Ocean but remains constrained by landing permit rejections in several Western markets.

Regional challengers, notably S.B. Submarine Systems in Bangladesh and PT Communication Cable Systems Indonesia, win localized installation jobs through in-country flag-fleets and rapid licensing turnarounds. Global Marine Group and Orange Marine pivot from episodic lay projects to recurring monitoring subscriptions using machine-learning analytics that predict sheath fatigue and anchor-drag threats. Component specialists such as Ciena and Infinera benefit from the open-line-system trend that decouples electronics from wet-plant consortia, allowing carriers to refresh transponders without touching seabed assets.

Patent filings show momentum in hollow-core and multi-core glass, suggesting that material science rather than digital signal processing will unlock the next order-of-magnitude capacity jump. Regulators under the International Cable Protection Committee (ICPC) have standardized seabed-route surveys, compressing differentiation on project engineering and heightening price competition on commoditized segments.

Submarine Optical Fiber Cable Industry Leaders

Alcatel Submarine Networks Ltd

Global Marine Group

HMN Technologies Co., Ltd.

IT International Telecom Inc.

SubCom, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2026: Meta completed the first stage of its 50,000 km Waterworth system with 24 fiber pairs spanning four continents, supplying proprietary capacity for video delivery and AI inference.

- July 2026: Far North Fiber obtained final environmental clearance for a 14,000 km trans-polar cable from Japan to the United Kingdom, with commercial service expected late-2026.

- December 2025: Google and Chile launched the 14,800 km Humboldt system linking South America and Oceania.

- November 2025: Omantel implemented Ciena WaveLogic 6 pluggables across its network, enabling 800 Gb s per wavelength and deferring USD 200 million in replacement spend.

Global Submarine Optical Fiber Cable Market Report Scope

The Submarine Optical Fiber Cable Market Report is Segmented by Component (Wet-Plant Equipment, Dry-Plant Equipment, Auxiliary and Marine Services, Other Components), Cable Type (Single-mode Fiber, Multimode Fiber, SDM/Multi-core Fiber), Client Type (Telecom Operators, Content and Hyperscale Cloud Providers, Government and Research Networks, Offshore Energy Operators, Other Client Types), Capacity Design (≤16 Tbps Systems, 16-60 Tbps Systems, >60 Tbps Systems), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Wet-Plant Equipment |

| Dry-Plant Equipment |

| Auxiliary and Marine Services |

| Other Components |

| Single-mode Fiber |

| Multimode Fiber |

| SDM / Multi-core Fiber |

| Telecom Operators |

| Content and Hyperscale Cloud Providers |

| Government and Research Networks |

| Offshore Energy Operators |

| Other Clinet Types |

| less than or equal to 16 Tbps Systems |

| 16 - 60 Tbps Systems |

| above 60 Tbps Systems |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Wet-Plant Equipment | |

| Dry-Plant Equipment | ||

| Auxiliary and Marine Services | ||

| Other Components | ||

| By Cable Type | Single-mode Fiber | |

| Multimode Fiber | ||

| SDM / Multi-core Fiber | ||

| By Client Type | Telecom Operators | |

| Content and Hyperscale Cloud Providers | ||

| Government and Research Networks | ||

| Offshore Energy Operators | ||

| Other Clinet Types | ||

| By Capacity Design | less than or equal to 16 Tbps Systems | |

| 16 - 60 Tbps Systems | ||

| above 60 Tbps Systems | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the expected value of the submarine optical fiber cable market in 2031?

It is forecast to reach USD 9.87 billion by 2031, growing at a 10.87% CAGR from 2026.

Which segment shows the fastest growth within the submarine optical fiber cable market?

Auxiliary and marine services, advancing at an 11.69% CAGR as operators prioritize rapid-response repair and seabed-route consulting.

Why are hyperscale cloud companies building their own cables?

Private ownership secures predictable bandwidth, reduces latency for AI workloads, and eliminates recurring lease fees, supporting long-term cost efficiency.

How does SDM / multi-core fiber improve capacity?

By placing multiple cores in a single strand, SDM lifts total throughput ten-fold over current single-mode designs, enabling 680 Tbit-s systems validated by NEC in 2025.

What makes Africa the fastest-growing region for subsea cables?

New systems such as 2Africa and Equiano deliver high-capacity, low-cost bandwidth that stimulates cloud adoption and data-center construction across the continent.

Do LEO satellites threaten the subsea cable business?

Satellites offer useful rural backhaul but lack the terabit-scale capacity of fiber, so they complement rather than replace undersea infrastructure.

Page last updated on: