Hunter Syndrome Treatment Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

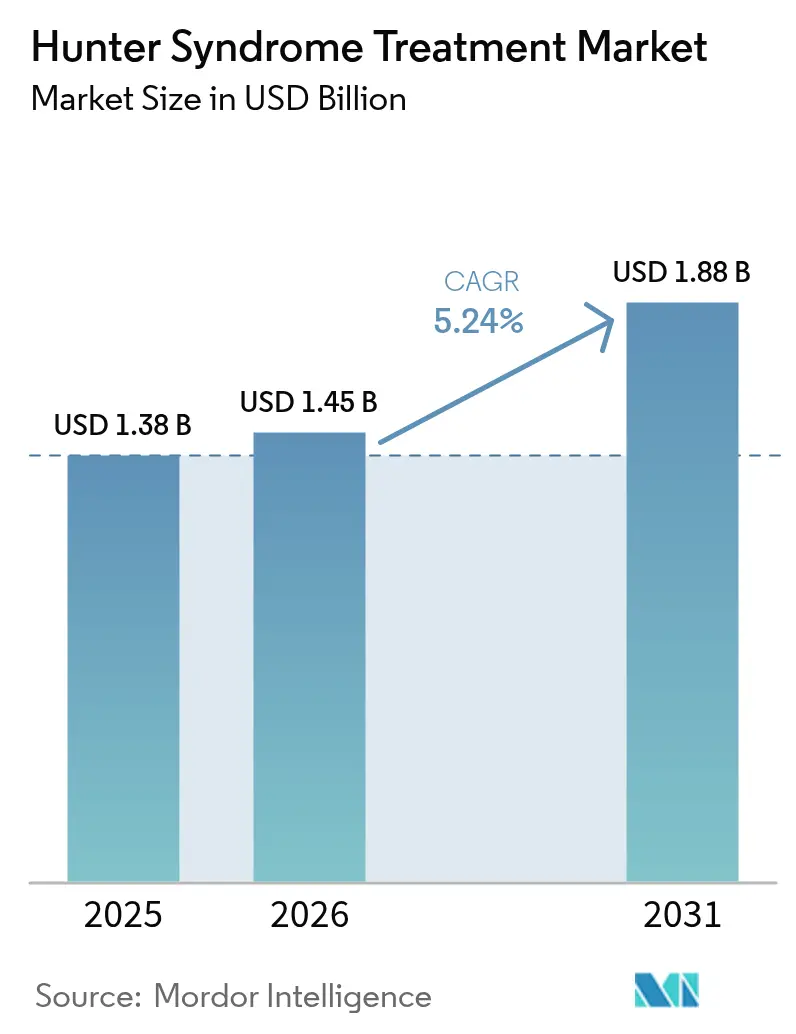

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 1.88 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

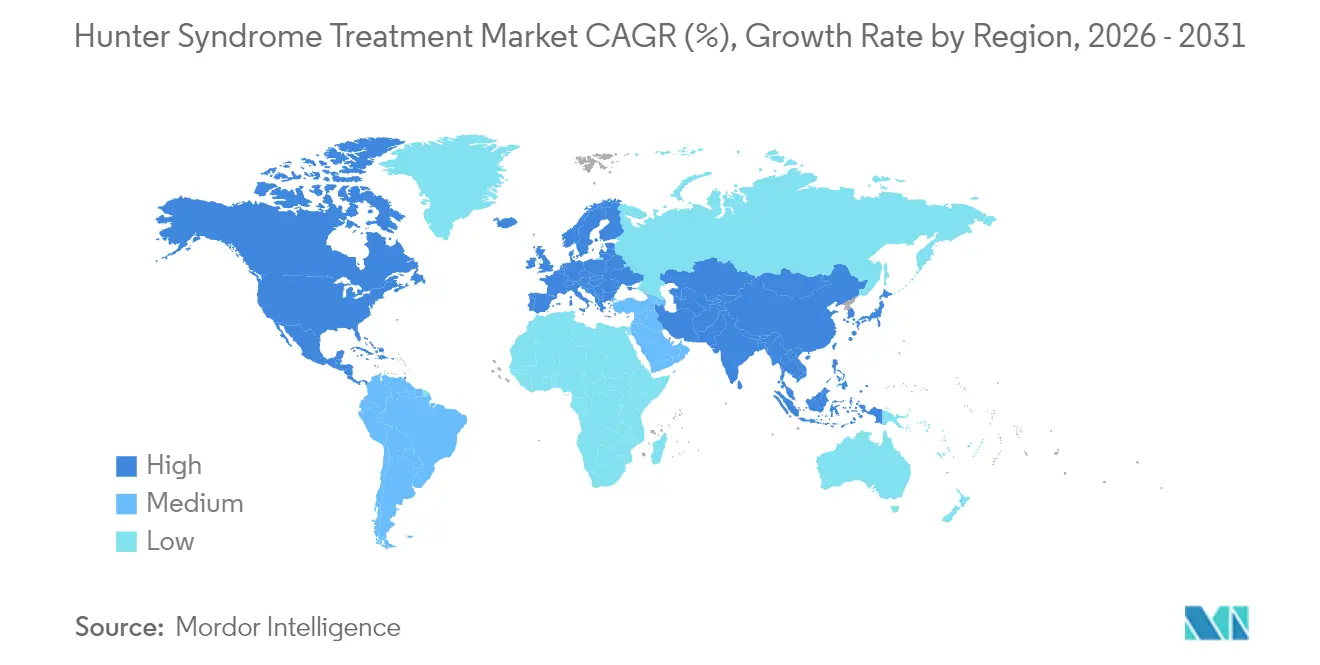

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hunter Syndrome Treatment Market Analysis by Mordor Intelligence

The Hunter syndrome treatment market size is expected to grow from USD 1.38 billion in 2025 to USD 1.45 billion in 2026 and is forecast to reach USD 1.88 billion by 2031 at 5.24% CAGR over 2026-2031. Robust orphan-drug incentives, accelerating approvals for blood-brain barrier (BBB)-penetrant enzyme replacement therapies (ERTs) and gene therapies, and the steady expansion of newborn screening programs underpin the upward trajectory of the Hunter syndrome treatment market. Enzyme replacement therapy (ERT) remains the revenue cornerstone. Yet, its neurological limitations have opened space for adeno-associated virus (AAV) and lentiviral vector gene therapies that promise durable central nervous system (CNS) benefits. Competitive intensity is rising as small innovators partner with large pharmaceutical companies to secure manufacturing scale and regional commercial know-how. Finally, home-infusion models are gaining traction because they cut administration costs and improve patient convenience, reinforcing overall demand.

Key Report Takeaways

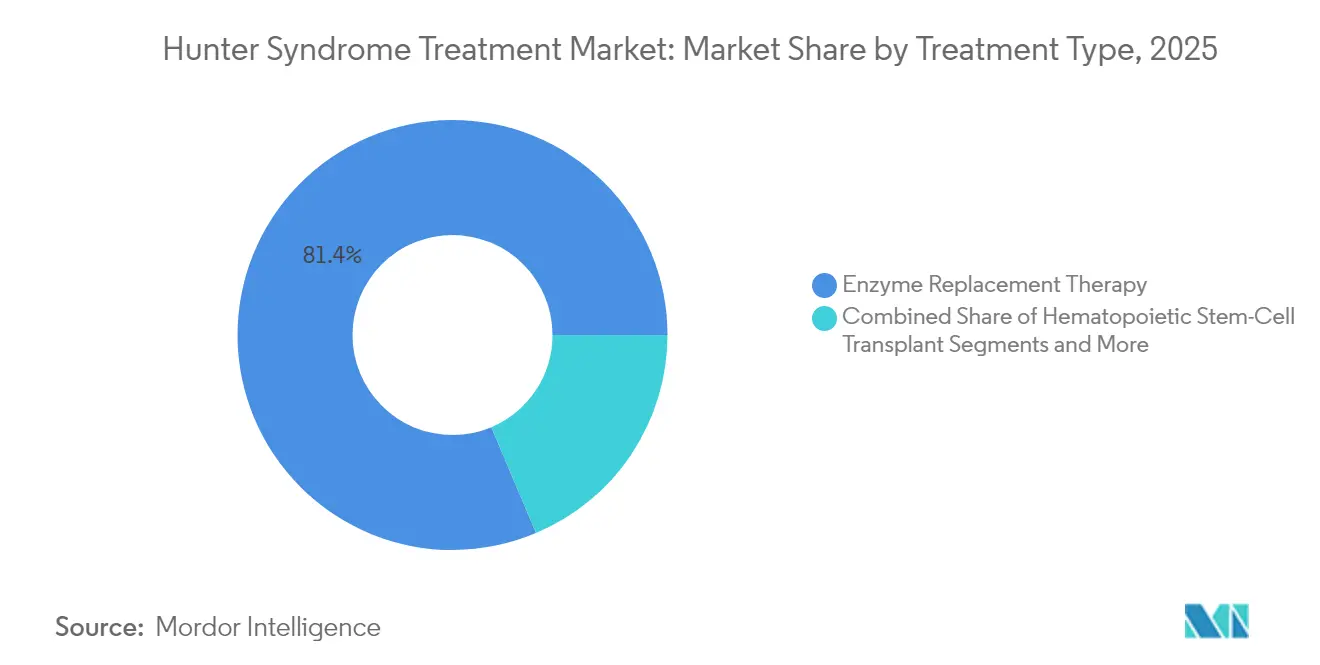

- By treatment type, enzyme replacement therapy commanded 81.35% of the Hunter syndrome treatment market share in 2025; gene and other advanced therapies are expanding at a 7.06% CAGR to 2031.

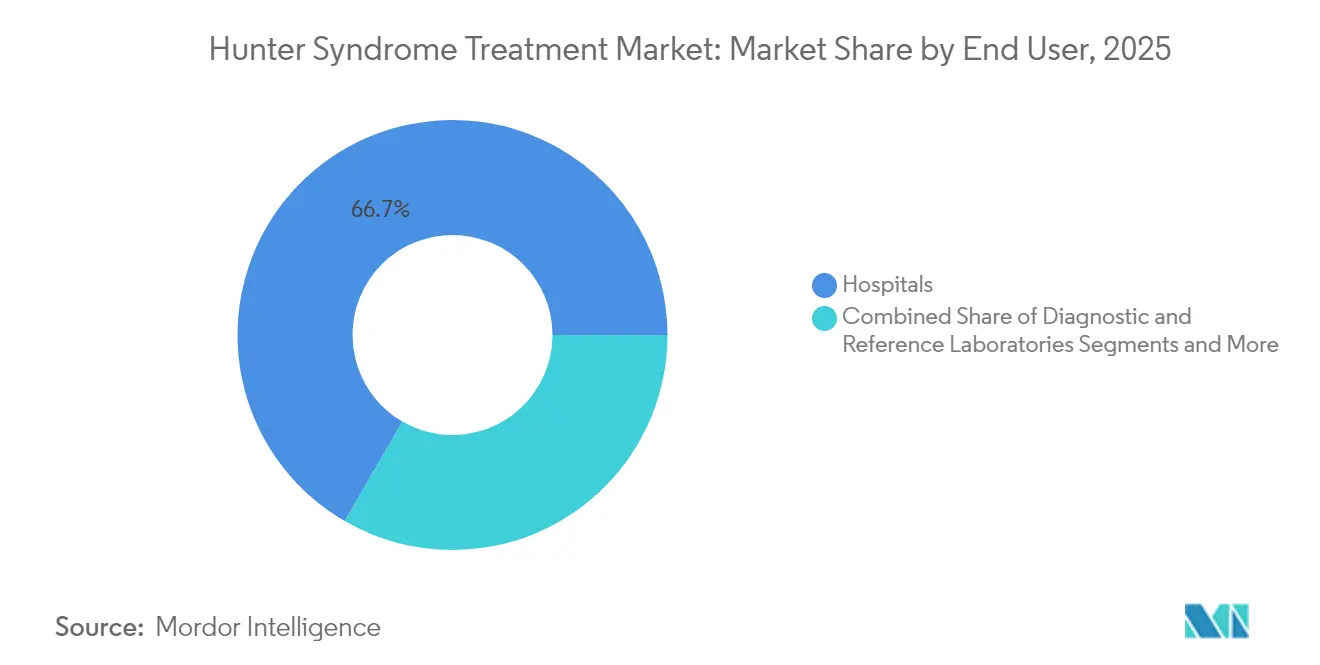

- By end user, hospitals held 66.65% of the Hunter syndrome treatment market share in 2025, while home-infusion and specialty clinics are set to grow at a 6.21% CAGR through 2031.

- By geography, North America led with 37.25% Hunter syndrome treatment market share in 2025; Asia Pacific is projected to post an 8.08% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hunter Syndrome Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Orphan-Drug Incentives & Pricing Power | +1.80% | North America & EU | Long term (≥ 4 years) |

| Expanding Government Rare-Disease Funding Programs | +1.20% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Commercial Launch Of BBB-Penetrant ERTs | +1.50% | Global | Short term (≤ 2 years) |

| Accelerating AAV9 & LV-Based Gene-Therapy Pipeline | +0.80% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Newborn-Screening Panel Inclusion For MPS II | +0.60% | North America & EU, expanding globally | Medium term (2-4 years) |

| Growth Of Home-Infusion Service Models | +0.40% | Global, led by developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Orphan-Drug Incentives & Pricing Power

Orphan designations confer market exclusivity—seven years in the United States and ten years in Europe, allowing sponsors to recoup high R&D costs from an ultra-small patient base.[1]Food and Drug Administration, “Orphan Drug Act—Exclusivity,” fda.govIn 2024, specialty-drug approvals represented more than 80% of all new U.S. medicines, underscoring the environment’s attractiveness to developers. Priority Review Vouchers deepen the appeal: Takeda’s hemophilia candidate ALHEMO secured one in December 2024, a transferrable asset that can shorten another drug’s regulatory review by four months. High list prices remain politically sensitive, but congressional proposals to soften Inflation Reduction Act provisions for sole orphan drugs signal continued legislative support. Consequently, pricing power is unlikely to erode materially over the 2025-2030 horizon, sustaining positive pressure on the Hunter syndrome treatment market.

Expanding Government Rare-Disease Funding Programs

Targeted grants stimulate discovery and translational science. The NIH PAR-25-266 call reserves resources for “high-value newborn-screen-eligible disorders,” explicitly citing mucopolysaccharidoses.[2]National Institutes of Health, “PAR-25-266: Screening and Treatments for Newborn-Detectable Rare Diseases,” nih.gov Europe’s proposed Orphan Genomic Therapies Fund similarly seeks to balance innovation incentives with equitable access across member states. These programs enlarge pre-symptomatic patient pools, permitting earlier intervention and supporting volume growth in the Hunter syndrome treatment market. Medium-term impact is expected because funding cycles launch new studies within two to four years.

Commercial Launch of BBB-Penetrant ERTs

Pabinafusp alfa demonstrated clinically meaningful CNS penetration by pairing iduronate-2-sulfatase with a transferrin-receptor antibody, achieving cognitive and behavioral improvements beyond somatic symptom control. Denali Therapeutics’ tividenofusp alfa cut cerebrospinal fluid heparan sulfate by 90% over 104 weeks and improved adaptive behavior scores, setting efficacy benchmarks that conventional IV ERTs cannot match. Early launch success is likely to accelerate the adoption of similar fusion-protein designs, immediately lifting the Hunter syndrome treatment market.

Accelerating AAV9 & LV-Based Gene-Therapy Pipeline

REGENXBIO’s RGX-121 delivered an 85% median cerebrospinal fluid heparan sulfate reduction sustained for two years and enabled 80% of pivotal-dose patients to discontinue ERT. Lentiviral hematopoietic stem-cell approaches report supraphysiologic enzyme expression and durable somatic correction, with first-in-human read-outs in 2024-2025.[3]HemaSphere, “Lentiviral Gene Therapy Trials in MPS II,” journal.hemasphere.org Improved vector manufacturing capacity is shortening lead times and lowering the cost-of-goods, further bolstering the Hunter syndrome treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Annual Therapy Cost & Reimbursement Friction | -1.50% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Limited CNS Efficacy Of IV ERTs | -0.80% | Global | Long term (≥ 4 years) |

| Ultra-Small Patient Pool Limits ROI For Entrants | -0.70% | Global, particularly in smaller markets | Long term (≥ 4 years) |

| Biologic Manufacturing Bottlenecks For Fusion Proteins | -0.50% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Annual Therapy Cost & Reimbursement Friction

Chronic IV ERT regimens can top USD 400,000 annually, stretching public budgets and private insurers alike. Gene therapies priced as one-time cures intensify budget-impact concerns despite long-run cost offsets. Payers, therefore, impose stringent prior-authorization hurdles and often reimburse only when a a sustained neurological benefit is demonstrated, slowing uptake in the Hunter syndrome treatment market. Outcome-based payment models such as milestone reimbursements contingent on biomarker normalization—are emerging but remain inconsistently applied across jurisdictions.

Limited CNS Efficacy of IV ERTs

The blood–brain barrier blocks adequate enzyme delivery to neuronal tissue, leaving severe phenotypes with progressive cognitive decline even under optimal somatic dosing. Intrathecal infusions partially address the gap but entail invasive procedures requiring operating-room resources. As newborn screening expands, clinicians and families increasingly demand disease-modifying options, relegating conventional IV ERTs to a maintenance role and capping their long-term contribution to the Hunter syndrome treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Gene Therapy Disrupts ERT Dominance

Enzyme replacement therapy generated JPY 91.6 billion (USD 610 million) for Takeda in fiscal 2025, translating to an 81.35% Hunter syndrome treatment market share that year. Yet gene and other advanced modalities are growing at a 7.06% CAGR, setting the stage for material share shifts by 2031. Early RGX-121 recipients recorded stable adaptive behavior and motor development, prompting 80% to discontinue weekly ERT altogether. Hospitals and payers recognize the clinical and logistical advantages of a one-time infusion, supporting rapid adoption even at multimillion-dollar list prices.

Pipeline momentum is not limited to AAV9 vectors. Lentiviral autologous stem-cell therapy yielded supraphysiologic iduronate-2-sulfatase expression without conditioning-related neurotoxicity in early studies. Several firms are now evaluating base-editing and CRISPR platforms that could further reduce vector loads, although those candidates remain pre-IND. Manufacturing capacity is a gating factor: viral-vector clean rooms ran near full utilization in 2024-2025, delaying supply for compassionate-use requests. Even so, the Hunter syndrome treatment market size tied to advanced therapies is expected to climb swiftly once the first gene therapy secures global approvals, reinforcing the segment’s leadership in value creation.

By End User: Home Infusion Gains Momentum

Hospitals accounted for 66.65% of the Hunter syndrome treatment market in 2025 because IV ERT infusions demand sterile environments and anaphylaxis preparedness. Home-infusion and specialty clinics, however, are on track to expand at a 6.21% CAGR to 2031 as payers seek to curb facility overheads. German cohort data showed identical urinary glycosaminoglycan clearance and patient-reported outcome scores when ERT shifted from hospital to nurse-supervised home settings.

Gene therapy rollouts could temporarily restore hospital dominance because one-time infusions require extended monitoring and specialized vector-handling protocols. Yet post-infusion follow-up, including biomarker draws and neurocognitive assessments, aligns well with community specialty clinic infrastructure. Over time, the Hunter syndrome treatment market size tied to home care is likely to expand further as remote patient-monitoring technologies mature and as regulators grow comfortable with decentralized care models for rare disease therapies.

Geography Analysis

North America led the Hunter syndrome treatment market with a 37.25% share in 2025, thanks to robust orphan-drug tax credits, FDA accelerated approval mechanisms, and broad commercial insurance coverage. Gene-therapy activity is mainly concentrated in the United States, where the FDA accepted cerebrospinal fluid heparan sulfate reduction as a surrogate for clinical benefit in pre-BLA meetings for RGX-121. The Inflation Reduction Act introduces uncertainty for long-term pricing, but current legislative drafts exempt sole-indication orphan drugs from Medicare negotiations, preserving headroom for premium pricing.

Europe offers streamlined centralized approval through the EMA, yet national reimbursement heterogeneity fragments access. Western European countries routinely reimburse high-cost orphan medicinal products within 12 months of marketing authorization, whereas Central and Eastern European markets often delay funding for two to three years. The proposed European Orphan Genomic Therapies Fund aims to bridge this gap by pooling risk and negotiating outcome-based contracts at an EU-wide level. Academic-industry consortia remain pivotal, with French, German, and UK centers running more than half of the active European clinical trials for Hunter syndrome gene therapy.

Asia Pacific is the fastest-growing region at an 8.08% CAGR through 2031, reflecting strengthening healthcare infrastructure and the proliferation of rare disease policies. Japan approved its first BBB-penetrant ERT in 2024 and signed accords to fast-track gene-therapy dossiers, driving regional interest from multinational sponsors. China expanded its National Rare Disease List to include mucopolysaccharidosis type II in 2025, unlocking provincial reimbursement pilots and boosting diagnostic rates. India rolled out state-level newborn screening programs that capture more than 40% of births, a significant leap from less than 10% coverage in 2023. Collectively, these reforms enlarge the patient pool and set the stage for sustained double-digit growth in the Hunter syndrome treatment market across Asia Pacific.

Competitive Landscape

The Hunter syndrome treatment market is moderately concentrated. Takeda’s ELAPRASE franchise generated JPY 91.6 billion (USD 610 million) in fiscal 2024, cementing the company’s leadership in conventional ERT. REGENXBIO, Denali Therapeutics, and JCR Pharmaceuticals spearhead the gene-therapy wave, each racing to secure first-in-class approval for CNS-penetrant modalities. Denali’s tividenofusp alfa earned FDA breakthrough therapy designation in January 2025 after delivering sustained cognitive gains in a Phase 1/2 study.

Strategic alliances mitigate commercial and manufacturing risk. REGENXBIO’s USD 110 million upfront partnership with Nippon Shinyaku includes potential milestones up to USD 700 million and grants the Japanese partner regional rights, ensuring culturally attuned market access. JCR Pharmaceuticals collaborates with Medipal Holdings to streamline distribution in East Asia, while Ultragenyx inked a supply agreement with WuXi Advanced Therapies to secure viral-vector capacity. Such moves underscore how manufacturing scale and local regulatory expertise have become competitive differentiators in the Hunter syndrome treatment market.

White-space opportunities persist in Latin America and the Middle East, where newborn screening infrastructure is catching up and reimbursement frameworks for ultra-rare diseases remain underdeveloped. Companies able to craft tiered-pricing and risk-sharing models could capture first-mover advantages. As of 2025, no biosimilar idursulfase candidates have progressed beyond preclinical stages, prolonging Takeda’s shield against price erosion. However, once biosimilar pathways mature, price competition could intensify, compressing margins for legacy ERTs but potentially expanding volume and overall value in the Hunter syndrome treatment market.

Hunter Syndrome Treatment Industry Leaders

REGENXBIO Inc.

Clinigen Group plc

JCR Pharmaceuticals

ArmaGen

Takeda Pharmaceutical Company Limited (Shire)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Avrobio introduced AVR-RD-05, a gene therapy that has gained orphan drug designation from the USFDA to treat mucopolysaccharidosis type II.

- January 2025: REGENXBIO and Nippon Shinyaku formed an exclusive partnership to commercialize RGX-121 (MPS II) and RGX-111 (MPS I) in Japan, featuring USD 110 million upfront and milestones up to USD 700 million.

- January 2025: The FDA granted breakthrough therapy designation to Denali’s tividenofusp alfa after 90% sustained cerebrospinal fluid heparan sulfate reductions over 104 weeks.

- December 2024: The FDA approved ALHEMO (concizumab-mtci) and issued a Rare Pediatric Disease Priority Review Voucher under its orphan program.

Global Hunter Syndrome Treatment Market Report Scope

As per the scope of the report, hunter syndrome, also known as mucopolysaccharidosis II or MPS II, is a type of rare disease caused by a lysosomal enzyme or iduronate-2-sulfatase enzyme deficiency. Enzyme replacement therapy (ERT) and hematopoietic stem cell transplant (HSCT) are the two main types of treatment that focus on providing symptomatic relief and managing complications associated with the disease.

The hunter syndrome treatment market is segmented by treatment type (enzyme replacement therapy (ERT), hematopoietic stem cell transplant (HSCT), and other treatment types), end user (hospitals, diagnostic centers, and other end users), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers the value (in USD million) for the above segments.

| Enzyme Replacement Therapy (ERT) |

| Hematopoietic Stem-Cell Transplant (HSCT) |

| Gene & Other Advanced Therapies |

| Hospitals |

| Diagnostic & Reference Laboratories |

| Home-Infusion & Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Enzyme Replacement Therapy (ERT) | |

| Hematopoietic Stem-Cell Transplant (HSCT) | ||

| Gene & Other Advanced Therapies | ||

| By End User | Hospitals | |

| Diagnostic & Reference Laboratories | ||

| Home-Infusion & Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Hunter syndrome treatment market?

The market is valued at USD 1.45 billion in 2026 and is projected to reach USD 1.88 billion by 2031.

Which treatment modality dominates revenue today?

Enzyme replacement therapy holds 81.35% of 2025 revenue, led by Takeda’s ELAPRASE franchise.

Which segment is growing the fastest?

Gene and other advanced therapies are expanding at a 7.06% CAGR thanks to BBB-penetrant ERTs and AAV-based gene therapies.

Which region shows the fastest growth?

Asia Pacific is forecast to grow at 8.08% CAGR between 2026 and 2031 as diagnostics and reimbursement frameworks mature.

How are home-infusion services impacting therapy delivery?

Home-infusion and specialty clinics are projected to grow at a 6.21% CAGR as they reduce facility costs while maintaining clinical outcomes.

Page last updated on: